Chapter 08 – Intercompany Indebtedness

E8–12A (continued)

e.

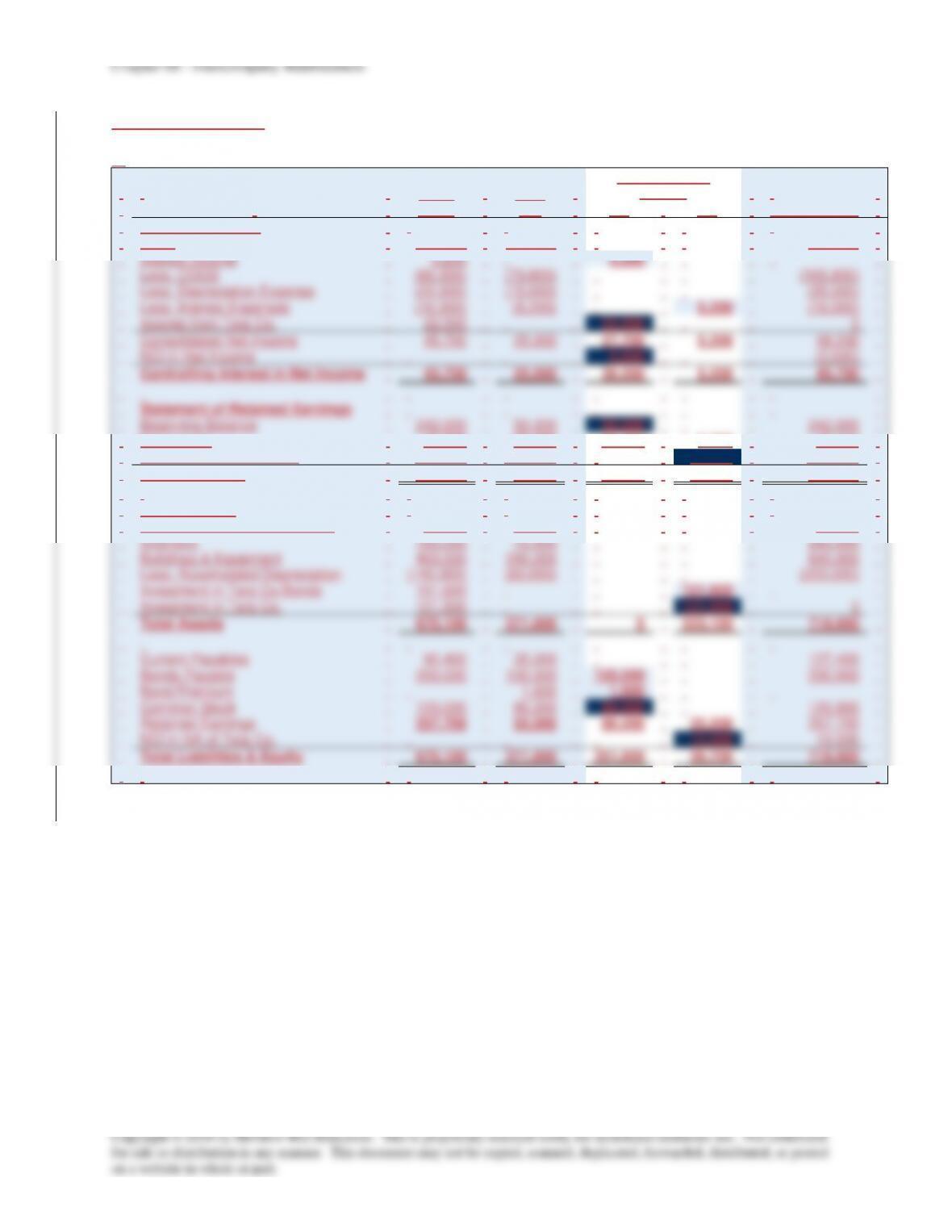

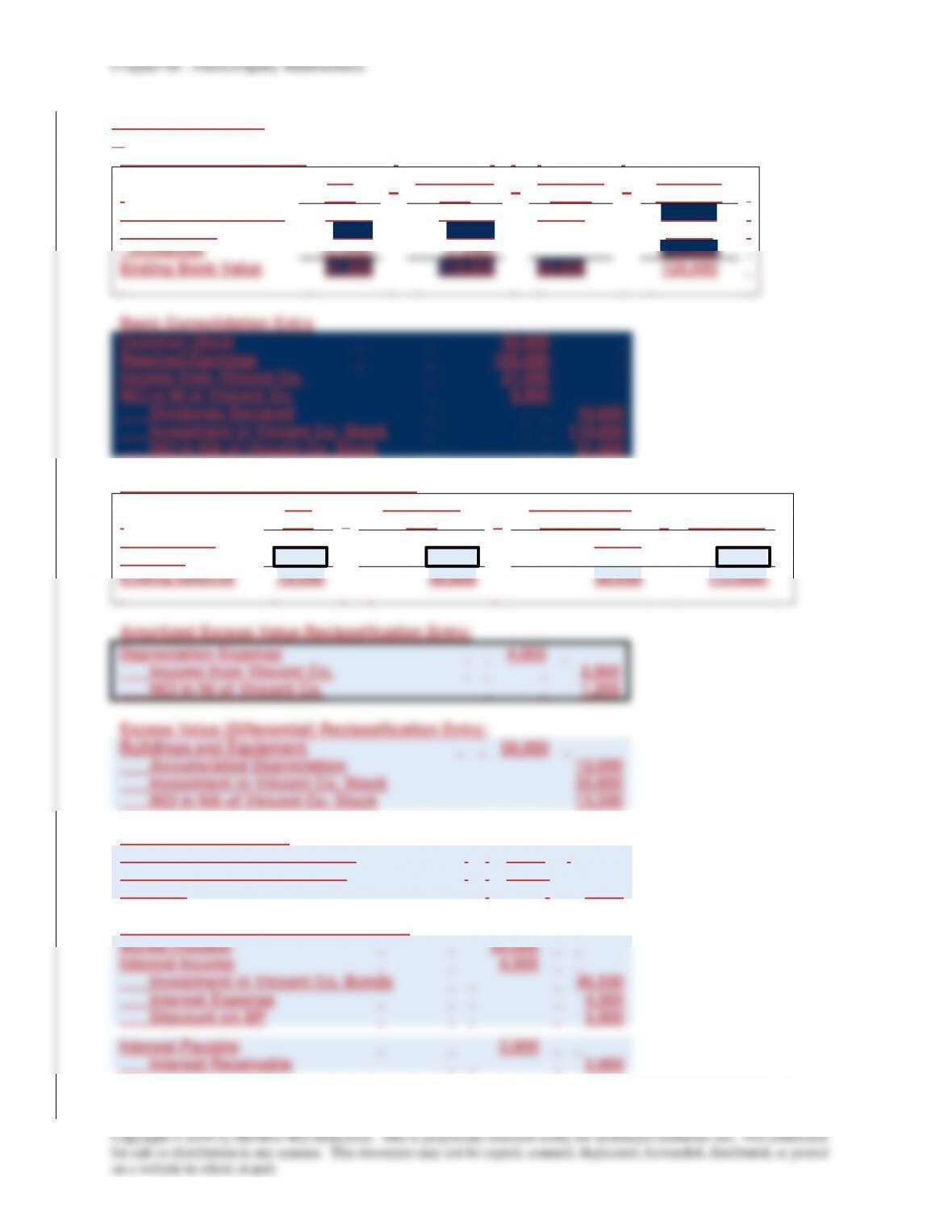

Consolidation entries, December 31, 20X7:

Bonds Payable

200,000

Premium on Bonds Payable

4,000

Interest Income

23,200

Investment in Bundle Company Bonds

194,000

Interest Expense

21,200

Investment in Bundle Co.

8,400

NCI in NA of Bundle Co.

3,600

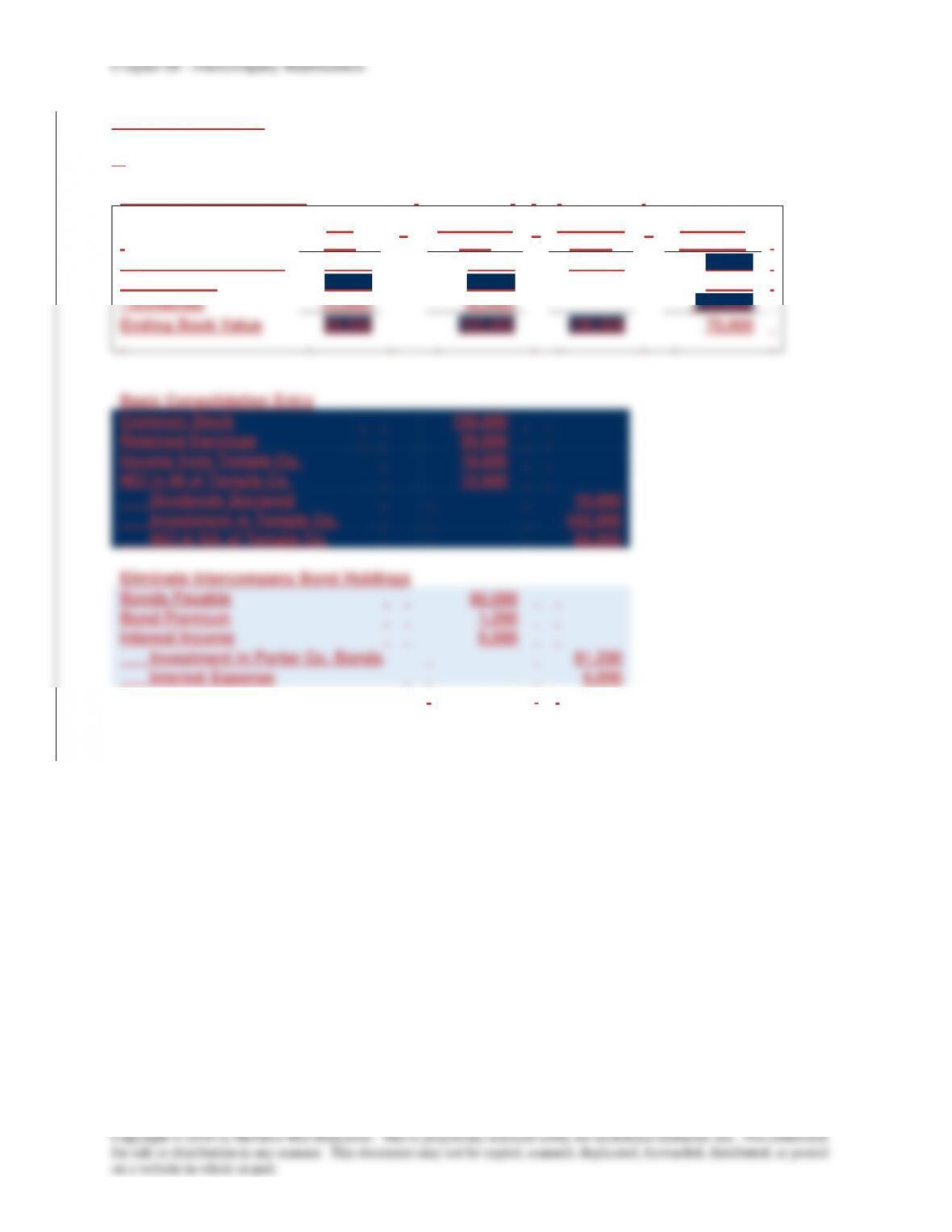

Eliminate intercompany bond holdings:

$4,000 = ($8,000 / 10 years) x 5 years

$23,200 = $22,000 + ($7,800 / 6.5 years)

$194,000 = $192,800 + ($7,800 / 6.5 years)

$21,200 = $22,000 – ($8,000 / 10 years)

$8,400 = ($13,000 – $1,000) x 0.70

$3,600 = ($13,000 – $1,000) x 0.30

Interest Payable

11,000

Interest Receivable

11,000

Eliminate intercompany receivable/payable.

The basic entry (not shown) would be adjusted by 2,000 (23,200-21,200) to

complete the elimination process.

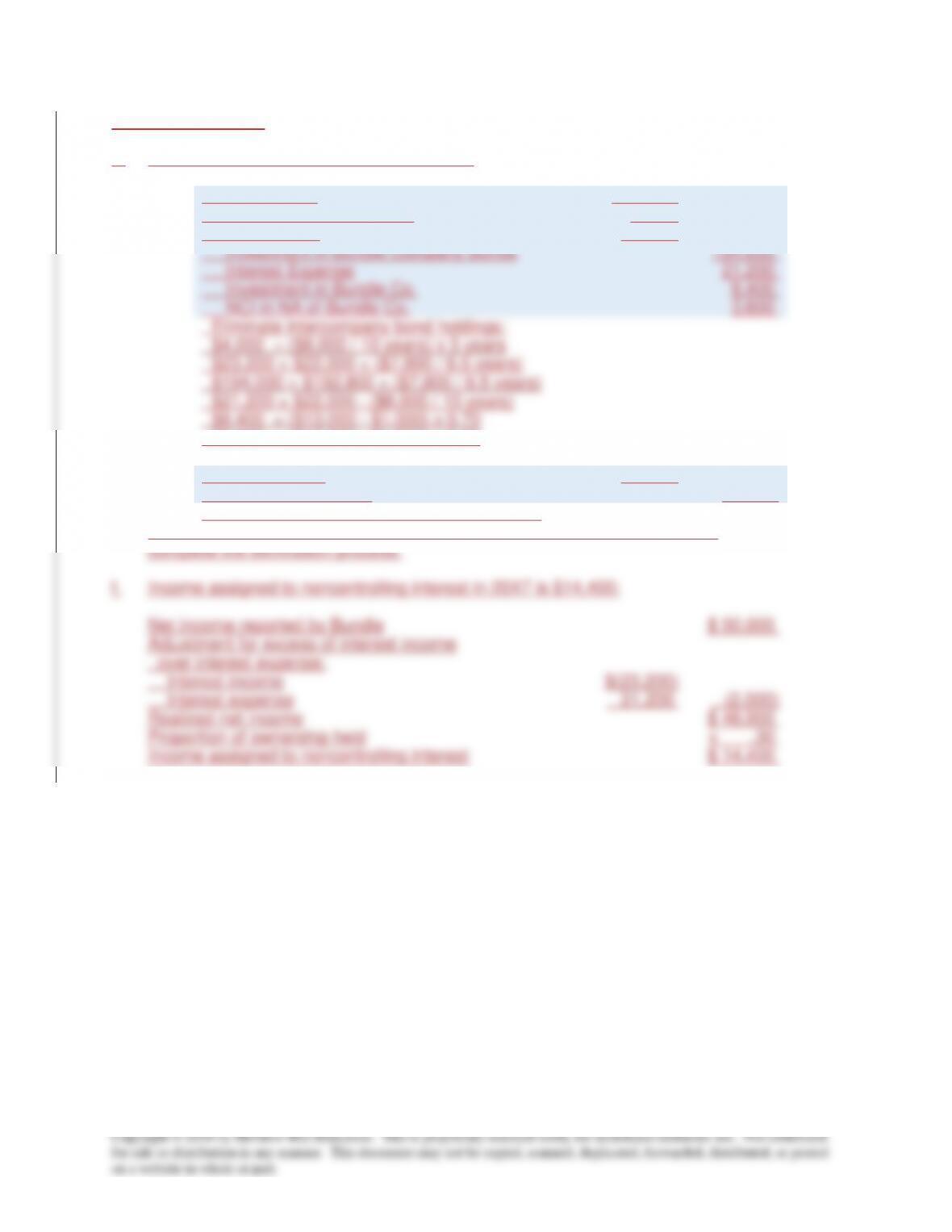

f.

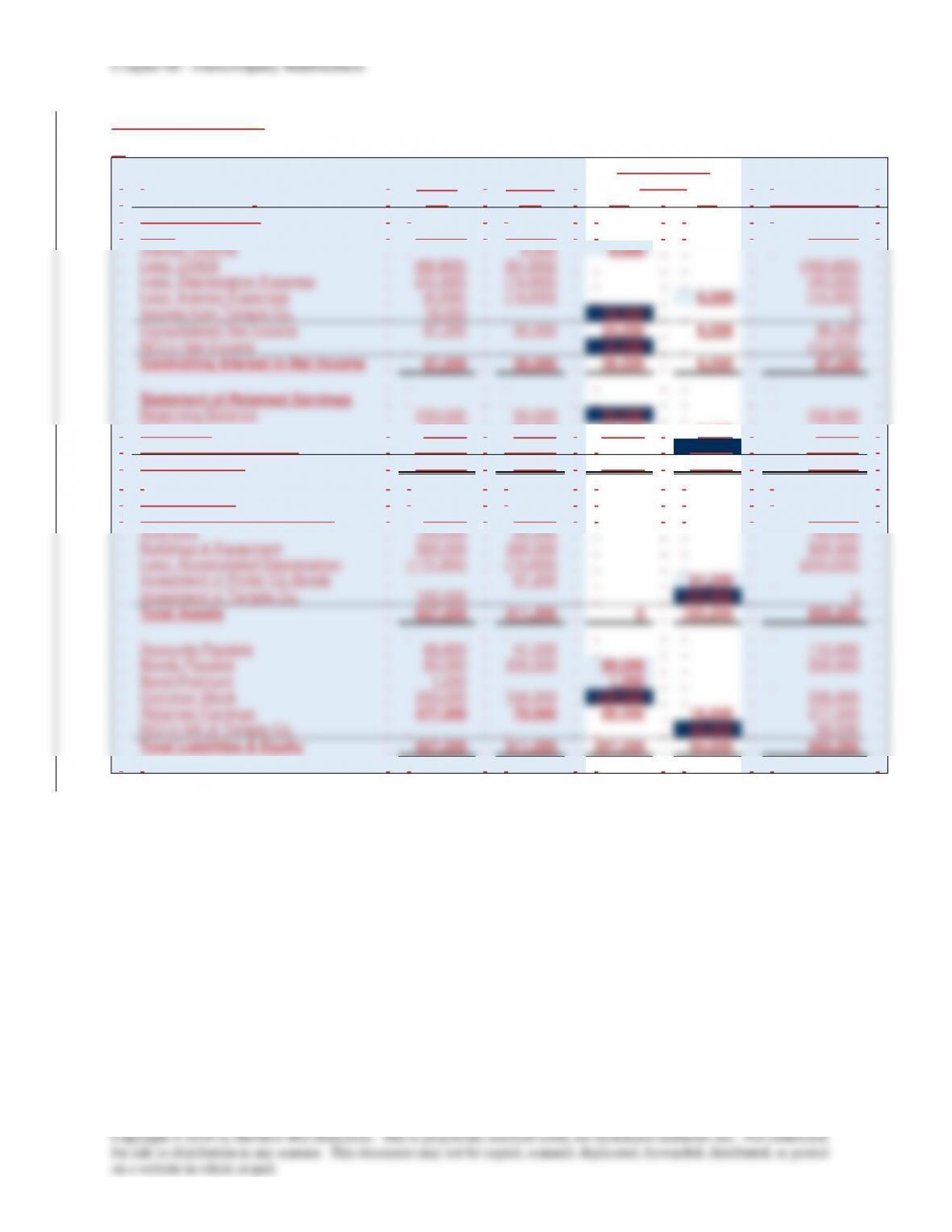

Income assigned to noncontrolling interest in 20X7 is $14,400:

Net income reported by Bundle

$ 50,000

Adjustment for excess of interest income

over interest expense:

Interest income

$(23,200)

Interest expense

21,200

(2,000)

Realized net income

$ 48,000

Proportion of ownership held

x .30

Income assigned to noncontrolling interest

$ 14,400

Chapter 08 – Intercompany Indebtedness

Eliminate intercompany receivable/payable.

The basic entry (not shown) would be adjusted by 200 (11,500-11,300) to complete

the elimination process.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

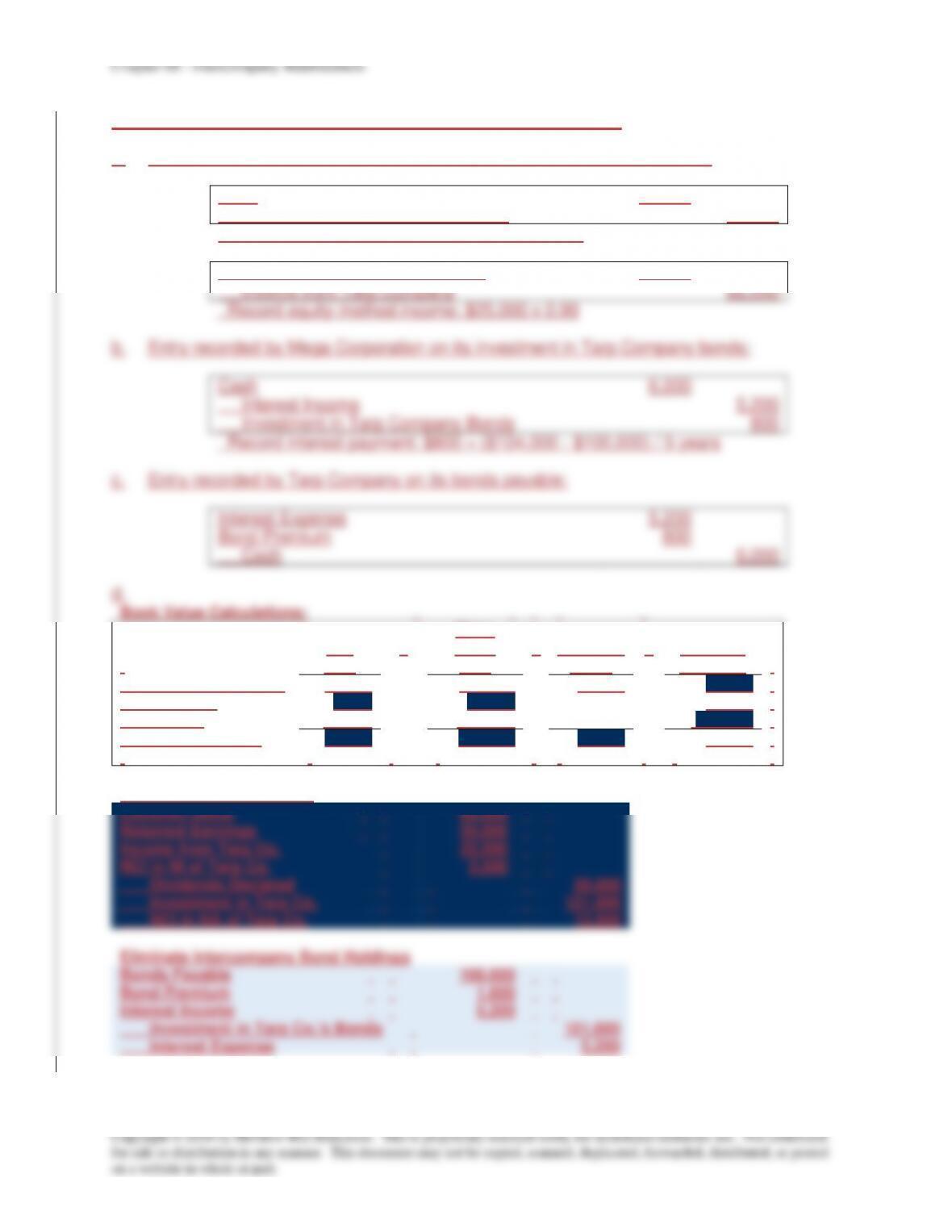

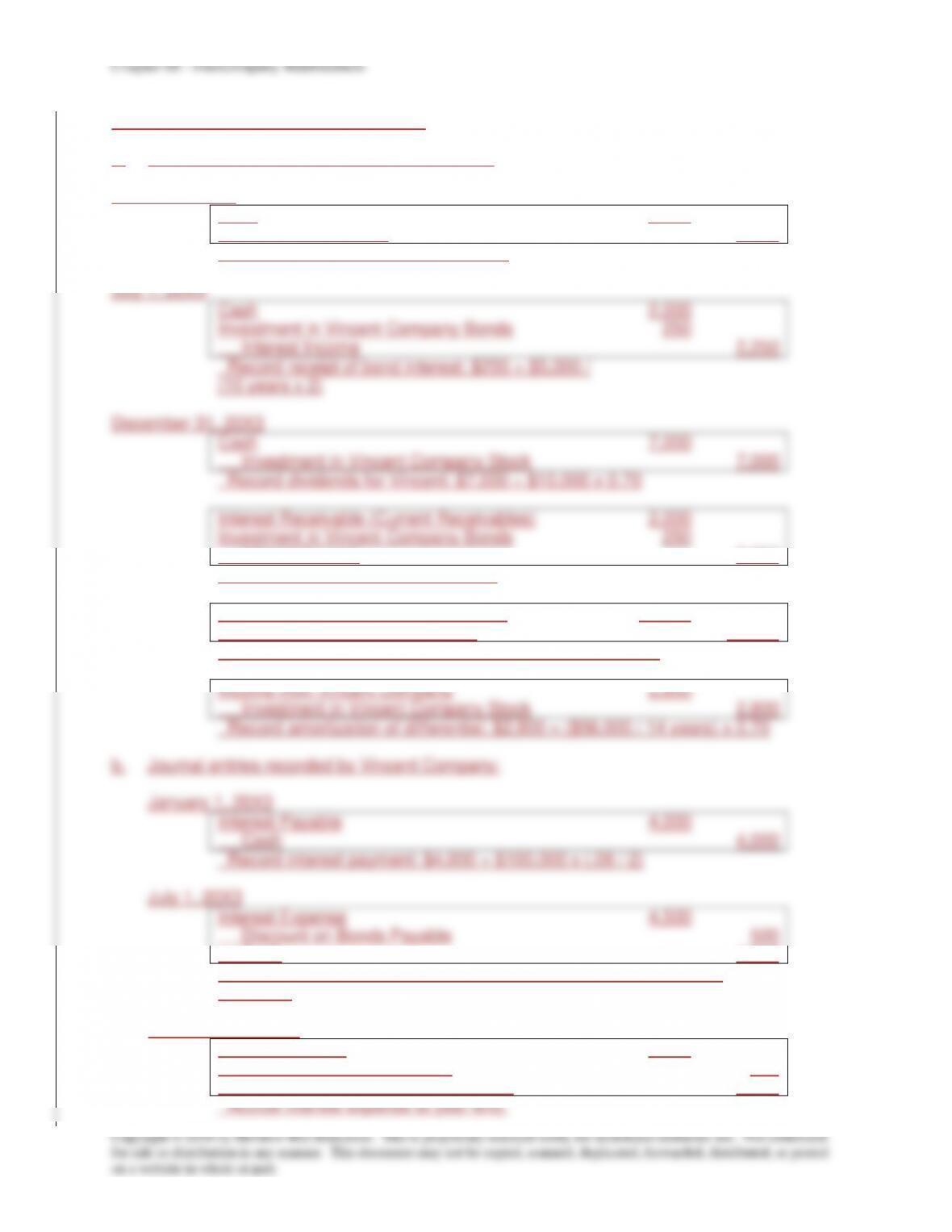

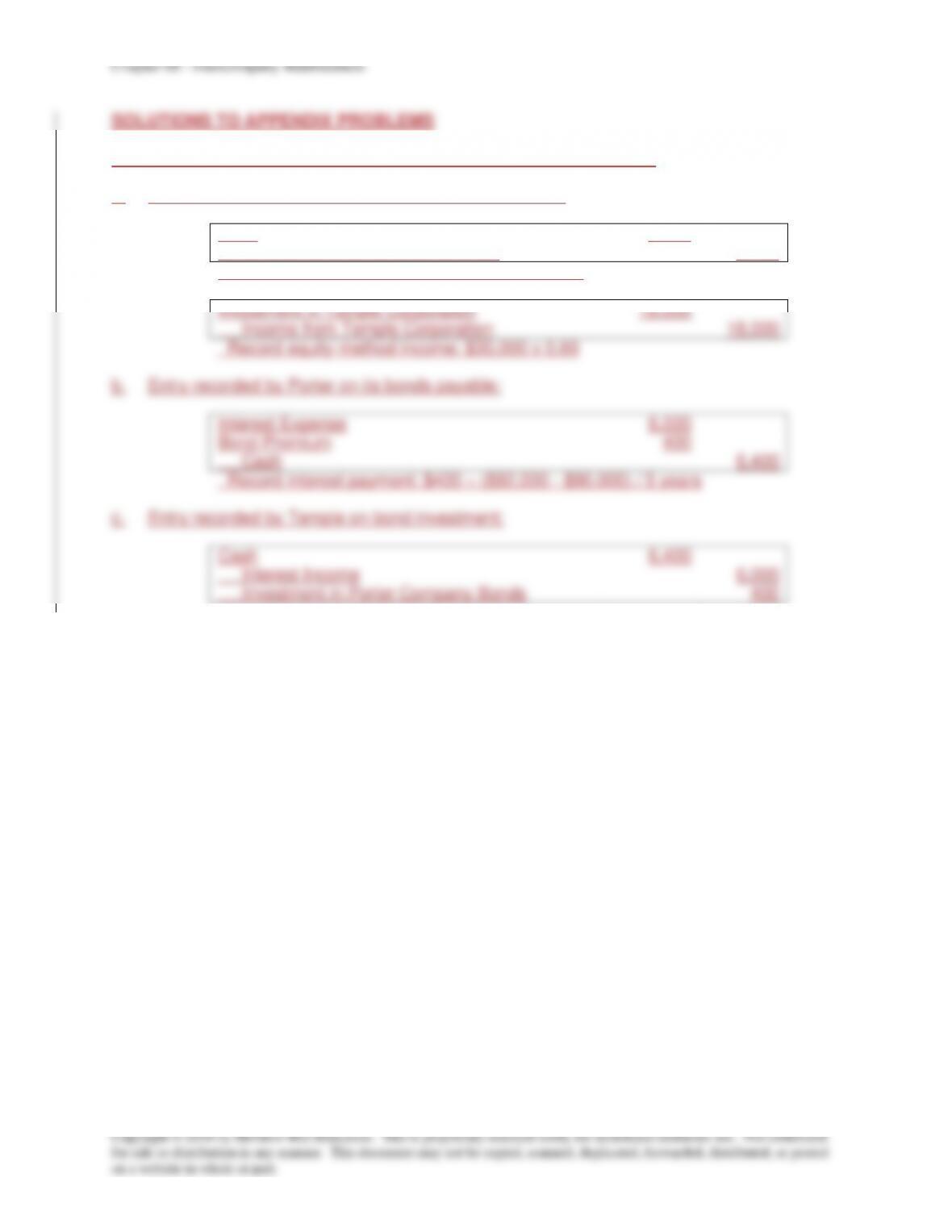

P8–14A Consolidation Worksheet with Sale of Bonds to Subsidiary

a.

Entries recorded by Porter on its investment in Temple:

Cash

6,000

Investment in Temple Corporation

6,000

Record dividends from Temple: $10,000 x 0.60

Investment in Temple Corporation

18,000

Income from Temple Corporation

18,000

Record equity-method income: $30,000 x 0.60

b.

Entry recorded by Porter on its bonds payable:

Interest Expense

6,000

Bond Premium

400

Cash

6,400

Record interest payment: $400 = ($82,000 – $80,000) / 5 years

c.

Entry recorded by Temple on bond investment:

Cash

6,400

Interest Income

6,000

Investment in Porter Company Bonds

400