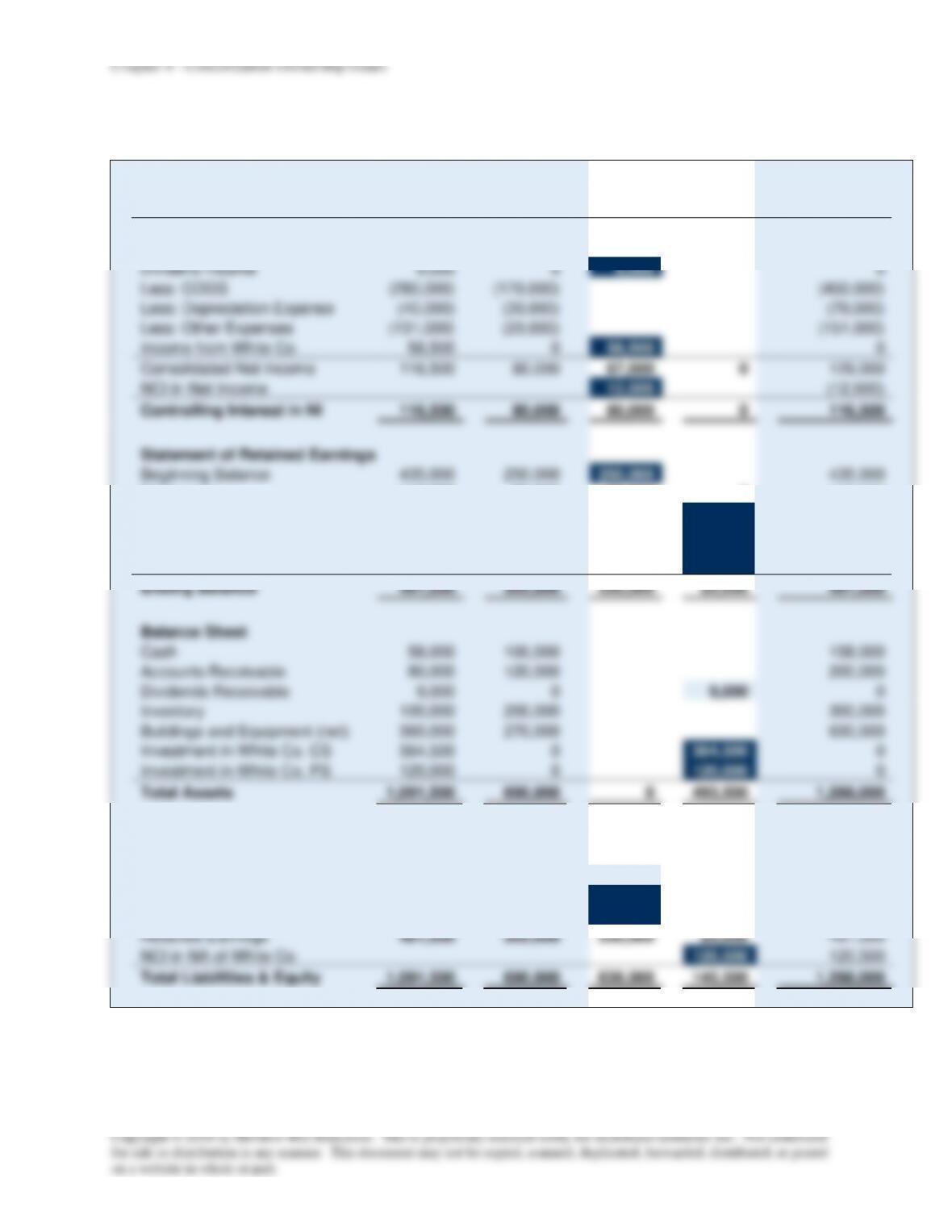

Chapter 9 – Consolidation Ownership Issues

P9-21 (continued)

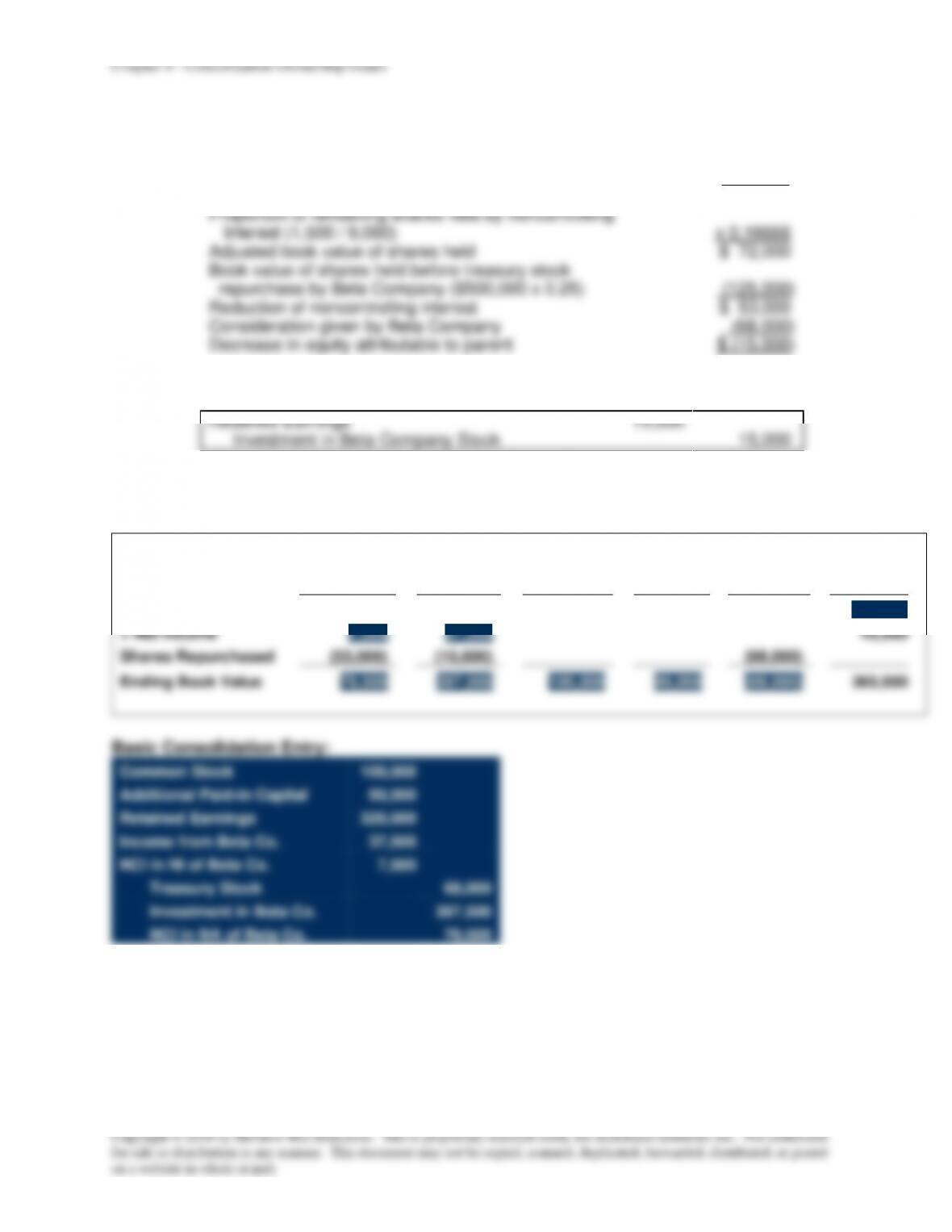

g. Consolidation entries:

Basic Consolidation Entry:

Preferred Stock

200,000

Premium on Preferred Stock

5,000

Common Stock

500,000

Additional Paid-In Capital

797,600

Retained Earnings

1,650,000

Income from Jacobs Jacuzzi

156,000

Dividends Income—Preferred

8,000

NCI in NI of Jacobs Jacuzzi

120,000

Dividends declared, Preferred

40,000

Dividends declared, Common

10,000

Investment in Jacobs Jacuzzi CS

1,909,800

Investment in Jacobs Jacuzzi PS

42,000

NCI in NA of Jacobs Jacuzzi

1,434,800

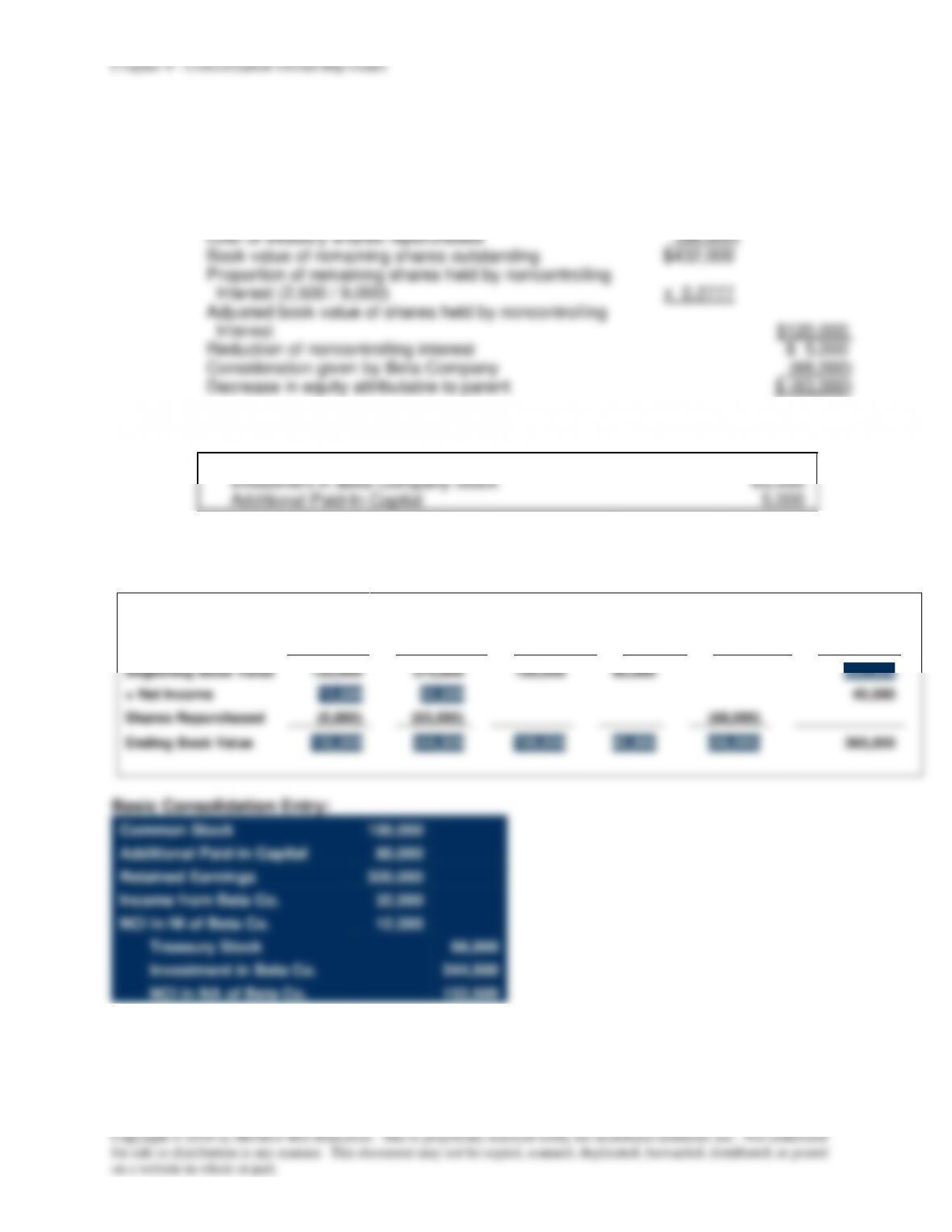

Excess Value (Differential) Calculations:

NCI 40%

+

Presley Pools

60%

=

Goodwill

Beginning Balance

26,800

40,200

67,000

Changes

(10,400)

(15,600)

(26,000)

Ending Balance

16,400

24,600

41,000

Amortized Excess Value Reclassification Entry:

Goodwill impairment loss

26,000

Income from Jacobs Jacuzzi

15,600

NCI in NI of Jacobs Jacuzzi

10,400

Excess Value (Differential) Reclassification Entry:

Goodwill

41,000

Investment in Jacobs Jacuzzi

24,600

NCI in NA of Jacobs Jacuzzi

16,400