Chapter 06 – Intercompany Inventory Transactions

P6–24 (continued)

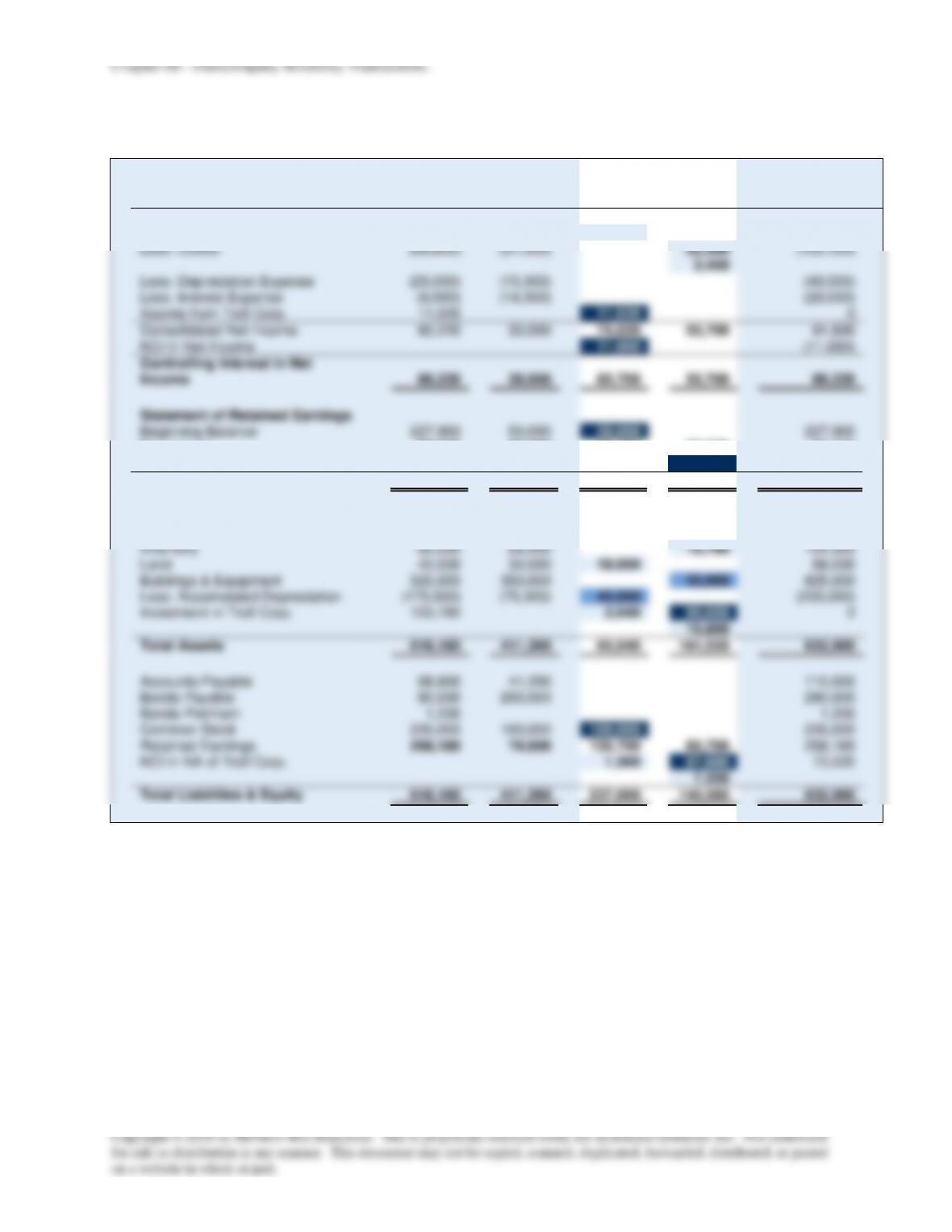

Adjustment to Basic Consolidation Entry

NCI

Priority

Net Income

9,000

81,000

+Reverse GP deferral (down)

8,000

+Reverse GP deferral (up)

600

5,400

– Gross profit deferral (down)

(2,000)

– Gross profit deferral (up)

(1,400)

(12,600)

Income to be eliminated

8,200

79,800

———————————————————-—————————

Ending Book Value

143,000

1,287,000

+Reverse GP deferral (down)

8,000

+Reverse GP deferral (up)

600

5,400

– Gross profit deferral (down)

(2,000)

– Gross profit deferral (up)

(1,400)

(12,600)

Adjusted Book Value

142,200

1,285,800

Basic Consolidation Entry

Common Stock

400,000

← Common stock balance

Additional Paid-in Capital

200,000

← Beginning balance in APIC

Retained Earnings

790,000

← Beginning balance in RE

Accumulated OCI

10,000

← Beginning balance in Acc. OCI

Income from Tall Corp.

79,800

← PC.’s % of NI with adjustment

NCI in NI of Tall Corp.

8,200

← NCI share of NI with adjustment

Dividends

Investment in Tall Corp.

60,000

1,285,800

← Dividends declared by subsidiary

← Net book value with adjustment

NCI in NA of Tall Corp.

142,200

← NCI share of BV with adjustment

Other Comprehensive Income Entry:

OCI from Tall Corp.

18,000

OCI to the NCI

2,000

Investment in Tall Corp.

18,000

NCI in NA of Tall Corp.

2,000

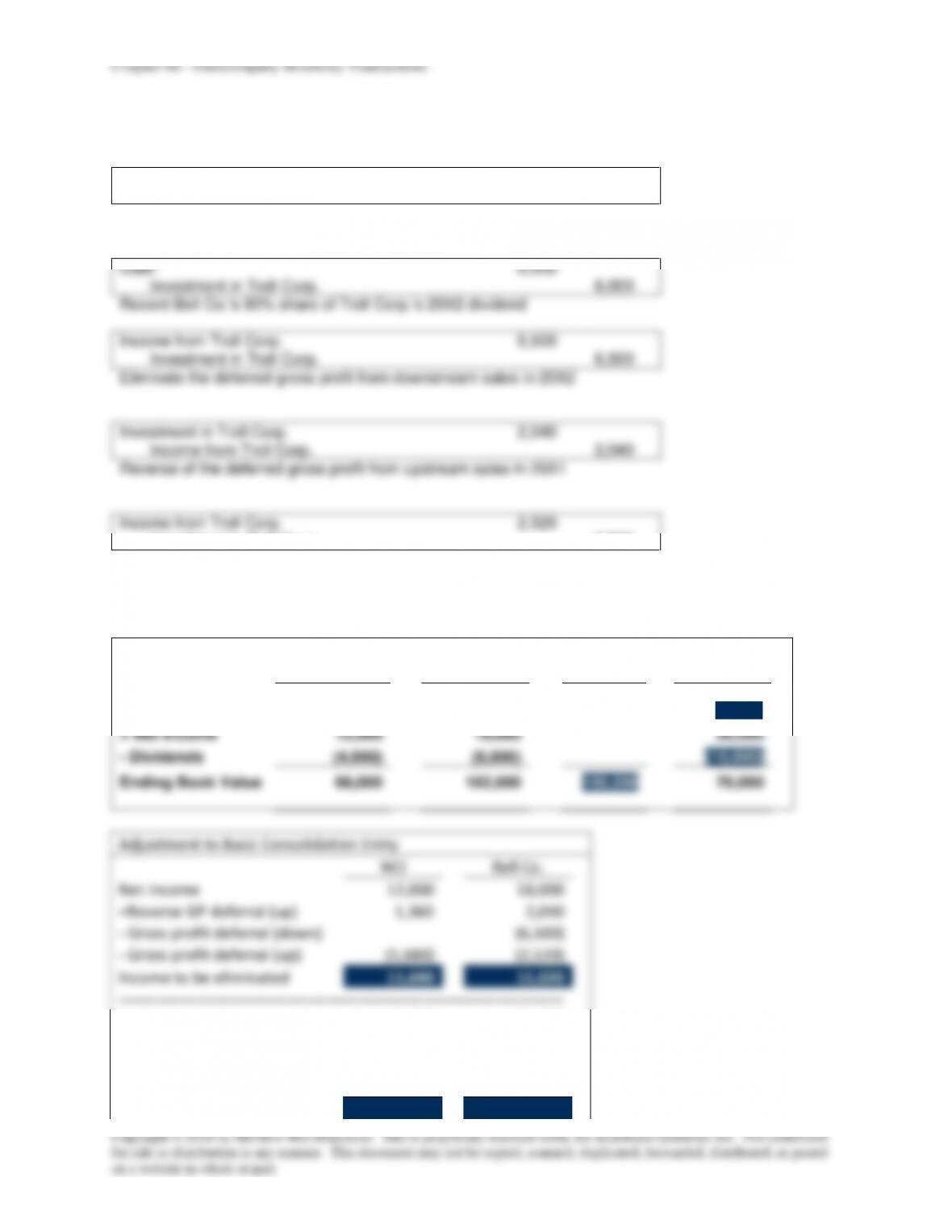

Reversal of last year’s deferral:

Investment in Tall Corp.

13,400

NCI in NA of Tall Corp.

600

Cost of Goods Sold

14,000

Deferral of this year’s unrealized profits on inventory transfers

Sales

126,000

Cost of Goods Sold

110,000

Inventory

16,000

Chapter 06 – Intercompany Inventory Transactions

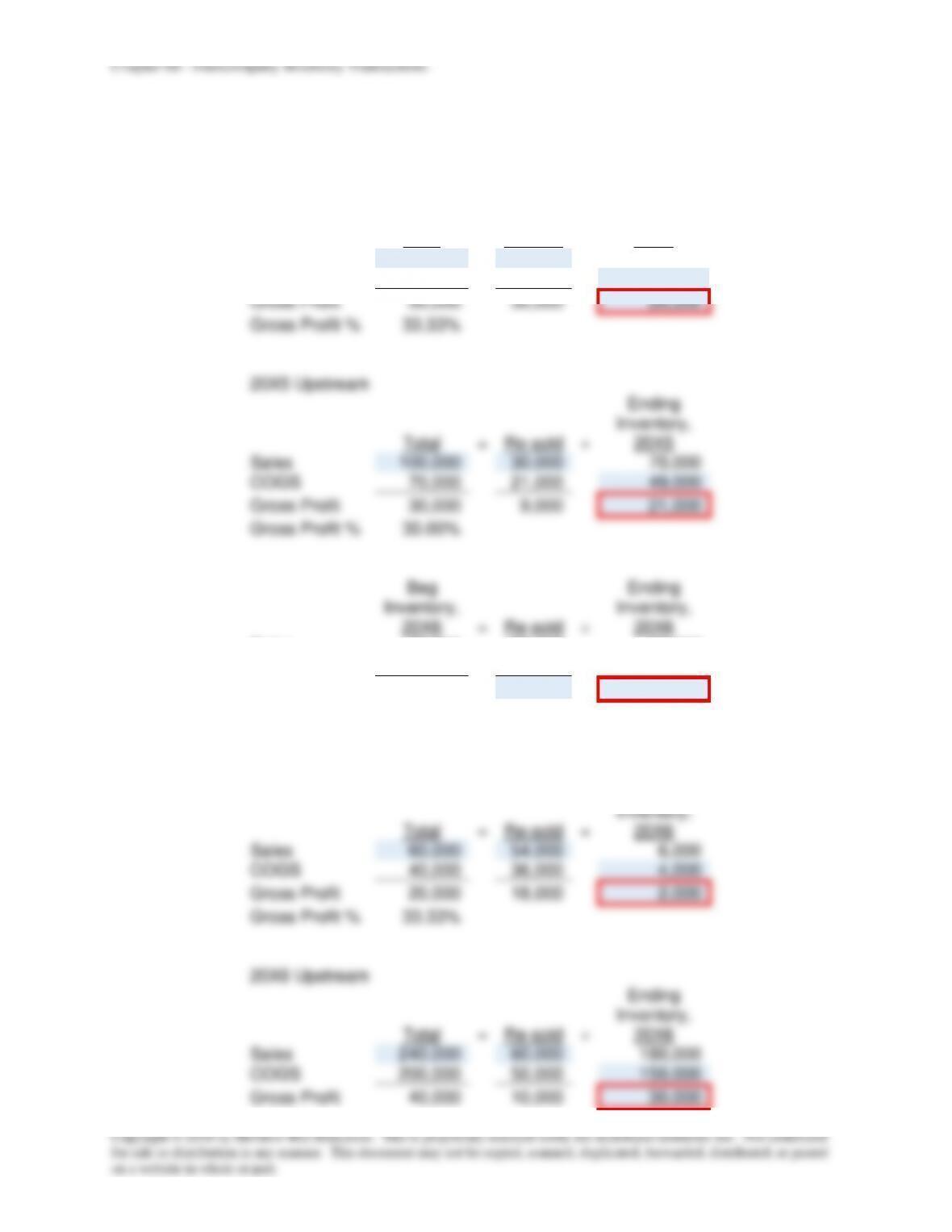

Gross Profit %

16.67%

Chapter 06 – Intercompany Inventory Transactions

a.

Consolidation entries:

Investment in Slinky

20,000

Cost of goods sold

20,000

Eliminate beginning inventory profit of Proud Company.

Investment in Slinky

12,600

NCI in NA of Slinky

8,400

Cost of goods sold

15,000

Inventory

6,000

Eliminate beginning inventory profit of Slinky Company.

Sales

60,000

Cost of goods sold

58,000

Inventory

2,000

Eliminate intercompany sale of inventory by Proud Company.

Sales

240,000

Cost of goods sold

210,000

Inventory

30,000

Eliminate intercompany sale of inventory by Slinky Company.

The basic entry (not shown) would be adjusted by 38,000 of deferred

profit and 35,000 to reverse the prior year gross profit deferral and

complete the elimination process.

b.

Computation of cost of goods sold for consolidated entity:

Inventory produced by Proud in 20X5

($100,000 x 0.40)

$ 40,000

Inventory produced by Slinky in 20X5

($70,000 x 0.50)

35,000

Inventory produced by Proud in 20X6

($40,000 x 0.90)

36,000

Inventory produced by Slinky in 20X6

($200,000 x 0.25)

50,000

Cost of goods sold reported in

consolidated income statement

$161,000