Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4-36 Comprehensive Problem: Differential Apportionment

a.

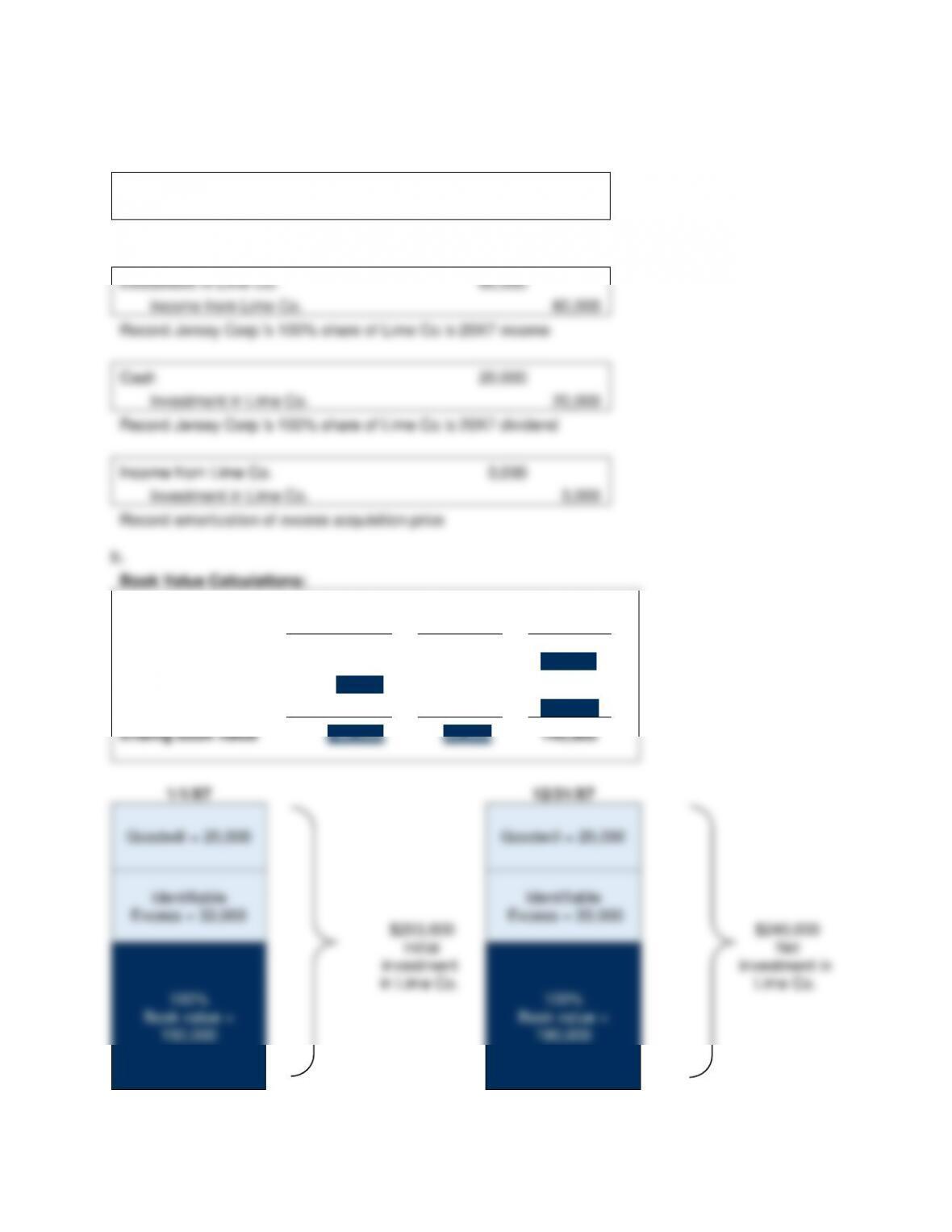

Equity Method Entries on Jersey Corp.’s Books:

Investment in Lime Co.

203,000

Cash

203,000

Record the initial investment in Lime Co.

Investment in Lime Co.

60,000

Income from Lime Co.

60,000

Record Jersey Corp.’s 100% share of Lime Co.’s 20X7 income

Cash

20,000

Investment in Lime Co.

20,000

Record Jersey Corp.’s 100% share of Lime Co.’s 20X7 dividend

Income from Lime Co.

3,000

Investment in Lime Co.

3,000

Record amortization of excess acquisition price

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

150,000

50,000

100,000

+ Net Income

60,000

60,000

– Dividends

(20,000)

(20,000)

Ending book value

190,000

50,000

140,000

1/1/X7

Goodwill = 20,000

Identifiable

Excess = 33,000

$203,000

Initial

investment

in Lime Co.

100%

Book value =

150,000

12/31/X7

Goodwill = 20,000

Identifiable

Excess = 30,000

$240,000

Net

investment in

Lime Co.

100%

Book value =

190,000

4-68

P4–36 (continued)

Basic Consolidation Entry

Common Stock

50,000

Retained Earnings

100,000

Income from Lime Co.

60,000

Dividends Declared

20,000

Investment in Lime Co.

190,000

Excess Value (Differential) Calculations:

Total

=

Buildings &

Equipment

+

Acc.

Depr.

+

Goodwill

Beginning balance

53,000

33,000

0

20,000

Changes

(3,000)

(3,000)

0

Ending balance

50,000

33,000

(3,000)

20,000

Amortized Excess Value Reclassification Entry:

Depreciation Expense

3,000

Income from Lime Co.

3,000

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

33,000

Goodwill

20,000

Accumulated Depreciation

3,000

Investment in Lime Co.

50,000

Eliminate Intercompany Accounts:

Accounts Payable

16,000

Accounts Receivable

16,000

Optional Accumulated Depreciation Consolidation Entry

Accumulated depreciation

60,000

Building & Equipment

60,000

Investment in

Income from

Lime Co.

Lime Co.

Acquisition Price

203,000

100% Net Income

60,000

60,000

100% Net Income

20,000

100% Dividends

3,000

Excess Val. Amort.

3,000

Ending Balance

240,000

57,000

Ending Balance

190,000

Basic

60,000

50,000

Excess Reclass.

3,000

0

0

4-69

P4–36 (continued)

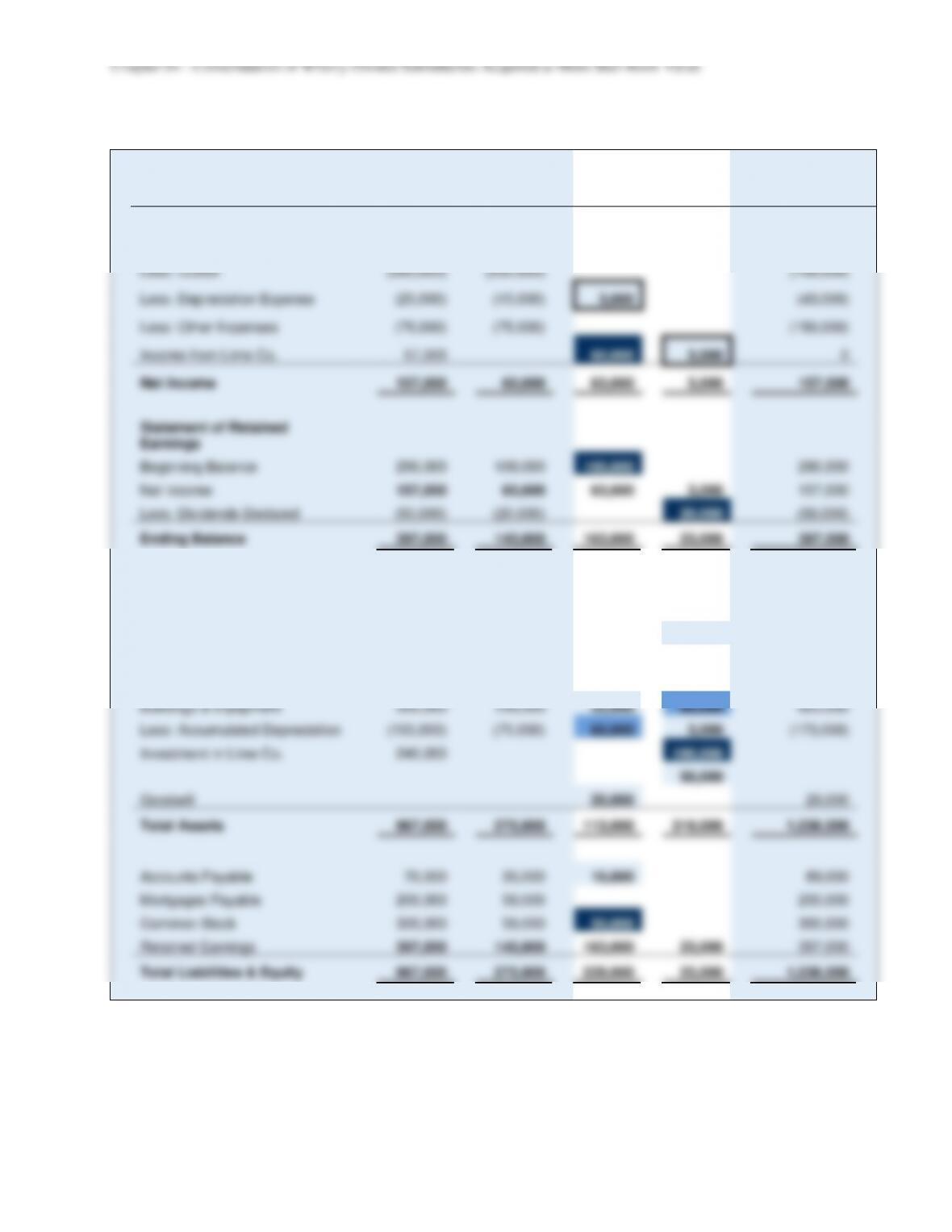

c.

Jersey

Corp.

Lime Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

700,000

400,000

1,100,000

Less: COGS

(500,000)

(250,000)

(750,000)

Less: Depreciation Expense

(25,000)

(15,000)

3,000

(43,000)

Less: Other Expenses

(75,000)

(75,000)

(150,000)

Income from Lime Co.

57,000

60,000

3,000

0

Net Income

157,000

60,000

63,000

3,000

157,000

Statement of Retained

Earnings

Beginning Balance

290,000

100,000

100,000

290,000

Net Income

157,000

60,000

63,000

3,000

157,000

Less: Dividends Declared

(50,000)

(20,000)

20,000

(50,000)

Ending Balance

397,000

140,000

163,000

23,000

397,000

Balance Sheet

Cash

82,000

25,000

107,000

Accounts Receivable

50,000

55,000

16,000

89,000

Inventory

170,000

100,000

270,000

Land

80,000

20,000

100,000

Buildings & Equipment

500,000

150,000

33,000

60,000

623,000

Less: Accumulated Depreciation

(155,000)

(75,000)

60,000

3,000

(173,000)

Investment in Lime Co.

240,000

190,000

50,000

Goodwill

20,000

20,000

Total Assets

967,000

275,000

113,000

319,000

1,036,000

Accounts Payable

70,000

35,000

16,000

89,000

Mortgages Payable

200,000

50,000

250,000

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

397,000

140,000

163,000

23,000

397,000

Total Liabilities & Equity

967,000

275,000

229,000

23,000

1,036,000

4-70

P4-37 Push-Down Accounting

a.

Entry to record acquisition of Lindy stock on books of Greenly:

Investment in Lindy Company Stock

935,000

Cash

935,000

b.

Entry to record revaluation of assets on books of Lindy Company at date of

combination:

Inventory

5,000

Land

85,000

Buildings

100,000

Equipment

70,000

Revaluation Capital

260,000

Revalue assets to reflect fair values at date of combination.

c.

Investment consolidation entry in consolidation worksheet prepared December 31,

20X6 (no other entries needed):

Common Stock — Lindy Company

100,000

Additional Paid-In Capital

400,000

Retained Earnings

175,000

Revaluation Capital

260,000

Investment in Lindy Company Stock

935,000

d.

Equity-method entries on the books of Greenly during 20X7:

Cash

50,000

Investment in Lindy Company Stock

50,000

Record dividend from Lindy Company.

Investment in Lindy Company Stock

88,000

Income from Lindy Company

88,000

Record equity-method income.

4-71

P4-37 (continued)

e.

Consolidation entries in consolidation worksheet prepared December 31, 20X7

(no other entries needed):

Common Stock — Lindy Company

100,000

Additional Paid-In Capital

400,000

Retained Earnings, January 1

175,000

Revaluation Capital

260,000

Income from Lindy Company

88,000

Dividends Declared

50,000

Investment in Lindy Company Stock

973,000

Eliminate ending investment balance.

$973,000 = $935,000 + $88,000 – $50,000

f.

Consolidation entries in consolidation worksheet prepared December 31, 20X8 (no

other entries needed):

Common Stock — Lindy Company

100,000

Additional Paid-In Capital

400,000

Retained Earnings, January 1

213,000

Revaluation Capital

260,000

Income from Lindy Company

90,000

Dividends Declared

50,000

Investment in Lindy Company Stock

1,013,000

Eliminate ending investment balance.

$213,000 = $175,000 + $88,000 – $50,000

$1,013,000 = $973,000 + $90,000 – $50,000