Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-41

P4-25 (continued)

b.

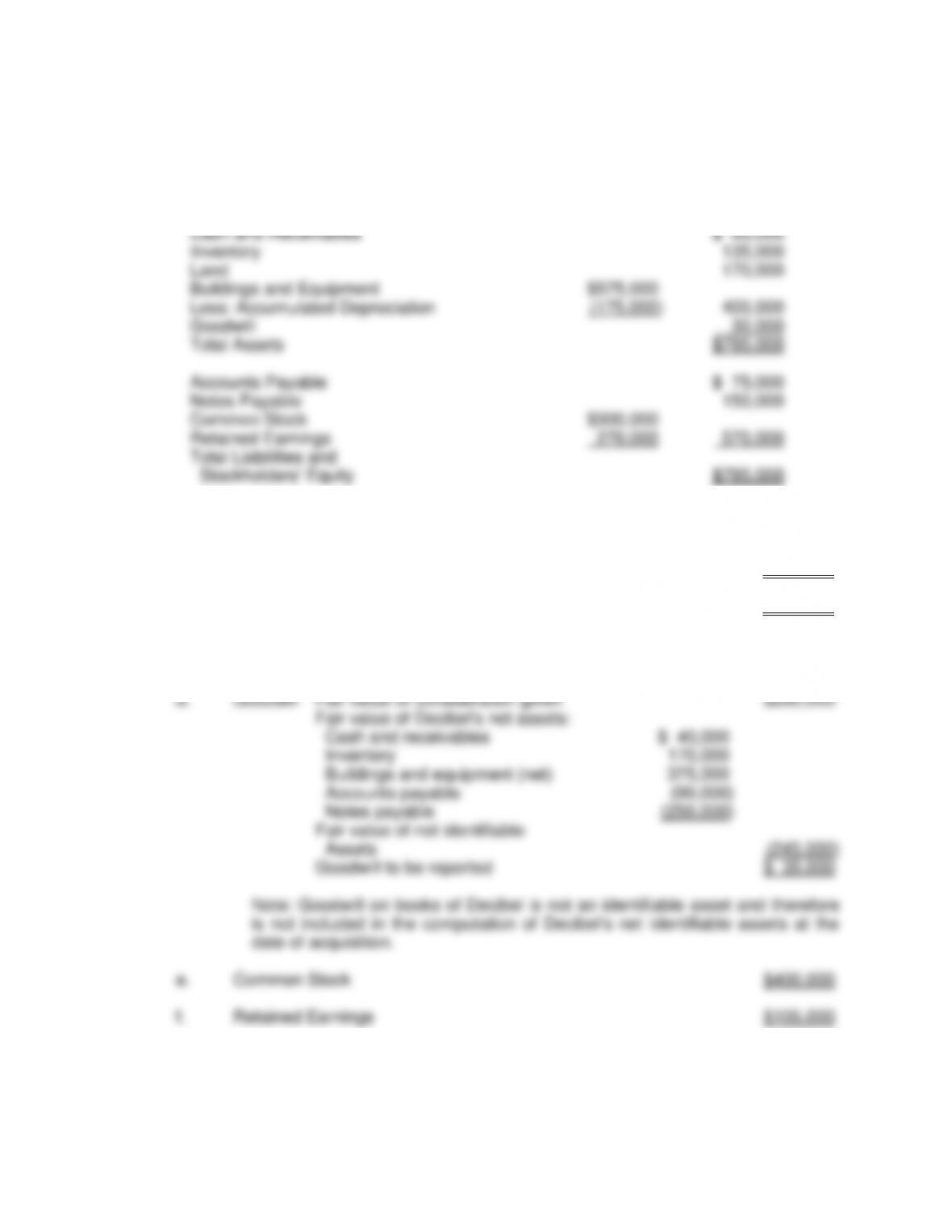

Teresa Corporation and Subsidiary

Consolidated Balance Sheet

January 1, 20X4

Cash and Receivables

$ 60,000

Inventory

135,000

Land

170,000

Buildings and Equipment

$575,000

Less: Accumulated Depreciation

(175,000)

400,000

Goodwill

30,000

Total Assets

$795,000

Accounts Payable

$ 75,000

Notes Payable

150,000

Common Stock

$300,000

Retained Earnings

270,000

570,000

Total Liabilities and

Stockholders‘ Equity

$795,000

P4-26 Computation of Consolidated Balances

a.

Inventories ($110,000 + $170,000)

$280,000

b.

Buildings and Equipment (net) ($350,000 + $375,000)

$725,000

c.

Investment in Decibel stock will be fully eliminated and will not

appear in the consolidated balance sheet.

d.

Goodwill

Fair value of consideration given

$280,000

Fair value of Decibel’s net assets:

Cash and receivables

$ 40,000

Inventory

170,000

Buildings and equipment (net)

375,000

Accounts payable

(90,000)

Notes payable

(250,000)

Fair value of net identifiable

Assets

(245,000)

Goodwill to be reported

$ 35,000

Note: Goodwill on books of Decibel is not an identifiable asset and therefore

is not included in the computation of Decibel’s net identifiable assets at the

date of acquisition.

e.

Common Stock

$400,000

f.

Retained Earnings

$105,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4-27 Balance Sheet Consolidation [AICPA Adapted]

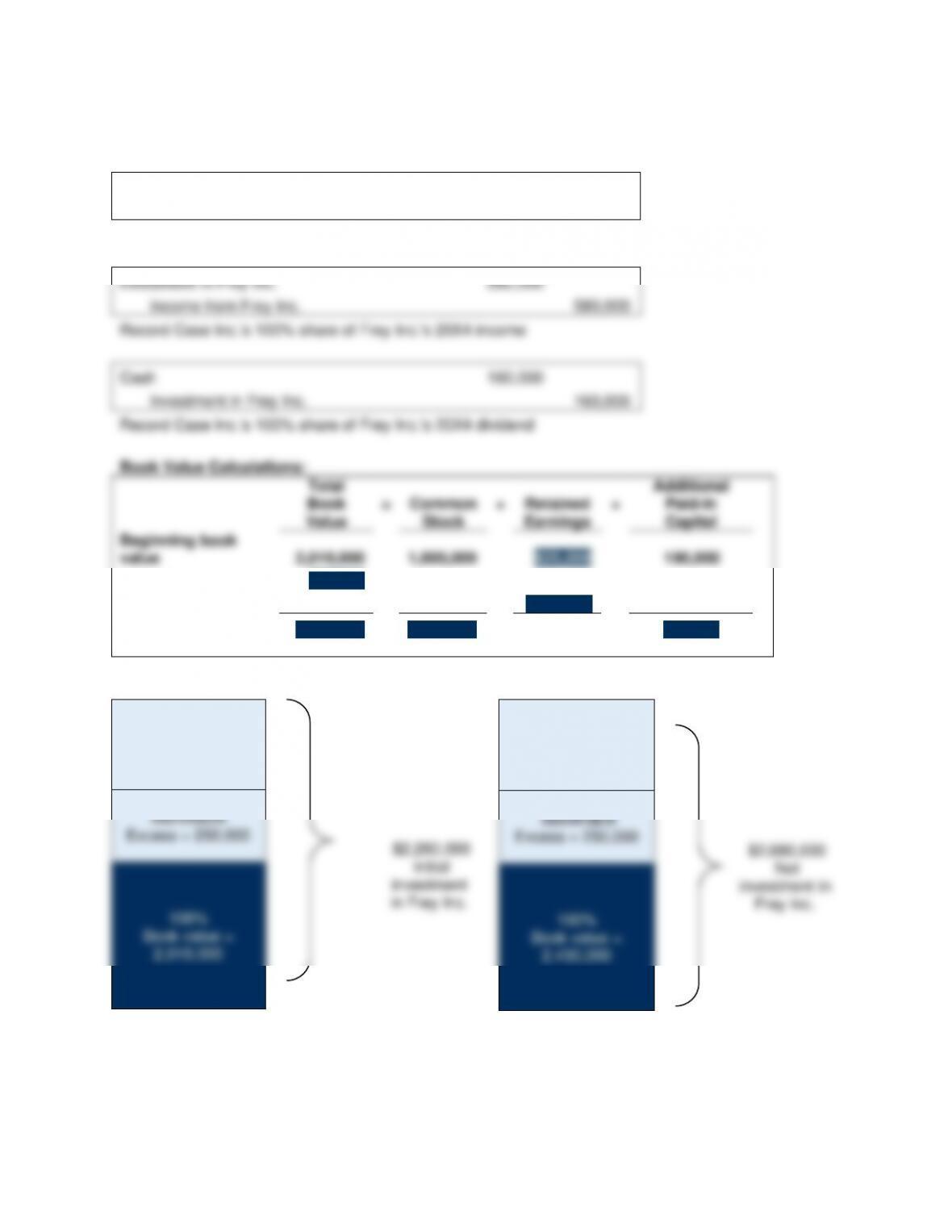

Equity Method Entries on Case Inc.’s Books:

Investment in Frey Inc.

2,260,000

Cash

2,260,000

Record the initial investment in Frey Inc.

Investment in Frey Inc.

580,000

Income from Frey Inc.

580,000

Record Case Inc.’s 100% share of Frey Inc.’s 20X4 income

Cash

160,000

Investment in Frey Inc.

160,000

Record Case Inc.’s 100% share of Frey Inc.’s 20X4 dividend

Book Value Calculations:

Total

Book

Value

=

Common

Stock

+

Retained

Earnings

+

Additional

Paid-In

Capital

Beginning book

value

2,010,000

1,000,000

820,000

190,000

+ Net Income

580,000

580,000

– Dividends

(160,000)

(160,000)

Ending book value

2,430,000

1,000,000

1,240,000

190,000

1/1/X4

Goodwill = 0

Identifiable

Excess = 250,000

$2,260,000

Initial

investment

in Frey Inc.

100%

Book value =

2,010,000

12/31/X4

Goodwill = 0

Identifiable

Excess = 250,000

$2,680,000

Net

investment in

Frey Inc.

100%

Book value =

2,430,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-43

P4-27 (continued)

Basic Consolidation Entry

Common Stock

1,000,000

Retained Earnings

820,000

Income from Frey Inc.

580,000

Additional Paid-In Capital

190,000

Dividends Declared

160,000

Investment in Frey Inc.

2,430,000

Excess Value (Differential) Calculations:

Total

=

Land

Beginning balance

250,000

250,000

Changes

0

0

Ending balance

250,000

250,000

Excess Value (Differential) Reclassification Entry:

Land

250,000

Investment in Frey Inc.

250,000

Investment in

Income from

Frey Inc.

Frey Inc.

Acquisition Price

2,260,000

100% Net Income

580,000

580,000

100% Net Income

160,000

100% Dividends

Ending Balance

2,680,000

580,000

Ending Balance

2,430,000

Basic

580,000

250,000

Excess Reclass.

0

0

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-44

P4-27 (continued)

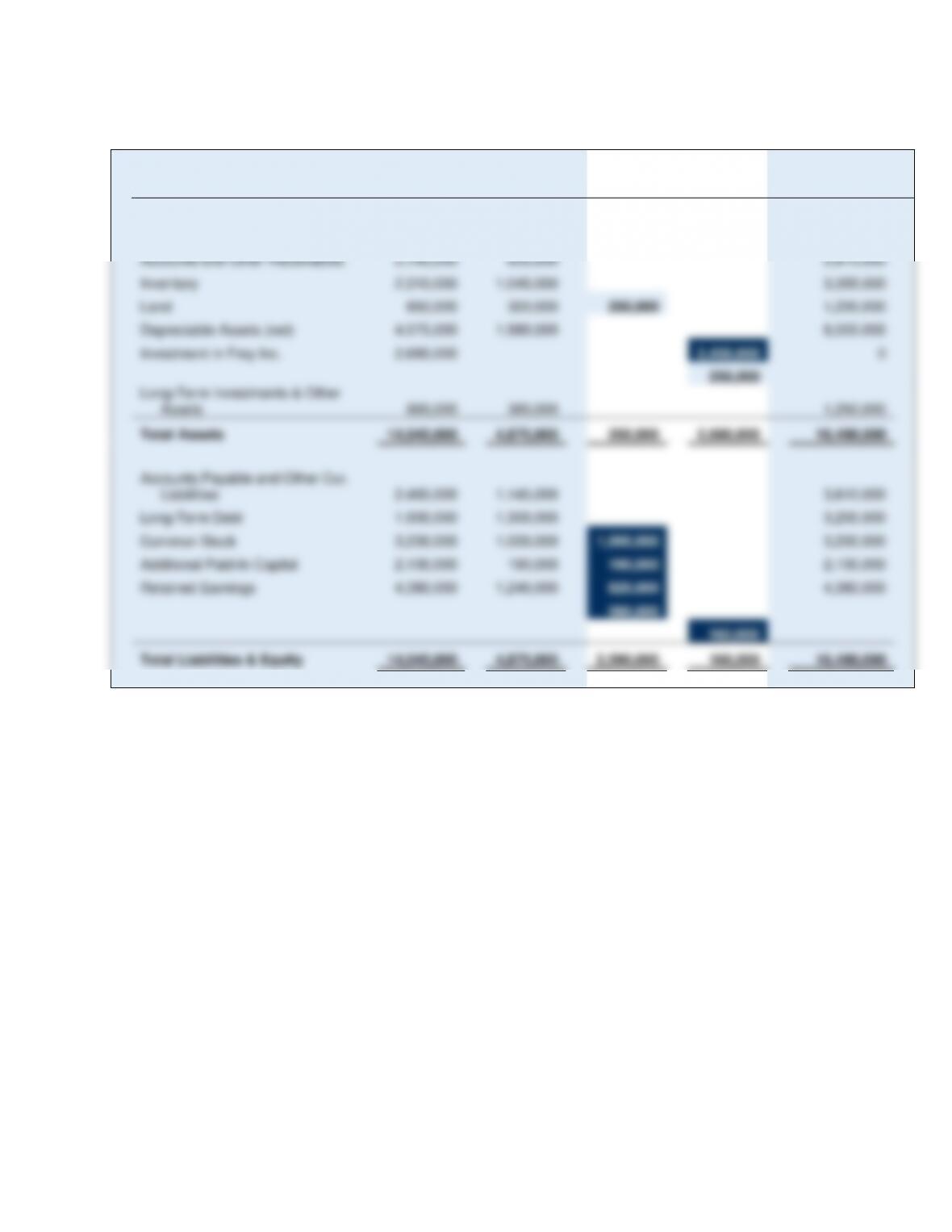

Case Inc.

Frey Inc.

Consolidation Entries

DR

CR

Consolidated

Balance Sheet

Cash

825,000

330,000

1,155,000

Accounts and Other Receivables

2,140,000

835,000

2,975,000

Inventory

2,310,000

1,045,000

3,355,000

Land

650,000

300,000

250,000

1,200,000

Depreciable Assets (net)

4,575,000

1,980,000

6,555,000

Investment in Frey Inc.

2,680,000

2,430,000

0

250,000

Long-Term Investments & Other

Assets

865,000

385,000

1,250,000

Total Assets

14,045,000

4,875,000

250,000

2,680,000

16,490,000

Accounts Payable and Other Cur.

Liabilities

2,465,000

1,145,000

3,610,000

Long-Term Debt

1,900,000

1,300,000

3,200,000

Common Stock

3,200,000

1,000,000

1,000,000

3,200,000

Additional Paid-In Capital

2,100,000

190,000

190,000

2,100,000

Retained Earnings

4,380,000

1,240,000

820,000

4,380,000

580,000

160,000

Total Liabilities & Equity

14,045,000

4,875,000

2,590,000

160,000

16,490,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-45

P4-28 Consolidated Balance Sheet

a.

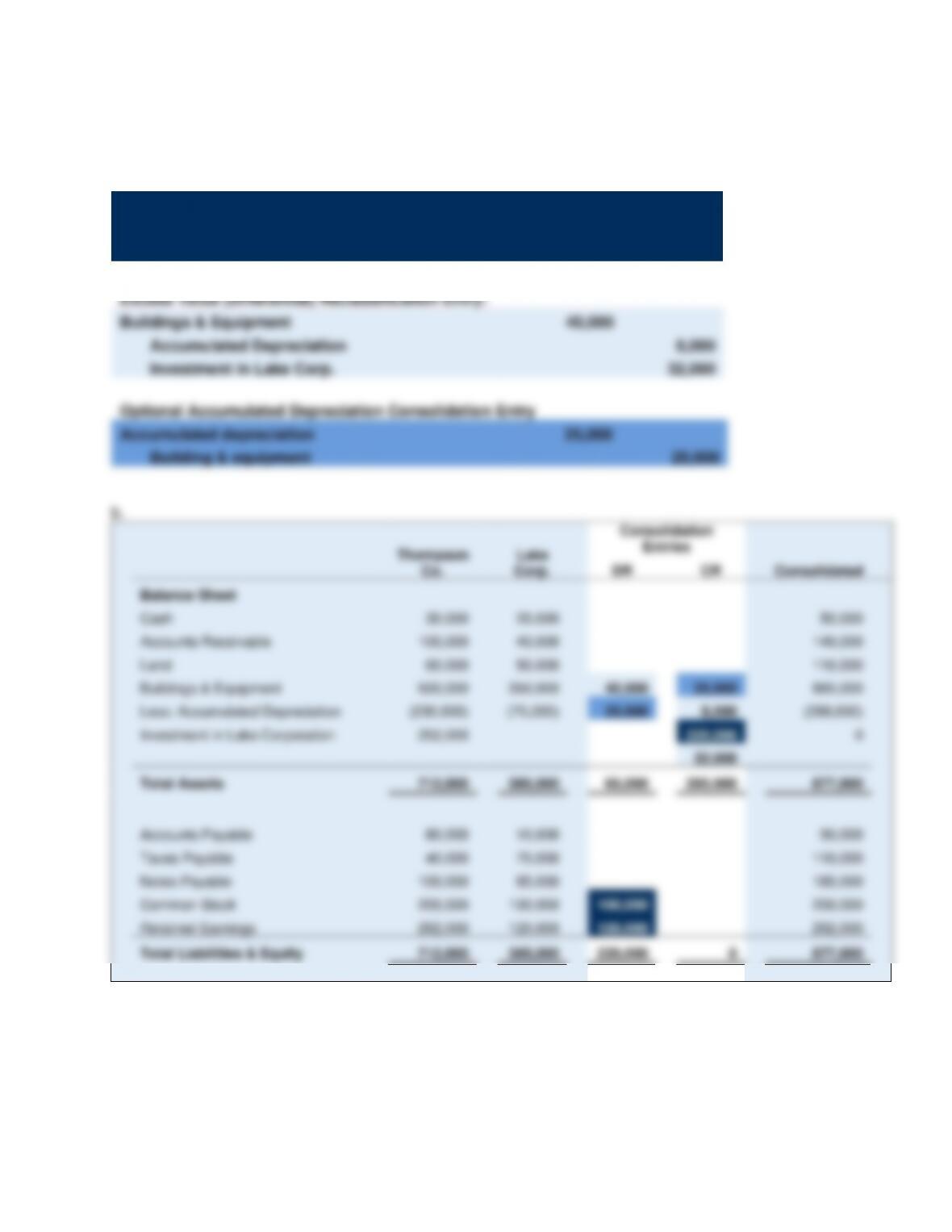

Basic Consolidation Entry

Common Stock

100,000

Retained Earnings

120,000

Investment in Lake Corp.

220,000

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

40,000

Accumulated Depreciation

8,000

Investment in Lake Corp.

32,000

Optional Accumulated Depreciation Consolidation Entry

Accumulated depreciation

25,000

Building & equipment

25,000

b.

Thompson

Co.

Lake

Corp.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

30,000

20,000

50,000

Accounts Receivable

100,000

40,000

140,000

Land

60,000

50,000

110,000

Buildings & Equipment

500,000

350,000

40,000

25,000

865,000

Less: Accumulated Depreciation

(230,000)

(75,000)

25,000

8,000

(288,000)

Investment in Lake Corporation

252,000

220,000

0

32,000

Total Assets

712,000

385,000

65,000

285,000

877,000

Accounts Payable

80,000

10,000

90,000

Taxes Payable

40,000

70,000

110,000

Notes Payable

100,000

85,000

185,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

292,000

120,000

120,000

292,000

Total Liabilities & Equity

712,000

385,000

220,000

0

877,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4-29 Comprehensive Problem: Consolidation in Subsequent Period

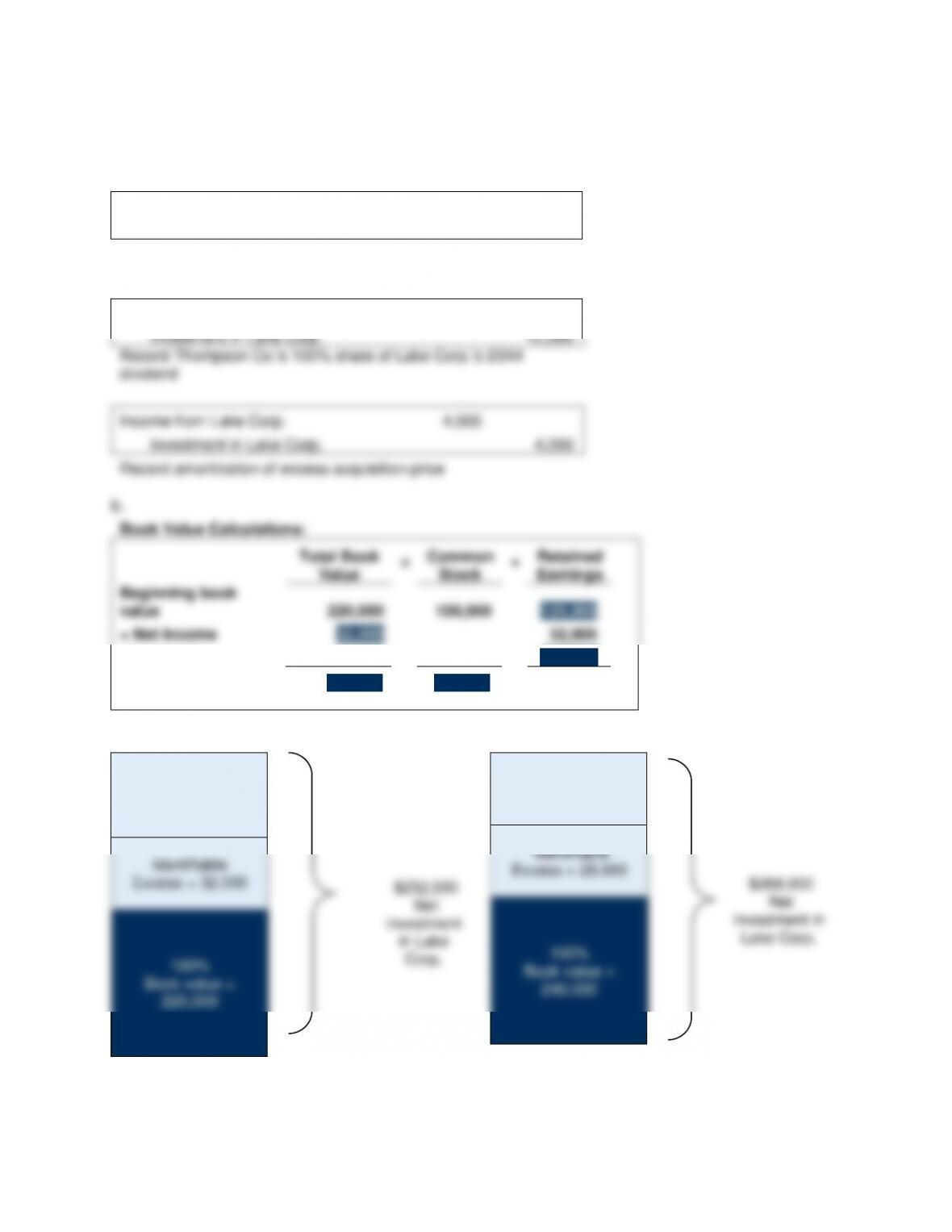

a.

Equity Method Entries on Thompson Co.’s Books:

Investment in Lake Corp.

32,000

Income from Lake Corp.

32,000

Record Thompson Co.’s 100% share of Lake Corp.’s 20X4

income

Cash

12,000

Investment in Lake Corp.

12,000

Record Thompson Co.’s 100% share of Lake Corp.’s 20X4

dividend

Income from Lake Corp.

4,000

Investment in Lake Corp.

4,000

Record amortization of excess acquisition price

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

220,000

100,000

120,000

+ Net Income

32,000

32,000

– Dividends

(12,000)

(12,000)

Ending book value

240,000

100,000

140,000

1/1/X4

Goodwill = 0

Identifiable

Excess = 32,000

$252,000

Net

investment

in Lake

Corp.

100%

Book value =

220,000

12/31/X4

Goodwill = 0

Identifiable

Excess = 28,000

$268,000

Net

investment in

Lake Corp.

100%

Book value =

240,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-47

P4–29 (continued)

Basic Consolidation Entry

Common Stock

100,000

Retained Earnings

120,000

Income from Lake Corp.

32,000

Dividends Declared

12,000

Investment in Lake Corp.

240,000

Excess Value (Differential) Calculations:

Total

=

Buildings &

Equipment

+

Acc.

Depr.

Beginning balance

32,000

40,000

(8,000)

Changes

(4,000)

(4,000)

Ending balance

28,000

40,000

(12,000)

Amortized Excess Value Reclassification Entry:

Depreciation Expense

4,000

Income from Lake Corp.

4,000

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

40,000

Accumulated Depreciation

12,000

Investment in Lake Corp.

28,000

Eliminate Intercompany Accounts:

Accounts Payable

2,500

Accounts Receivable

2,500

Investment in

Income from

Lake Corp.

Lake Corp.

Beginning

Balance

252,000

100% Net Income

32,000

32,000

100% Net Income

12,000

100% Dividends

4,000

Excess Val. Amort.

4,000

Ending Balance

268,000

28,000

Ending Balance

240,000

Basic

32,000

28,000

Excess Reclass.

4,000

0

0

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

25,000

Building & Equipment

25,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-48

P4–29 (continued)

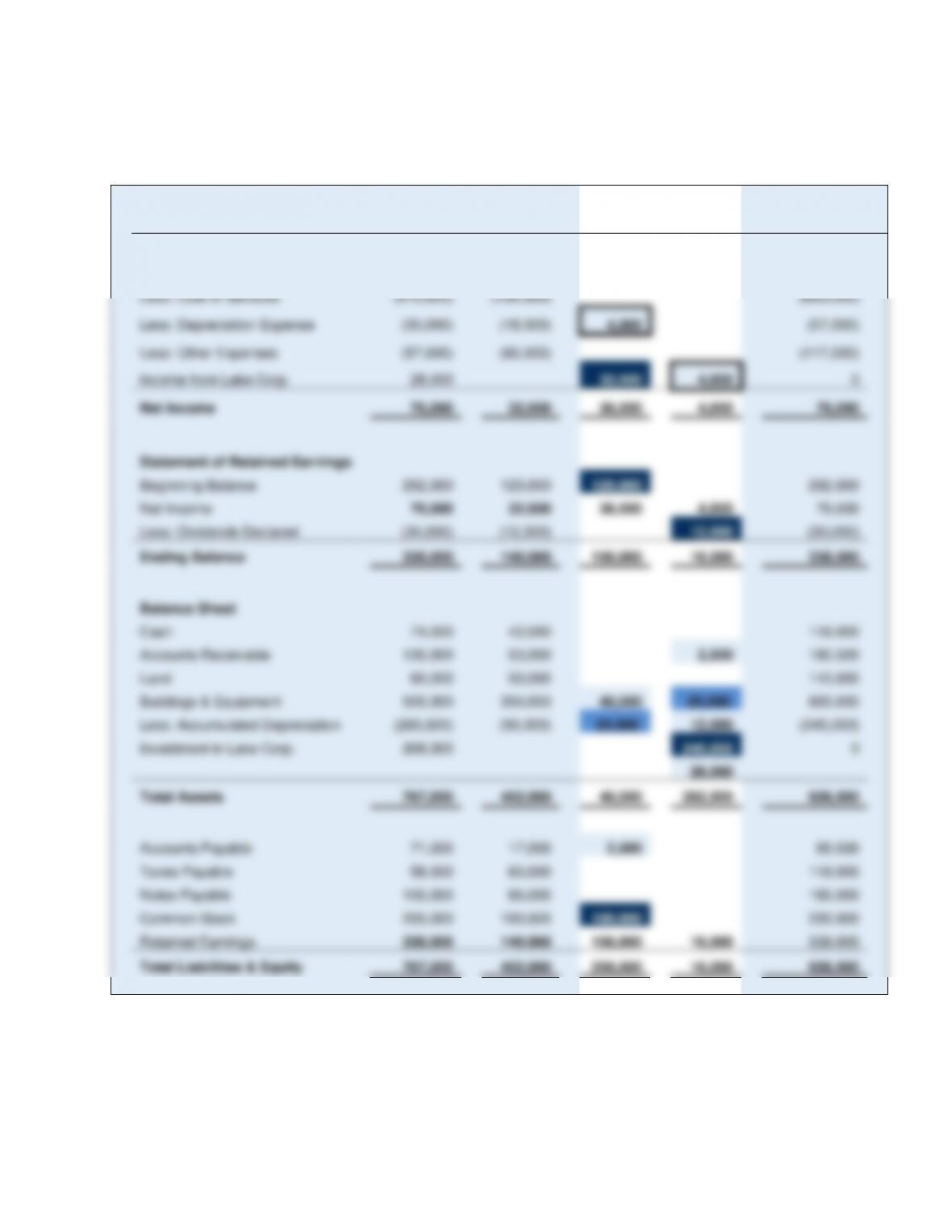

c.

Thompson

Co.

Lake

Corp.

Consolidation Entries

DR

CR

Consolidated

Income Statement

Service Revenue

610,000

240,000

850,000

Less: Cost of Services

(470,000)

(130,000)

(600,000)

Less: Depreciation Expense

(35,000)

(18,000)

4,000

(57,000)

Less: Other Expenses

(57,000)

(60,000)

(117,000)

Income from Lake Corp.

28,000

32,000

4,000

0

Net Income

76,000

32,000

36,000

4,000

76,000

Statement of Retained Earnings

Beginning Balance

292,000

120,000

120,000

292,000

Net Income

76,000

32,000

36,000

4,000

76,000

Less: Dividends Declared

(30,000)

(12,000)

12,000

(30,000)

Ending Balance

338,000

140,000

156,000

16,000

338,000

Balance Sheet

Cash

74,000

42,000

116,000

Accounts Receivable

130,000

53,000

2,500

180,500

Land

60,000

50,000

110,000

Buildings & Equipment

500,000

350,000

40,000

25,000

865,000

Less: Accumulated Depreciation

(265,000)

(93,000)

25,000

12,000

(345,000)

Investment in Lake Corp.

268,000

240,000

0

28,000

Total Assets

767,000

402,000

40,000

282,500

926,500

Accounts Payable

71,000

17,000

2,500

85,500

Taxes Payable

58,000

60,000

118,000

Notes Payable

100,000

85,000

185,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

338,000

140,000

156,000

16,000

338,000

Total Liabilities & Equity

767,000

402,000

258,500

16,000

926,500

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4-30 Acquisition at Other than Fair Value of Net Assets

a. Ownership acquired for $280,000:

Equity Method Entries on Mason Corp.’s Books:

Investment in Best Co.

280,000

Cash

280,000

Record the initial investment in Best Co.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

255,000

80,000

175,000

Basic Consolidation Entry

Common stock

80,000

Retained earnings

175,000

Investment in Best Co.

Excess Value (Differential) Calculations:

=

+

Inventories

+

Balances

Excess Value (Differential) Reclassification Entry:

Land

Goodwill

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4-30 (continued)

Investment in

Best Co.

Acquisition Price

280,000

255,000

Basic

25,000

Excess Reclass.

0

b. Ownership acquired for $251,000:

Equity Method Entries on Mason Corp.’s Books:

Investment in Best Co.

268,000

Cash

Gain on Bargain Purchase

251,000

17,000

Record the initial investment in Best Co.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

255,000

80,000

175,000

Common Stock

Retained Earnings

Investment in Best Co.

Excess Value (Differential) Calculations:

=

Balances

Excess Value (Differential) Reclassification Entry:

Land

Inventories

Investment in Best Co.

Investment in

Best Co.

Acquisition Price

268,000

255,000

Basic

13,000

Excess Reclass.