Wally Corporation acquired 70 percent of the common shares and 60 percent of the

preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At

that date, the fair value of the noncontrolling interest in Safety’s common stock was

equal to 30 percent of the book value of its common stock. Safety’s balance sheet at the

time of acquisition contained the following balances:

Assets $700,000 Liabilities $110,000

Preferred Stock 100,000

Common Stock 200,000

Retained Earnings 290,000

Total Assets $700,000 Total Liabilities and Equities $700,000

The preferred shares are cumulative and have an 8 percent annual dividend rate and are

three years in arrears on January 1, 20X6. All of the $10 par value preferred shares are

callable at $12 per share. During 20X6, Safety reported net income of $80,000 and paid

no dividends.

Based on the information provided, what amount will be reported as the noncontrolling

interest in the consolidated balance sheet on January 1, 20X6?

A. $133,800

B. $191,400

C. $204,600

D. $210,000

Jupiter Corporation’s consolidated cash flow statement for the year ended December 31,

20X8, reported operating cash inflows of $160,000, financing cash outflows of

$90,000, and investing cash outflows $55,000, and an ending cash balance of $75,000.

Jupiter acquired 75 percent of Ganymede Company’s common stock on July 1, 20X6, at

book value. At that date, the fair value of the noncontrolling interest was equal to 25

percent of Ganymede Company’s book value. Ganymede reported net income of

$20,000, paid dividends of $8,000 in 20X8, and is included in Jupiter’s consolidated

statements. Jupiter paid dividends of $25,000 in 20X8. The indirect method is used in

computing cash flow from operations.

Based on the information provided, what amount was reported as dividends paid in the

cash flow from financing activities section of the consolidated statement of cash flows?

A. $25,000

B. $33,000

C. $27,000

D. $8,000

On October 15, 20X8, an enterprise fund of Blacksburg purchased office supplies at a

cost of $10,000. The inventory of office supplies on hand at the June 30, 20X9, fiscal

year end was $4,000. There was no beginning inventory. Blacksburg should make

entries that include:

A. debiting Supplies $10,000 at October 15, and debiting Expenses $4,000 on June 30.

B. debiting Expenditures $10,000 at October 15, and debiting Supplies $4,000 at June

30.

C. debiting Supplies $10,000 at October 15, and crediting Supplies $6,000 on June 30.

D. debiting Expenditures $10,000 at October 15, and crediting Expenses $4,000 at June

30.

On January 1, 20X7, Servant Company purchased a machine with an expected

economic life of five years. On January 1, 20X9, Servant sold the machine to Master

Corporation and recorded the following entry:

Master Corporation holds 75 percent of Servant’s voting shares. Servant reported net

income of $50,000, and Master reported income from its own operations of $100,000 for

20X9. There is no change in the estimated economic life of the equipment as a result of the

intercorporate transfer.

Based on the preceding information, in the preparation of the 20X9 consolidated balance

sheet, machine will be:

A. debited for $1,000.

B. debited for $15,000.

C. credited for $45,000.

D. debited for $25,000.

Big Company acquired the following assets and liabilities of Little Company (fair

values listed below) for $470,000 cash.

Inventory $ 70,000

Land 100,000

Buildings and Equipment 320,000

Current Liabilities 50,000

Assuming these items are all recorded at their acquisition date fair values, what

additional item needs to be recorded and how will it be accounted for in the future?

A. $30,000 Goodwill, capitalized and tested for impairment

B. $30,000 Bargain purchase, recognized in current earnings

C. $30,000 Bargain purchase, capitalized and recognized over time

D. $30,000 Goodwill, capitalized and amortized over time

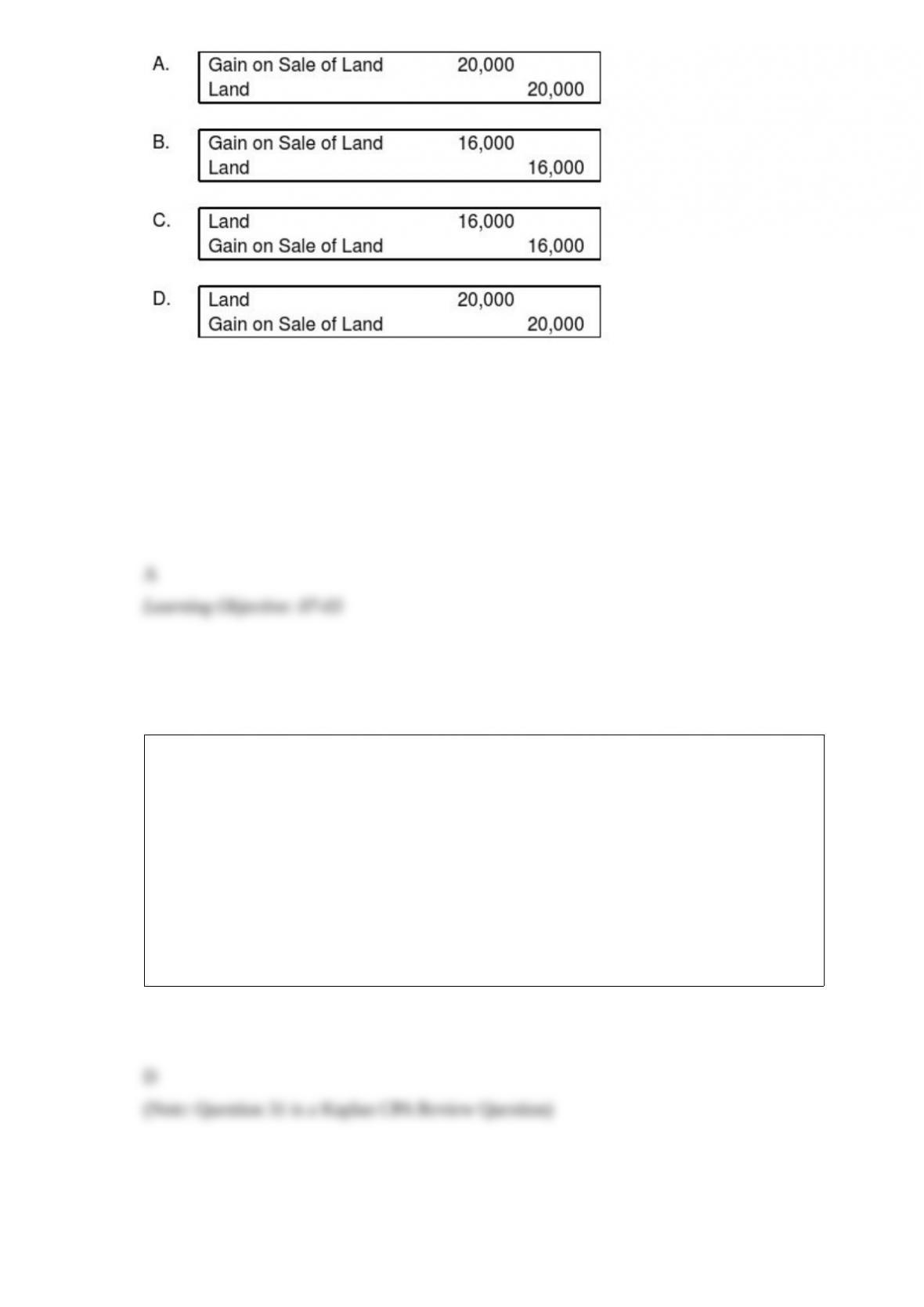

ABC Corporation purchased land on January 1, 20X6, for $50,000. On July 15, 20X8,

it sold the land to its subsidiary, XYZ Corporation, for $70,000. ABC owns 80 percent

of XYZ’s voting shares.

Based on the preceding information, what will be the worksheet consolidating entry to

remove the effects of the intercompany sale of land in preparing the consolidated

financial statements for 20X8?

A. Option A

B. Option B

C. Option C

D. Option D

On November 6, 20X7, Zucor Corp. purchased merchandise from an unaffiliated

foreign company for 50,000 units of the foreign company’s local currency. On that date,

the spot rate was $1.259. Zucor paid the bill in full three months later when the spot rate

was $1.258. The spot rate was $1.255 on December 31, 20X7. What amount should

Zucor report as a foreign currency transaction gain in its income statement for the year

ended December 31, 20X7?

A. $0

B. $50

C. $150

D. $200

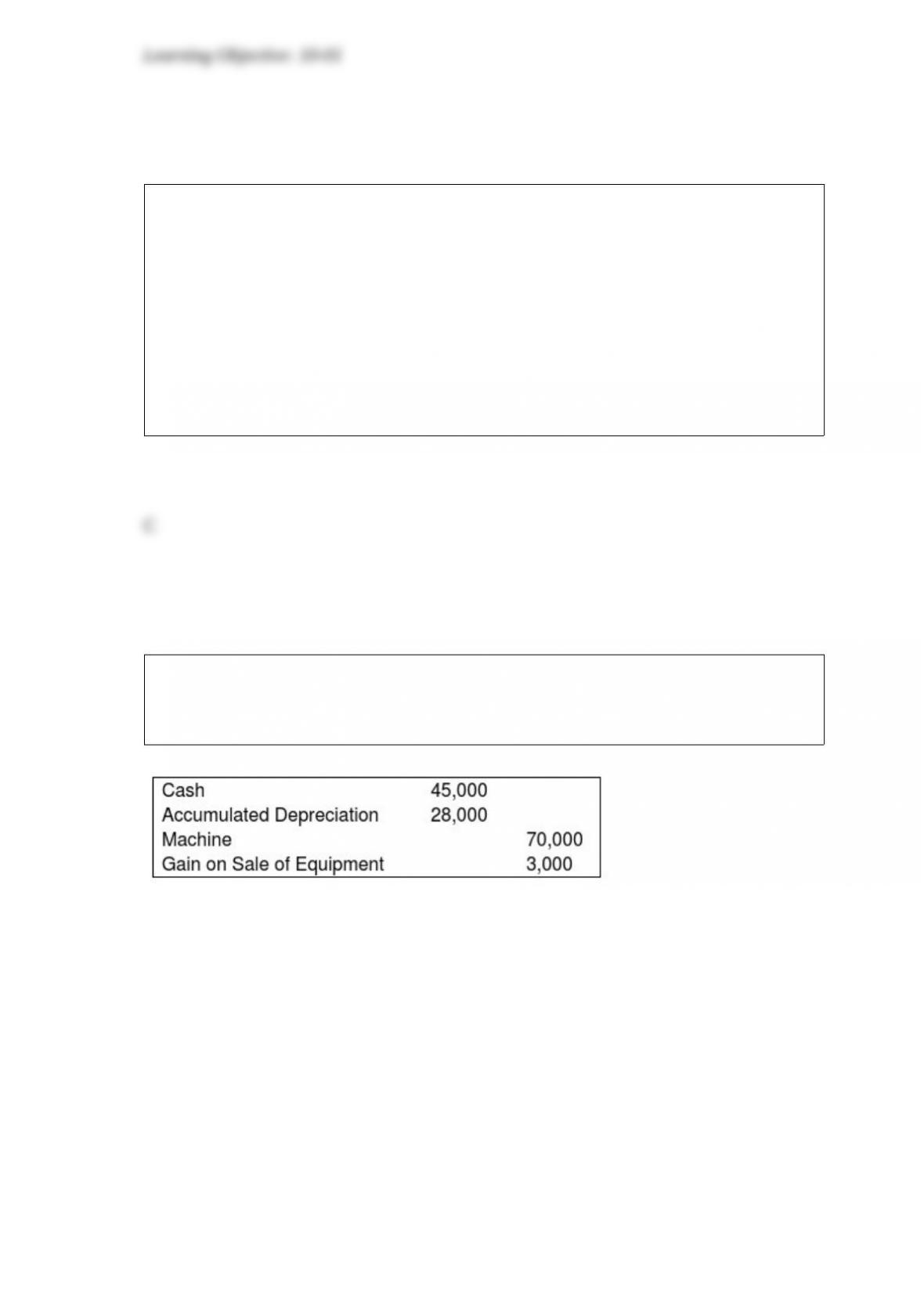

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite

for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment

is expected to have a 10-year useful life and no salvage value. Both companies

depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of consolidation entries related

to the equipment transfer for the 20X9 consolidated financial statements, the net effect

on accumulated depreciation will be:

A. a decrease of $160,000.

B. an increase of $160,000.

C. an increase of $135,000.

D. a decrease of $135,000.

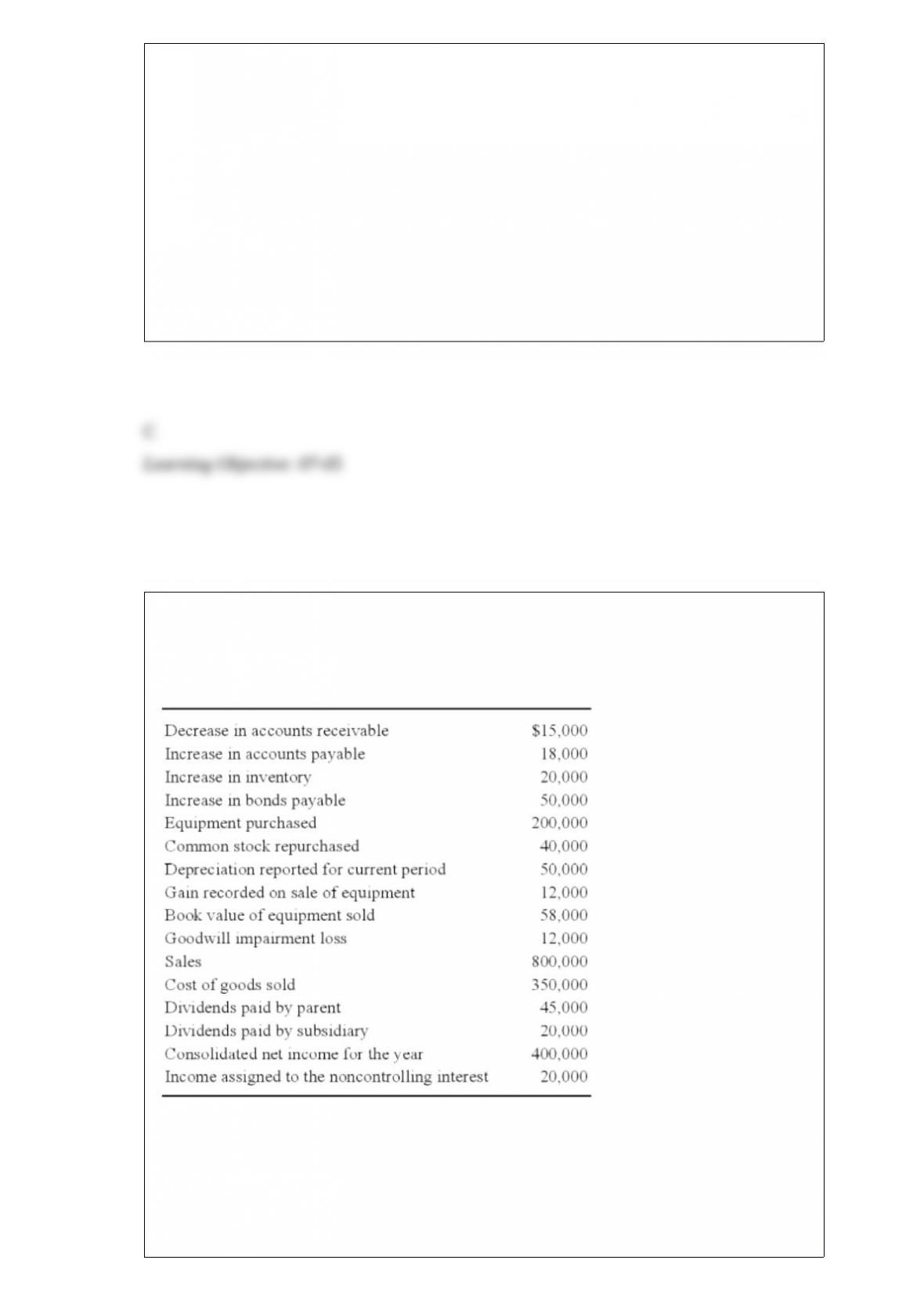

New Life Corporation has just finished preparing a consolidated balance sheet, income

statement, and statement of changes in retained earnings for 20X9. The following items

are proposed for inclusion in the consolidated cash flow statement:

New Life holds 75 percent of the voting stock of Shane Pharmaceuticals, acquired at

book value on June 21, 20X6. On the date of the acquisition, the fair value of the

noncontrolling interest was equal to 25 percent of the book value of Shane.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash used in investing activities for 20X9?

A. $200,000

B. $142,000

C. $155,000

D. $130,000

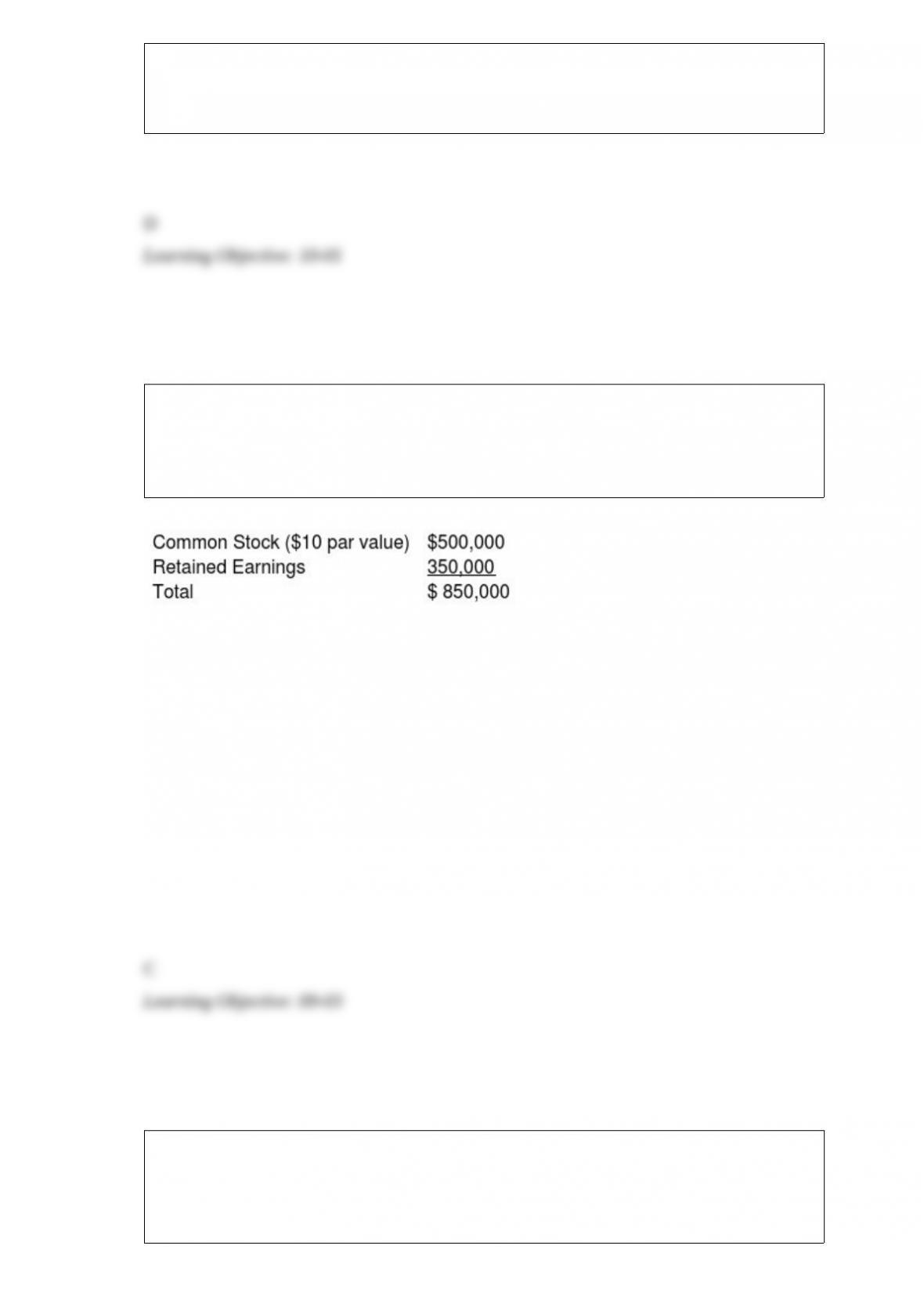

On January 1, 20X7, Pisa Company acquired 80 percent of Siena Company by

purchasing 40,000 shares of Siena’s common stock. There was no differential related to

this transaction. The noncontrolling interest had a fair value equal to 20 percent of book

value. The book value of Siena on December 31, 20X7 was as follows:

On January 1, 20X8, Siena sold an additional 12,500 shares to a nonaffiliate for $25 per

share.

Based on the preceding information, the elimination entry to prepare the consolidated

financial statements on December 31, 20X7 would include a:

A. debit to common stock for $812,500

B. credit to additional paid-in capital for $187,500

C. credit to Investment in Siena Co. for $744,000

D. credit to retained earnings for $350,000

On January 1, 20X8, Ramon Corporation acquired 75 percent of Tester Company’s

voting common stock for $300,000. At the time of the combination, Tester reported

common stock outstanding of $200,000 and retained earnings of $150,000, and the fair

value of the noncontrolling interest was $100,000. The book value of Tester’s net assets

approximated market value except for patents that had a market value of $50,000 more

than their book value. The patents had a remaining economic life of ten years at the date

of the business combination. Tester reported net income of $40,000 and paid dividends

of $10,000 during 20X8.

Based on the preceding information, what balance will Ramon report as its investment

in Tester at December 31, 20X8, assuming Ramon uses the equity method in accounting

for its investment?

A. $318,750

B. $317,500

C. $330,000

D. $326,250

Accountants are liable for any materially false or misleading information contained in

the registration statement filed with the SEC up to:

A. the date the registration statement is filed.

B. the date of the audit report.

C. the effective date of the registration statement.

D. the date securities are sold.

The balance in Newsprint Corp.’s foreign exchange loss account was $10,000 on

December 31, 20X8, before any necessary year-end adjustment relating to the

following:

(1) Newsprint had a $15,000 debit resulting from the restatement in dollars of the

accounts of its wholly owned foreign subsidiary for the year ended December 31, 20X8.

(2) Newsprint had an account payable to an unrelated foreign supplier, payable in the

supplier’s local currency unit (LCU) on January 15, 20X9. The U.S. dollar–equivalent

of the payable was $50,000 on the December 1, 20X8, invoice date and $53,000 on

December 31, 20X8.

Based on the information provided, in Newsprint’s 20X8 consolidated income

statement, what amount should be included as foreign exchange loss in computing net

income, if the LCU is the functional currency and the translation method is appropriate?

A. $28,000

B. $13,000

C. $25,000

D. $8,000

Tinitoys, Inc., a domestic company, purchased inventory from a Brazilian company for

500,000 Brazilian reals (Br. reals) on May 1, 20X2. Payment is due on June 30, 20X2.

On May 1, 20X2, Tinitoys also entered into a 60-day forward contract to purchase

500,000 Brazilian reals. The forward contract is not designated as a hedge. Tinitoys’

fiscal year ends on May 31. The direct exchange rates were as follows:

Spot Rate Forward Rate

May 1, 20X2 $0.523 $0.525 (60 days)

May 31, 20X2 $0.516 $0.52 (30 days)

June 30, 20X2 $0.508

Based on the preceding information, the entries on June 30, 20X2, include a

A. debit to Foreign Currency Transaction Loss, $4,000

B. credit to Foreign Currency Units (Br. reals), $262,500

C. credit to Cash, $262,500.

D. debit to Dollars Payable to Exchange Broker, $254,000

“Preference payments” made by the debtor to one creditor to the detriment of all other

creditors within 90 days before the bankruptcy petition was filed:

A. is reduced from the monies available to the general unsecured creditors.

B. is usually written off.

C. may be recovered and returned to the cash available for all creditors.

D. are not recovered, as management assurances are binding.

Parent Corporation owns 90 percent of Subsidiary 1 Company’s stock and 75 percent of

Subsidiary 2 Company’s stock. During 20X8, Parent sold inventory purchased in 20X7

for $48,000 to Subsidiary 1 for $60,000. Subsidiary 1 then sold the inventory at its cost

of $60,000 to Subsidiary 2. Prior to December 31, 20X8, Subsidiary 2 sold $45,000 of

inventory to a nonaffiliate for $67,000 and held $15,000 in inventory at December 31,

20X8.

Based on the information given above, what amount should be reported in the 20X8

consolidated income statement as cost of goods sold?

A. $36,000

B. $12,000

C. $48,000

D. $45,000

At the end of the year, a parent acquires a wholly owned subsidiary’s bonds from

unaffiliated parties at a cost less than the subsidiary’s carrying value. The consolidated

net income for the year of acquisition should include the parent’s separate operating

income plus:

A. the subsidiary’s net income increased by the gain on constructive retirement of debt.

B. the subsidiary’s net income decreased by the loss on constructive retirement of debt.

C. the subsidiary’s net income increased by the gain on constructive retirement of debt,

and decreased by the subsidiary’s bond interest expense.

D. the subsidiary’s net income decreased by the loss on constructive retirement of debt,

and decreased by the subsidiary’s bond interest expense.

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Billed patients for services rendered.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

22. Simmons Corporation paid $170,000 to acquire all of Bush Company’s net assets.

Bush reported assets with a book value of $189,000 and a fair value of $206,000 and

liabilities with a book value and fair value of $48,000 on the date of the combination.

Simmons also paid $8,000 to a search firm for finder’s fees related to the acquisition.

What amount will be recorded as goodwill by Simmons Corporation when recording its

investment in Bush?

A. $29,000

B. $20,000

C. $12,000

D. $10,000

According to ASC 958, not-for-profit entities should report investments in the financial

statements at:

I. fair market value.

II. lower of cost or market.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

For all acquired contingencies, the acquirer should do all of the following except:

A. Provide documentation from the acquirer’s attorney regarding pending lawsuits and

loan guarantees

B. Provide a description of each contingency

C. Disclose the amount recognized at the acquisition date

D. Describe the estimated range of possible undiscounted outcomes of the contingency

Spartan Company purchased interior decoration material from Egypt for 100,000

Egyptian pounds on September 5, 20X8, with payment due on December 2, 20X8.

Additionally, on September 5, Spartan acquired a 90-day forward contract to purchase

100,000 Egyptian pounds of E = $.1850. The forward contract was acquired to manage

the exposed net liability position in Egyptian pounds, but it was not designated as a

hedge. The spot rates were:

September 5, 20X8 E1 = $0.1835

December 2, 20X8 E1 = $0.1865

Based on the preceding information, in the entry made on December 2nd to revalue

foreign currency receivable to current equivalent U.S. dollar value,

A. Accounts Payable will be debited for $18,350.

B. Foreign Currency Units will be debited for $18,500.

C. Foreign Currency Transaction Gain will be credited for $150.

D. Other Comprehensive Income will be credited for $300.

Financing for the renovation of Cherry City’s municipal park, begun and completed

during 20X1, came from the following sources:

In its 20X1 capital projects fund operating statement, Cherry should report these amounts

as:

Revenues Other financing sources

A. $ 0 $2,750,000

B. $ 600,000 $2,150,000

C. $2,750,000 $ 0

D. $2,600,000 $ 150,000

The town of Stow was incorporated and began governmental operations on July 1,

20X8. Stow’s transactions and events for the fiscal year ended June 30, 20X9, are listed

below. Stow uses the consumption method of accounting for purchases of supplies.

Encumbrances do not lapse at year end.

Required:

Prepare the journal entry (ies) required in the general fund for each of the following

transactions or events.

a. The town budget was approved, providing for revenues of $800,000, a $40,000

transfer to establish an internal service fund (ISF), and expenditures of $750,000.

b. Property taxes were levied in the amount of $700,000, with 4 percent of the total

estimated to be uncollectible.

c. Purchase orders were issued in the amount of $90,000 for equipment, and $635,000

for other goods and services.

d. Collections for fines and licenses totaled $99,000 for the year.

e. Property taxes collected amounted to $680,000; the balance was reclassified as

delinquent, and the allowance for uncollectible taxes was reduced to $15,000.

f. The equipment ordered was received, and a voucher was issued for the final invoice

cost of $91,000.

g. All but $12,000 of the other goods and services ordered was received. Vouchers were

issued for the invoice cost of $622,000.

h. All but $10,000 of the vouchers issued during the year was paid.

i. A transfer in the amount of $40,000 was made to establish an internal service fund for

the town. The general fund received services of $7,000 from the internal service fund

during the year, with $2,000 remaining unpaid at year end.

j. Expenditures recorded for the year included the purchase of supplies. The estimated

balance of supplies on hand at year end was $2,000.

k. A reserve was established at year end for the outstanding encumbrances, all of which

will be honored in the next fiscal year.

l. Closing entries were made.

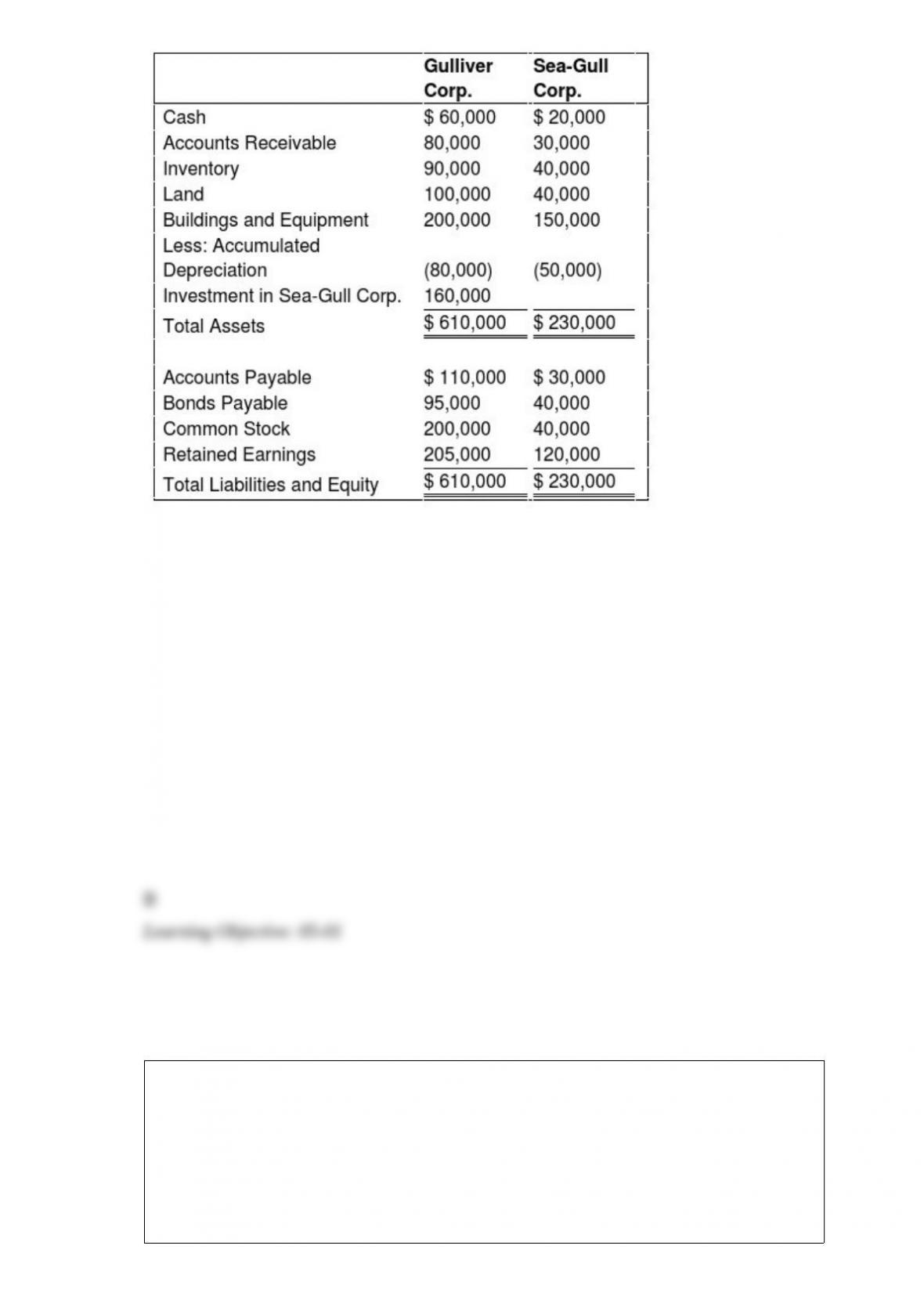

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount of total inventory will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $130,000

B. $135,000

C. $90,000

D. $45,000

Nash Company acquired Seel Corporation through an exchange of common shares. All

of Seel’s assets and liabilities were immediately transferred to Nash. Nash’s common

stock was trading at $25 per share at the time of the exchange. The total par value of

Nash’s stock outstanding before and after the acquisition was $750,000 and $840,000,

respectively. Nash’s additional paid-in capital before and after the acquisition were

$200,000 and $560,000, respectively.

Based on the preceding information, what number of shares did Nash issue at the time

of the exchange?

A. 3,600

B. 5,000

C. 14,400

D. 18,000

Wally Corporation acquired 70 percent of the common shares and 60 percent of the

preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At

that date, the fair value of the noncontrolling interest in Safety’s common stock was

equal to 30 percent of the book value of its common stock. Safety’s balance sheet at the

time of acquisition contained the following balances:

Assets $700,000 Liabilities $110,000

Preferred Stock 100,000

Common Stock 200,000

Retained Earnings 290,000

Total Assets $700,000 Total Liabilities and Equities $700,000

The preferred shares are cumulative and have an 8 percent annual dividend rate and are

three years in arrears on January 1, 20X6. All of the $10 par value preferred shares are

callable at $12 per share. During 20X6, Safety reported net income of $80,000 and paid

no dividends.

Based on the preceding information, what is Safety’s contribution to consolidated net

income for 20X6?

A. $48,000

B. $56,000

C. $72,000

D. $80,000

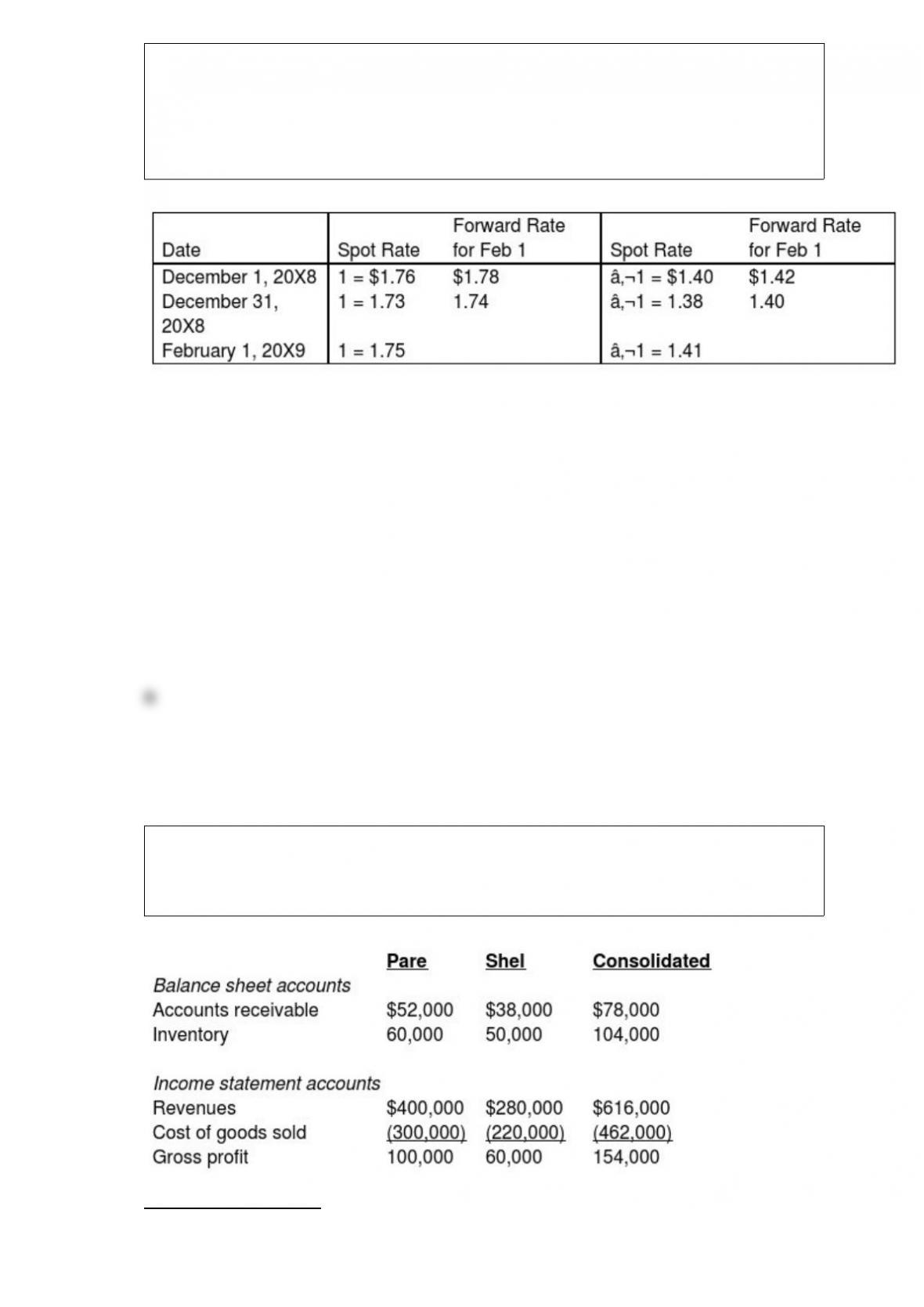

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the overall effect of speculation on 20X8 net

income?

A. $4,000 gain

B. $6,000 gain

C. $8,000 loss

D. $8,000 gain

Selected information from the separate and consolidated balance sheets and income

statements of Pare, Inc. and its subsidiary, Shel Co., as of December 31, 20X5, and for

the year then ended is as follows:

Additional information:

During 20X5, Pare sold goods to Shel at the same markup on cost that Pare uses for all

sales.

At December 31, 20X5, what was the amount of Shel’s payable to Pare for intercompany

sales?

A. $12,000

B. $6,000

C. $58,000

D. $64,000

In the RST partnership, Ron’s capital is $80,000, Stella’s is $75,000, and Tiffany’s is

$50,000. They share income in a 3:2:1 ratio, respectively. Tiffany is retiring from the

partnership. Each of the following questions is independent of the others.

Refer to the above information. Tiffany is paid $56,000, and all implied goodwill is

recorded. What is the total amount of goodwill recorded?

A. $0

B. $6,000

C. $30,000

D. $36,000

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount of inventory will be included in the

consolidated balance sheet immediately following the acquisition?

A. $0

B. $65,000

C. $70,000

D. $60,000

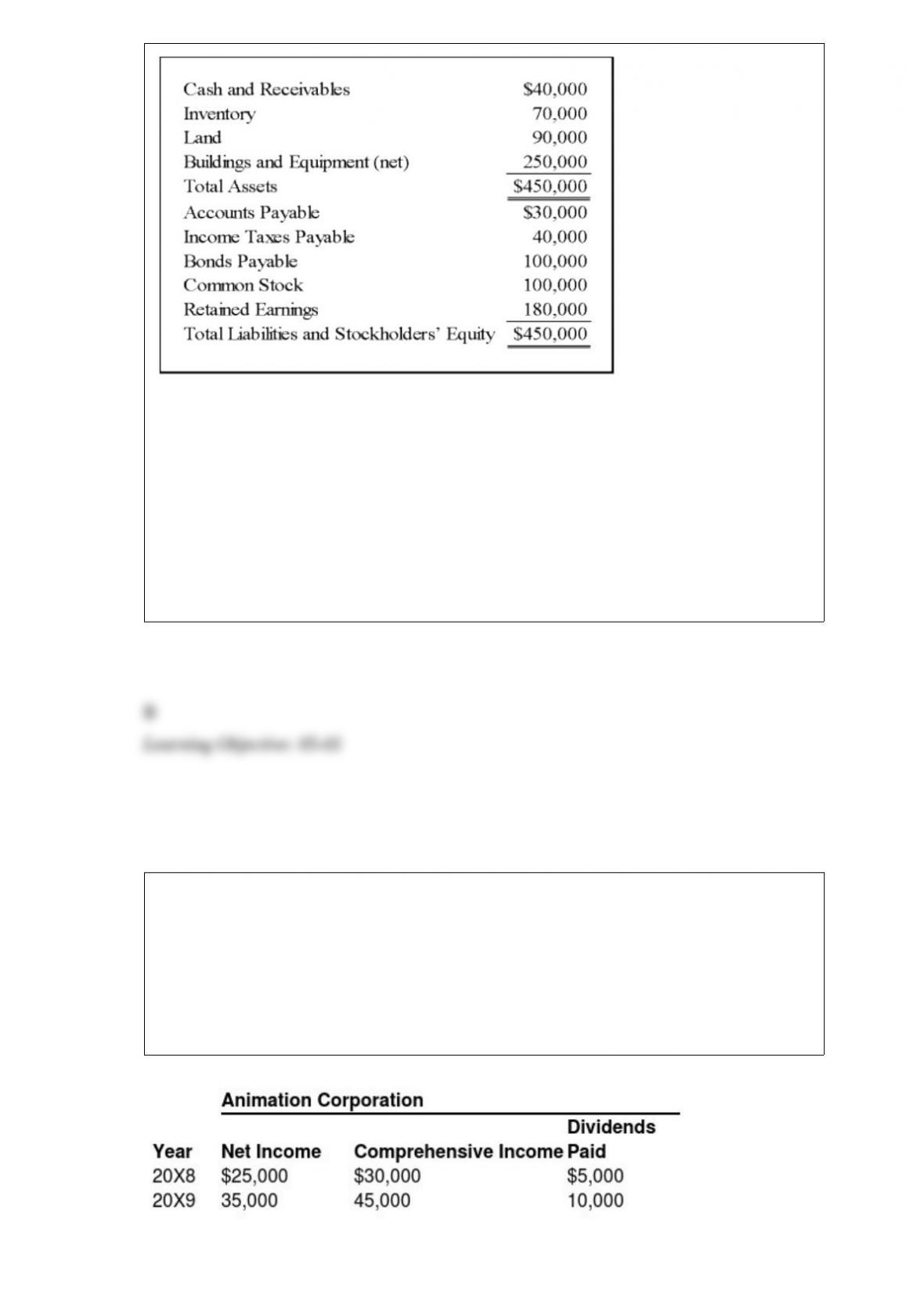

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company’s

common stock for $280,000 cash. At that date, Animation reported common stock

outstanding of $200,000 and retained earnings of $100,000, and the fair value of the

noncontrolling interest was $70,000. The book values and fair values of Animation’s

assets and liabilities were equal, except for other intangible assets which had a fair

value $50,000 greater than book value and an 8-year remaining life. Animation reported

the following data for 20X8 and 20X9:

Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

Based on the preceding information, what is the amount of comprehensive income

attributable to the controlling interest for 20X9?

A. $138,750

B. $131,000

C. $128,750

D. $135,000

Mercury Corporation acquired 100 percent of the stock of Jupiter Company when the

book value of Jupiter’s net assets was $250,000. The fair value of Jupiter’s net assets

was $280,000 on the acquisition date.

Based on the preceding information, what amount of goodwill will be reported in

consolidated financial statements presented immediately following the combination if

Mercury paid $295,000 for the acquisition?

A. $0

B. $5,000

C. $15,000

D. $45,000