Patch Corporation purchased land from Sub1 Corporation for $350,000 on December 3,

20X5. This purchase followed a series of transactions between Patch-controlled

subsidiaries. On January 23, 20X5, Sub3 Corporation purchased the land from a

nonaffiliate for $240,000. It sold the land to Sub2 Company for $220,000 on July 15,

20X5, and Sub2 sold the land to Sub1 for $305,000 on September 5, 20X5. Patch has

control of the following companies:

Subsidiary Level of Ownership 20X5 Net Income

Sub3 60 percent $60,000

Sub2 90 percent $140,000

Sub1 70 percent $90,000

Patch reported income from its separate operations of $345,000 for 20X5.

Based on the preceding information, what should be the amount of income assigned to

the controlling shareholders in the consolidated income statement for 20X5?

A. $110,000

B. $474,000

C. $525,000

D. $635,000

The following information pertains to property taxes levied by Sycamore City for

20X7:

Collections during 20X7 $1,200,000

Expected collections during the first 60 days of 20X8 200,000

Expected collections during the balance of 20X8 110,000

Expected collections during January 20X9 40,000

Estimated to be uncollectible 30,000

Total levy $1,580,000

What amount should Sycamore report for 20X7 net property tax revenues?

A. $1,200,000

B. $1,400,000

C. $1,550,000

D. $1,580,000

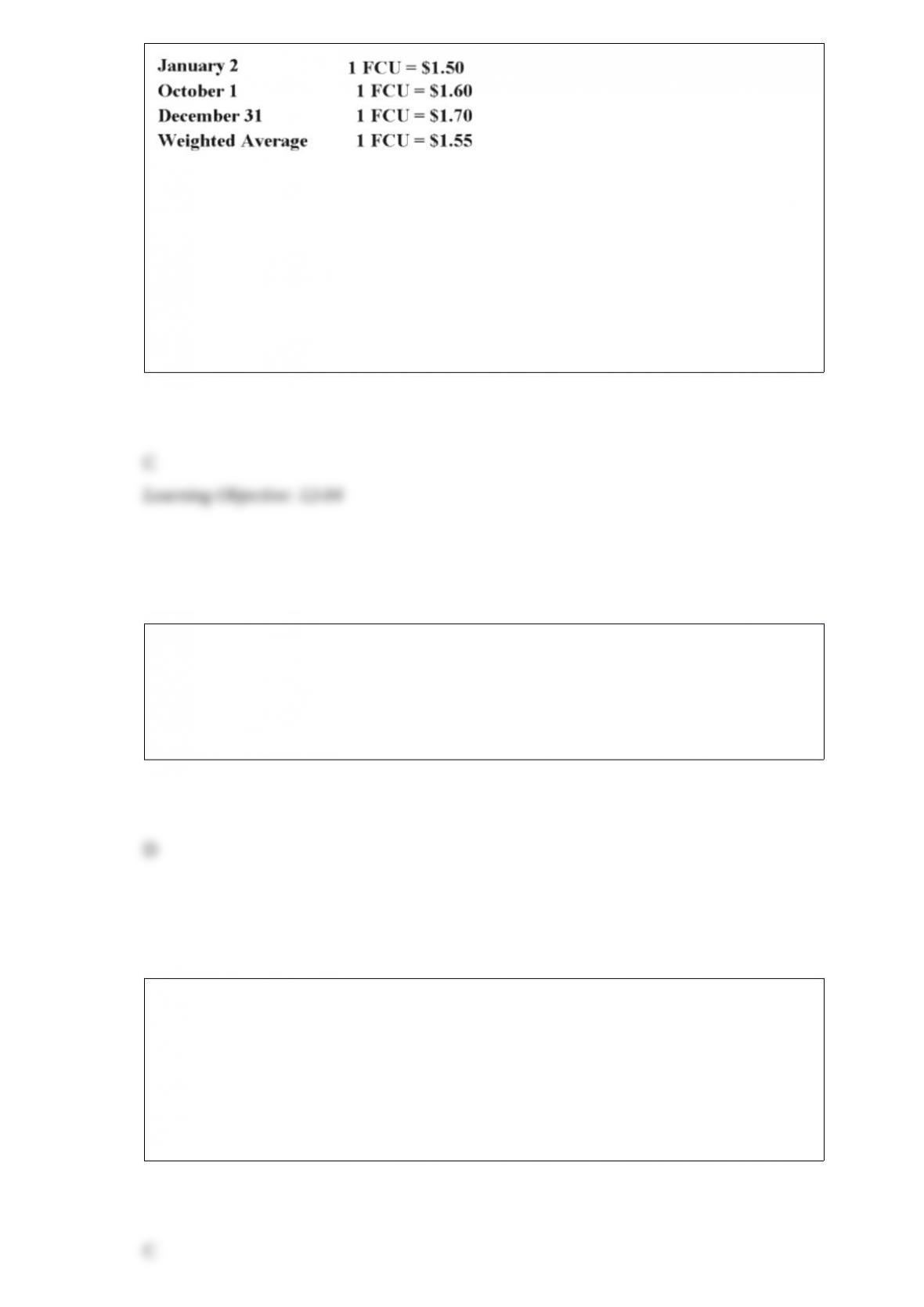

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming Perth’s local currency is the functional

currency, what is the amount of translation adjustments that result from translating

Perth’s trial balance into U.S. dollars at December 31, 20X8?

A. $396,500 debit

B. $285,000 credit

C. $405,000 credit

D. $411,000 credit

Which of the following observations is true of futures contracts?

A. Contracted through a dealer, usually a bank.

B. Customized to meet contracting company’s terms and needs.

C. Typically no margin deposit required.

D. Traded on an exchange and acquired through an exchange broker

Unrestricted gifts and endowment income of a private university are reported as

A. increases in the unrestricted current fund balance on the statement of changes in fund

balances.

B. unrestricted revenues on the statement of current funds revenues, expenditures, and

other changes.

C. unrestricted revenues on the statement of activities.

D. increases in the unrestricted current fund balance on the statement of activities.

Samuel Corporation foresees a downturn in its business in the medium term. It expects

to sustain an operating loss of $160,000 for the full year ending December 31, 20X8.

Samuel’s tax rate is 35 percent. Anticipated tax credits for 20X8 total $8,000. No

permanent differences are expected. Realization of the full tax benefit of the expected

operating loss and realization of anticipated tax credits are assured beyond any

reasonable doubt because they will be carried back. For the first quarter ended March

31, 20X8, Samuel reported an operating loss of $30,000. How much of a tax benefit

should Samuel report for the interim period ended March 31, 20X8?

A. $8,000

B. $12,000

C. $13,500

D. $15,500

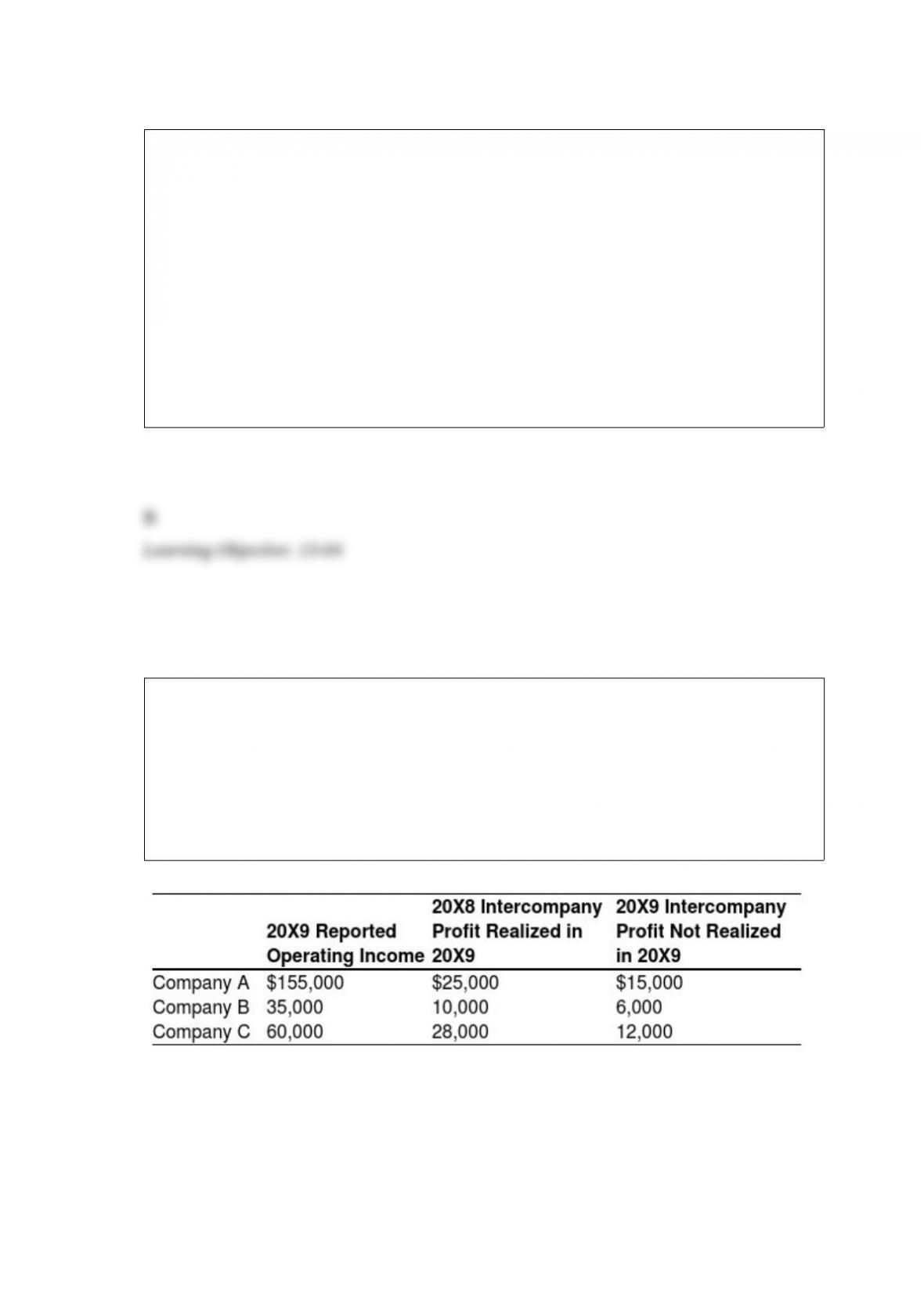

Company A owns 85 percent of Company B’s stock and 80 percent of Company C’s

stock. All acquisitions were made at book value. The fair values of noncontrolling

interests at the time of acquisition were equal to the proportionate share of the book

values of the companies. The companies file a consolidated tax return each year and in

20X9 paid a total tax of $112,000. Each company is involved in a number of

intercompany inventory transfers each period. Information on the companies’ activities

for 20X9 is as follows:

Company A does not record income tax expense on income from subsidiaries because a

consolidated tax return is filed.

Based on the information provided, income to the controlling interest for 20X9 is:

A. $155,370.

B. $56,000.

C. $168,000.

D. $250,000.

On July 1, 20X8, Fair Logic Corporation acquires 75 percent of Integrated Systems Inc.

common stock for its underlying book value. At the time of acquisition, the fair value of

the noncontrolling interest is equal to its proportionate share of book value of Integrated

Systems. On January 1, 20X8 Integrated reported common stock of $100,000 and

retained earnings of $130,000. For the year 20X8, Integrated reports the following

items:

Fair Logic uses the equity method in accounting for this investment.

Based on the preceding information, what is the book value of shares acquired by Fair

Logic on July 1, 20X8?

A. $240,000

B. $191,250

C. $230,000

D. $180,000

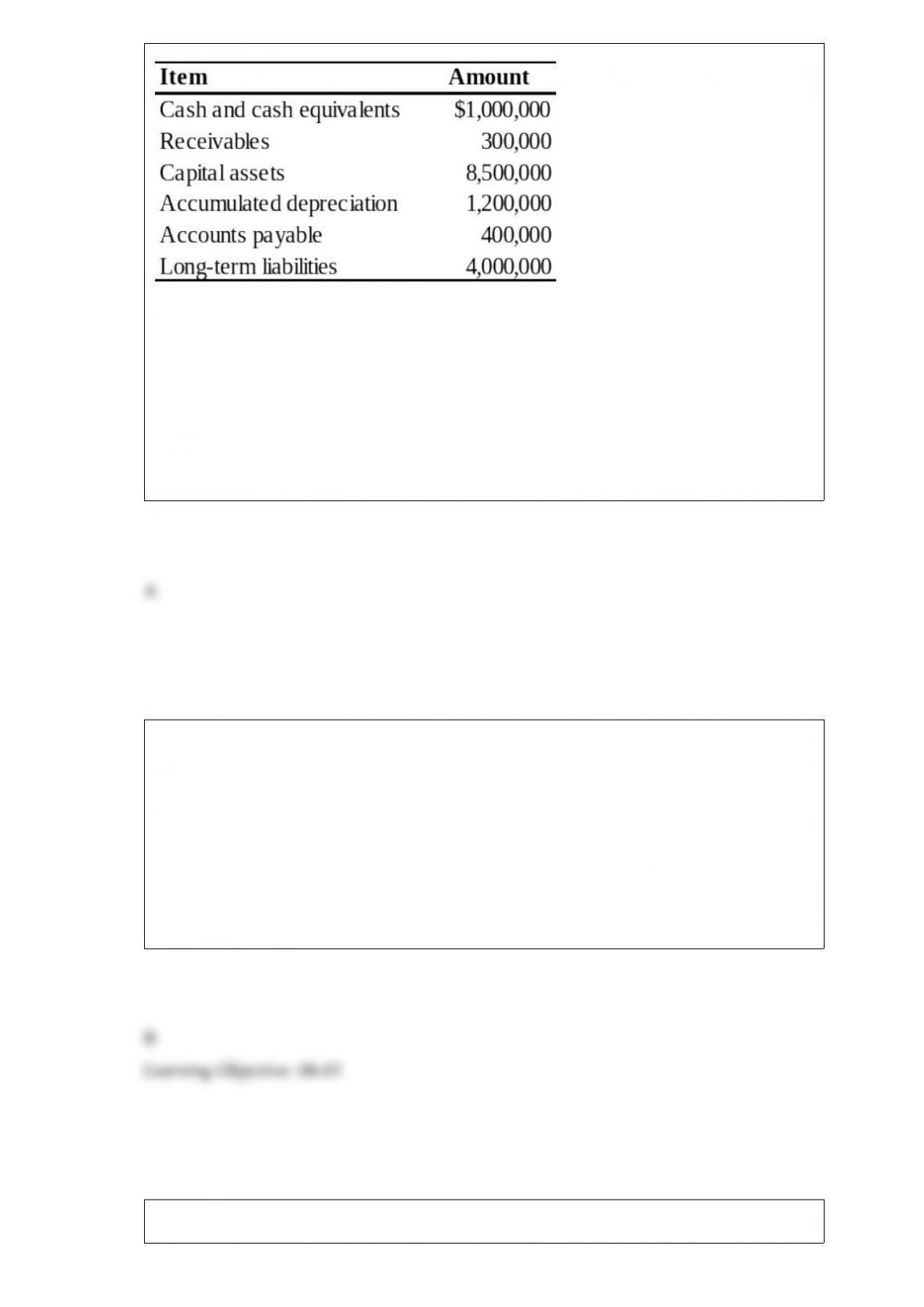

Riviera Township reported the following data for its governmental activities for the year

ended June 30, 20X9:

Additional information available is as follows:

All of the long-term debt was used to acquire capital assets. Cash of $475,000 is

restricted for debt service.

Based on the preceding information, on the statement of net assets prepared at June 30,

20X9, what amount should be reported for net assets, unrestricted?

A. $425,000

B. $900,000

C. $525,000

D. $825,000

During the year a parent makes sales of inventory at a profit to its 75 percent owned

subsidiary. The subsidiary also makes sales of inventory at a profit to its parent during

the same year. Both the parent and the subsidiary have on hand at the end of the year 20

percent of the inventory acquired from one another. Consolidated revenues for the year

should exclude:

A. 80 percent of the total revenues from intercompany sales.

B. total revenues from intercompany sales.

C. only the revenues from the subsidiary’s intercompany sales.

D. only the revenues from the parent’s intercompany sales.

Under the temporal method, which of the following is usually used to translate

monetary amounts to the functional currency?

I. The current exchange rate

II The historical exchange rate

III. Average exchange rate

A. I

B. III

C. II

D. Either I or II

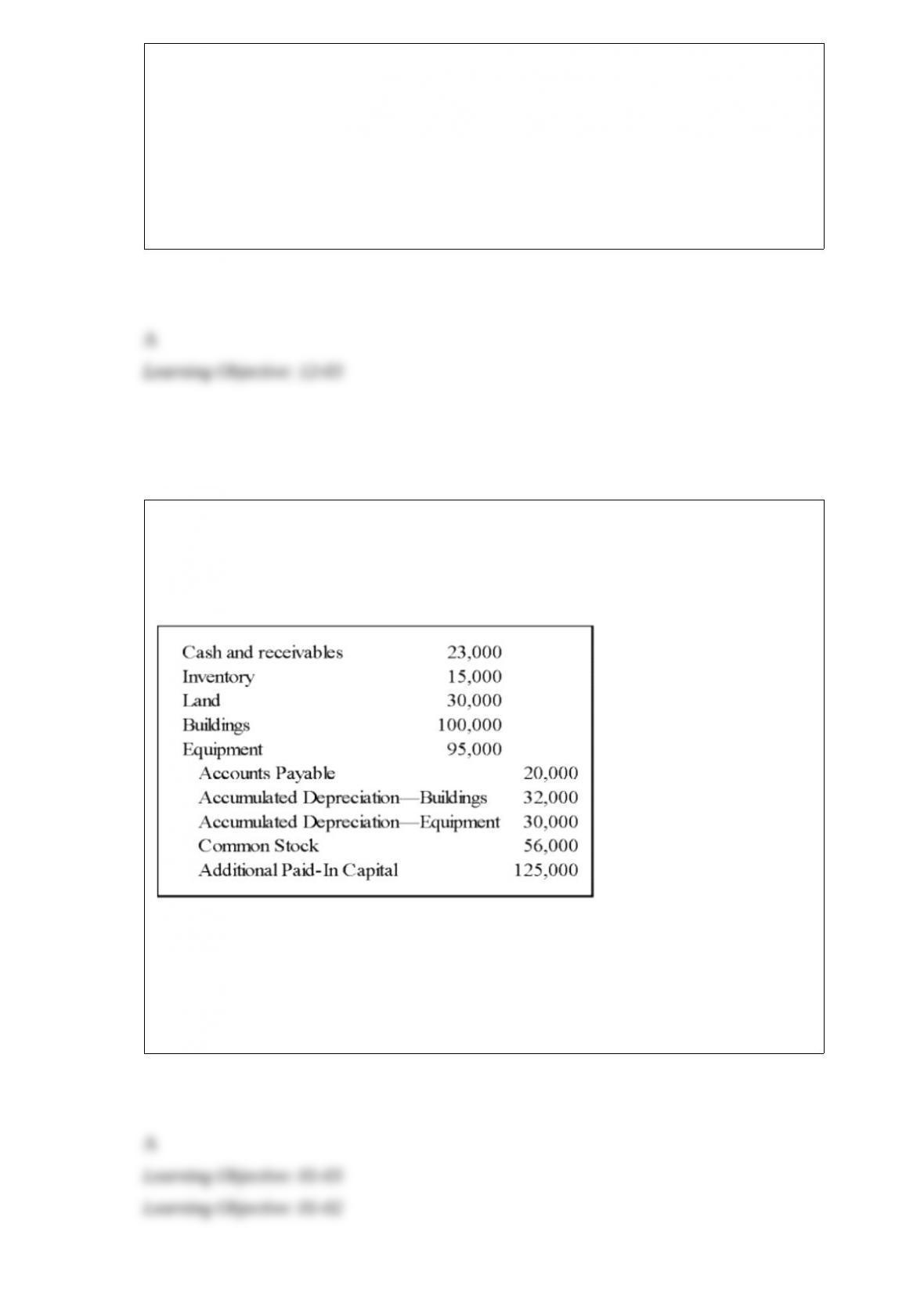

In order to reduce the risk associated with a new line of business, Conservative

Corporation established Spin Company as a wholly owned subsidiary. It transferred

assets and accounts payable to Spin in exchange for its common stock. Spin recorded

the following entry when the transaction occurred:

Based on the preceding information, what amount did Conservative report as its

investment in Spin after the transfer of assets and liabilities?

A. $181,000

B. $221,000

C. $263,000

D. $243,000

Beta Company acquired 100 percent of the voting common shares of Standard Video

Corporation, its bitter rival, by issuing bonds with a par value and fair value of

$150,000. Immediately prior to the acquisition, Beta reported total assets of $500,000,

liabilities of $280,000, and stockholders’ equity of $220,000. At that date, Standard

Video reported total assets of $400,000, liabilities of $250,000, and stockholders’ equity

of $150,000. Included in Standard’s liabilities was an account payable to Beta in the

amount of $20,000, which Beta included in its accounts receivable.

Based on the preceding information, what amount of total liabilities was reported in the

consolidated balance sheet immediately after acquisition?

A. $500,000

B. $530,000

C. $280,000

D. $660,000

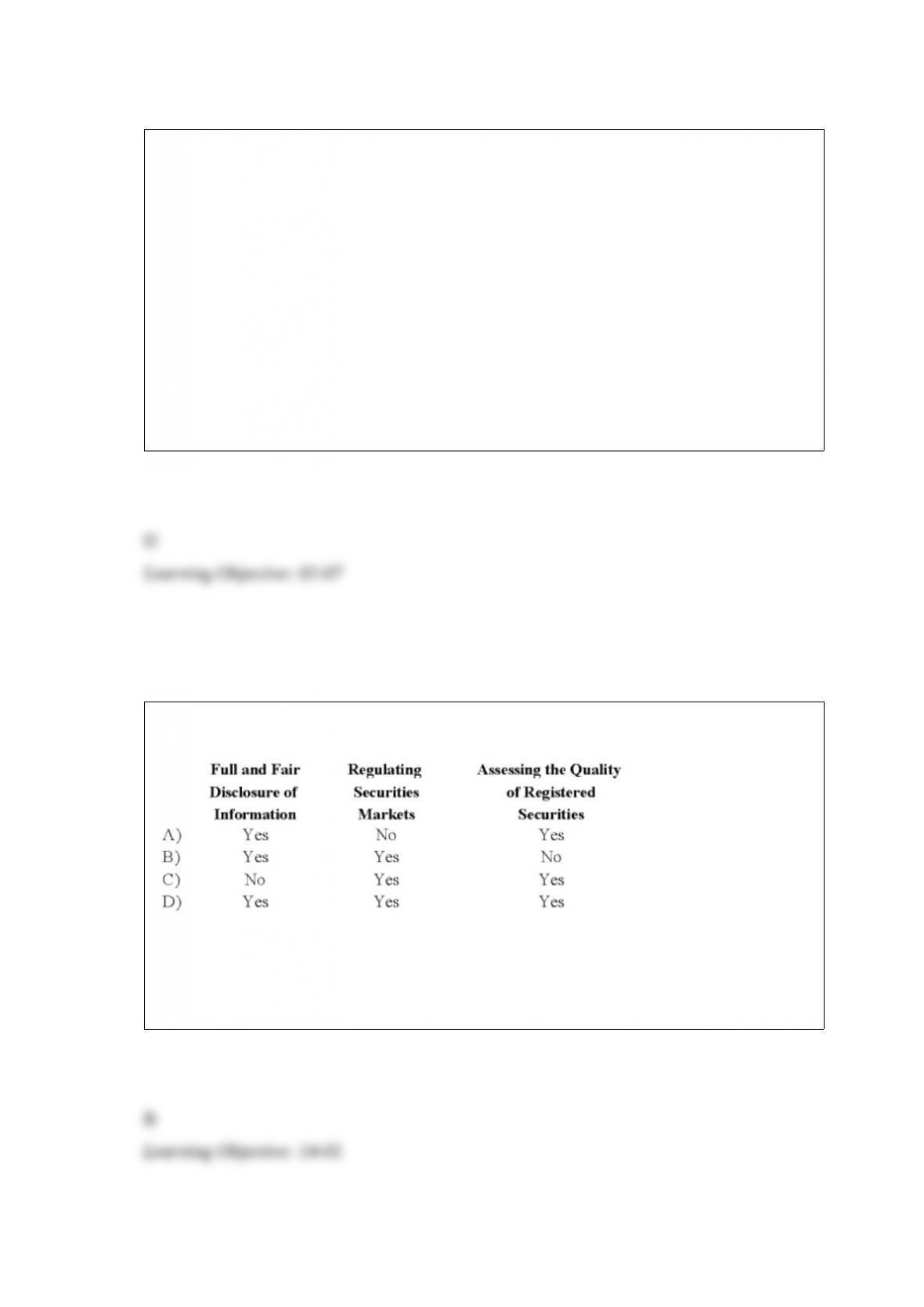

The Securities and Exchange Commission is responsible for:

A. Option A

B. Option B

C. Option C

D. Option D

The following information pertains to property taxes levied by Oak City for 20X4:

Collections during 20X4 $500,000

Expected collections during the first 60 days of 20X5 100,000

Expected collections during the balance of 20X5 60,000

Expected collections during January 20X6 30,000

Estimated to be uncollectible 10,000

Total levy $700,000

What amount should Oak report for 20X4 net property tax revenues?

A. $690,000

B. $700,000

C. $600,000

D. $500,000

Sky Corporation owns 75 percent of Earth Company’s stock. On July 1, 20X8, Sky sold

a building to Earth for $33,000. Sky had purchased this building on January 1, 20X6,

for $36,000. The building’s original eight-year estimated total economic life remains

unchanged. Both companies use straight-line depreciation. The equipment’s residual

value is considered negligible.

Based on the information provided, while preparing the 20X8 consolidated income

statement, depreciation expense will be:

A. debited for $750 in the consolidating entries.

B. credited for $750 in the consolidating entries.

C. credited for $1,500 in the consolidating entries.

D. debited for $1,500 in the consolidating entries.

What portion of the subsidiary stockholders’ equity account balances should be

eliminated in preparing the consolidated balance sheet?

A. Common stock

B. Additional paid-in capital

C. Retained Earnings

D. All of the balances are eliminated

Consolidated net income for a parent and its 80 percent owned subsidiary should be

computed by eliminating:

A. all unrealized profit in downstream intercompany inventory sales, and unrealized

profit in upstream intercompany inventory sales made during the current year.

B. all unrealized profit in downstream intercompany inventory sales, and the

noncontrolling interest’s share of unrealized profit in upstream inventory sales made

during the current year.

C. the controlling interest’s share of unrealized profit in downstream intercompany

sales, and the controlling interest’s share of unrealized profit in upstream sales made

during the current year.

D. all unrealized profit in downstream intercompany sales, and the noncontrolling

interest’s share of unrealized profit in upstream sales made during the current year.

In a university, class cancellation refunds of tuition and fees should be recorded as:

I. a reduction of revenue from tuition and fees.

II. a reduction of accounts receivable.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Infinity Corporation acquired 80 percent of the common stock of an Egyptian company

on January 1, 20X8. The goodwill associated with this acquisition was $18,350.

Exchange rates at various dates during 20X8 follow:

January 1, 20X8 1 E = $0.1835

December 31, 20X8 1 E = 0.1850

Average for 20X8 1 E = 0.1840

Goodwill suffered an impairment of 20 percent during the year. If the functional

currency is the U.S. dollar, how much goodwill impairment loss should be reported on

Infinity’s consolidated statement of income for 20X8?

A. $3,680

B. $3,670

C. $3,690

D. $3,700

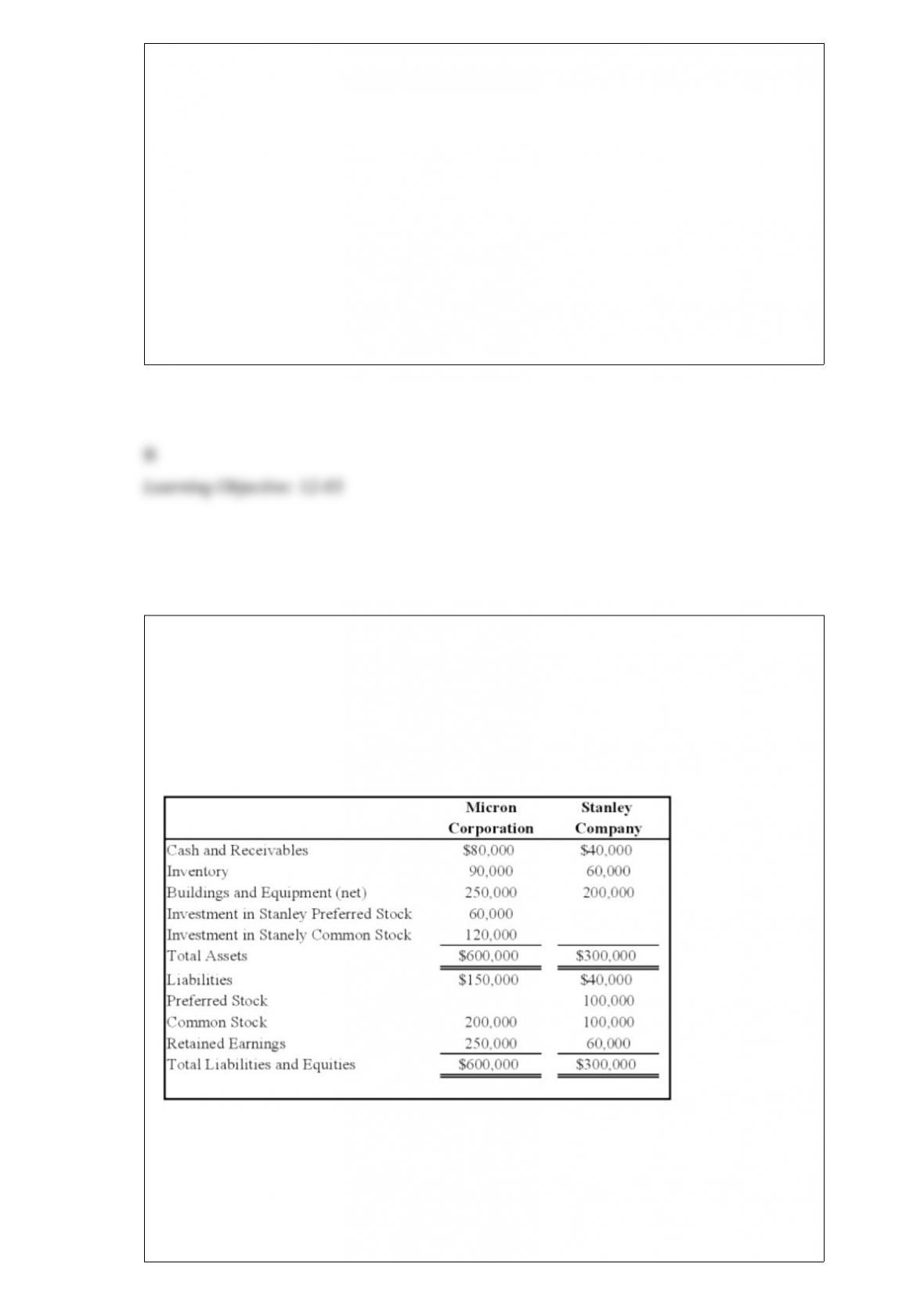

Micron Corporation owns 75 percent of the common shares and 60 percent of the

preferred shares of Stanley Company, all acquired at underlying book value on January

1, 20X8. At that date, the fair value of the noncontrolling interest in Stanley’s common

stock was equal to 25 percent of the book value of its common stock. The balance

sheets of Micron and Stanley immediately after the acquisition contained these

balances:

Stanley’s preferred stock pays a 12 percent dividend and is cumulative. For 20X8,

Stanley reports net income of $40,000 and pays no dividends. Micron reports income

from its separate operations of $75,000 and pays dividends of $30,000 during 20X8.

Based on the preceding information, what amount is reported as preferred stock

outstanding reported in the consolidated balance sheet as of January 1, 20X8?

A. $0

B. $40,000

C. $50,000

D. $44,000

The disclosure, “net assets released from restrictions,” is reported on which of the

following financial statements for a voluntary health and welfare organization?

I. The statement of cash flows.

II. The statement of activities.

A. I only

B. II only

C. Both I and II.

D. Neither I nor II.

A reorganization value in excess of amounts assignable to identifiable assets is:

A. not reported.

B. reported as an intangible asset called Reorganization Value in Excess of Amounts

Allocable to Identifiable Assets.

C. reported as Goodwill Associated with Exit or Disposal Activities.

D. passed on to prior shareholders of the company.

Which of the following types of securities or securities transactions are exempt from the

need to be registered under the Securities Act of 1933?

I. Commercial paper with a maturity of nine months or less.

II. Intrastate issues in which the securities are offered and sold only within one state.

III. Securities exchanged by an issuer exclusively with its existing shareholders with no

commission charged.

A. I and II

B. II

C. I, II, and III

D. III

A change from the cost method to the equity method of accounting for an investment in

common stock resulting from an increase in the number of shares held by the investor

requires:

A. only a footnote disclosure.

B. that the cumulative amount of the change be shown as a line item on the income

statement, net of tax.

C. that the change be accounted for as an unrealized gain included in other

comprehensive income.

D. retroactive restatement as if the investor always had used the equity method.

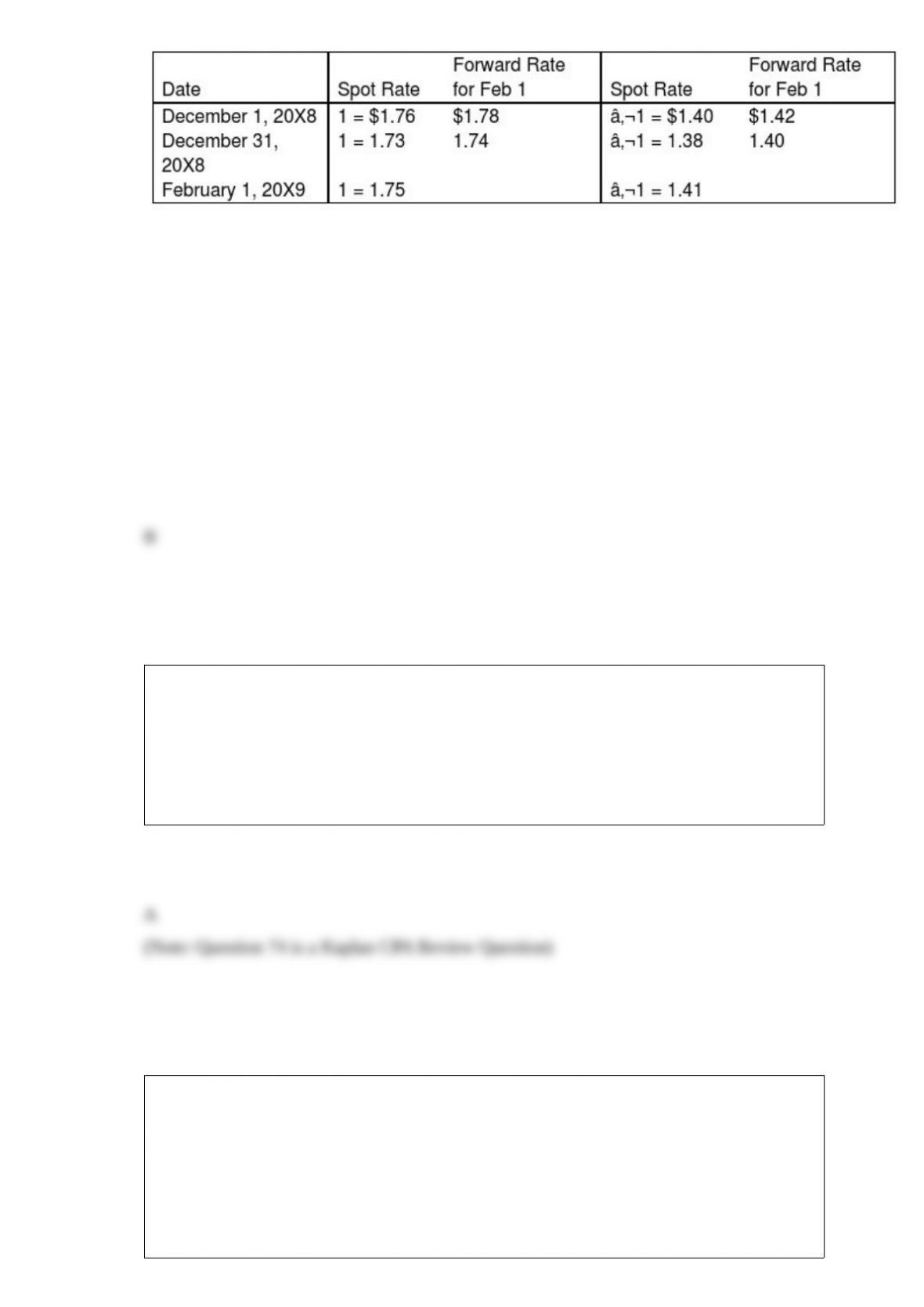

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the effect of the euro speculative contract on

20X9 net income?

A. $4,000 loss

B. $1,000 gain

C. $8,000 gain

D. $2,000 loss

In government-wide statement of activities, special items are transactions or other

events that are:

A. unusual in nature or infrequent in occurrence and within management’s control.

B. unusual in nature or infrequent in occurrence and not within management’s control.

C. unusual in nature and infrequent in occurrence and within management’s control.

D. unusual in nature and infrequent in occurrence.

Berlin, Inc. holds 100 percent of the common stock of Sea Company, an investment

acquired for $520,000. Immediately following the combination, Berlin’s net assets have

a book value of $900,000 and a fair value of $1,050,000. The book and fair value of

Sea’s net assets on the date of combination are $350,000 and $425,000, respectively.

Immediately following the combination, a consolidated balance sheet is prepared.

Based on the information given above, goodwill will be reported at what amount in a

consolidated balance sheet?

A. $170,000

B. $150,000

C. $95,000

D. $75,000

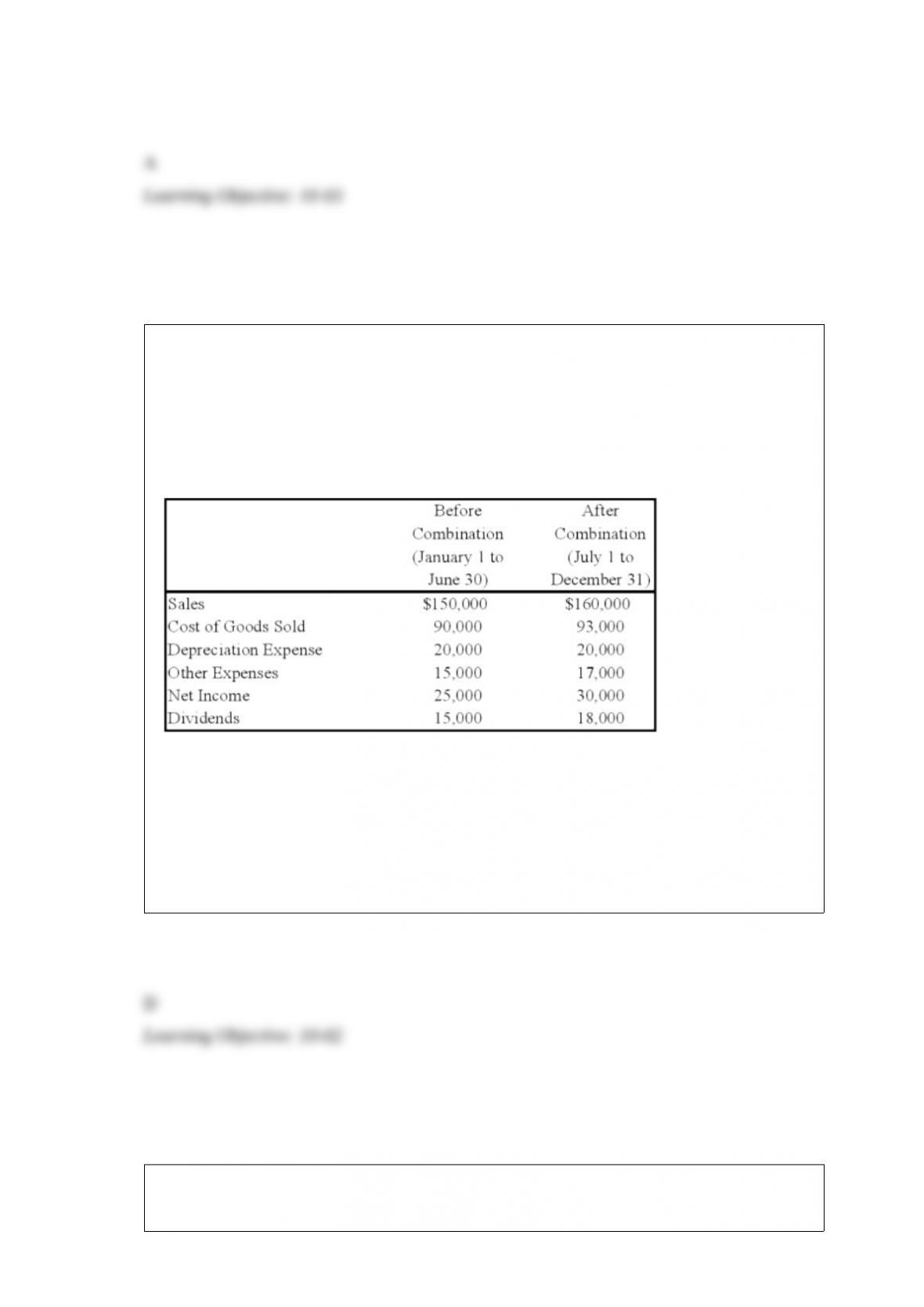

Miguel Corporation and Forest Company merged as of January 1, 20X3. Miguel paid

finder’s fees of $36,000 and legal fees of $8,000. Miguel also paid audit fees related to

the stock issuance of $12,000, stock registration fees of $7,000, and stock listing

application fees of $3,000.

Based on the preceding information, under the acquisition method, what amount

relating to the business combination would be expensed?

A. $22,000

B. $36,000

C. $44,000

D. $66,000

A private university received $2,640,000 from student tuition and fees for the year

20X6 summer session. The session began on May 16, 20X6, and ended on July 15,

20X6. The university’s fiscal year end is June 30. According to the AICPA College and

University Audit Guide, how should the university report the $2,640,000 of receipts in

its financial statements for the year ended June 30, 20X6?

A. Current revenue of $2,640,000.

B. Current revenue of $1,980,000 and deferred revenue of $660,000.

C. Deferred revenue of $2,640,000.

D. Restricted current revenue of $2,640,000.

GASB 31 “Accounting for Financial Reporting for Certain Investments and for

External Reporting Investment Pools,” establishes a general rule that government

entities value investments in option contracts, open-ended mutual funds, and debt

securities for balance sheet presentation at:

A. lower of cost or market.

B. fair value.

C. cost.

D. amortized cost.

Sky Corporation owns 75 percent of Earth Company’s stock. On July 1, 20X8, Sky sold

a building to Earth for $33,000. Sky had purchased this building on January 1, 20X6,

for $36,000. The building’s original eight-year estimated total economic life remains

unchanged. Both companies use straight-line depreciation. The equipment’s residual

value is considered negligible.

Based on the information provided, in the preparation of the 20X8 consolidated

financial statements, building will be _____ in the consolidating entries.

A. debited for $33,000

B. debited for $36,000

C. credited for $36,000

D. debited for $3,000

The purpose of a “tombstone ad” is:

A. to inform investors an upcoming offering has been canceled.

B. to inform investors of an upcoming offering.

C. to inform investors an upcoming offering will be delayed for 30 days.

D. to inform investors securities will be offered for sale after the company has

responded to the SEC’s comment letter.

Pilfer Company acquired 90 percent ownership of Scrooge Corporation in 20X7, at

underlying book value. On that date, the fair value of noncontrolling interest was equal

to 10 percent of the book value of Scrooge Corporation. Pilfer purchased inventory

from Scrooge for $90,000 on August 20, 20X8, and resold 70 percent of the inventory

to unaffiliated companies on December 1, 20X8, for $100,000. Scrooge produced the

inventory sold to Pilfer for $67,000. The companies had no other transactions during

20X8.

Based on the information given above, what amount of cost of goods sold will be

reported in the 20X8 consolidated income statement?

A. $60,900

B. $90,000

C. $46,900

D. $67,000

The fair market value of a near-month call option with a strike price of $45 is $5, when

the stock is trading at $48.

Based on the preceding information, the call option:

A. has no intrinsic value currently.

B. is at the money.

C. is out of the money.

D. is in the money.