Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 01 - Intercorporate Acquisitions and Investments in Other Entities

E1-2 Multiple-Choice Questions on Recording Business Combinations

[AICPA Adapted]

1. a – The excess sum of the consideration given over the sum of the fair value of identifiable

assets less liabilities equals goodwill.

(b) Incorrect. Assets considered only need be identifiable, not just tangible. For example,

patents would be identifiable, but not tangible.

(c) Incorrect. Assets considered only have to be identifiable. This includes both tangible

and intangible identifiable assets.

(d) Incorrect. The calculation of goodwill requires a remeasurement of the assets and

liabilities at fair value, not book value.

Chapter 01 - Intercorporate Acquisitions and Investments in Other Entities

E1-3 Multiple-Choice Questions on Reported Balances [AICPA Adapted]

1. d – $2,900,000. New APIC Balance = existing APIC on Poe’s books + APIC from new stock

issuance. (200,000*($18-$10) + $1,300,000 = $2,900,000)

E1-4 Multiple-Choice Questions Involving Account Balances

1. c – When the parent creates the subsidiary, the equipment is transferred at cost with the

accompanying accumulated depreciation (which in effect is the book value).

($100,000/10 = $10,000 per year * 4 = $40,000.)

(a) Incorrect. When a subsidiary is created internally, the assets are transferred as they

were on the parent’s books (carrying value). Fair value is not considered.

(b) Incorrect. This is the proper carrying value of the asset, but it should be recorded at

cost with the accompanying accumulated depreciation.

(d) Incorrect. When a subsidiary is created internally, the assets are transferred as they

were on the parent’s books (carrying value).

E1-5 Asset Transfer to Subsidiary

a. Journal entry recorded by Pale Company for transfer of assets to Bright Company:

Investment in Bright Company Common Stock

408,000

Accumulated Depreciation – Buildings

24,000

Accumulated Depreciation – Equipment

36,000

Cash

21,000

Inventory

37,000

Land

80,000

Buildings

240,000

Equipment

90,000

b. Journal entry recorded by Bright Company for receipt of assets from Pale Company:

Cash

21,000

Inventory

37,000

Land

80,000

Buildings

240,000

Equipment

90,000

Accumulated Depreciation – Buildings

24,000

Accumulated Depreciation – Equipment

36,000

Common Stock

60,000

Additional Paid-In Capital

348,000

E1-6 Creation of New Subsidiary

a. Journal entry recorded by Lester Company for transfer of assets to Mumby Corporation:

Investment in Mumby Corporation Common Stock

498,000

Allowance for Uncollectible Accounts Receivable

7,000

Accumulated Depreciation – Buildings

35,000

Accumulated Depreciation – Equipment

60,000

Cash

40,000

Accounts Receivable

75,000

Inventory

50,000

Land

35,000

Buildings

160,000

Equipment

240,000

b. Journal entry recorded by Mumby Corporation for receipt of assets from Lester Company:

Cash

40,000

Accounts Receivable

75,000

Inventory

50,000

Land

35,000

Buildings

160,000

Equipment

240,000

Allowance for Uncollectible

Accounts Receivable

7,000

Accumulated Depreciation – Buildings

35,000

Accumulated Depreciation – Equipment

60,000

Common Stock

120,000

Additional Paid-In Capital

378,000

E1-7 Balance Sheet Totals of Parent Company

a. Journal entry recorded by Foster Corporation for transfer of assets and accounts payable to

Kline Company:

Investment in Kline Company Common Stock

66,000

Accumulated Depreciation

28,000

Accounts Payable

22,000

Cash

15,000

Accounts Receivable

24,000

Inventory

9,000

Land

3,000

Depreciable Assets

65,000

b. Journal entry recorded by Kline Company for receipt of assets and accounts payable from

Foster Corporation:

Cash

15,000

Accounts Receivable

24,000

Inventory

9,000

Land

3,000

Depreciable Assets

65,000

Accumulated Depreciation

28,000

Accounts Payable

22,000

Common Stock

48,000

Additional Paid-In Capital

18,000

E1-8 Acquisition of Net Assets

Sun Corporation will record the following journal entries:

(1)

Assets

71,000

Goodwill

9,000

Liabilities

20,000

Cash

60,000

(2)

Merger Expense

4,000

Cash

4,000

E1-9 Reporting Goodwill

a. Goodwill: $120,000 = $310,000 - $190,000

E1-10 Stock Acquisition

Journal entry to record the purchase of Tippy Inc., shares:

Investment in Tippy Inc., Common Stock

986,000

Common Stock

425,000

Additional Paid-In Capital

561,000

$986,000 = $58 x 17,000 shares

$425,000 = $25 x 17,000 shares

$561,000 = ($58 - $25) x 17,000 shares

Chapter 01 - Intercorporate Acquisitions and Investments in Other Entities

E1-11 Balances Reported Following Combination

a.

Stock Outstanding: $200,000 + ($10 x 8,000 shares)

$280,000

b.

Cash and Receivables: $150,000 + $40,000

190,000

c.

Land: $100,000 + $85,000

185,000

d.

Buildings and Equipment (net): $300,000 + $230,000

530,000

e.

Goodwill: ($50 x 8,000) - $355,000

45,000

f.

Additional Paid-In Capital:

$20,000 + [($50 - $10) x 8,000]

340,000

g.

Retained Earnings

330,000

E1-12 Goodwill Recognition

Journal entry to record acquisition of Spur Corporation net assets:

Cash and Receivables

40,000

Inventory

150,000

Land

30,000

Plant and Equipment

350,000

Patent

130,000

Goodwill

55,000

Accounts Payable

85,000

Cash

670,000

Computation of goodwill

Fair value of consideration given

$670,000

Fair value of assets acquired

$700,000

Fair value of liabilities assumed

(85,000)

Fair value of net assets acquired

615,000

Goodwill

$ 55,000

Chapter 01 - Intercorporate Acquisitions and Investments in Other Entities

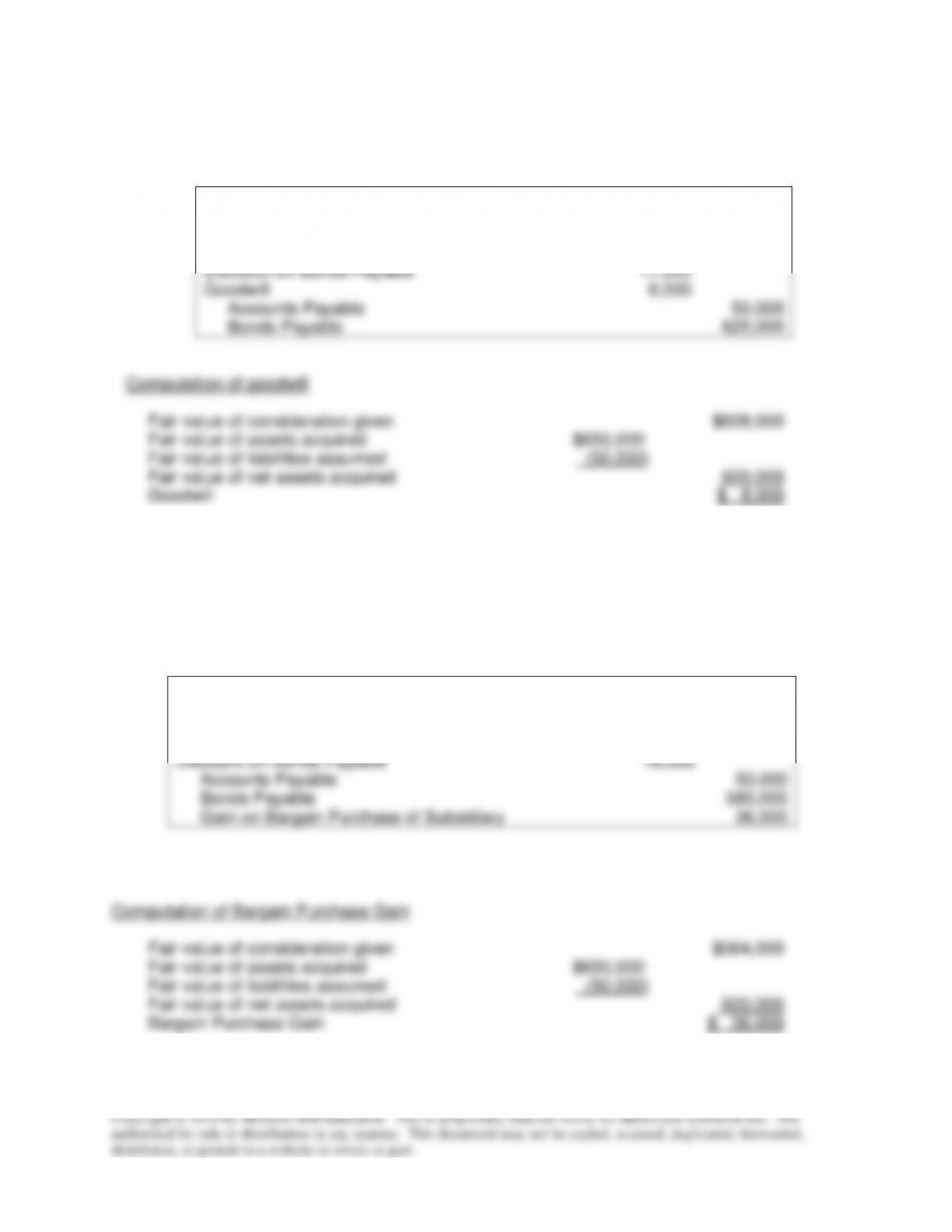

E1-13 Acquisition Using Debentures

Journal entry to record acquisition of Sorden Company net assets:

Cash and Receivables

50,000

Inventory

200,000

Land

100,000

Plant and Equipment

300,000

Discount on Bonds Payable

17,000

Goodwill

8,000

Accounts Payable

50,000

Bonds Payable

625,000

Computation of goodwill

Fair value of consideration given

$608,000

Fair value of assets acquired

$650,000

Fair value of liabilities assumed

(50,000)

Fair value of net assets acquired

600,000

Goodwill

$ 8,000

E1-14 Bargain Purchase

Journal entry to record acquisition of Sorden Company net assets:

Cash and Receivables

50,000

Inventory

200,000

Land

100,000

Plant and Equipment

300,000

Discount on Bonds Payable

16,000

Accounts Payable

50,000

Bonds Payable

580,000

Gain on Bargain Purchase of Subsidiary

36,000

Fair value of consideration given

$564,000

Fair value of assets acquired

$650,000

Fair value of liabilities assumed

(50,000)

Fair value of net assets acquired

600,000

Bargain Purchase Gain

$ 36,000

E1-15 Impairment of Goodwill

a. Goodwill of $80,000 will be reported. The fair value of the reporting unit ($340,000) is

greater than the carrying amount of the investment ($290,000) and the goodwill

E1-16 Assignment of Goodwill

a. No impairment loss will be recognized. The fair value of the reporting unit ($530,000) is

greater than the carrying value of the investment ($500,000) and goodwill does not

E1-17 Goodwill Assigned to Reporting Units

Goodwill of $158,000 ($60,000 + $48,000 + $0 + $50,000) should be reported, computed

as follows:

Reporting Unit A: Goodwill of $60,000 should be reported. The implied value of

E1-18 Goodwill Measurement

a. Goodwill of $150,000 will be reported. The fair value of the reporting unit ($580,000) is

greater than the carrying value of the investment ($550,000) and goodwill does not

need to be tested for impairment. No loss will be recorded.

E1-19 Computation of Fair Value

Amount paid

$517,000

Book value of assets

$624,000

Book value of liabilities

(356,000)

Book value of net assets

$268,000

Adjustment for research and development costs

(40,000)

Adjusted book value

$228,000

Fair value of patent rights

120,000

Goodwill recorded

93,000

(441,000)

Fair value increment of buildings and equipment

$ 76,000

Book value of buildings and equipment

341,000

Fair value of buildings and equipment

$417,000