Chapter 20 – Corporations in Financial Difficulty

E20-2 (continued)

b.

Journal entries to record reorganization:

(1)

Accounts Payable

80,000

Notes Payable, 10%

150,000

Interest Payable

40,000

Cash

6,000

Accounts Receivable (net)

72,000

Land

85,000

Gain on Disposal of Land

40,000

Gain on Discharge of Debt

67,000

Record discharge of debt.

(2)

Common Stock ($1 par)

100,000

Additional Paid-In Capital

171,000

Gain on Disposal of Land

40,000

Gain on Discharge of Debt

67,000

Common Stock ($2 par)

200,000

Retained Earnings

178,000

Record change in par value of stock and elimination of deficit.

E20-3 Multiple-Choice Questions on Chapter

7 Liquidations

1.

b –

The amount of wages cannot exceed $10,000.

2.

a –

These costs have the highest priority of all unsecured claims.

(b) incorrect. These are the sixth priority.

(c) incorrect. These are the third priority.

(d) incorrect. These are treated as regular employees, third priority.

3.

d –

costs of filing the involuntary petition and appointment of trustees has the highest

priority of all unsecured claims.

(a) incorrect. Administrative expenses have first claim.

(b) incorrect. Employee wages have a higher priority than governmental units.

(c) incorrect. Administrative expenses have first claim.

4.

a –

3 or more creditors are required to file the petition.

(b) incorrect. There are 2 requirements, (1) the debtor is generally not paying

debts as they become due or within the last 120 days has had a custodian

appointed by other creditors, by the debtor, or by some other agency to take

possession of the debtor’s assets. (2) if more than 12 creditors exist, 3 or more

must combine to file the petition, and these must have aggregate unsecured

claims of at least $5,000.

(c) incorrect. See answer to B.

(d) incorrect. See answer to B.

5.

c –

A transaction of the type is voidable. The money will be returned to the debtor and

paid according to priority.

(a) incorrect. The debtor must meet all the demands of his creditors according to

priority until funds run out.

(b) incorrect. Insolvency is a required disclosure regardless of the expected time

period.

(d) incorrect. Debtors are allowed to file a voluntary petition for bankruptcy, it is

called a voluntary petition.

E20-4 Chapter 7 Liquidation

a.

Schedule to calculate amount available for general unsecured creditors:

Total estimated fair values

$471,000

Claims of secured creditors:

Notes payable and interest

(Receivables and Inventory)

$115,000

Bonds payable and interest

(Land and Building)

231,000

(346,000)

$125,000

Claims of creditors with priority:

Wages payable

$ 9,500

Taxes payable

14,000

(23,500)

Available to general unsecured creditors

$101,500

b.

Accounts payable

$ 95,000

Notes payable and interest

$195,000

Less: Secured by receivables and inventory

(115,000)

80,000

Total unsecured claims

$175,000

Estimated dividend:

$101,500

= 58%

$175,000

c.

Group

Credit

Percentage

Distributed

Accounts Payable

$ 95,000

58%

$ 55,100

Wages Payable

9,500

100

9,500

Taxes Payable

14,000

100

14,000

Notes Payable

80,000

58

46,400

and Interest

115,000

100

115,000

Bonds Payable

and Interest

231,000

100

231,000

$471,000

E20-5 Statement of Realization and Liquidation

Pace Corporation

Statement of Realization and Liquidation

Assets

Assets to be Realized

Assets Realized

Old Receivables, net

$ 38,000

Old Receivables

$ 21,000

Marketable Securities

12,000

New Receivables

47,000

Old Inventory

60,000

Marketable Securities

10,500

Depreciable Assets, net

96,000

Sales of Inventory

75,000

Assets Acquired

Assets Not Realized

New Receivables

75,000

Old Receivables, net

17,000

New Receivables, net

28,000

Depreciable Assets

80,000

Supplementary Items

Supplementary Charges

Supplementary Credits

Trustee’s Fee

$ 4,300

Net Loss

$ 6,800

Liabilities

Liabilities Liquidated

Liabilities to be Liquidated

Old Current Payables

$ 22,000

Old Current Payables

$ 48,000

Liabilities Not Liquidated

Liabilities Incurred

Old Current Payables

26,000

$333,300

$333,300

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This

document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website in whole or part.

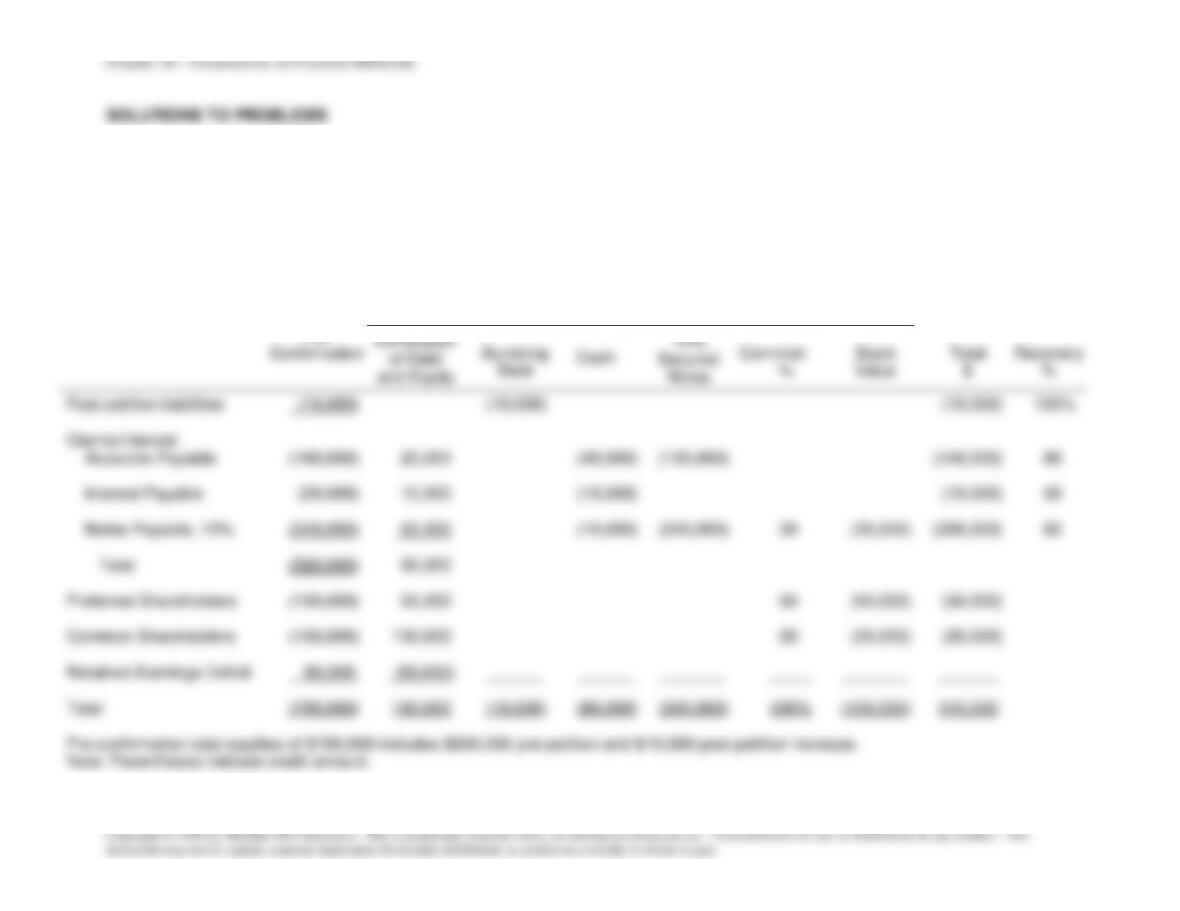

P20-6 Chapter 11 Reorganization

a.

Recovery analysis for plan of reorganization:

Polydorous Corporation

Plan of Reorganization

Recovery Analysis

Recovery

Pre-

Confirmation

Elimination

of Debt

and Equity

Surviving

Debt

Cash

12%

Secured

Notes

Common

%

Stock

Value

Total

$

Recovery

%

Post-petition liabilities

(10,000)

(10,000)

(10,000)

100%

Claims/Interest:

Accounts Payable

(160,000)

20,000

(40,000)

(100,000)

(140,000)

88

Interest Payable

(20,000)

10,000

(10,000)

(10,000)

50

Notes Payable, 10%

(340,000)

60,000

(10,000)

(240,000)

30

(30,000)

(280,000)

82

Total

(520,000)

90,000

Preferred Shareholders

(100,000)

50,000

50

(50,000)

(50,000)

Common Shareholders

(150,000)

130,000

20

(20,000)

(20,000)

Retained Earnings Deficit

80,000

(80,000)

Total

(700,000)

190,000

(10,000)

(60,000)

(340,000)

100%

(100,000)

510,000

Pre-confirmation total equities of $700,000 includes $690,000 pre-petition and $10,000 post-petition increase.

Note: Parentheses indicate credit amount.

P20-6 (continued)

b.

Analysis for evaluating qualifications for fresh start accounting:

First condition:

Post-petition liabilities

$ 10,000

Liabilities deferred pursuant to Chapter 11 proceedings

520,000

Total post-petition liabilities and allowed claims

$530,000

Reorganization value

(510,000)

Excess of liabilities over reorganization value

$ 20,000

Second condition:

Holders of existing voting shares immediately before confirmation receive 20%

of voting shares of emerging entity.

Therefore, both conditions for a fresh start occur, and fresh start accounting is

used to account for the company.

c.

Entries for execution of plan of reorganization:

(1)

Liabilities Subject to Compromise

520,000

Cash

60,000

Notes Payable, 12%, secured

340,000

Common Stock (new)

30,000

Gain on Debt Discharge

90,000

Record debt discharge.

(2)

Preferred Stock

100,000

Common Stock (old)

150,000

Common Stock (new)

70,000

Additional Paid-In Capital

180,000

Record exchange of stock for stock.

(3)

Reorganization Value in Excess of Amounts

Allocable to Identifiable Assets

30,000

Gain on Debt Discharge

90,000

Additional Paid-In Capital

180,000

Accounts Receivable (net)

30,000

Inventory

7,000

Property, Plant, and Equipment

183,000

Retained Earnings – Deficit

80,000

Record fresh start accounting and eliminate deficit.

P20-6 (continued)

Schedule to support allocation of reorganization value:

Book

Fair

Value

Value

Difference

Cash

$ 30,000

$ 30,000

$ -0-

Accounts Receivable (net)

140,000

110,000

(30,000)

Inventory

25,000

18,000

(7,000)

Property, Plant, and

Equipment (net)

445,000

262,000

(183,000)

Reorganization Value in Excess

of Amounts Allocable to

Identifiable Assets

-0-

30,000

30,000

Total

$640,000

$450,000

$(190,000)

Note:

The post-reorganization total fair value is the reorganization value of

$510,000 less the $60,000 paid to fulfill the plan of reorganization.

P20-6 (continued)

d. Fresh start balance sheet worksheet for company emerging from reorganization:

(Worksheet not required)

Pre-confirmation

Adjustments to Record

Confirmation of Plan

Company’s

Reorganized

Balance

Sheet

Debt

Exchange

Fresh

Discharge

of Stock

Start

Assets:

Cash

90,000

(60,000)

30,000

Accounts Receivable (net)

140,000

(30,000)

110,000

Inventory

25,000

(7,000)

18,000

255,000

(60,000)

-0-

(37,000)

158,000

Property, Plant,

and Equipment (net)

445,000

(183,000)

262,000

Reorganization Value In

Excess of Amounts

Allocable to

Identifiable Assets

30,000

30,000

Total Assets

700,000

(60,000)

-0-

(190,000)

450,000

Liabilities:

Liabilities Not Subject

to Compromise:

Current Liabilities

(10,000)

(10,000)

Liabilities Subject

to Compromise

(520,000)

520,000

Notes Payable, 12%, secured

(340,000)

(340,000)

Total Liabilities

(530,000)

180,000

-0-

-0-

(350,000)

Shareholders’ Equity:

Preferred Stock

(100,000)

100,000

Common Stock (old)

(150,000)

150,000

Common Stock (new)

(30,000)

(70,000)

(100,000)

Additional Paid-In Capital

(180,000)

180,000

Retained Earnings

80,000

(90,000)

90,000

(80,000)

-0-

Total Shareholders‘ Equity

(170,000)

(120,000)

-0-

190,000

(100,000)

Total Liabilities and

Shareholders’ Equity

(700,000)

60,000

-0-

190,000

(450,000)

Note: Parentheses indicate credit amount.

P20-6 (continued)

d. Balance sheet for company emerging from Chapter 11 reorganization with fresh start

accounting:

Polydorous Company

Balance Sheet

Emerging Date

Assets:

Cash

$ 30,000

Accounts Receivable (net)

110,000

Inventory

18,000

Total Current Assets

$158,000

Property, Plant, and Equipment (net)

262,000

Reorganization Value In Excess of Amounts

Allocable to Identifiable Assets

30,000

Total Assets

$450,000

Liabilities:

Accounts Payable

$ 10,000

Notes Payable, 12%, secured

340,000

Total Liabilities

$350,000

Shareholders’ Equity:

Common Stock

100,000

Total Shareholders‘ Equity

$100,000

Total Liabilities and Shareholders’ Equity

$450,000