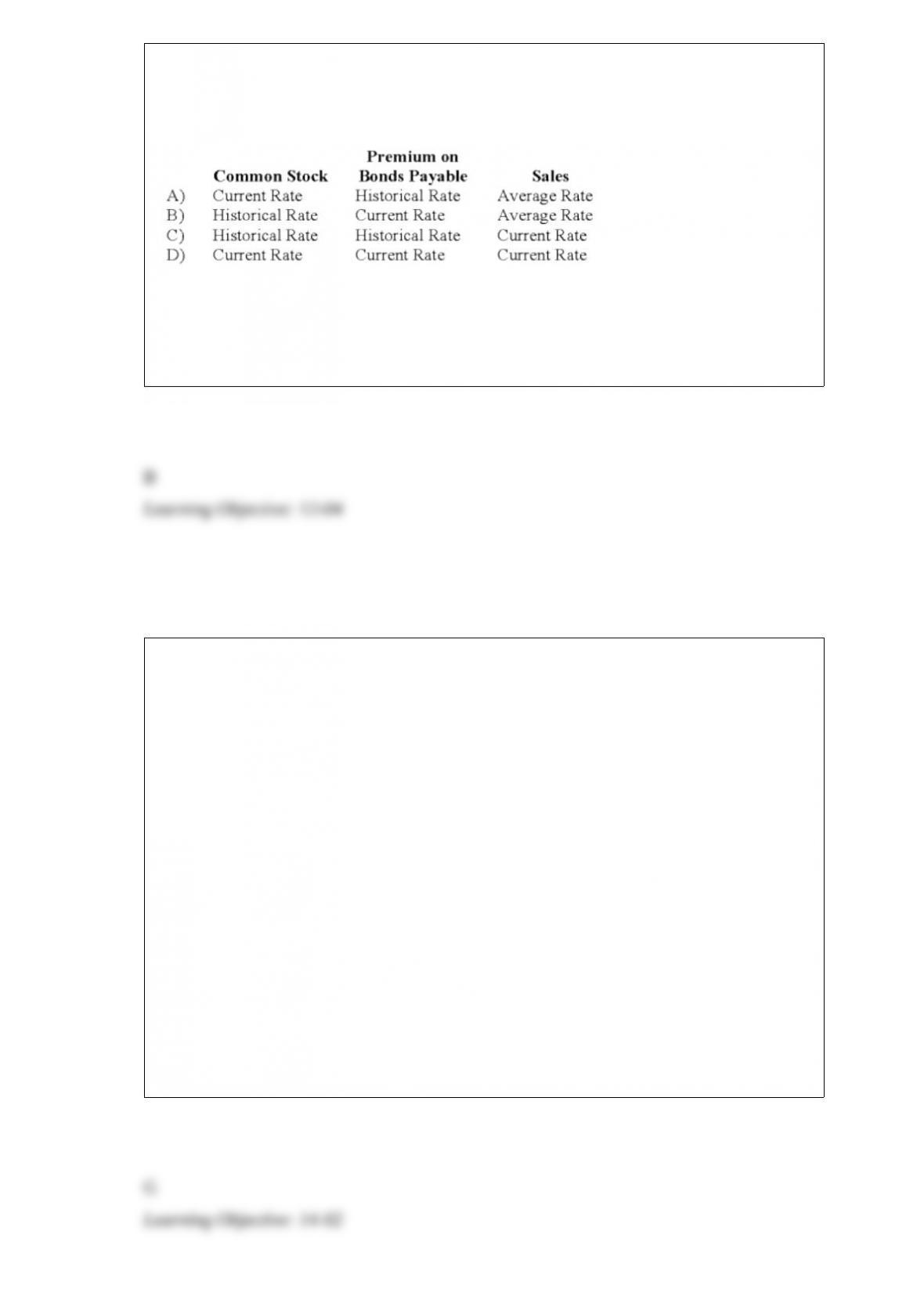

If the functional currency is the local currency of a foreign subsidiary, what exchange

rates should be used to translate the items below, assuming the foreign subsidiary is in a

country which has not experienced hyperinflation over three years?

A. Option A

B. Option B

C. Option C

D. Option D

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Comment Letter

A private, not-for-profit hospital received a cash contribution of $100,000 from

Samantha Hicks on November 14, 20X8. Ms. Hicks specified the money be used to

acquire equipment. On December 31, 20X8, the hospital had not expended any of Ms.

Hicks’ contribution. On the statement of changes in net assets for the year ended

December 31, 20X8, the hospital should report the contribution as a $100,000 increase

in

A. temporarily restricted net assets.

B. unrestricted net assets.

C. fund balance.

D. deferred revenue.

Under ASC 805, consolidation follows largely which theory approach?

A. Proprietary

B. Parent company

C. Entity

D. Variable

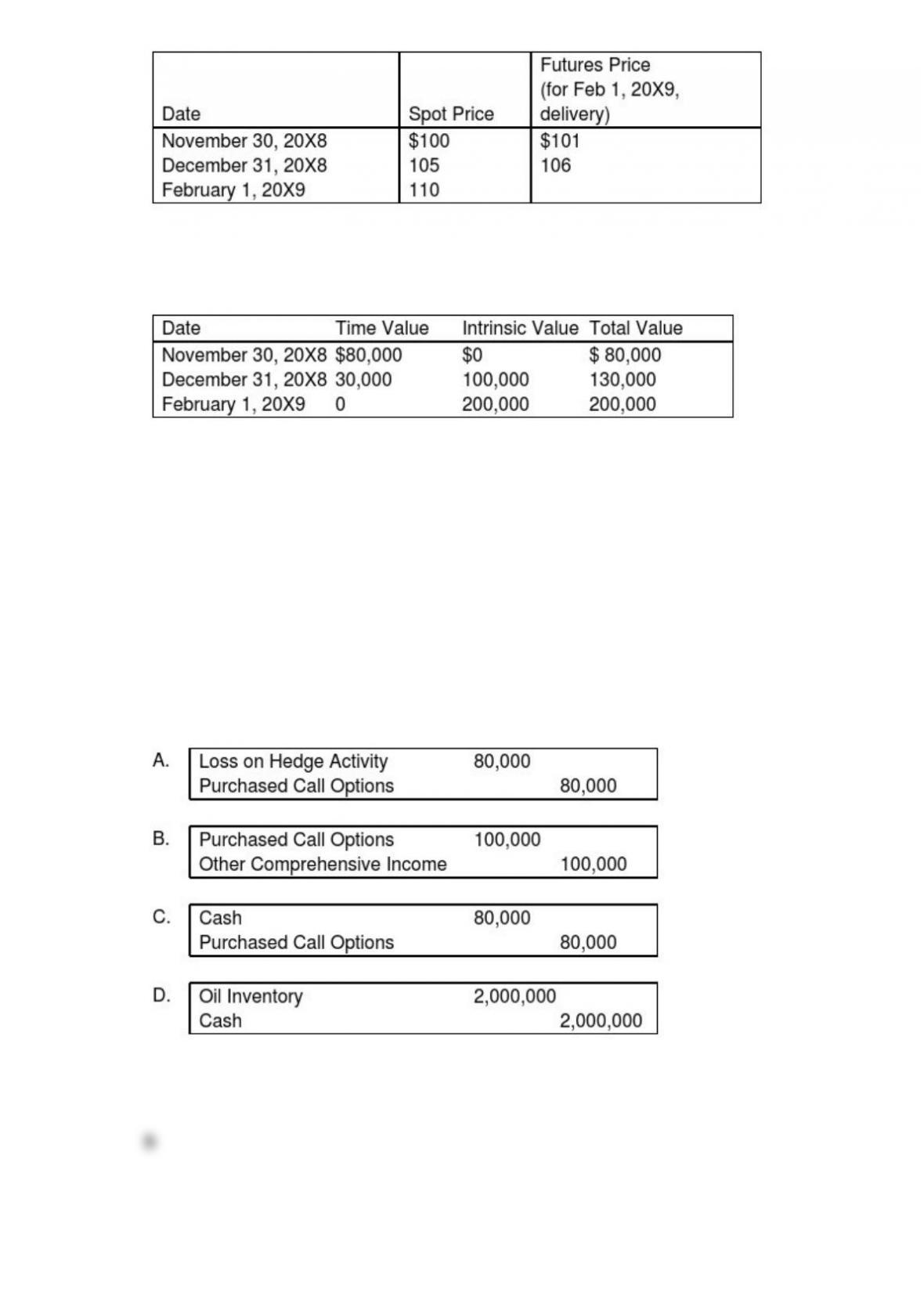

Spiralling crude oil prices prompted AMAR Company to purchase call options on oil as

a price-risk-hedging device to hedge the expected increase in prices on an anticipated

purchase of oil. On November 30, 20X8, AMAR purchases call options for 20,000

barrels of oil at $100 per barrel at a premium of $4 per barrel, with a February 1, 20X9,

call date. The following is the pricing information for the term of the call:

The information for the change in the fair value of the options follows:

On February 1, 20X9, AMAR sells the options at their value on that date and acquires

20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per

barrel.

Based on the preceding information, which of the following entries will be required on

February 1, 20X9?

Creditors may file which type of petition when seeking remedy under the Bankruptcy

Code?

I. Voluntary

II. Involuntary

A. I only

B. II only

C. Either I or II

D. Neither I nor II

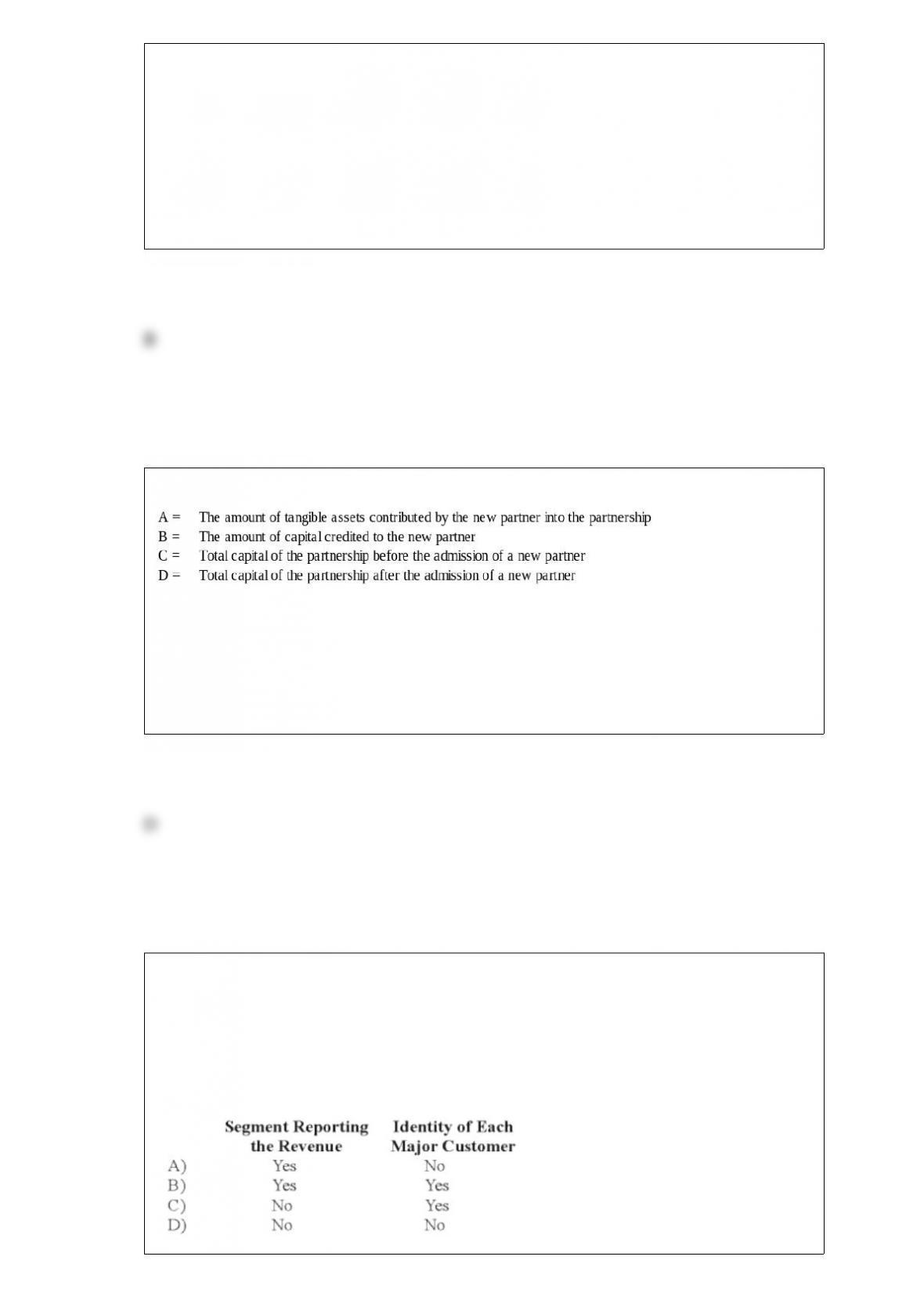

Refer to the above information. Which statement below is correct if a new partner’s

goodwill is recognized upon contributing assets into the partnership?

A. B = A and D > C + A

B. B < A and D < C + A

C. B > A and D = C + A

D. B > A and D > C + A

Stone Company reported $100,000,000 of revenues on its 20X8 income statement.

During the year ended December 31, 20X8, Stone made sales of $8,000,000 to external

customers in Western Europe. In addition, Stone made sales of $10,000,000 to the U.S.

government and $4,000,000 of sales to various state governments. In the footnotes to its

financial statements for 20X8, in reporting enterprisewide disclosures, Stone is required

to disclose:

A. Option A

B. Option B

C. Option C

D. Option D

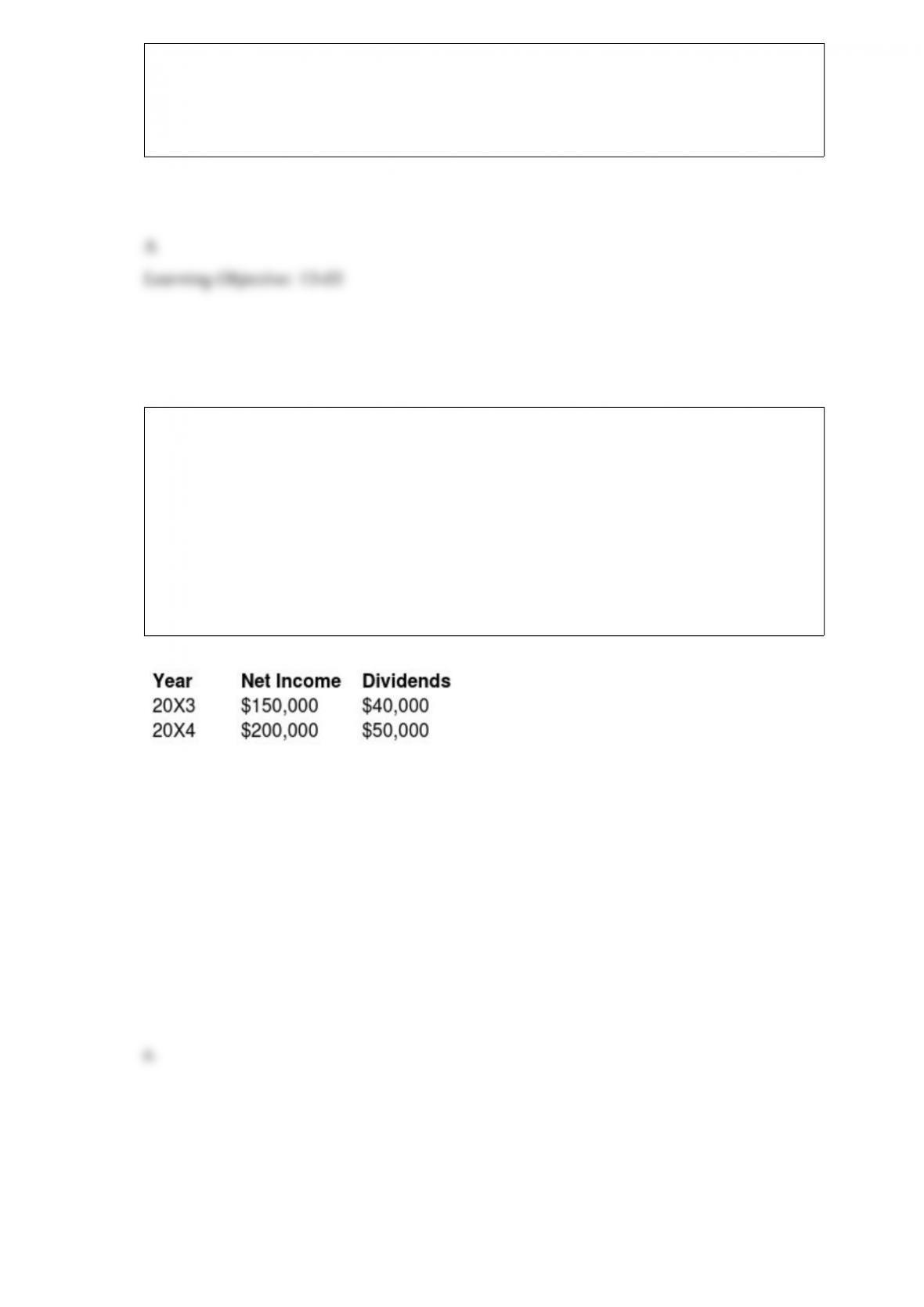

Pisa Company acquired 75 percent of Siena Company on January 1, 20X3 for

$712,500. The fair value of the noncontrolling interest was equal to 25 percent of book

value. On the date of acquisition, Siena had common stock outstanding of $300,000 and

a balance in retained earnings of $650,000. During 20X3, Siena purchased inventory for

$35,000 and sold it to Pisa for $50,000. Of this amount, Pisa reported $20,000 in ending

inventory in 20X3 and later sold it in 20X4. In 20X4, Pisa sold inventory it had

purchased for $40,000 to Siena for $60,000. Siena sold $45,000 of this inventory in

20X4.

Income and dividend information for Siena for 20X3 and 20X4 are as follows:

Pisa Company uses the fully adjusted equity method.

Required:

a. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X3.

b. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X4.

Tower Corporation’s controller has just finished preparing a consolidated balance sheet,

income statement, and statement of changes in retained earnings for the year ended

December 31, 20X9. Tower owns 80 percent of Network Corporation’s stock, which it

acquired at underlying book value on November 1, 20X6. At that date, the fair value of

the noncontrolling interest was equal to 20 percent of Network Corporation’s book

value. The following information is available:

Consolidated net income for 20X9 was $160,000.

Network reported net income of $50,000 for 20X9.

Tower paid dividends of $30,000 in 20X9.

Network paid dividends of $10,000 in 20X9.

Tower issued common stock on February, 18, 20X9, for a total of $100,000.

Consolidated wages payable decreased by $6,000 in 20X9.

Consolidated depreciation expense for the year was $15,000.

Consolidated accounts receivable decreased by $20,000 in 20X9.

Bonds payable of Tower with a book value of $102,000 were retired for $100,000 on

December 31, 20X9.

Consolidated amortization expense on patents was $10,000 for 20X9.

Tower sold land that it had purchased for $75,000 to a nonaffiliate for $80,000 on June

10, 20X9.

Consolidated accounts payable decreased by $7,000 during 20X9.

Total purchases of equipment by Tower and Network during 20X9 were $180,000.

Consolidated inventory increased by $36,000 during 20X9.

There were no intercompany transfers between Tower and Network in 20X9 or prior

years except for Network’s payment of dividends. Tower uses the indirect method in

preparing its cash flow statement.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash provided by operating activities for 20X9?

A. $207,000

B. $163,000

C. $180,000

D. $149,000

Beta Company acquired 100 percent of the voting common shares of Standard Video

Corporation, its bitter rival, by issuing bonds with a par value and fair value of

$150,000. Immediately prior to the acquisition, Beta reported total assets of $500,000,

liabilities of $280,000, and stockholders’ equity of $220,000. At that date, Standard

Video reported total assets of $400,000, liabilities of $250,000, and stockholders’ equity

of $150,000. Included in Standard’s liabilities was an account payable to Beta in the

amount of $20,000, which Beta included in its accounts receivable.

Based on the preceding information, what amount of total assets was reported in the

consolidated balance sheet immediately after acquisition?

A. $650,000

B. $880,000

C. $920,000

D. $750,000

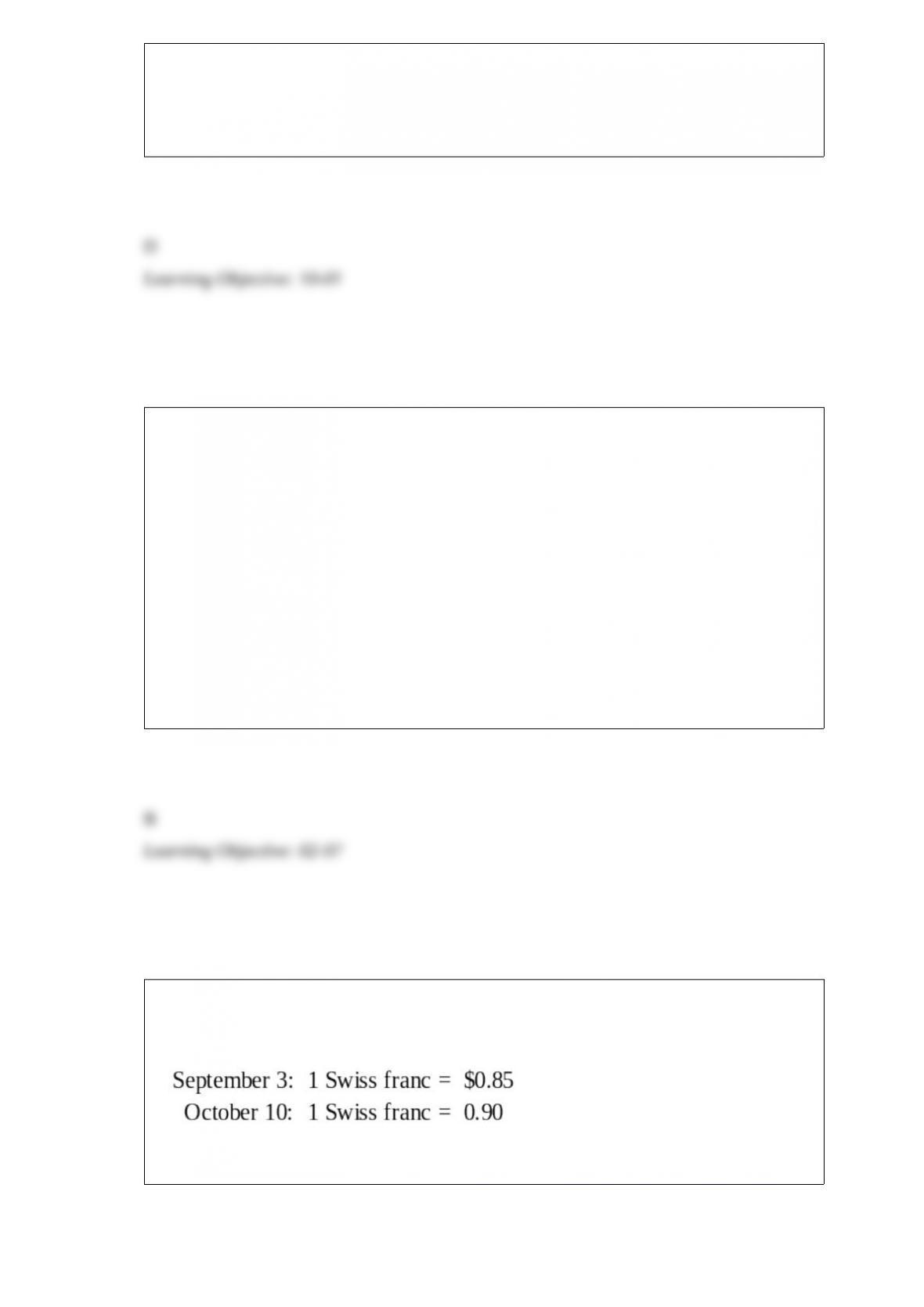

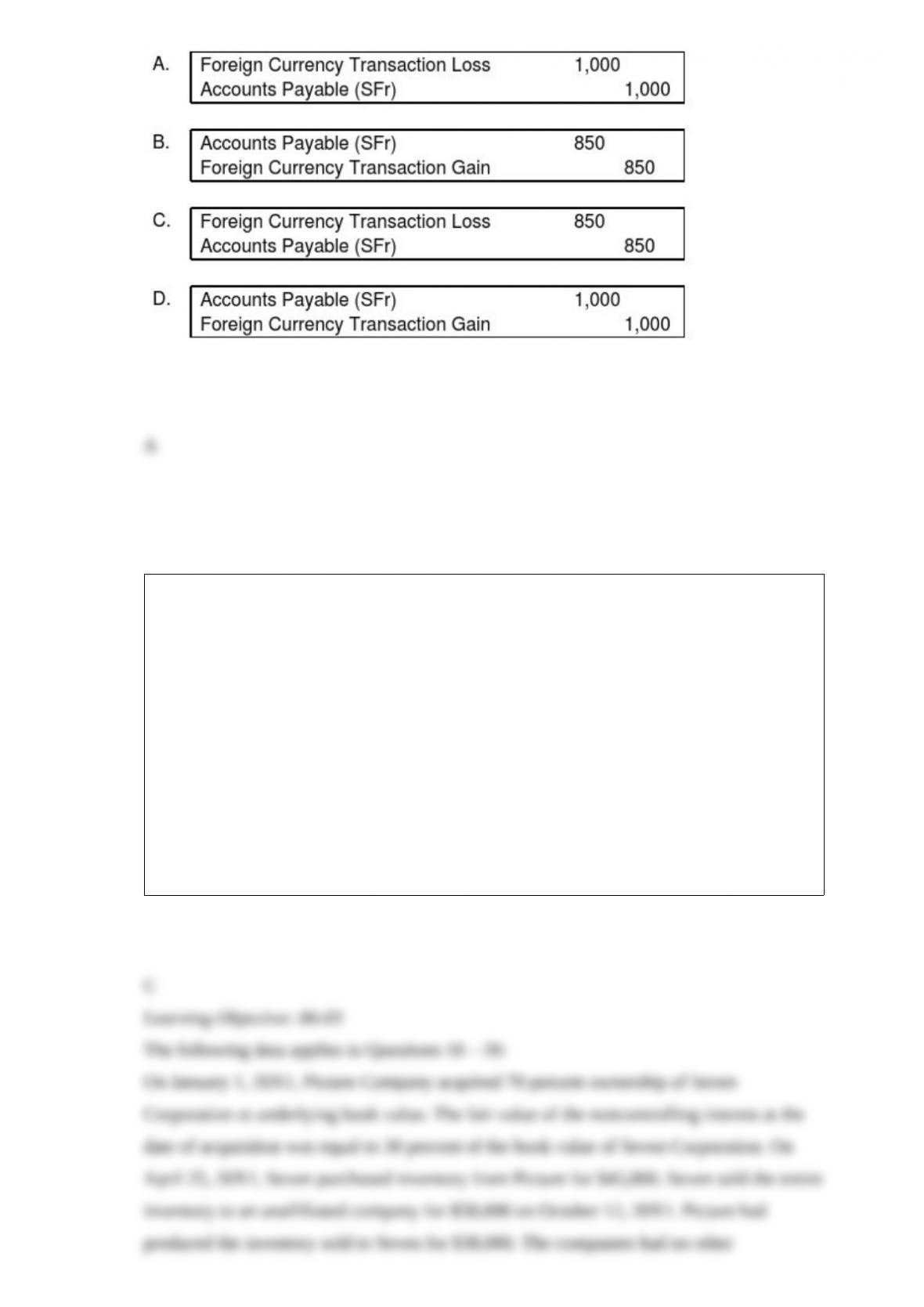

On September 3, 20X8, Jackson Corporation purchases goods for a U.S. dollar

equivalent of $17,000 from a Swiss company. The transaction is denominated in Swiss

francs (SFr). The payment is made on October 10. The exchange rates were:

What entry is required to revalue foreign currency payable to U.S. dollar equivalent

value on October 10?

On January 1, 20X8, Parent Company acquired 90 percent ownership of Subsidiary

Corporation, at underlying book value. The fair value of the noncontrolling interest at

the date of acquisition was equal to 10 percent of the book value of Subsidiary

Corporation. On Mar 17, 20X8, Subsidiary purchased inventory from Parent for

$90,000. Subsidiary sold the entire inventory to an unaffiliated company for $120,000

on November 21, 20X8. Parent had produced the inventory sold to Subsidiary for

$62,000. The companies had no other transactions during 20X8.

Based on the information given above, what amount of consolidated net income will be

assigned to the controlling shareholders for 20X8?

A. $58,000

B. $59,000

C. $55,000

D. $52,200

In which of the following cases would consolidation be inappropriate?

A. The subsidiary is in bankruptcy.

B. Subsidiary’s operations are dissimilar from those of the parent.

C. The parent owns 90 percent of the subsidiary’s common stock, but all of the

subsidiary’s nonvoting preferred stock is held by a single investor.

D. Subsidiary is foreign.

Which of the following accounts is not maintained for each partner in its accounting

records?

A. Capital account

B. Drawing account

C. Earnings account

D. Loan account

Good Faith Hospital, operated by a religious organization, billed patients $4,000,000

for services rendered during the year ended June 30, 20X9. The hospital realized cash

of $3,500,000 from the patient billings because of the following reductions:

(1) contractual adjustments of $140,000 granted to private insurance companies and to

the federal government; and

(2) uncollectible accounts receivable of $360,000.

On the statement of operations prepared for the year ended June 30, 20X9, Good Faith

Hospital should report net patient service revenue of:

A. $3,500,000.

B. $3,860,000.

C. $4,000,000.

D. $3,640,000.

The fair value of net identifiable assets of a reporting unit of Y Company is $270,000.

The carrying value of the reporting unit’s net assets on Y Company’s books is $320,000,

including $50,000 goodwill. If the reported goodwill impairment for the unit is

$10,000, what would be the fair value of the reporting unit?

A. $320,000

B. $310,000

C. $270,000

D. $290,000

Pilfer Company acquired 90 percent ownership of Scrooge Corporation in 20X7, at

underlying book value. On that date, the fair value of noncontrolling interest was equal

to 10 percent of the book value of Scrooge Corporation. Pilfer purchased inventory

from Scrooge for $90,000 on August 20, 20X8, and resold 70 percent of the inventory

to unaffiliated companies on December 1, 20X8, for $100,000. Scrooge produced the

inventory sold to Pilfer for $67,000. The companies had no other transactions during

20X8.

Based on the information given above, what amount of consolidated net income will be

assigned to the controlling interest for 20X8?

A. $51,490

B. $53,100

C. $37,000

D. $20,100

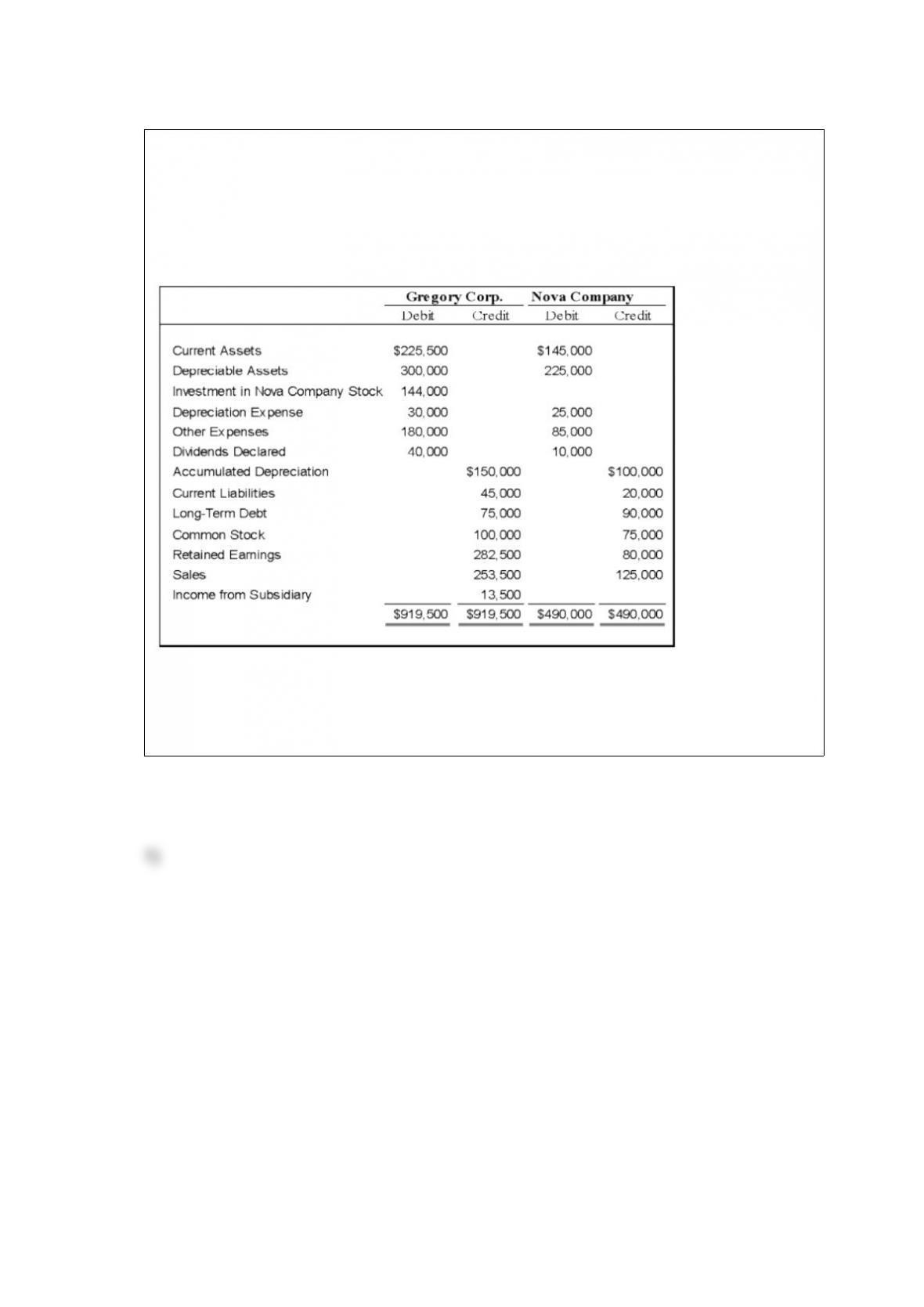

On January 1, 20X8, Gregory Corporation acquired 90 percent of Nova Company’s

voting stock, at underlying book value. The fair value of the noncontrolling interest was

equal to 10 percent of the book value of Nova at that date. Gregory uses the equity

method in accounting for its ownership of Nova. On December 31, 20X9, the trial

balances of the two companies are as follows:

Required:

1) Give all consolidating entries required on December 31, 20X8, to prepare

consolidated financial statements.

2) Prepare a three-part consolidation worksheet as of December 31, 20X8.

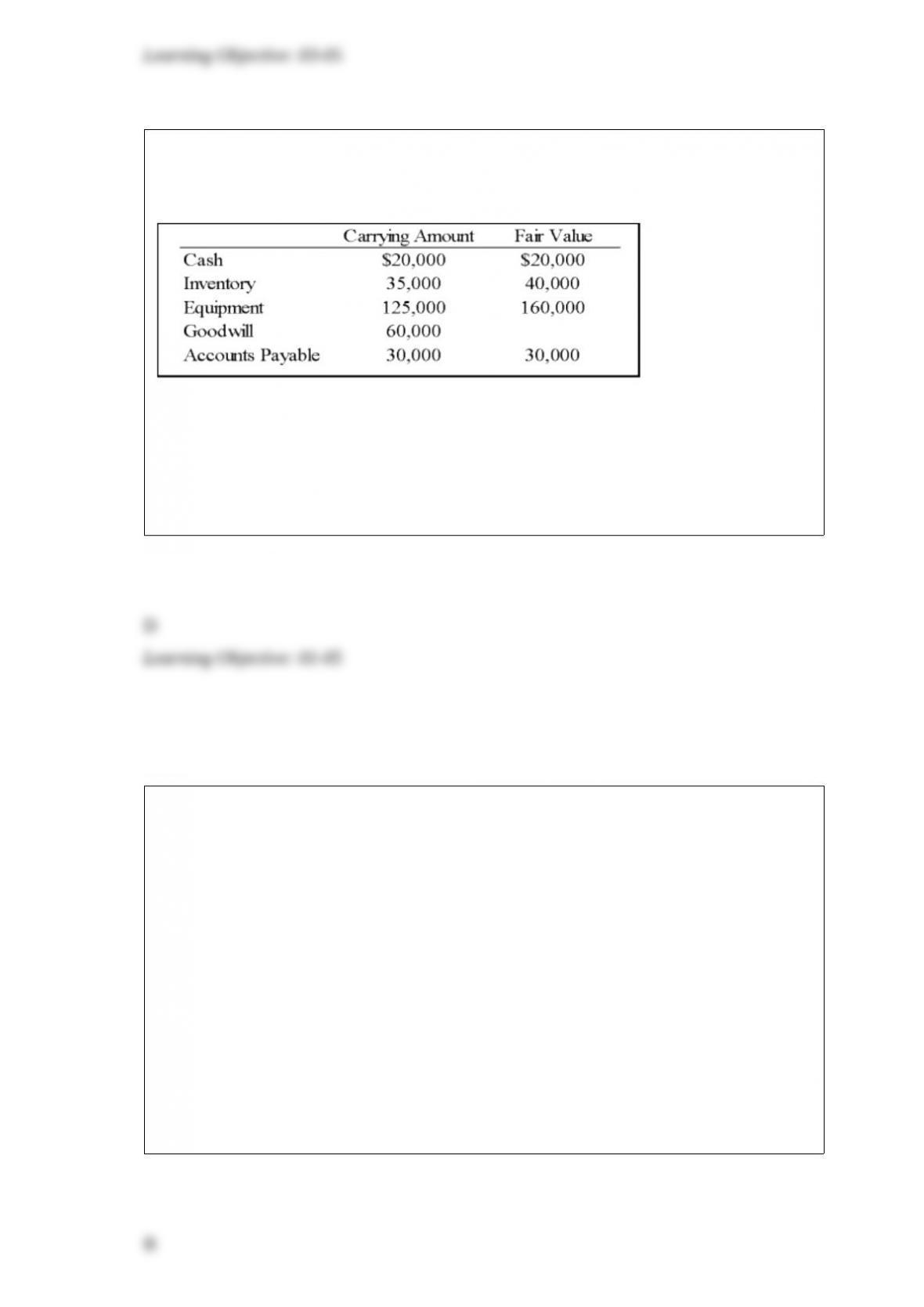

Following its acquisition of the net assets of Dan Company, Empire Company assigned

goodwill of $60,000 to one of the reporting divisions. Information for this division

follows:

Based on the preceding information, what amount of goodwill (after any impairment)

will be reported for this division if its fair value is determined to be $200,000?

A. $0

B. $60,000

C. $30,000

D. $10,000

Winter Corporation’s consolidated cash flow statement for the year ended December

31, 20X2, reported operating cash inflows of $100,000, financing cash inflows of

$30,000, investing cash outflows of $120,000, and an ending cash balance of $50,000.

Winter acquired 60 percent of Snowboard Company’s common stock on April 1, 20X0

at book value. At that date, the fair value of the noncontrolling interest was equal to 40

percent of Snowboard’s book value. Snowboard reported net income of $30,000, paid

dividends of $20,000 in 20X2, and is included in Winter’s consolidated statements.

Winter paid dividends of $40,000 in 20X2. The indirect method is used in computing

cash flows from operations.

Based on the information provided, what amount was reported as dividends paid in the

cash flow from financing activities section of the consolidated statement of cash flows?

A. $60,000

B. $48,000

C. $40,000

D. $20,000

On December 31, 20X8, Melkor Corporation acquired 80 percent of Sydney Company’s

common stock for $160,000. At that date, the fair value of the noncontrolling interest

was $40,000. Of the $75,000 differential, $10,000 related to the increased value of

Sydney’s inventory, $20,000 related to the increased value of its land, and $25,000

related to the increased value of its equipment that had a remaining life of 10 years

from the date of combination. Sydney sold all inventory it held at the end of 20X8

during 20X9. The land to which the differential related was also sold during 20X9 for a

large gain. At the date of combination, Sydney reported retained earnings of $75,000

and common stock outstanding of $50,000. In 20X9, Sydney reported net income of

$60,000, but paid no dividends. Melkor accounts for its investment in Sydney using the

equity method.

Based on the preceding information, what is the amount of write-off of differential

associated with this acquisition recorded by Melkor during 20X9?

A. $0

B. $32,500

C. $26,000

D. $20,000

When a new partner is admitted into a partnership and the new partner receives a capital

credit less than the tangible assets contributed, which of the following explains the

difference?

I. The new partner’s goodwill has been recognized.

II. The old partners received a bonus from the new partner.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Regulation D of the SEC presents important exemptions from full registration

requirements for:

A. private placements.

B. issuances of securities by savings and loan associations.

C. issuances of securities by common carriers regulated by the Interstate Commerce

Commission.

D. foreign companies.

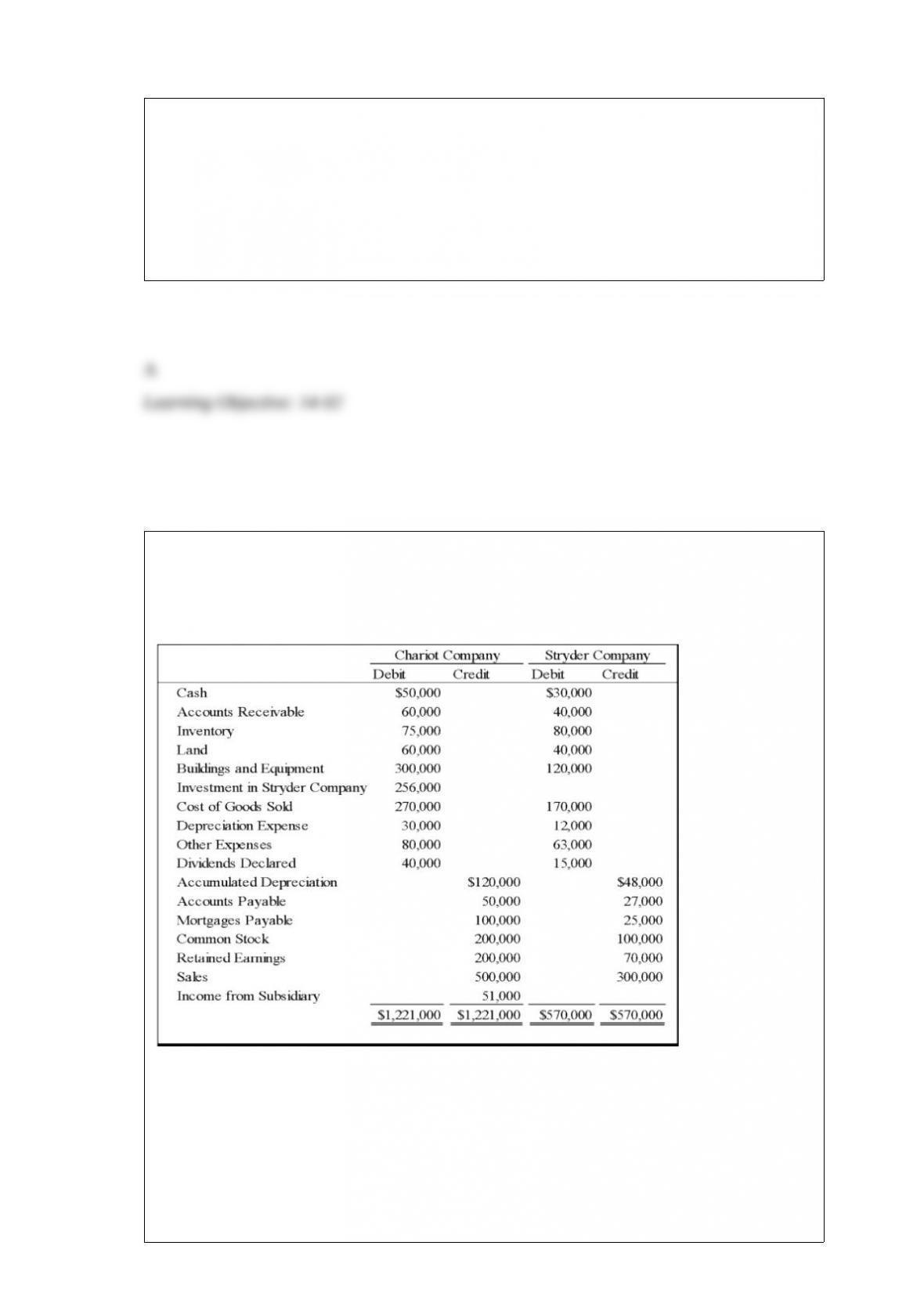

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder’s depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, what amount of net income will be reported in the

consolidated financial statements for the year?

A. $226,000

B. $55,000

C. $230,000

D. $171,000

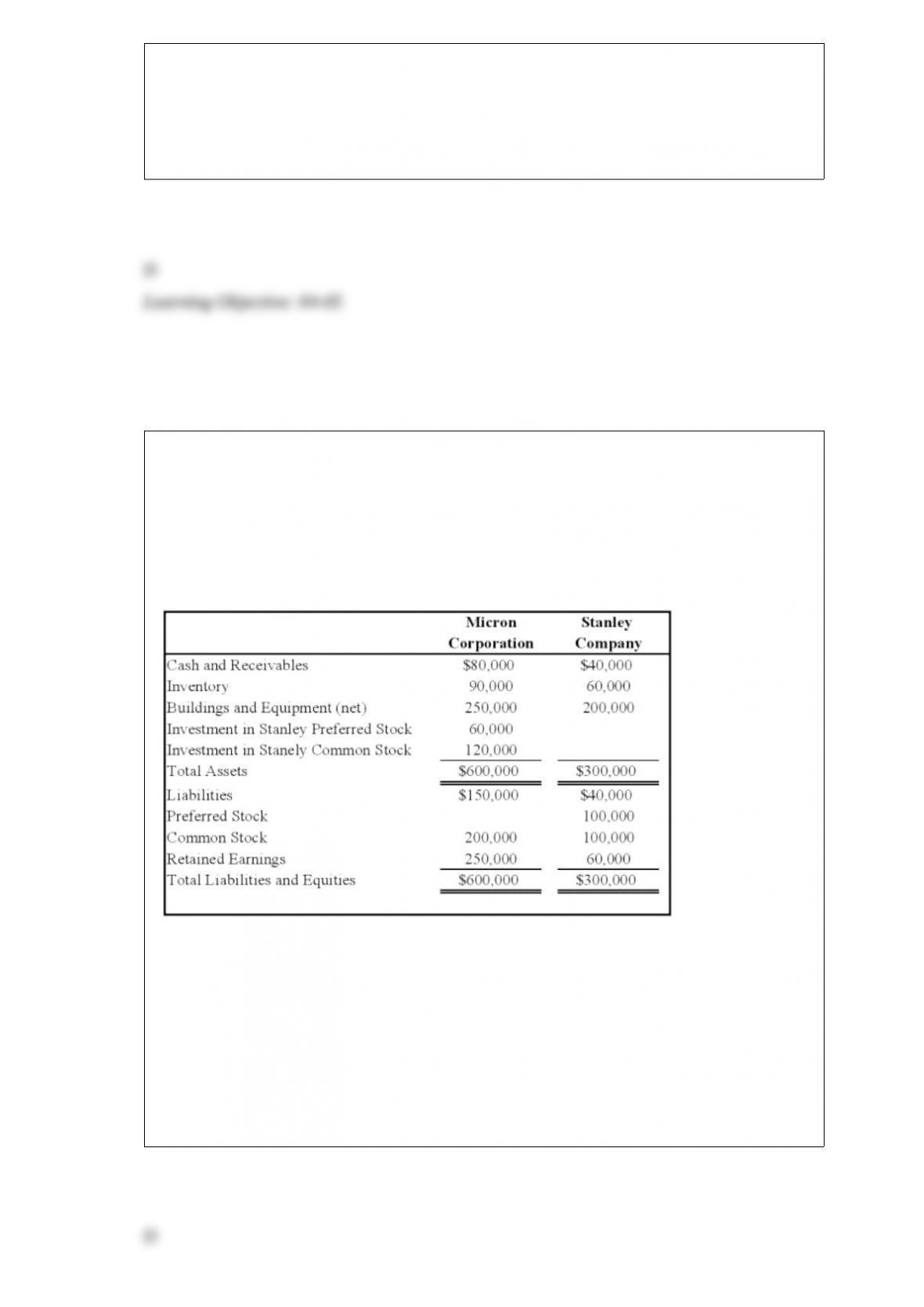

Micron Corporation owns 75 percent of the common shares and 60 percent of the

preferred shares of Stanley Company, all acquired at underlying book value on January

1, 20X8. At that date, the fair value of the noncontrolling interest in Stanley’s common

stock was equal to 25 percent of the book value of its common stock. The balance

sheets of Micron and Stanley immediately after the acquisition contained these

balances:

Stanley’s preferred stock pays a 12 percent dividend and is cumulative. For 20X8,

Stanley reports net income of $40,000 and pays no dividends. Micron reports income

from its separate operations of $75,000 and pays dividends of $30,000 during 20X8.

Based on the preceding information, what amount of income is attributable to the

controlling interest in the consolidated income statement for 20X8?

A. $75,000

B. $105,000

C. $96,000

D. $103,200

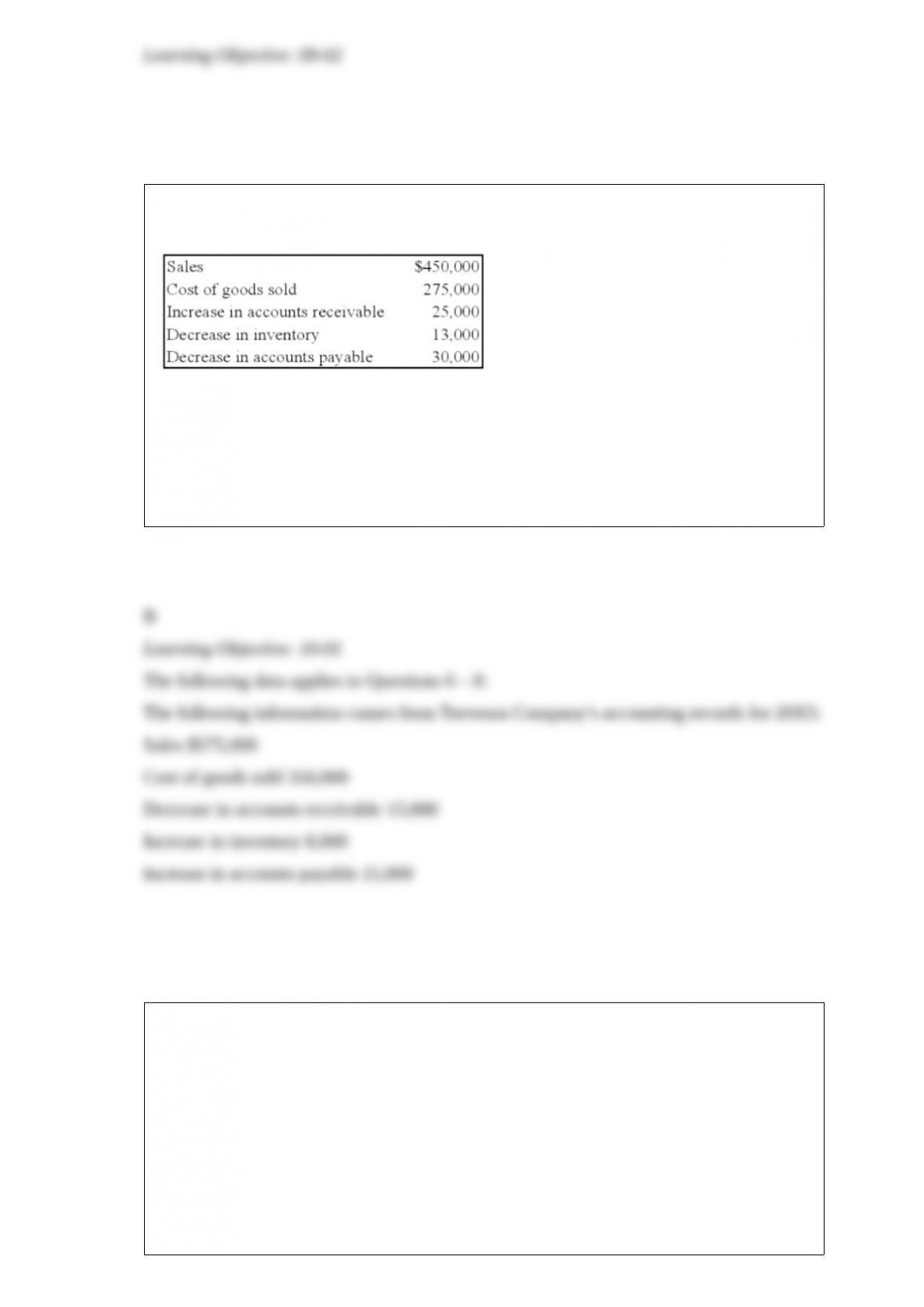

Sigma Company develops and markets organic food products to natural foods retailers.

The following information is available for the company for the year 20X8:

Based on the preceding information, what amount will be reported by the company as

cash flows from operating activities for 20X8?

A. $175,000

B. $133,000

C. $167,000

D. $207,000

Sun Corporation owns 60 percent of Moon Company’s voting shares. On January 1,

20X4, Moon sold bonds with a par value of $400,000 when the market rate was 6

percent. Sun purchased one-third of the bonds; the remainder was sold to nonaffiliates.

The bonds mature in 15 years and pay an annual interest rate of 5 percent. Interest is

paid semiannually on June 30 and December 31.

Based on the information given above, what amount of interest expense should be

reported in the 20X5 consolidated income statement?

A. $0

B. $14,448

C. $14,516

D. $21,775

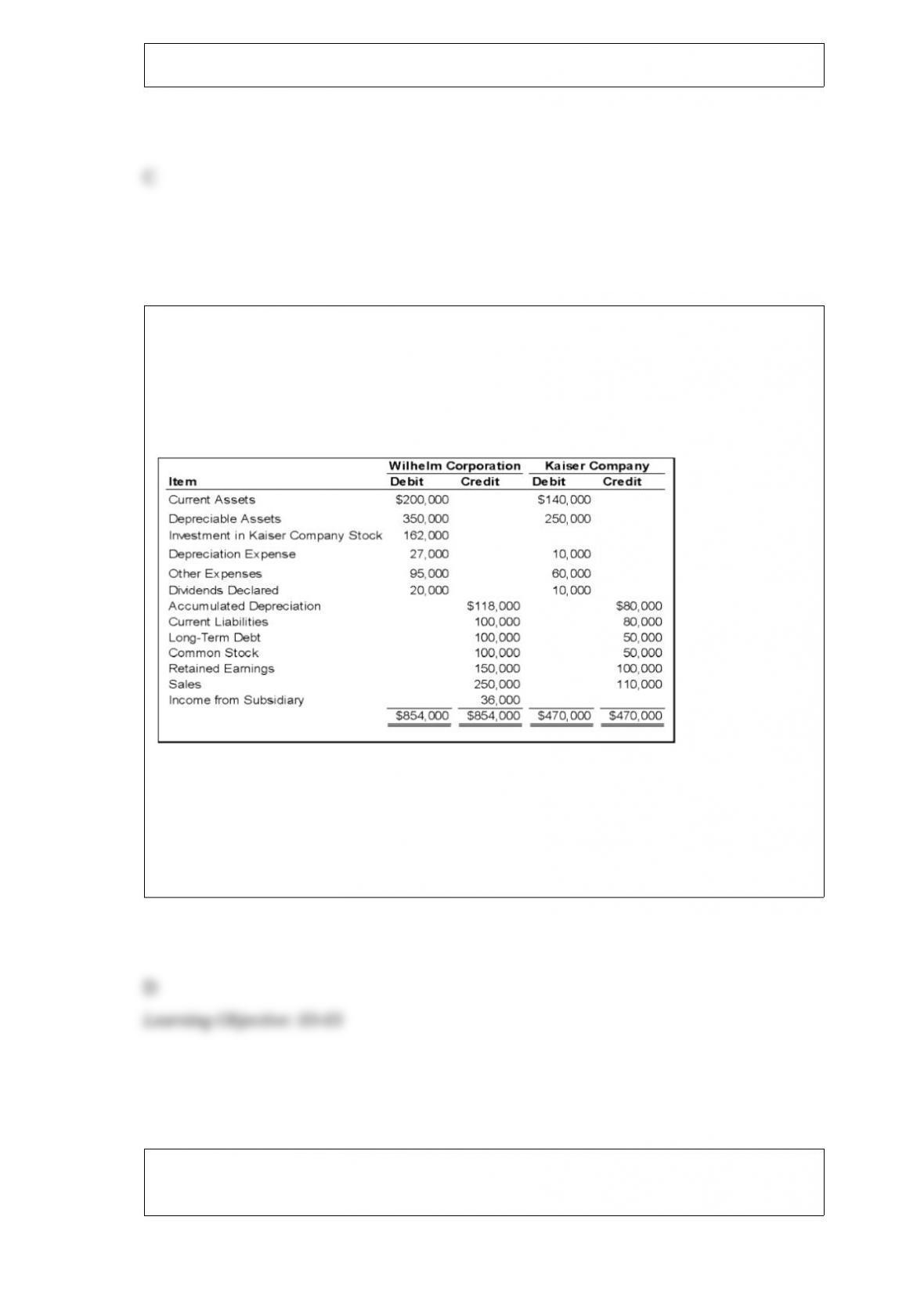

On January 1, 20X8, Wilhelm Corporation acquired 90 percent of Kaiser Company’s

voting stock, at underlying book value. The fair value of the noncontrolling interest was

equal to 10 percent of the book value of Kaiser at that date. Wilhelm uses the equity

method in accounting for its ownership of Kaiser. On December 31, 20X9, the trial

balances of the two companies are as follows:

Based on the preceding information, what amount would be reported as noncontrolling

interest in the consolidated balance sheet at December 31, 20X9?

A. $27,000

B. $4,000

C. $15,000

D. $18,000

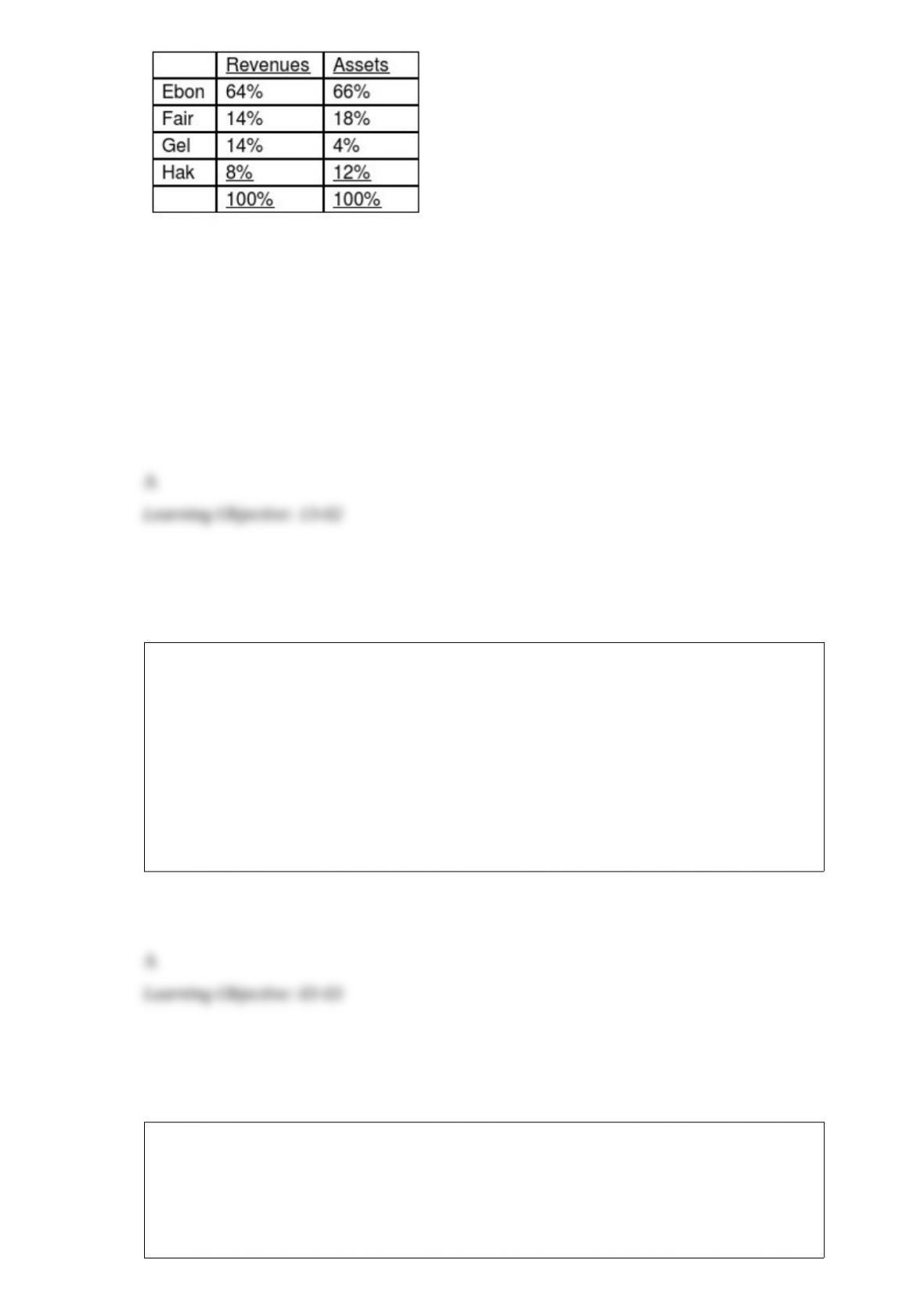

Cott Co.’s four business segments have revenues and identifiable assets expressed as

percentages of Cott’s total revenues and total assets as follows:

Which of these business segments are deemed to be reportable segments?

A. Ebon, Fair, Gel, and Hak

B. Ebon only

C. Ebon and Fair only

D. Ebon, Fair, and Gel only

On January 1, 20X8, Zeta Company acquired 85 percent of Theta Company’s common

stock for $100,000 cash. The fair value of the noncontrolling interest was determined to

be 15 percent of the book value of Theta at that date. What portion of the retained

earnings reported in the consolidated balance sheet prepared immediately after the

business combination is assigned to the noncontrolling interest?

A. None

B. 15 percent

C. 100 percent

D. Cannot be determined

The Securities Exchange Act of 1934 requires publicly held companies to file periodic

financial disclosures as updates of their economic activity. The three basic forms used

for this updating are Form 10-K, Form 10-Q, and Form 8-K.

Required:

Describe the information contained in each of the three basic forms noted above.

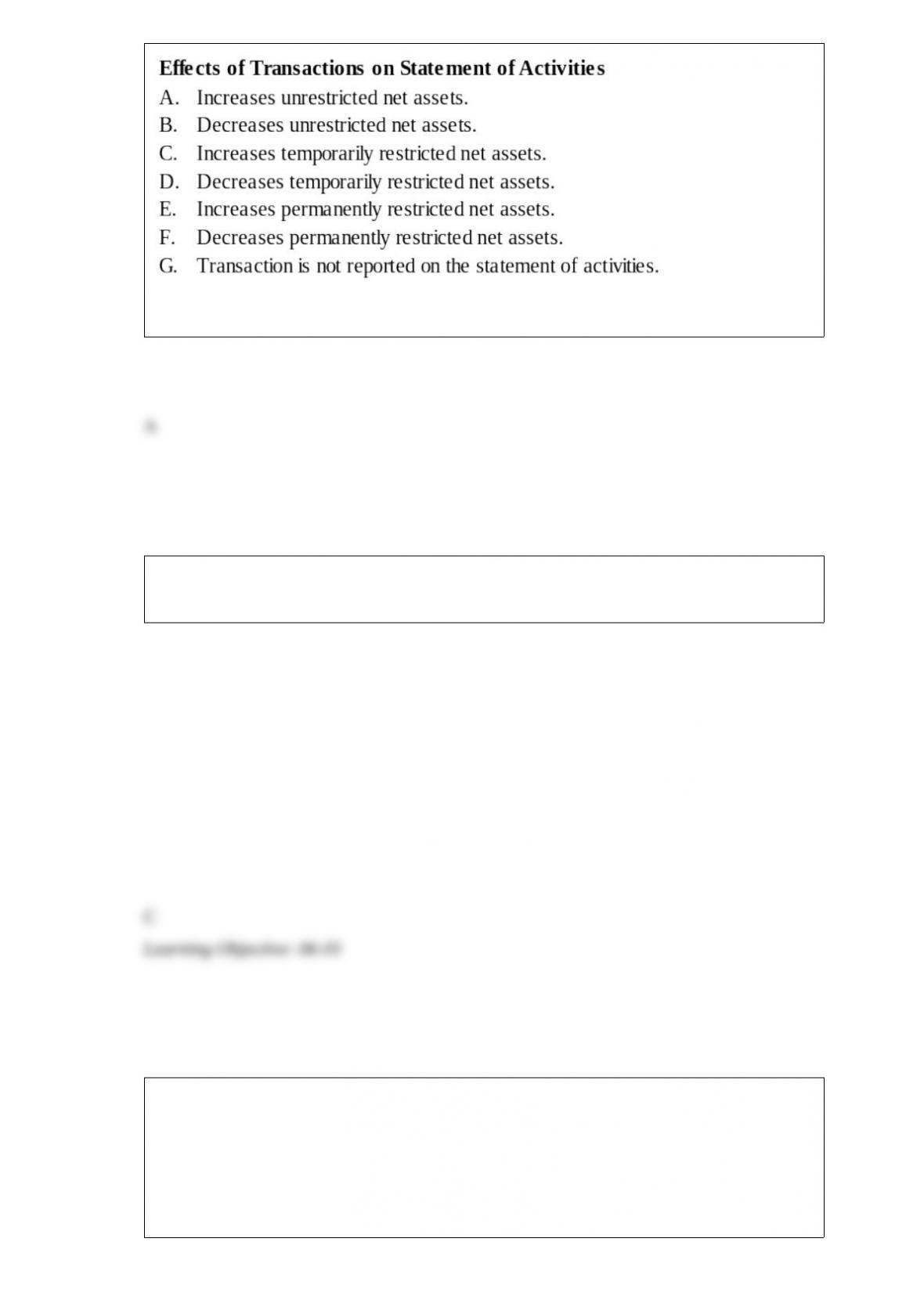

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Received pledges from donors who placed no time or use restrictions on how the

pledges were to be spent.

Based on the information given above, what balance will be reported for inventory in

the consolidated balance sheet for December 31, 20X3?

A. $8,800

B. $44,286

C. $53,086

D. $73,000

Fisher Company pays its executives a bonus of 4 percent of income before deducting

the bonus and income taxes. For the quarter ended March 31, 20X1, Fisher had income

before the bonus and income tax of $10,000,000. For the year ended December 31,

20X1, Fisher estimates that its income before bonus and income taxes will be

$50,000,000. For the quarter ended March 31, 20X1, what is the amount of the bonus

that Fisher should deduct on its income statement?

A. $100,000

B. $400,000

C. $500,000

D. $2,000,000

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

A gain was realized from the sale of securities which were permanently invested. The

gain is restricted as to use.

The terms of a partnership agreement provide that one of the partners is to receive a

salary allowance of $20,000 plus a bonus of 10 percent of income after deduction of the

bonus and the salary allowance. If income is $130,000, the bonus should be

A. $10,000

B. $11,000

C. $12,222

D. $20,000

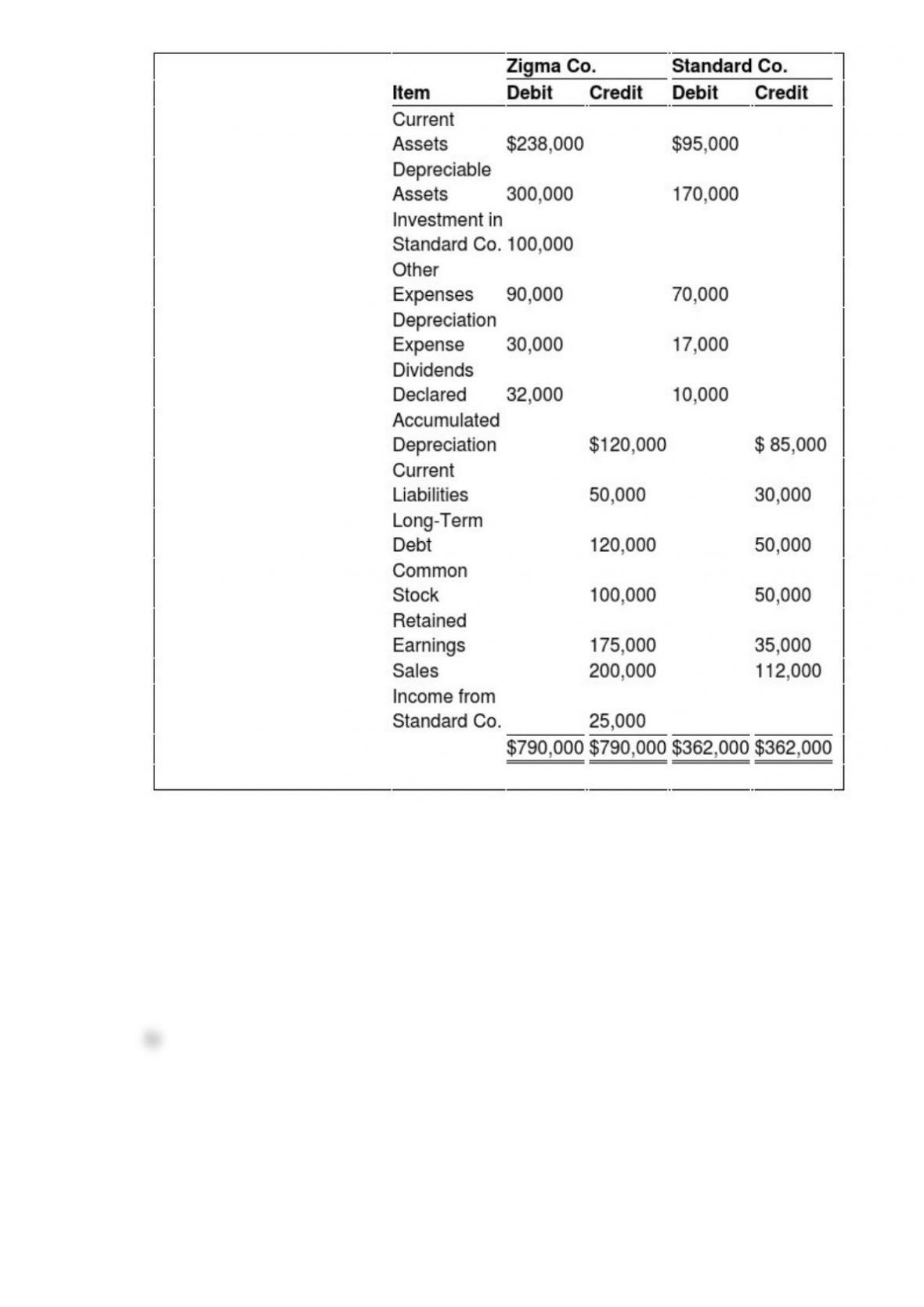

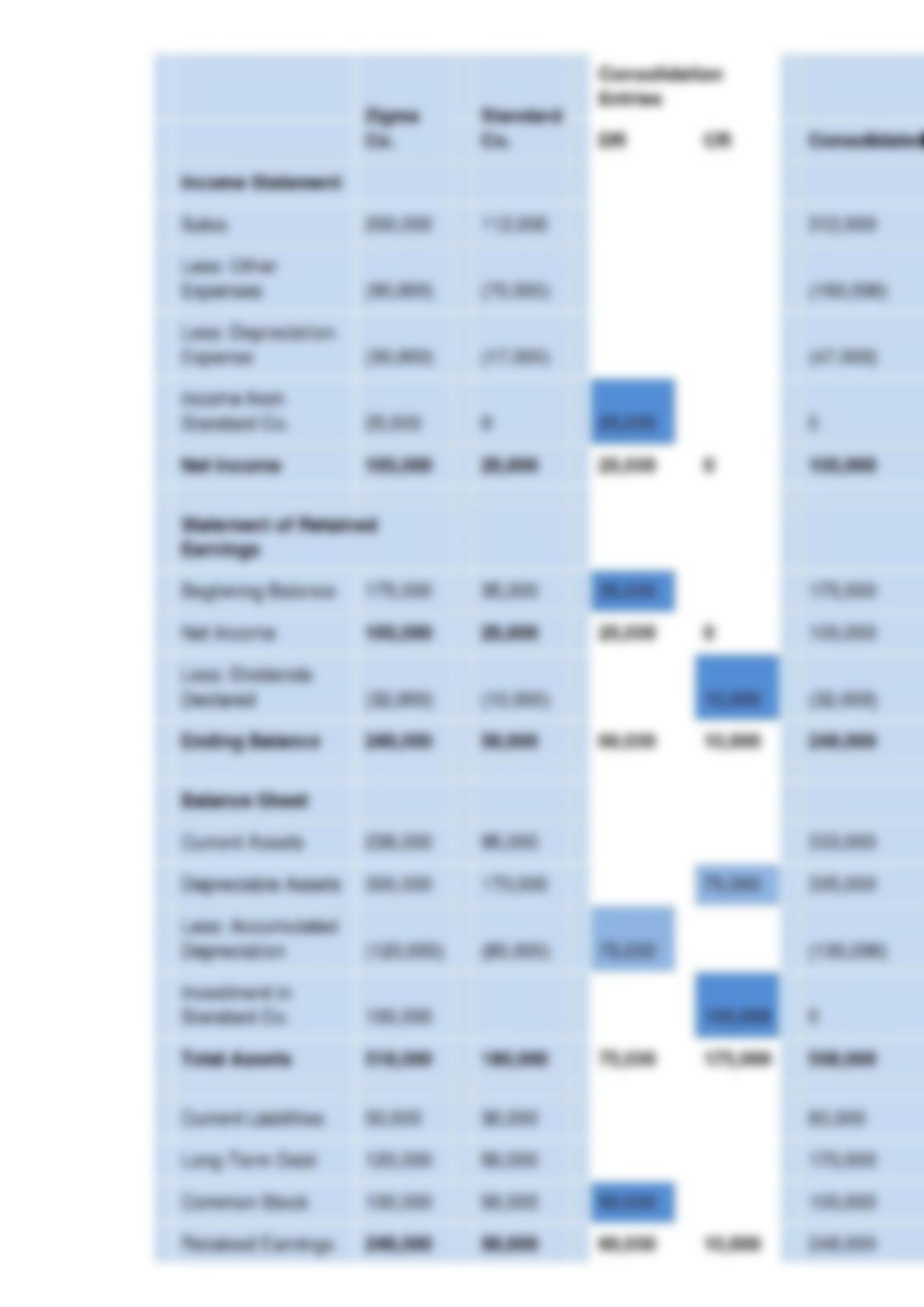

On January 1, 20X9, Zigma Company acquired 100 percent of Standard Company’s

common shares at underlying book value. Zigma uses the equity method in accounting

for its ownership of Standard. On December 31, 20X9, the trial balances of the two

companies are as follows:

Required:

1) Prepare the consolidation entries needed as of December 31, 20X9, to complete a

consolidation worksheet.

2) Prepare a three-part consolidation worksheet as of December 31, 20X9.

Partners David and Goliath have decided to liquidate their business. The following

information is available:

Cash $100,000

Inventory $200,000

$300,000

Accounts Payable $80,000

David, Capital $140,000

Goliath, Capital $80,000

$300,000

David and Goliath share profits and losses in a 3:1 ratio, respectively. During the first

month of liquidation, half the inventory is sold for $70,000, and $50,000 of the

accounts payable are paid. During the second month, the rest of the inventory is sold for

$55,000, and the remaining accounts payable are paid. Cash is distributed at the end of

each month, and the liquidation is completed at the end of the second month.

Refer to the information provided above. Using a safe payment schedule, how much

cash will be distributed to David at the end of the first month?

A. $22,500

B. $42,500

C. $75,000

D. $117,500

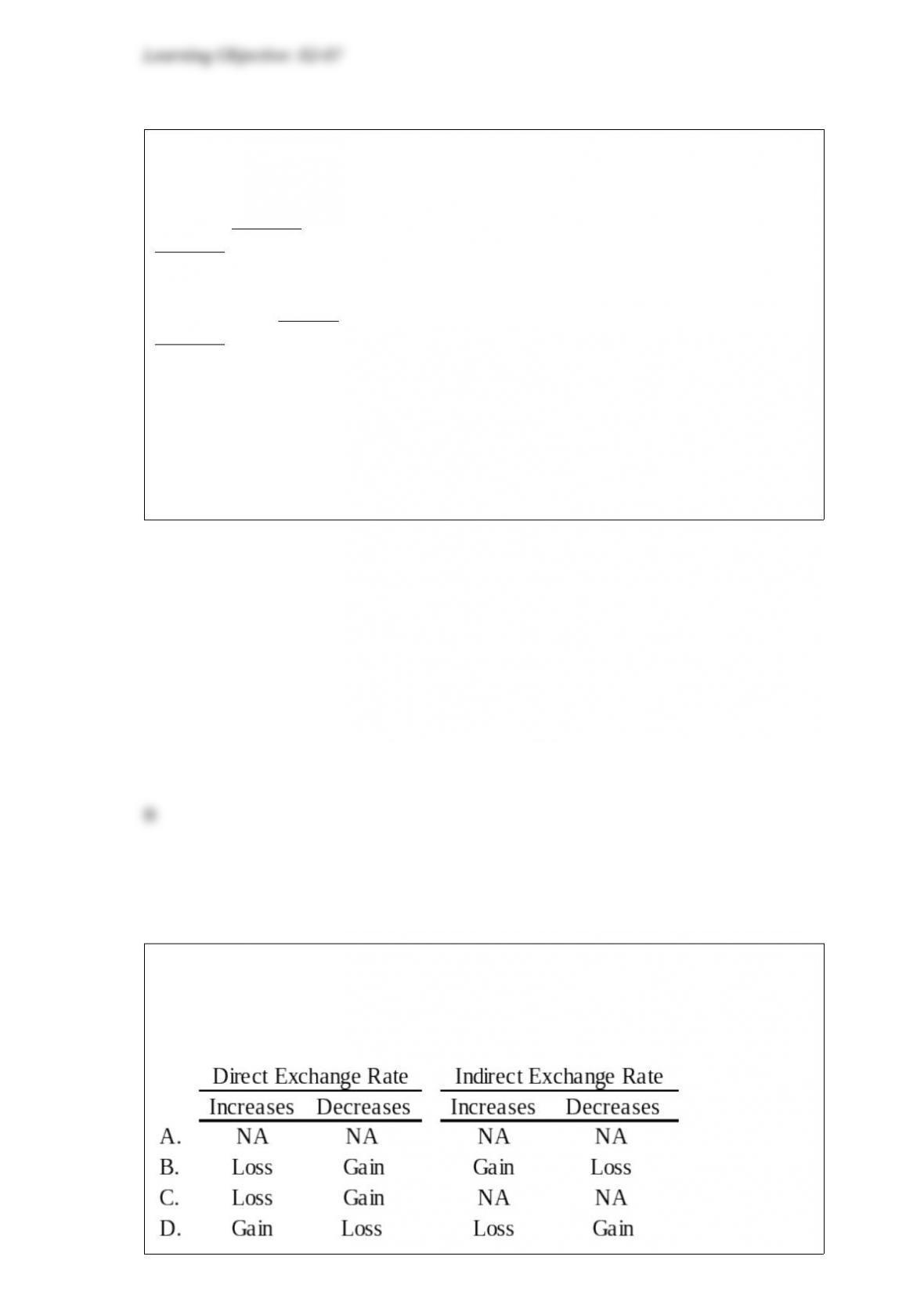

Chicago based Corporation X has a number of importing transactions with companies

based in UK. Importing activities result in payables. If the settlement currency is the

British Pound, which of the following will happen by changes in the direct or indirect

exchange rates?

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. What amount will Erin have to invest to give

her a one-fourth interest in the capital of the partnership if no goodwill or bonus is

recorded?

A. $45,000

B. $50,000

C. $60,000

D. $66,000

Windsor Corporation acquired 90 percent of Agro Corporation’s common shares on

January 1, 20X6, at underlying book value.

In reading a set of consolidated financial statements you are surprised to see the term

noncontrolling interest not reported under the Liability section of the Balance Sheet.

Required:

a. What is a non-controlling interest?

b. Why must it be reported in the financial statements as an element of equity rather

than a liability?

Apple and Betty are planning on beginning a new business. They plan on forming a

partnership. Apple will contribute $300,000 and will not be working. Betty will be

working full time. They plan on splitting profits equally. They approach you, as an

accounting major, to confirm their thoughts. What do you recommend?

Tuttle Company discloses supplementary operating segment information for its three

reportable segments. Data for 20X3 are available as follows:

Segment A Segment B Segment C

Sales $500,000 $300,000 $200,000

Traceable operating expenses 250,000 120,000 90,000

Allocable costs for the year were $54,000. Allocable costs are assigned based on the

ratio of a segment’s income before allocable costs to total income before allocable

costs. The 20X3 operating profit for Segment A was

A. $196,000

B. $223,000

C. $225,000

D. $250,000

Based on the information given above, what amount of cost of goods must be

eliminated from the consolidated income statement for 20X5?

E. $3,596,000

F. $3,379,000

G. $806,000

H. $589,000

Orange Corporation owns 70 percent of the voting common shares of McNichols

Corporation, purchased at book value. Noncontrolling interest was assigned $21,000 of

income in the 20X0 consolidated income statement. What amount of net income did

McNichols Corporation report for the year?

A. $70,000

B. $63,000

C. $30,000

D. $147,000