Chapter 12 – Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements

E12-13 (continued)

c.

Translated December 31, 20X7, balance sheet:

Subsidiary’s

Direct

Translated

Trial Balance

Exchange

Trial Balance

(in rupees)

Rate

(in $)

Cash

R 80,000

$0.025

$ 2,000

Receivables

550,000

$0.025

13,750

Inventory

720,000

$0.025

18,000

Fixed assets

900,000

$0.025

22,500

Total

R 2,250,000

$56,250

AOCI translation adjustment (debit)

5,635

Total debits

$61,885

Current payables

R 340,000

$0.025

$ 8,500

Long-term debt

1,100,000

$0.025

27,500

Common stock

500,000

$0.03333

16,665

Retained earnings

310,000

(a)

9,220

Total credits

R 2,250,000

$61,885

(a) The retained earnings in dollars would begin with the December 31, 20X6’s,

dollar balance ($6,809) that would be carried forward. To this would be added

20X7’s net income of R 90,000, which is the change in retained earnings in

rupees multiplied by the average 20X7 exchange rate of $.02679 [($.02857 +

$.025)/2] which equals $2,411. Therefore, translated retained earnings on

December 31, 20X7, is $9,220 ($9,220 = $6,809 + $2,411).

(Not required: Proof of translation adjustment (debit) of $5,635)

Translation

Rupees

Rate

Dollars

Net assets, 1/1/X7

R 720,000

$0.02857

$20,570

Adjustment for changes in

net assets during year:

Net income

90,000

$0.02679

2,411

Net assets translated at:

Rates during year

$22,981

Other comprehensive income —

Rate at end of year

R 810,000

$0.025

(20,250)

Change in other comprehensive

Income — translation

adjustment during year (debit)

$ 2,731

Accumulated other comprehensive

Income — translation adjustment, 1/1/X7

2,904

Accumulated other comprehensive

Income — translation adjustment,12/31/X7 (debit)

$ 5,635

d. The $2,731 change in the accumulated other comprehensive income — translation

adjustment during 20X7 would be reported as a component of other

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

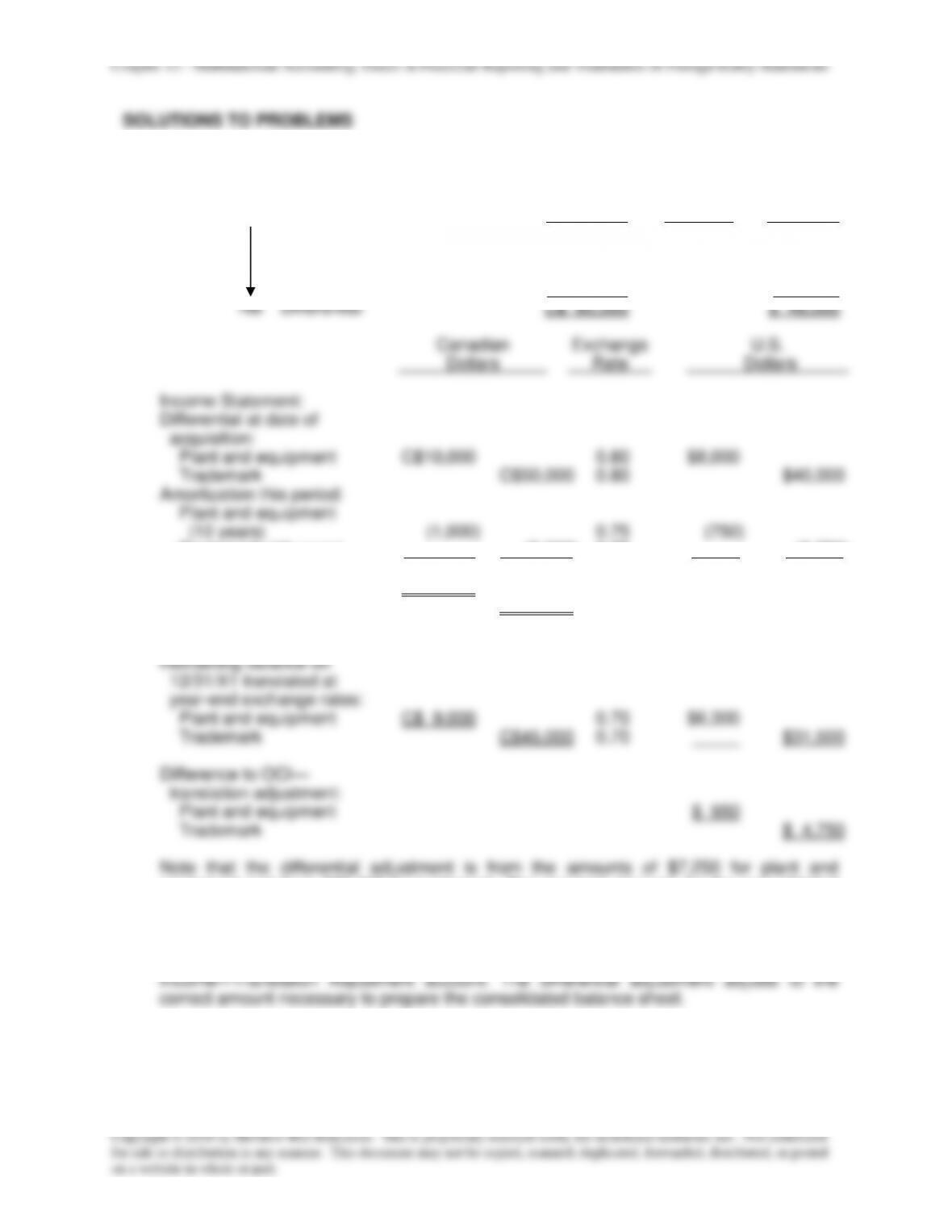

P12-16 Parent Company Journal Entries and Translation

a.

Canadian

Exchange

U.S.

P

Dollars

Rate

Dollars

Investment cost

C$150,000

0.80

$120,000

1/1/X1

Book value of investment

100%

on January 1, 20X1

90,000

0.80

72,000

NB

Differential

C$ 60,000

$ 48,000

Canadian

Exchange

U.S.

Dollars

Rate

Dollars

Income Statement:

Differential at date of

acquisition:

Plant and equipment

C$10,000

0.80

$8,000

Trademark

C$50,000

0.80

$40,000

Amortization this period:

Plant and equipment

(10 years)

(1,000)

0.75

(750)

Trademark (10 years)

(5,000)

0.75

(3,750)

Remaining balance:

Plant and equipment

C$ 9,000

$7,250

Trademark

C$45,000

$36,250

Balance Sheet:

Remaining balance on

12/31/X1 translated at

year-end exchange rates:

Plant and equipment

C$ 9,000

0.70

$6,300

Trademark

C$45,000

0.70

$31,500

Difference to OCI—

translation adjustment:

Plant and equipment

$ 950

Trademark

$ 4,750

Note that the differential adjustment is from the amounts of $7,250 for plant and

equipment and from $36,250 for trademark. The required amounts for the consolidated

balance sheet are $6,300 for plant and equipment, and $31,500 for trademark. Therefore,

in each of these cases, the differential adjustment will reduce the amount of the

differential component in the investment account, requiring a credit to the Investment in

North Bay Company account with a corresponding debit to the Other Comprehensive

Income—Translation Adjustment account. The differential adjustment adjusts to the

correct amount necessary to prepare the consolidated balance sheet.