Wright Company recently petitioned for bankruptcy and is now in the process of

preparing a statement of affairs. The carrying values and estimated fair values of the

assets of Wright Company are as follows:

Carrying Value Fair Value

Cash $10,000 $10,000

Accounts Receivable 60,000 20,000

Inventory 70,000 40,000

Land 90,000 75,000

Building (net) 200,000 150,000

Equipment (net) 80,000 25,000

Total $510,000 $320,000

Debts of Wright are as follows:

Accounts Payable $40,000

Wages Payable (all have priority) 6,000

Taxes Payable 12,000

Notes Payable (secured by receivables and inventory) 90,000

Interest on Notes Payable 5,000

Bonds Payable (secured by land and buildings) 200,000

Interest on Bonds Payable 8,000

Total $361,000

Based on the preceding information, what estimated amount will be available for

general unsecured creditors upon liquidation?

A. $34,000

B. $52,000

C. $56,000

D. $75,000

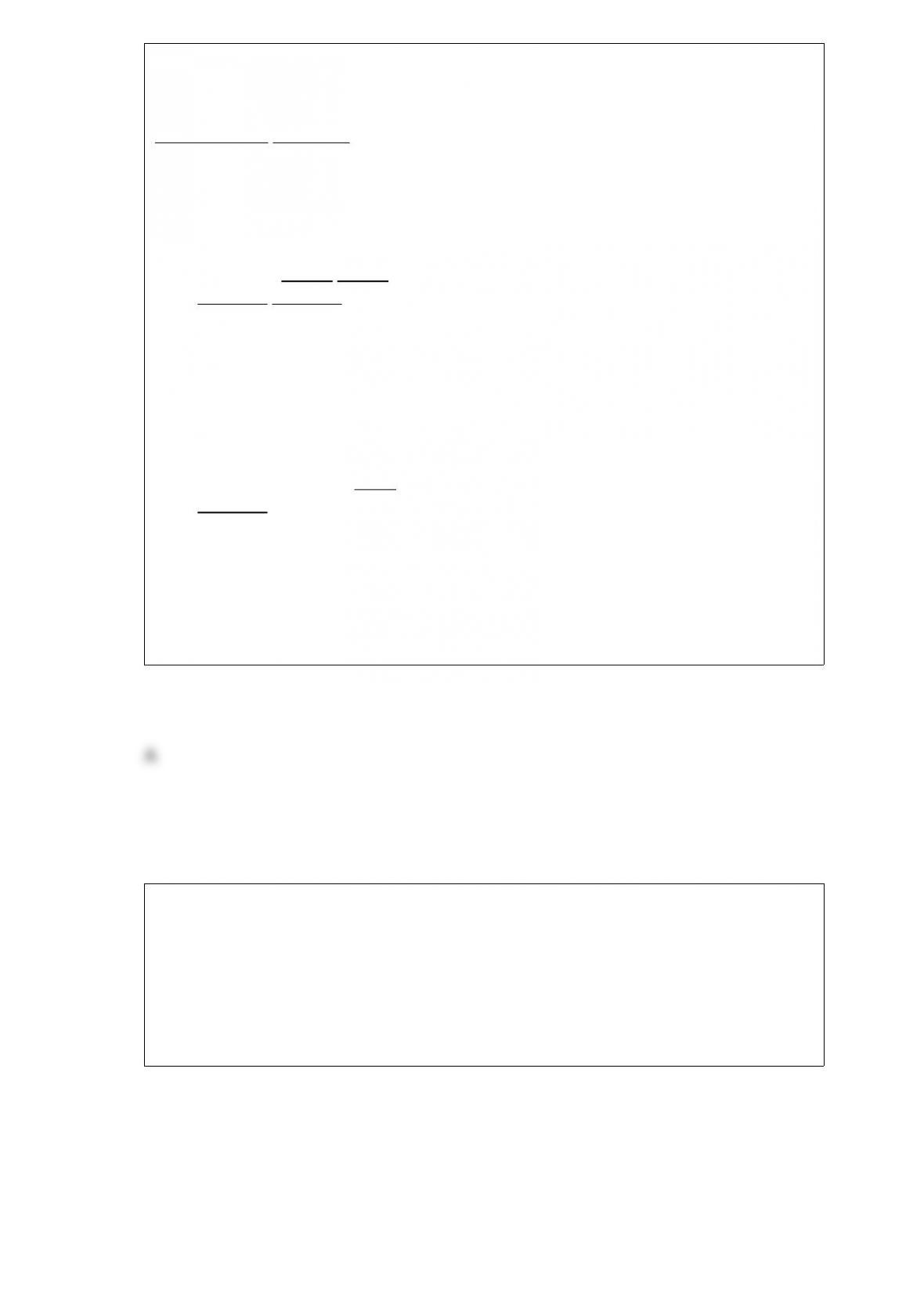

Moon Corporation issued $300,000 par value 10-year bonds at 107 on January 1, 20X3,

which Star Corporation purchased. Sun Corporation owns 65% of Moon’s voting

shares. On Jan 1, 20X7, Sun Corporation purchased $120,000 face value of Moon

bonds from Star for $118,020. On the date Sun purchased the bonds, the bonds’

carrying value on Moon’s book was $126,019. The bonds pay 12 percent interest

annually on December 31. The preparation of consolidated financial statements for

Moon and Sun at December 31, 20X9, required the following consolidating entry:

Based on the information given above, if 20X9 consolidated net income of $50,000 would

have been reported without the consolidating entry provided, what amount will actually be

reported?

A. $45,286

B. $47,774

C. $51,244

D. $48,756

The Statement of Realization and Liquidation contains sections for all the following

items except:

A. assets.

B. supplementary items.

C. liabilities.

D. stockholders equity.

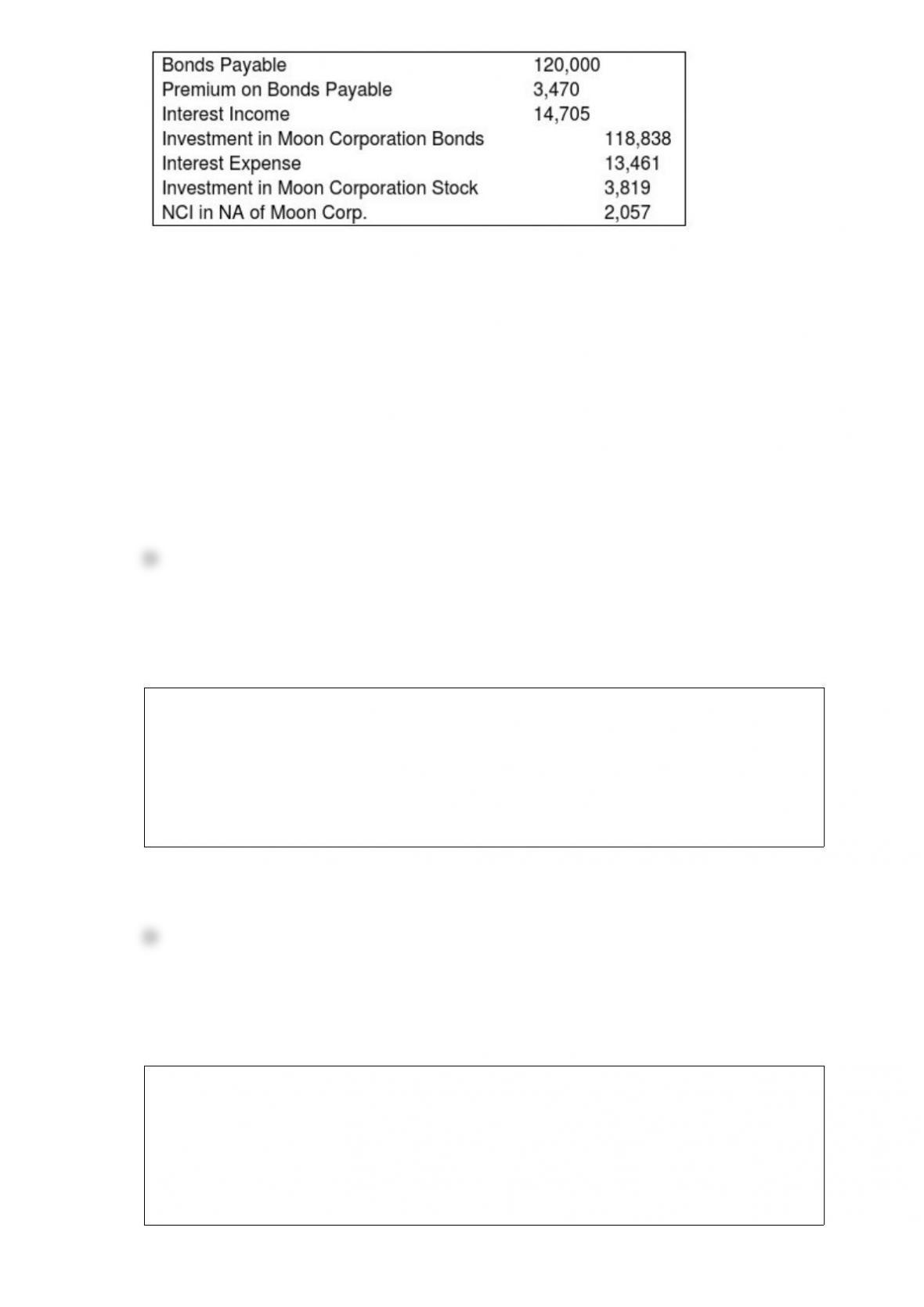

Tom, Dick, and Harry are partners in an equipment leasing business that has not been

able to generate the type of revenue expected by the partners. They share profits and

losses in a ratio of 5:3:2. They have decided to liquidate the business and have sold all

the assets except for one piece of heavy machinery. All partnership liabilities have been

settled and all the partners are personally insolvent. The machinery has a book value of

$85,000, and the partners have capital account balances as follows:

Each of the following are independent cases.

Refer to the information given above. What amount of cash will each partner receive as

a liquidating distribution if the machinery is sold for 65,000 dollars?

A. Option A

B. Option B

C. Option C

D. Option D

Parent Corporation owns 90 percent of Subsidiary 1 Company’s stock and 75 percent of

Subsidiary 2 Company’s stock. During 20X8, Parent sold inventory purchased in 20X7

for $48,000 to Subsidiary 1 for $60,000. Subsidiary 1 then sold the inventory at its cost

of $60,000 to Subsidiary 2. Prior to December 31, 20X8, Subsidiary 2 sold $45,000 of

inventory to a nonaffiliate for $67,000 and held $15,000 in inventory at December 31,

20X8.

Based on the information given above, what amount of sales must be eliminated from

the consolidated income statement for 20X8?

A. $117,000

B. $120,000

C. $150,000

D. $128,000

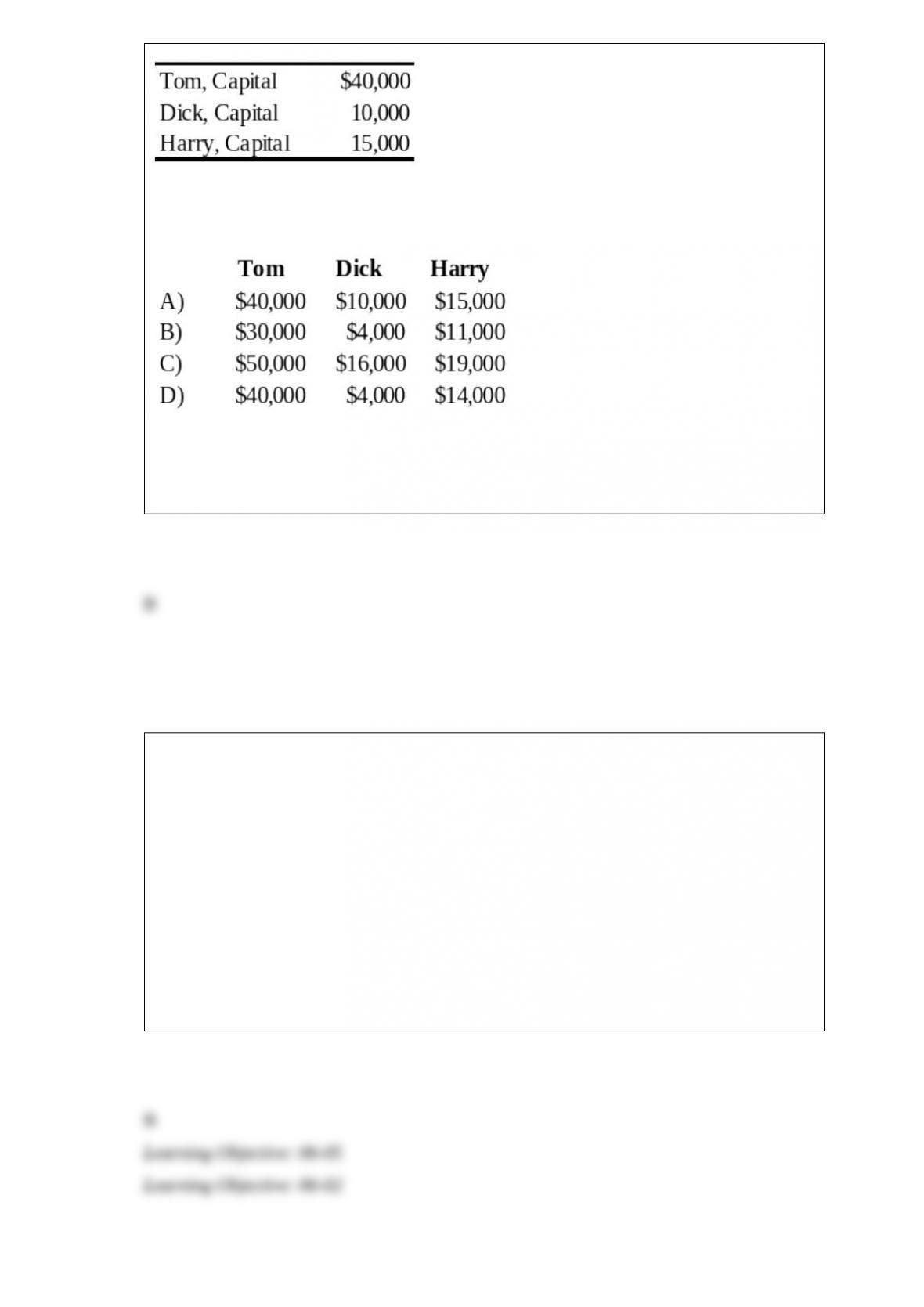

Trevor Company discloses supplementary operating segment information for its three

reportable segments. Data for 20X8 are available as follows:

Allocable costs for the year was $180,000. Allocable costs are assigned based on the

ratio of a segment’s income before allocable costs to total income before allocable costs.

The 20X8 operating profit for Segment B was:

A. $110,000

B. $180,000

C. $126,000

D. $120,000

A private university received $280,000 from student tuition and fees for the year 20X9

summer session. The session began on June 20, 20X9, and ended on July 30, 20X9. The

university’s fiscal year end is June 30. According to the AICPA College and University

Audit Guide, how should the university report the $280,000 of receipts in its financial

statements for the year ended June 30, 20X9?

A. Current revenue of $280,000.

B. Current revenue of $70,000 and deferred revenue of $210,000.

C. Deferred revenue of $280,000.

D. Restricted current revenue of $280,000.

The Bankruptcy Reform Act contains chapters which deal with:

I. Individuals.

II. Corporations.

III. Municipal governments.

A. Only I and II

B. Only II and III

C. Only I and III

D. I, II, and III

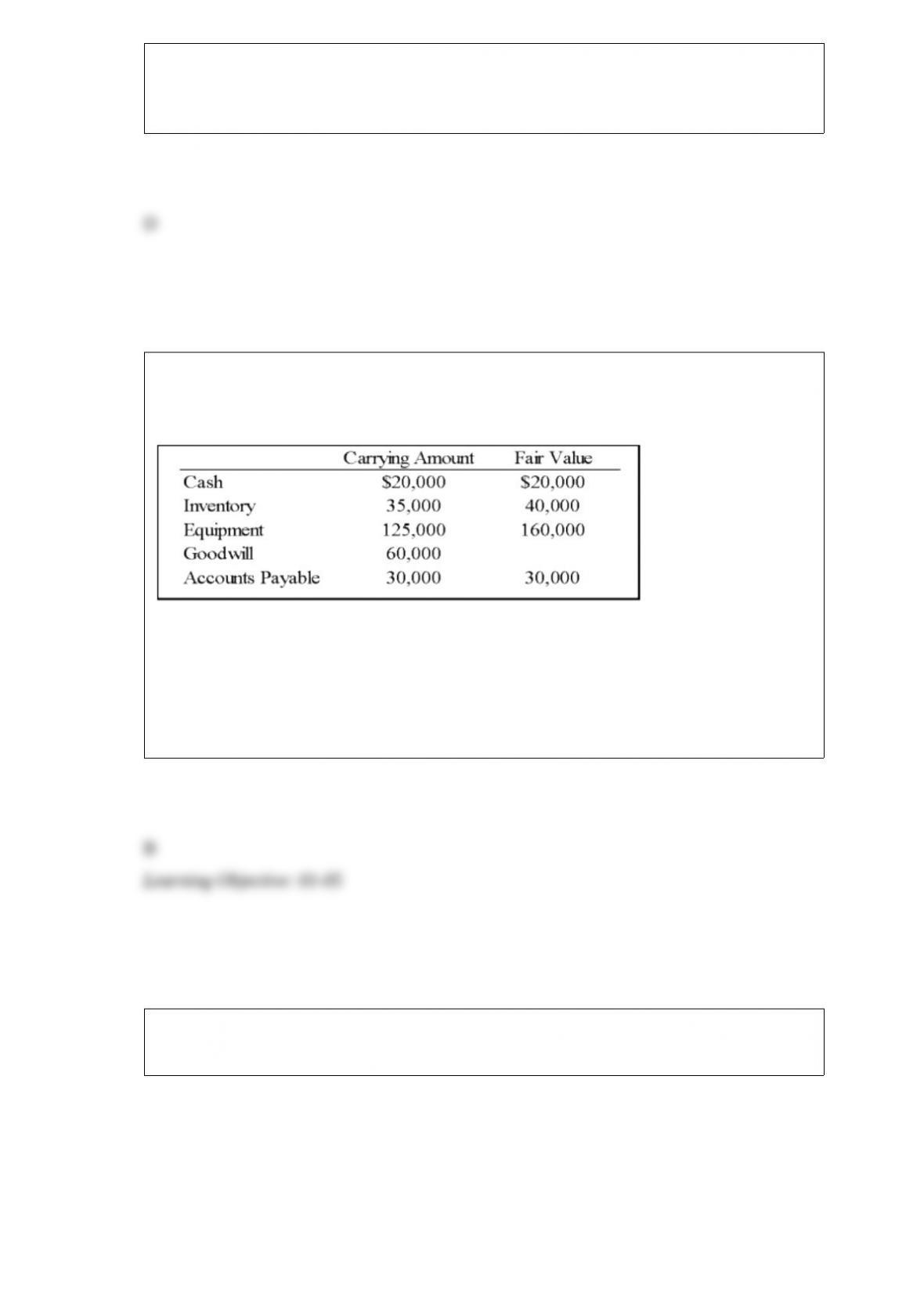

Following its acquisition of the net assets of Dan Company, Empire Company assigned

goodwill of $60,000 to one of the reporting divisions. Information for this division

follows:

Based on the preceding information, what amount of amount of goodwill impairment

will be recognized for this division if its fair value is determined to be $245,000?

A. $0

B. $5,000

C. $60,000

D. $55,000

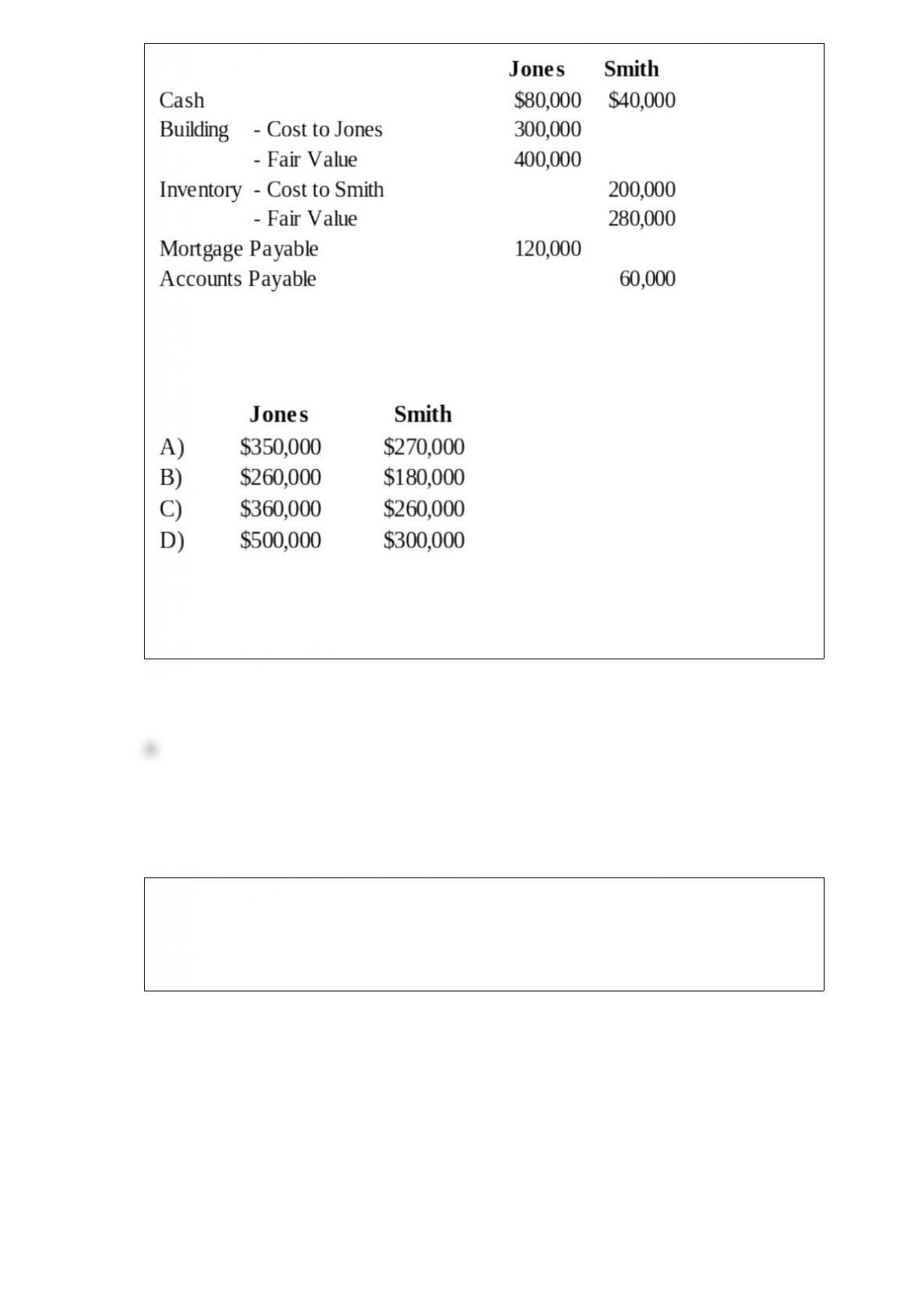

Jones and Smith formed a partnership with each partner contributing the following

items:

Assume that for tax purposes Jones and Smith agree to share equally in the liabilities

assumed by the Jones and Smith partnership.

Refer to the above information. What is each partner’s tax basis in the Jones and Smith

partnership?

A. Option A

B. Option B

C. Option C

D. Option D

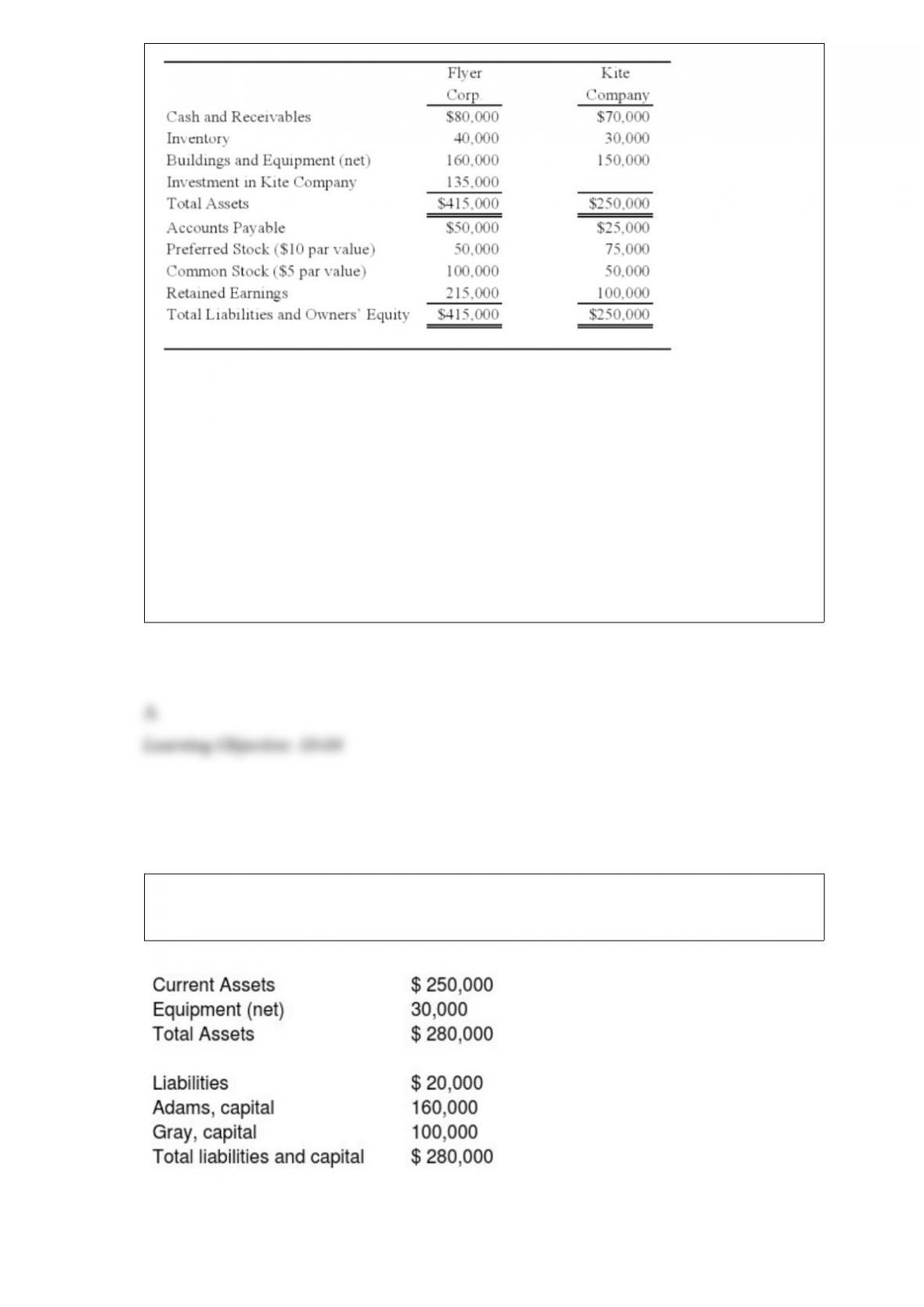

Flyer Corporation holds 90 percent of Kite Company’s common shares but none of its

preferred shares. On the date of acquisition, the fair value of the noncontrolling interest

was equal to 10 percent of the book value of Kite Company. Summary balance sheets

for the companies on December 31, 20X8, are as follows:

Flyer’s preferred pays a 8 percent annual dividend, and Kite’s preferred pays a 10

percent dividend. Kite’s preferred shares can be converted into 20,000 shares of

common stock at any time. Kite reported net income of $35,000 and paid a total of

$10,000 of dividends in 20X8. Flyer reported income from its separate operations of

$80,000 and paid total dividends of $25,000 in 20X8.

Based on the information provided, what is the basic earnings per share for the

consolidated entity for 20X8?

A. 5.04

B. 5.24

C. 3.80

D. 5.18

The condensed balance sheet of Adams & Gray, a partnership, at December 31, 20X1,

follows:

On December 31, 20X1, the fair values of the assets and liabilities were appraised at

$240,000 and $20,000, respectively, by an independent appraiser. On January 2, 20X2, the

partnership was incorporated and 1,000 shares of $5 par value common stock were issued.

Immediately after the incorporation, what amount should the new corporation report as

additional paid-in capital?

A. $275,000

B. $215,000

C. $260,000

D. $0

When the local currency of the foreign subsidiary is the functional currency, a foreign

subsidiary’s income statement accounts would be converted to U.S. dollars by:

A. translation using historical exchange rates.

B. remeasurement using current exchange rates at the time of statement preparation.

C. translation using average exchange rate for the period.

D. remeasurement using the current exchange rate at the time of statement preparation.

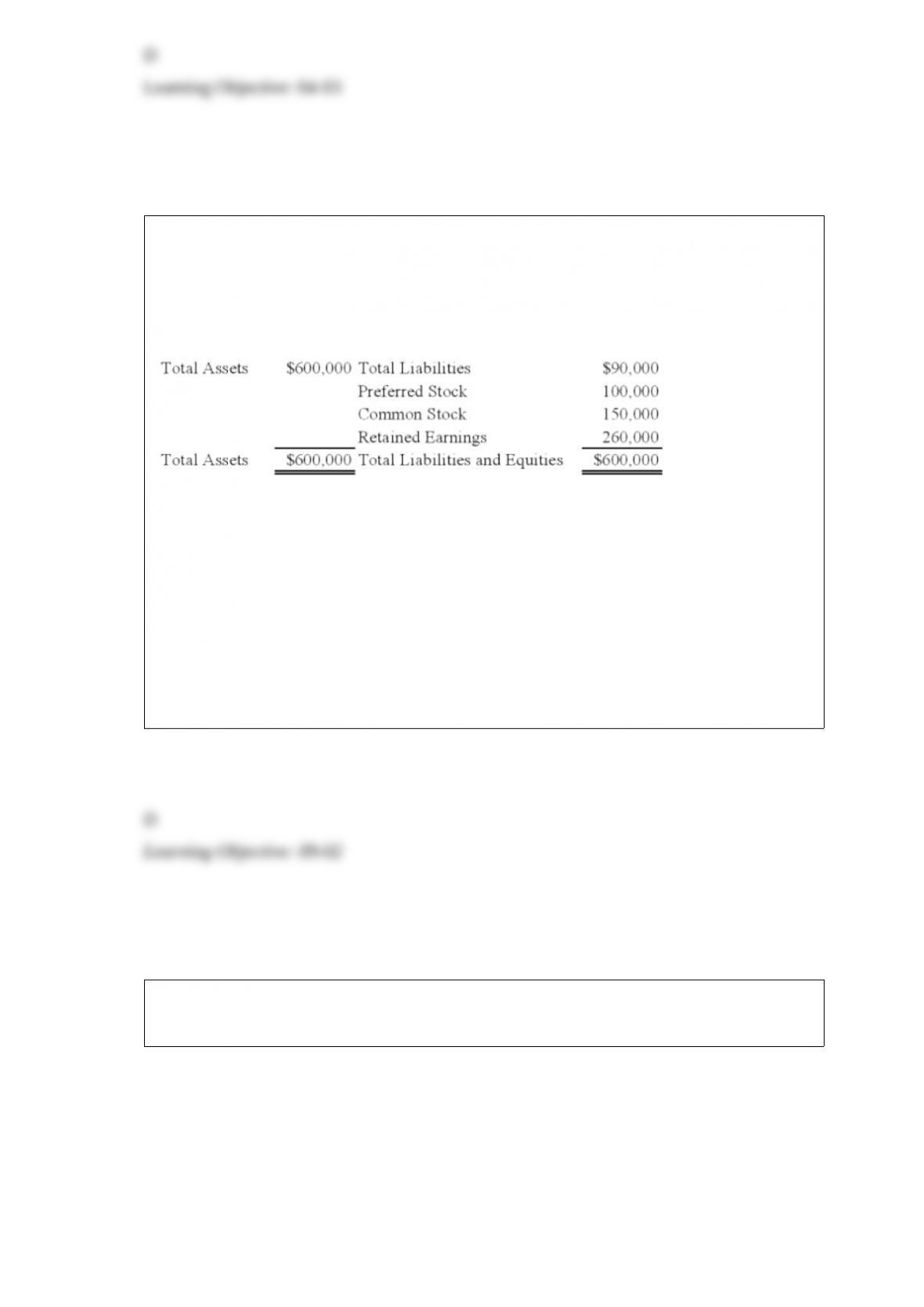

Berlin, Inc. holds 100 percent of the common stock of Sea Company, an investment

acquired for $520,000. Immediately following the combination, Berlin’s net assets have

a book value of $900,000 and a fair value of $1,050,000. The book and fair value of

Sea’s net assets on the date of combination are $350,000 and $425,000, respectively.

Immediately following the combination, a consolidated balance sheet is prepared.

Based on the information given above, what will be the amount of net assets reported in

the consolidated balance sheet?

A. $1,420,000

B. $1,325,000

C. $1,250,000

D. $900,000

Winner Corporation acquired 80 percent of the common shares and 70 percent of the

preferred shares of First Corporation at underlying book value on January 1, 20X9. At

that date, the fair value of the noncontrolling interest in First’s common stock was equal

to 20 percent of the book value of its common stock. First’s balance sheet at the time of

acquisition contained the following balances:

The preferred shares are cumulative and have a 10 percent annual dividend rate and are

four years in arrears on January 1, 20X9. All of the $5 par value preferred shares are

callable at $6 per share. During 20X9, First reported net income of $100,000 and paid

no dividends.

Based on the information provided, what is the book value of the common stock on

January 1, 20X9?

A. $410,000

B. $360,000

C. $390,000

D. $350,000

On January 1, 20X9, Wilton Company acquired all of Sirius Company’s common

shares, for $365,000 cash. On that date, Sirius’s balance sheet appeared as follows:

The fair values of all of Sirius’s assets and liabilities were equal to their book values

except for inventory that had a fair value of $85,000, land that had a fair value of

$60,000, and buildings and equipment that had a fair value of $250,000. Buildings and

equipment have a remaining useful life of 10 years with zero salvage value. Wilton

Company decided to employ push-down accounting for the acquisition. Subsequent to

the combination, Sirius continued to operate as a separate company.

Based on the preceding information, what amount will be present in the revaluation

capital account, when consolidating entries are prepared?

A. $0

B. $65,000

C. $60,000

D. $15,000

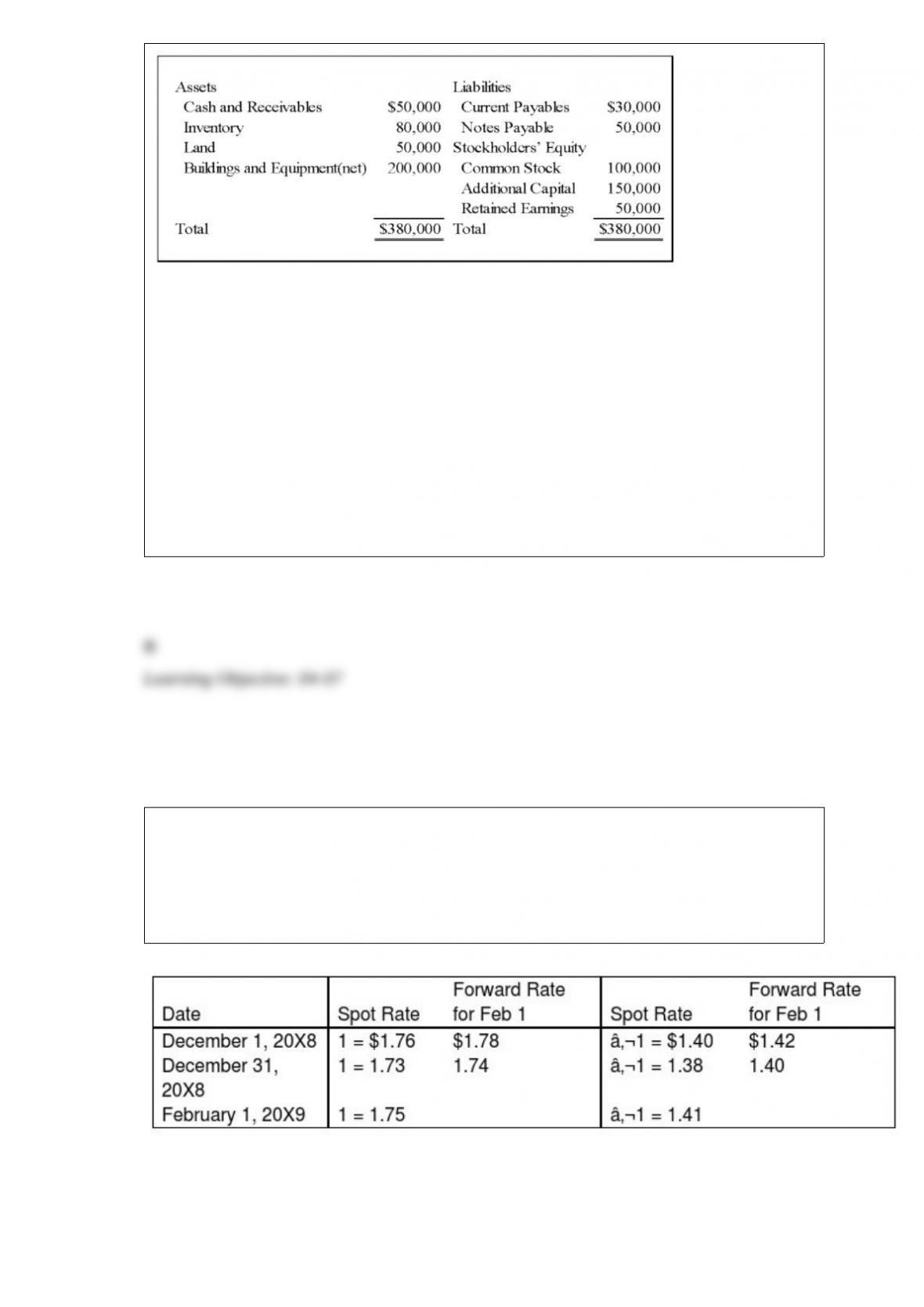

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the net gain or loss on the euro speculative

contract?

A. $8,000 gain

B. $6,000 gain

C. $3,000 loss

D. $1,000 loss

Which division of the SEC develops and administers the disclosure requirements for the

securities acts and reviews all registration statements and other issue-oriented

disclosures?

A. Division of Enforcement

B. Division of Corporation Finance

C. Division of Investment Management

D. Division of Market Regulation

Assuming no impairment in value prior to transfer, assets transferred by a parent

company to another entity it has created should be recorded by the newly created entity

at the assets’:

A. cost to the parent company.

B. book value on the parent company’s books at the date of transfer.

C. fair value at the date of transfer.

D. fair value of consideration exchanged by the newly created entity.

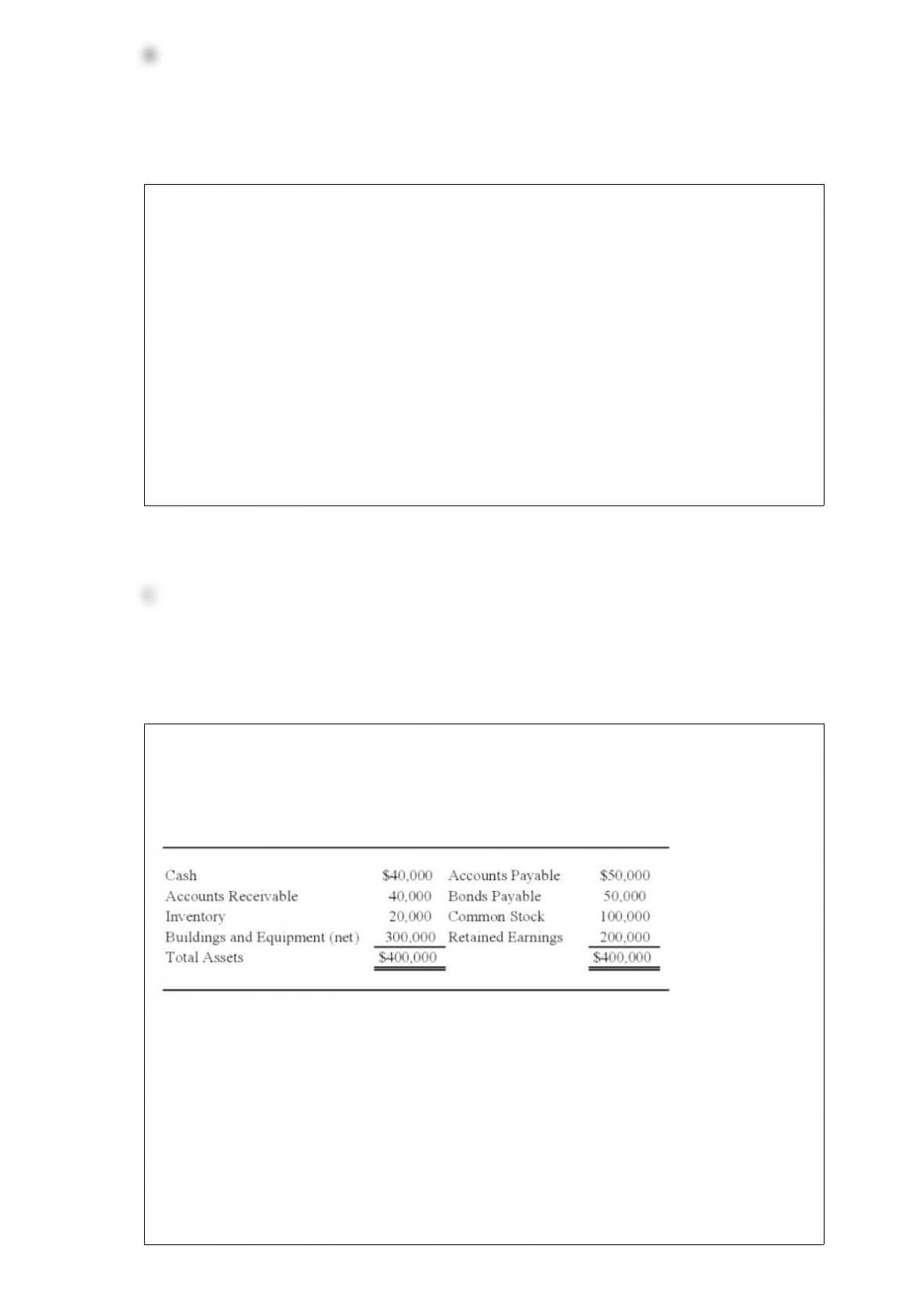

Autumn Corporation acquired 90 percent of the stock of Spring Company on January 1,

20X2, for $360,000. At that date, the fair value of the noncontrolling interest was

$40,000. Spring’s balance sheet contained the following amounts at the time of the

combination:

Cash $20,000 Accounts Payable $25,000

Accounts Receivable 60,000 Bonds Payable 75,000

Inventory 70,000 Common Stock 100,000

Buildings and Equipment (net) 350,000 Retained Earnings 300,000

Total Assets $500,000 Total Liabilities & Equity $500,000

During each of the next three years, Spring reported net income of $70,000 and paid

dividends of $20,000. On January 1, 20X4, Autumn sold 3,000 shares of Spring’s $5

par value shares for $90,000 in cash. Autumn used the fully adjusted equity method in

accounting for its ownership of Spring Company.

Based on the preceding information, in the consolidation entries to complete a

consolidation worksheet at January 1, 20X4 (after the sale of the 3,000 shares of Spring

stock), Investment in Spring Stock will be credited for

A. $360,000.

B. $375,000.

C. $405,000.

D. $450,000.

Shue, a partner in the Financial Brokers Partnership, has a 30 percent share in

partnership profits and losses. Shue’s capital account had a net decrease of $100,000

during 20X8. During 20X8, Shue withdrew $240,000 as withdrawals and contributed

equipment valued at $50,000 to the partnership. What was the net income of the

Financial Brokers Partnership for 20X8?

A. $633,334

B. $466,666

C. $300,000

D. $190,000

ABC Corporation owns 75 percent of XYZ Company’s voting shares. During 20X8,

ABC produced 50,000 chairs at a cost of $79 each and sold 35,000 chairs to XYZ for

$90 each. XYZ sold 18,000 of the chairs to unaffiliated companies for $117 each prior

to December 31, 20X8, and sold the remainder in early 20X9 to unaffiliated companies

for $130 each. Both companies use perpetual inventory systems.

Based on the information given above, what amount of cost of goods sold must be

eliminated from the consolidated income statement for 20X8?

A. $2,765,000

B. $1,620,000

C. $1,422,000

D. $2,963,000

Big Corporation receives management consulting services from its 92 percent owned

subsidiary, Small Inc. During 20X7, Big paid Small $125,432 for its services. For the

year 20X8, Small billed Big $140,000 for such services and collected all but $7,900 by

year-end. Small’s labor cost and other associated costs for the employees providing

services to Big totaled $86,000 in 20X7 and $121,000 in 20X8. Big reported

$2,567,000 of income from its own separate operations for 20X8, and Small reported

net income of $695,000.

Based on the preceding information, what amount of income should be assigned to the

noncontrolling shareholders in the consolidated income statement for 20X8?

A. $47,700

B. $44,400

C. $55,600

D. $60,000

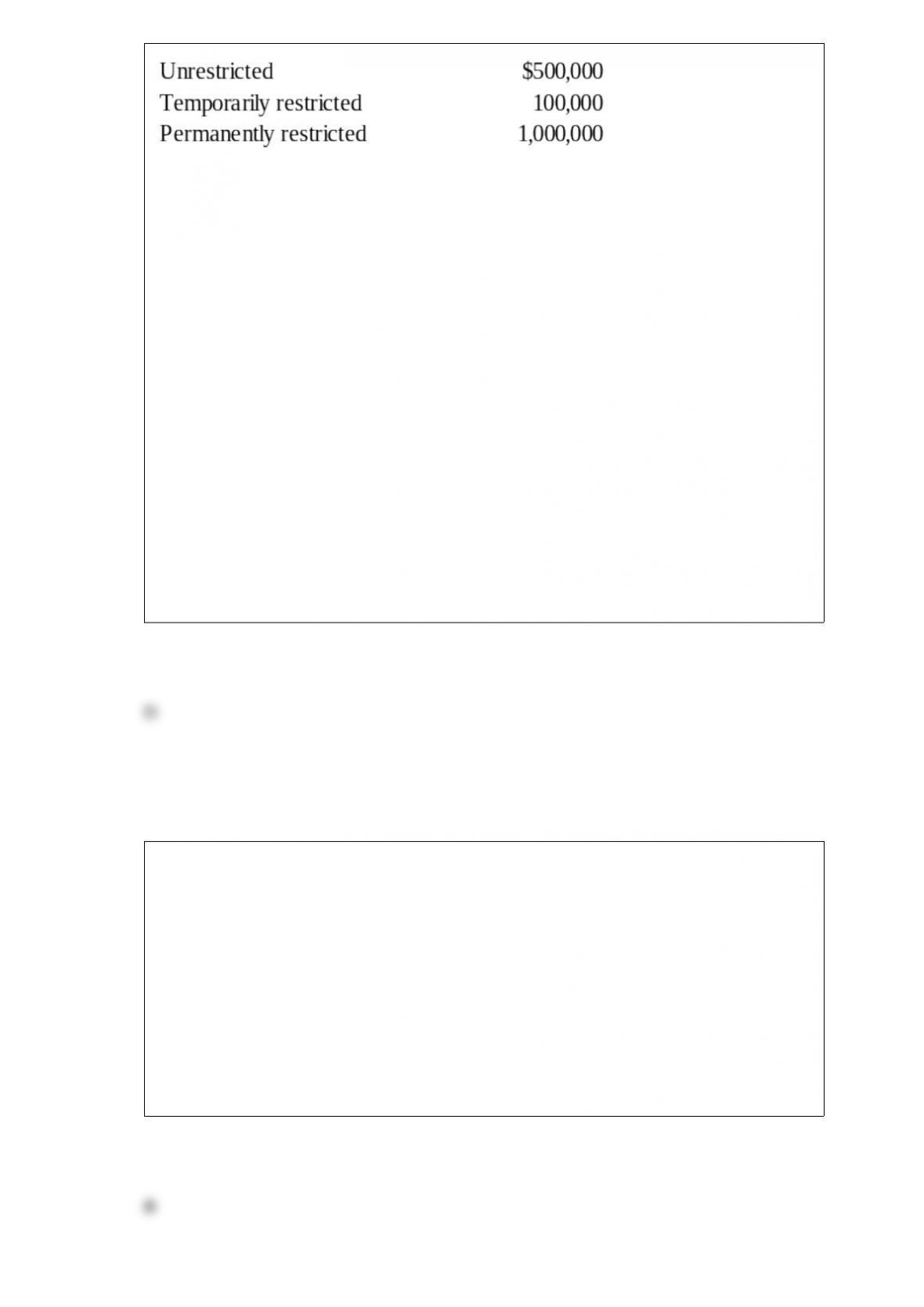

Local Services, a voluntary health and welfare organization had the following classes of

net assets on July 1, 20X8, the beginning of its fiscal year:

During the year ended June 30, 20X9, the following events occurred:

(1) It purchased equipment, costing $100,000, with contributions restricted for this

purpose. The contributions had been received from donors during June of 20X8.

(2) It received $130,000 of cash donations which were restricted for research activities.

During the year ended June 30, 20X9, $90,000 of the contributions were expended on

research.

(3) It sold investments classified in the permanently restricted class for a loss of

$40,000. Dividends and interest income earned on the investments amounted to

$70,000. There were no restrictions on how investment income was to be used.

(4) It received cash contributions of $200,000 from donors who did not place either

time or use restrictions upon their donations.

(5) Expenses, excluding depreciation expense, for program services and supporting

services incurred during the year ended June 30, 20X9, amounted to $260,000.

(6) Depreciation expense for the year ended June 30, 20X9, was $80,000.

Refer to the above information. On the statement of activities for the year ended June

30, 20X9, temporarily restricted net assets:

A. increased $130,000.

B. increased $40,000.

C. decreased $100,000.

D. decreased $60,000.

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. Allen and Daniel agree that some of the

inventory is obsolete. The inventory account is decreased before David is admitted.

David invests $40,000 for a one-fifth interest. What is the amount of inventory written

down?

A. $4,000

B. $20,000

C. $15,000

D. $10,000

Wright Company recently petitioned for bankruptcy and is now in the process of

preparing a statement of affairs. The carrying values and estimated fair values of the

assets of Wright Company are as follows:

Carrying Value Fair Value

Cash $10,000 $10,000

Accounts Receivable 60,000 20,000

Inventory 70,000 40,000

Land 90,000 75,000

Building (net) 200,000 150,000

Equipment (net) 80,000 25,000

Total $510,000 $320,000

Debts of Wright are as follows:

Accounts Payable $40,000

Wages Payable (all have priority) 6,000

Taxes Payable 12,000

Notes Payable (secured by receivables and inventory) 90,000

Interest on Notes Payable 5,000

Bonds Payable (secured by land and buildings) 200,000

Interest on Bonds Payable 8,000

Total $361,000

Based on the preceding information, what is the total amount of unsecured claims?

A. $52,000

B. $71,000

C. $75,000

D. $95,000

Grant, Inc. acquired 30 percent of South Co.’s voting stock for $200,000 on January 2,

20X4. Grant’s 30 percent interest in South gave Grant the ability to exercise significant

influence over South’s operating and financial policies. During 20X4, South earned

$80,000 and paid dividends of $50,000. South reported earnings of $100,000 for the six

months ended June 30, 20X5, and $200,000 for the year ended December 31, 20X5. On

July 1, 20X5, Grant sold half of its stock in South for $150,000 cash. South paid

dividends of $60,000 on October 1, 20X5.

In its 20X5 income statement, what amount should Grant report as a gain from the sale

of half of its investment?

A. $35,000

B. $24,500

C. $30,500

D. $45,500

On January 1, 20X1, Big Company (Big) bought 30% of the outstanding stock of Little

Company (Little) for $110,000 which provided Big with the ability to significantly

influence the decisions of Little. Little reported assets of $400,000 and liabilities of

$100,000 on that date. As part of its analysis before buying these shares, Big

determined that Little owned a patent that had not been recorded despite having a

remaining useful life of five years and a value of $20,000. During 20X1, Little reported

net income of $70,000 and paid cash dividends of $30,000. What investment income

should Big report for 20X1?

A. $9,000

B. $19,800

C. $17,000

D. $21,000

In 20X9, a private not-for-profit hospital received a $200,000 cash contribution to its

endowment fund. During the year, hospital administration invested $150,000 of the

funds. Which of the following statements regarding the effect of these transactions on

the preparation of the hospital’s statement of cash flow is true?

A. The $200,000 contribution will appear in the investing activities section of the cash

flow statement as a cash inflow.

B. The $200,000 contribution will appear in the financing activities section of the cash

flow statement as a cash inflow.

C. The $150,000 investment will appear in the investing activities section of the cash

flow statement as a cash inflow.

D. The $150,000 contribution will appear in the financing activities section of the cash

flow statement as a cash inflow.

Healing Angel Hospital, operated by a religious organization, billed patients

$13,000,000 for services rendered during the year ended June 30, 20X3. The hospital

realized cash of $10,700,000 from the patient billings because of the following

reductions:

(1) contractual adjustments of $1,400,000 granted to private insurance companies and

to the federal government; and

(2) uncollectible accounts receivable of $900,000.

On the statement of operations prepared for the year ended June 30, 20X3, Healing

Angel Hospital should report net patient service revenue of:

A. $13,000,000.

B. $12,100,000.

C. $11,600,000.

D. $10,700,000.

Vision Corporation acquired 75 percent of the stock of Meta Company on January 1,

20X7, for $225,000. At that date, the fair value of the noncontrolling interest was

$75,000. Meta’s balance sheet contained the following amounts at the time of the

combination:

During each of the next three years, Meta reported net income of $30,000 and paid

dividends of $10,000. On January 1, 20X9, Vision sold 1,500 shares of Meta’s $10 par

value shares for $60,000 in cash. Vision used the fully adjusted equity method in

accounting for its ownership of Meta Company.

Based on the preceding information, what was the balance in the investment account

reported by Vision on January 1, 20X9, before its sale of shares?

A. $225,000

B. $285,000

C. $245,000

D. $255,000

Which of the following items would not be reported on the financial statements of a

special revenue fund?

A. Long-term productive assets.

B. Expenditures and revenues.

C. Vouchers payable and unreserved fund balance.

D. Fund balance reserved for encumbrances and expenditures.

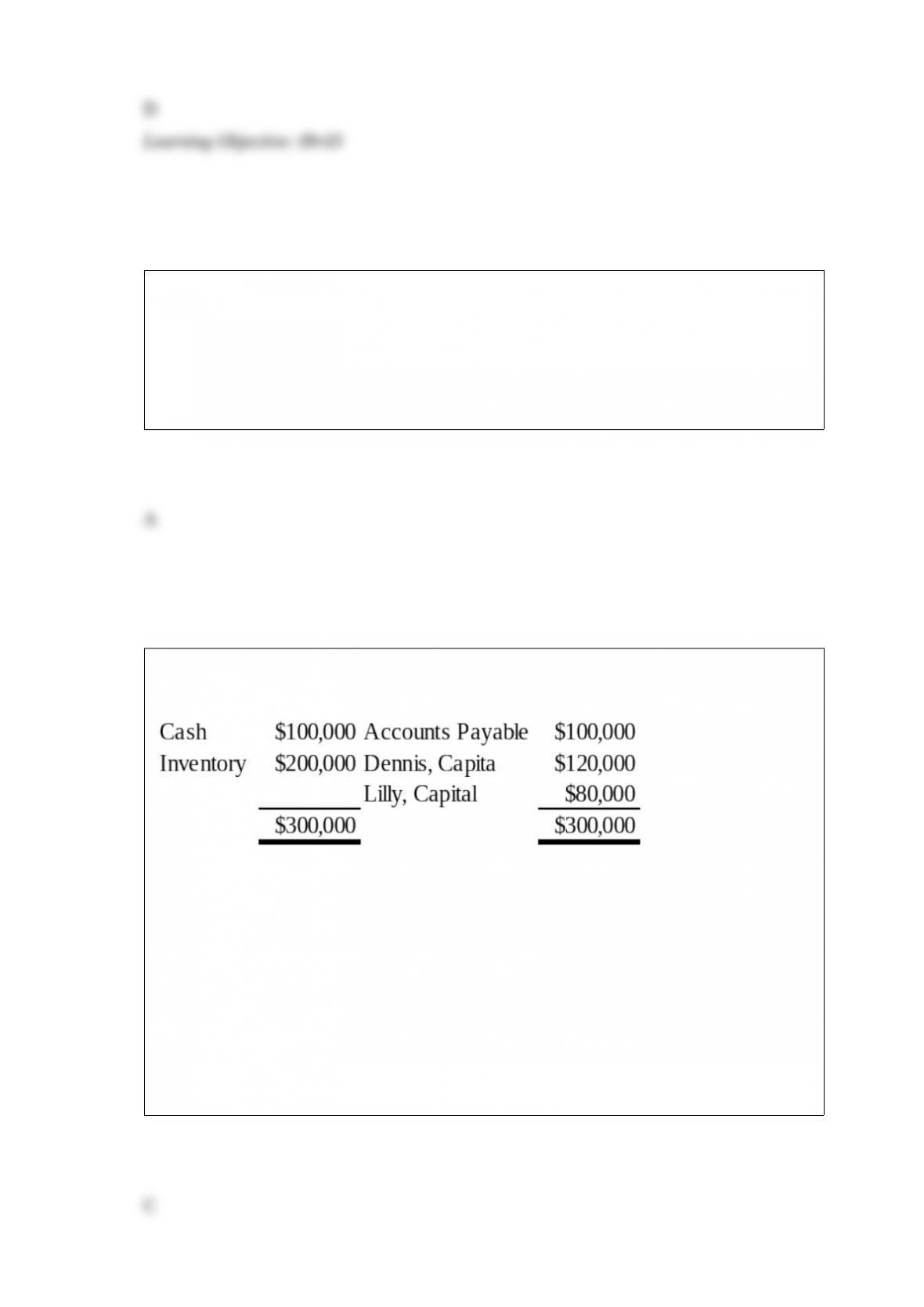

Partners Dennis and Lilly have decided to liquidate their business. The following

information is available:

Dennis and Lilly share profits and losses in a 3:2 ratio. During the first month of

liquidation, half the inventory is sold for $60,000, and $60,000 of the accounts payable

is paid. During the second month, the rest of the inventory is sold for $45,000, and the

remaining accounts payable are paid. Cash is distributed at the end of each month, and

the liquidation is completed at the end of the second month.

Refer to the information provided above. Using a safe payments schedule, how much

cash will be distributed to Lilly at the end of the second month?

A. $27,000

B. $36,000

C. $18,000

D. $0

Autumn Corporation acquired 90 percent of the stock of Spring Company on January 1,

20X2, for $360,000. At that date, the fair value of the noncontrolling interest was

$40,000. Spring’s balance sheet contained the following amounts at the time of the

combination:

Cash $20,000 Accounts Payable $25,000

Accounts Receivable 60,000 Bonds Payable 75,000

Inventory 70,000 Common Stock 100,000

Buildings and Equipment (net) 350,000 Retained Earnings 300,000

Total Assets $500,000 Total Liabilities & Equity $500,000

During each of the next three years, Spring reported net income of $70,000 and paid

dividends of $20,000. On January 1, 20X4, Autumn sold 3,000 shares of Spring’s $5

par value shares for $90,000 in cash. Autumn used the fully adjusted equity method in

accounting for its ownership of Spring Company.

Based on the preceding information, in the consolidation entries to complete a full

consolidation worksheet for 20X4, noncontrolling interest in the net income of Spring

will be credited for

A. $2,000.

B. $7,000.

C. $12,500.

D. $17,500.

Tower Corporation’s controller has just finished preparing a consolidated balance sheet,

income statement, and statement of changes in retained earnings for the year ended

December 31, 20X9. Tower owns 80 percent of Network Corporation’s stock, which it

acquired at underlying book value on November 1, 20X6. At that date, the fair value of

the noncontrolling interest was equal to 20 percent of Network Corporation’s book

value. The following information is available:

Consolidated net income for 20X9 was $160,000.

Network reported net income of $50,000 for 20X9.

Tower paid dividends of $30,000 in 20X9.

Network paid dividends of $10,000 in 20X9.

Tower issued common stock on February, 18, 20X9, for a total of $100,000.

Consolidated wages payable decreased by $6,000 in 20X9.

Consolidated depreciation expense for the year was $15,000.

Consolidated accounts receivable decreased by $20,000 in 20X9.

Bonds payable of Tower with a book value of $102,000 were retired for $100,000 on

December 31, 20X9.

Consolidated amortization expense on patents was $10,000 for 20X9.

Tower sold land that it had purchased for $75,000 to a nonaffiliate for $80,000 on June

10, 20X9.

Consolidated accounts payable decreased by $7,000 during 20X9.

Total purchases of equipment by Tower and Network during 20X9 were $180,000.

Consolidated inventory increased by $36,000 during 20X9.

There were no intercompany transfers between Tower and Network in 20X9 or prior

years except for Network’s payment of dividends. Tower uses the indirect method in

preparing its cash flow statement.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash used in financing activities for 20X9?

A. $32,000

B. $38,000

C. $42,000

D. $70,000