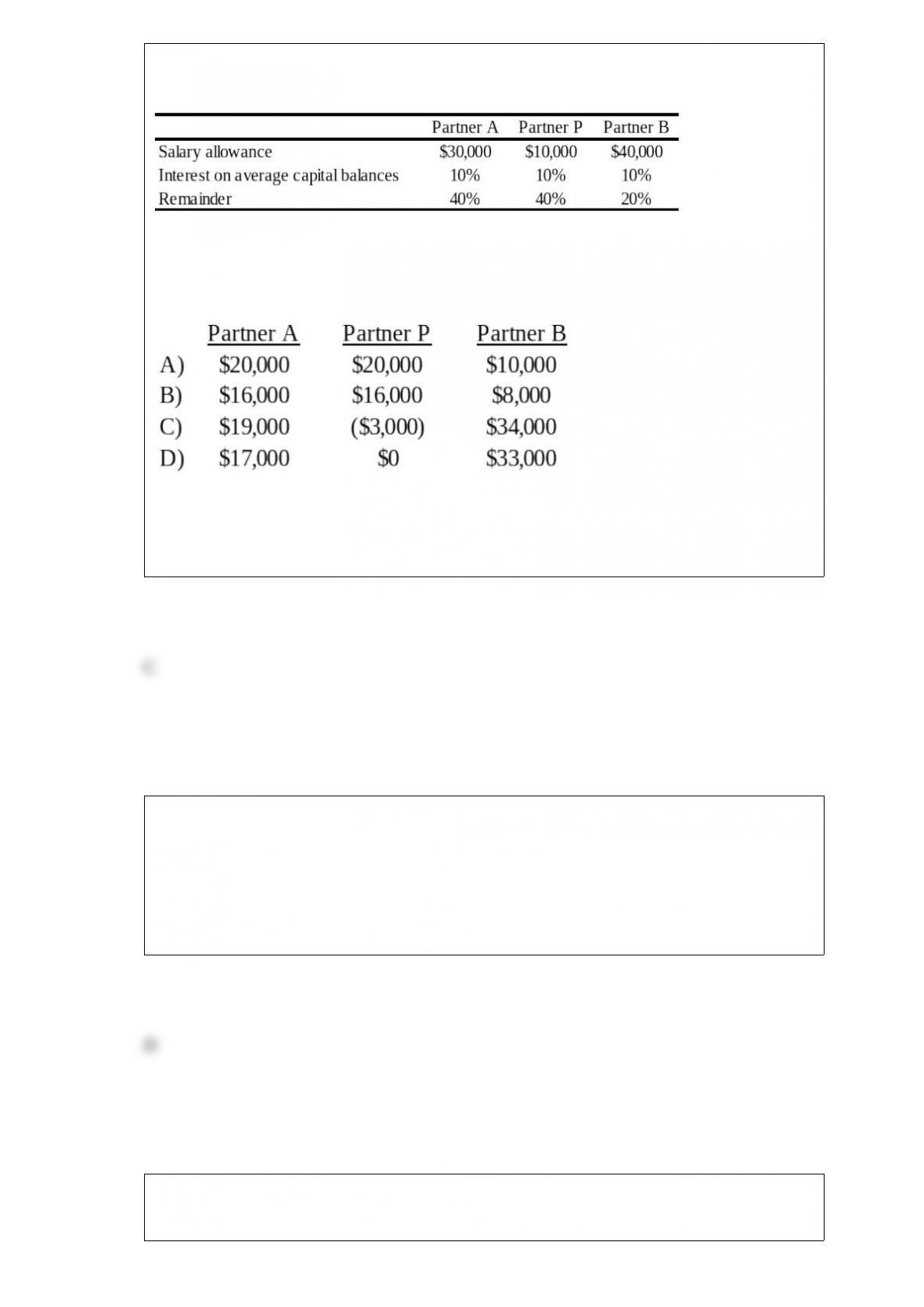

The APB partnership agreement specifies that partnership net income be allocated as

follows:

Average capital balances for the current year were $50,000 for A, $30,000 for P, and

$20,000 for B.

Refer to the information given. Assuming a current year net income of $50,000, what

amount should be allocated to each partner?

A. Option A

B. Option B

C. Option C

D. Option D

Which of the financial statements described below is prepared by the general fund of a

state or local government?

A. A statement of cash flows.

B. An income statement.

C. A statement of revenues, expenses, and changes in retained earnings.

D. A statement of revenues, expenditures, and changes in fund balance.

On June 30, 20X9, a voluntary health and welfare organization received pledges from

donors amounting to $50,000. The donors did not place any time or use restrictions on

the amount pledged. It was estimated that 10 percent of the pledges would not be

collected. How should the voluntary health and welfare organization report these

pledges on its financial statements prepared at the end of its fiscal year, June 30, 20X9?

A. As fund balance for $45,000.

B. As contribution revenue-unrestricted for $45,000.

C. As contribution revenue-unrestricted for $50,000.

D. As fund balance-unrestricted for $50,000.

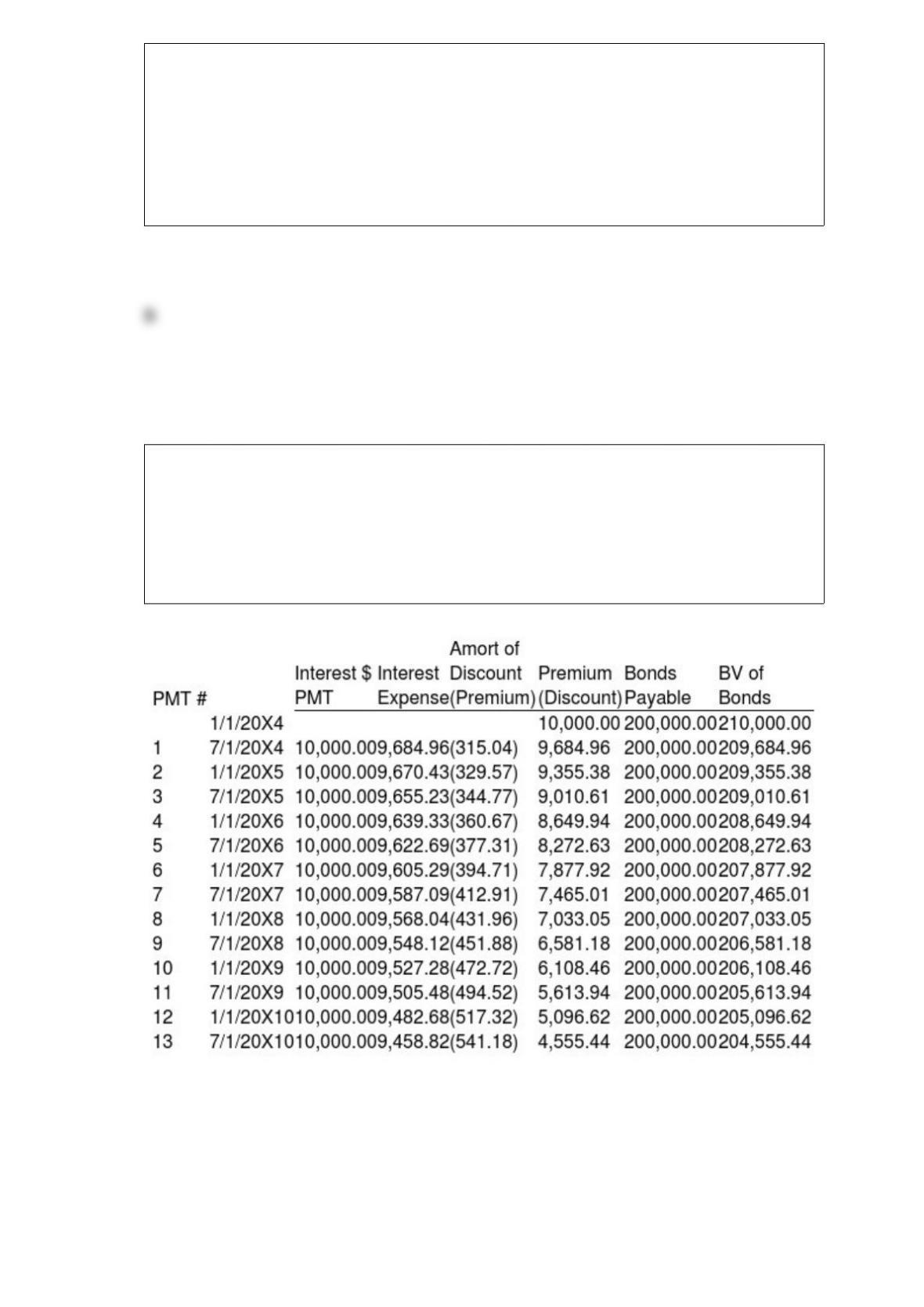

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on January 1, 20X8, for $122,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of gain or loss on bond retirement

will be reported in the 20X8 consolidated financial statements?

A. $84,018 loss

B. $84,108 gain

C. $22,923 loss

D. $22,923 gain

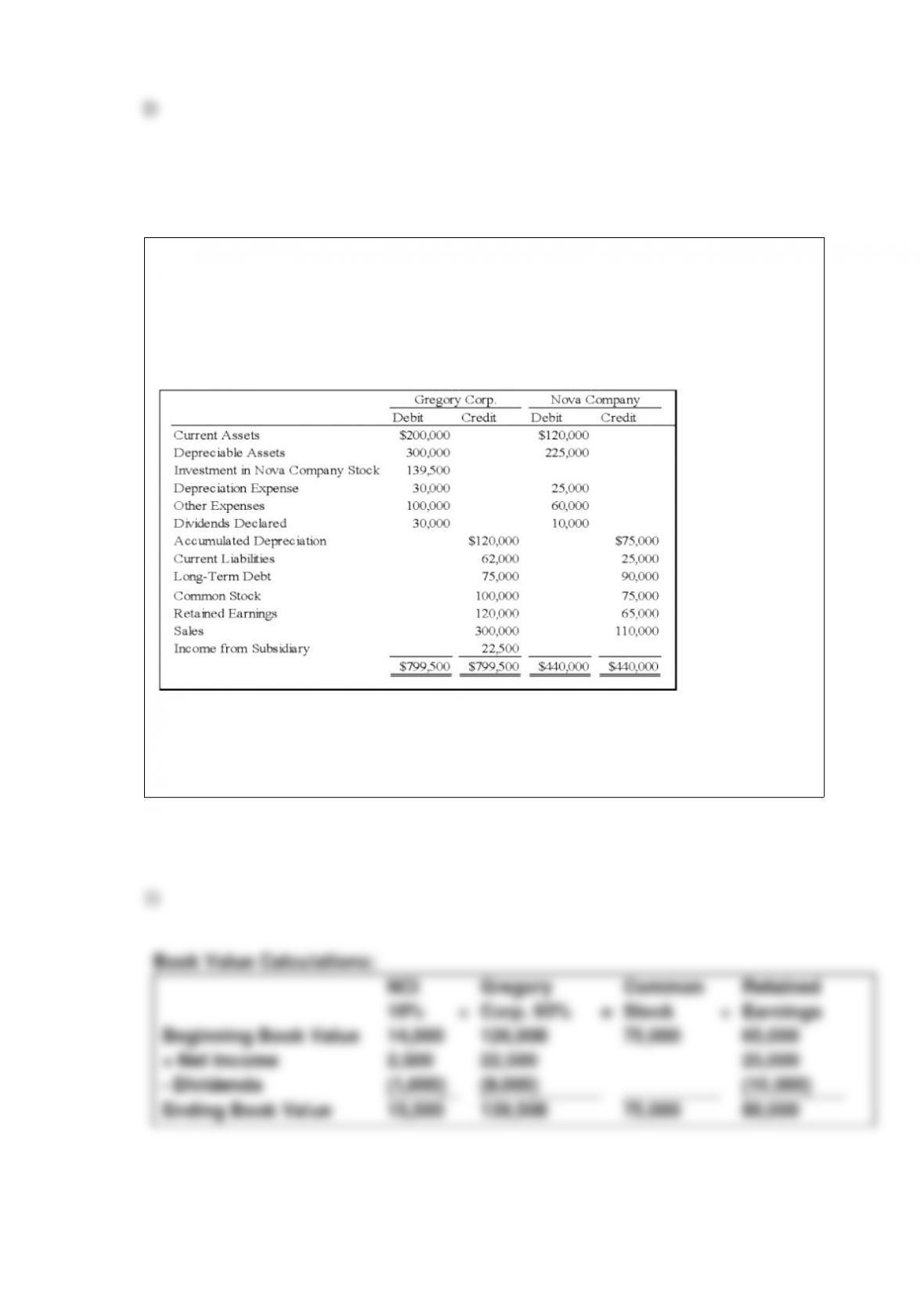

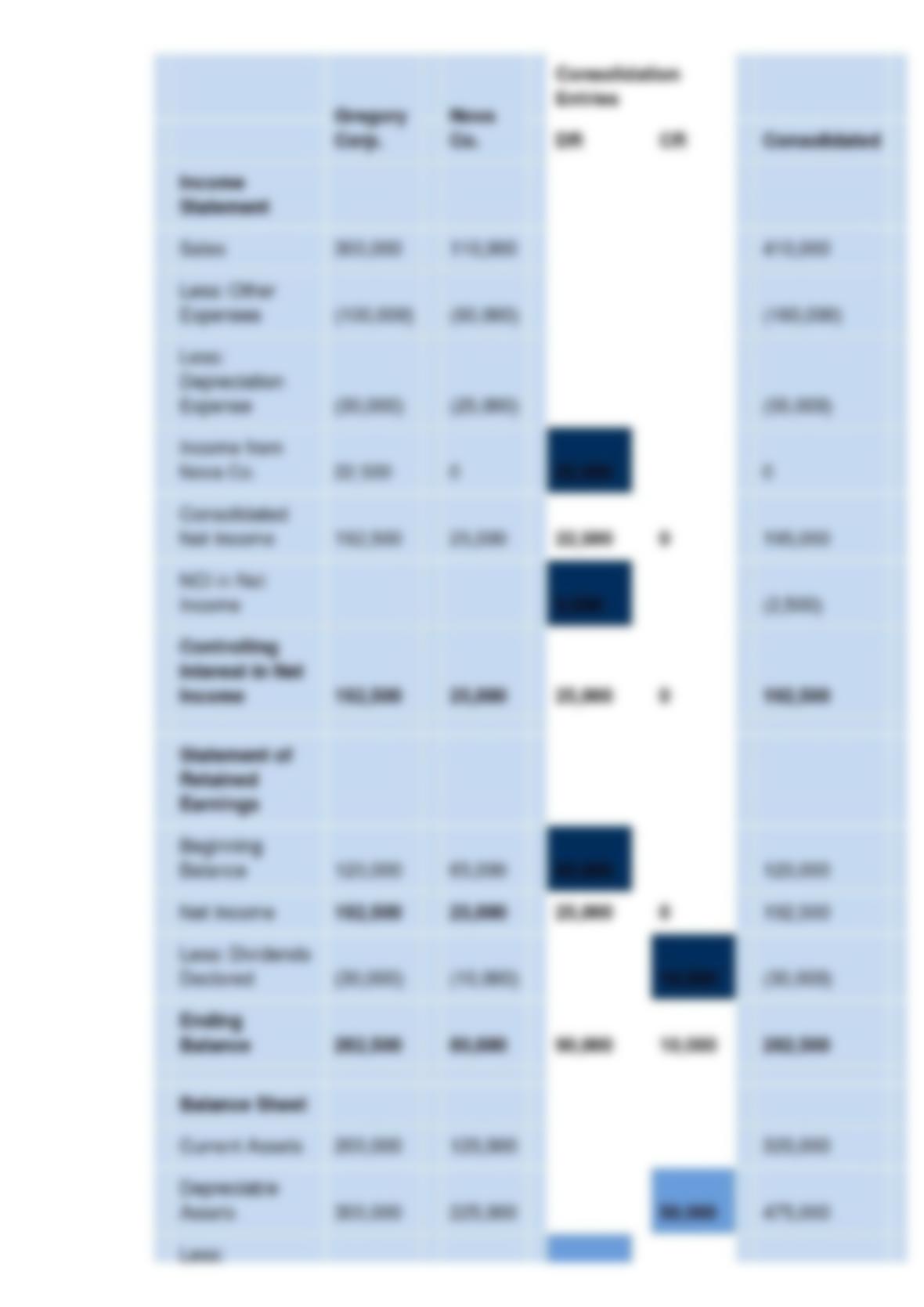

On January 1, 20X8, Gregory Corporation acquired 90 percent of Nova Company’s

voting stock, at underlying book value. The fair value of the noncontrolling interest was

equal to 10 percent of the book value of Nova at that date. Gregory uses the equity

method in accounting for its ownership of Nova. On December 31, 20X8, the trial

balances of the two companies are as follows:

Required:

1) Provide all consolidating entries required as of December 31, 20X8, to prepare

consolidated financial statements.

2) Prepare a three-part consolidation worksheet.

On December 31, 20X8, Melkor Corporation acquired 80 percent of Sydney Company’s

common stock for $160,000. At that date, the fair value of the noncontrolling interest

was $40,000. Of the $75,000 differential, $10,000 related to the increased value of

Sydney’s inventory, $20,000 related to the increased value of its land, and $25,000

related to the increased value of its equipment that had a remaining life of 10 years

from the date of combination. Sydney sold all inventory it held at the end of 20X8

during 20X9. The land to which the differential related was also sold during 20X9 for a

large gain. At the date of combination, Sydney reported retained earnings of $75,000

and common stock outstanding of $50,000. In 20X9, Sydney reported net income of

$60,000, but paid no dividends. Melkor accounts for its investment in Sydney using the

equity method.

Based on the preceding information, the amount of goodwill reported in the

consolidated financial statements prepared immediately after the combination is:

A. $0

B. $32,500

C. $26,000

D. $20,000

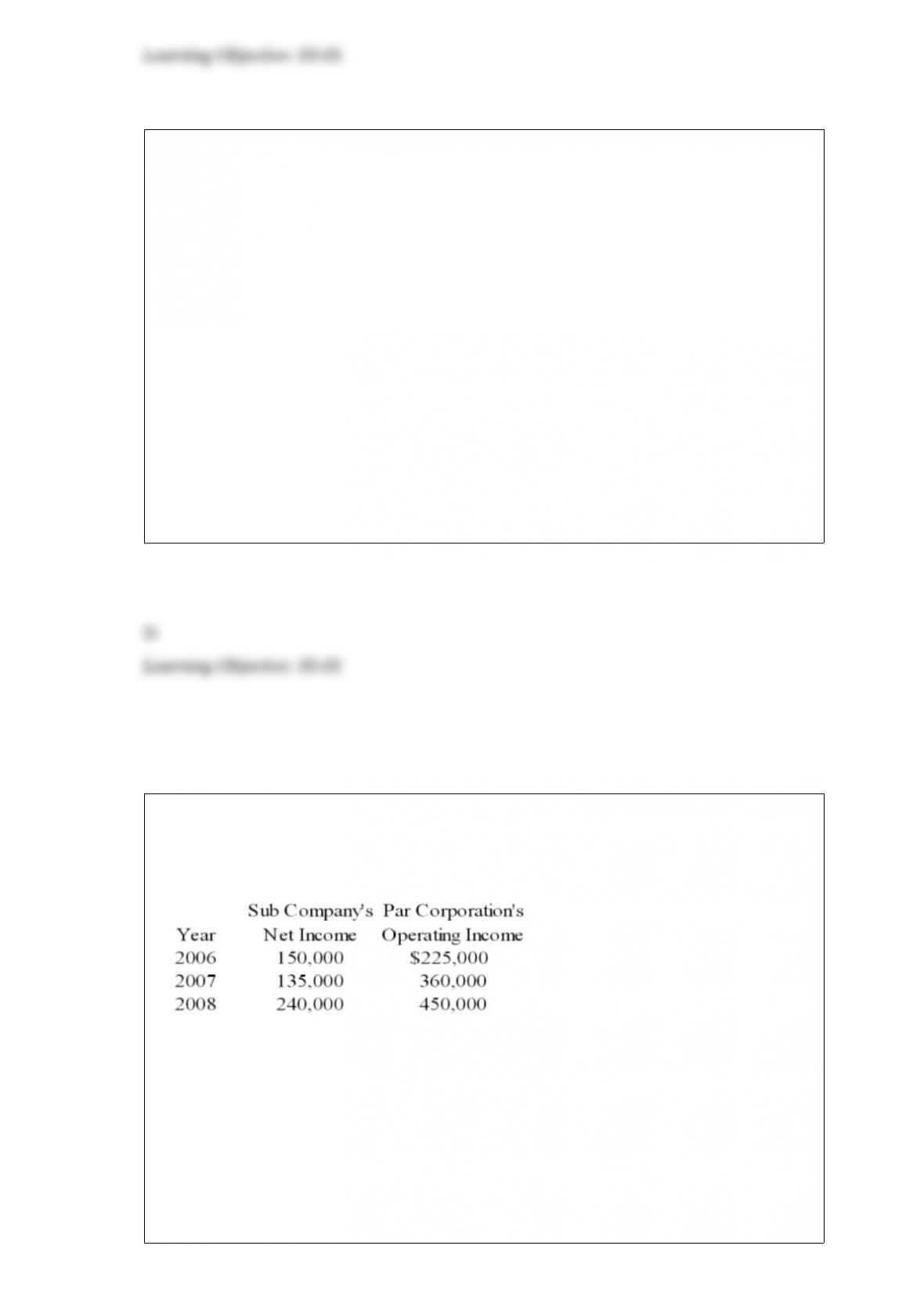

Sub Company sells all its output at 20 percent above cost to Par Corporation. Par

purchases its entire inventory from Sub. The incomes reported by the companies over

the past three years are as follows:

Sub Company sold inventory for $300,000, $262,500 and $337,500 in the years 20X6,

20X7, and 20X8 respectively. Par Company reported ending inventory of $105,000,

$157,500 and $180,000 for 20X6, 20X7, and 20X8 respectively. Par acquired 70

percent of the ownership of Sub on January 1, 20X6, at underlying book value. The fair

value of the noncontrolling interest at the date of acquisition was equal to 30 percent of

the book value of Sub Company.

Based on the information given above, what will be the income to noncontrolling

interest for 20X8?

A. $39,750

B. $37,875

C. $71,275

D. $70,875

For a subsidiary to be eligible to be included in a consolidated tax return, at least _____

of its stock must be held by the parent company or another company included in the

consolidated return.

A. 50 percent

B. 40 percent

C. 75 percent

D. 80 percent

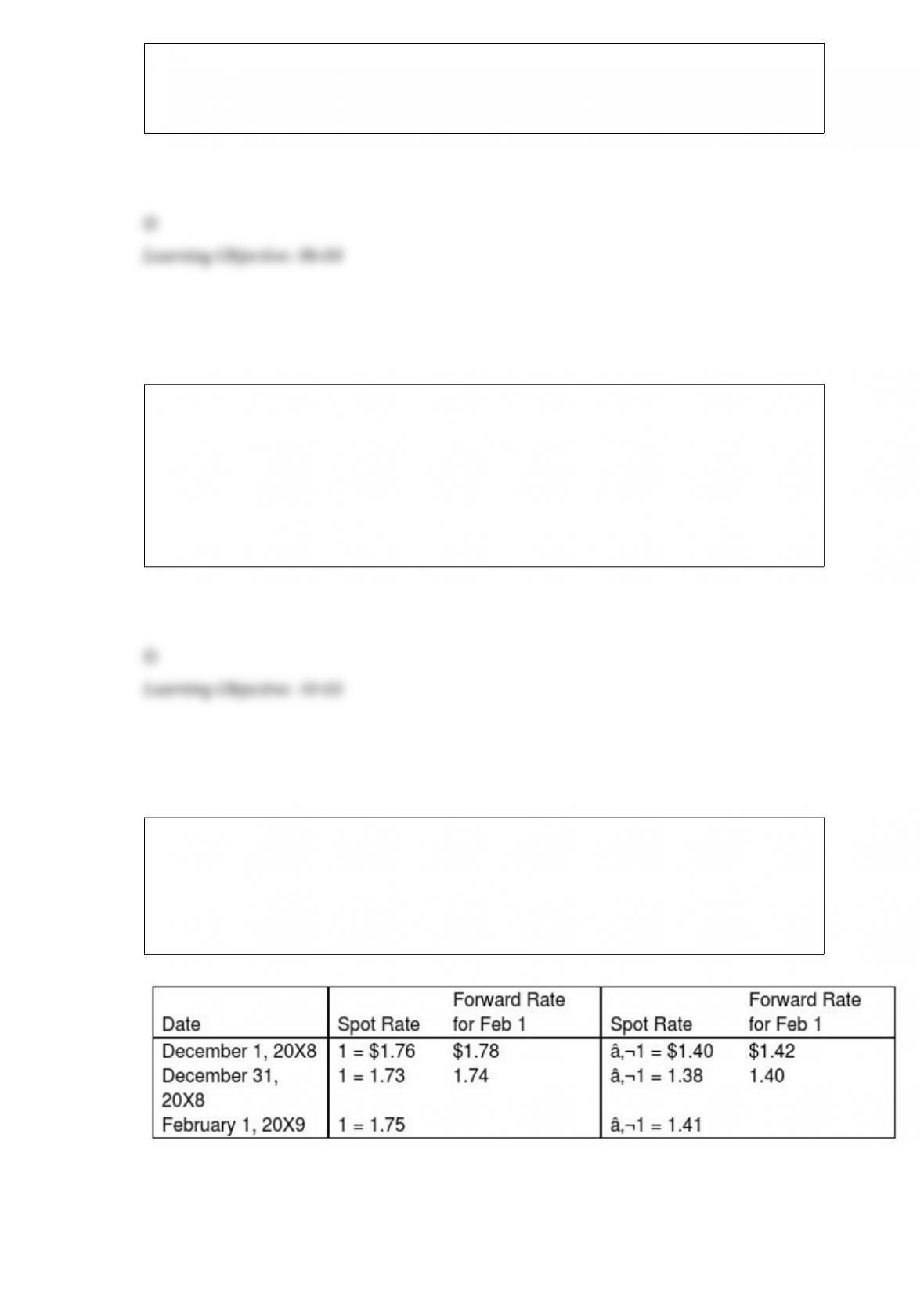

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the net gain or loss on the British pound

speculative contract?

A. $8,000 gain

B. $6,000 gain

C. $3,000 loss

D. $10,000 gain

Perfect Corporation acquired 70 percent of Trevor Company’s shares on December 31,

2008, for $140,000. At that date, the fair value of the noncontrolling interest was

$60,000. On January 1, 2010, Perfect acquired an additional 10 percent of Trevor’s

common stock for $32,500. Summarized balance sheets for Trevor on the dates

indicated are as follows:

Trevor paid dividends of $10,000 in each of the three years. Perfect uses the fully

adjusted equity method in accounting for its investment in Trevor and amortizes all

differentials over 5 years against the related investment income. All differentials are

assigned to patents in the consolidated financial statements.

Based on the preceding information, Trevor Company’s net income for 2009 and 2010

are:

A. $10,000 and $20,000 respectively.

B. $25,000 and $35,000 respectively.

C. $35,000 and $45,000 respectively.

D. $25,000 and $45,000 respectively.

In order to reduce the risk associated with a new line of business, Conservative

Corporation established Spin Company as a wholly owned subsidiary. It transferred

assets and accounts payable to Spin in exchange for its common stock. Spin recorded

the following entry when the transaction occurred:

Based on the preceding information, what number of shares of $7 par value stock did

Spin issue to Conservative?

A. 10,000

B. 7,000

C. 8,000

D. 25,000

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital’s statement

of operations for the year ended December 31, 20X8.

Transaction: Endowment income was earned. The donor placed no restrictions on the

investment earnings.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

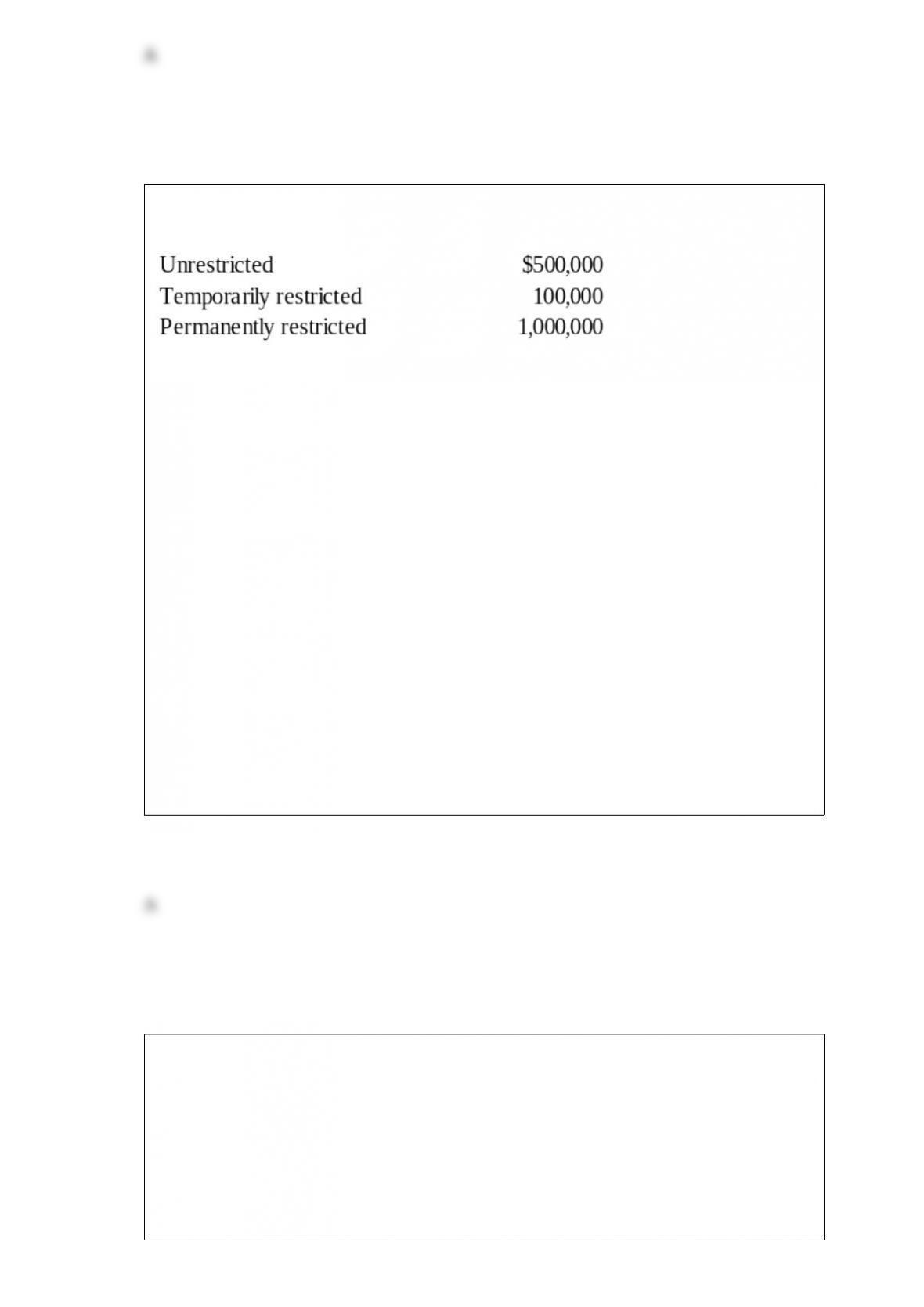

Local Services, a voluntary health and welfare organization had the following classes of

net assets on July 1, 20X8, the beginning of its fiscal year:

During the year ended June 30, 20X9, the following events occurred:

(1) It purchased equipment, costing $100,000, with contributions restricted for this

purpose. The contributions had been received from donors during June of 20X8.

(2) It received $130,000 of cash donations which were restricted for research activities.

During the year ended June 30, 20X9, $90,000 of the contributions were expended on

research.

(3) It sold investments classified in the permanently restricted class for a loss of

$40,000. Dividends and interest income earned on the investments amounted to

$70,000. There were no restrictions on how investment income was to be used.

(4) It received cash contributions of $200,000 from donors who did not place either

time or use restrictions upon their donations.

(5) Expenses, excluding depreciation expense, for program services and supporting

services incurred during the year ended June 30, 20X9, amounted to $260,000.

(6) Depreciation expense for the year ended June 30, 20X9, was $80,000.

Refer to the above information. On the statement of activities for the year ended June

30, 20X9, reclassifications would be reported at

A. $190,000.

B. $100,000.

C. $90,000.

D. $230,000.

On January 1, 20X8, Transport Corporation acquired 75 percent interest in Steamship

Company for $300,000. Steamship is a Norwegian company. The local currency is the

Norwegian kroner (NKr). The acquisition resulted in an excess of cost-over-book value

of $25,000 due solely to a patent having a remaining life of 5 years. Transport uses the

fully adjusted equity method to account for its investment. Steamship’s December 31,

20X8, trial balance has been translated into U.S. dollars, requiring a translation

adjustment debit of $8,000. Steamship’s net income translated into U.S. dollars is

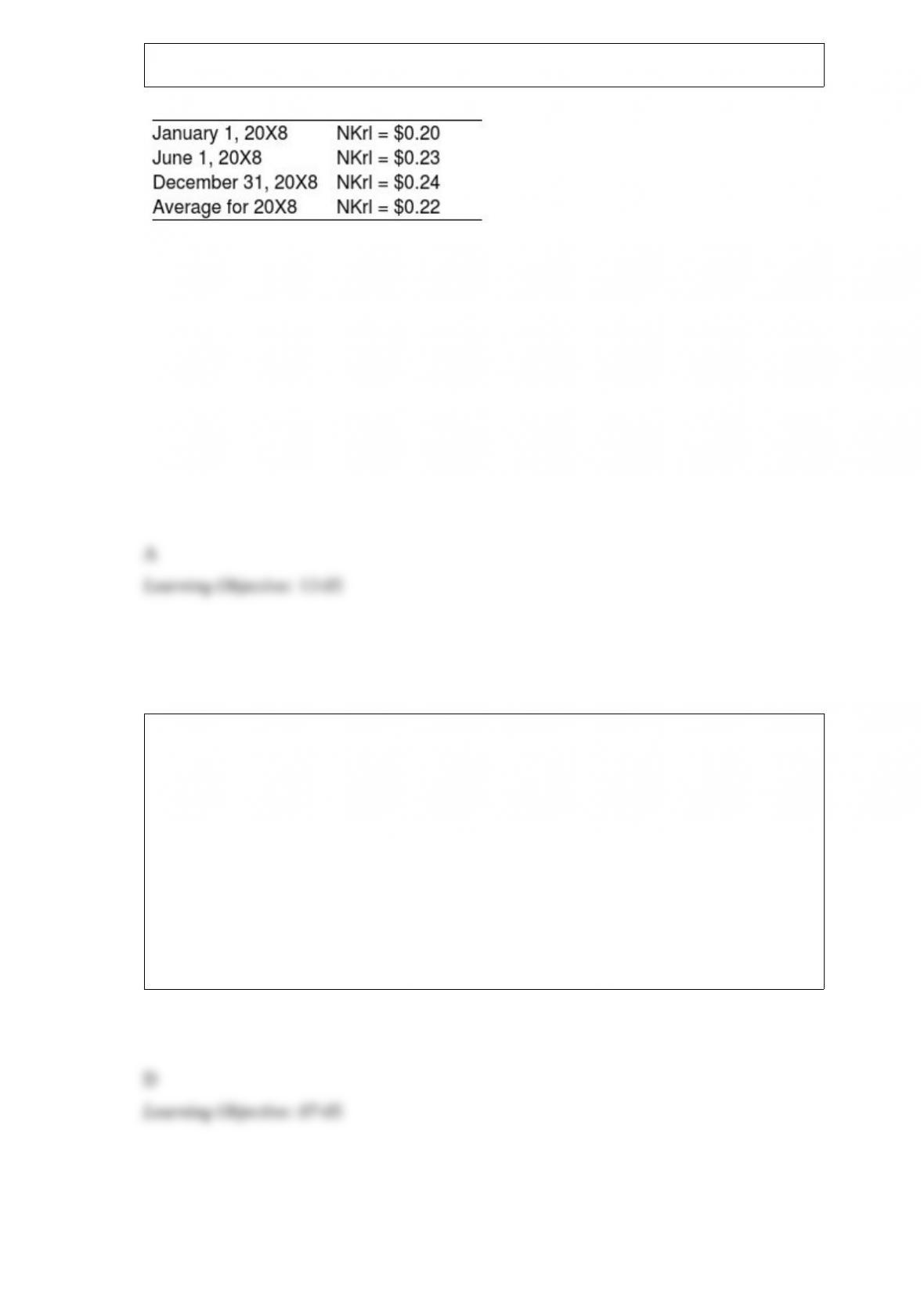

$35,000. It declared and paid an NKr 20,000 dividend on June 1, 20X8. Relevant

exchange rates are as follows:

Assume the kroner is the functional currency.

Based on the preceding information, in the journal entry to record the receipt of dividend

from Steamship,

A. Investment in Steamship Company will be credited for $3,450.

B. Cash will be debited for $3,300.

C. Investment in Steamship Company will be credited for $4,000.

D. Cash will be debited for $3,600.

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite

for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment

is expected to have a 10-year useful life and no salvage value. Both companies

depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X9 consolidated

income statement, depreciation expense will be:

A. debited for $25,000 in the consolidating entries.

B. credited for $15,000 in the consolidating entries.

C. debited for $15,000 in the consolidating entries.

D. credited for $25,000 in the consolidating entries.

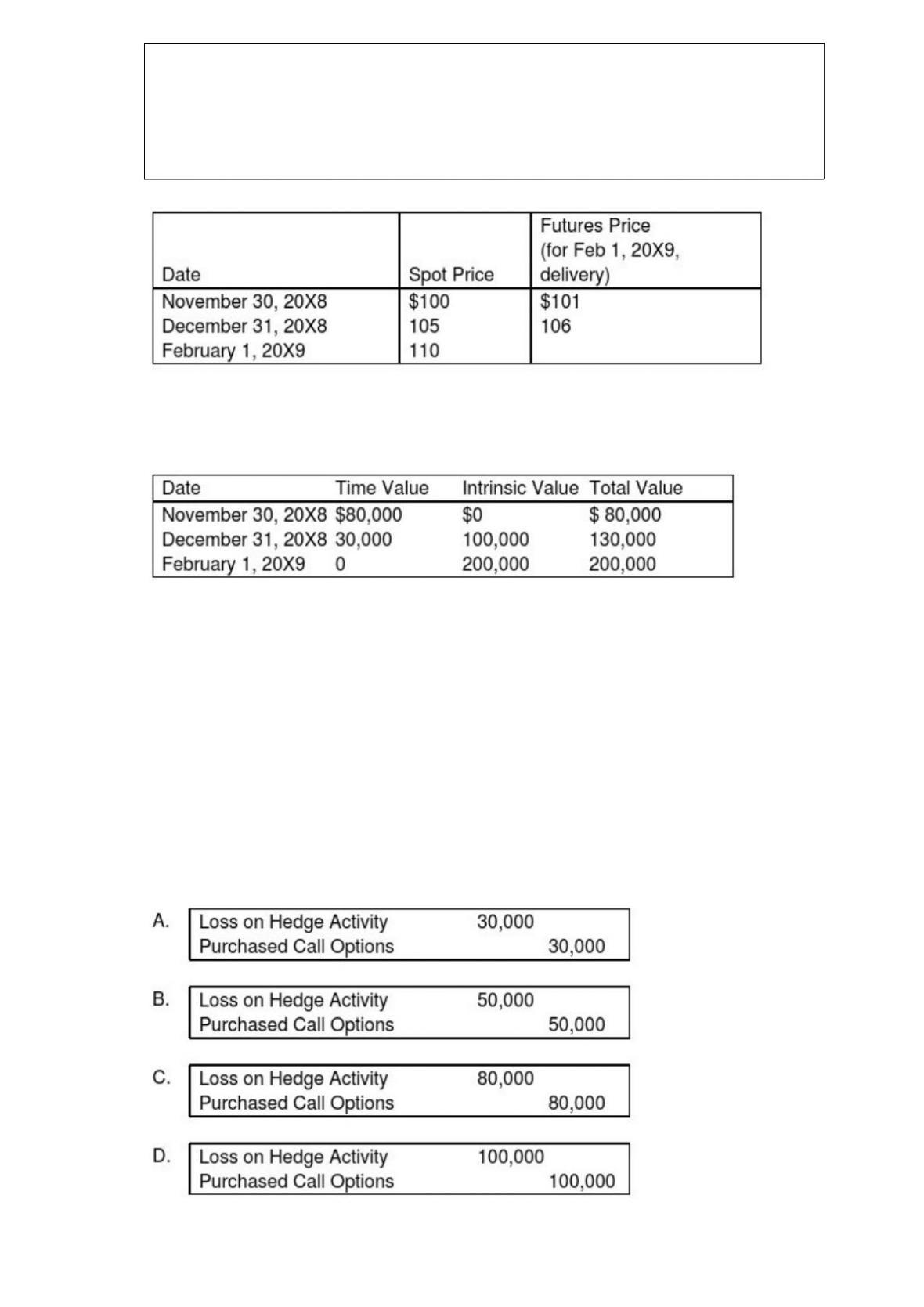

Spiralling crude oil prices prompted AMAR Company to purchase call options on oil as

a price-risk-hedging device to hedge the expected increase in prices on an anticipated

purchase of oil. On November 30, 20X8, AMAR purchases call options for 20,000

barrels of oil at $100 per barrel at a premium of $4 per barrel, with a February 1, 20X9,

call date. The following is the pricing information for the term of the call:

The information for the change in the fair value of the options follows:

On February 1, 20X9, AMAR sells the options at their value on that date and acquires

20,000 barrels of oil at the spot price. On April 1, 20X9, AMAR sells the oil for $112 per

barrel.

Based on the preceding information, which of the following adjusting entries would be

required on December 31, 20X8?

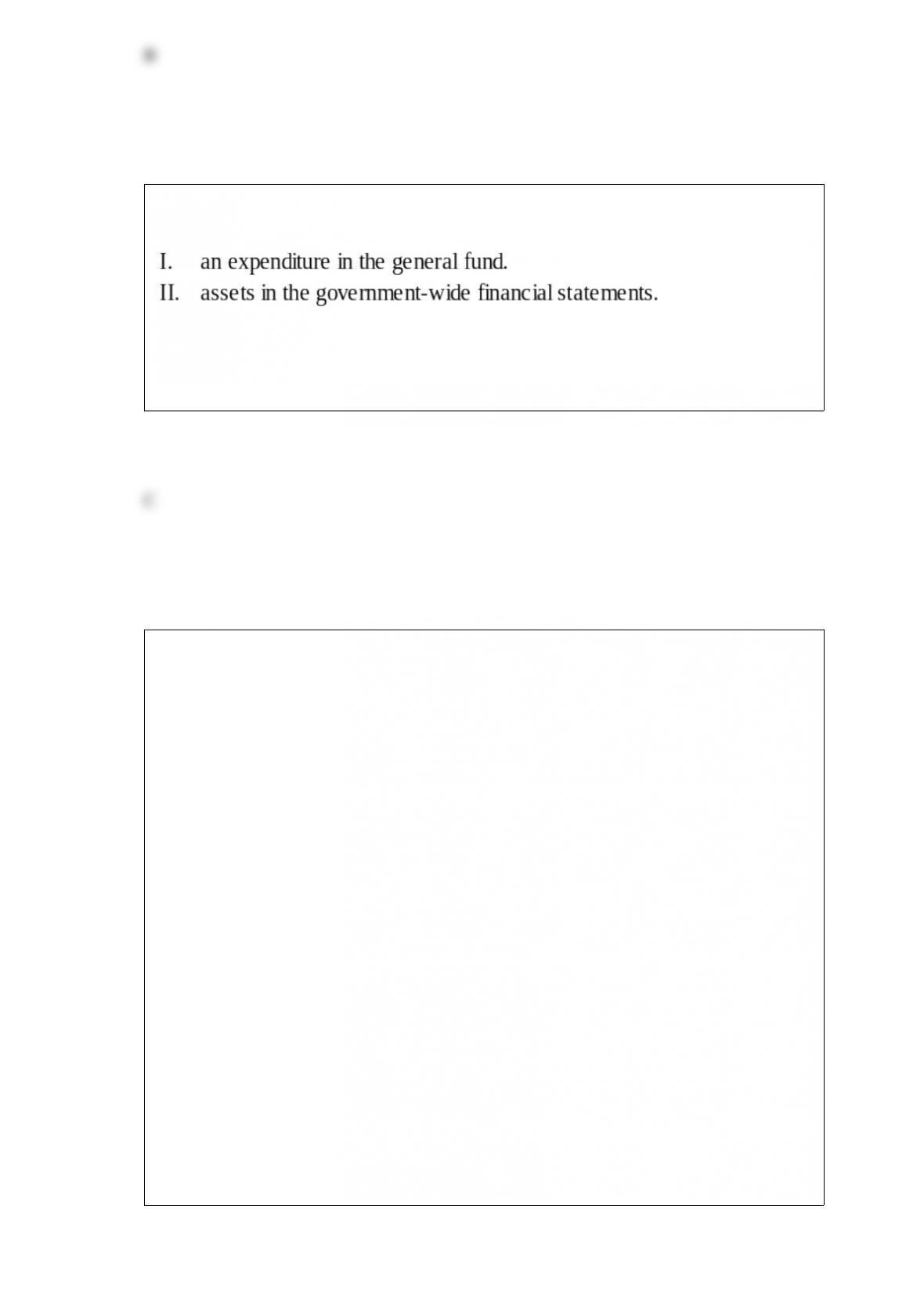

Works of art and historical treasures purchased by the general fund should be reported

as:

A. I only.

B. II only.

C. Both I and II

D. Neither I nor II.

Michigan-based Leo Corporation acquired 100 percent of the common stock of a

British company on January 1, 20X8, for $1,100,000. The British subsidiary’s net assets

amounted to 500,000 pounds on the date of acquisition. On January 1, 20X8, the book

values of its identifiable assets and liabilities approximated their fair values. As a result

of an analysis of functional currency indicators, Leo determined that the British pound

was the functional currency. On December 31, 20X8, the British subsidiary’s adjusted

trial balance, translated into U.S. dollars, contained $17,000 more debits than credits.

The British subsidiary reported income of 33,000 pounds for 20X8 and paid a cash

dividend of 8,000 pounds on October 25, 20X8. Included on the British subsidiary’s

income statement was depreciation expense of 3,500 pounds. Leo uses the fully

adjusted equity method of accounting for its investment in the British subsidiary and

determined that goodwill in the first year had an impairment loss of 25 percent of its

initial amount. Exchange rates at various dates during 20X8 follow:

January 1 1 = $2.10

October 25 1 = 2.25

December 31 1 = 2.20

Average for 20X8 1 = 2.21

Based on the preceding information, on Leo’s consolidated balance sheet at December

31, 20X8, what amount should be reported for the goodwill acquired on January 1,

20X8?

A. $36,845

B. $39,286

C. $36,905

D. $36,607

A subsidiary issues bonds. The parent can then acquire the bonds either directly from

the subsidiary or from a nonaffiliate that had originally acquired the subsidiary’s bonds.

Required:

a) Discuss the parent’s accounting as it relates to the preparation of consolidated

financial statements, for their acquisition of the bonds:

1) from the nonaffiliate.

2) directly from the subsidiary.

b) Why does it matter who the bonds are acquired from?

Fixed assets of an enterprise fund should be accounted for in the

A. Enterprise fund but no depreciation on the fixed assets should be recorded.

B. General fixed asset account group but no depreciation on the fixed assets should be

recorded.

C. General fixed asset account group and depreciation on the fixed assets should be

recorded.

D. Enterprise fund and depreciation on the fixed assets should be recorded.

A trust fund of Bruge City received $100,000 from a donor during the year ended June

30, 20X9. During the year ended June 30, 20X9, $94,000 of the cash received was used

to provide food and clothing to the city’s poor. How should the trust fund report these

resource flows on its statement of changes in fiduciary net assets for the year ended

June 30, 20X9?

A. As revenues of $100,000 and as expenditures of $94,000.

B. As contributions for $100,000 and as deductions for benefits for $94,000.

C. As revenues of $100,000 and as an operating transfer out for $94,000.

D. As a transfer in from trust fund for $100,000 and as a transfer out for $94,000.

Which of the following observations is NOT consistent with the cost method of

accounting?

A. Investee dividends from earnings since acquisition by investor are treated as a

reduction of the investment.

B. Investments are carried by the investor at historical cost.

C. No journal entry is made regarding the earnings of the investee.

D. It is consistent with the treatment normally accorded noncurrent assets.

Master Corporation owns 85 percent of Servant Corporation’s voting shares. On

January 1, 20X8, Master Corporation sold $200,000 par value 8 percent bonds to

Servant when the market interest rate was 5 percent. The bonds mature in 10 years and

pay interest semiannually on June 30 and Dec 31.

Based on the information given above, in the preparation of the 20X8 consolidated

financial statements, premium on bonds payable will be:

A. debited for $46,767 in the consolidating entries.

B. credited for $43,060 in the consolidating entries.

C. debited for $43,060 in the consolidating entries.

D. credited for $46,767 in the consolidating entries.

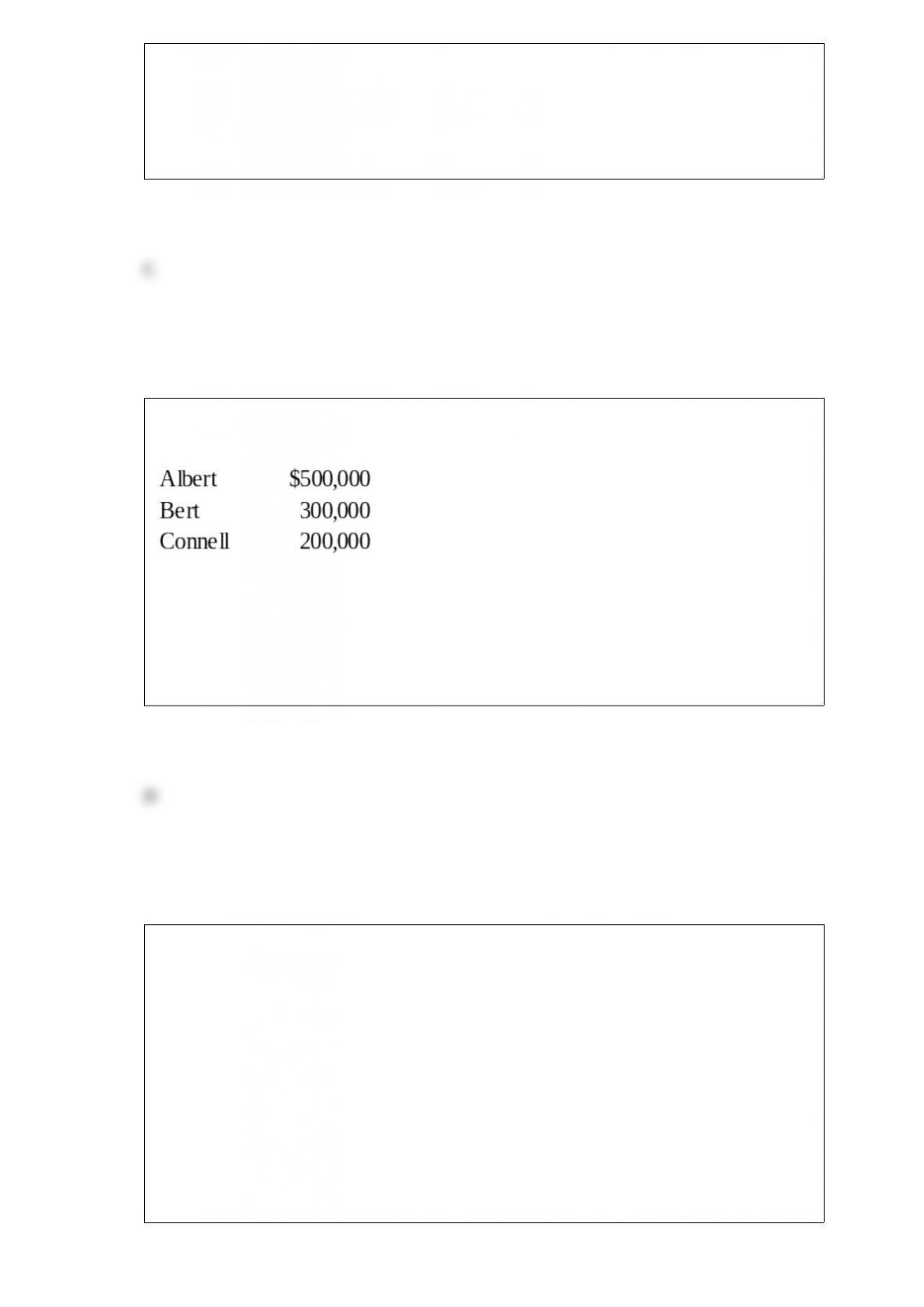

In the ABC partnership (to which Daniel seeks admittance), the capital balances of

Albert, Bert, and Connell, who share income in the ratio of 5:3:2 are:

Based on the preceding information, if no goodwill or bonus is recorded, how much

should Daniel invest for a 20 percent interest?

A. $400,000

B. $200,000

C. $300,000

D. $250,000

Grant, Inc. (Grant) acquired 30% of South Co.’s (South) voting stock for $200,000 on

January 1, 20X1. Grant’s 30% interest in South gave Grant the ability to exercise

significant influence over South’s operating and financial policies. On that date, South

reported assets of $500,000 and liabilities of $100,000. South had equipment with a

book value of $60,000 that was actually worth $160,000. The equipment had a

remaining useful life of five years. During 20X1, South reported net income of $80,000

and paid dividends of $50,000. What amount of income should Grant recognize in

20X1 as a result of this investment?

A. $18,000

B. $4,000

C. $15,000

D. $16,750

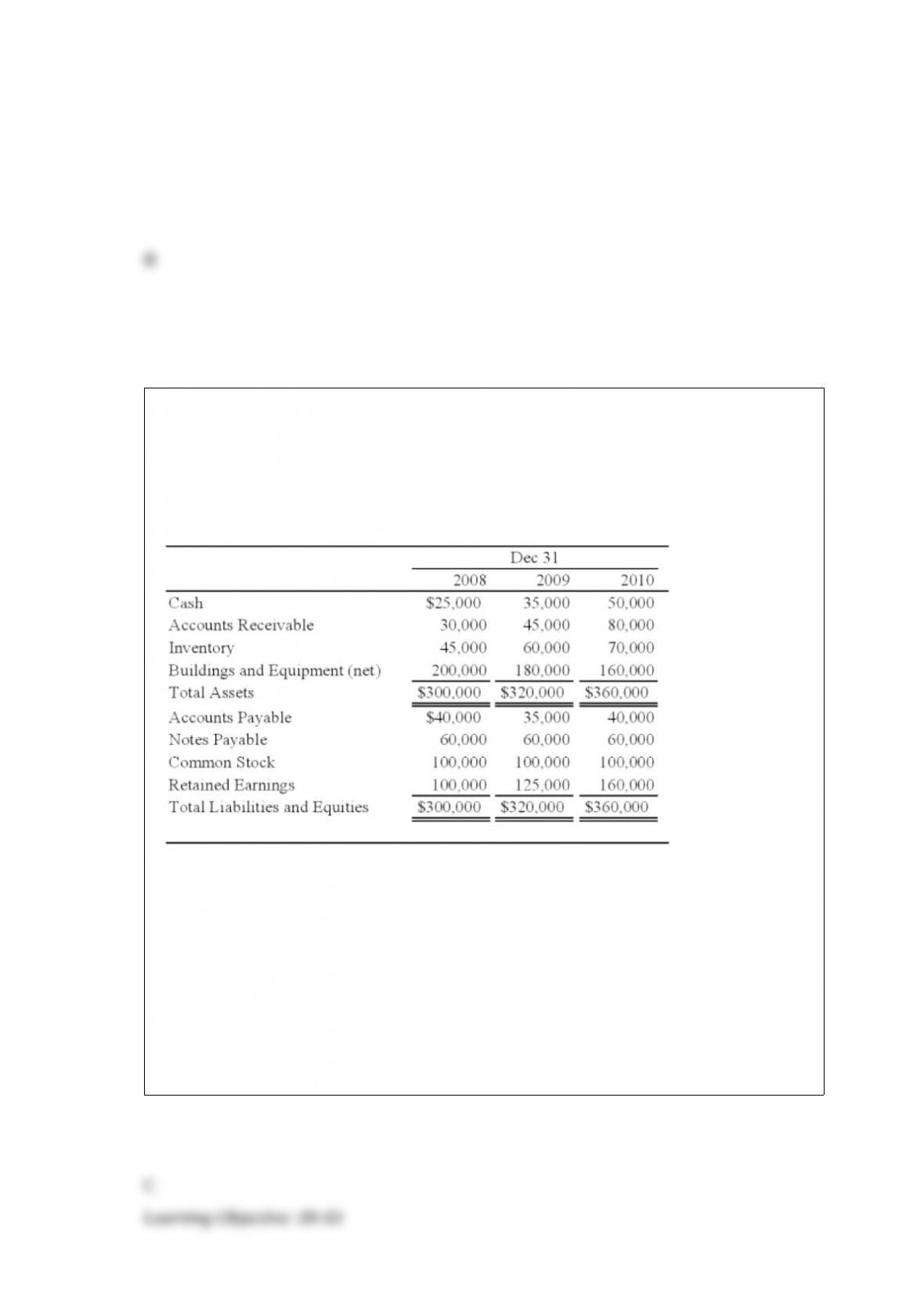

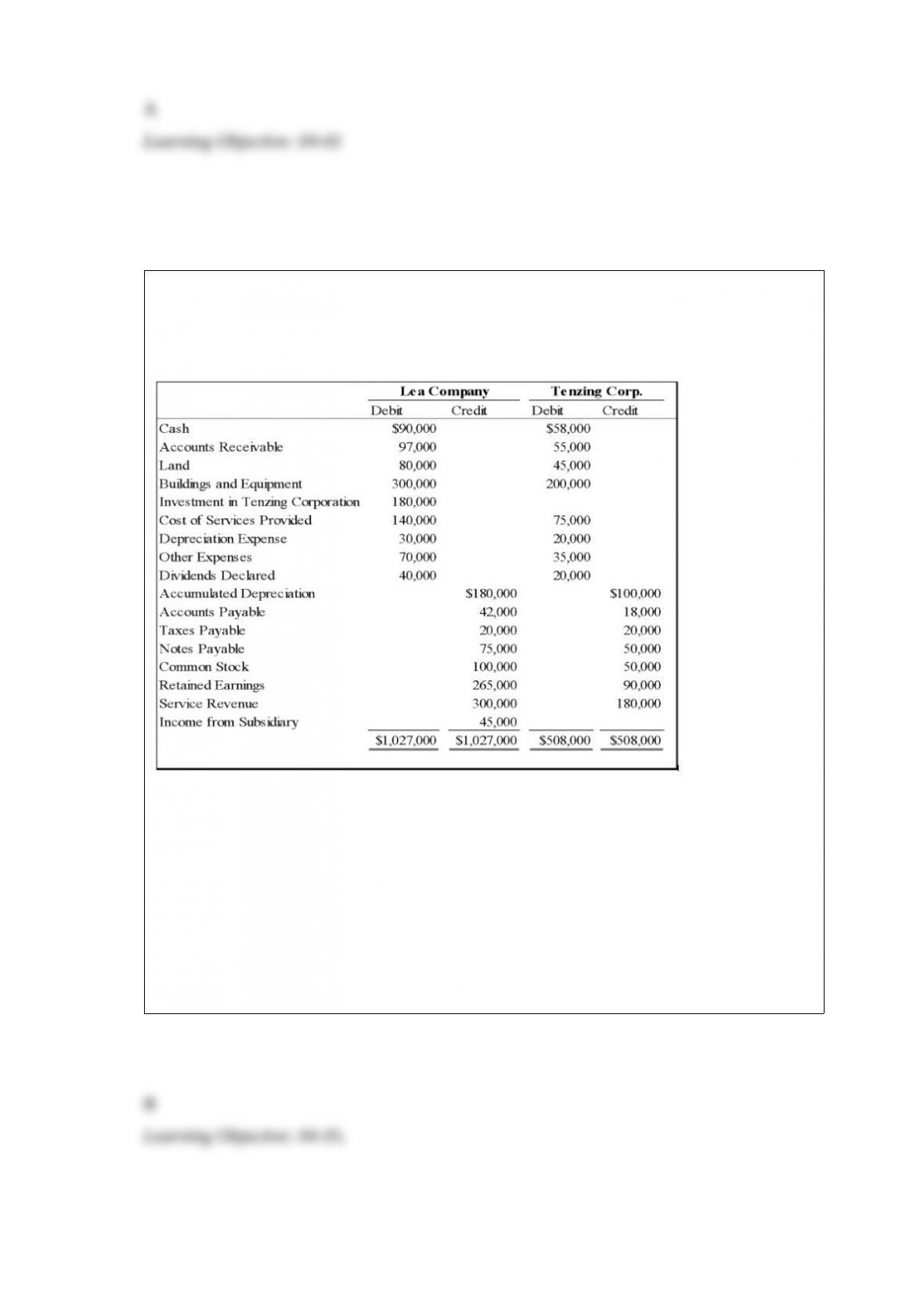

Lea Company acquired all of Tenzing Corporation’s stock on January 1, 20X6 for

$150,000 cash. On December 31, 20X8, the trial balances of the two companies were as

follows:

Tenzing Corporation reported retained earnings of $75,000 at the date of acquisition.

The difference between the acquisition price and underlying book value is assigned to

buildings and equipment with a remaining economic life of five years from the date of

acquisition. At December 31, 20X8, Tenzing owed Lea $4,000 for services provided.

Based on the preceding information, what amount of total liabilities will be reported in

the consolidated balance sheet for 20X8?

A. $225,000

B. $221,000

C. $217,000

D. $137,000

Clay University, a not-for-profit university, earned $300,000 from bookstore revenue

and spent $100,000 for faculty research in 20X1. The $100,000 for faculty research

came from a $150,000 research grant received in the previous year. What is the effect of

these events on unrestricted net assets in 20X1?

A. Increase $450,000

B. Increase $400,000

C. Increase $300,000

D. Increase $200,000

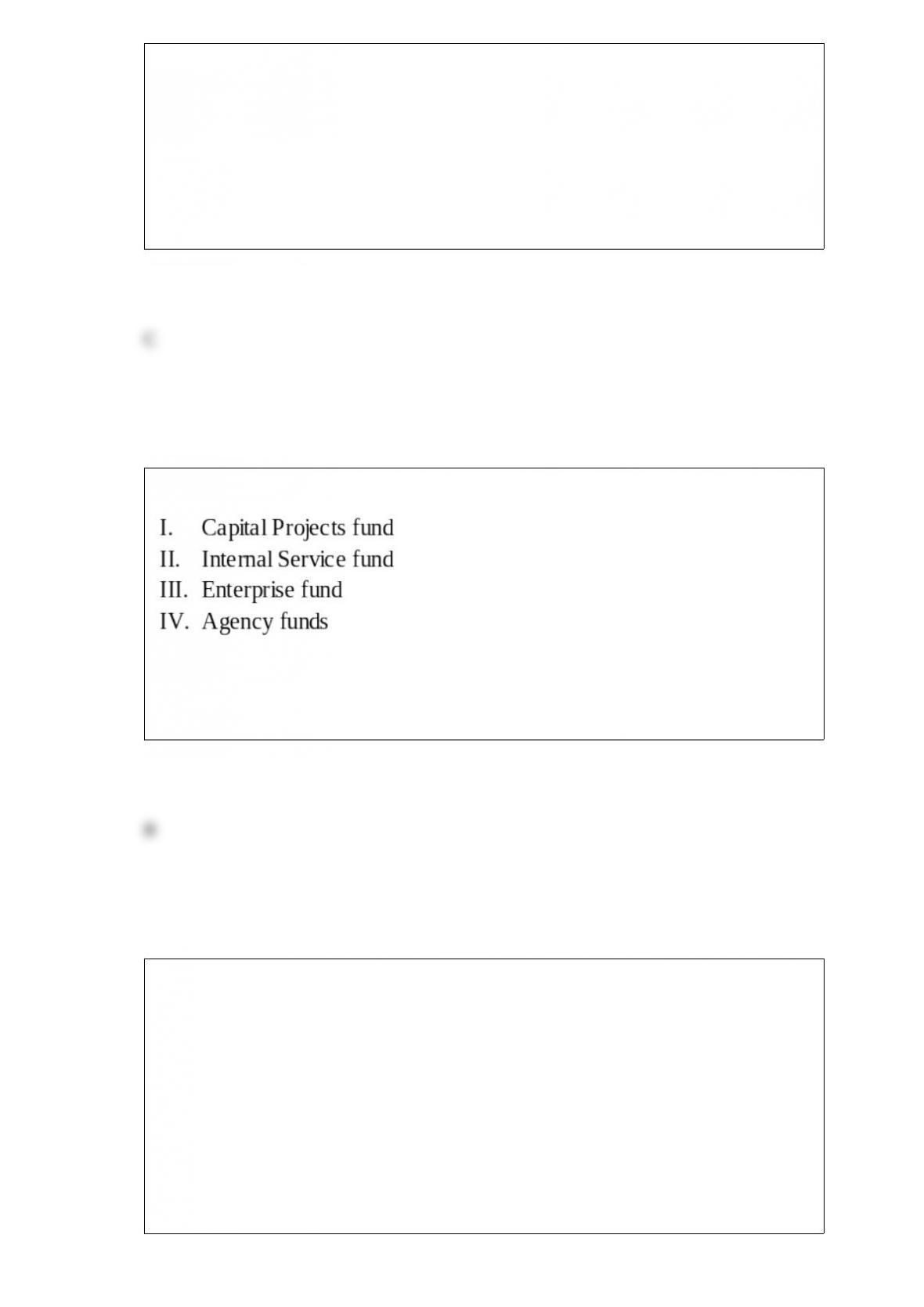

Which of the following funds report fixed assets on their balance sheets?

A. I, II

B. II, III

C. I, IV

D. III, IV

Parent Co. purchases 100 percent of Son Company on January 1, 20X1, when Parent’s

retained earnings balance is $520,000 and Son’s is $150,000. During 20X1, Son reports

$15,000 of net income and declares $6,000 of dividends. Parent reports $105,000 of

separate operating earnings plus $15,000 of equity-method income from its 100 percent

interest in Son; Parent declares dividends of $40,000.

Based on the preceding information, what is Parent’s post-closing retained earnings

balance on December 31, 20X1?

A. $485,000

B. $505,000

C. $525,000

D. $600,000

If A is the total capital of a partnership before the admission of a new partner, B is the

total capital of the partnership after the admission of the new partner, C is the amount of

the new partner’s investment, and D is the amount of capital credited to the new partner,

then there is:

A. goodwill to the new partner if B > (A + C) and D < C.

B. goodwill to the old partners if B = A + C and D > C.

C. a bonus to the new partner if B = A + C and D > C.

D. neither bonus nor goodwill if B > (A + C) and D > C.

When a new partner is admitted into a partnership and the new partner receives a capital

credit greater than the tangible assets contributed, which of the following explains the

difference?

I. The old partners’ goodwill is being recognized.

II. The new partner’s goodwill is being recognized.

A. I only

B. II only

C. Either I or II

D. Both I and II

For each of the items listed below, state whether they increase or decrease the balance

in cumulative translation adjustments (assuming a credit balance at the beginning of the

year) when the foreign currency strengthened relative to the U.S. dollar during the year.

A. Option A

B. Option B

C. Option C

D. Option D

On a partner’s personal statement of financial condition, how should liabilities be

valued?

I. Present value

II. Lower of present value or cash settlement amount

A. I

B. II

C. Both I and II

D. Neither I nor II

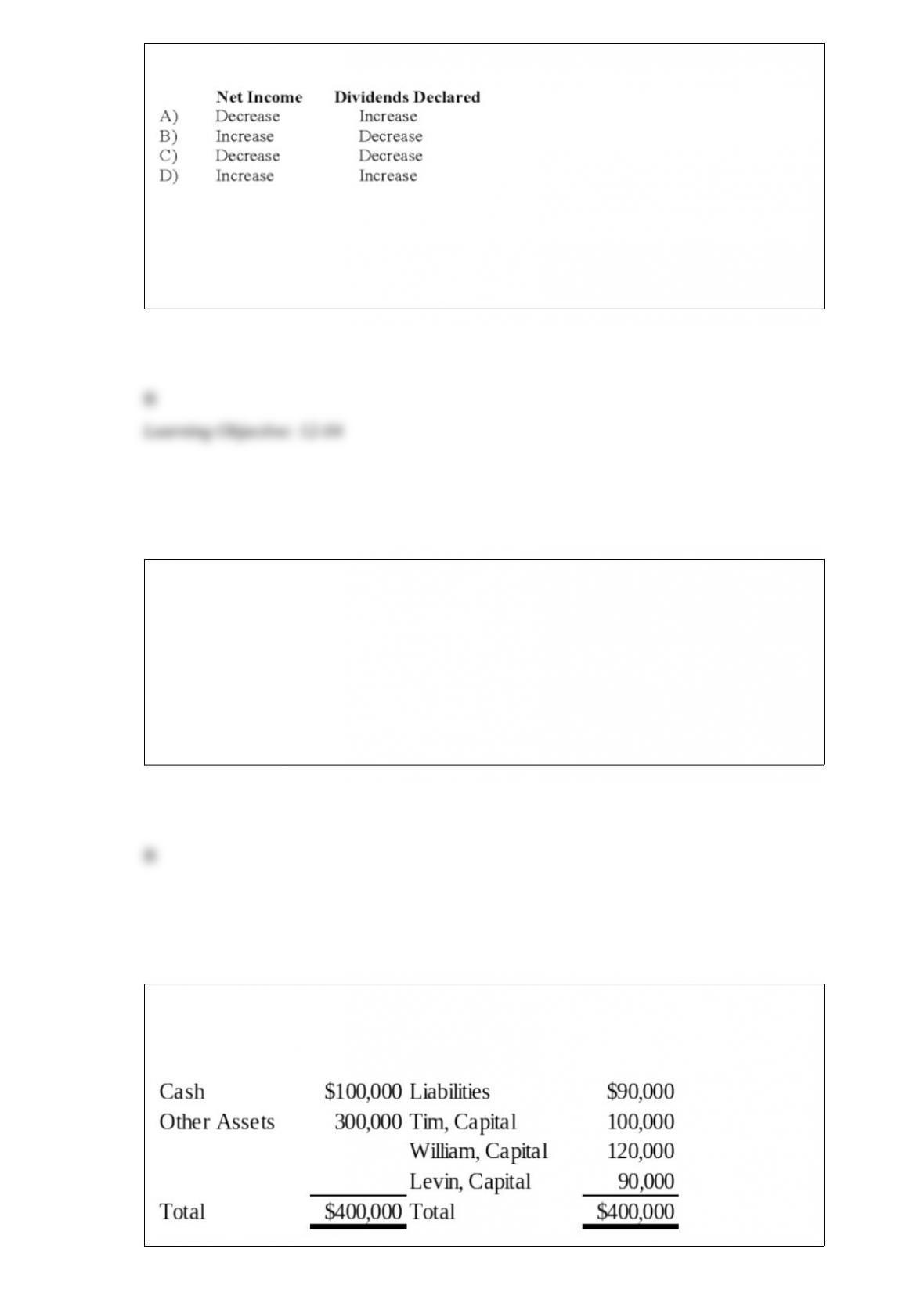

On December 1, 20X9, the partners of Tim, Williams, and Levin, who share profits and

losses in the ratio of 4:4:2, decided to liquidate their partnership. On this date the

partnership condensed balance sheet was as follows:

On December 11, 20X9, the first cash sale of other assets with a carrying amount of

$200,000 realized $140,000. Safe installment payments to the partners were made on

the same date. How much cash should be distributed to each partner?

A. Option A

B. Option B

C. Option C

D. Option D

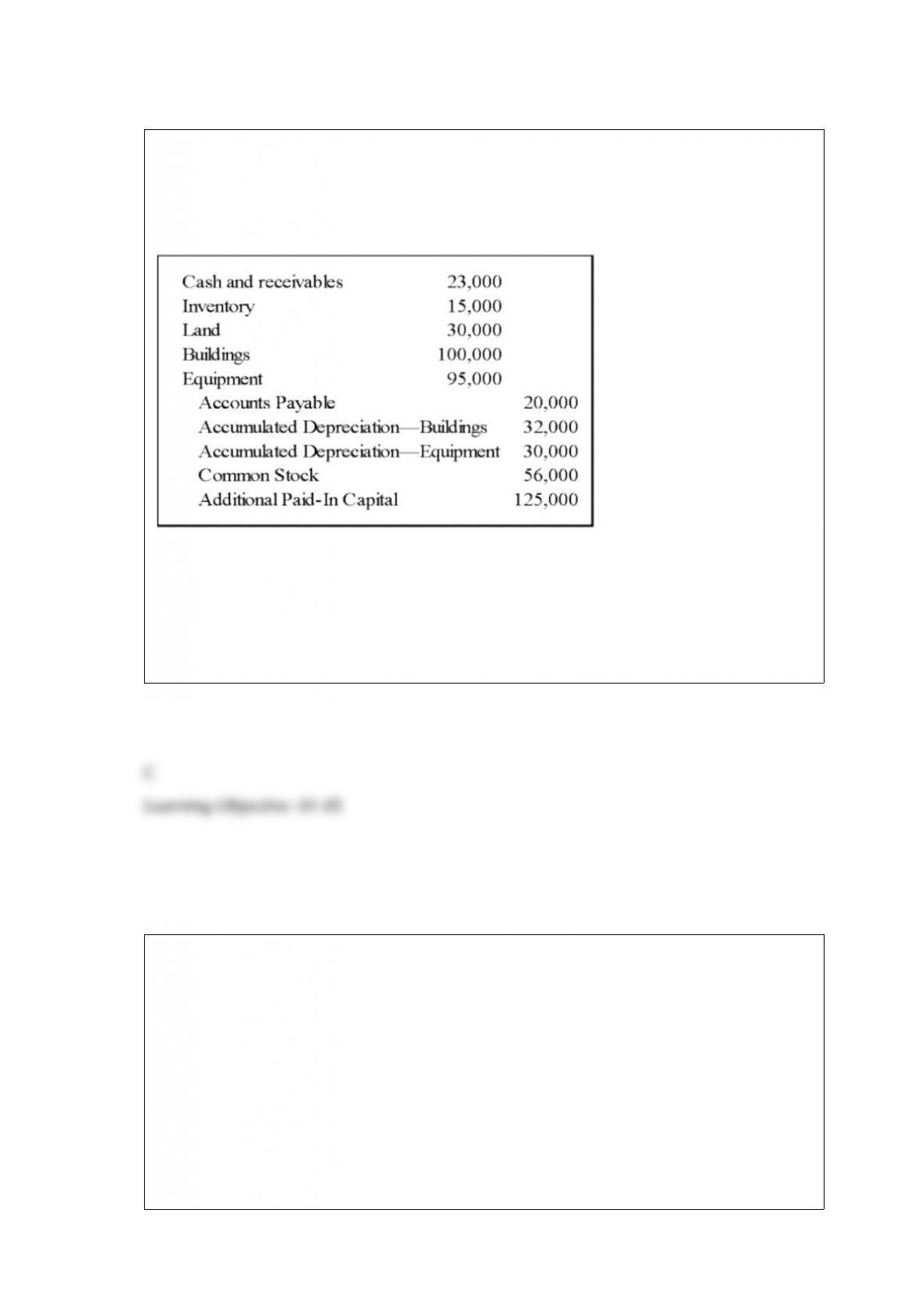

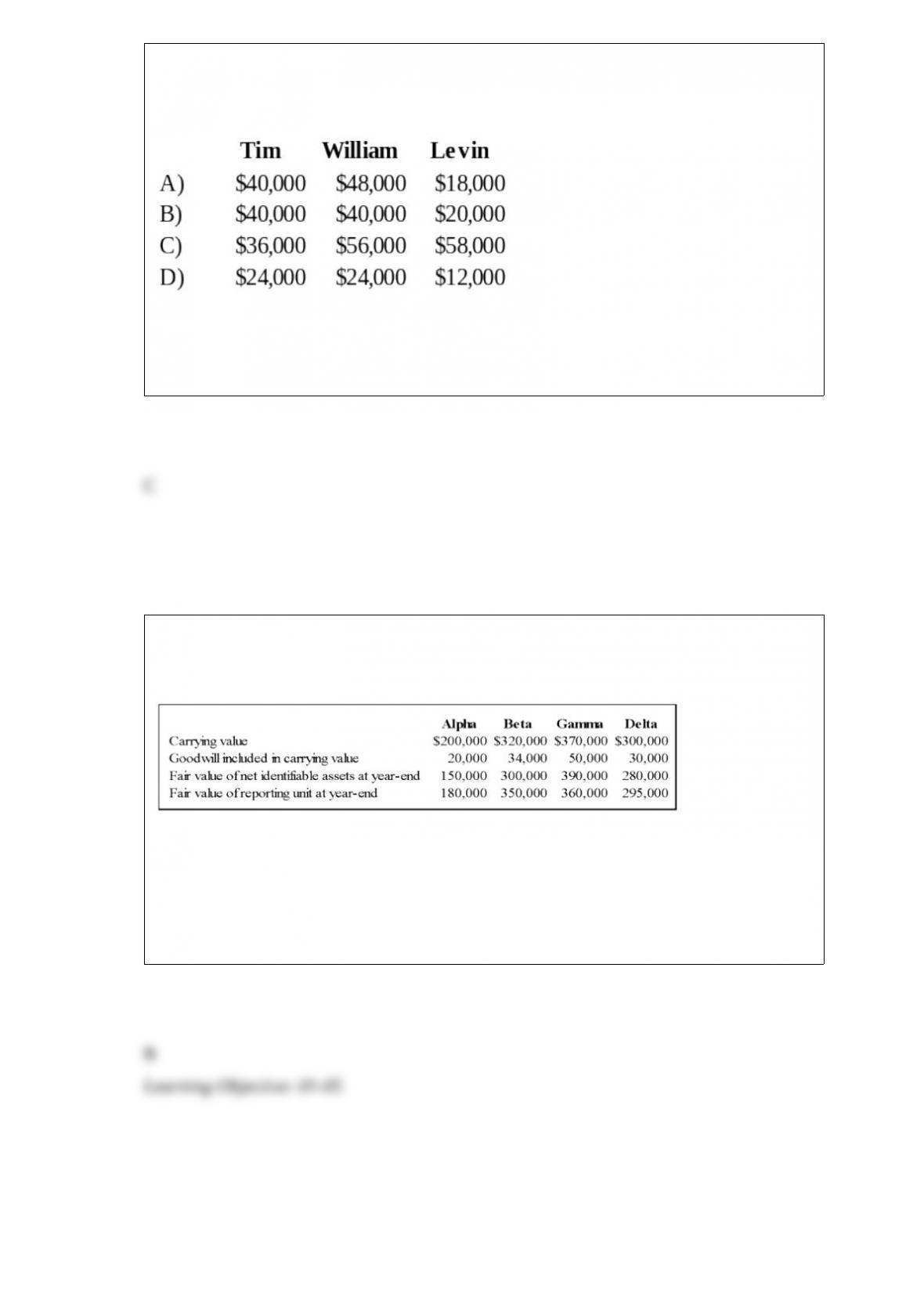

Pursuing an inorganic growth strategy, Wilson Company acquired Venus Company’s net

assets and assigned them to four separate reporting divisions. Wilson assigned total

goodwill of $134,000 to the four reporting divisions as given below:

Based on the preceding information, what would be the total amount of goodwill that

Wilson should report at year-end?

A. $0

B. $69,000

C. $79,000

D. $94,000