Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5-17A Consolidation of Subsidiary with Negative Retained Earnings

Equity Method Entries on General Corp.’s Books:

Investment in Strap Co.

138,000

Cash

138,000

Record the initial investment in Strap Co.

Book Value Calculations:

NCI

20%

+

General

Corp.

80%

=

Common

Stock

+

Add. Paid-

in Capital

+

Retained

Earnings

Book value at

acquisition

29,000

116,000

100,000

75,000

(30,000)

Basic Consolidation Entry

Common Stock

100,000

Additional Paid-in Capital

75,000

Retained Earnings

30,000

Investment in Strap Co.

NCI in NA of Strap Co.

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-42

E5-17A (continued)

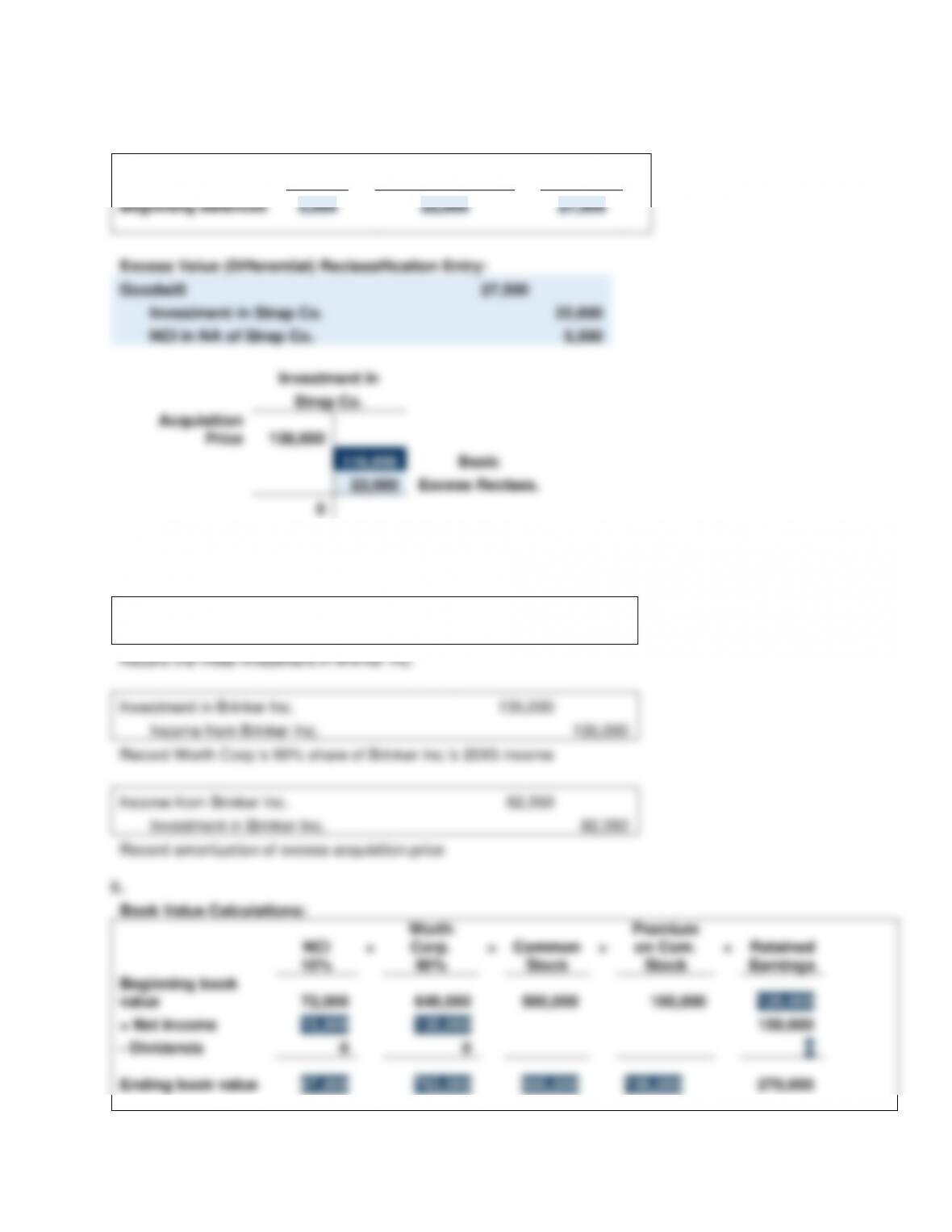

Excess Value (Differential) Calculations:

NCI

20%

+

General Corp.

80%

=

Goodwill

Beginning balances

5,500

22,000

27,500

Excess Value (Differential) Reclassification Entry:

Goodwill

27,500

Investment in Strap Co.

22,000

NCI in NA of Strap Co.

5,500

Investment in

Strap Co.

Acquisition

Price

138,000

116,000

Basic

22,000

Excess Reclass.

0

E5–18A Complex Assignment of Differential

a.

Equity Method Entries on Worth Corp.’s Books:

Investment in Brinker Inc.

864,000

Cash

864,000

Record the initial investment in Brinker Inc.

Investment in Brinker Inc.

135,000

Income from Brinker Inc.

135,000

Record Worth Corp.’s 90% share of Brinker Inc.’s 20X5 income

Income from Brinker Inc.

82,350

Investment in Brinker Inc.

82,350

Record amortization of excess acquisition price

Book Value Calculations:

NCI

10%

+

Worth

Corp.

90%

=

Common

Stock

+

Premium

on Com.

Stock

+

Retained

Earnings

Beginning book

value

72,000

648,000

500,000

100,000

120,000

+ Net Income

15,000

135,000

150,000

– Dividends

0

0

0

Ending book value

87,000

783,000

500,000

100,000

270,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

E5–18A (continued)

12/1/X5

Goodwill = 45,000

Identifiable

Excess = 171,000

$864,000

Initial

investment in

Brinker Inc.

90%

Book value =

648,000

12/31/X5

Goodwill = 45,000

Identifiable

Excess = 88,650

$916,650

Net

investment in

Brinker Inc.

90%

Book value =

783,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-44

E5–18A (continued)

Excess Value (Differential) Reclassification

entry:

Equipment

60,000

Discount on Notes Payable

42,500

Goodwill

50,000

Accumulated Depreciation

4,000

Investment in Brinker Inc.

133,650

NCI in NA of Brinker Inc.

14,850

SOLUTIONS TO PROBLEMS

P5-19 Reported Balances

a.

The investment balance reported by Roof will be $192,000.

b.

The amount of goodwill for the entity as a whole will be $25,000

[($192,000 + $48,000) – ($310,000 – $95,000)].

c.

Noncontrolling interest will be reported at $48,000 ($240,000 x 0.20).

P5-20 Acquisition Price

a.

$57,000 = ($120,000 – $25,000) x 0.60

b.

$81,000 = ($120,000 – $25,000) + $40,000 – $54,000

c.

$48,800 = ($120,000 – $25,000) + $27,000 – $73,200

P5–21 Multiple-Choice Questions on Applying the Equity Method [AICPA Adapted]

1. a – $20,000 = 100,000 x 20%. Because significant influence is not obtained, the cost method

2. a – Net increase to investment during 20X3: $18,000 (0.25 x $120,000 – 0.25 x $48,000)

3. c – $230,000 = ($600,000 x 0.4) – (($1,800,000 – $1,740,000) / 6)

4. d – $808,000 = $800,000 – (0.2 x $40,000) + (0.2 x $180,000) – (($800,000 – $600,000) / 10)

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-45

P5-22 Amortization of Differential

Journal entries recorded by Ball Corporation:

Equity Method Entries on Ball Corp.’s Books:

Investment in Krown Corp.

120,000

Preferred Stock

50,000

Additional Paid-in Capital

70,000

Record the initial investment in Krown Corp.

Investment in Krown Corp.

12,000

Income from Krown Corp.

12,000

Record Ball Corp.’s 30% share of Krown Corp.’s 20X5 income

Cash

3,000

Investment in Krown Corp.

3,000

Record Ball Corp.’s 30% share of Krown Corp.’s 20X5 dividend

Income from Krown Corp.

4,575

Investment in Krown Corp.

4,575

Record amortization of excess acquisition price

Amortization of differential assigned to buildings and equipment:

Fair value of buildings and equipment

$360,000

Book value of buildings and equipment

300,000

Differential

$60,000

Portion of stock held by Ball

x

0.30

Differential assigned to buildings and equipment

$18,000

Remaining life

÷

15

Yearly amortization

$1,200

Amortization of differential assigned to copyrights:

Purchase price

$120,000

Fair value of Krown‘s:

Total assets

$560,000

Total liabilities

(250,000)

$310,000

Proportion of stock held by Ball

x .30

(93,000)

Amount assigned to copyrights

$27,000

Remaining life

÷

8

Yearly amortization

$3,375

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-46

P5–23 Computation of Account Balances

a. Easy Chair Company 20X1 equity-method income:

Proportionate share of reported income ($30,000 x .40)

$ 12,000

Amortization of differential assigned to:

Buildings and equipment [($35,000 x .40) / 5 years]

(2,800)

Goodwill ($8,000: not impaired)

-0-

Investment Income

$

9,200

Assignment of differential

Purchase price

$150,000

Proportionate share of book value of

net assets ($320,000 x .40)

(128,000)

Proportionate share of fair value increase in

buildings and equipment ($35,000 x .40)

(14,000)

Goodwill

$ 8,000

b.

Dividend income, 20X1 ($9,000 x .40)

$ 3,600

c.

Cost-method account balance (unchanged):

$150,000

Equity-method account balance:

Balance, January 1, 20X1

$150,000

Investment income

9,200

Dividends received

(3,600)

Balance, December 31, 20X1

$155,600

P5–24 Complex Differential

a. Essex Company 20X2 equity-method income:

Proportionate share of reported net income

($80,000 x .30)

$24,000

Deduct increase in cost of goods sold for purchase

differential assigned to inventory ($30,000 x .30)

(9,000)

Deduct amortization of differential assigned to:

Buildings and equipment

[($320,000 – $260,000) x .30] / 12 years]

(1,500)

Patent [($25,000 x .30) / 10 years]

(750)

Equity-method income for 20X2

$12,750

Purchase Price

$165,000

Investment income for 20X2

$12,750

Dividends received in 20X2 ($9,000 x .30)

(2,700)

10,050

Investment account balance on December 31, 20X2

$175,050

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-47

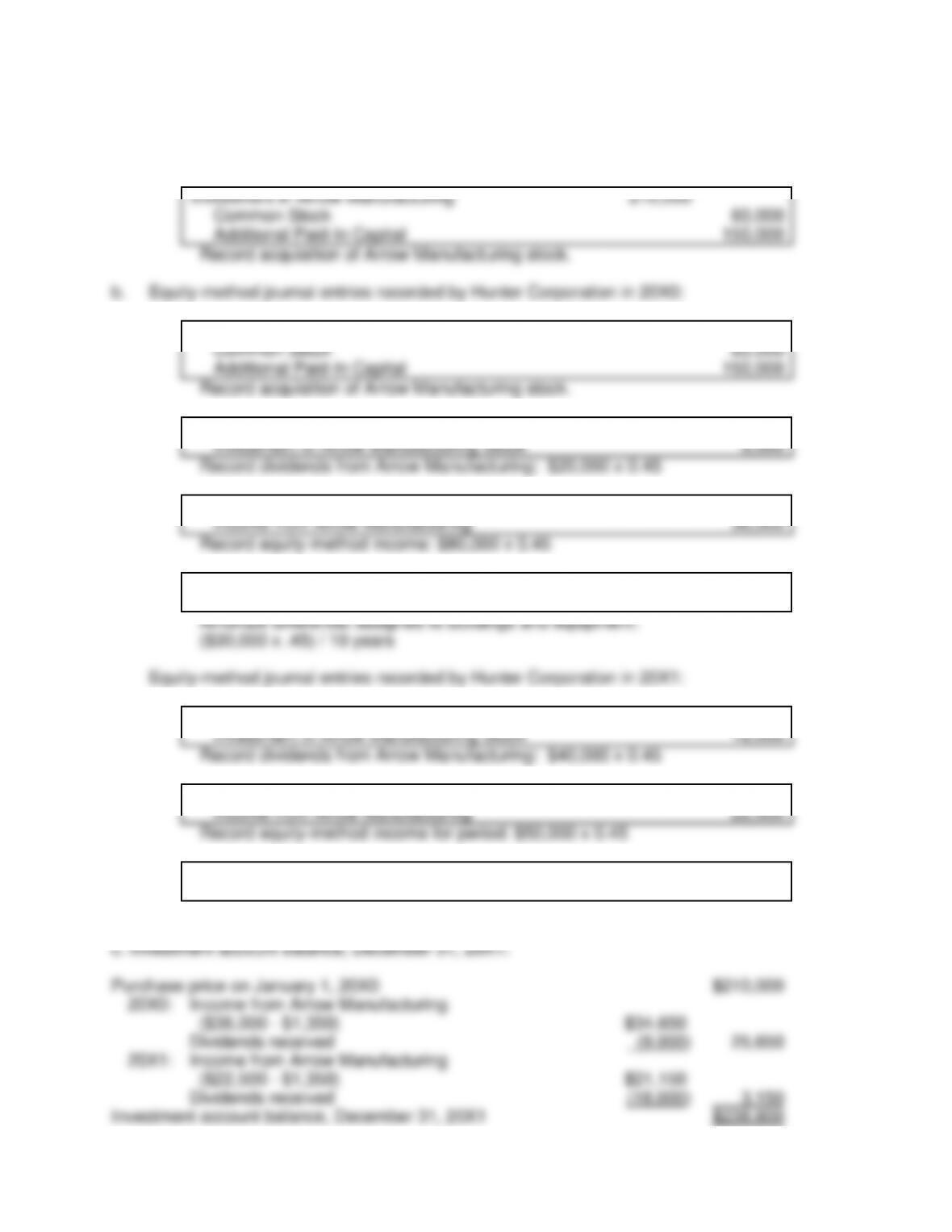

P5–25 Equity Entries with Differential

a. Journal entry recorded by Hunter Corporation:

Investment in Arrow Manufacturing

210,000

Common Stock

60,000

Additional Paid-In Capital

150,000

Record acquisition of Arrow Manufacturing stock.

(1)

Investment in Arrow Manufacturing Stock

210,000

Common Stock

60,000

Additional Paid-In Capital

150,000

Record acquisition of Arrow Manufacturing stock.

(2)

Cash

9,000

Investment in Arrow Manufacturing Stock

9,000

Record dividends from Arrow Manufacturing: $20,000 x 0.45

(3)

Investment in Arrow Manufacturing Stock

36,000

Income from Arrow Manufacturing

36,000

Record equity-method income: $80,000 x 0.45

(4)

Income from Arrow Manufacturing

1,350

Investment in Arrow Manufacturing Stock

1,350

Amortize differential assigned to buildings and equipment:

($30,000 x .45) / 10 years

(1)

Cash

18,000

Investment in Arrow Manufacturing Stock

18,000

Record dividends from Arrow Manufacturing: $40,000 x 0.45

(2)

Investment in Arrow Manufacturing Stock

22,500

Income from Arrow Manufacturing

22,500

Record equity-method income for period: $50,000 x 0.45

(3)

Income from Arrow Manufacturing

1,350

Investment in Arrow Manufacturing Stock

1,350

Amortize differential assigned to buildings and equipment.

Purchase price on January 1, 20X0

$210,000

20X0:

Income from Arrow Manufacturing

($36,000 – $1,350)

$34,650

Dividends received

(9,000)

25,650

20X1:

Income from Arrow Manufacturing

($22,500 – $1,350)

$21,150

Dividends received

(18,000)

3,150

Investment account balance, December 31, 20X1

$238,800

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-48

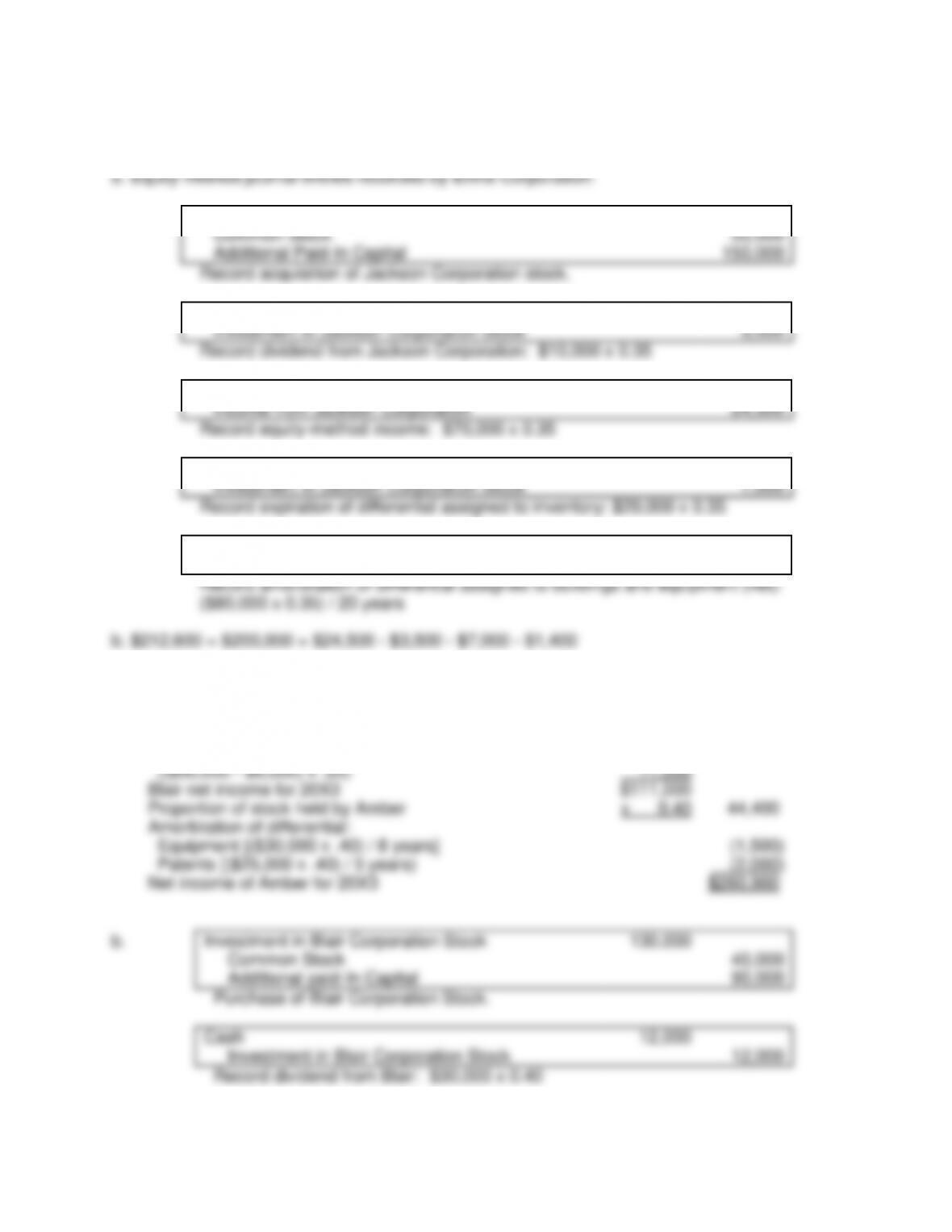

P5–26 Equity Entries with Differential

(1)

Investment in Jackson Corporation Stock

200,000

Common Stock

50,000

Additional Paid-In Capital

150,000

Record acquisition of Jackson Corporation stock.

(2)

Cash

3,500

Investment in Jackson Corporation Stock

3,500

Record dividend from Jackson Corporation: $10,000 x 0.35

(3)

Investment in Jackson Corporation Stock

24,500

Income from Jackson Corporation

24,500

Record equity-method income: $70,000 x 0.35

(4)

Income from Jackson Corporation

7,000

Investment in Jackson Corporation Stock

7,000

Record expiration of differential assigned to inventory: $20,000 x 0.35

(5)

Income from Jackson Corporation

1,400

Investment in Jackson Corporation Stock

1,400

Record amortization of differential assigned to buildings and equipment (net):

($80,000 x 0.35) / 20 years

b. $212,600 = $200,000 + $24,500 – $3,500 – $7,000 – $1,400

P5–27 Additional Ownership Level

a.

Operating income of Amber for 20X3

$220,000

Operating income of Blair for 20X3

$100,000

Add: Equity income from Carmen

[($50,000 – $6,000) x .25)

11,000

Blair net income for 20X3

$111,000

Proportion of stock held by Amber

x 0.40

44,400

Amortization of differential:

Equipment [($30,000 x .40) / 8 years]

(1,500)

Patents [($25,000 x .40) / 5 years)

(2,000)

Net income of Amber for 20X3

$260,900

b.

Investment in Blair Corporation Stock

130,000

Common Stock

40,000

Additional paid-In Capital

90,000

Purchase of Blair Corporation Stock.

Cash

12,000

Investment in Blair Corporation Stock

12,000

Record dividend from Blair: $30,000 x 0.40

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-49

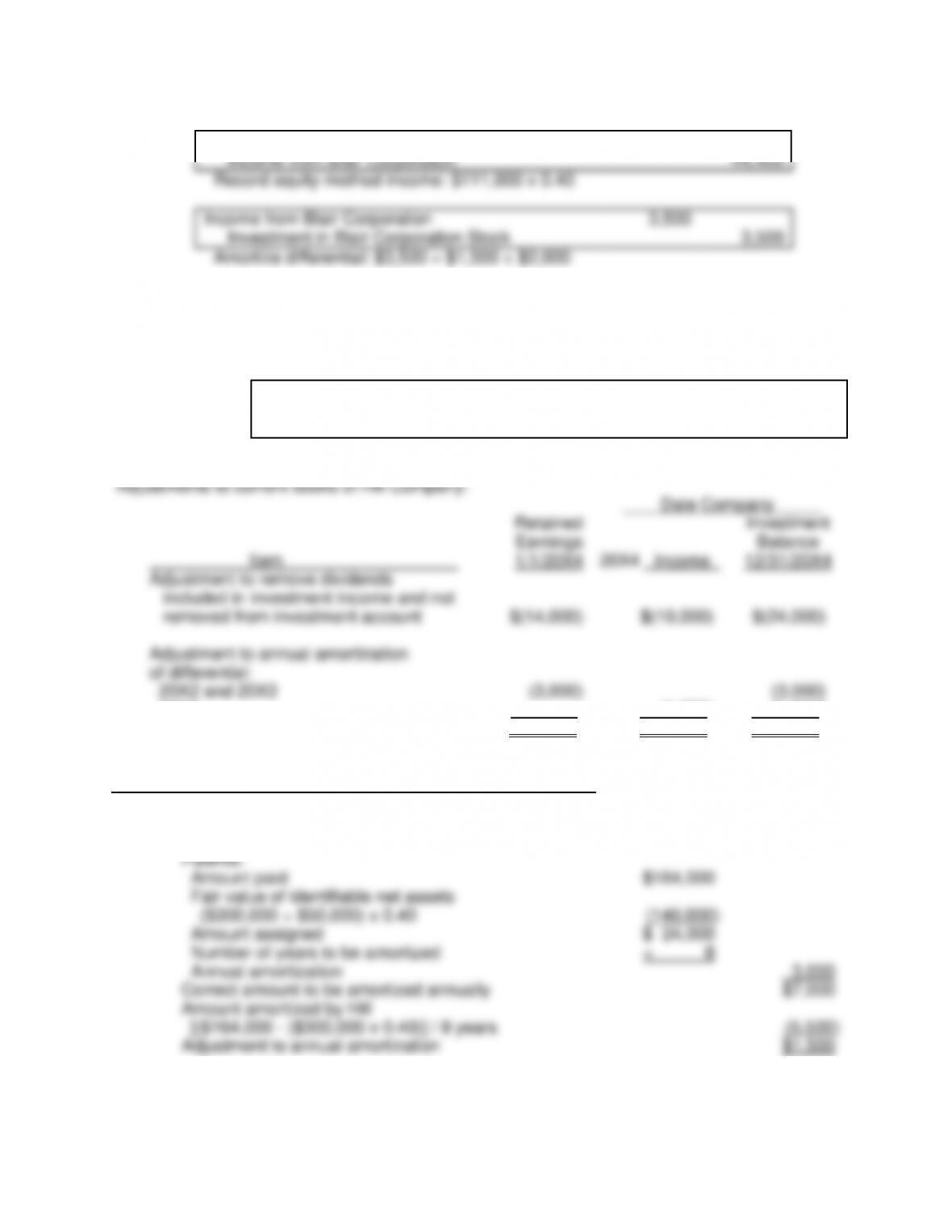

Investment in Blair Corporation Stock

44,400

Income from Blair Corporation

44,400

Record equity-method income: $111,000 x 0.40

Income from Blair Corporation

3,500

Investment in Blair Corporation Stock

3,500

Amortize differential: $3,500 = $1,500 + $2,000

P5–28 Correction of Error

Required correcting entry:

Retained Earnings

17,000

Income from Dale Company

11,500

Investment in Dale Company Stock

28,500

Dale Company

Item

Retained

Earnings

1/1/20X4

20X4 Income

Investment

Balance

12/31/20X4

Adjustment to remove dividends

included in investment income and not

removed from investment account

$(14,000)

$(10,000)

$(24,000)

Adjustment to annual amortization

of differential:

20X2 and 20X3

(3,000)

(3,000)

20X4

(1,500)

(1,500)

Required adjustment to account balance

$(17,000)

$(11,500)

$(28,500)

Computation of adjustment to annual amortization of differential

Correct amortization of differential assigned to:

Equipment [($120,000 – $70,000) x 0.40] / 5 years

$4,000

Patents:

Amount paid

$164,000

Fair value of identifiable net assets

($300,000 + $50,000) x 0.40

(140,000)

Amount assigned

$ 24,000

Number of years to be amortized

÷ 8

Annual amortization

3,000

Correct amount to be amortized annually

$7,000

Amount amortized by Hill

[($164,000 – ($300,000 x 0.40)] / 8 years

(5,500)

Adjustment to annual amortization

$1,500

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-29 Majority-Owned Subsidiary Acquired at Greater than Book Value

a.

Equity Method Entries on Porter Corp.’s Books:

Investment in Darla Corp.

102,200

Cash

102,200

Record the initial investment in Darla Corp.

Book Value Calculations:

NCI

30%

+

Porter

Corp.

70%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

37,500

87,500

40,000

85,000

Basic consolidation entry

40,000

85,000

Investment in Darla Corp.

NCI in NA of Darla Corp.

Excess Value (Differential) Calculations:

+

=

Inventory

+

Beginning balances