Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-21

E4-16 (continued)

b.

Gold

Enterprises

Premium

Builders

Consolidation Entries

DR

CR

Consolidated

Balance Sheet

Cash and Receivables

80,000

30,000

2,000

108,000

Inventory

150,000

350,000

7,000

507,000

Buildings & Equipment (net)

430,000

80,000

12,000

522,000

Investment in Premium Builders

167,000

150,000

0

17,000

Total Assets

827,000

460,000

19,000

169,000

1,137,000

Current Liabilities

100,000

110,000

210,000

Long-Term Debt

400,000

200,000

600,000

Common Stock

200,000

140,000

140,000

200,000

Retained Earnings

127,000

10,000

10,000

127,000

Total Liabilities & Equity

827,000

460,000

150,000

0

1,137,000

c.

Gold Enterprises and Subsidiary

Consolidated Balance Sheet

January 1, 20X5

Cash and Receivables

$ 108,000

Current Liabilities

$ 210,000

Inventory

507,000

Long-Term Debt

600,000

Buildings and

Common Stock

$200,000

Equipment (net)

522,000

Retained Earnings

127,000

327,000

Total Liabilities &

Total Assets

$1,137,000

Stockholders' Equity

$1,137,000

Investment in

Premium Builders

Acquisition Price

167,000

150,000

Basic

17,000

Excess Reclass.

0

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-22

E4-17 Computation of Consolidated Balances

a.

Inventory

$ 440,000

b.

Land

$ 145,000

c.

Buildings and Equipment

$ 1,750,000

d. Goodwill:

Fair value of consideration given

$ 576,000

Book value of net assets

at acquisition

$450,000

Fair value increment for:

Inventory

20,000

Land

(10,000)

Buildings and equipment

70,000

Fair value of net assets

at acquisition

(530,000)

Balance assigned to goodwill

$ 46,000

e.

Investment in Astor Corporation: Nothing would be reported; the balance in the

investment account is eliminated.

E4-18 Multiple-Choice Questions on Balance Sheet Consolidation

1.

d –

$215,000

=

$130,000 + $85,000

2.

b –

$23,000

=

$198,000 – ($405,000 - $265,000 + $15,000 + $20,000)

3.

c –

$1,109,000

=

Total Assets of Top Corp.

$ 844,000

Less: Investment in Sun Corp.

(198,000)

Book value of assets of Top Corp.

$ 646,000

Book value of assets of Sun Corp.

405,000

Total book value

$1,051,000

Payment in excess of book value

($198,000 - $140,000)

58,000

Total assets reported

$1,109,000

4.

c –

$701,500

=

($61,500 + $95,000 + $280,000) + ($28,000 + $37,000

+ $200,000)

5.

d –

$257,500

=

The amount reported by Top Corporation

6.

a –

$407,500

=

The amount reported by Top Corporation

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

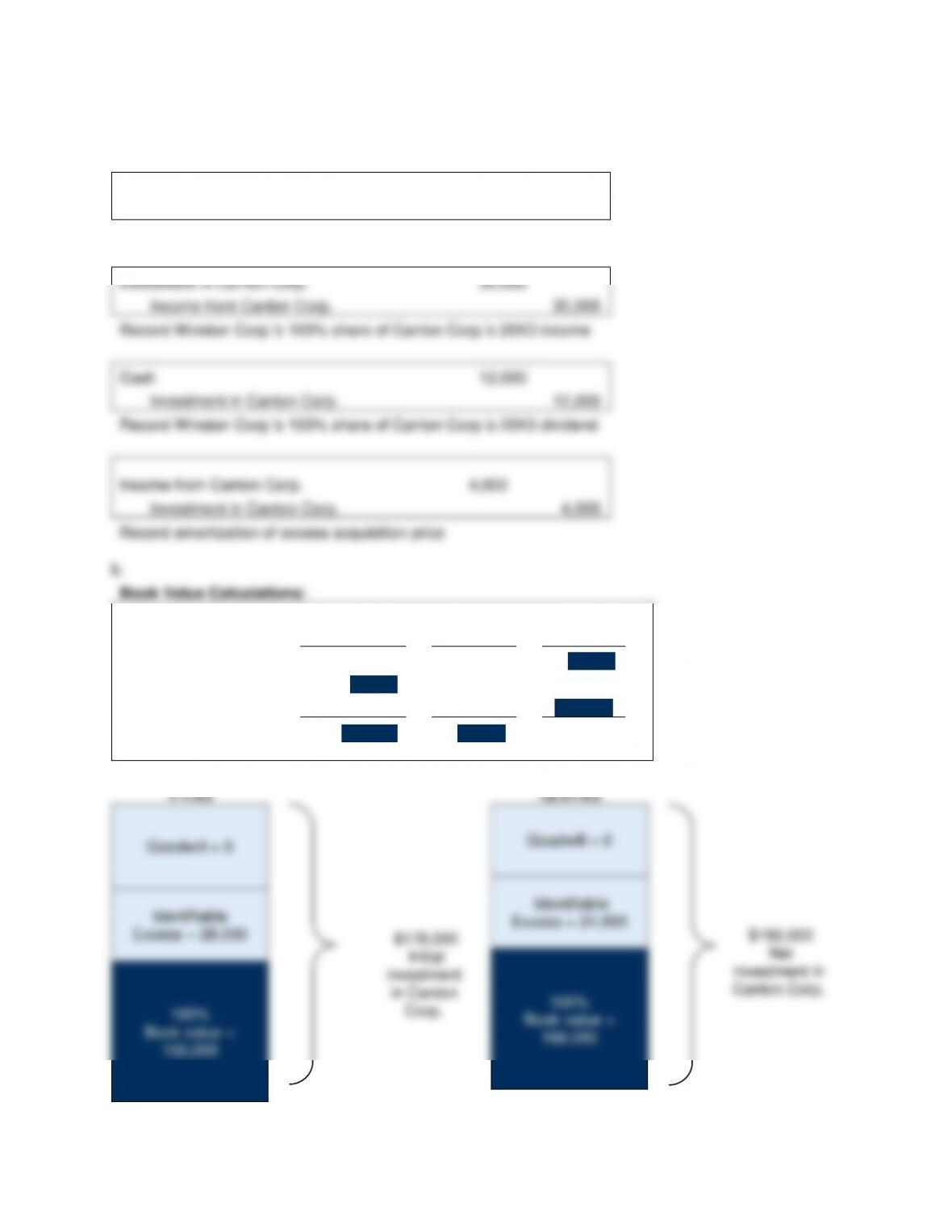

E4-19 Wholly Owned Subsidiary with Differential

a.

Equity Method Entries on Winston Corp.'s Books:

Investment in Canton Corp.

178,000

Cash

178,000

Record the initial investment in Canton Corp.

Investment in Canton Corp.

30,000

Income from Canton Corp.

30,000

Record Winston Corp.'s 100% share of Canton Corp.'s 20X3 income

Cash

12,000

Investment in Canton Corp.

12,000

Record Winston Corp.'s 100% share of Canton Corp.'s 20X3 dividend

Income from Canton Corp.

4,000

Investment in Canton Corp.

4,000

Record amortization of excess acquisition price

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book value

150,000

60,000

90,000

+ Net Income

30,000

30,000

- Dividends

(12,000)

(12,000)

Ending book value

168,000

60,000

108,000

1/1/X3

Goodwill = 0

Identifiable

Excess = 28,000

$178,000

Initial

investment

in Canton

Corp.

100%

Book value =

150,000

12/31/X3

Goodwill = 0

Identifiable

Excess = 24,000

$192,000

Net

investment in

Canton Corp.

100%

Book value =

168,000

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-24

E4-19 (continued)

Basic Consolidation Entry

Common stock

60,000

Retained earnings

90,000

Income from Canton Corp.

30,000

Dividends declared

12,000

Investment in Canton Corp.

168,000

Excess Value (Differential) Calculations:

Total

=

Equipment

+

Acc.

Depr.

Beginning Balances

28,000

28,000

Changes

(4,000)

(4,000)

Ending Balances

24,000

28,000

(4,000)

Amortized Excess Value Reclassification Entry:

Depreciation Expense

4,000

Income from Canton Corp.

4,000

Excess value (differential) reclassification entry:

Equipment

28,000

Accumulated depreciation

4,000

Investment in Canton Corp.

24,000

Investment in

Income from

Canton Corp.

Canton Corp.

Acquisition Price

178,000

100% Net Income

30,000

30,000

100% Net Income

12,000

100% Dividends

4,000

Excess Val. Amort.

4,000

Ending Balance

192,000

26,000

Ending Balance

168,000

Basic

30,000

24,000

Excess Reclass.

4,000

0

0

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

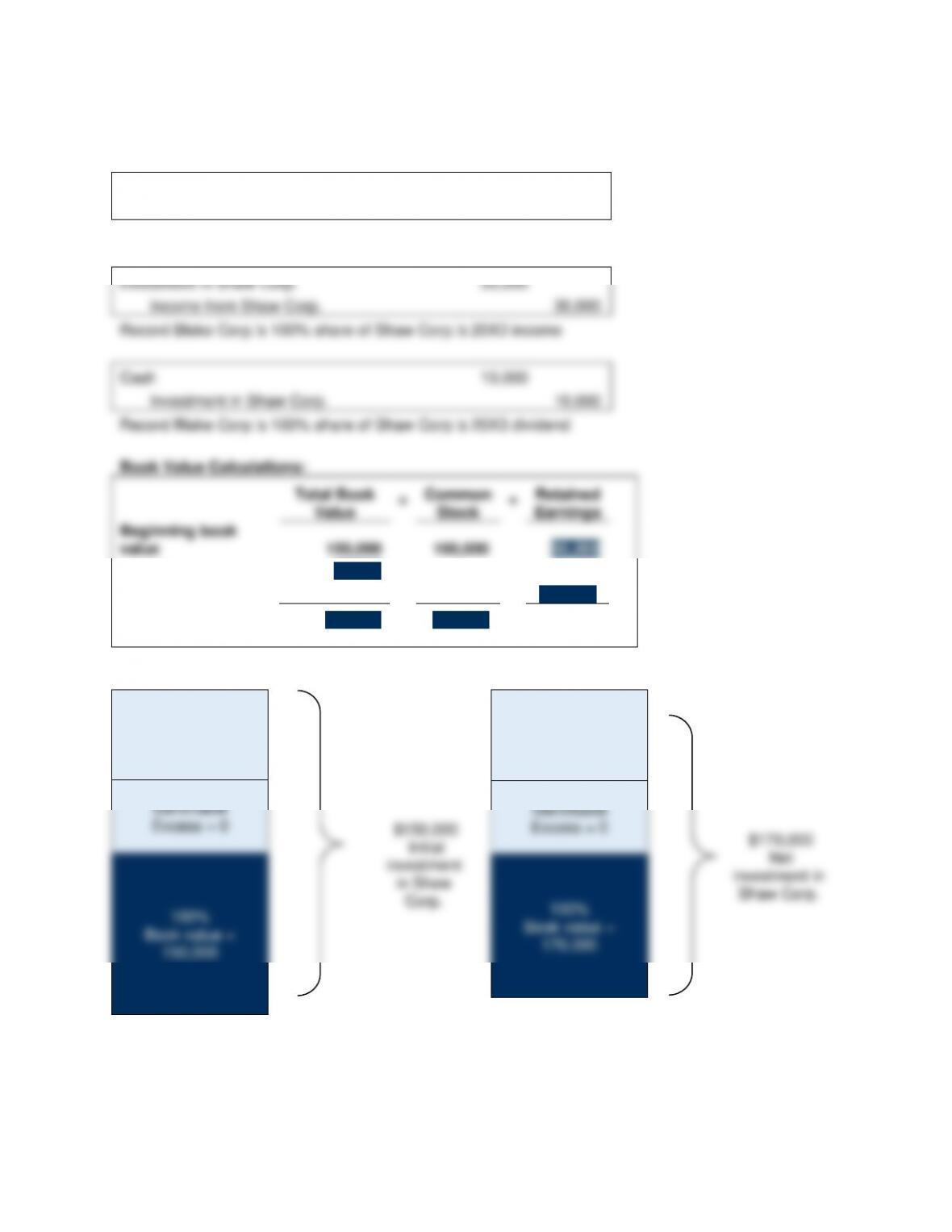

E4-20 Basic Consolidation Worksheet

a.

Equity Method Entries on Blake Corp.'s Books:

Investment in Shaw Corp.

150,000

Cash

150,000

Record the initial investment in Shaw Corp.

Investment in Shaw Corp.

30,000

Income from Shaw Corp.

30,000

Record Blake Corp.'s 100% share of Shaw Corp.'s 20X3 income

Cash

10,000

Investment in Shaw Corp.

10,000

Record Blake Corp.'s 100% share of Shaw Corp.'s 20X3 dividend

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

150,000

100,000

50,000

+ Net Income

30,000

30,000

- Dividends

(10,000)

(10,000)

Ending book value

170,000

100,000

70,000

1/1/X3

Goodwill = 0

Identifiable

Excess = 0

$150,000

Initial

investment

in Shaw

Corp.

100%

Book value =

150,000

12/31/X3

Goodwill = 0

Identifiable

Excess = 0

$170,000

Net

investment in

Shaw Corp.

100%

Book value =

170,000

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-26

E4-20 (continued)

Basic Consolidation Entry

Common Stock

100,000

Retained Earnings

50,000

Income from Shaw Corp.

30,000

Dividends Declared

10,000

Investment in Shaw Corp.

170,000

Investment in

Income from

Shaw Corp.

Shaw Corp.

Acquisition Price

150,000

100% Net Income

30,000

30,000

100% Net Income

10,000

100%

Dividends

Ending Balance

170,000

30,000

Ending Balance

170,000

Basic

30,000

0

0

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-27

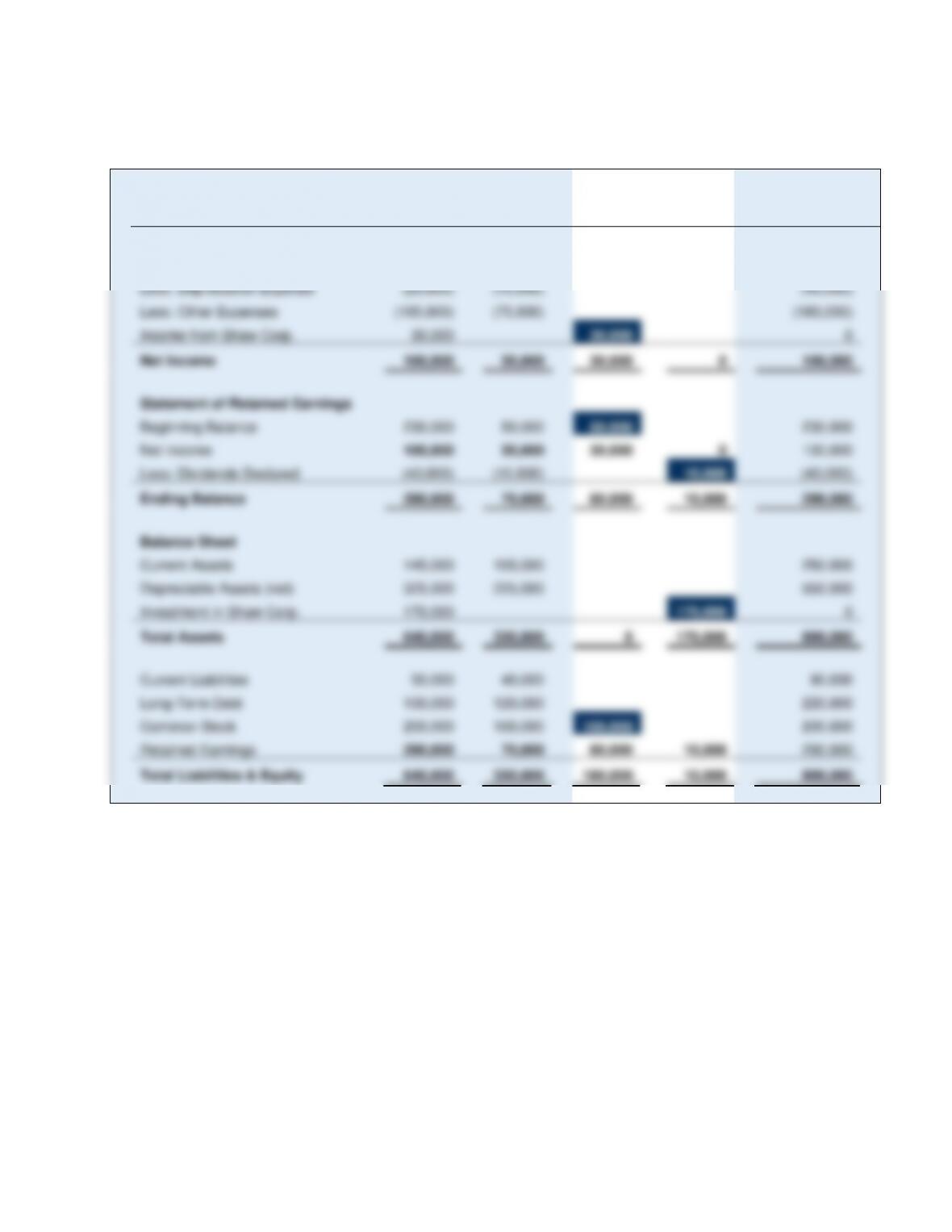

E4-20 (continued)

b.

Blake

Corp.

Shaw

Corp.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

200,000

120,000

320,000

Less: Depreciation Expense

(25,000)

(15,000)

(40,000)

Less: Other Expenses

(105,000)

(75,000)

(180,000)

Income from Shaw Corp.

30,000

30,000

0

Net Income

100,000

30,000

30,000

0

100,000

Statement of Retained Earnings

Beginning Balance

230,000

50,000

50,000

230,000

Net Income

100,000

30,000

30,000

0

100,000

Less: Dividends Declared

(40,000)

(10,000)

10,000

(40,000)

Ending Balance

290,000

70,000

80,000

10,000

290,000

Balance Sheet

Current Assets

145,000

105,000

250,000

Depreciable Assets (net)

325,000

225,000

550,000

Investment in Shaw Corp.

170,000

170,000

0

Total Assets

640,000

330,000

0

170,000

800,000

Current Liabilities

50,000

40,000

90,000

Long-Term Debt

100,000

120,000

220,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

290,000

70,000

80,000

10,000

290,000

Total Liabilities & Equity

640,000

330,000

180,000

10,000

800,000

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

E4-21 Basic Consolidation Worksheet for Second Year

a.

Equity Method Entries on Blake Corp.'s Books:

Investment in Shaw Corp.

35,000

Income from Shaw Corp.

35,000

Record Blake Corp.'s 100% share of Shaw Corp.'s 20X4 income

Cash

15,000

Investment in Shaw Corp.

15,000

Record Blake Corp.'s 100% share of Shaw Corp.'s 20X4 dividend

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

170,000

100,000

70,000

+ Net Income

35,000

35,000

- Dividends

(15,000)

(15,000)

Ending book value

190,000

100,000

90,000

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-29

E4-21 (continued)

Basic Consolidation Entry

Common Stock

100,000

Retained Earnings

70,000

Income from Shaw Corp.

35,000

Dividends Declared

15,000

Investment in Shaw Corp.

190,000

Investment in

Income from

Shaw Corp.

Shaw Corp.

Beginning Balance

170,000

100% Net Income

35,000

35,000

100% Net Income

15,000

100%

Dividends

Ending Balance

190,000

35,000

Ending Balance

190,000

Basic

35,000

0

0

Chapter 04 - Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-30

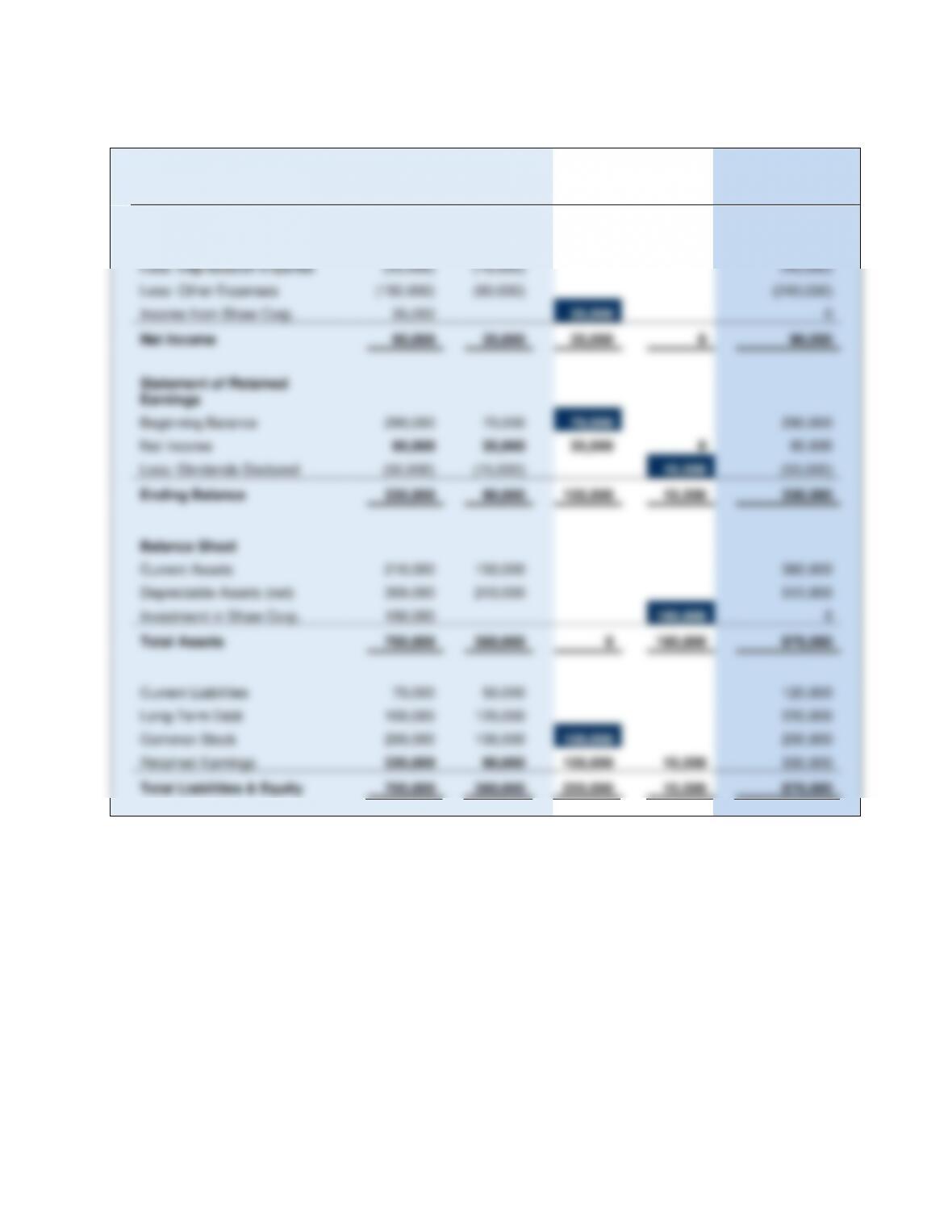

E4-21 (continued)

b.

Blake

Corp.

Shaw

Corp.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

230,000

140,000

370,000

Less: Depreciation Expense

(25,000)

(15,000)

(40,000)

Less: Other Expenses

(150,000)

(90,000)

(240,000)

Income from Shaw Corp.

35,000

35,000

0

Net Income

90,000

35,000

35,000

0

90,000

Statement of Retained

Earnings

Beginning Balance

290,000

70,000

70,000

290,000

Net Income

90,000

35,000

35,000

0

90,000

Less: Dividends Declared

(50,000)

(15,000)

15,000

(50,000)

Ending Balance

330,000

90,000

105,000

15,000

330,000

Balance Sheet

Current Assets

210,000

150,000

360,000

Depreciable Assets (net)

300,000

210,000

510,000

Investment in Shaw Corp.

190,000

190,000

0

Total Assets

700,000

360,000

0

190,000

870,000

Current Liabilities

70,000

50,000

120,000

Long-Term Debt

100,000

120,000

220,000

Common Stock

200,000

100,000

100,000

200,000

Retained Earnings

330,000

90,000

105,000

15,000

330,000

Total Liabilities & Equity

700,000

360,000

205,000

15,000

870,000