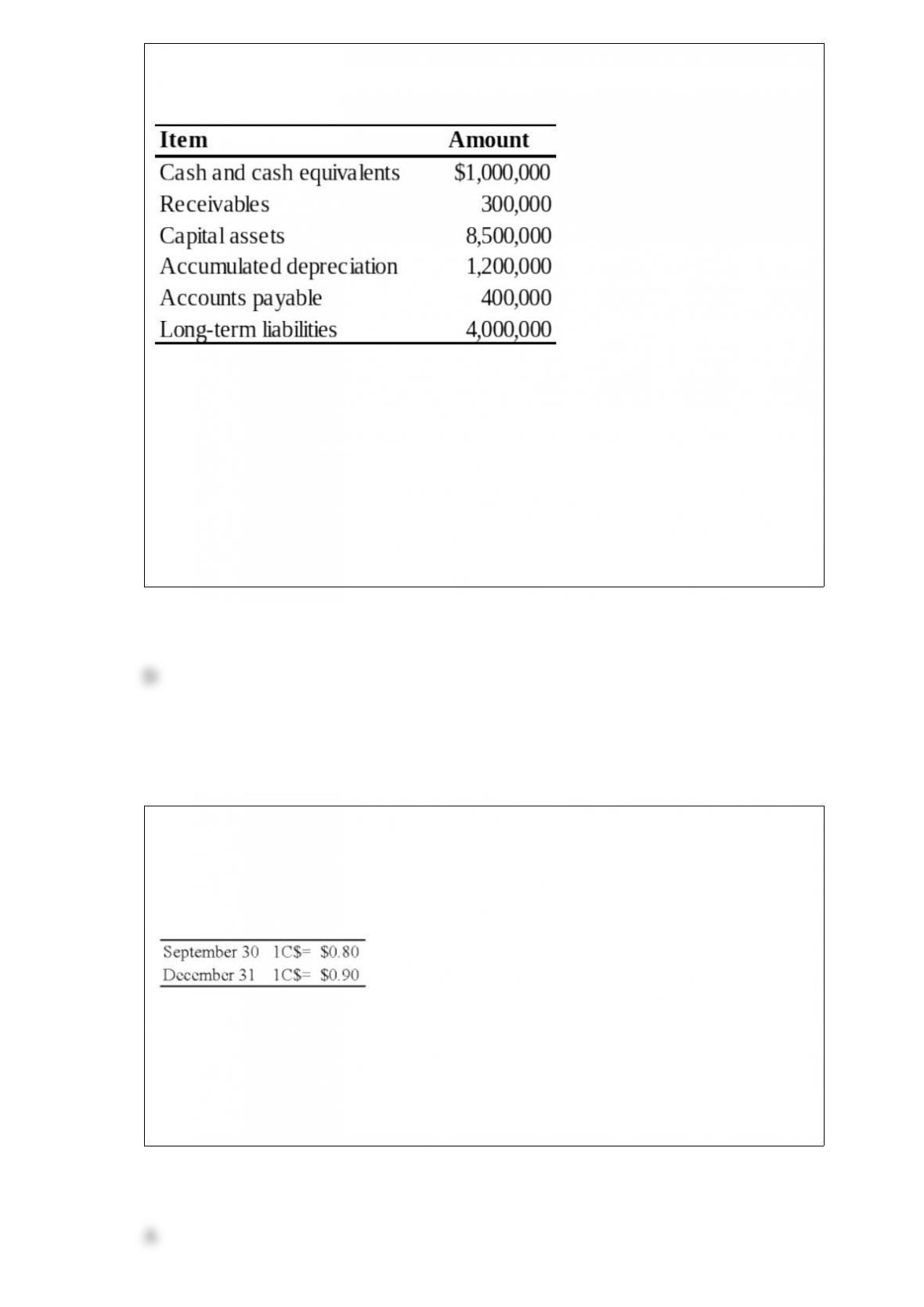

Riviera Township reported the following data for its governmental activities for the year

ended June 30, 20X9:

Additional information available is as follows:

All of the long-term debt was used to acquire capital assets. Cash of $475,000 is

restricted for debt service.

Based on the preceding information, on the statement of net assets prepared at June 30,

20X9, what amount should be reported for net assets invested in capital assets, net of

related debt?

A. $4,200,000

B. $2,900,000

C. $2,825,000

D. $3,300,000

On September 30, 20X8, Wilfred Company sold inventory to Jackson Corporation, its

Canadian subsidiary. The goods cost Wilfred $30,000 and were sold to Jackson for

$40,000, payable in Canadian dollars. The goods are still on hand at the end of the year

on December 31. The Canadian dollar (C$) is the functional currency of the Canadian

subsidiary. The exchange rates follow:

Based on the preceding information, at what dollar amount is the ending inventory

shown in the trial balance of the consolidated worksheet?

A. $45,000

B. $50,000

C. $40,000

D. $35,000

Michigan-based Leo Corporation acquired 100 percent of the common stock of a

British company on January 1, 20X8, for $1,100,000. The British subsidiary’s net assets

amounted to 500,000 pounds on the date of acquisition. On January 1, 20X8, the book

values of its identifiable assets and liabilities approximated their fair values. As a result

of an analysis of functional currency indicators, Leo determined that the British pound

was the functional currency. On December 31, 20X8, the British subsidiary’s adjusted

trial balance, translated into U.S. dollars, contained $17,000 more debits than credits.

The British subsidiary reported income of 33,000 pounds for 20X8 and paid a cash

dividend of 8,000 pounds on October 25, 20X8. Included on the British subsidiary’s

income statement was depreciation expense of 3,500 pounds. Leo uses the fully

adjusted equity method of accounting for its investment in the British subsidiary and

determined that goodwill in the first year had an impairment loss of 25 percent of its

initial amount. Exchange rates at various dates during 20X8 follow:

January 1 1 = $2.10

October 25 1 = 2.25

December 31 1 = 2.20

Average for 20X8 1 = 2.21

Based on the preceding information, the receipt of the dividend will result in a credit to

the investment account for:

A. $16,800

B. $17,680

C. $18,000

D. $17,600

Windsor Corporation owns 75 percent of Elven Corporation’s outstanding common

stock. Elven, in turn, owns 15 percent of Windsor’s outstanding common stock. What

percent of the dividends paid by Windsor is reported as dividends declared in the

consolidated retained earnings statement?

A. None

B. 100 percent

C. 85 percent

D. 75 percent

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount will be reported as total stockholders’

equity in the consolidated balance sheet prepared immediately after the business

combination?

A. $360,000

B. $590,000

C. $770,000

D. $860,000

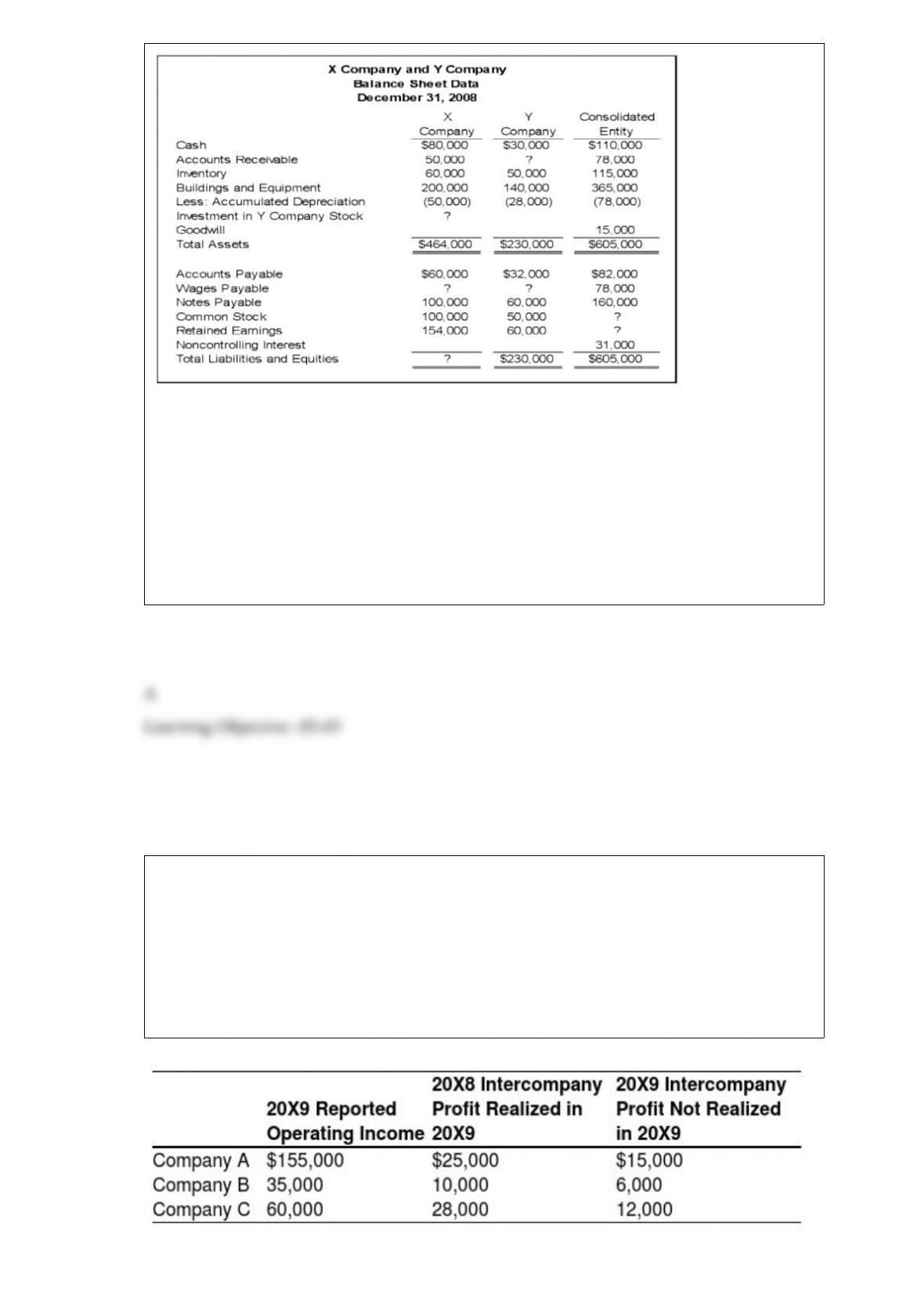

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A

consolidated balance sheet was prepared immediately. Partial balance sheet data for the

two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet

paid for them. There were no other receivables or payables between the companies at

December 31, 20X8.

Based on the information given, what was the fair value of Y Company as a whole at

the date of acquisition?

A. $155,000

B. $110,000

C. $115,000

D. $135,000

Company A owns 85 percent of Company B’s stock and 80 percent of Company C’s

stock. All acquisitions were made at book value. The fair values of noncontrolling

interests at the time of acquisition were equal to the proportionate share of the book

values of the companies. The companies file a consolidated tax return each year and in

20X9 paid a total tax of $112,000. Each company is involved in a number of

intercompany inventory transfers each period. Information on the companies’ activities

for 20X9 is as follows:

Company A does not record income tax expense on income from subsidiaries because a

consolidated tax return is filed.

Based on the information provided, what amount of consolidated net income will be

reported for the year 20X9?

A. $168,000

B. $280,000

C. $165,000

D. $250,000

On January 1, 20X1, Washington City received 200,000 from an estate with the

stipulation that the money be invested and the income be used to provide maintenance

to the city cemetery. The money was invested in 7% governmental securities at 90 to

yield an effective interest rate of 10%. The following journal entry would be made to

account for the accrued interest of the permanent fund:

Which of the following is defined as directly or indirectly having the power to vote the

shares or investment power to sell the security?

A. Proxy

B. Significant influence

C. Control

D. Beneficial ownership

Which of the following funds are classified as proprietary funds?

A. Agency and special revenue funds.

B. Enterprise and internal service funds.

C. Debt service and capital projects funds.

D. Agency and pension trust funds.

A voluntary health and welfare organization developed and printed informational

materials which were intended to both educate the public about how its resources are

used to help people in need and to also appeal to the public for much needed support. In

this situation, the cost of the informational materials should be

A. accounted for as fund-raising expense.

B. allocated to expenses for program services.

C. allocated between expenses for program services and fund-raising expense.

D. accounted for as management and general expense.

Wally Corporation acquired 70 percent of the common shares and 60 percent of the

preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At

that date, the fair value of the noncontrolling interest in Safety’s common stock was

equal to 30 percent of the book value of its common stock. Safety’s balance sheet at the

time of acquisition contained the following balances:

Assets $700,000 Liabilities $110,000

Preferred Stock 100,000

Common Stock 200,000

Retained Earnings 290,000

Total Assets $700,000 Total Liabilities and Equities $700,000

The preferred shares are cumulative and have an 8 percent annual dividend rate and are

three years in arrears on January 1, 20X6. All of the $10 par value preferred shares are

callable at $12 per share. During 20X6, Safety reported net income of $80,000 and paid

no dividends.

Based on the information provided, what is the book value of the common stock on

January 1, 20X6?

A. $390,000

B. $420,000

C. $446,000

D. $490,000

When the old partners receive a bonus upon admission of a new partner into a

partnership, the bonus is allocated to:

I. all the partners in their profit and loss sharing ratio.

II. the existing partners in their profit and loss sharing ratio.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

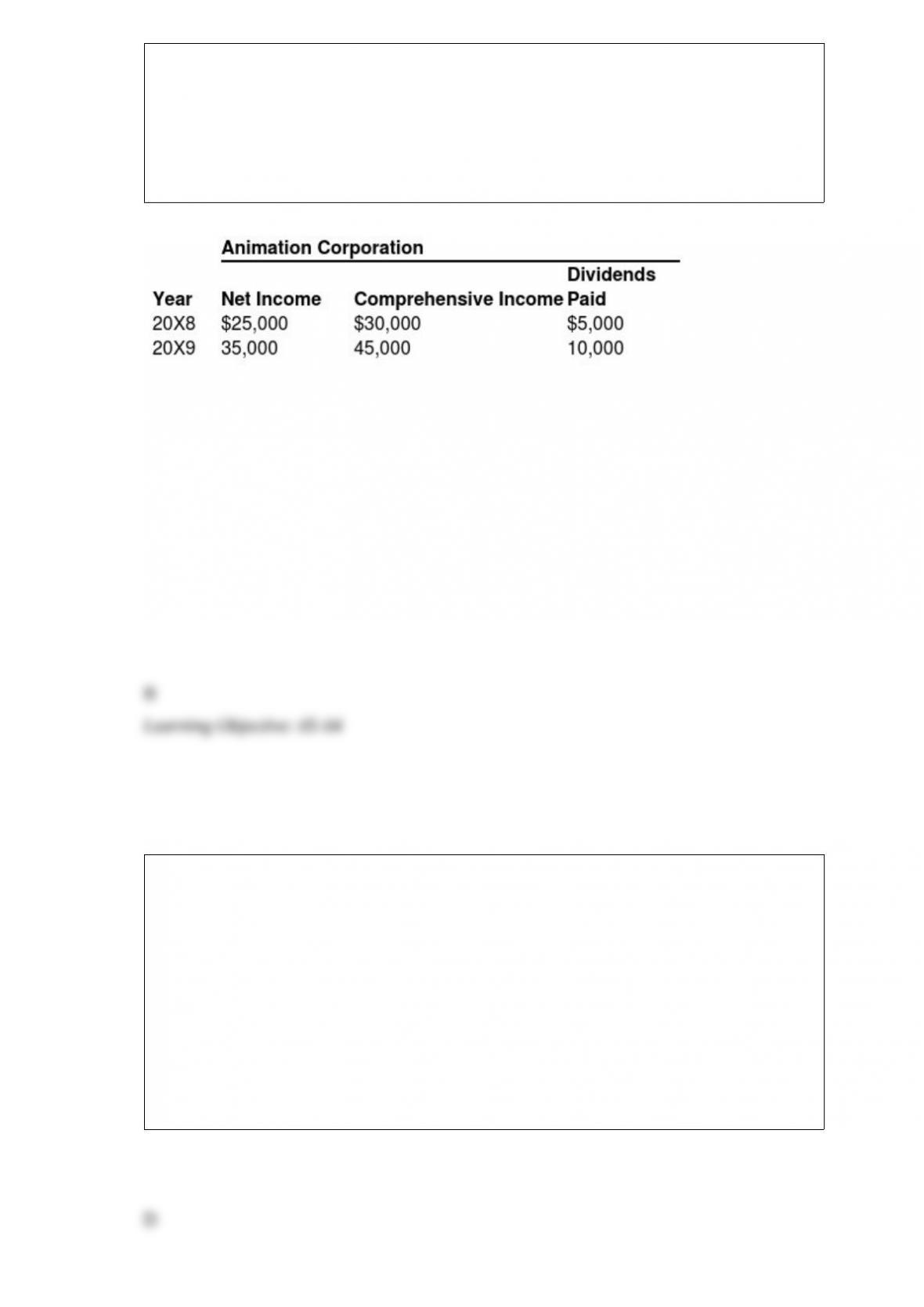

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company’s

common stock for $280,000 cash. At that date, Animation reported common stock

outstanding of $200,000 and retained earnings of $100,000, and the fair value of the

noncontrolling interest was $70,000. The book values and fair values of Animation’s

assets and liabilities were equal, except for other intangible assets which had a fair

value $50,000 greater than book value and an 8-year remaining life. Animation reported

the following data for 20X8 and 20X9:

Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

Based on the preceding information, what is the amount of consolidated comprehensive

income reported for 20X8?

A. $125,000

B. $123,750

C. $118,750

D. $130,000

In the computation of a partner’s Loss Absorption Power (LAP), which of the following

statements is incorrect?

I. The computation of LAPs for all partners allows cash to be distributed before all

partnership assets have been sold and all creditors have been paid.

II. The computation of LAPs for all partners indicates the relative strength of each

partner’s net capital position so that available cash is distributed in respective

loss-sharing ratios.

A. I

B. II

C. Both I and II

D. Neither I nor II

Mom Corporation acquired 75 percent of Daughter Company’s voting shares on

January 1, 20X7, at underlying book value. On December 31, 20X7, it also purchased

$300,000 par value 9 percent Daughter bonds, which had been issued on January 1,

20X3 to Parry Corporation (unaffiliated with either Mom or Daughter) at a $20,000

premium. The bonds were originally issued with a 10-year maturity and pay interest

annually on December 31. During preparation of the consolidated financial statements

for December 31, 20X7, the following consolidation entry was included in the

consolidation worksheet:

Bonds Payable 300,000

Bond Premium 11,902

Loss on Bond Retirement 12,098

Investment in Daughter Company Bonds 324,000

Based on the information given above, what was the carrying amount of the bonds on

Daughter’s books on the date of purchase by Mom?

A. $300,000

B. $311,902

C. $312,098

D. $324,000

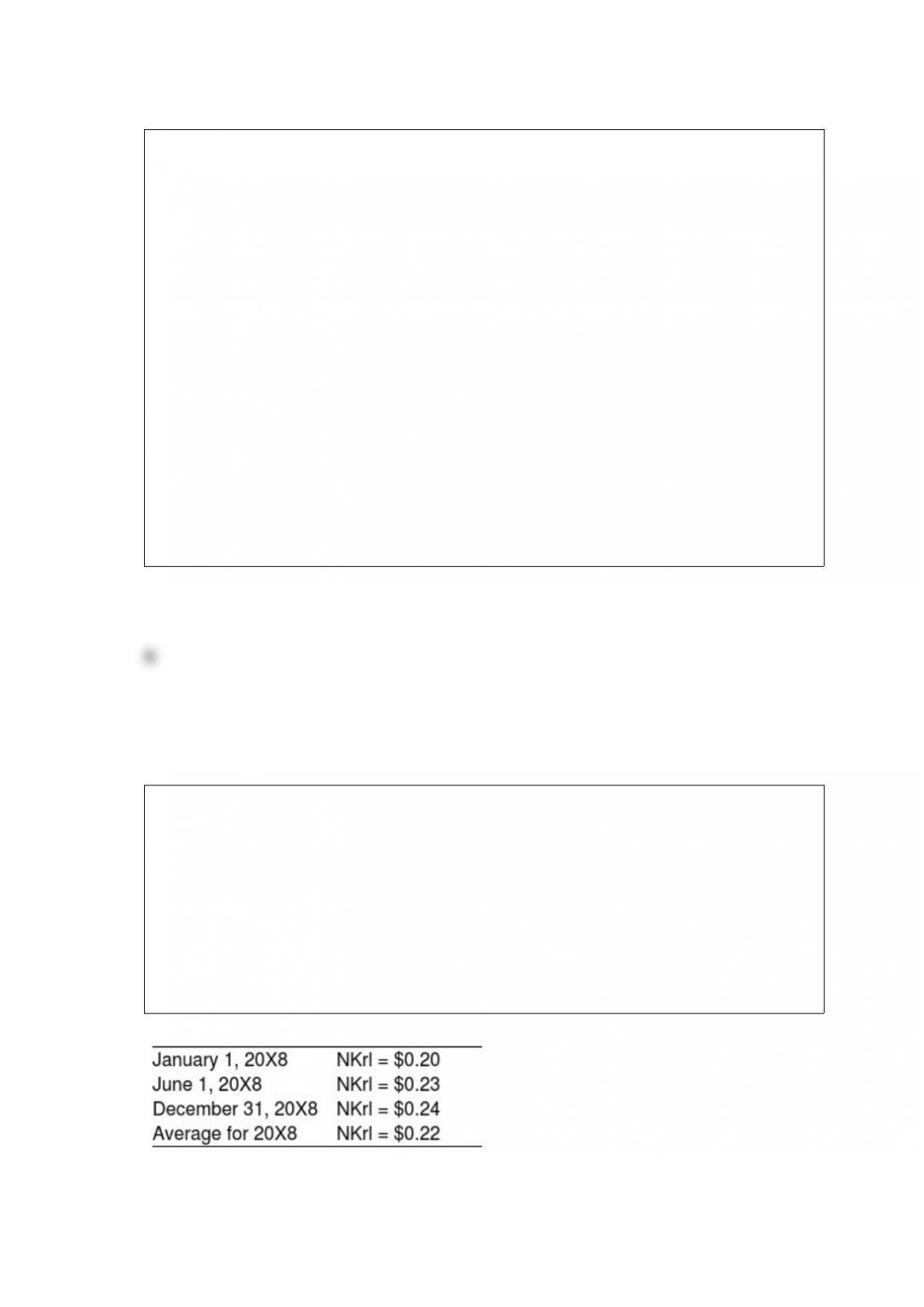

On January 1, 20X8, Transport Corporation acquired 75 percent interest in Steamship

Company for $300,000. Steamship is a Norwegian company. The local currency is the

Norwegian kroner (NKr). The acquisition resulted in an excess of cost-over-book value

of $25,000 due solely to a patent having a remaining life of 5 years. Transport uses the

fully adjusted equity method to account for its investment. Steamship’s December 31,

20X8, trial balance has been translated into U.S. dollars, requiring a translation

adjustment debit of $8,000. Steamship’s net income translated into U.S. dollars is

$35,000. It declared and paid an NKr 20,000 dividend on June 1, 20X8. Relevant

exchange rates are as follows:

Assume the kroner is the functional currency.

Based on the preceding information, what amount of translation adjustment is required for

increase in differential?

A. $3,000

B. $5,500

C. $4,500

D. $5,000

A parent and its 80 percent owned subsidiary have made several intercompany sales of

noncurrent assets during the past two years. The amount of income assigned to the

noncontrolling interest for the second year should include the noncontrolling interest’s

share of gains:

A. unrealized in the second year from upstream sales made in the second year.

B. realized in the second year from downstream sales made in both years.

C. realized in the second year from upstream sales made in both years.

D. both realized and unrealized from upstream sales made in the second year.

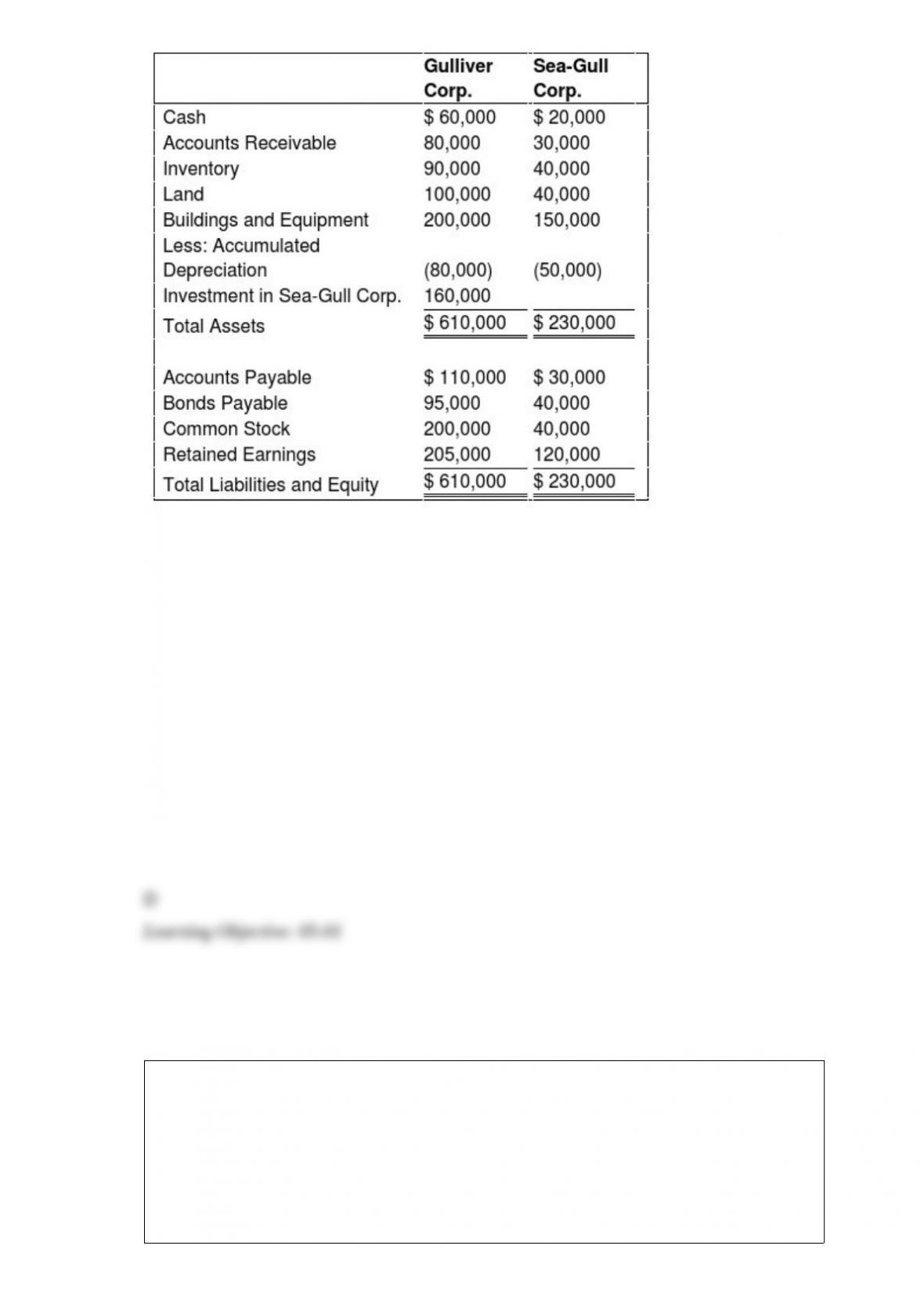

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $0

B. $40,000

C. $20,000

D. $15,000

On January 1, 20X8, Parent Company acquired 90 percent ownership of Subsidiary

Corporation, at underlying book value. The fair value of the noncontrolling interest at

the date of acquisition was equal to 10 percent of the book value of Subsidiary

Corporation. On Mar 17, 20X8, Subsidiary purchased inventory from Parent for

$90,000. Subsidiary sold the entire inventory to an unaffiliated company for $120,000

on November 21, 20X8. Parent had produced the inventory sold to Subsidiary for

$62,000. The companies had no other transactions during 20X8.

Based on the information given above, what amount of sales will be reported in the

20X8 consolidated income statement?

A. $62,000

B. $120,000

C. $90,000

D. $58,000

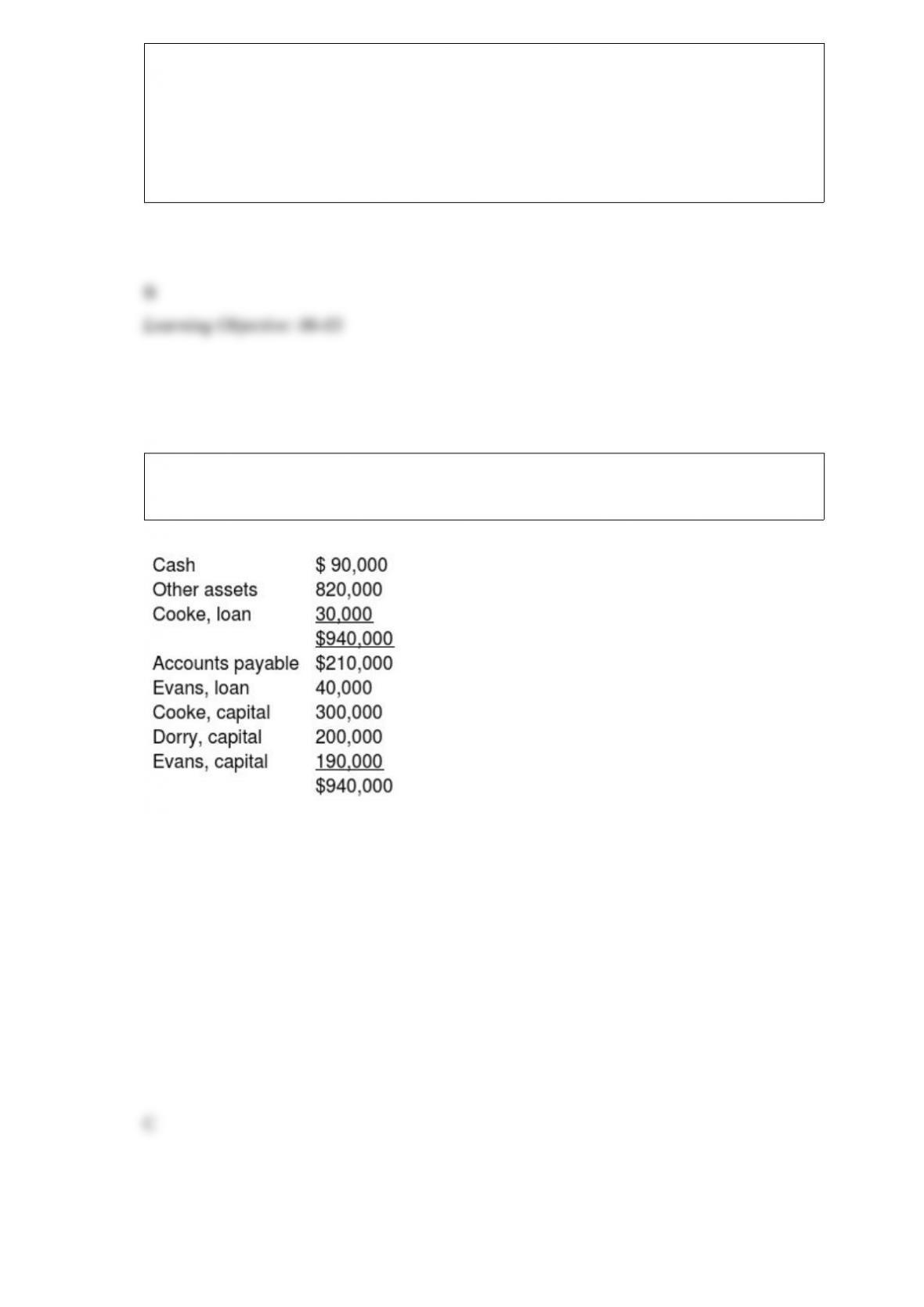

The following condensed balance sheet is presented for the partnership of Cooke,

Dorry, and Evans who share profits and losses in the ratio of 4:3:3, respectively:

Assume that the partners decide to liquidate the partnership. If the other assets are sold for

$600,000, how much of the available cash should be distributed to Cooke?

A. $212,000

B. $170,000

C. $182,000

D. $300,000

A private, not-for-profit hospital received a contribution of $40,000 on June 15, 20X8.

The donor restricted the contribution to funding research activities currently being

performed by the hospital. For the year ended December 31, 20X8, the hospital spent

$30,000 of the contribution on research activities. The hospital expended the remaining

$10,000 on research activities in January of 20X9.

Refer to the above information. On the statement of cash flows prepared for the year

ended December 31, 20X8, the events described would increase net cash flows

provided by

A. operating activities by $40,000.

B. financing activities by $40,000.

C. financing activities by $10,000.

D. operating activities by $10,000.

Hilldale Corporation purchased land on January 1, 20X0, for $60,000. On August 7,

20X2, it sold the land to its subsidiary, Allen Corporation, for $35,000. Hilldale owns

60 percent of Allen’s voting shares

Which worksheet consolidation entry will be made on December 31, 20X3, if Allen

Corporation had initially purchased the land for $60,000 and then sold it to Hilldale on

August 7, 20X2, for $35,000?

A. Investment in Allen 15,000

NCI in NA of Allen 10,000

Land 25,000

B. Investment in Allen 20,000

NCI in NA of Allen 5,000

Land 25,000

C. Land 25,000

Investment in Allen 15,000

NCI in NA of Allen 10,000

D. Land 25,000

Investment in Allen 20,000

NCI in NA of Allen 5,000

The Board of Commissioners of the City of Rockton adopted its budget for the year

ending July 31, 20X2, which indicated revenues of $1,000,000 and appropriations of

$900,000. If the budget is formally integrated into the accounting records, what is the

required journal entry?

Dr. Cr.

A. Memorandum entry only

B. APPROPRIATIONS $900,000

GENERAL FUND $100,000

ESTIMATED REVENUES $1,000,000

C. ESTIMATED REVENUES $1,000,000

APPROPRIATIONS $900,000

BUDGETARY FUND BALANCE $100,000

D. REVENUES RECEIVABLE $1,000,000

EXPENDITURES PAYABLE $900,000

GENERAL FUND BALANCE $100,000

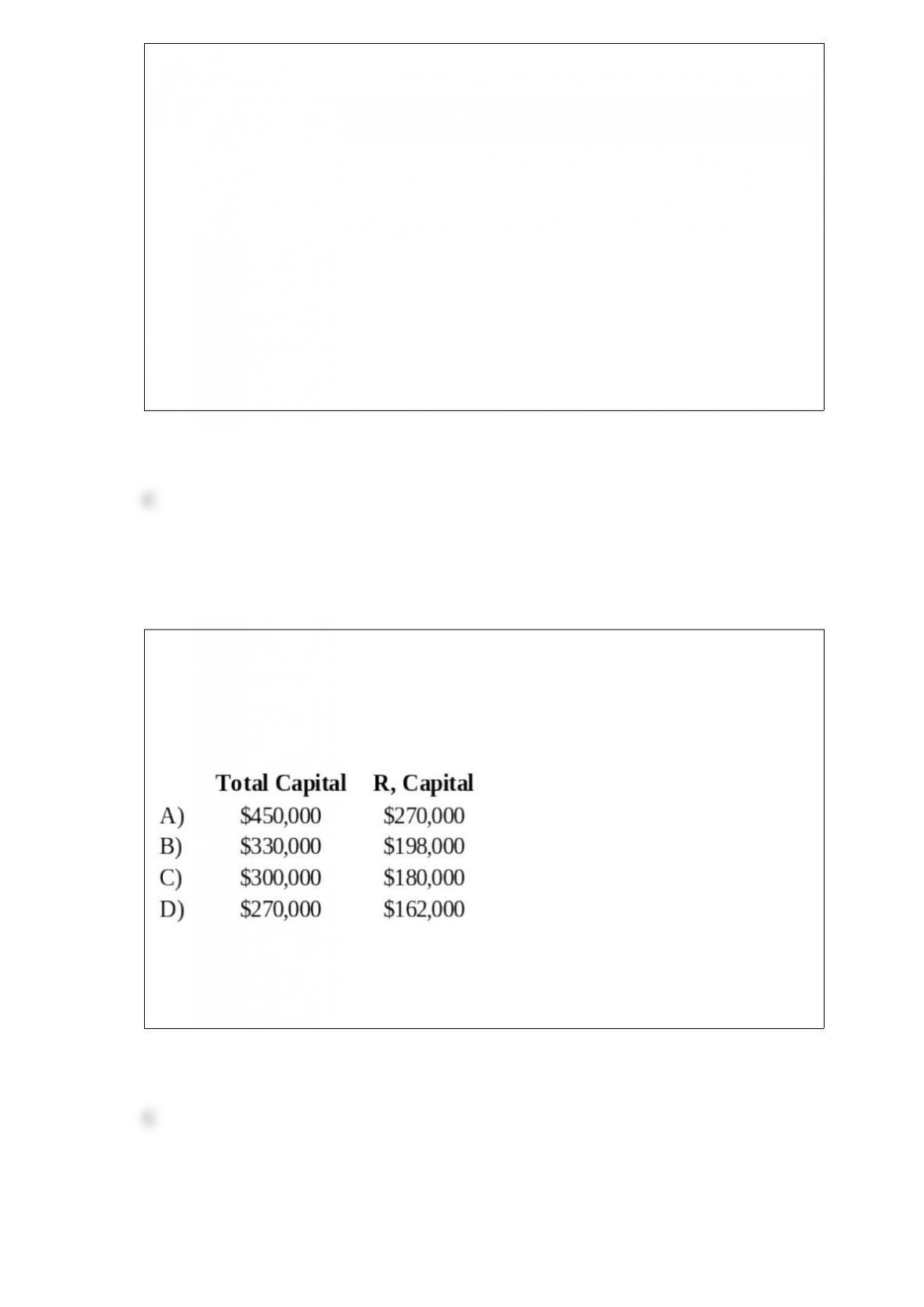

RD formed a partnership on February 10, 20X9. R contributed cash of $150,000, while

D contributed inventory with a fair value of $120,000. Due to R’s expertise in selling, D

agreed that R should have 60 percent of the total capital of the partnership. R and D

agreed to recognize goodwill. What is the total capital of the RD partnership and the

capital balance of R after the goodwill is recognized?

A. Option A

B. Option B

C. Option C

D. Option D

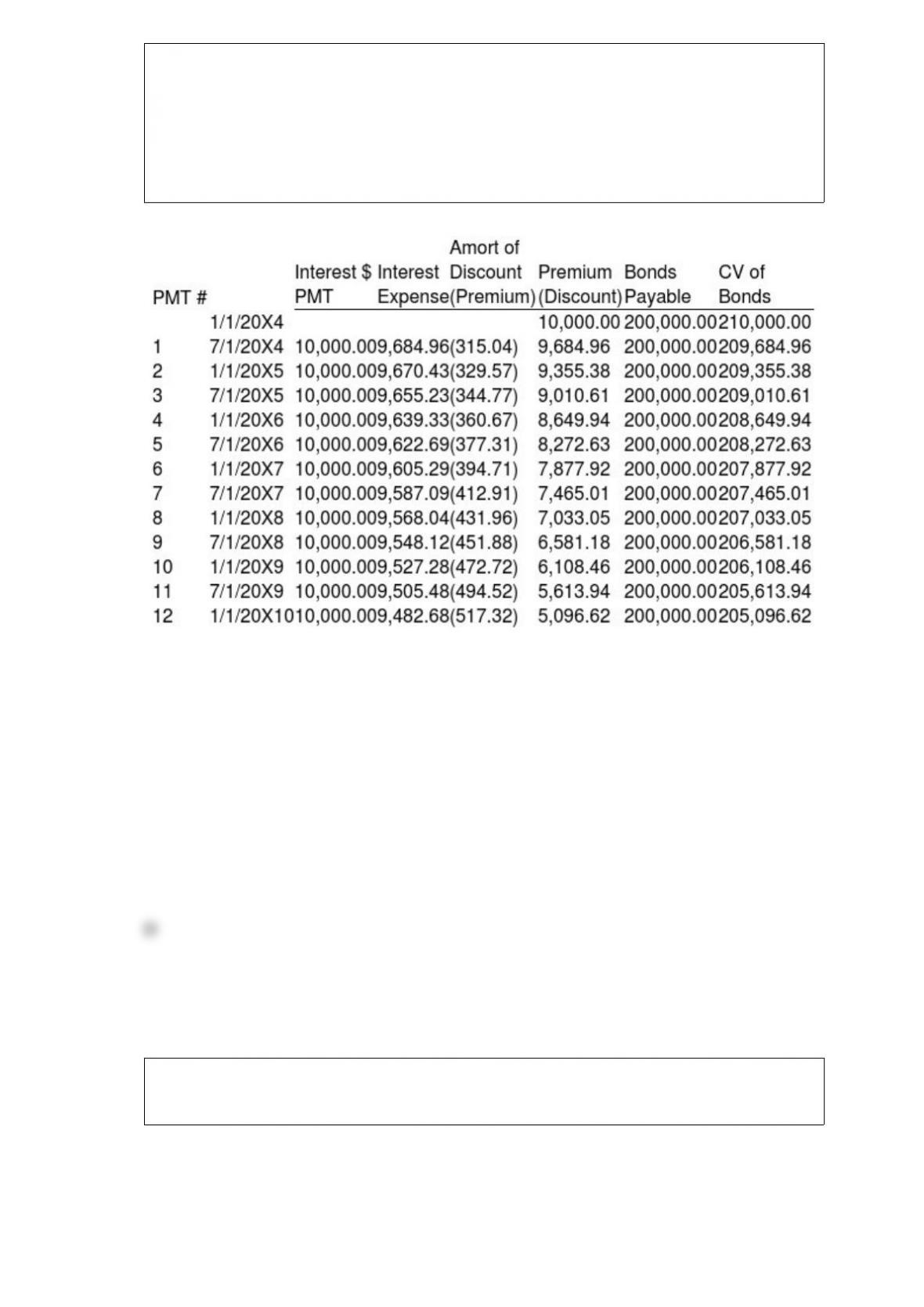

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on December 31, 20X8, for $125,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of constructive gain or loss will be

allocated to noncontrolling interest in 20X8 consolidated financial statements?

A. $20,277 loss

B. $2,223 loss

C. $20,277 gain

D. $4,819 gain

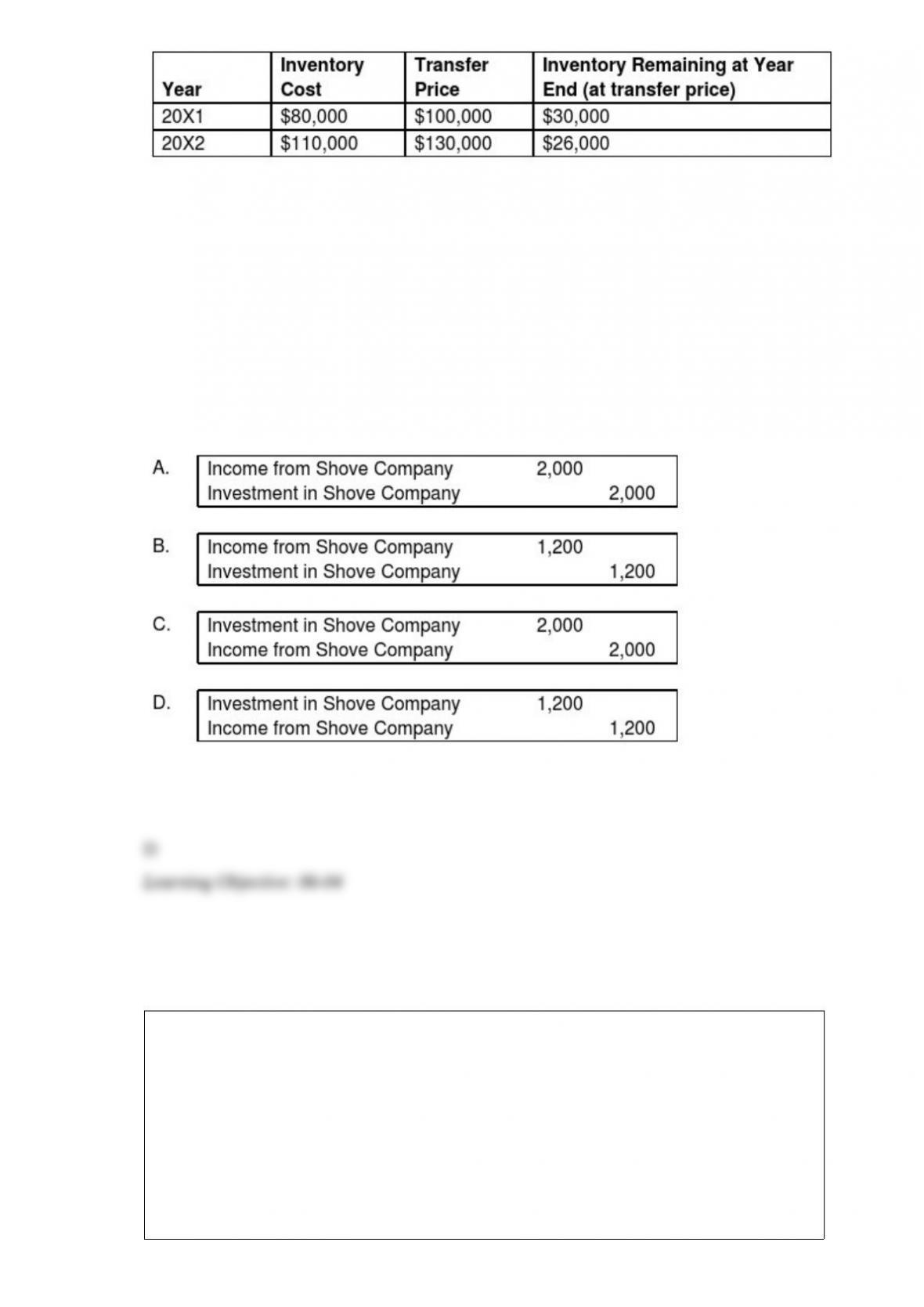

Push Company owns 60% of Shove Company’s outstanding common stock. Intra-entity

sales are as follows:

Assume Shove sold the inventory to Push. Using the fully adjusted equity method, what

journal entry would be recorded by Push to recognize the realization of the 20X1 deferred

intercompany profit and to defer the 20X2 unrealized gross profit on inventory sales to

Shove?

At its inception, Peacock Company purchased land for $50,000 and a building for

$220,000. After exactly 4 years, it transferred these assets and cash of $75,000 to a

newly created subsidiary, Selvick Company, in exchange for 25,000 shares of Selvick’s

$5 par value stock. Peacock uses straight-line depreciation. When purchased, the

building had a useful life of 20 years with no expected salvage value. An appraisal at

the time of the transfer revealed that the building has a fair value of $250,000.

Based on the preceding information, Selvick Company will report additional paid-in

capital of

A. $125,000.

B. $176,000.

C. $220,000.

D. $250,000.

All of the following situations require a retrospective application of a change in a

reporting entity except for:

A. Presenting consolidated financials rather than individual statements for separate

entities

B. Changing the specific subsidiaries that make up a consolidated entity.

C. Presenting foreign subsidiaries in addition to domestic subsidiaries.

D. Changing entities that are included in combined financial statements.

The billings for transportation services provided to other governmental units are

recorded by the internal service fund as

A. Intergovernmental transfers.

B. Interfund exchanges.

C. Charges for services.

D. Transportation appropriations.

On December 31, 20X8, Mercury Corporation acquired 100 percent ownership of

Saturn Corporation. On that date, Saturn reported assets and liabilities with book values

of $300,000 and $100,000, respectively, common stock outstanding of $50,000, and

retained earnings of $150,000. The book values and fair values of Saturn’s assets and

liabilities were identical except for land which had increased in value by $10,000 and

inventories which had decreased by $5,000.

Based on the preceding information, what amount of differential will appear in the

consolidating entries required to prepare a consolidated balance sheet immediately after

the business combination, if the acquisition price was $240,000?

A. $0

B. $40,000

C. $25,000

D. $5,000

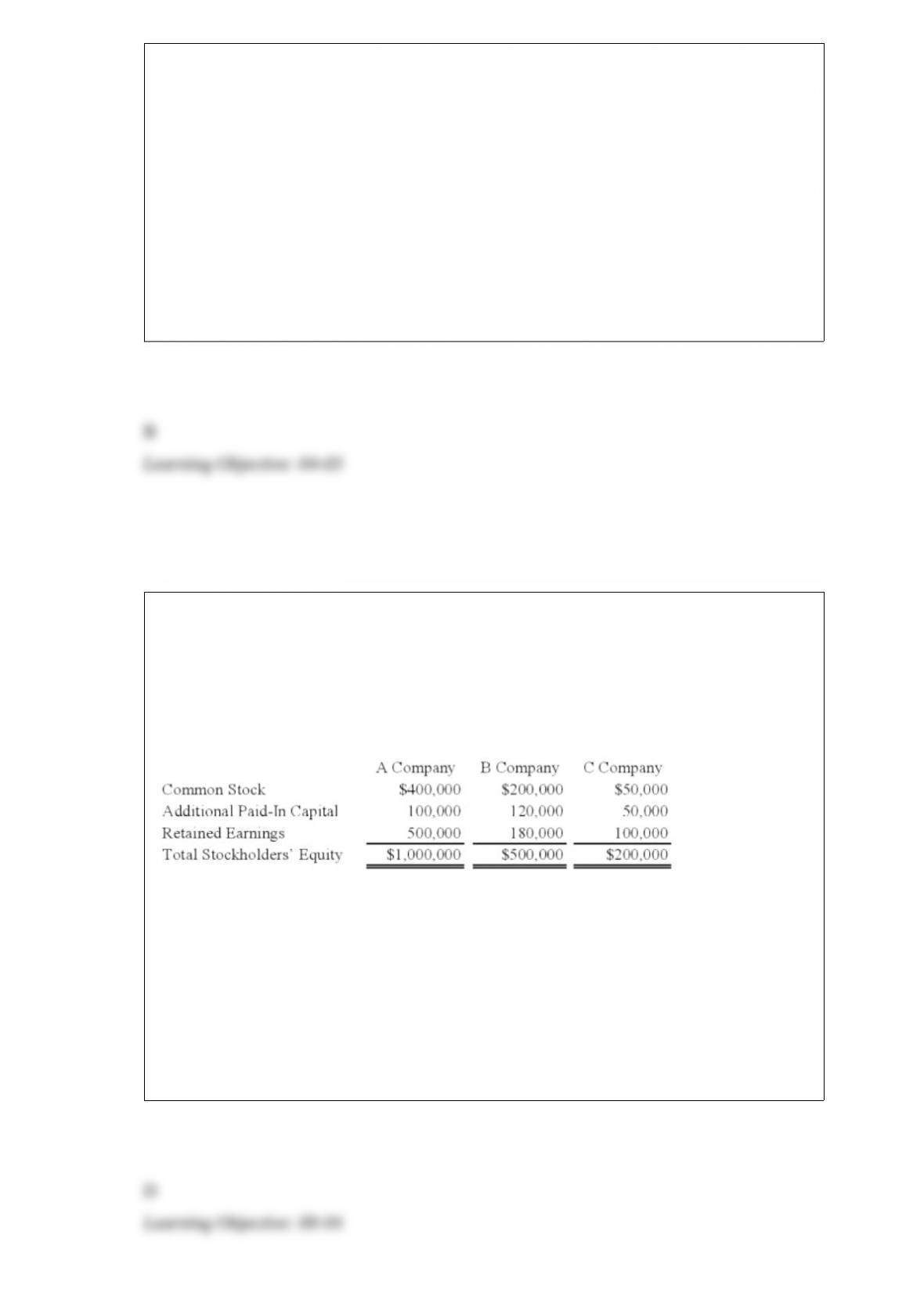

On January 1, 20X9, A Company acquired 85 percent of B Company’s voting common

stock for $425,000. At that date, the fair value of the noncontrolling interest of B

Company was $75,000. Immediately after A Company acquired its ownership, B

Company acquired 75 percent of C Company’s stock for $150,000. The fair value of the

noncontrolling interest of C Company was $50,000 at that date. At January 1, 20X9, the

stockholders’ equity sections of the balance sheets of the companies were as follows:

During 20X9, A Company reported operating income of $175,000 and paid dividends

of $50,000. B Company reported operating income of $125,000 and paid dividends of

$40,000. C Company reported net income of $100,000 and paid dividends of $25,000.

Based on the information provided, what amount of consolidated net income will A

Company report for 20X9?

A. $175,000

B. $285,000

C. $356,250

D. $400,000

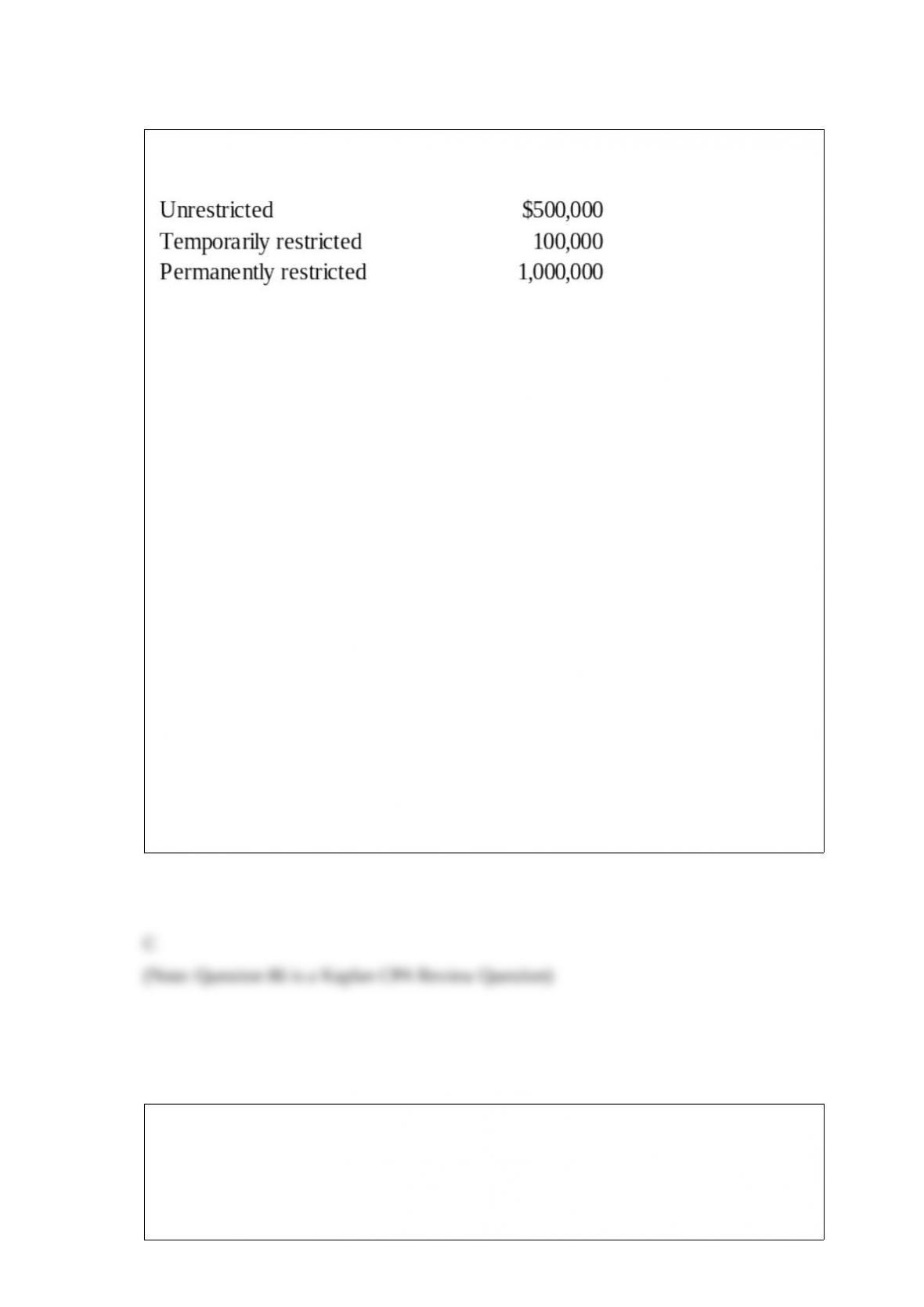

Local Services, a voluntary health and welfare organization had the following classes of

net assets on July 1, 20X8, the beginning of its fiscal year:

During the year ended June 30, 20X9, the following events occurred:

(1) It purchased equipment, costing $100,000, with contributions restricted for this

purpose. The contributions had been received from donors during June of 20X8.

(2) It received $130,000 of cash donations which were restricted for research activities.

During the year ended June 30, 20X9, $90,000 of the contributions were expended on

research.

(3) It sold investments classified in the permanently restricted class for a loss of

$40,000. Dividends and interest income earned on the investments amounted to

$70,000. There were no restrictions on how investment income was to be used.

(4) It received cash contributions of $200,000 from donors who did not place either

time or use restrictions upon their donations.

(5) Expenses, excluding depreciation expense, for program services and supporting

services incurred during the year ended June 30, 20X9, amounted to $260,000.

(6) Depreciation expense for the year ended June 30, 20X9, was $80,000.

Refer to the above information. Which of the following statements is (are) correct about

the program and supporting expenses that would be reported on the statement of

activities for the year ended June 30, 20X9?

I. Program and supporting expenses should be reported at $340,000.

II. All of the program and supporting expenses should be reported as a deduction from

unrestricted revenues and other support.

A. I only

B. II only

C. I and II

D. Neither I nor II

During the third quarter of 20X8, Pride Company sold a piece of equipment at an

$8,000

gain. What portion of the gain should Pride report in its income statement for the third

quarter of 20X8?

A. $0

B. $2,000

C. $4,000

D. $8,000

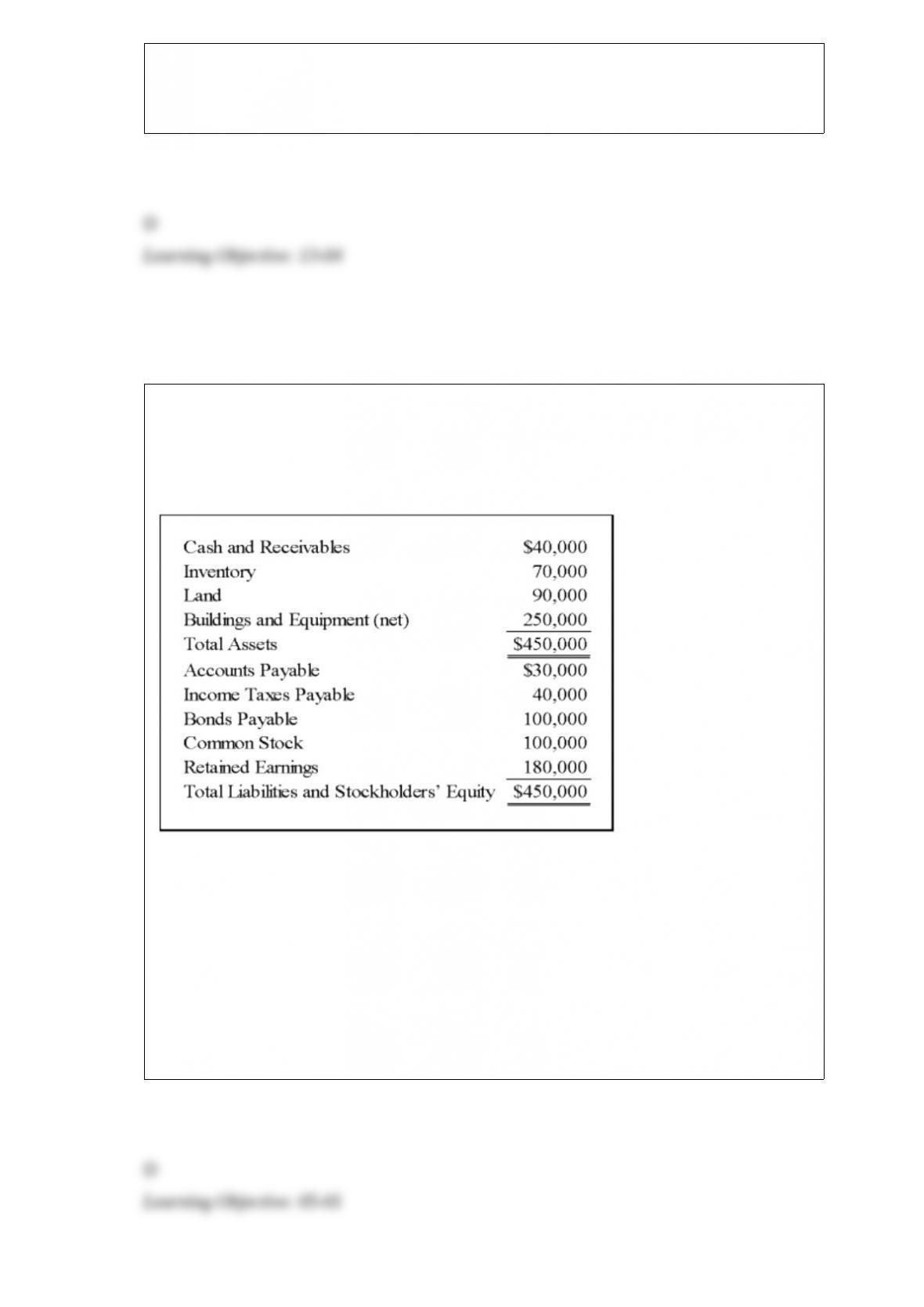

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount will be reported as noncontrolling

interest in the consolidated balance sheet immediately following the acquisition?

A. $0

B. $70,000

C. $83,750

D. $100,000