Collins Company reported consolidated revenue of $120,000,000 in 20X8. Collins

operates in two geographic areas, domestic and Asia. The following information

pertains to these two areas:

What calculation below is correct to determine if the revenue test is satisfied for the

Asian operations?

A. $58,000,000/$140,000,000

B. $50,000,000/$120,000,000

C. $58,000,000/$120,000,000

D. $50,000,000/$140,000,000

The Board of Commissioners of Vane City adopted its budget for the year ending July

31, comprising estimated revenues of $30,000,000 and appropriations of $29,000,000.

Vane formally integrates its budget into the accounting records. What entry should be

made for budgeted revenues?

A. Memorandum entry only.

B. Debit ESTIMATED REVENUES CONTROL, $30,000,000.

C. Debit ESTIMATED REVENUES RECEIVABLE CONTROL, $30,000,000.

D. Credit ESTIMATED REVENUES CONTROL, $30,000,000.

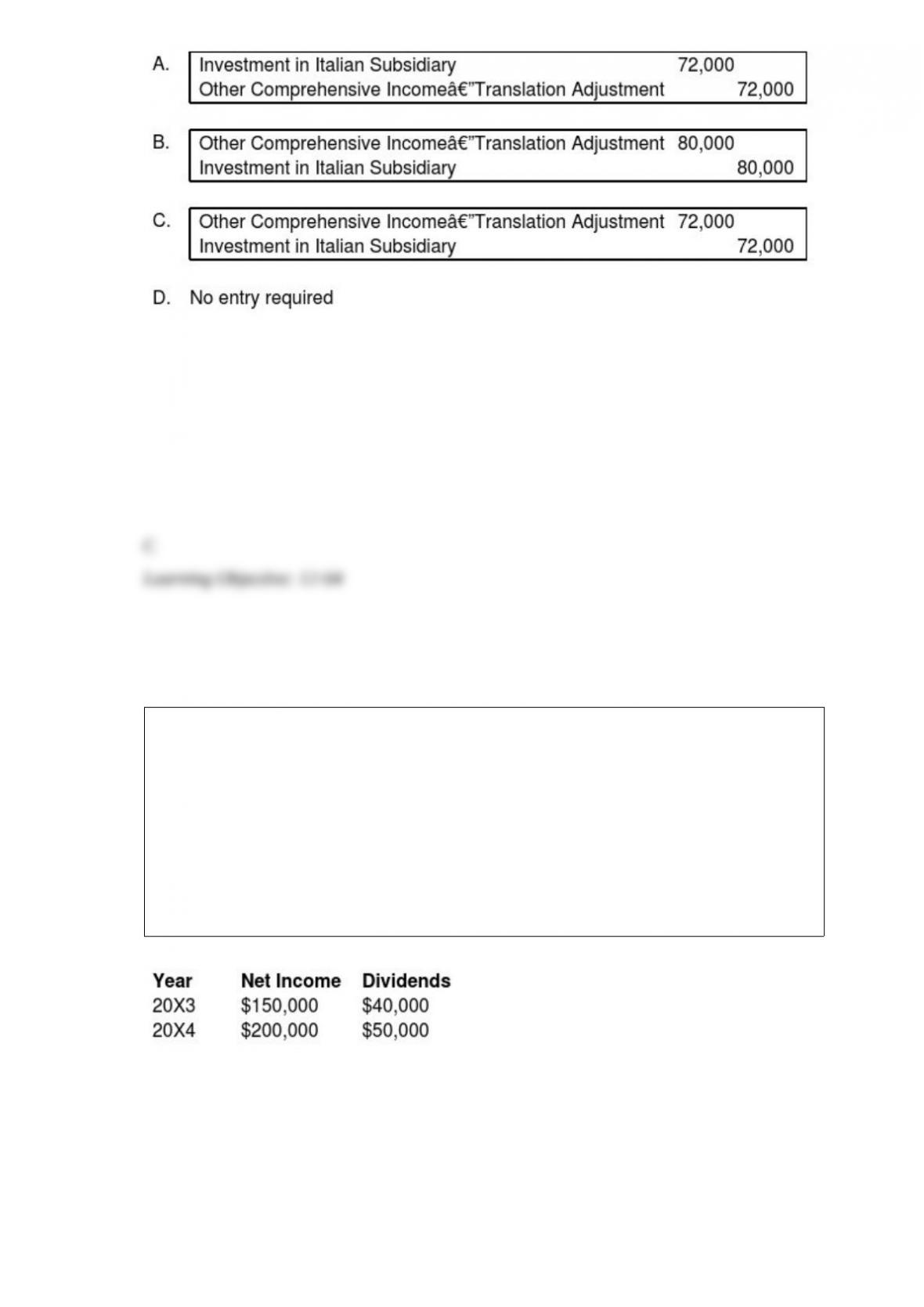

Dover Company owns 90% of the capital stock of a foreign subsidiary located in Italy.

Dover’s accountant has just translated the accounts of the foreign subsidiary and

determined that a debit translation adjustment of $80,000 exists. If Dover uses the fully

adjusted equity method for its investment, what entry should Dover record in order to

recognize the translation adjustment?

A. Option A

B. Option B

C. Option C

D. Option D

Pisa Company acquired 75 percent of Siena Company on January 1, 20X3 for

$712,500. The fair value of the noncontrolling interest was equal to 25 percent of book

value. On the date of acquisition, Siena had common stock outstanding of $300,000 and

a balance in retained earnings of $650,000. During 20X3, Siena purchased inventory for

$35,000 and sold it to Pisa for $50,000. Of this amount, Pisa reported $20,000 in ending

inventory in 20X3 and later sold it in 20X4. In 20X4, Pisa sold inventory it had

purchased for $40,000 to Siena for $60,000. Siena sold $45,000 of this inventory in

20X4.

Income and dividend information for Siena for 20X3 and 20X4 are as follows:

Pisa Company uses the cost method.

Required:

a. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X3.

b. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X4.

Good Care Hospital, which is operated by a religious organization, received

contributions of $1,000,000 from donors who stipulated that the cash be used to

construct an addition to the hospital. As of the balance sheet date, none of the

contributions had been expended for construction. On the hospital’s balance sheet, the

cash contributions would be disclosed in which of the following classes of net assets?

A. Temporarily restricted net assets

B. Donor restricted net assets

C. Assets whose use is limited

D. Permanently restricted net assets

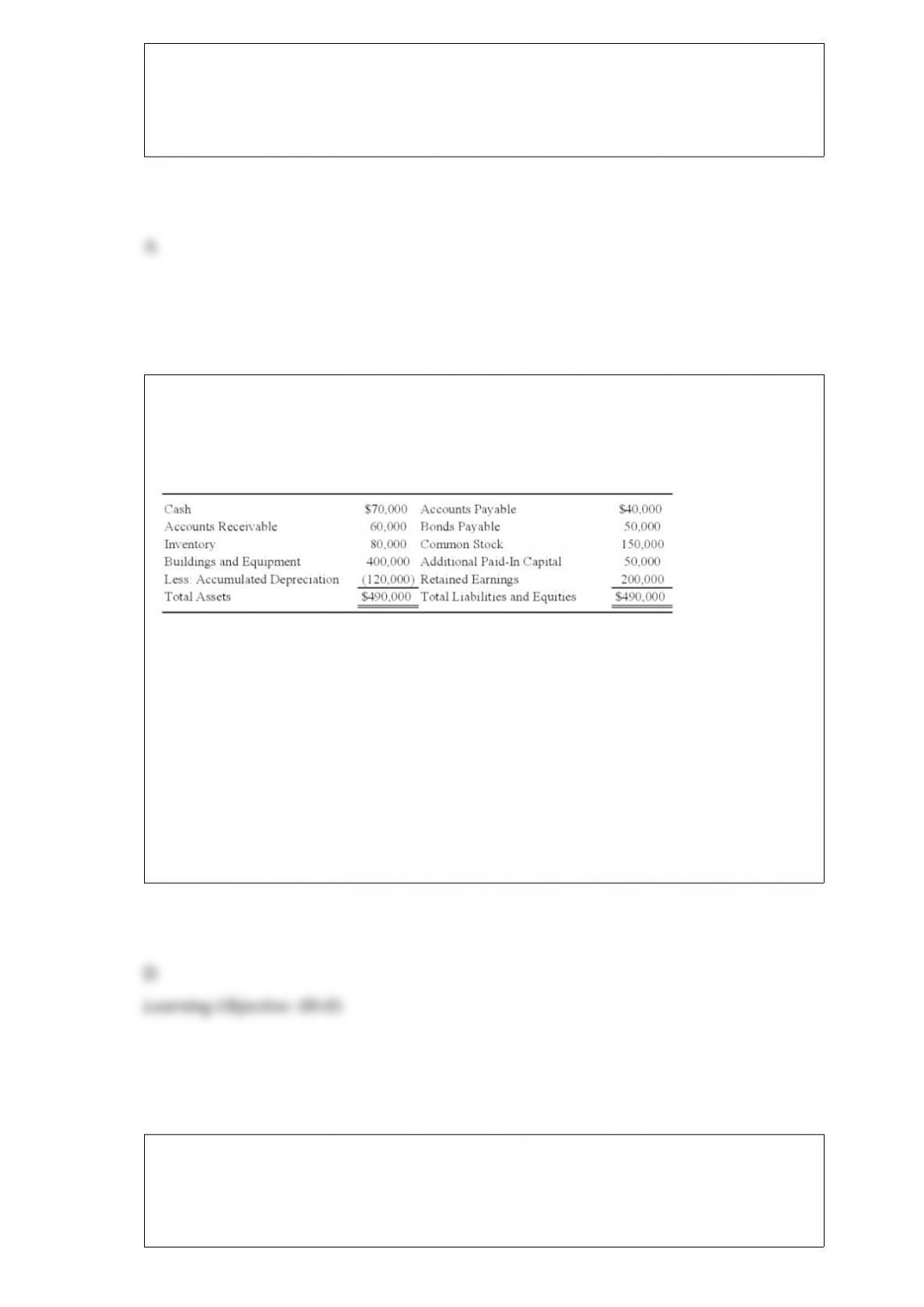

Lemon Corporation acquired 80 percent of Bricks Corporation’s common shares on

January 1, 20X7, at underlying book value. At that date, the fair value of the

noncontrolling interest was equal to 20 percent of the book value of Bricks Corporation.

Bricks prepared the following balance sheet as of December 31, 20X8:

On January 1, 20X9, Bricks declares a stock dividend of 9,000 shares on its $5 par

value common stock. The current market price per share of Bricks stock on January 1,

20X9, is $20.

Begin with the information provided, but assume instead that Bricks declared a stock

dividend of 3,000 shares on its $5 par value common stock. The investment elimination

entry required to prepare a consolidated balance sheet immediately after the stock

dividend is issued will include a debit to Retained Earnings for:

A. $185,000.

B. $65,000.

C. $155,000.

D. $200,000

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Accounting and Auditing Enforcement Releases

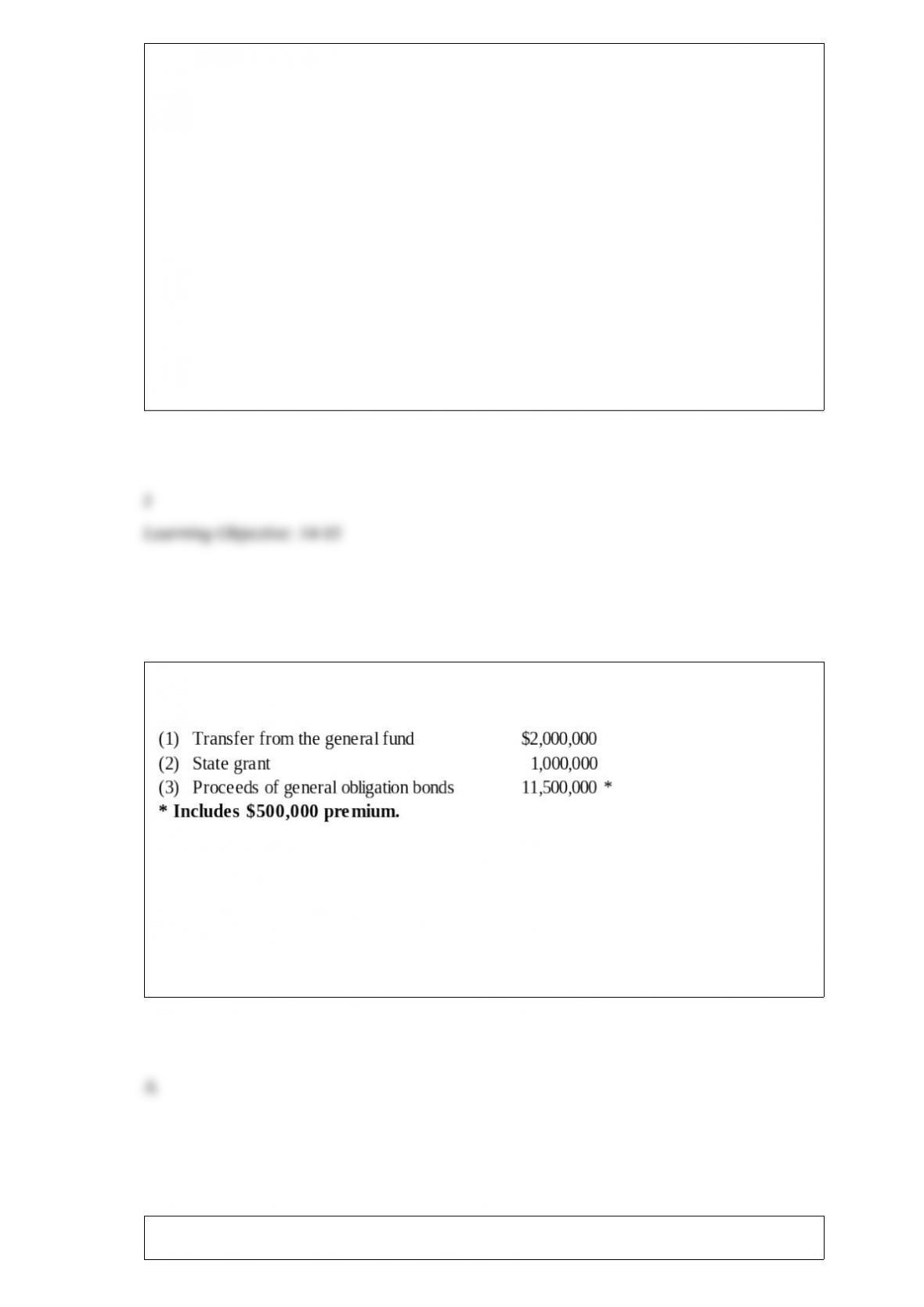

On July 1, 20X8, Cleveland established a capital projects fund to construct a new town

hall. Financing for construction came from the following sources:

Construction of the town hall was completed on June 15, 20X9. For the fiscal year

ended June 30, 20X9, what amount should Cleveland’s capital projects fund report for

revenues on its statement of revenues, expenditures, and changes in fund balance?

A. $1,000,000

B. $1,500,000

C. $3,500,000

D. $14,500,000

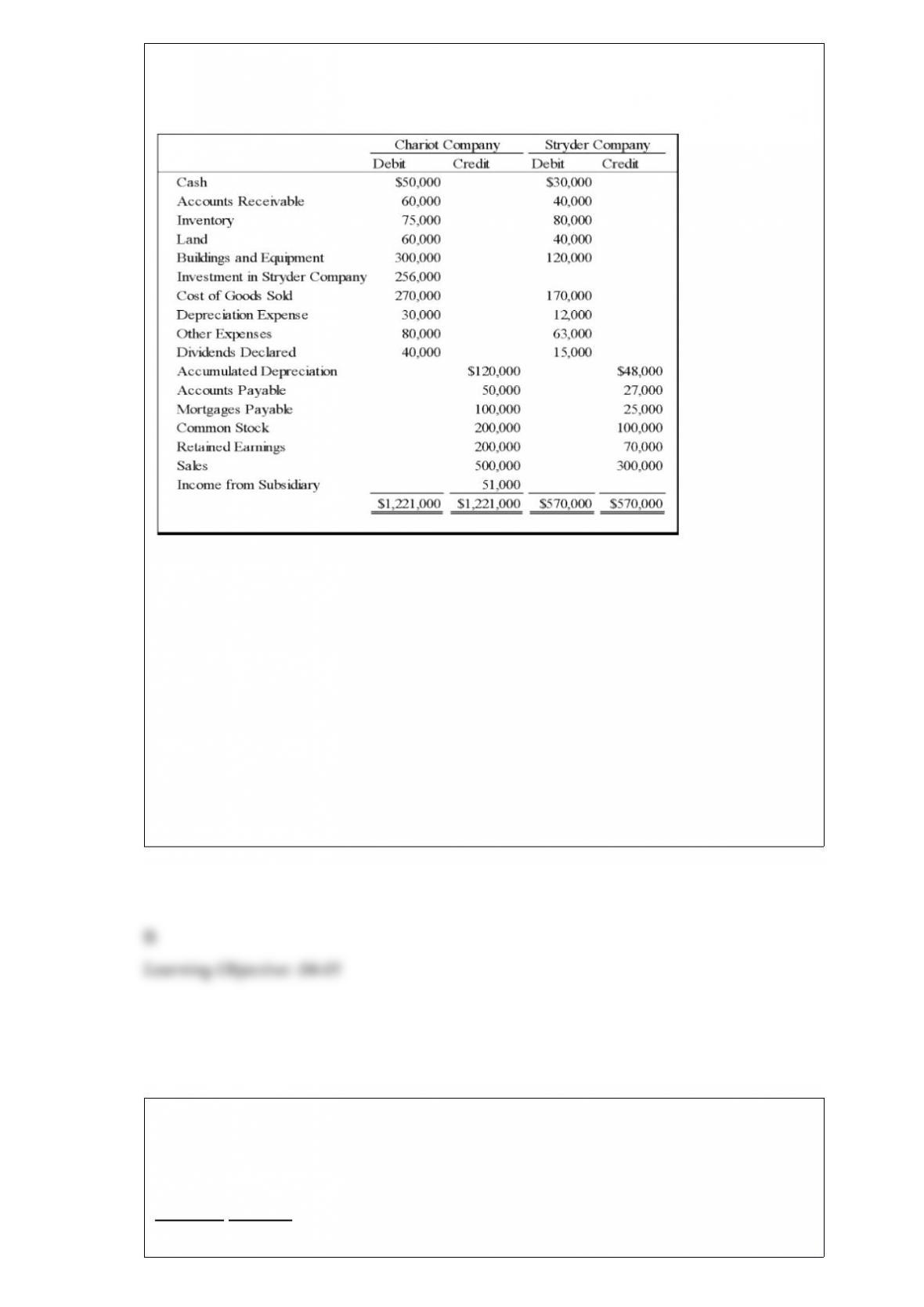

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder’s depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, the beginning differential assigned to buildings and

equipment is:

A. $50,000.

B. $40,000.

C. $10,000.

D. $36,000.

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company’s

common stock for $210,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $90,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

Interstate Catapult

Cash $50,000 $15,000

Accounts Receivable 70,000 25,000

Inventory 30,000 20,000

Land 150,000 80,000

Buildings and Equipment 250,000 200,000

Less: Accumulated Depreciation (70,000) (20,000)

Investment in Catapult Co. 210,000

Total Assets $690,000 $320,000

Accounts Payable $40,000 $10,000

Bonds Payable 150,000 40,000

Common Stock 300,000 90,000

Retained Earnings 200,000 180,000

Total Liabilities and Equity $690,000 $320,000

At the date of the business combination, the book values of Catapult’s assets and

liabilities approximated fair value except for inventory, which had a fair value of

$30,000, and land, which had a fair value of $95,000.

Based on the preceding information, what amount of total assets will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $800,000

B. $830,000

C. $1,010,000

D. $1,040,000

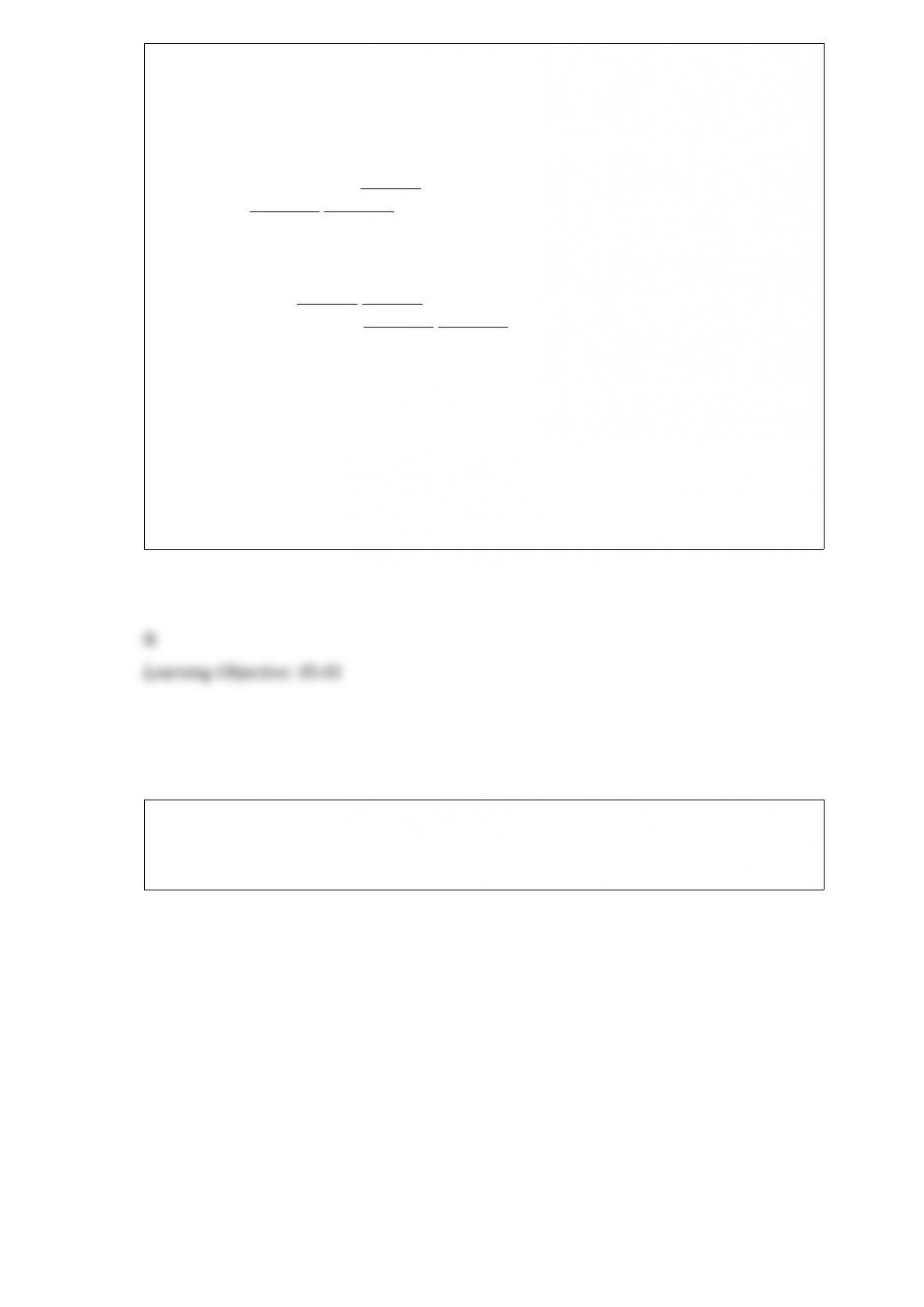

Pace Corporation acquired 100 percent of Spin Company’s common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what amount of liabilities will be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $615,000

B. $406,000

C. $300,000

D. $265,000

When a partnership is formed, noncash assets contributed by partners should be

recorded:

I. at their respective book values for income tax purposes.

II. at their respective fair values for financial accounting purposes.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

On January 1, 20X7, Pisa Company acquired 80 percent of Siena Company by

purchasing 40,000 shares of Siena’s common stock. There was no differential related to

this transaction. The noncontrolling interest had a fair value equal to 20 percent of book

value. The book value of Siena on December 31, 20X7 was as follows:

On January 1, 20X8, Siena sold an additional 12,500 shares to a nonaffiliate for $25 per

share.

Based on the preceding information, what is Pisa’s new ownership interest?

A. 84 percent

B. 55 percent

C. 70 percent

D. 64 percent

On January 1, 20X7, Pisa Company acquired 80 percent of Siena Company by

purchasing 40,000 shares of Siena’s common stock. There was no differential related to

this transaction. The noncontrolling interest had a fair value equal to 20 percent of book

value. The book value of Siena on December 31, 20X7 was as follows:

On January 1, 20X8, Pisa purchased an additional 12,500 shares directly from Siena for

$25 per share.

Based on the preceding information, the ending balance in Additional Paid-In Capital

would be:

A. $0

B. $187,500

C. $312,500

D. $125,000

A tax collection fund that collects property taxes and then distributes them to local

governmental units is an example of a(n):

A. trust fund.

B. agency fund.

C. internal service fund.

D. permanent fund.

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

“Red Herring” Prospectus

Earth Company owns 100 percent of the capital stock of both Mars Corporation and

Venus Corporation. Mars purchases merchandise inventory from Venus at 125 percent

of Venus’s cost. During 20X8, Venus sold inventory to Mars that it had purchased for

$25,000. Mars sold all of this merchandise to unrelated customers for $56,892 during

20X8. In preparing combined financial statements for 20X8, Earth’s bookkeeper

disregarded the common ownership of Mars and Venus.

Based on the information given above, by what amount was unadjusted revenue

overstated in the combined income statement for 20X8?

A. $25,000

B. $56,892

C. $31,250

D. $6,250

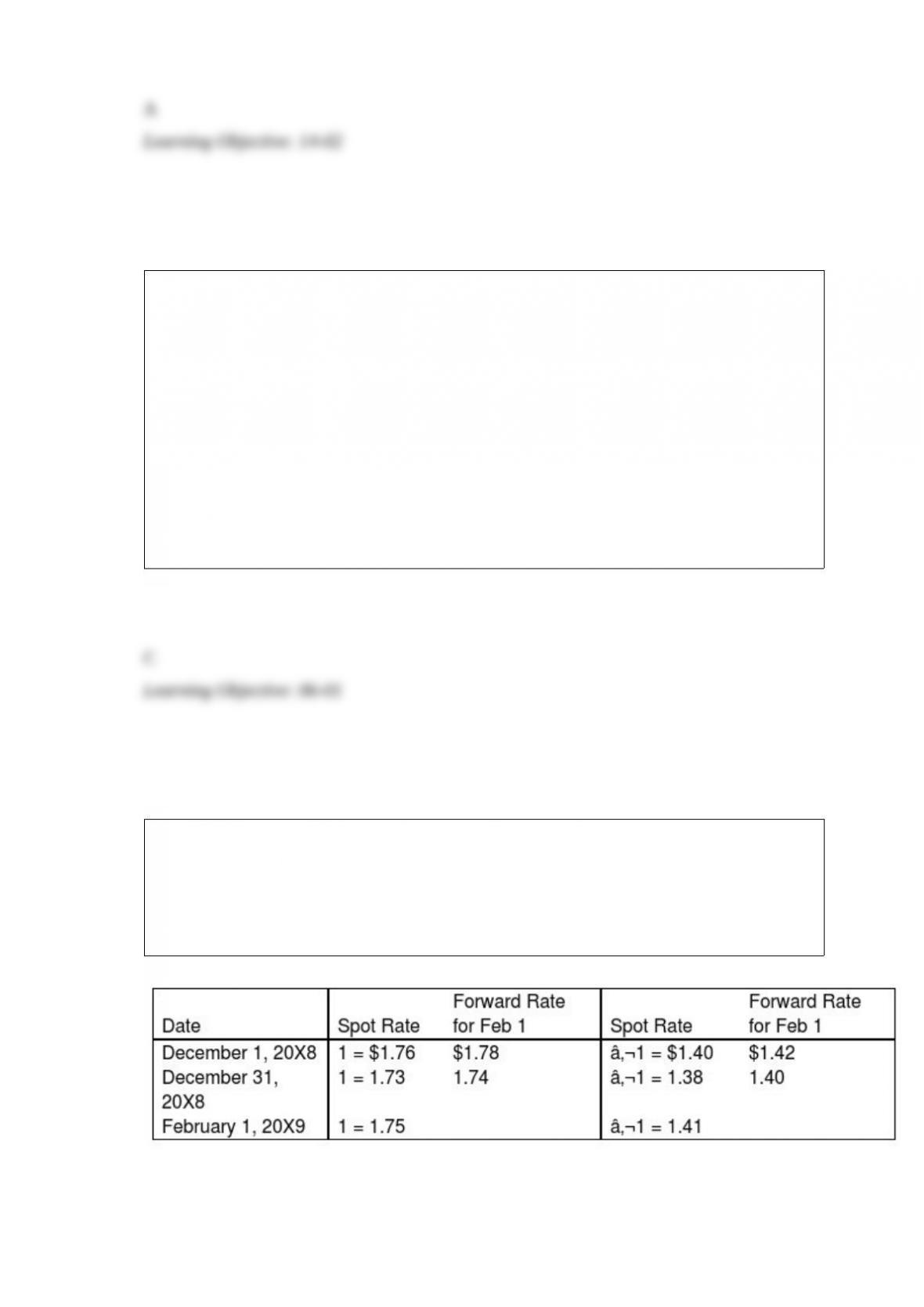

On December 1, 20X8, Hedge Company entered into a 60-day speculative forward

contract to sell 200,000 British pounds () at a forward rate of 1 = $1.78. On the same

day it purchased a 60-day speculative forward contract to buy 100,000 euros (€) at a

forward rate of €1 = $1.42.

The rates are as follows:

Hedge had no other speculation transactions in 20X8 and 20X9. Ignore taxes.

Based on the preceding information, what is the effect of the British pound speculative

contract on 20X8 net income?

A. $10,000 gain

B. $6,000 gain

C. $8,000 gain

D. $2,000 loss

Assuming there is a budget surplus, which of the following accounts are credited when

the general fund records its operating budget at the beginning of the year?

A. Appropriations Control and Budgetary Fund Balance—Unassigned.

B. Estimated Revenues Control and Estimated Residual Equity Transfer Out.

C. Budgetary Fund Balance—Assigned For Encumbrances and Expenditures.

D. Estimated Residual Equity Transfer Out and Estimated Transfer In.

Given the increased development of complex business structures, which of the

following regulators is responsible for the continued usefulness of accounting reports?

A. Securities and Exchange Commission (SEC)

B. Public Company Accounting Oversight Board (PCAOB)

C. Financial Accounting Standards Board (FASB)

D. All of the above

A private not-for-profit university generally must depreciate all tangible fixed assets,

except:

I. works of art and other historical treasures.

II. administration buildings.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

A debtor-in-possession balance sheet should report:

I. Liabilities not subject to compromise.

II. Liabilities subject to compromise.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

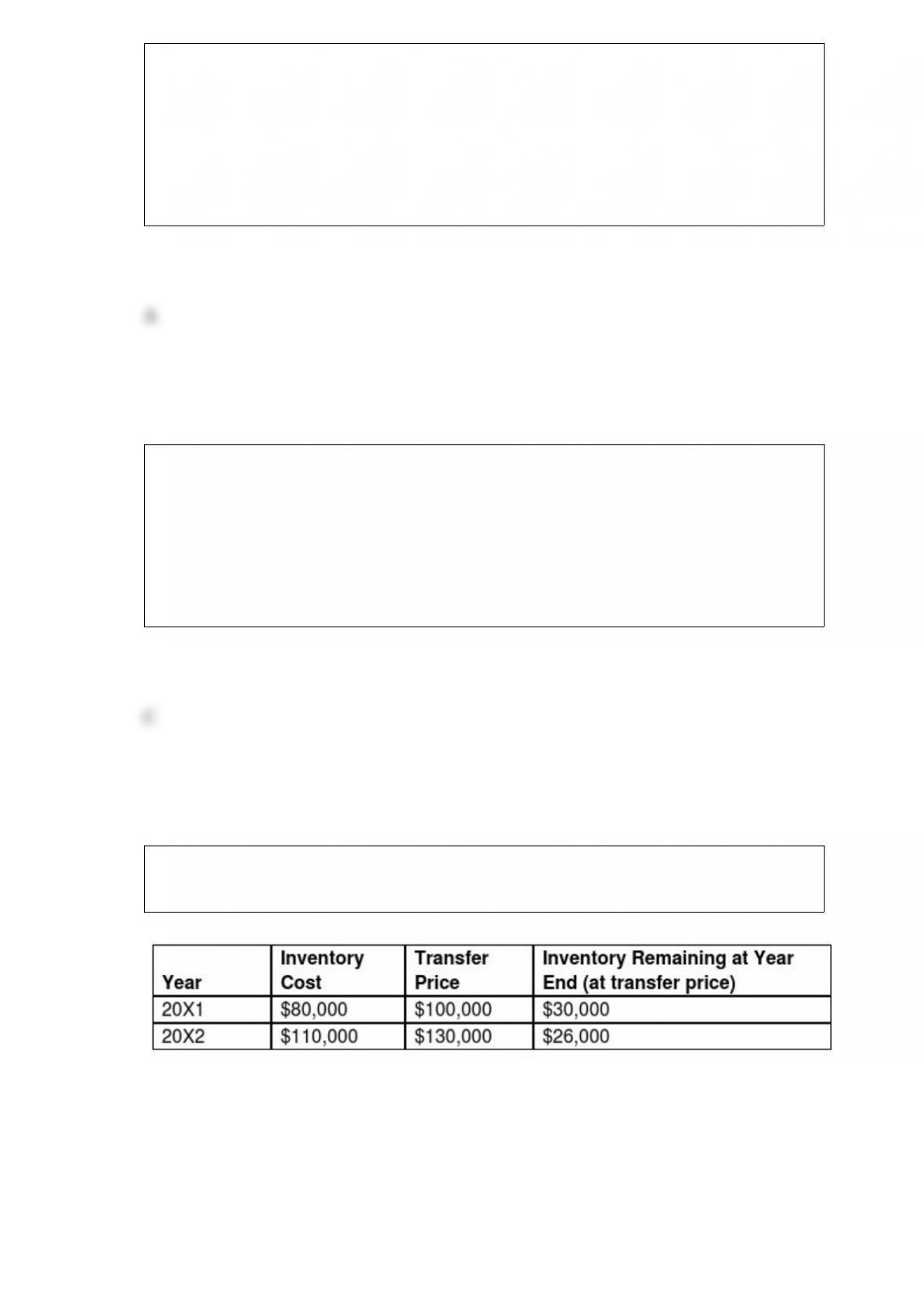

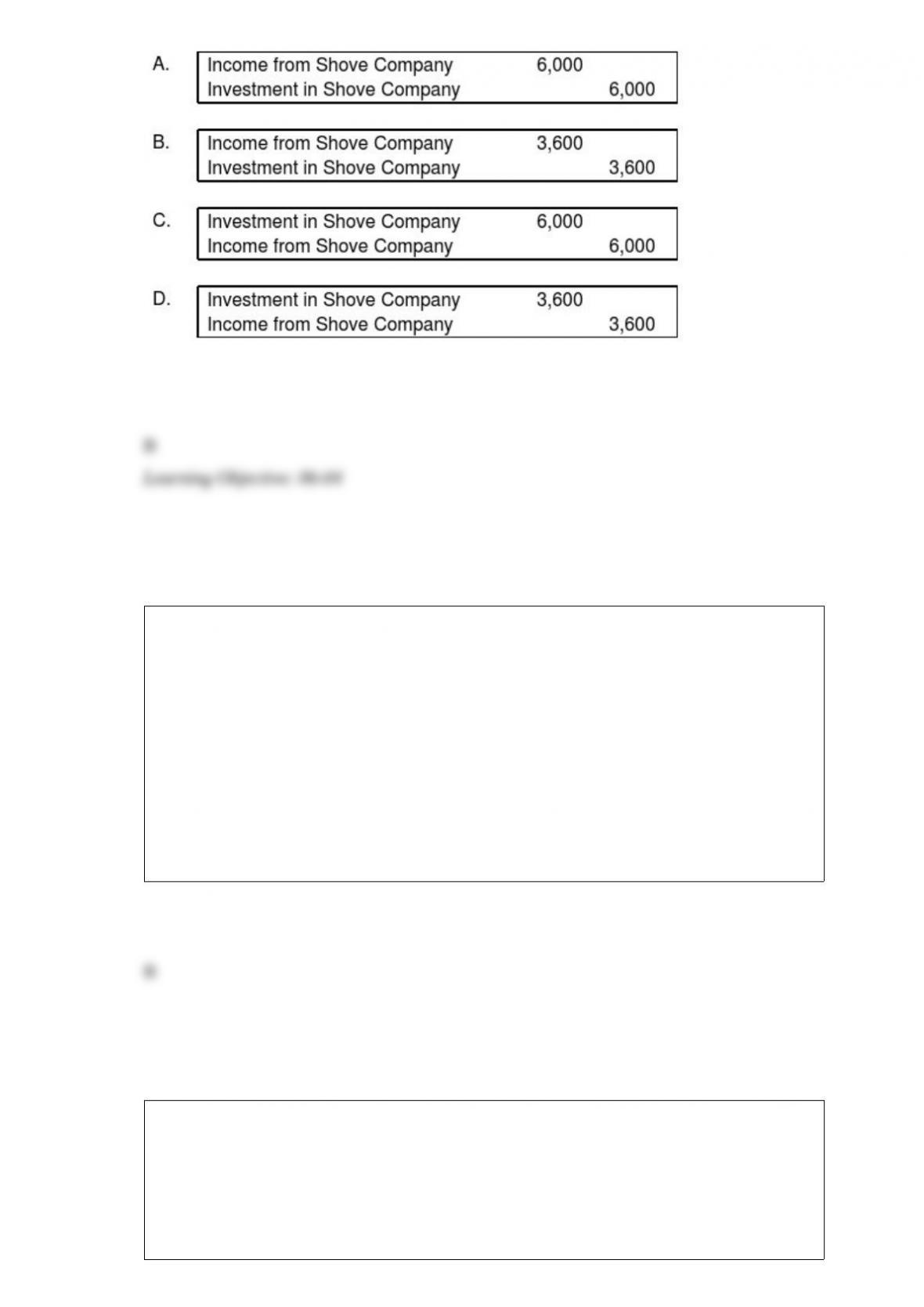

Push Company owns 60% of Shove Company’s outstanding common stock. Intra-entity

sales are as follows:

Assume Shove sold the inventory to Push. Using the fully adjusted equity method, what

journal entry would be recorded by Push to defer the unrealized gross profit on inventory

sales to Shove in 20X1?

A donor agrees to contribute $5,000 per year at the end of each of the next five years to

a voluntary health and welfare organization. The donor did not place any use

restrictions on the amount pledged. The stream of the payments is discounted at 6

percent. The first payment of $5,000 is received at the end of the first year. The present

value factor for a five-payment annuity due on June 30, 20X9, at 6 percent is 4.2124.

Based on the preceding information, the increase in present value of the contributions

receivable recognized at the end of the first year equals:

A. $5,000.

B. $1,264.

C. $4,212.

D. $787.

On January 1, 20X7, Yang Corporation acquired 25 percent of the outstanding shares of

Spiel Corporation for $100,000 cash. Spiel Company reported net income of $75,000

and paid dividends of $30,000 for both 20X7 and 20X8. The fair value of shares held

by Yang was $110,000 and $105,000 on December 31, 20X7 and 20X8 respectively.

Based on the preceding information, what amount will be reported by Yang as income

from its investment in Spiel for 20X8 if it used the fair value option to account for its

investment in Spiel?

A. $11,250

B. $2,500

C. $6,250

D. $7,500

From an investor’s point of view, a liquidating dividend from an investee is:

A. A dividend declared by the investee in excess of its earnings in the current year.

B. A dividend declared by the investee in excess of its earnings since acquisition by the

investor.

C. Any dividend declared by the investee since acquisition.

D. A dividend declared by the investee in excess of the investee’s retained earnings.

A private, not-for-profit geographic society received cash contributions which were

restricted by the donors for the acquisition of fixed assets. In which section of the

statement of cash flows would these cash contributions be reported?

A. Financing activities

B. Investing activities

C. Operating activities

D. Capital and related financing activities

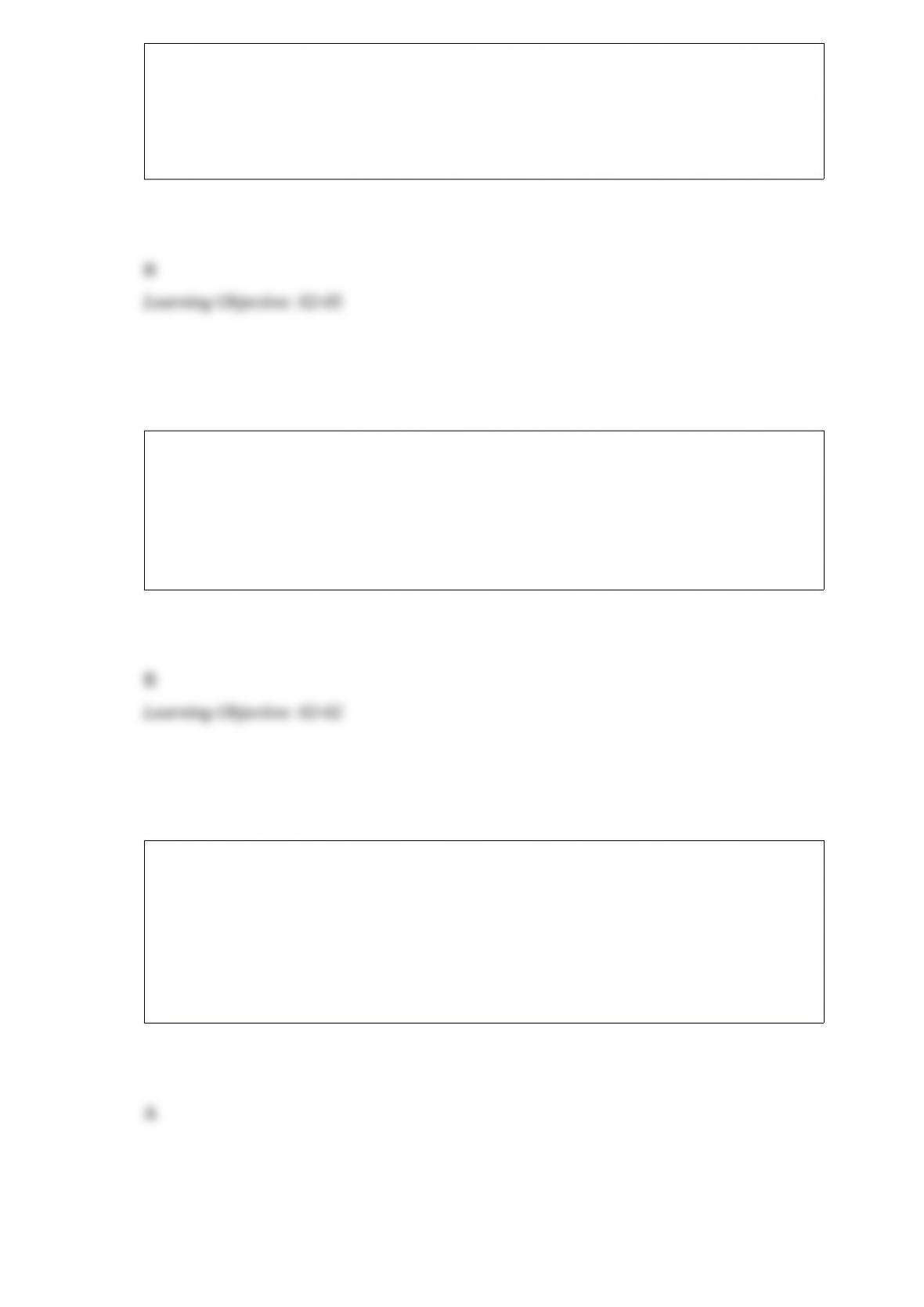

Electric Corporation holds 80 percent of Utility Company’s voting common shares,

acquired at book values, but none of its preferred shares. At the date of acquisition, the

fair value of the noncontrolling interest was equal to 20 percent of the book value of

Utility Company. Summary balance sheets for the companies on December 31, 20X8,

are as follows:

Neither of the preferred issues is convertible. Electric’s preferred pays a 8 percent

annual dividend, and Utility’s preferred pays a 12 percent dividend. Utility reported net

income of $30,000 and paid a total of $10,000 of dividends in 20X8. Electric reported

income from its separate operations of $70,000 and paid total dividends of $25,000 in

20X8.

Based on the preceding information, what is the amount of earnings available to

common shareholders reported in the consolidated financial statements for the year?

A. $89,200

B. $87,000

C. $91,000

D. $82,800

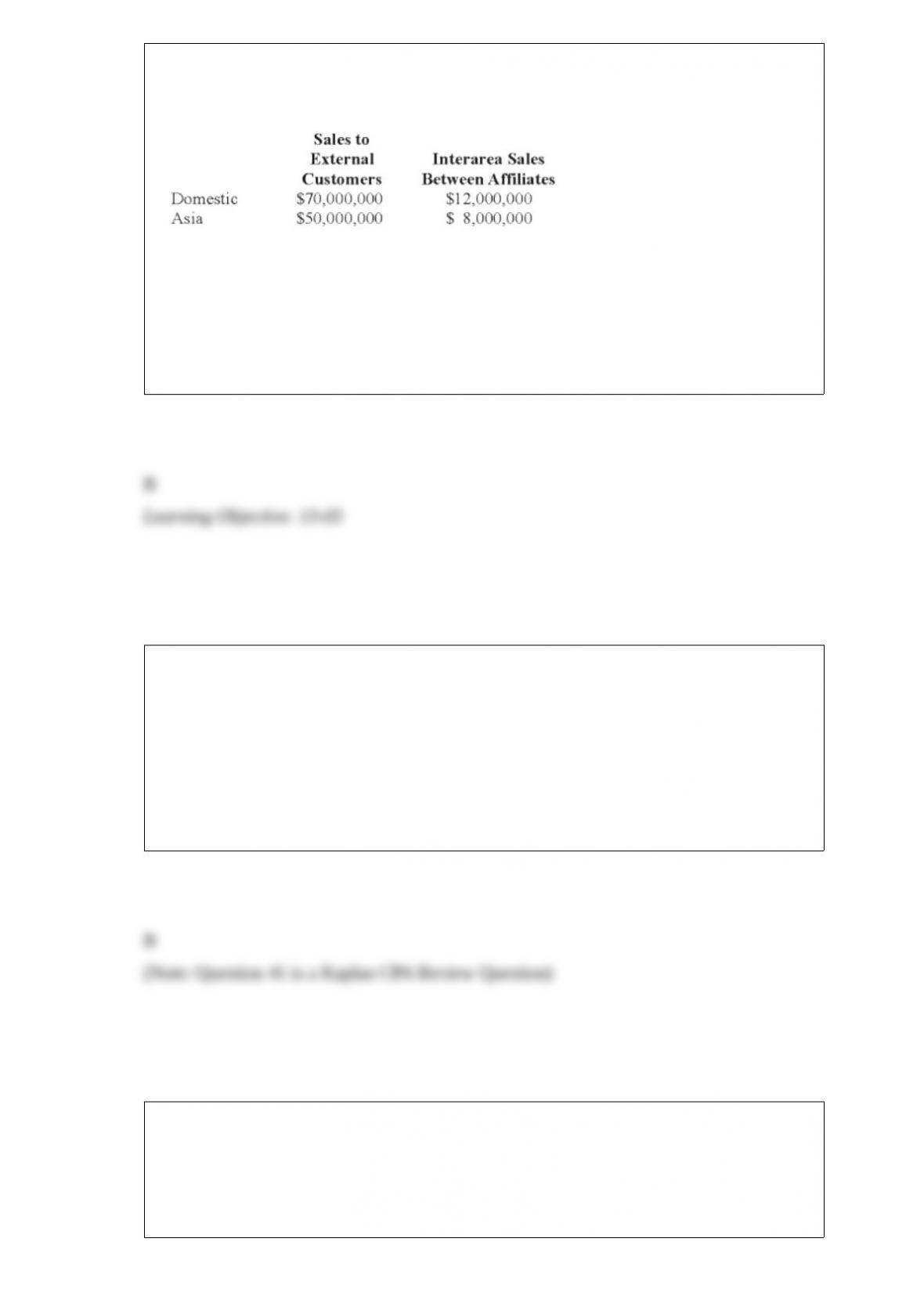

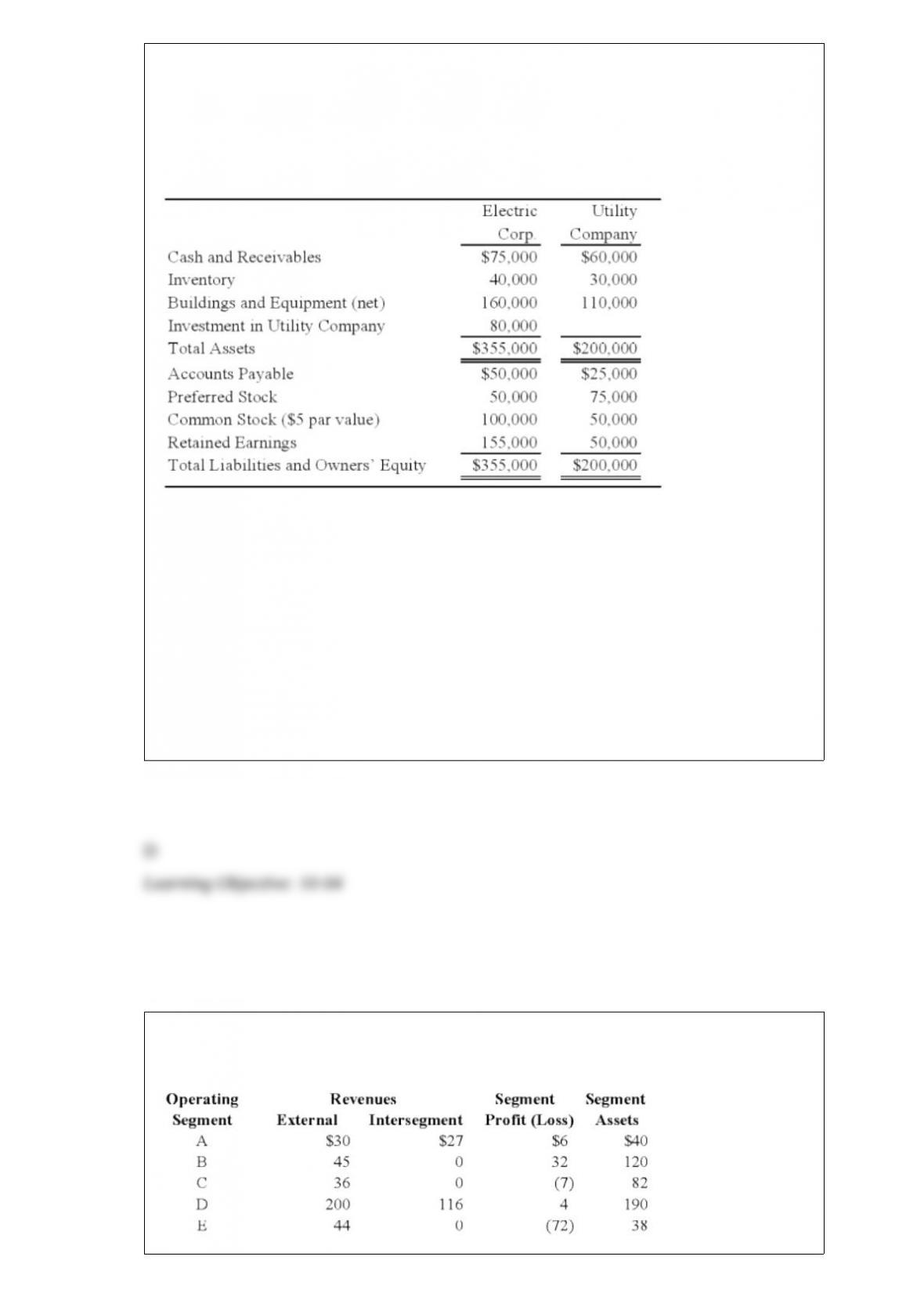

An analysis of Abbey Company’s operating segments provides the following

information:

Refer to the above information. Which of the operating segments above meet the

revenue test?

A. B, D, and E

B. A and D

C. A, B, and D

D. B, C, D, and E

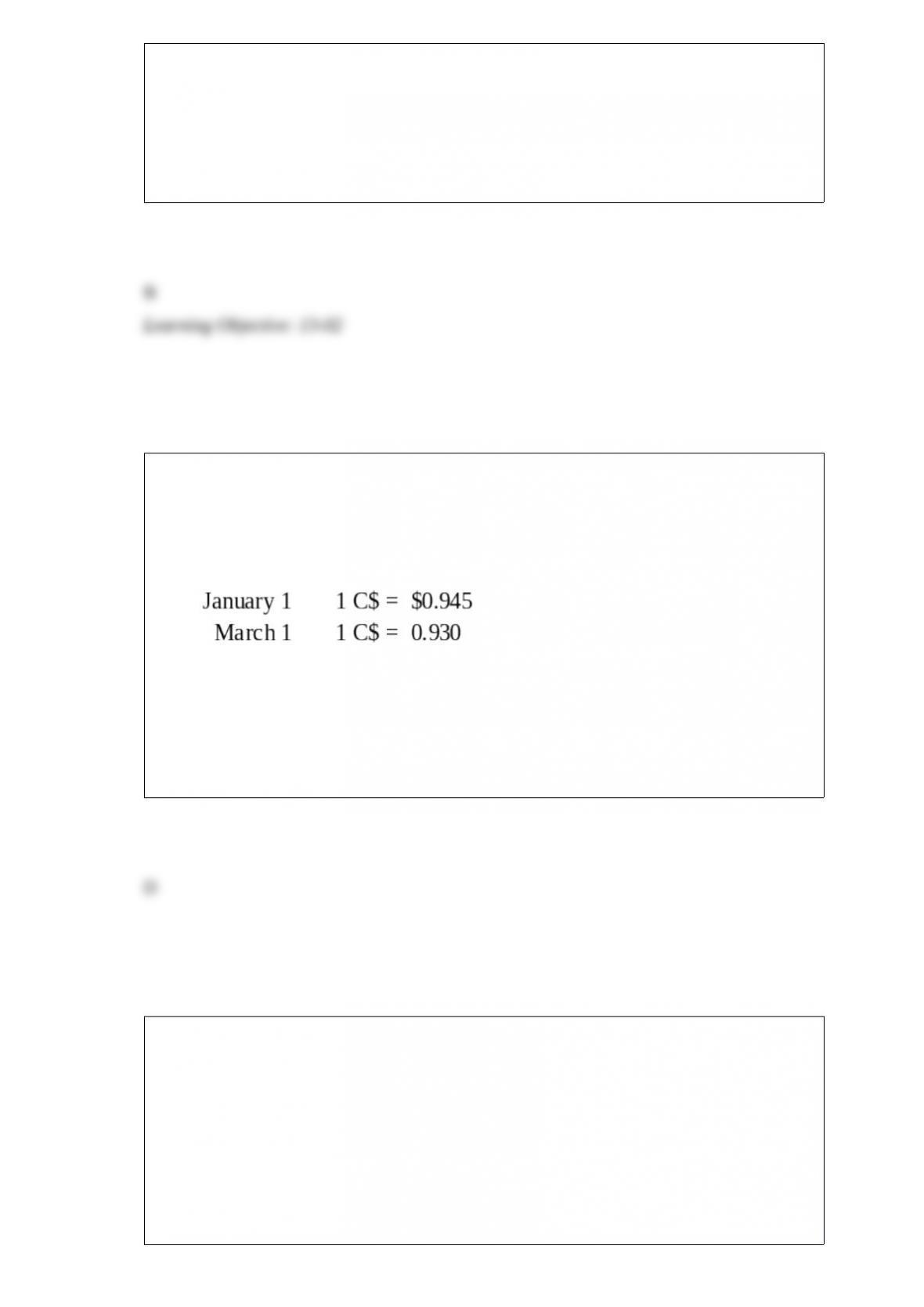

Myway Company sold equipment to a Canadian company for 100,000 Canadian dollars

(C$) on January 1, 20X9 with settlement to be in 60 days. On the same date, Myway

entered into a 60-day forward contract to sell 100,000 Canadian dollars at a forward

rate of 1 C$ = $.94 in order to manage its exposed foreign currency receivable. The

forward contract is not designated as a hedge. The spot rates were:

Based on the preceding information, the entry to revalue foreign currency payable to

current U.S. dollar value on March 1 will have:

A. a credit to Foreign Currency Transaction Gain for $1,500.

B. a debit to Foreign Currency Transaction Loss for $2,500.

C. a debit to Foreign Currency Transaction Loss for $1,500.

D. a credit to Foreign Currency Transaction Gain for $1,000.

Hilldale Corporation purchased land on January 1, 20X0, for $60,000. On August 7,

20X2, it sold the land to its subsidiary, Allen Corporation, for $35,000. Hilldale owns

60 percent of Allen’s voting shares

Based on the preceding information, what will be the worksheet consolidation entry to

remove the effects of the intercompany sale of land in preparing the consolidated

financial statements for 20X2?

A. Land 15,000

Loss on Sale of Land 15,000

B. Land 25,000

Loss on Sale of Land 25,000

C. Loss on Sale of Land 15,000

Land 15,000

D. Loss on Sale of Land 25,000

Land 25,000

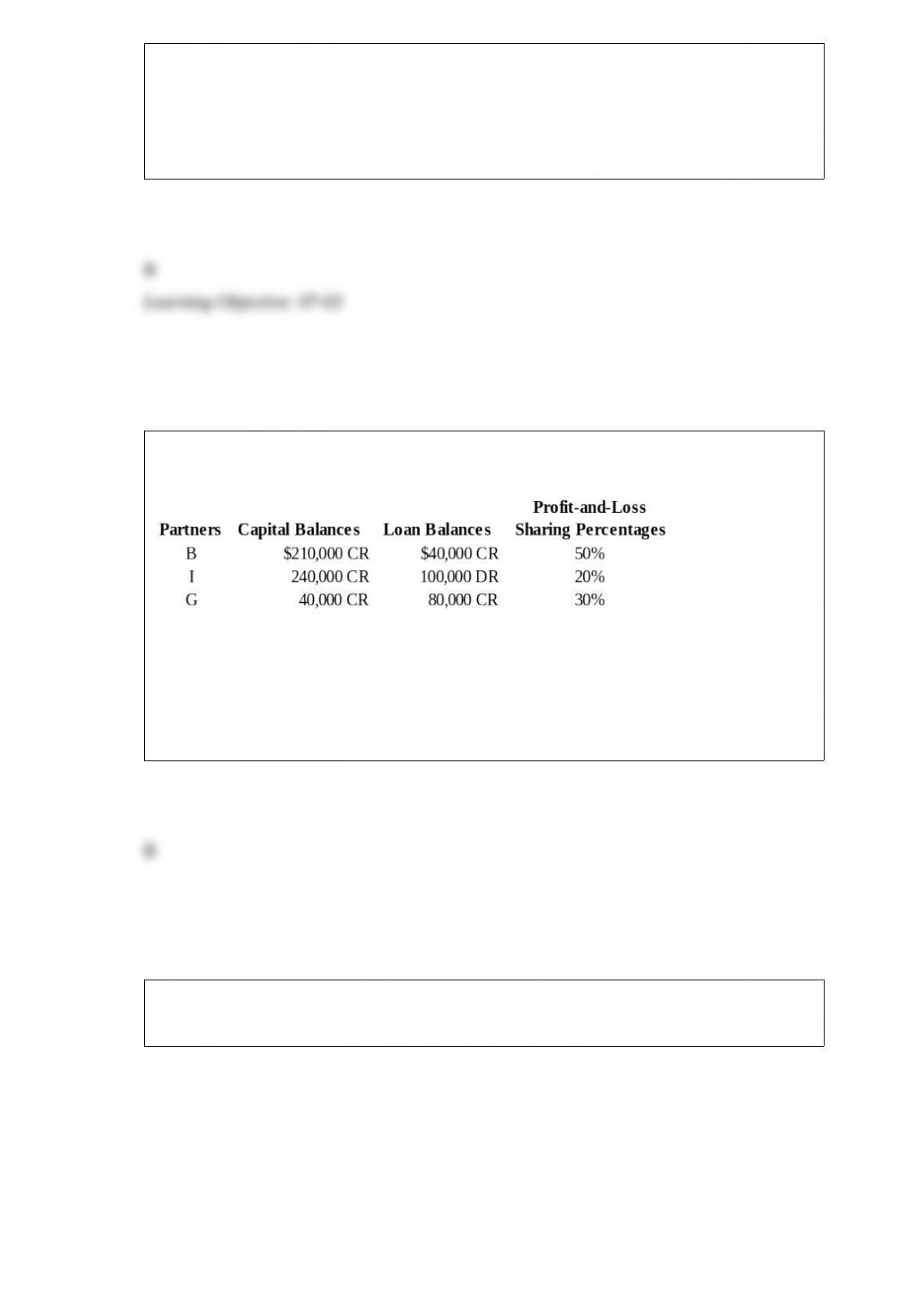

The BIG Partnership has decided to liquidate at December 31, 20X8. The capital and

loan balances of the partners at December 31, 20X8, are provided below:

If you were to calculate the Loss Absorption Power for each partner, how would the

partners rank (from highest to lowest LAP)?

A. B, I, G

B. I, B, G

C. B, G, I

D. G, I, B

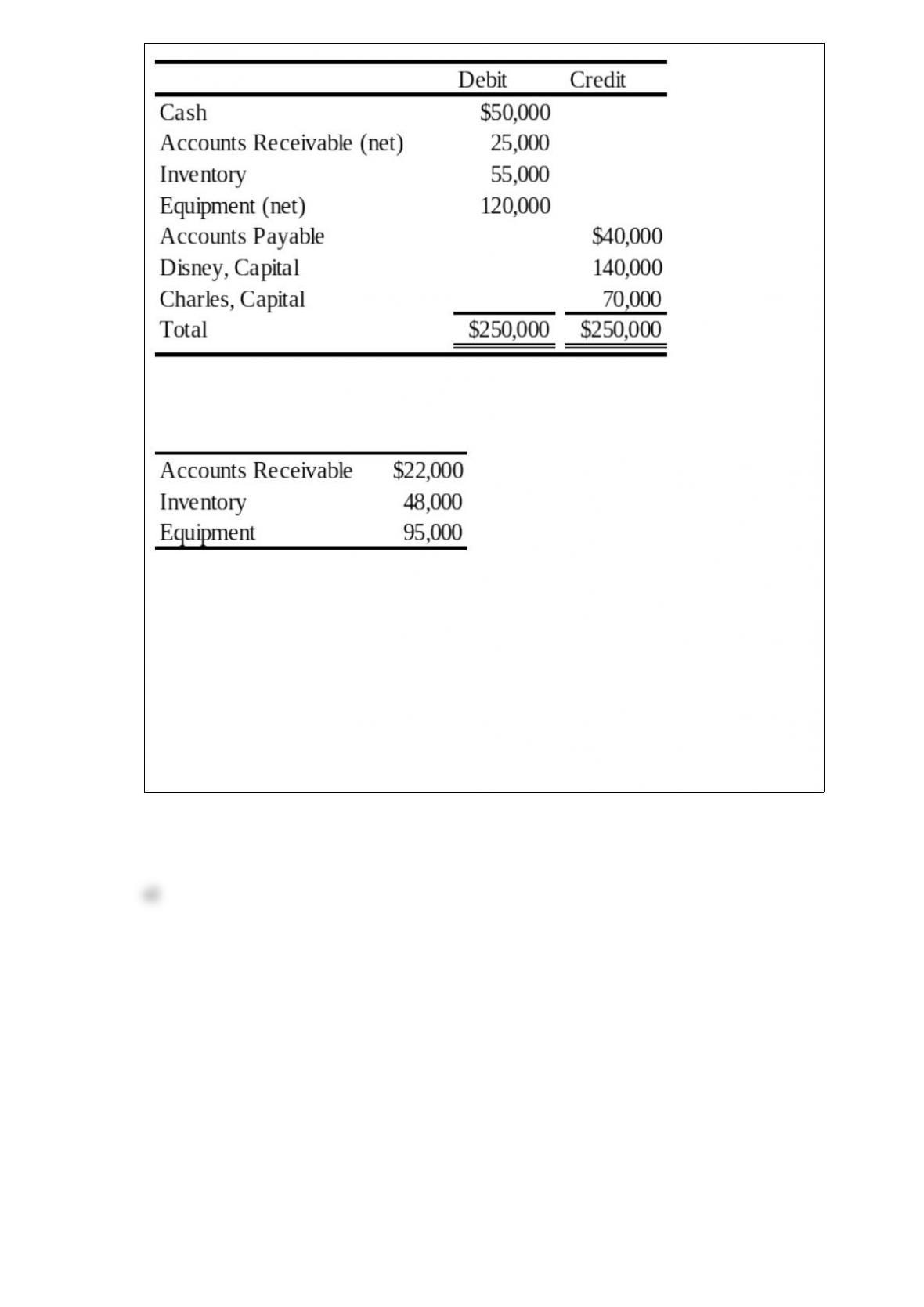

When Disney and Charles decided to incorporate their partnership, the trial balance was

as follows:

The partnership’s books will be closed, and new books will be used for D & C

Corporation. The following additional information is available:

1) The estimated fair values of the assets follow:

2) All assets and liabilities are transferred to the corporation.

3) The common stock is $5 par. Alice and Betty receive a total of 24,000 shares.

4) Disney and Charles share profits and losses in the ratio 6:4.

Required:

a. Prepare the entries on the partnership’s books to record (1) the revaluation of assets,

(2) the

transfer of the assets to the D & C Corporation and the receipt of the common stock,

and (3) the closing of the books.

b. Prepare the entries on D & C Corporation’s books to record the assets and the

issuance of the common stock.

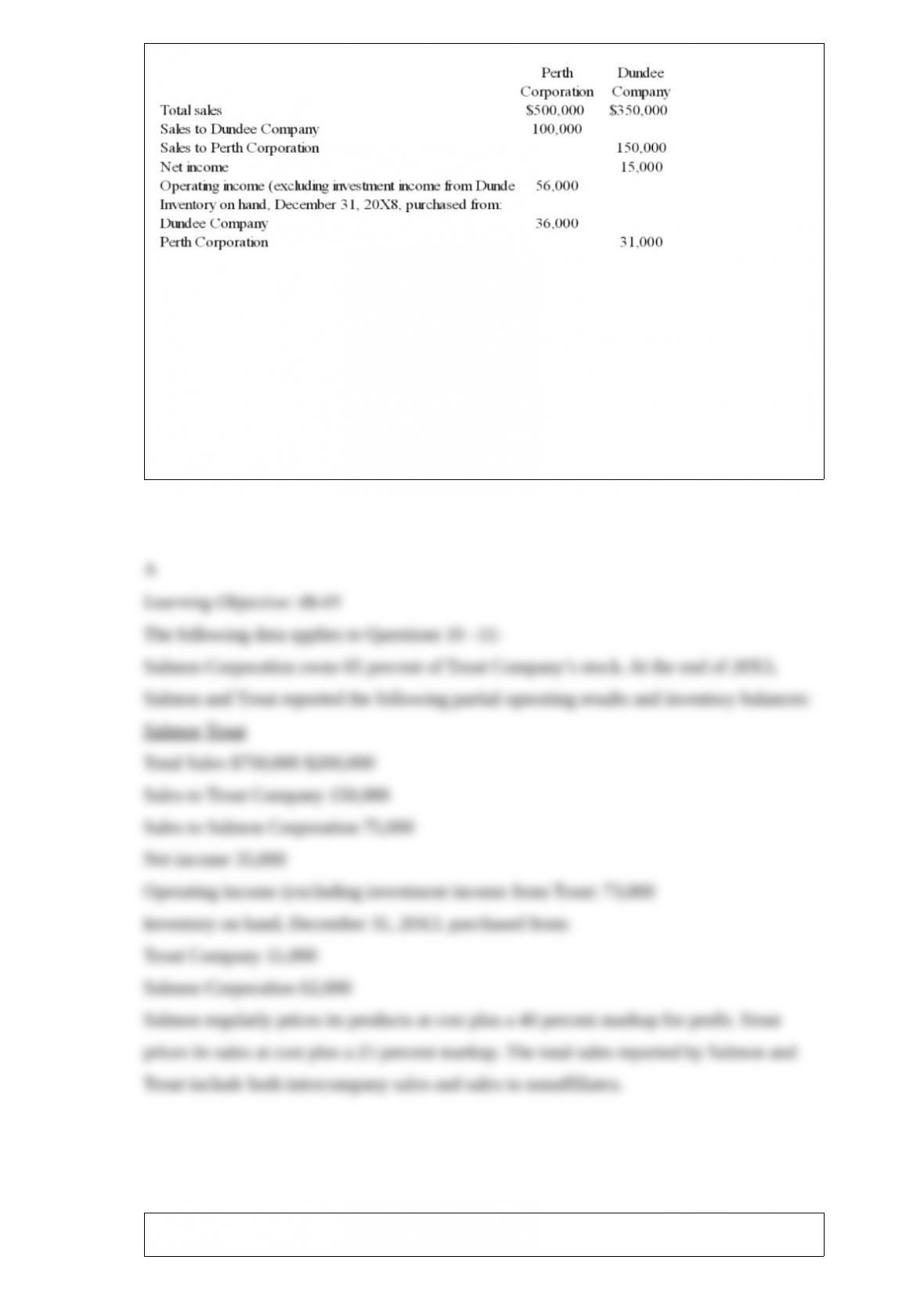

Perth Corporation owns 90 percent of Dundee Company’s stock. At the end of 20X8,

Perth and Dundee reported the following partial operating results and inventory

balances:

Perth regularly prices its products at cost plus a 30 percent markup for profit. Dundee

prices its sales at cost plus a 10 percent markup. The total sales reported by Perth and

Dundee include both intercompany sales and sales to nonaffiliates.

Based on the information given above, what balance will be reported for inventory in

the consolidated balance sheet for December 31, 20X8?

A. $56,573

B. $23,846

C. $32,727

D. $67,000

Siera, Lani, and Cecilia are partners in an equipment leasing business that has not been

able to generate the type of revenue expected by the partners. They share profits and

losses in a ratio of 5:3:2, respectively. They have decided to liquidate the business and

have sold all the assets except for one piece of heavy machinery. All the partners are

personally insolvent. The machinery has a book value of $120,000, and the partners

have capital balances as follows:

Siera, Capita $40,000

Lani, Capital $20,000

Cecilia, Capital $30,000

Each of the following is an independent case.

Refer to the information given above. What amount of cash will each partner receive as

a liquidating distribution if the machinery is sold for $44,000?

Siera Lani Cecilia

A. $2,000 $2,800 $14,800

B. $2,000 $0 $14,000

C. $0 $0 $14,000

D. $0 $0 $16,000

In the LMN partnership, Lynn’s capital is $60,000, Marty’s is $80,000, and Nancy’s is

$70,000. They share income in a 4:3:3 ratio, respectively. Nancy is retiring from the

partnership. Each of the following questions is independent of the others.

Refer to the above information. Nancy is paid $84,000, and no goodwill is recorded.

What is Lynn’s capital balance after Nancy withdraws from the partnership?

A. $68,000

B. $54,000

C. $53,000

D. $52,000

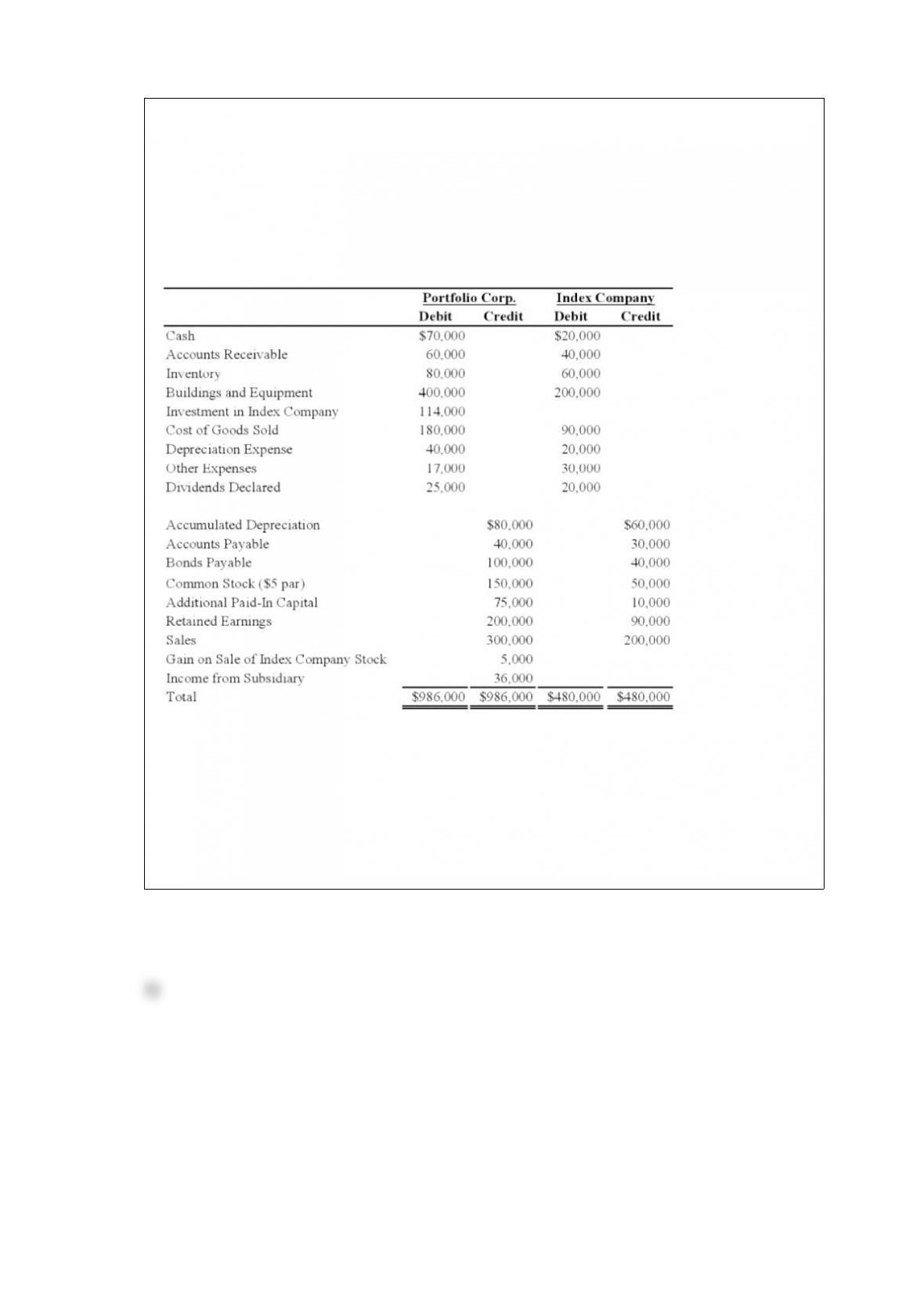

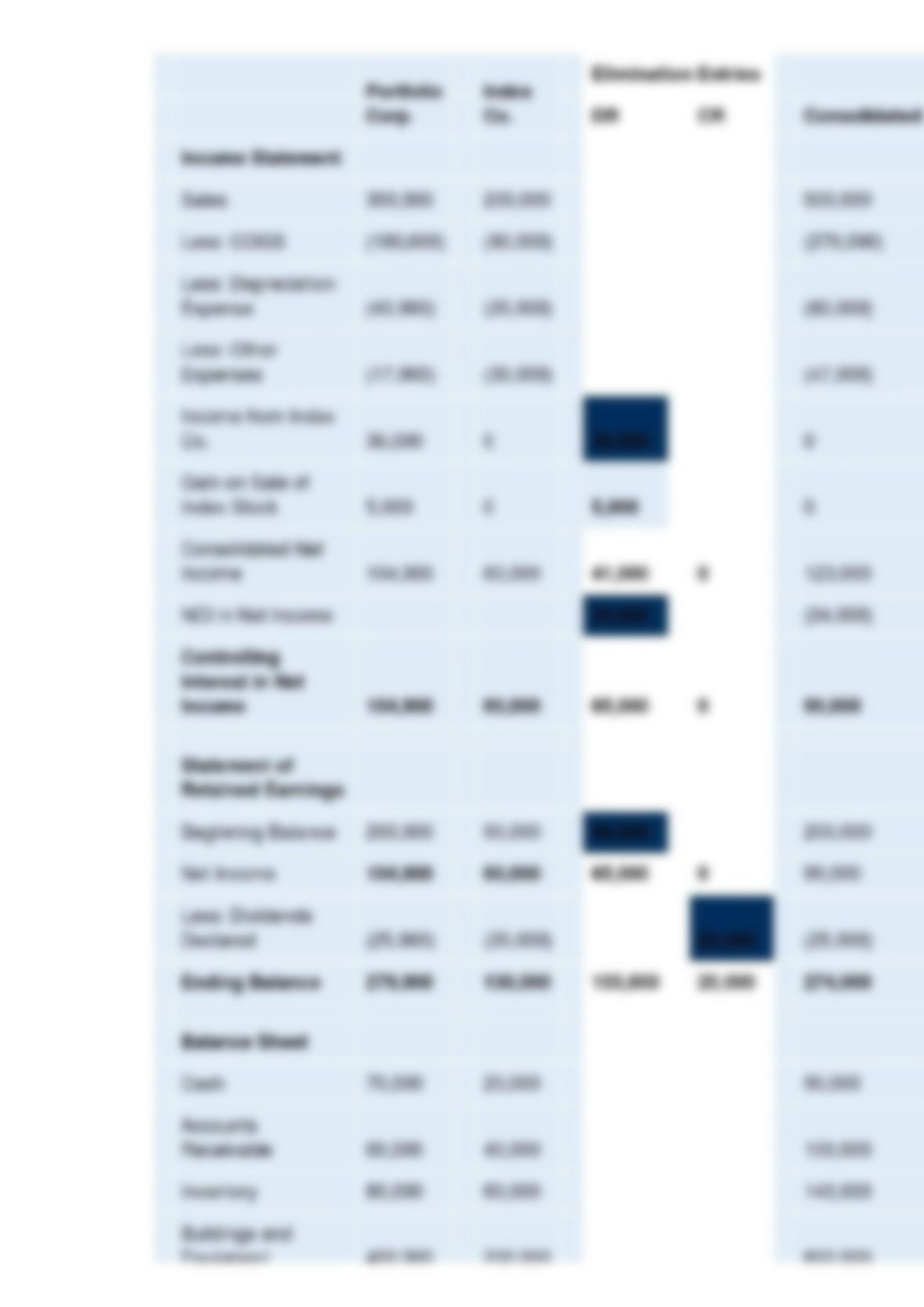

Portfolio Corporation acquired 70 percent ownership of Index Company on January 1,

20X6, at underlying book value. At that date, the fair value of the noncontrolling

interest was equal to 30 percent of the book value of Index. On January 1, 20X8,

Portfolio sold 1,000 shares of Index Company for $20,000 to Adventure Corporation

and recorded a $5,000 gain. Trial balances for the companies on December 31, 20X8,

contain the following data:

Index Company’s net income was earned evenly throughout the year. Both companies

declared and paid their dividends on December 31, 20X8. Portfolio uses the fully

adjusted equity method in accounting for its investment in Index.

Required:

1) Prepare the elimination entries needed to complete a full consolidation worksheet for

20X8.

2) Prepare a consolidation worksheet for 20X8.

Discuss major differences between a governmental entity’s uses of the modified accrual

method and a for-profit corporation’s use of the accrual method.

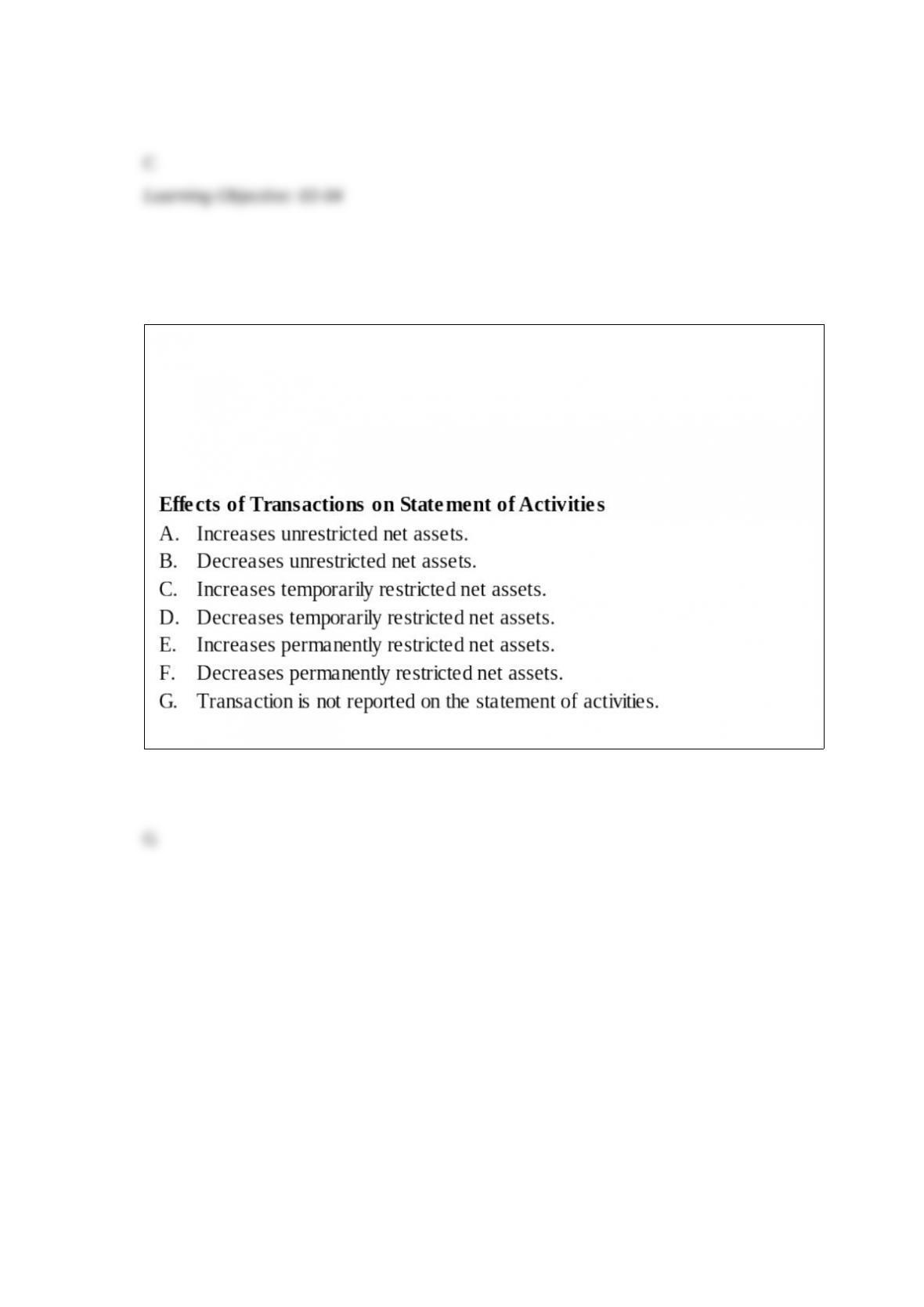

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Expended 75 percent of the contributions previously received from donors for research.

Iona Corporation is in the process of preparing its financial statements for the first

quarter of 20X9 and has asked your advice as to how to report several items. These

items include the following events which took place during the first quarter of 20X9

(assume all amounts are material):

1) Iona redeemed bonds with a carrying value of $4,000,000 at a cost of $3,760,000.

This early extinguishment occurred because Iona wants to issue new debt at lower

interest rates.

2) Iona uses the LIFO method for its inventories. On January 1, 20X9, inventories

amounted to $10,000,000, while, on March 31, 20X9, inventories totaled $9,200,000.

Iona expects to replace the liquidated inventory at the beginning of the second quarter

at a cost of $1,000,000.

3) Iona changed its depreciation method on $4,000,000 of its delivery trucks from the

declining balance method to the straight-line method. On January 1, 20X9, accumulated

depreciation under the declining balance method was $2,800,000. Had the straight-line

method been used, accumulated depreciation on January 1, 20X9, would have been

$2,300,000. The remaining life of the trucks is two years.

4) Iona pays its top executives a bonus at year-end of 6 percent of operating income

before bonus and income taxes. Operating income before bonus and income taxes for

the three months ended March 31, 20X9, was $10,000,000. Iona estimates that its

yearly operating income before bonus and income taxes will be $60,000,000.

5) Iona closes its manufacturing operations in July of each year in order to make its

major annual repairs. Iona estimates that the cost of these repairs in 20X9 will be

$1,000,000.

Required:

For each of the events numbered 1 through 5, indicate how that event should be

reported on Iona’s income statement for the three months ended March 31, 20X9, and

the balance sheet accounts effects at March 31, 20X9. Ignore income taxes.

Consolidated financial statements are required by GAAP in certain circumstances. This

information can be very useful to stockholders and creditors. Yet, there are limitations

to these financial statements for which the users must be aware. What are at least three

(3) limitations of consolidated financial statements?

Which of the following recognition and measurement bases best summarizes the usual

treatment of current contributions to private not-for-profit entities in accordance with

ASC 958?

On March 15, 20X7, Barrel Company paid property taxes of $120,000 on its factory

building for calendar year 20X7. On July 1, 20X7, Barrel made $20,000 in

unanticipated repairs to its machinery. The repairs will benefit operations for the

remainder of the calendar year. What total amount of these expenses should be included

in Barrel’s quarterly income statement for the three months ended September 30, 20X7?

A. $30,000

B. $35,000

C. $40,000

D. $50,000

Pie Company acquired 75 percent of Strawberry Company’s stock at the underlying

book value on January 1, 20X8. At that date, the fair value of the noncontrolling interest

was equal to 25 percent of the book value of Strawberry Company. Strawberry

Company reported shares outstanding of $350,000 and retained earnings of $100,000.

During 20X8, Strawberry Company reported net income of $60,000 and paid dividends

of $3,000. In 20X9, Strawberry Company reported net income of $90,000 and paid

dividends of $15,000. The following transactions occurred between Pie Company and

Strawberry Company in 20X8 and 20X9:

Strawberry Co. sold equipment to Pie Co. for a $42,000 gain on December 31, 20X8.

Strawberry Co. had originally purchased the equipment for $140,000 and it had a

carrying value of $28,000 on December 31, 20X8. At the time of the purchase, Pie Co.

estimated that the equipment still had a seven-year remaining useful life.

Pie Co. sold land costing $90,000 to Strawberry Co. on June 28, 20X9, for $110,000.

Required:

Give all consolidating entries needed to prepare a consolidation worksheet for 20X9

assuming that Pie Co. uses the fully adjusted equity method to account for its

investment in Strawberry Company.

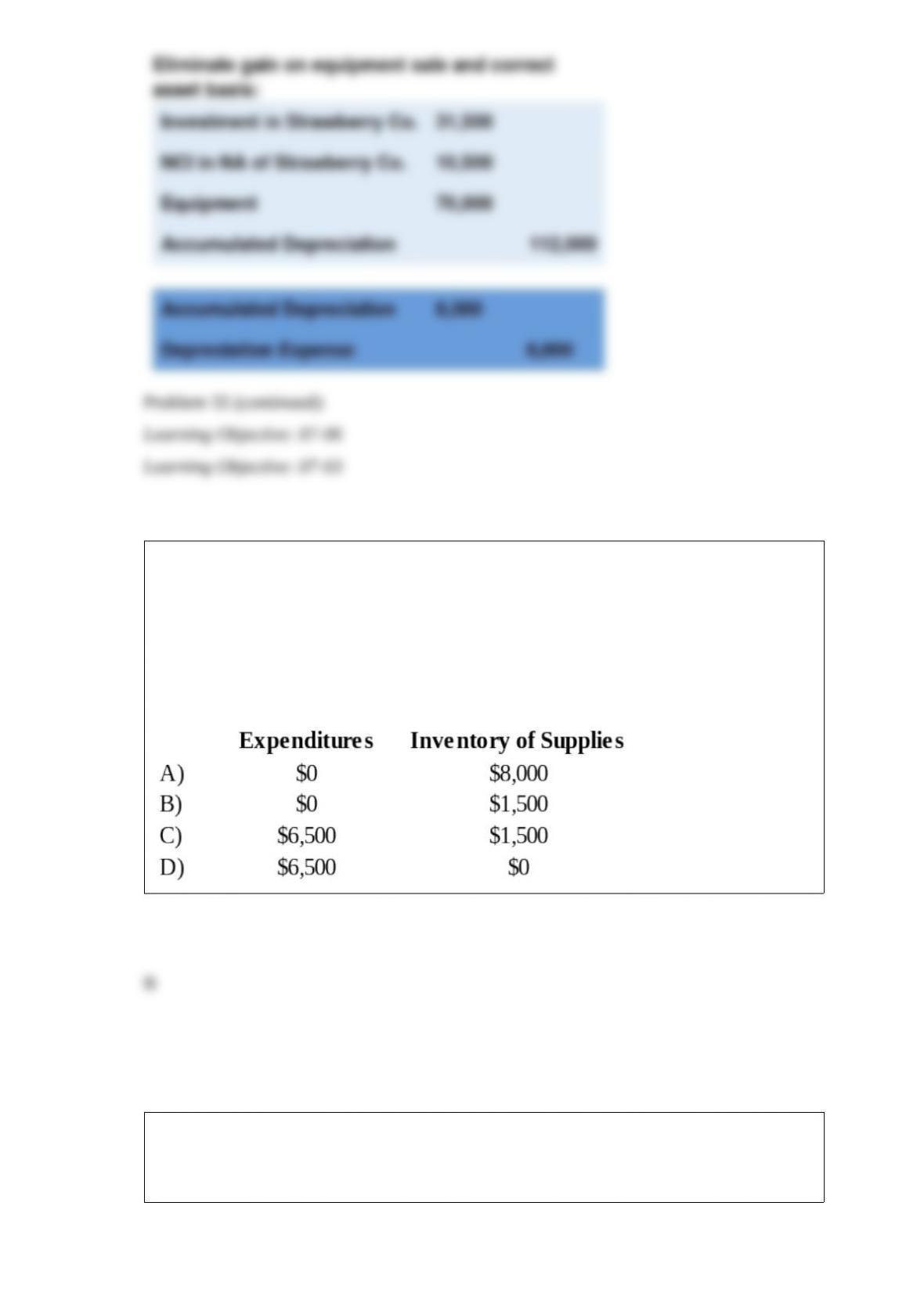

Gotham City acquires $25,000 of inventory on November 1, 20X7, having held no

inventory previously. On December 31, 20X7, the end of Gotham City’s fiscal year, a

physical count shows $8,000 still in stock. During 20X8, $6,500 of this inventory is

used, resulting in a $1,500 remaining balance of supplies on December 31, 20X8.

Based on the preceding information, which of the following would be the correct

account balances for 20X8 if Gotham City used the purchase method of accounting for

inventories?

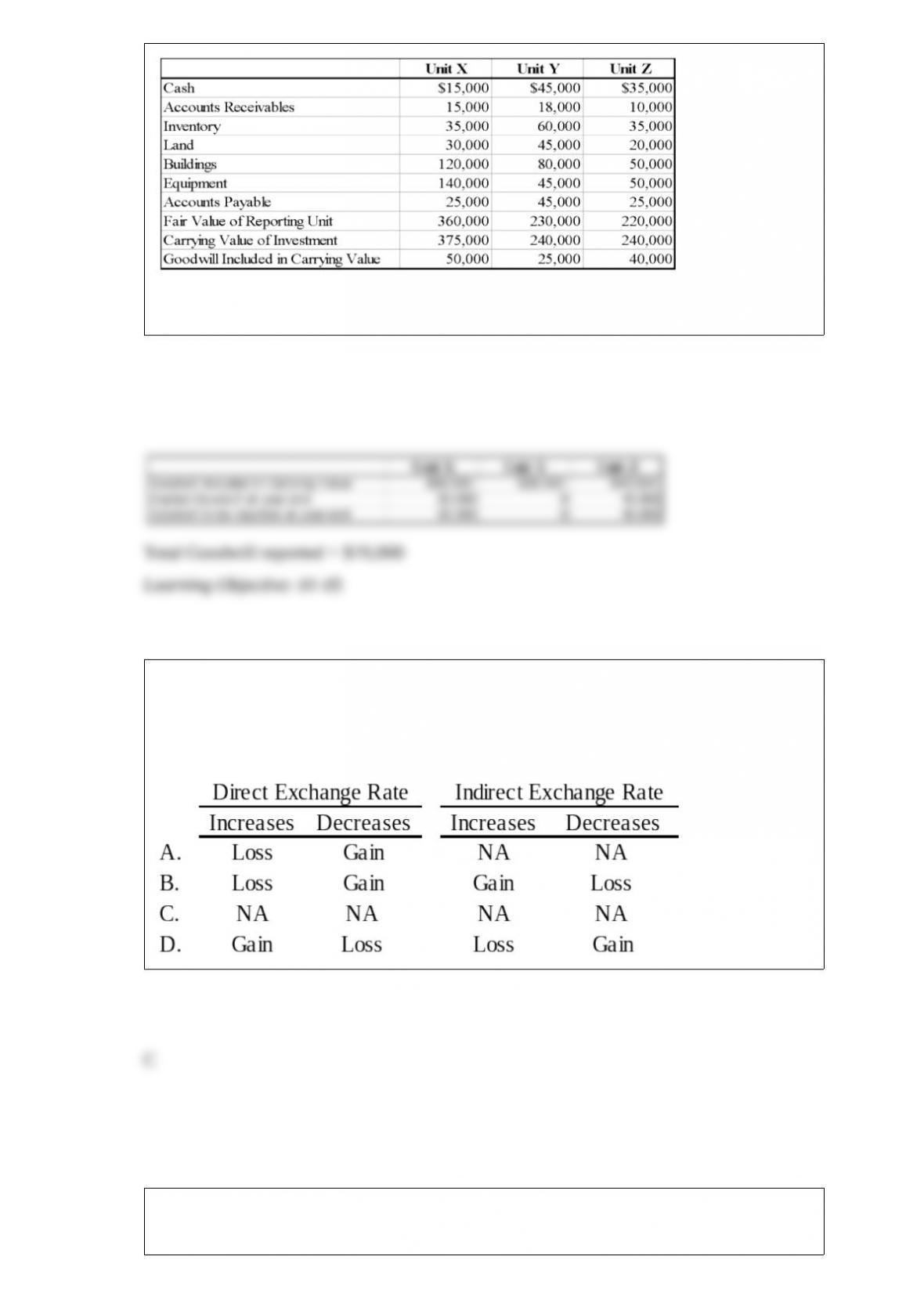

SeaLine Corporation is involved in the distribution of processed marine products. The

fair values of assets and liabilities held by three reporting units and other information

related to the reporting units owned by SeaLine are as follows:

Required: Determine the amount of goodwill that SeaLine should report in its current

financial statements.

Corporation X has a number of exporting transactions with companies based in

Vietnam. Exporting activities result in receivables. If the settlement currency is the US

dollar, which of the following will happen by changes in the direct or indirect exchange

rates?

GASB 34 requires a Reconciliation schedule for the Statement of Net Assets. What

does this schedule document?

The SRT partnership agreement specifies that partnership net income be allocated as

follows:

Partner S Partner R Partner T

Salary allowance $20,000 $25,000 $15,000

Interest on average capital balance 10% 10% 10%

Remainder 30% 30% 40%

Average capital balances for the current year were $60,000 for S, $50,000 for R, and

$40,000 for T.

Refer to the information given. Assuming a current year net income of $45,000, what

amount should be allocated to each partner?

Partner S Partner R Partner T

A. $17,000 $21,000 $7,000

B. ($9,000) ($9,000) ($12,000)

C. $13,500 $13,500 $18,000

D. $22,500 $22,500 $0

Maple Corporation and its subsidiary reported consolidated net income of $380,000 for

the year ended December 31, 20X5. Maple owns 75% of the common shares of its

subsidiary, acquired at book value. Noncontrolling interest was assigned income of

$25,000 in the consolidated income statement for 20X5. What is the amount of separate

operating income reported by Maple for the year?

A. $95,000

B. $100,000

C. $280,000

D. $285,000

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

The governing board designated assets for plant expansion.