Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–29

P17-15 (continued)

3.

ENCUMBRANCES

1,800,000

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

1,800,000

Record purchase orders.

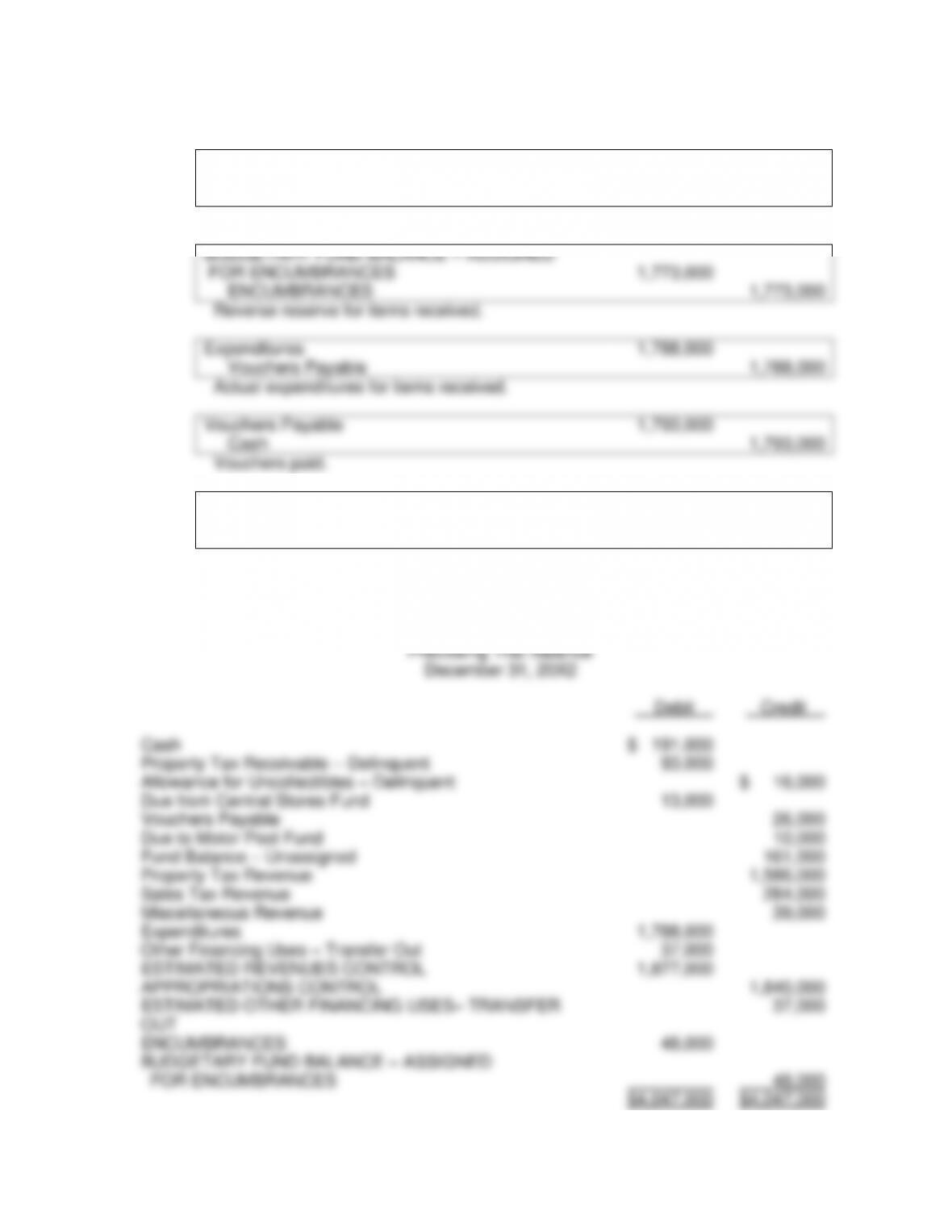

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

1,773,000

ENCUMBRANCES

1,773,000

Reverse reserve for items received.

Expenditures

1,788,000

Vouchers Payable

1,788,000

Actual expenditures for items received.

Vouchers Payable

1,793,000

Cash

1,793,000

Vouchers paid.

4.

Due from Central Stores Fund

13,000

Other Financing Uses – Transfer Out

37,000

Cash

50,000

Other cash payments and transfer.

b.

Pine Ridge

General Fund

Preclosing Trial Balance

December 31, 20X2

Debit

Credit

Cash

$ 191,000

Property Tax Receivable – Delinquent

93,000

Allowance for Uncollectibles – Delinquent

$ 16,000

Due from Central Stores Fund

13,000

Vouchers Payable

26,000

Due to Motor Pool Fund

10,000

Fund Balance – Unassigned

161,000

Property Tax Revenue

1,586,000

Sales Tax Revenue

284,000

Miscellaneous Revenue

39,000

Expenditures

1,788,000

Other Financing Uses – Transfer Out

37,000

ESTIMATED REVENUES CONTROL

1,877,000

APPROPRIATIONS CONTROL

1,840,000

ESTIMATED OTHER FINANCING USES– TRANSFER

OUT

37,000

ENCUMBRANCES

48,000

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

48,000

$4,047,000

$4,047,000

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

P17-15 (continued)

c.

Closing entries:

APPROPRIATIONS CONTROL

1,840,000

ESTIMATED OTHER FINANCING

USES – TRANSFER OUT

37,000

ESTIMATED REVENUES CONTROL

1,877,000

Close budgetary accounts.

BUDGETARY FUND BALANCE – ASSIGNED

FOR ENCUMBRANCES

48,000

ENCUMBRANCES

48,000

Close remaining encumbrances.

Fund Balance – Unassigned

48,000

Fund Balance – Assigned for

Encumbrances

48,000

Reserve fund balance for outstanding purchase orders.

Property Tax Revenue

1,586,000

Sales Tax Revenue

284,000

Miscellaneous Revenue

39,000

Expenditures

1,788,000

Other Financing Uses – Transfer Out

37,000

Fund Balance – Unassigned

84,000

Close operating statement accounts.

d.

Pine Ridge

General Fund

Balance Sheet

December 31, 20X2

Assets

Cash

$191,000

Property Tax Receivables – Delinquent

$ 93,000

Less: Allowance for Uncollectibles – Delinquent

(16,000)

77,000

Due from Central Stores Fund

13,000

Total Assets

$281,000

Liabilities and Fund Balance

Vouchers Payable

$ 26,000

Due to Motor Pool Fund

10,000

Fund Balance:

Spendable:

Assigned to:

General Government Services

$ 48,000

Unassigned

197,000

245,000

Total Liabilities and Fund Balance

$281,000

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–31

P17-15 (continued)

e.

Pine Ridge

General Fund

Statement of Revenues, Expenditures, and Changes

in Fund Balance

For Fiscal Year Ended December 31, 20X2

Revenue:

Property Taxes

$1,586,000

Sales Taxes

284,000

Miscellaneous

39,000

Total Revenue

$1,909,000

Expenditures:

Current

$1,746,000

Capital Outlay – Furniture

Total Expenditures

42,000

$1,788,000

Excess of Revenue over Expenditures

$ 121,000

Other Financing Sources (Uses):

Transfer Out

(37,000)

Change in Fund Balance

$ 84,000

Fund Balance, January 1, 20X2

161,000

Fund Balance, December 31, 20X2

$ 245,000

[Note that the $42,000 expenditure for the office furniture capital outlay is reported

separately. The theoretical support for this is that the expenditure will also benefit future

periods. Some governmental entities report capital outlays made in the general fund with

current expenditures because current financial resources were expended. Some

governments integrate capital outlay expenditures into the appropriate functional

categories (e.g., fire protection, government administration, or streets and highways)

rather than separately report the expenditures for capital outlays. The choice of reporting

alternative for the general fund is up to the governmental entity because the total

expenditures will be the same regardless of how or where the capital outlay is reported.]

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–32

P17-16 Matching Governmental Terms with Descriptions

1.

J

2.

I

3.

H

4.

G

5.

M

6.

Q

7.

R

8.

E

9.

N

10.

D

11.

F

12.

P

13.

A

14.

B

15.

L

16.

C

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–33

P17-17 Identification of Governmental Accounting Terms

1. Government-wide financial statements

2. The Governmental Accounting Standards Board (GASB)

3. A fund

4. Interfund services provided or used

5. Internal service and enterprise funds

6. Infrastructure assets

7. Agency and trust funds

8. Modified accrual basis

9. Flow of total economic resources

10. The property tax levy

11. The general, special revenue, capital projects, debt service funds and permanent

funds

12. The allowance for uncollectible property taxes

13. Budgetary fund balance – unassigned

14. Encumbrances

15. The consumption method

16. Other financing uses – transfer out

17. Expenditures

18. Fund balance – unassigned

19. Expenditures

20. Appropriations

21. Nonlapsing method

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–34

P17-18 Questions on General Fund Entries [AICPA Adapted]

1. D

2. C

3. C

4. C

5. N

6. D

7. N

8. C

9. C

10. N

11. D

12. C

13. N

14. N

15. N

16. C

17. D

18. D

19. C

20. N

21. N

22. N

23. C

24. D

25. N

26. C

27. D

28. D

29. D

30. C

31. D

32. C

33. D

34. N

35. N

36. C

37. D

38. D

39. C

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–35

P17–19 Questions on Fund Items [AICPA Adapted]

a.

16

$700,000 = $630,000 of current year’s taxes collected plus $70,000 of 20X1

taxes expected to be collected within 60 days after the end of the year

b.

8

$170,000 = $80,000 of the restricted grant that has been expended, plus

$50,000 in fines plus $40,000 in fees

c.

3

$50,000 = the fair and present value of the lease agreement

d.

6

$140,000 = the capital outlay for the new police vehicles

e.

2

$30,000 = the amount of the transfer in received by the debt service fund and

then expended for interest for the year

f.

18

$760,000 = $260,000 for governmental services and $500,000 for public

safety and welfare services. For this problem, the capital outlay of $140,000

was separately reported in the listing of expenditures. In practice, some

governmental entities include capital outlays in the general fund as an

expenditure under the appropriate functional activity. However, in a capital

projects fund, capital outlays are generally separately reported in the

expenditures reported on the statement of revenues, expenditures, and

changes in fund balances.

g.

7

$150,000 = the amount of the state grant. The bond proceeds would be

reported as an other financing source.

h.

13

$500,000 = the amount of the expenditures in the capital projects fund

i.

11

$345,000 = Fund Balance-Unassigned on 1/1/X1

$

110,000

Add: Grant revenues

$150,000

Other financing sources

610,000

760,000

Less: Expenditures

$500,000

Fund balance – assigned

for encumbrances

25,000

(525,000)

Fund Balance – Unassigned

on 12/31/X1

$345,000

Chapter 17 – Governmental Entities: Introduction and General Fund Accounting

17–36

P17-20 Identifying Types of Revenue Transactions

1. B

2. E

3. D

4. A

5. B

6. E

7. C

8. D

9. C

10. D

11. C

12. D

13. D

14. D