On September 1, 20X1, Brady Corp. entered into a foreign exchange contract for

speculative purposes by purchasing 50,000 deutsche marks for delivery in 60 days. The

rates to exchange $1 for 1 deutsche mark follow:

9/1/20X1 9/30/20X1

Spot-rate 0.75 0.70

30-day forward rate 0.73 0.72

60-day forward rate 0.74 0.73

In its September 30, 20X1 income statement, what amount should Brady report as

foreign exchange loss?

A. $1,000

B. $2,500

C. $1,500

D. $500

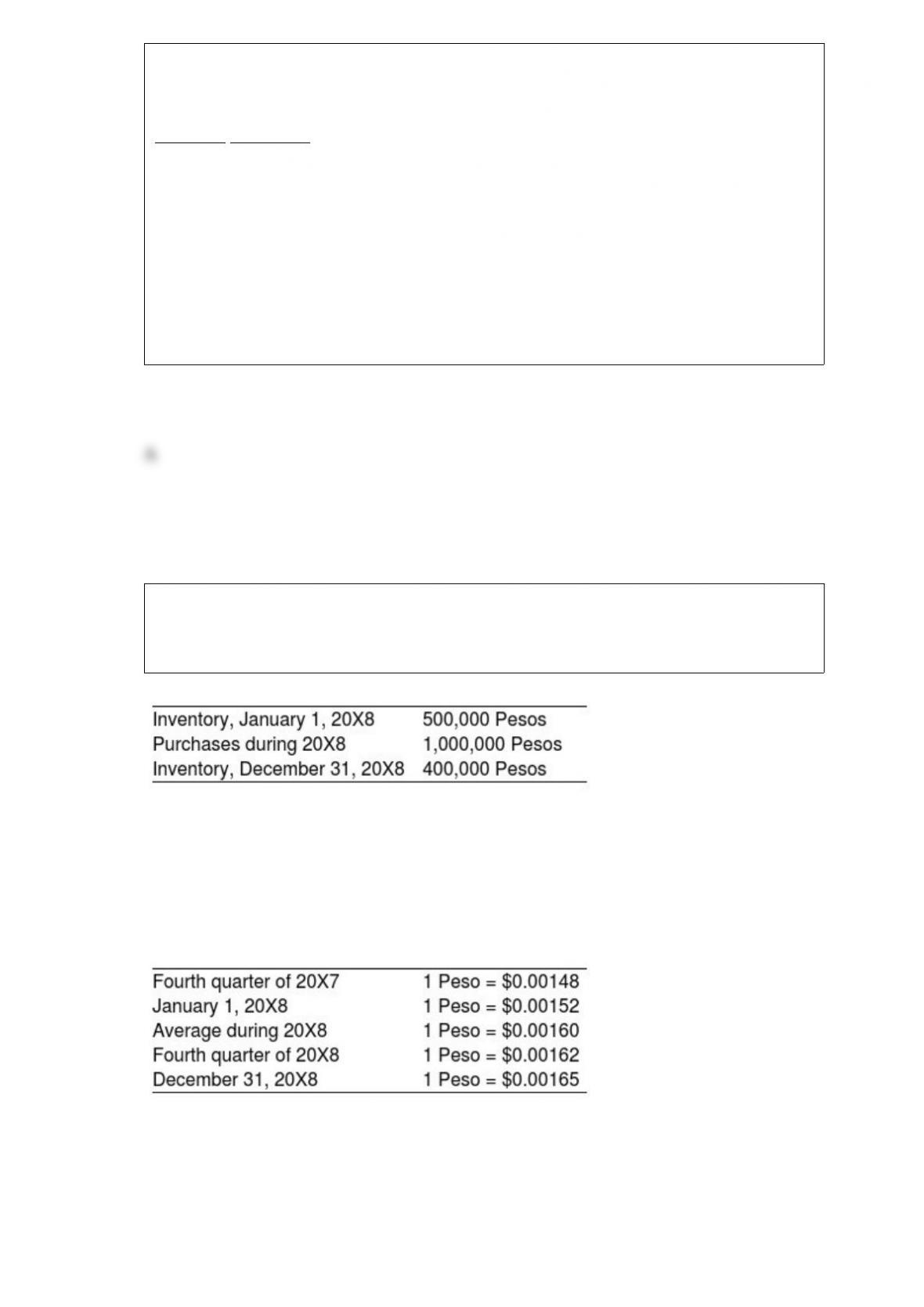

Mercury Company is a subsidiary of Neptune Company and is located in Valparaso,

Chile, where the currency is the Chilean Peso. Data on Mercury’s inventory and

purchases are as follows:

The beginning inventory was acquired during the fourth quarter of 20X7, and the ending

inventory was acquired during the fourth quarter of 20X8. Purchases were made evenly

over the year. Exchange rates were as follows:

Refer the information provided above. Assuming the U.S. dollar is the functional currency,

what is the amount of Mercury’s cost of goods sold remeasured in U.S. dollars?

A. $1,680

B. $1,712

C. $1,700

D. $1,692

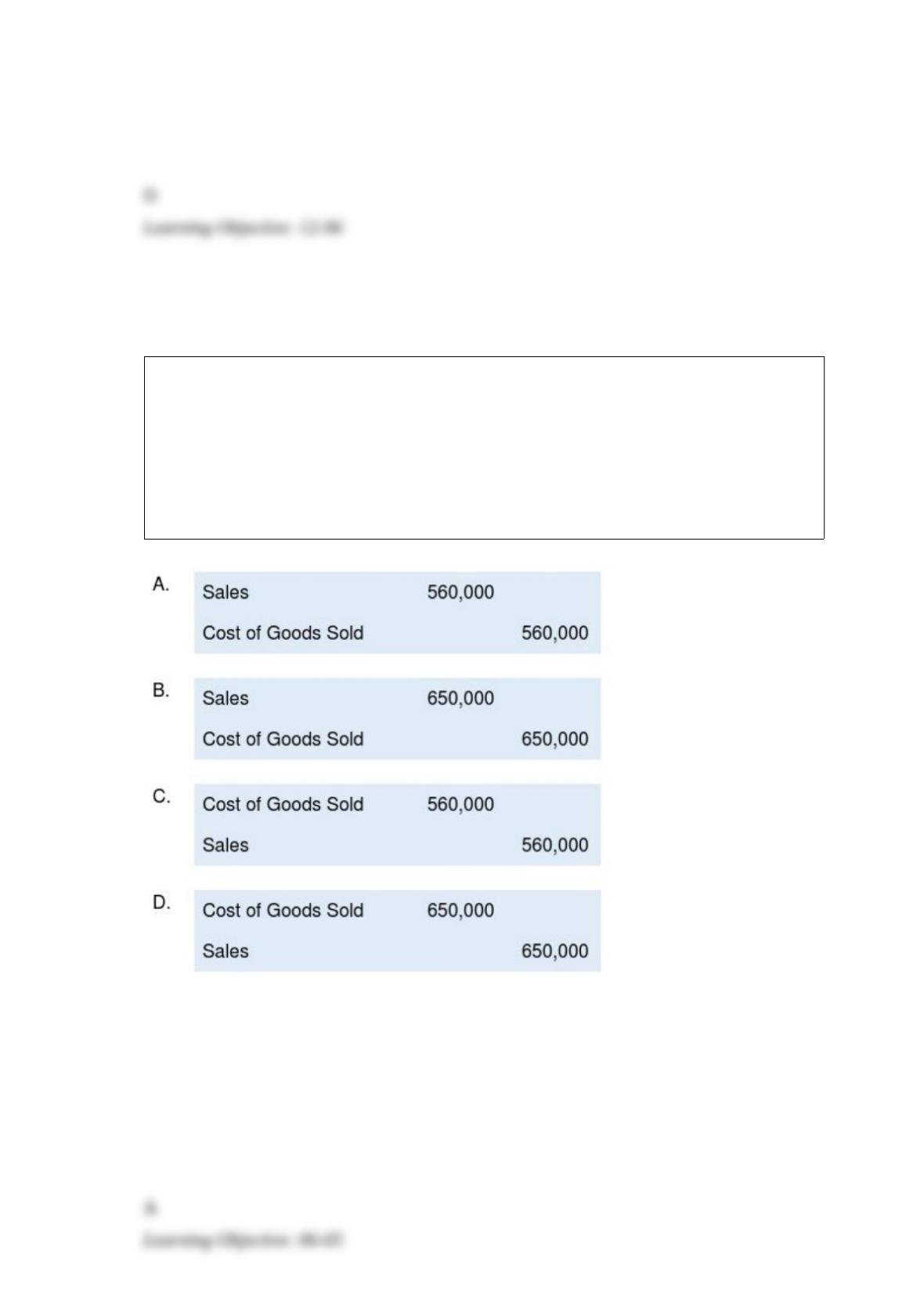

Global Corporation acquired 85 percent of Local Company’s voting shares of stock in

20X7. During 20X8, Global purchased 50,000 picture tubes for $15 each and sold

28,000 of them to Local for $20 each. Local sold all of the units to unrelated entities

prior to December 31, 20X8, for $30 each. Both companies use perpetual inventory

systems.

Which worksheet consolidating entry is needed in preparing consolidated financial

statements for 20X8 to remove all effects of the intercompany sale?

A. Option A

B. Option B

C. Option C

D. Option D

Company X issues variable-rate debt but wishes to fix its interest rates because it

believes the variable rate may increase. Company Y has a fixed-rate bond but is looking

for a variable-rate interest because it assumes the interest rates may decrease. The two

companies agree to exchange cash flows. Such an arrangement is called:

A. a futures contract.

B. a forward contract.

C. a swap.

D. an option.

For the year ended June 30, 20X9, a university assessed its students a total of

$4,000,000 for tuition and fees. Included in this amount was $300,000 of tuition

remissions awarded to graduate teaching assistants, and $150,000 of scholarships

awarded to undergraduate students. Tuition and fees totaling $3,550,000 were collected

during the year ended June 30, 20X9. What amount should be reported in the

unrestricted fund as net revenue from tuition and fees for the year ended June 30,

20X9?

A. $4,000,000

B. $3,550,000

C. $3,700,000

D. $3,850,000

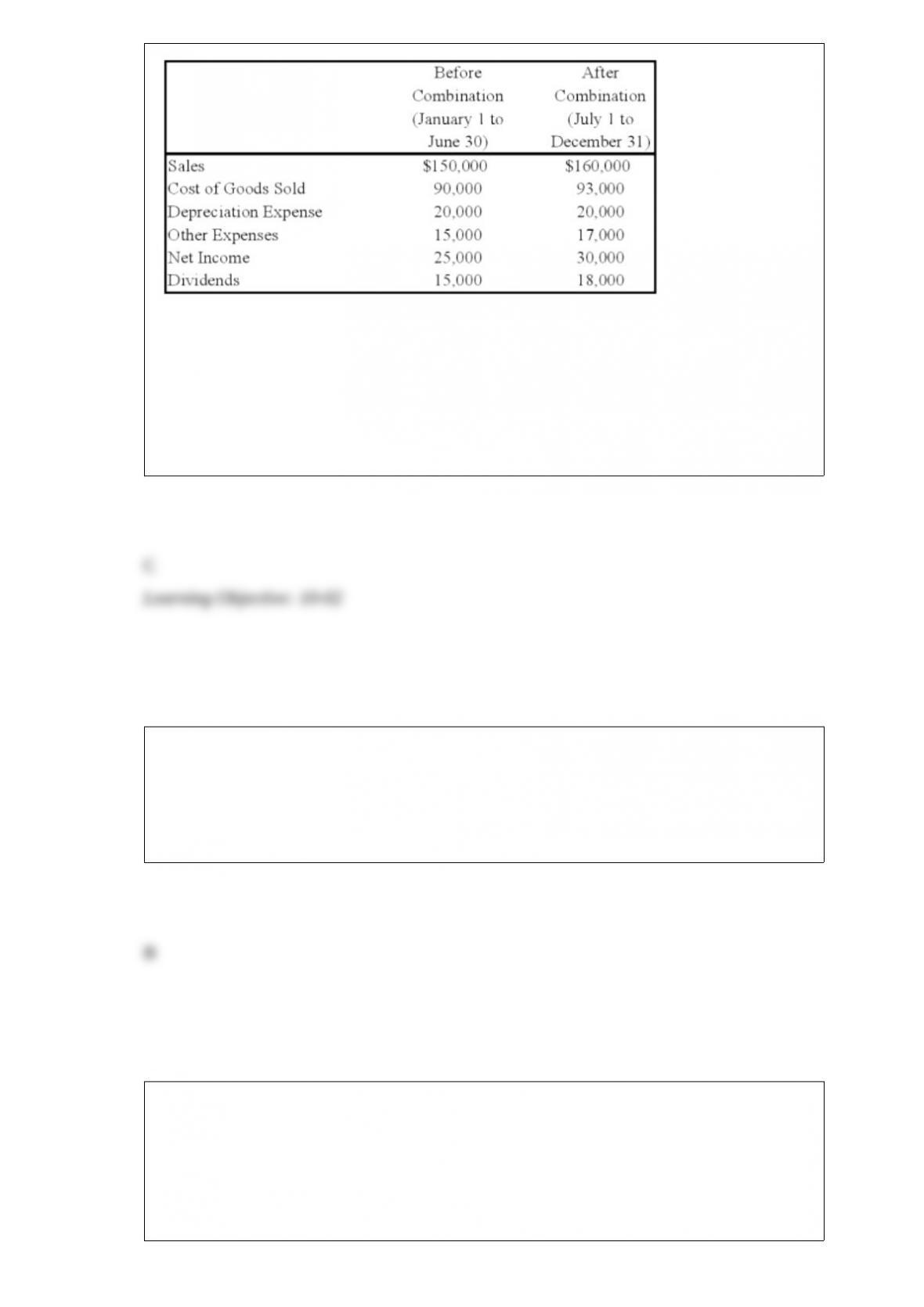

On July 1, 20X8, Fair Logic Corporation acquires 75 percent of Integrated Systems Inc.

common stock for its underlying book value. At the time of acquisition, the fair value of

the noncontrolling interest is equal to its proportionate share of book value of Integrated

Systems. On January 1, 20X8 Integrated reported common stock of $100,000 and

retained earnings of $130,000. For the year 20X8, Integrated reports the following

items:

Fair Logic uses the equity method in accounting for this investment.

Based on the preceding information, what is the fair value of the noncontrolling interest

at the time of acquisition?

A. $47,813

B. $57,500

C. $60,000

D. $45,000

The payment to general unsecured creditors is often termed:

A. a “preference payment.”

B. a “dividend.”

C. a “write-off.”

D. a “bonus.”

Based on the preceding information, had Robert not used the forward exchange

contract, what would have been the foreign currency transaction gain or loss for the

year?

A. Gain of $200

B. Gain of $150

C. Loss of $350

D. Loss of $200

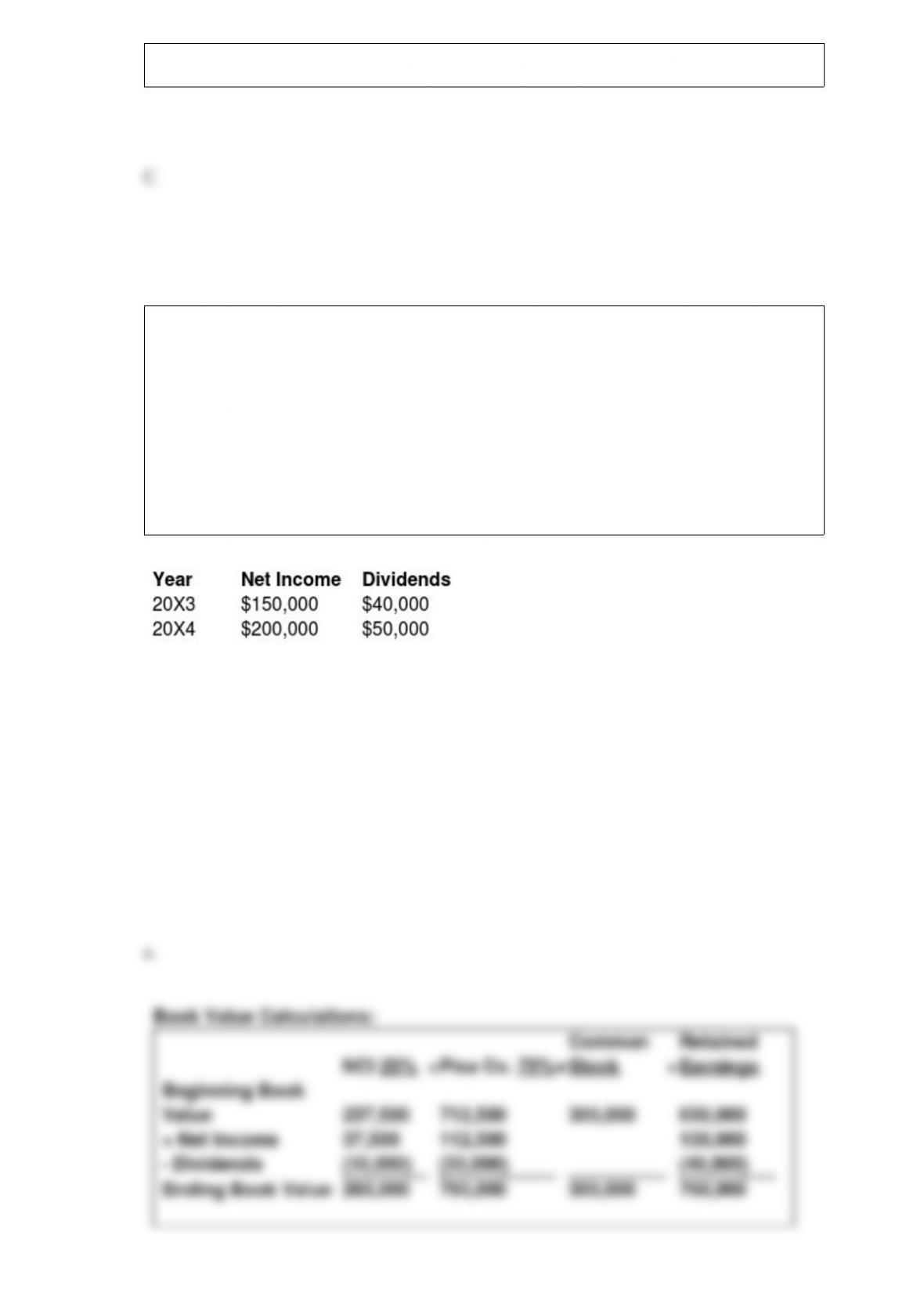

Pisa Company acquired 75 percent of Siena Company on January 1, 20X3 for

$712,500. The fair value of the noncontrolling interest was equal to 25 percent of book

value. On the date of acquisition, Siena had common stock outstanding of $300,000 and

a balance in retained earnings of $650,000. During 20X3, Siena purchased inventory for

$35,000 and sold it to Pisa for $50,000. Of this amount, Pisa reported $20,000 in ending

inventory in 20X3 and later sold it in 20X4. In 20X4, Pisa sold inventory it had

purchased for $40,000 to Siena for $60,000. Siena sold $45,000 of this inventory in

20X4.

Income and dividend information for Siena for 20X3 and 20X4 are as follows:

Pisa Company uses the modified equity method.

Required:

a. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X3.

b. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X4.

A joint venture may be organized as a:

I. Partnership.

II. Corporation.

III. Undivided interest.

A. I only

B. II only

C. I or III only

D. I, II, or III

Vision Corporation acquired 75 percent of the stock of Meta Company on January 1,

20X7, for $225,000. At that date, the fair value of the noncontrolling interest was

$75,000. Meta’s balance sheet contained the following amounts at the time of the

combination:

During each of the next three years, Meta reported net income of $30,000 and paid

dividends of $10,000. On January 1, 20X9, Vision sold 1,500 shares of Meta’s $10 par

value shares for $60,000 in cash. Vision used the fully adjusted equity method in

accounting for its ownership of Meta Company.

Based on the preceding information, in the consolidating entries to complete a full

consolidation worksheet, Investment in Meta Stock at January 1, 20X9, will be credited

for:

A. $255,000.

B. $240,000.

C. $204,000.

D. $136,000.

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Staff Accounting Bulletins

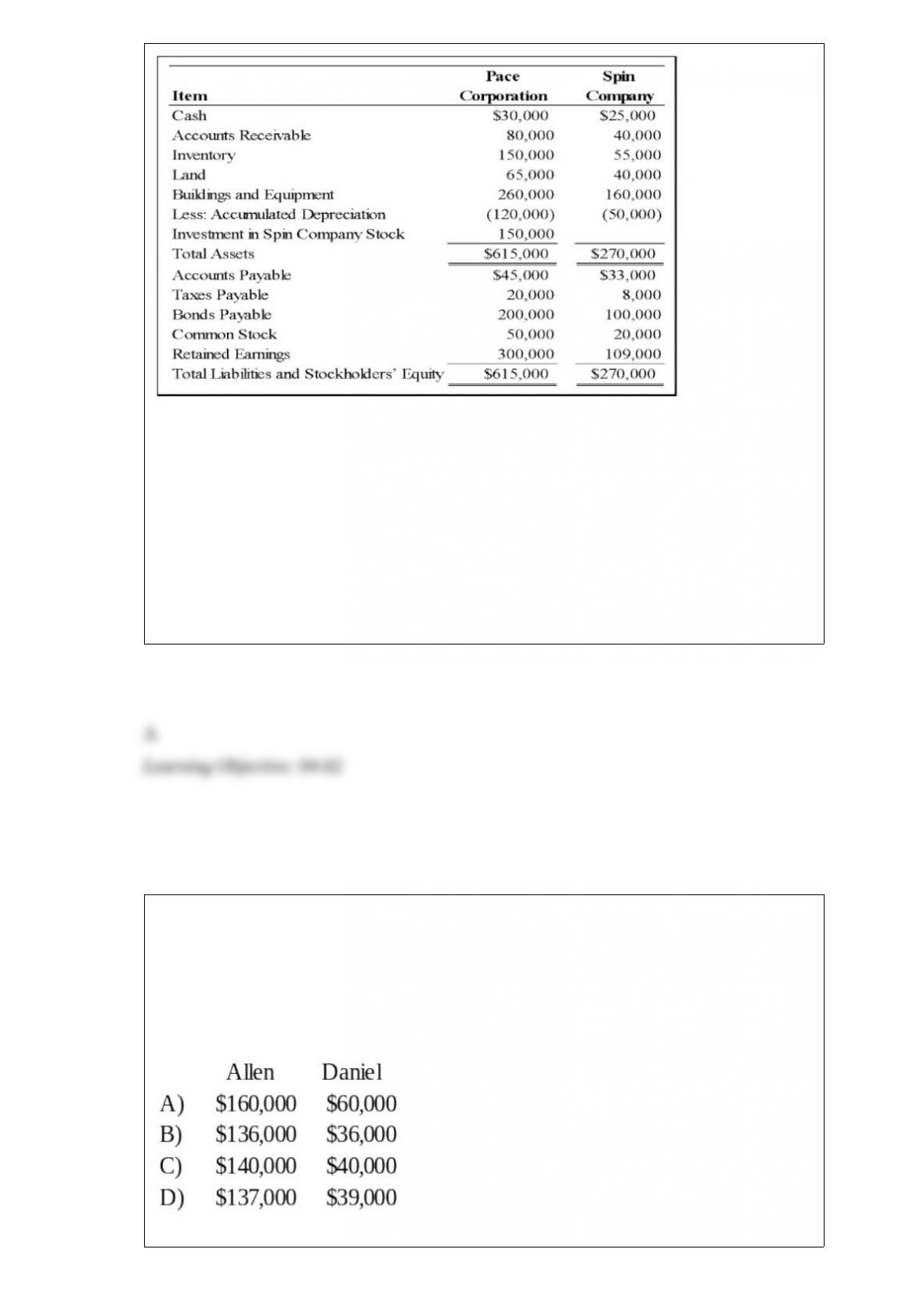

Pace Corporation acquired 100 percent of Spin Company’s common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what amount of retained earnings will be reported

in the consolidated balance sheet prepared immediately after the business combination?

A. $300,000

B. $409,000

C. $259,000

D. $191,000

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. David invests $40,000 for a one-fifth interest

in the total capital of $220,000. What are the capital balances of Allen and Daniel after

David is admitted into the partnership?

A. Option A

B. Option B

C. Option C

D. Option D

Xing Corporation owns 80 percent of the voting common shares of Adams Corporation.

Noncontrolling interest was assigned $24,000 of income in the 20X9 consolidated

income statement. What amount of net income did Adams Corporation report for the

year?

A. $150,000

B. $96,000

C. $120,000

D. $30,000

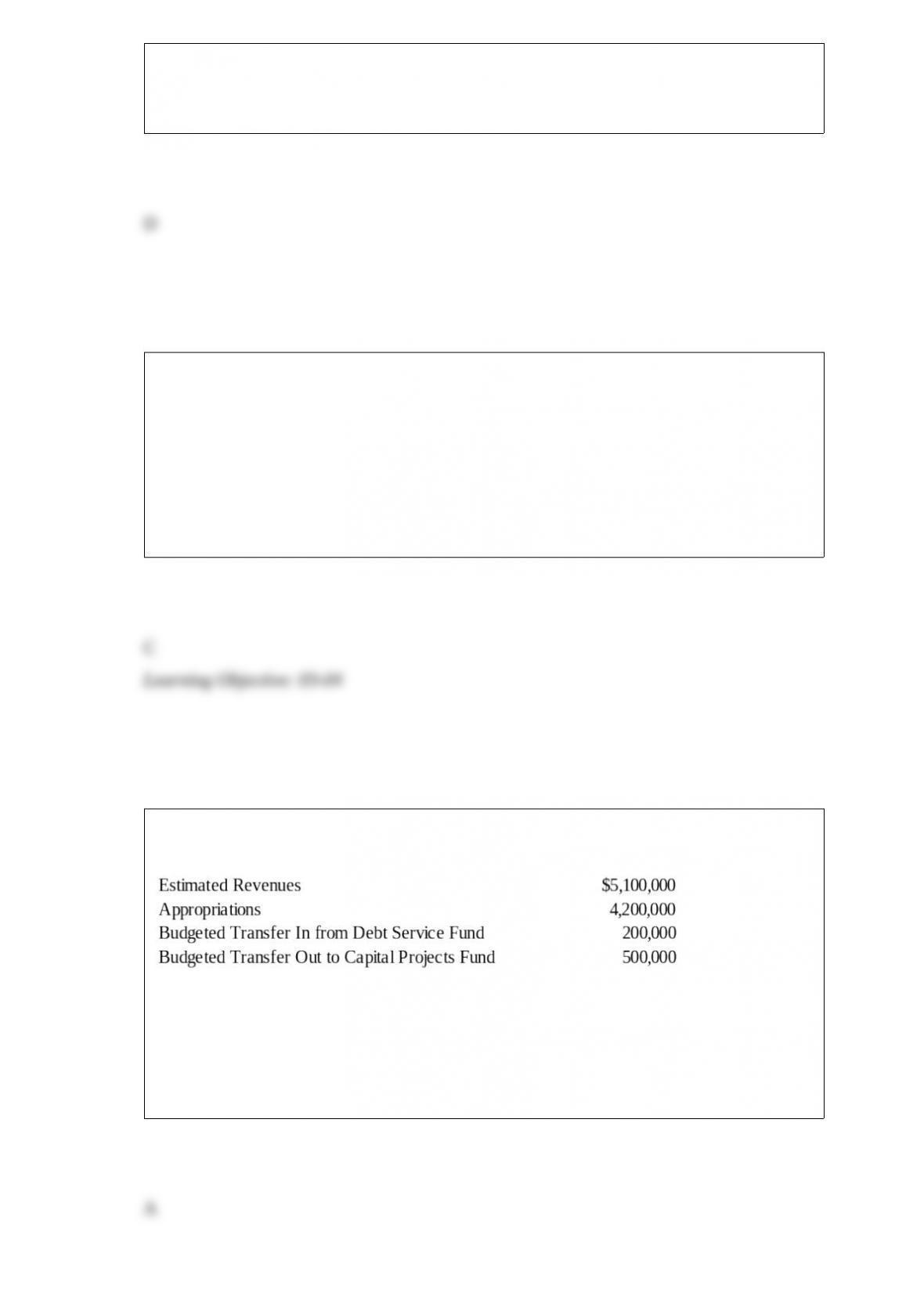

The general fund of Caldwell had the following operating budget for the fiscal year

beginning July 1, 20X9:

When the general fund records its operating budget on July 1, 20X9, Budgetary Fund

Balance—Unassigned should be

A. credited for $600,000.

B. debited for $900,000.

C. debited for $600,000.

D. credited for $900,000.

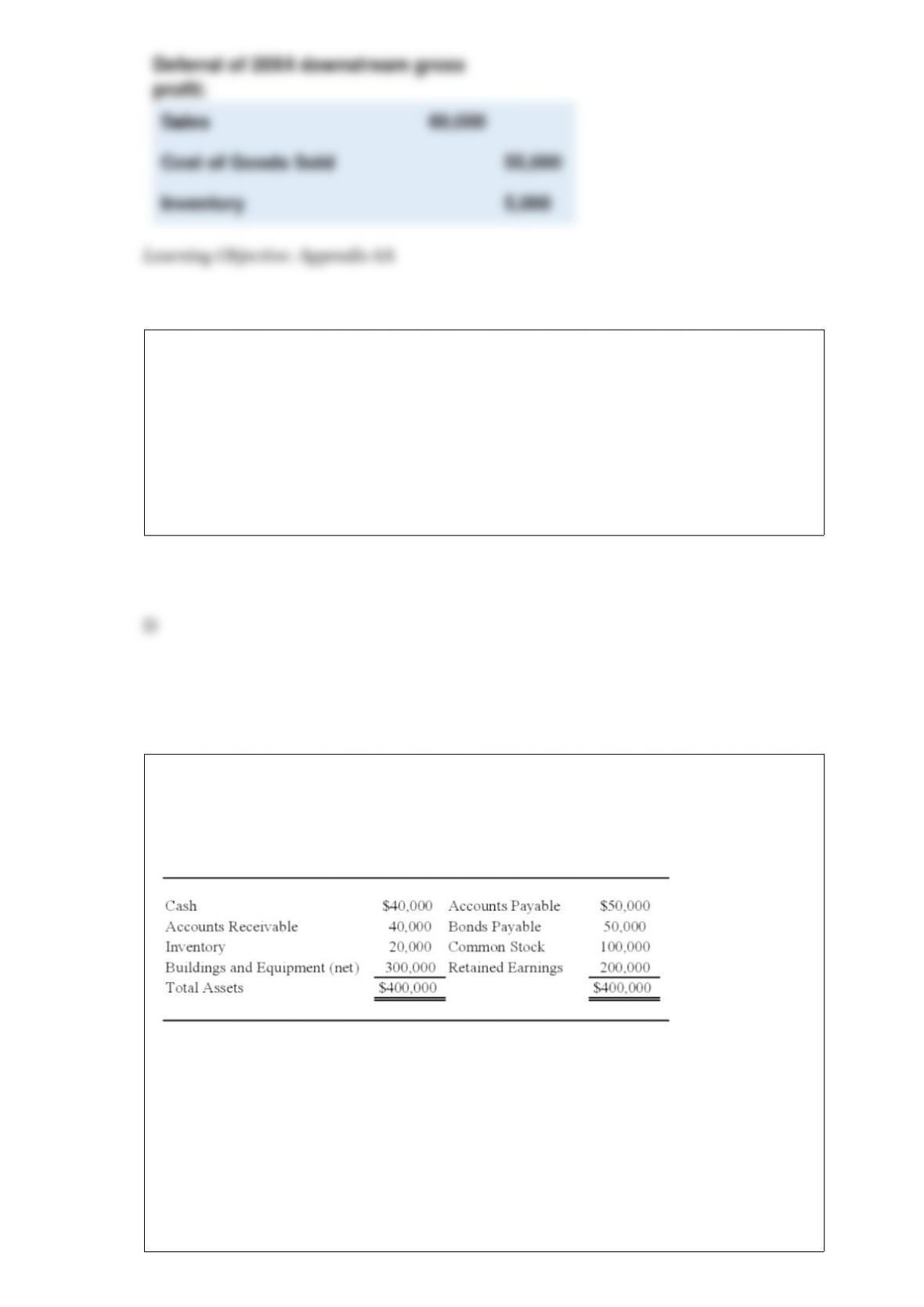

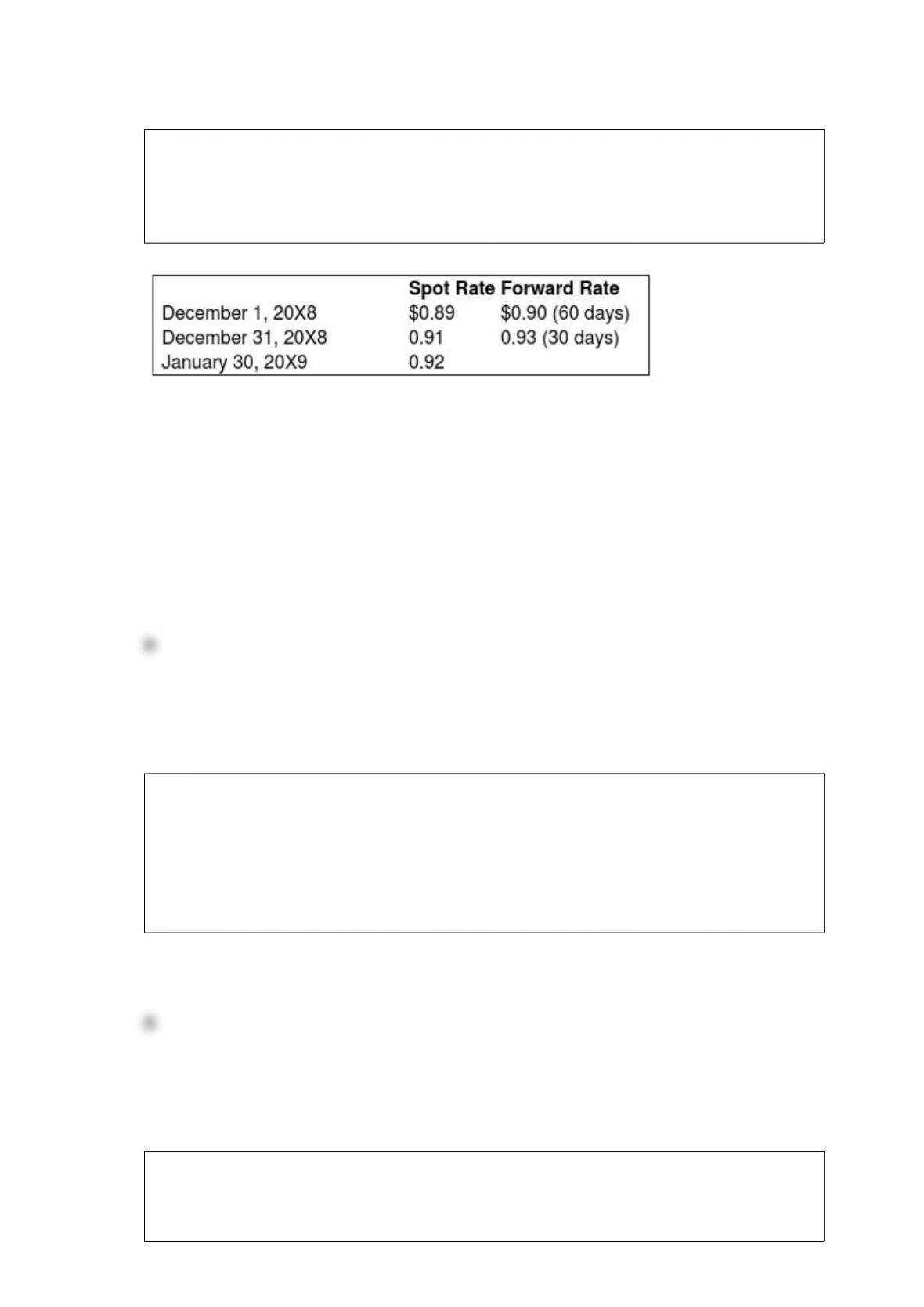

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr)

on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the

company also entered into a 60-day forward contract to purchase 100,000 Swiss francs.

The forward contract is not designated as a hedge. The rates were as follows:

Based on the preceding information, the entries on December 31, 20X8, include a:

A. Credit to Foreign Currency Payable to Exchange Broker, $4,000.

B. Debit to Foreign Currency Receivable from Exchange Broker, $6,000.

C. Debit to Foreign Currency Receivable from Exchange Broker, $186,000.

D. Debit to Foreign Currency Transaction Gain, $4,000.

Which of the following items are likely to be reported in the supplementary items

section of a statement of realization and liquidation?

A. Creditors’ claims settled during the period.

B. Trustee’s administration fees.

C. New obligations incurred by the trustee.

D. Assets subsequently acquired by the trustee.

Which of the following funds provides goods and services only to other departments or

agencies of the government on a cost-reimbursement basis?

A. Internal service funds

B. Enterprise funds

C. Special revenue funds

D. The general fund

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units

from its LIFO-base inventory, which had originally cost $35 per unit. The replacement

cost is expected to be $45 per unit. The company is planning to reduce its inventory and

expects to replace only 1,500 of these units by December 31, the end of its fiscal year.

The company replaced 1,500 units in November at an actual cost of $50 per unit.

Based on the preceding information, in the entry to record the replacement of the 1,500

units in November, Accounts Payable will be credited for:

A. $67,500.

B. $75,000.

C. $62,500.

D. $60,000.

Phips Co. purchases 100 percent of Sips Company on January 1, 20X2, when Phips’

retained earnings balance is $320,000 and Sips’ is $120,000. During 20X2, Sips reports

$20,000 of net income and declares $8,000 of dividends. Phips reports $125,000 of

separate operating earnings plus $20,000 of equity-method income from its 100 percent

interest in Sips; Phips declares dividends of $35,000.

Based on the preceding information, what is the consolidated retained earnings balance

on December 31, 20X2?

A. $402,000

B. $410,000

C. $430,000

D. $562,000

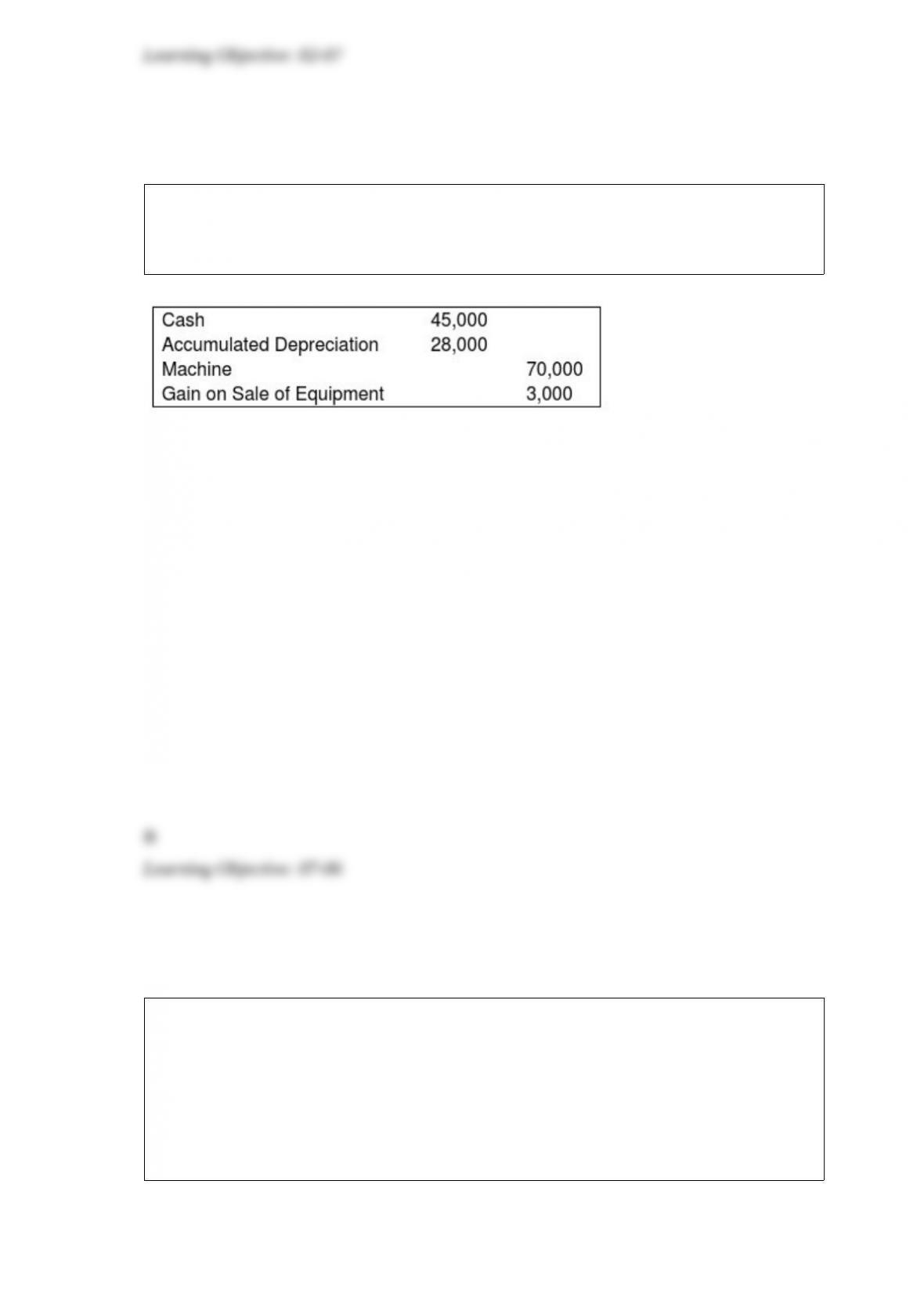

On January 1, 20X7, Servant Company purchased a machine with an expected

economic life of five years. On January 1, 20X9, Servant sold the machine to Master

Corporation and recorded the following entry:

Master Corporation holds 75 percent of Servant’s voting shares. Servant reported net

income of $50,000, and Master reported income from its own operations of $100,000 for

20X9. There is no change in the estimated economic life of the equipment as a result of the

intercorporate transfer.

Based on the preceding information, in the preparation of the 20X9 consolidated income

statement, depreciation expense will be:

A. Debited for $1,000 in the consolidating entries.

B. Credited for $1,000 in the consolidating entries.

C. Debited for $15,000 in the consolidating entries.

D. Credited for $15,000 in the consolidating entries.

In accordance with ASC 958, pledges, which are temporarily restricted by donors, are

reported as increases in temporarily restricted net assets on the statement of activities of

a voluntary health and welfare organization when the

A. pledges are received in cash.

B. cash received from the pledges is expended in accordance with the donors’ wishes.

C. pledges are made by the donors.

D. cash is received from the pledges is transferred to unrestricted net assets.

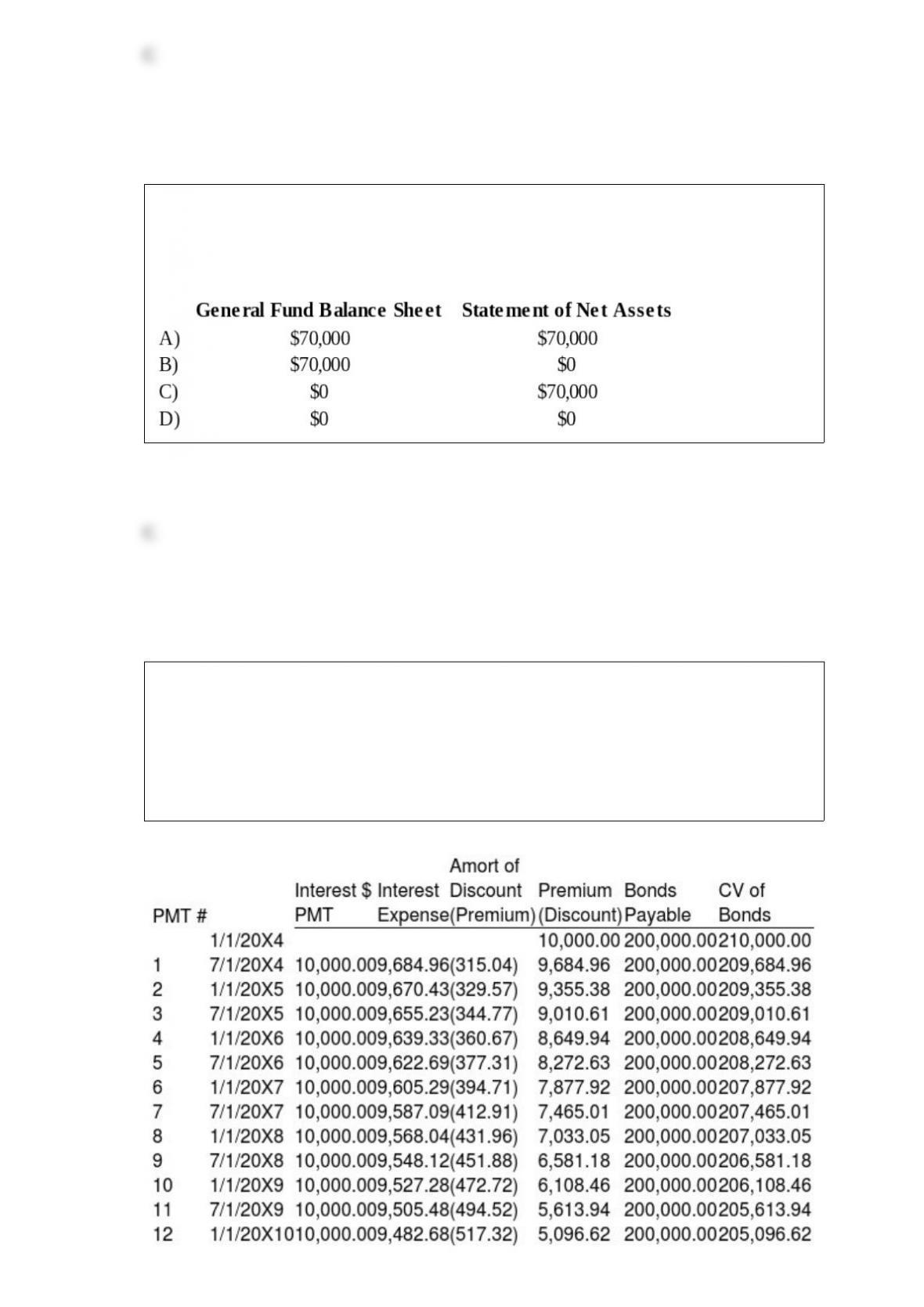

The general fund of Reston acquired computer equipment costing $70,000 during the

fiscal year ended June 30, 20X9. Machinery and Equipment should be reported in

Reston’s General Fund Balance Sheet and government-wide Statement of Net Assets at

June 30, 20X9, as follows:

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on December 31, 20X8, for $125,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of interest expense will be eliminated

in the preparation of the December 31, 20X9 consolidated financial statements?

A. $13,292

B. $18,988

C. $16,296

D. $9,483

On January 1, 20X9, Gold Rush Company acquires 80 percent ownership in California

Corporation for $200,000. The fair value of the noncontrolling interest at that time is

determined to be $50,000. It reports net assets with a book value of $200,000 and fair

value of $230,000. Gold Rush Company reports net assets with a book value of

$600,000 and a fair value of $650,000 at that time, excluding its investment in

California. What will be the amount of goodwill that would be reported immediately

after the combination under current accounting practice?

A. $50,000

B. $30,000

C. $40,000

D. $20,000

ABC, a holder of a $400,000 XYZ Inc. bond, collected the interest due on June 30,

20X8, and then sold the bond to DEF Inc. for $365,000. On that date the bond issuer,

XYZ, a 90 percent owner of DEF, had a $450,000 carrying amount for this bond.

Based on the information given above, what amount of gain or loss on bond retirement

was recorded?

A. No gain or loss

B. $85,000 gain

C. $85,000 loss

D. $35,000 loss

Which presentation method combines the component unit’s results into the primary

government’s financial results?

A. Blended presentation

B. Discrete presentation

C. Combined presentation

D. Consolidated presentation

When is a partnership considered to be insolvent?

I. When the total of all partners’ capital accounts results in a debit balance.

II. When at least one of the partners is personally insolvent.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

On December 31, 20X1, Oak Corporation acquired 100 percent ownership of Cherry

Corporation. On that date, Cherry reported assets and liabilities with books values of

$450,000 and $200,000, respectively, common stock outstanding of $150,000, and

retained earnings of $100,000. The book values and fair values of Cherry’s assets and

liabilities were identical except for land which had increased in value by $15,000 and

inventories which had decreased by $5,000.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet on the acquisition date if the acquisition price was

$240,000?

A. $35,000

B. $30,000

C. $20,000

D. $0

In which of the following ways can debt be restructured?

I. Assets can be transferred to the creditor.

II. An equity interest can be granted to the creditor.

III. The terms of the debt can be modified.

A. I and II only

B. I and III only

C. II and III only

D. I, II, and III

Based on the information given above, in the preparation of the 20X3 consolidated

financial statements, premium on bonds payable will be

A. credited for $95,766 in the consolidation entries.

B. debited for $95,766 in the consolidation entries.

C. credited for $100,784 in the consolidation entries.

D. debited for $100,784 in the consolidation entries.

On September 1, 20X1, Bain Corp. received an order for equipment from a foreign

customer for 300,000 local currency units (LCU) when the U.S. dollar equivalent was

$96,000. Bain shipped the equipment on October 15, 20X1, and billed the customer for

300,000 LCU when the U.S. dollar equivalent was $100,000. Bain received the

customer’s remittance in full on November 16, 20X1, and sold the 300,000 LCU for

$105,000. In its income statement for the year ended December 31, 20X1, Bain should

report a foreign exchange gain of

A. $9,000

B. $4,000

C. $0

D. $5,000

A voluntary health and welfare organization received $200,000 of pledges from donors

on February 15, 20X9. The donors did not place either time or use restrictions on the

amount pledged. The governing board estimated that 10 percent of the pledges would

be uncollectible. During the remainder of fiscal 20X9, cash received from pledges

amounted to $184,000. For the year ended June 30, 20X9, what amount should the

voluntary health and welfare organization report as Contributions-Unrestricted?

A. $0

B. $200,000

C. $184,000

D. $180,000

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount of total liabilities will be reported in

the consolidated balance sheet prepared immediately after the business combination?

A. $190,000

B. $230,000

C. $240,000

D. $440,000