Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

CHAPTER 1

INTERCORPORATE ACQUISITIONS AND INVESTMENTS

IN OTHER ENTITIES

IMPORTANT NOTE TO INSTRUCTORS

The 11th edition of Advanced Financial Accounting continues the approach to

consolidation which was used in the 10th edition. While we encourage instructors to read through

the description of all changes in the 11th edition provided in the preface to the book, we

summarize this consolidation approach here since it is the fundamental organizational structure

for several chapters in the text. As this approach is developed in chapters 2-5 we believe it offers

students an intuitive foundation for developing consolidated financial statements. We summarize

the two main features in our approach to consolidation in the 11th edition here:

✓ A Building-Block Approach to Consolidation—Virtually all advanced financial

accounting classes cover consolidation topics. While this topic is perhaps the most

important to instructors, students frequently struggle to gain a firm grasp of consolidation

principles. This edition provides students with a learning friendly framework to

consolidations by introducing consolidation concepts and procedures gradually. This is

accomplished by a building-block approach which introduces consolidations earlier than

some texts by beginning the consolidation discussion in chapters 2 and 3. The building-

block approach can be summarized as follows:

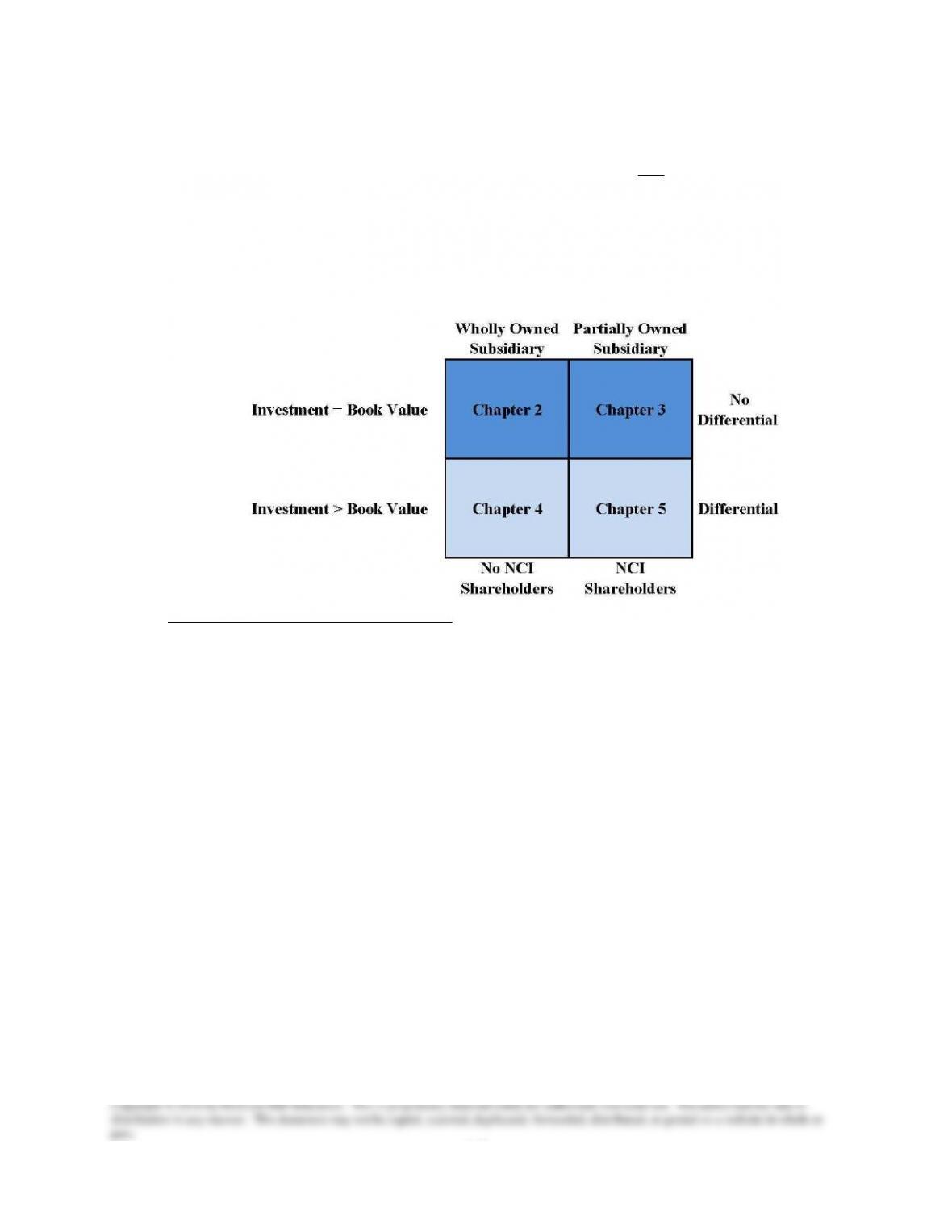

• Chapter 2 begins with the most basic consolidation situation: the consolidation of

a wholly owned subsidiary that is either created or purchased at an amount equal

to the book value of net assets. Thus, students practice basic consolidation

procedures without having to worry about the complications associated with a

differential or with noncontrolling shareholders.

• Chapter 3 introduces the notion of partial ownership of a subsidiary that is

created or acquired at an amount equal to the book value of net assets. In this way

students are exposed to the nuances associated with the existence of

noncontrolling shareholders, but without the details associated with a differential.

• Chapter 4 exposes students to the intricacies of consolidation when the subsidiary

is acquired for an amount that exceeds the book value of net assets. In order to

isolate the new concepts and procedures that accompany the consolidation of a

subsidiary with a differential, this chapter focuses on wholly owned subsidiaries.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

• Chapter 5 finally brings students full circle to the point where they are ready to

tackle more realistic situations where the parent company purchases a controlling

interest in a subsidiary (but less than 100% ownership) and the acquisition price

exceeds the book value of net assets. Thus, students learn how to simultaneously

handle all of the details associated with a differential and with noncontrolling

shareholders.

The overall coverage of the consolidation process by chapter is illustrated below.

✓ Organization of Consolidation Entries—Consistent with the building block approach to

consolidation, the this edition facilitates the elimination of the investment in a subsidiary

in two steps: (1) first the book value portion of the investment and income from the

subsidiary are eliminated and (2) then the differential portion of the investment and

income from subsidiary are eliminated with separate entries. This approach facilitates the

building-block approach in chapters 2-5. This edition also uses frequent illustrations to

help students visualize the steps in the consolidation process.

OVERVIEW OF CHAPTER 1

Chapter 1 provides students with an understanding of the legal forms of business

combinations and the financial statement effects of the accounting procedures used in recording

a business combination. It also discusses the proliferation of complex organizational structures

and regulatory as well as ethical considerations. This chapter fully illustrates accounting for

business combinations on the date of acquisition, using the acquisition method, both for business

combinations effected through an acquisition of net assets and by an acquisition of common

shares.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

The discussions contain specific illustrations of the valuation of tangible and intangible

assets and liabilities held by the acquired company on the date of acquisition. Chapter 1 also

illustrates the measurement and reporting of goodwill and the treatment of a bargain purchase

and discusses the impairment of goodwill. It also explains the treatment of costs associated with

completing a merger and the associated disclosure requirements.

The Additional Considerations portion of the chapter discusses factors adding to

uncertainty in business combinations; in-process research and development; and noncontrolling

equity held prior to combination.

LEARNING OBJECTIVES

When students finish studying this chapter, they should be able to:

LO 1-1 Understand and explain the reasons for and different methods of business

expansion, the types of organizational structures, and the types of acquisitions.

LO 1-2 Understand the development of standards related to acquisition accounting over

time.

LO 1-3 Make calculations and prepare journal entries for the creation of a business entity.

LO 1-4 Understand and explain the differences between different forms of business

combinations.

LO 1-5 Make calculations and business combination journal entries in the presence of a

differential, goodwill, or a bargain purchase element.

LO 1-6 Understand additional considerations associated with business combinations.

SYNOPSIS OF CHAPTER 1

Intercorporate Acquisitions and Investments in Other Entities

Kraft’s Acquisition of Cadbury

A Brief Introduction

LO 1-1 Understand and explain the reasons for and different methods of business

expansion, the types of organizational structures, and the types of acquisitions.

An Introduction to Complex Business Structures

Enterprise Expansion

Business Objectives

Frequency of Business Combinations

Ethical Considerations

Business Expansion and Forms of Organizational Structure

Internal Expansion: Creating a Business Entity

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

External Expansion: Business Combinations

Organizational Structure and Financial Reporting

LO 1-2 Understand the development of standards related to acquisition accounting over

time.

The Development of Accounting for Business Combinations

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

LO 1-3 Make calculations and prepare journal entries for the creation of a business entity.

Accounting for Internal Expansion: Creating Business Entities

LO 1-4 Understand and explain the differences between different forms of business

combinations.

Accounting for External Expansion: Business Combinations

Legal Forms of Business Combinations

Methods of Effecting Business Combinations

Valuation of Business Entities

LO 1-5 Make calculations and business combination journal entries in the presence of a

differential, goodwill, or a bargain purchase element.

Acquisition Accounting

Fair Value Measurements

Applying the Acquisition Method

Goodwill

Combination Effected through the Acquisition of Net Assets

Combination Effected through Acquisition of Stock

Financial Reporting Subsequent to a Business Combination

LO 1-6 Understand additional considerations associated with business combinations.

Additional Considerations in Accounting for Business Combinations

Uncertainty in Business Combinations

In-Process Research and Development

Noncontrolling Equity Held Prior to Combination

NOTES ON POWERPOINT SLIDES

We have attempted to provide PowerPoint slides that will be useful to a broad set of users. Since

instructors often have different styles and preferences, we have attempted to include slides that

will accommodate different approaches and that can be adapted to classes with different levels of

preparation. For example, some instructors prefer to introduce the material before students have

read the chapter. We have tried to facilitate these types of introductory discussions by including

slides that replicate key points from the chapter. Other instructors expect students to have read

the chapter and attempted homework problems before coming to class. As a result, they may not

find it useful to review all of the topics in the chapter or to include slides that simply review

many of the details they expect students to study before class. However, instructors following

this approach often like to use sample exercises and problems built into the slides that allow

them to have extended discussions or to facilitate group interaction in class.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

If instructors elect to spend two class periods on the same subject, they might find a combination

of both styles to be useful by first introducing foundational material before students have read

the chapter and studied the topic, followed by an extended discussion the next class period after

students have read the chapter and attempted homework problems.

We have tried to develop slides that can facilitate a flexible approach to allow instructors to

select the slides that best match their objectives and style for class discussions. This is the reason

we are including over 100 slides for some chapters in the text. We do not expect all instructors

to use all slides, but the slide files should help support different teaching approaches and allow

instructors to select the subset of slides that best matches their specific discussion objectives.

The slides are organized by learning objective. We have included a slide at the beginning of

each learning objective to show where the new material begins. Instructors may or may not want

to use these learning objective slides in class. We provide them primarily as a way of organizing

the material. We also include short multiple choice questions at the end of most learning

objectives. Some instructors find it useful to pause periodically during class to assess students’

level of understanding. For this reason, we include several “practice quiz questions” that can be

used throughout class discussions to engage students, help them focus on key points, or to

facilitate group interaction. Finally, we provide longer exercises and problems that many

instructors find useful in assessing understanding and encouraging group learning.

LO 1-1 Understand and explain the reasons for and different methods of business expansion,

the types of organizational structures, and the types of acquisitions.

• Slides 3-14 summarize basic concepts related to LO1.

• Slide 7 provides a visual overview of internal and external expansion

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

LO 1-2 Understand the development of standards related to acquisition accounting over time.

• Slides 18-20 summarize basic concepts related to LO 1-2.

• Instructors should choose slides from this LO that they deem most important to

emphasize to their students

•

LO 1-3 Make calculations and prepare journal entries for the creation of a business entity.

• Slide 26 summarize basic concepts related to LO3.

• Slide 27 provides a hands-on example about internal expansion to allow students to

think through the journal entries on the parent’s and subsidiary’s books. This

example is set up to engage students without spending a lot of time. Display the

example information and ask students to explain what journal entries the parent (Slide

28) and subsidiary (Slide 29) would make. Instructors can click to show each journal

entry as students give their answers.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

LO 1-4 Understand and explain the differences between different forms of business

combinations.

• Slides 33-44 summarize basic business combinations as presented in the chapter.

• Slides 45-56 provide additional diagrams and detail to help students better understand

how these and other types of business combinations are consummated.

LO 1-5 Make calculations and business combination journal entries in the presence of a

differential, goodwill, or a bargain purchase element.

• Slides 60-69 introduce the concepts of this learning objective with a simple example.

• Slides 70-78 summarize the accounting for acquisition-related costs classified into

three general categories. The examples in slides 73–74 and 76-77 are helpful in giving

students hands on practice. Some instructors find it useful to have students take a few

minutes on each example to work individually or in small groups to attempt to solve

each exercise.

• Slides 79-87 summarizes acquisition accounting for a combination resulting in

goodwill using an asset acquisition to help students visualize the calculation and

recording of goodwill.

• Slides 88-89 summarize accounting for an asset acquisition that results in a bargain

purchase.

• Slides 90-97 use a practice exercise to help students visualize how accounting for a

bargain purchase differs from a goodwill scenario.

• Slides 98-102 provide an overview of how intangibles acquired in an acquisition

should be recorded. This topic is not covered extensively in the book. Instructors may

find it useful to take a few minutes to mention this topic using these slides. In

particular, slides 101-102 provide a brief example to help students understand how

separately identifiable intangibles should be recorded separately from goodwill.

• Slide 103 is an optional example to illustrate the journal entries associated with

acquisition accounting from the perspectives of both the acquiring and the target

companies.

• Slides 104-106 summarize the journal entries that would be used in an acquisition of

stock.

• Slide107 summarizes financial reporting subsequent to a business combination

LO 1-6 Understand additional considerations associated with business combinations.

• Slides 113-116 summarize basic concepts related to LO 1-6 (additional

considerations).

Preview Slides:

Slides 117-122 introduce the notion of consolidation in a very basic manner. While

chapter 1 alludes to consolidation briefly, it doesn’t go into any detail. Some

instructors find it useful to introduce a very simplistic view of consolidation in

chapter 1 as a teaser for chapters 2-5. While this material is not covered in the

students’ reading, some instructors find it useful to use these slides to preview what

students will be learning in the next several chapters.

Chapter 01 – INTERCORPORATE ACQUISITIONS AND INVESTMENTS IN OTHER ENTITIES

TEACHING IDEAS

1. Students could be asked to prepare a “Company Mergers & Acquisitions History.” Each

student (or group) is assigned a company from the Fortune 500 list that appears annually

in the April issue of Fortune. This could be reproduced and students could be assigned a

company based on their seating order in the class. Alternatively, the instructor may have

the list and then students may select a number between 1 and 100 at random and the

instructor will tell them the name of “their” company. The students then must obtain the

M&A activity of that company for the last 10 years from Moody’s Industrial Manual or

some similar source. Moody’s presents this information at the beginning of each

company’s profile information. The students should determine the number and magnitude

of the business combinations and investments for their company and prepare a historical

time line showing the business combinations and any other information they can obtain

on selected (or all) combinations. Several activities during the semester or quarter can be

based on the student’s company selection made at this time.

2. Students can be required to conduct a key word search online and asked to provide

examples and brief descriptions of several different types of merger activities.

3. Students could access the Wall Street Journal on-line article data base and search for an

article on a recent business combination. The students could be asked to provide a brief

oral or written summary of the article.