Chapter 16 – Partnerships: Liquidation

16–11

E16-2 Multiple-Choice Questions on Partnership Liquidation

1.

a –

Casey

Dithers

Edwards

Profit and loss ratio

5

3

2

Beginning capital

80,000

90,000

70,000

Actual loss on assets

(15,000)

(9,000)

(6,000)

Potential loss on

other assets

(50,000)

(30,000)

(20,000)

Balances

15,000

51,000

44,000

Safe payments

(15,000)

(51,000)

(44,000)

2.

b –

3.

d –

Art

Blythe

Cooper

Profit and loss ratio

40%

40%

20%

Capital balances

37,000

65,000

48,000

Loss absorption potential

92,500

162,500

240,000

Loss to reduce C to B:

(77,500 x 0.20 = 15,500)

(77,500)

Balances

92,500

162,500

162,500

Loss to reduce B & C to A:

(B:70,000 x 0.40 = 28,000)

(70,000)

(C:70,000 x 0.20 = 14,000)

(70,000)

Balances

92,500

92,500

92,500

Cash of $20,000 after settlement of liabilities: Cooper receives first $15,500;

remaining $4,500 split 2/3 to Blythe and 1/3 to Cooper.

4.

d –

Cash of $17,000: Cooper receives first $15,500; remaining $1,500 split 2/3 to

Blythe and 1/3 to Cooper.

5.

a –

If all partners received cash after the second sale, then the remaining $12,000

is distributed in the loss ratio.

6.

a –

Arnie

Bart

Kurt

Profit and loss ratio

40%

30%

30%

Capital balances

40,000

180,000

30,000

Loss of $100,000

(40,000)

(30,000)

(30,000)

Remaining equities

-0-

150,000

-0-

Arnie will receive nothing; the entire $150,000 will be paid to Bart.

Chapter 16 – Partnerships: Liquidation

16–12

E16-3 Computing Alternative Cash Distributions to Partners

Capital Balances

Bracken

Louden

Menser

40%

30%

30%

a

Capital balances before sale of equipment

25,000

5,000

10,000

Equipment sold for $30,000;

allocation of $10,000 loss

(4,000)

(3,000)

(3,000)

Capital balances after sale

21,000

2,000

7,000

Final distribution of cash

(21,000)

(2,000)

(7,000)

b.

Capital balances before sale of equipment

25,000

5,000

10,000

Equipment sold for $21,000;

allocation of $19,000 loss

(7,600)

(5,700)

(5,700)

Capital balances after sale

17,400

(700)

4,300

Allocate capital deficit of Louden:

700

4/7 x $700

(400)

3/7 X $700

______

______

_ (300)

Capital balances after allocation of Louden’s deficit

17,000

____-0-

_4,000

Final distribution of cash

(17,000)

_-0-

(4,000)

c.

Capital balances before sale of equipment

25,000

5,000

10,000

Equipment sold for $7,000;

allocation of $33,000 loss

(13,200)

(9,900)

(9,900)

Capital balances after sale

11,800

(4,900)

100

Allocate capital deficit of Louden:

4,900

4/7 x $4,900

(2,800)

3/7 X $4,900

______

______

(2,100)

Capital balances after allocation of Louden’s deficit

9,000

-0-

(2,000)

Allocate capital deficit of Menser:

2,000

4/4 x $2,000

(2,000)

_____

_____

Capital balances after allocation of Menser’s deficit

7,000

___-0-

___-0-

Final distribution of cash

(7,000)

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–13

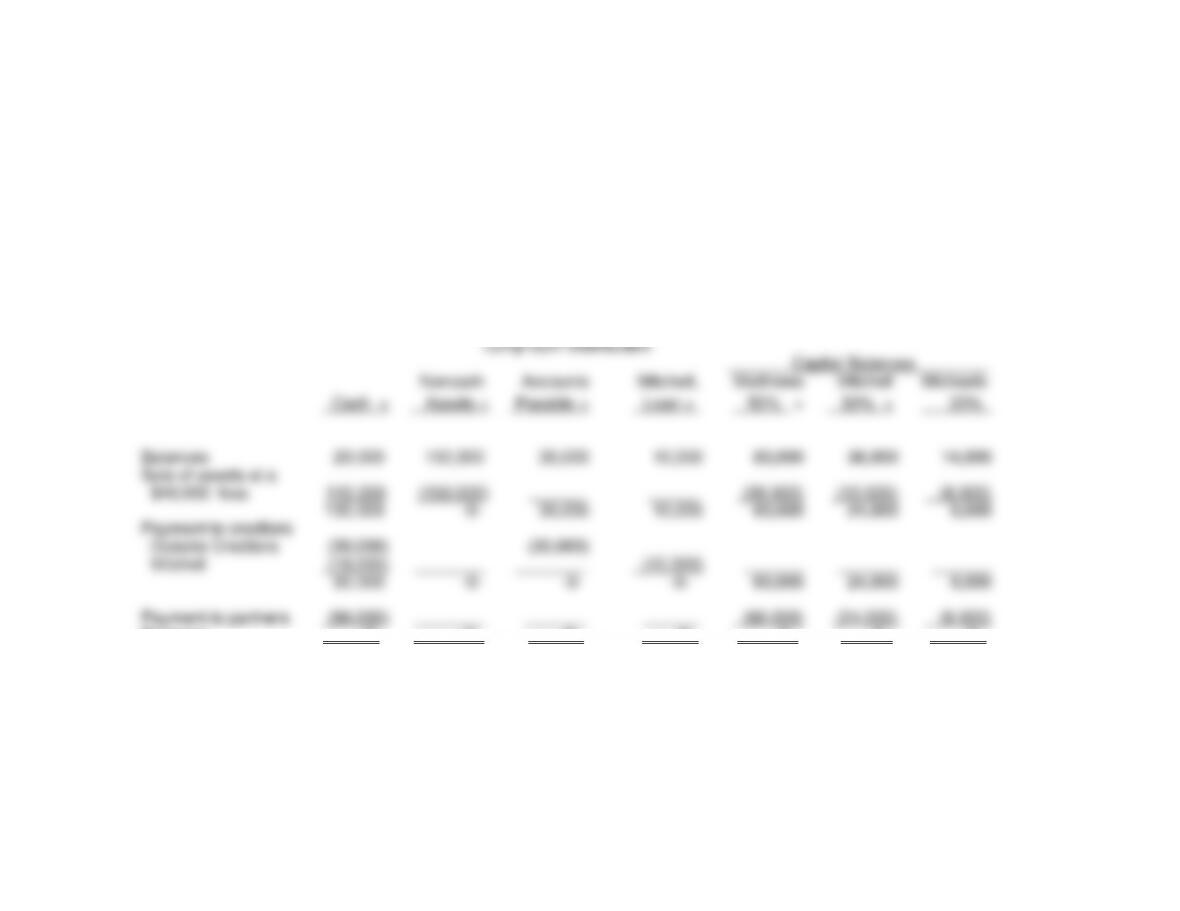

E16-4 Lump-Sum Liquidation

a.

BG Land Development Company

Statement of Partnership Realization and Liquidation

Lump-Sum Distribution

Capital Balances

Noncash

Accounts

Mitchell,

Matthews

Mitchell

Michaels

Cash +

Assets =

Payable +

Loan +

50% +

30% +

20%

Balances

20,000

150,000

30,000

10,000

80,000

36,000

14,000

Sale of assets at a

$40,000 loss

110,000

(150,000)

(20,000)

(12,000)

(8,000)

130,000

-0-

30,000

10,000

60,000

24,000

6,000

Payment to creditors

Outside Creditors

(30,000)

(30,000)

Mitchell

(10,000)

(10,000)

90,000

-0-

-0-

-0-

60,000

24,000

6,000

Payment to partners

(90,000)

(60,000)

(24,000)

(6,000)

Balances

-0-

-0-

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–14

E16-4 (continued)

b.

(1)

Cash

110,000

Matthews, Capital

20,000

Mitchell, Capital

12,000

Michaels, Capital

8,000

Noncash Assets

150,000

Sell noncash assets at a loss of $40,000.

(2)

Accounts Payable

30,000

Mitchell, Loan

10,000

Cash

40,000

Pay creditors, including Mitchell.

(3)

Matthews, Capital

60,000

Mitchell, Capital

24,000

Michaels, Capital

6,000

Cash

90,000

Final lump-sum distribution to partners.

E16-5 Schedule of Safe Payments

Based on strict observance of UPA 1997

Kitchens Just For You

Schedule of Safe Payments to Partners

Terry

Phyllis

Connie

_ (30%)_

__(50%)_

__(20%)_

Capital balances, September 1, 20X9

12,000

36,000

54,000

Write-off of $28,000 in goodwill

(8,400)

(14,000)

(5,600)

Write-off of $12,000 of receivables

(3,600)

(6,000)

(2,400)

Loss of $4,000 on sale of $24,000 of

inventory (one-half of $48,000 book value)

(1,200)

(2,000)

(800)

Capital balances, September 30, 20X9 (* = deficit)

(1,200)*

14,000

45,200

Possible loss of $19,000 for remaining

receivables (including $9,000 receivable from Terry)

and $24,000 for remaining inventory

(12,900)

(21,500)

(8,600)

Possible liquidation costs of $6,000

(1,800)

(3,000)

(1,200)

Balances (* = potential deficit)

(15,900)*

(10,500)*

35,400

Distribute Terry’s and Phyllis’ potential deficits to

Connie, the only partner with a capital credit

15,900

10,500

(26,400)

Safe payments to partners, September 30, 20X9

-0-

-0-

9,000

Chapter 16 – Partnerships: Liquidation

16–15

E16-5 (continued)

Based on practical approach:

Kitchens Just For You

Schedule of Safe Payments to Partners

Terry

Phyllis

Connie

_ (30%)_

__(50%)_

__(20%)_

Capital balances, September 1, 20X9

12,000

36,000

54,000

Loans to (from) partner

(9,000)

15,000

Total

3,000

36,000

69,000

Write-off of $28,000 in goodwill

(8,400)

(14,000)

(5,600)

Write-off of $12,000 of receivables

(3,600)

(6,000)

(2,400)

Loss of $4,000 on sale of $24,000 of

inventory (one-half of $48,000 book value)

(1,200)

(2,000)

(800)

Capital balances, September 30, 20X9 (* = deficit)

(10,200)*

14,000

60,200

Possible loss of $19,000 for remaining

receivables (including $9,000 receivable from Terry)

and $24,000 for remaining inventory

(12,900)

(21,500)

(8,600)

Possible liquidation costs of $6,000

(1,800)

(3,000)

(1,200)

Balances (* = potential deficit)

(24,900)*

(10,500)*

50,400

Distribute Terry’s and Phyllis’ potential deficits to

Connie, the only partner with a capital credit

24,900

10,500

(35,400)

Safe payments to partners, September 30, 20X9

-0-

-0-

15,000

Chapter 16 – Partnerships: Liquidation

16–16

E16-6 Schedule of Safe Payments to Partners

Maness and Joiner Partnership

Combined Statement of Realization and Schedule of Safe Payments

Capital

Accounts

Maness

Joiner

Cash +

Inventory=

Payable+

80% +

20%

Balances

25,000

120,000

15,000

65,000

65,000

Sale of inventory

40,000

(60,000)

(16,000)

(4,000)

Payment to creditors

(10,000)

(10,000)

55,000

60,000

5,000

49,000

61,000

Payments to partners

(Schedule 1)

(50,000)

(1,000)

(49,000)

5,000

60,000

5,000

48,000

12,000

Sale of inventory

30,000

(60,000)

(24,000)

(6,000)

Payment to creditors

(5,000)

(5,000)

30,000

-0-

-0-

24,000

6,000

Payments to partners

(30,000)

______

(24,000)

(6,000)

Balances

-0-

-0-

-0-

-0-

-0-

Schedule 1 Safe payments at end of first month:

Maness

Joiner

80%

20%

Capital balances

49,000

61,000

Potential loss of $60,000 on remaining inventory

(48,000)

(12,000)

Safe payments to partners

1,000

49,000

Chapter 16 – Partnerships: Liquidation

16–17

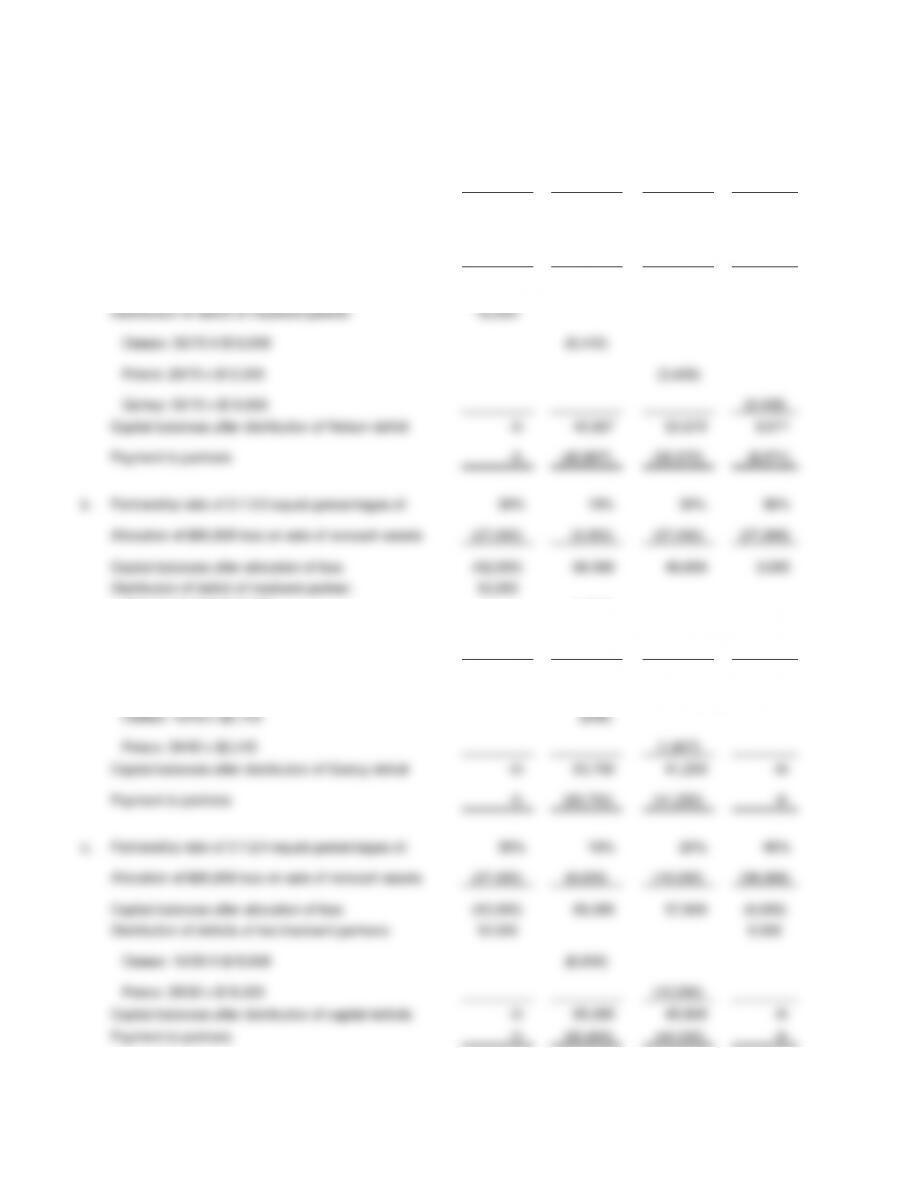

E16-7 Alternative Profit and Loss Sharing Ratios in a Partnership Liquidation

Nelson

Osman

Peters

Quincy

Capital balances at beginning of liquidation

15,000

75,000

75,000

30,000

a.

Partnership ratio of 3:3:2:2 equals percentages of:

30%

30%

20%

20%

Allocation of $90,000 loss on sale of noncash assets

(27,000)

(27,000)

(18,000)

(18,000)

Capital balances after allocation of loss

(12,000)

48,000

57,000

12,000

Distribution of deficit of insolvent partner:

12,000

Osman: 30/70 X $12,000

(5,143)

Peters: 20/70 x $12,000

(3,428)

Quincy: 20/70 x $12,000

(3,429)

Capital balances after distribution of Nelson deficit

-0-

42,857

53,572

8,571

Payment to partners

-0-

(42,857)

(53,572)

(8,571)

b.

Partnership ratio of 3:1:3:3 equals percentages of:

30%

10%

30%

30%

Allocation of $90,000 loss on sale of noncash assets

(27,000)

(9,000)

(27,000)

(27,000)

Capital balances after allocation of loss

(12,000)

66,000

48,000

3,000

Distribution of deficit of insolvent partner:

12,000

Osman: 10/70 X $12,000

(1,714)

Peters: 30/70 x $12,000

(5,143)

Quincy: 30/70 x $12,000

(5,143)

Capital balances after distribution of Nelson deficit

-0-

64,286

42,857

(2,143)

Distribution of deficit of insolvent partner:

2,143

Osman: 10/40 x $2,143

(536)

Peters: 30/40 x $2,143

(1,607)

Capital balances after distribution of Quincy deficit

-0-

63,750

41,250

-0-

Payment to partners

-0-

(63,750)

(41,250)

-0-

c.

Partnership ratio of 3:1:2:4 equals percentages of:

30%

10%

20%

40%

Allocation of $90,000 loss on sale of noncash assets

(27,000)

(9,000)

(18,000)

(36,000)

Capital balances after allocation of loss

(12,000)

66,000

57,000

(6,000)

Distribution of deficits of two insolvent partners:

12,000

6,000

Osman: 10/30 X $18,000

(6,000)

Peters: 20/30 x $18,000

(12,000)

Capital balances after distribution of capital deficits

-0-

60,000

45,000

-0-

Payment to partners

-0-

(60,000)

(45,000)

-0-

Chapter 16 – Partnerships: Liquidation

In case c. both Nelson and Quincy are personally insolvent so their capital deficits resulting

from the allocation of the loss can be added together and distributed to the two solvent

partners. However, if Quincy had been personally solvent, then he would be required to

remedy any capital deficit, including one that was distributed to him because of the insolvency

of another partner, as from the distribution of Nelson’s capital deficit in case b.

16–19

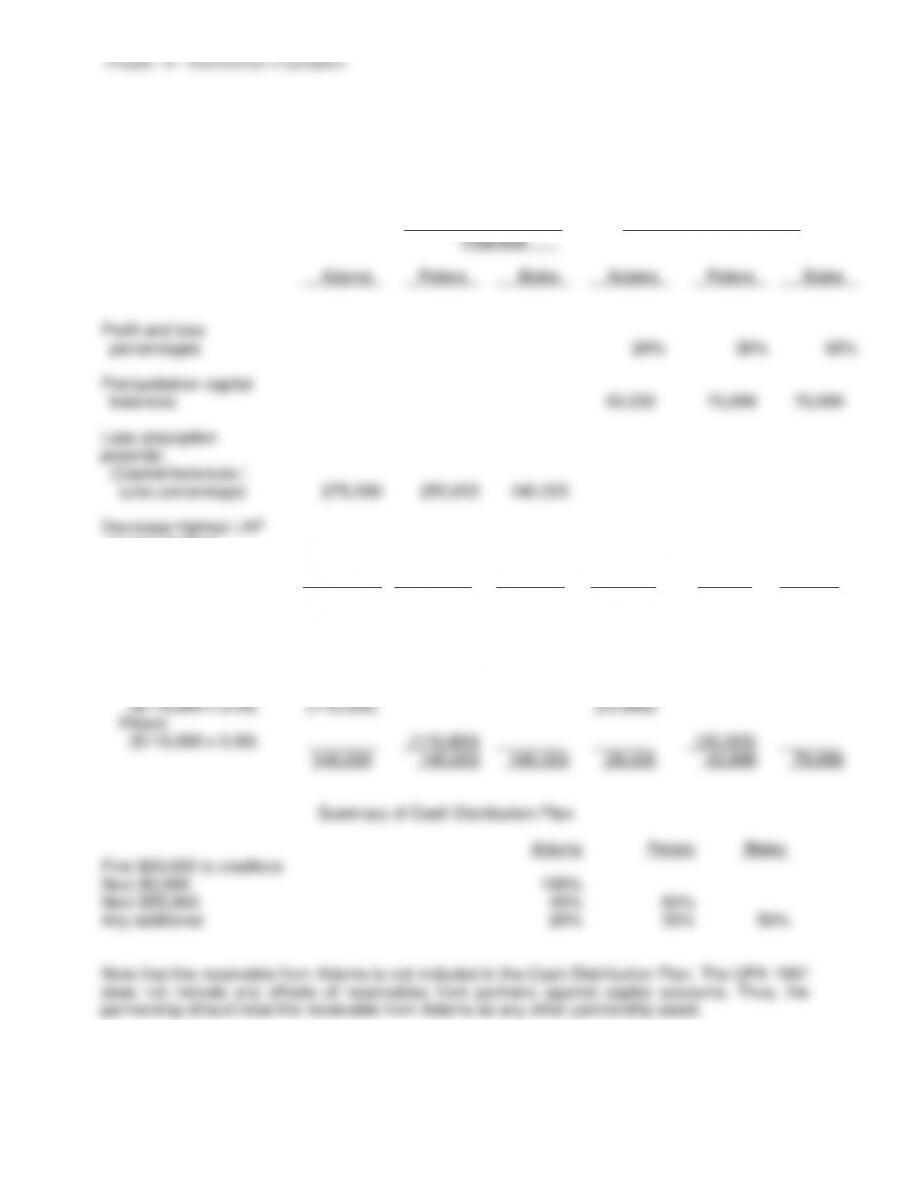

E16-8 Cash Distribution Plan

Based on strict observance of UPA 1997:

APB Partnership

Cash Distribution Plan

Loss Absorption

Potential

Capital Accounts

Adams

Peters

Blake

Adams

Peters

Blake

Profit and loss

percentages

20%

30%

50%

Preliquidation capital

balances

55,000

75,000

70,000

Loss absorption

potential

(Capital balances /

Loss percentage)

275,000

250,000

140,000

Decrease highest LAP

to next highest:

Adams

($25,000 x 0.20)

(25,000)

(5,000)

250,000

250,000

140,000

50,000

75,000

70,000

Decrease LAPs

to next highest:

Adams

($110,000 x 0.20)

(110,000)

(22,000)

Peters

($110,000 x 0.30)

(110,000)

(33,000)

140,000

140,000

140,000

28,000

42,000

70,000

Summary of Cash Distribution Plan

Adams

Peters

Blake

First $50,000 to creditors

Next $5,000

100%

Next $55,000

40%

60%

Any additional

20%

30%

50%

Note that the receivable from Adams is not included in the Cash Distribution Plan. The UPA 1997

does not include any offsets of receivables from partners against capital accounts. Thus, the

partnership should treat the receivable from Adams as any other partnership asset.

Chapter 16 – Partnerships: Liquidation

16–20