Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

E7-16 Intercompany Sale at a Loss

a. Consolidated net income for 20X8 will be greater than Parent Company’s income from

operations plus Sunway’s reported net income. The consolidation entries at December 31,

expense.

E7-17 Consolidation Entries Following Intercompany Sale at a Loss

a.

Consolidation entry, December 31, 20X7:

Buildings and Equipment

156,000

Loss on Sale of Building

36,000

Accumulated Depreciation

120,000

Eliminate unrealized loss on building.

The basic entry (not shown) would be adjusted by 36,000 of deferred

loss on sale of building to complete the elimination process.

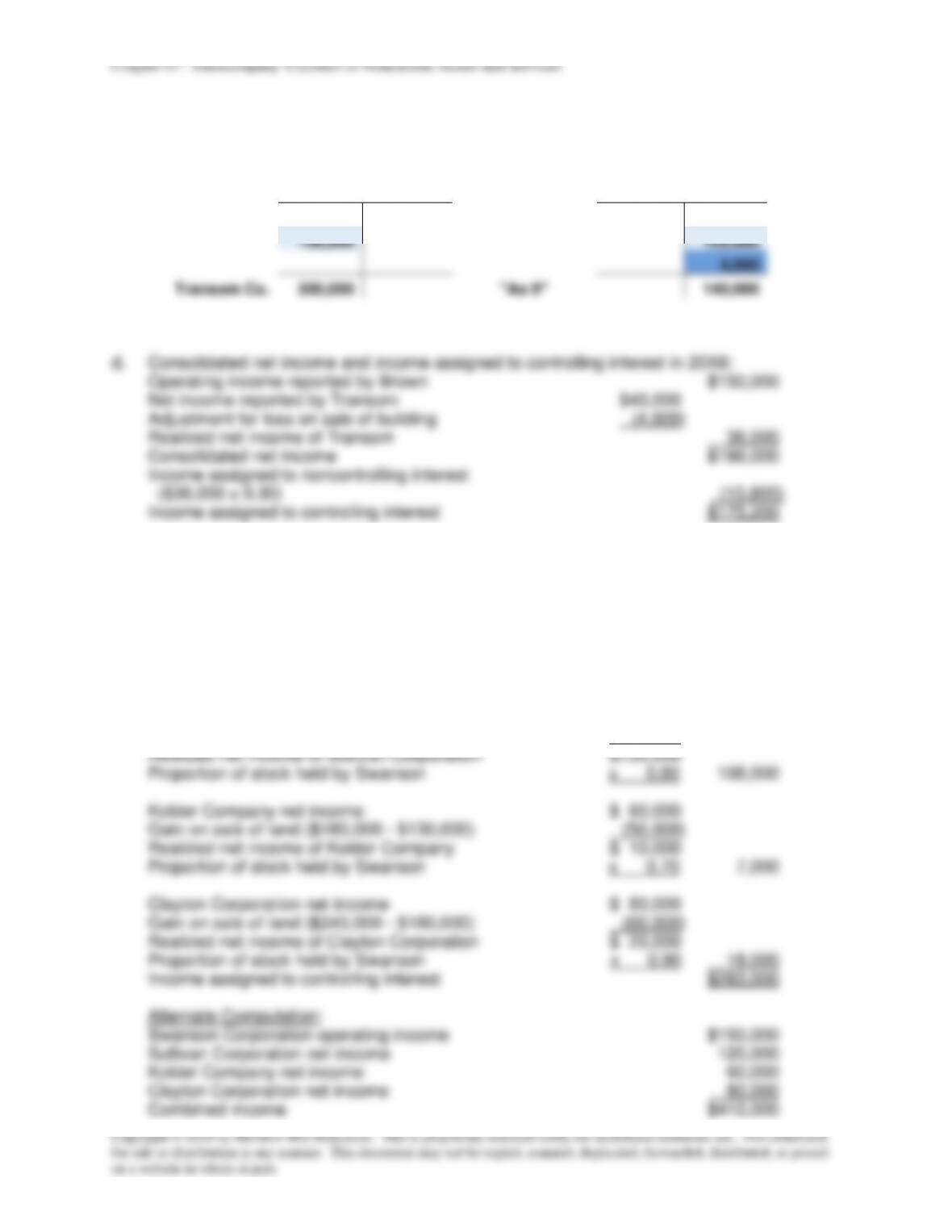

b.

Consolidated net income and income to controlling

interest for 20X7:

Operating income reported by Brown

$125,000

Net income reported by Transom

$ 15,000

Add: Loss on sale of building

36,000

Realized net income of Transom

51,000

Consolidated net income

$176,000

Income to noncontrolling interest ($51,000 x 0.30)

(15,300)

Income to controlling interest

$160,700

c.

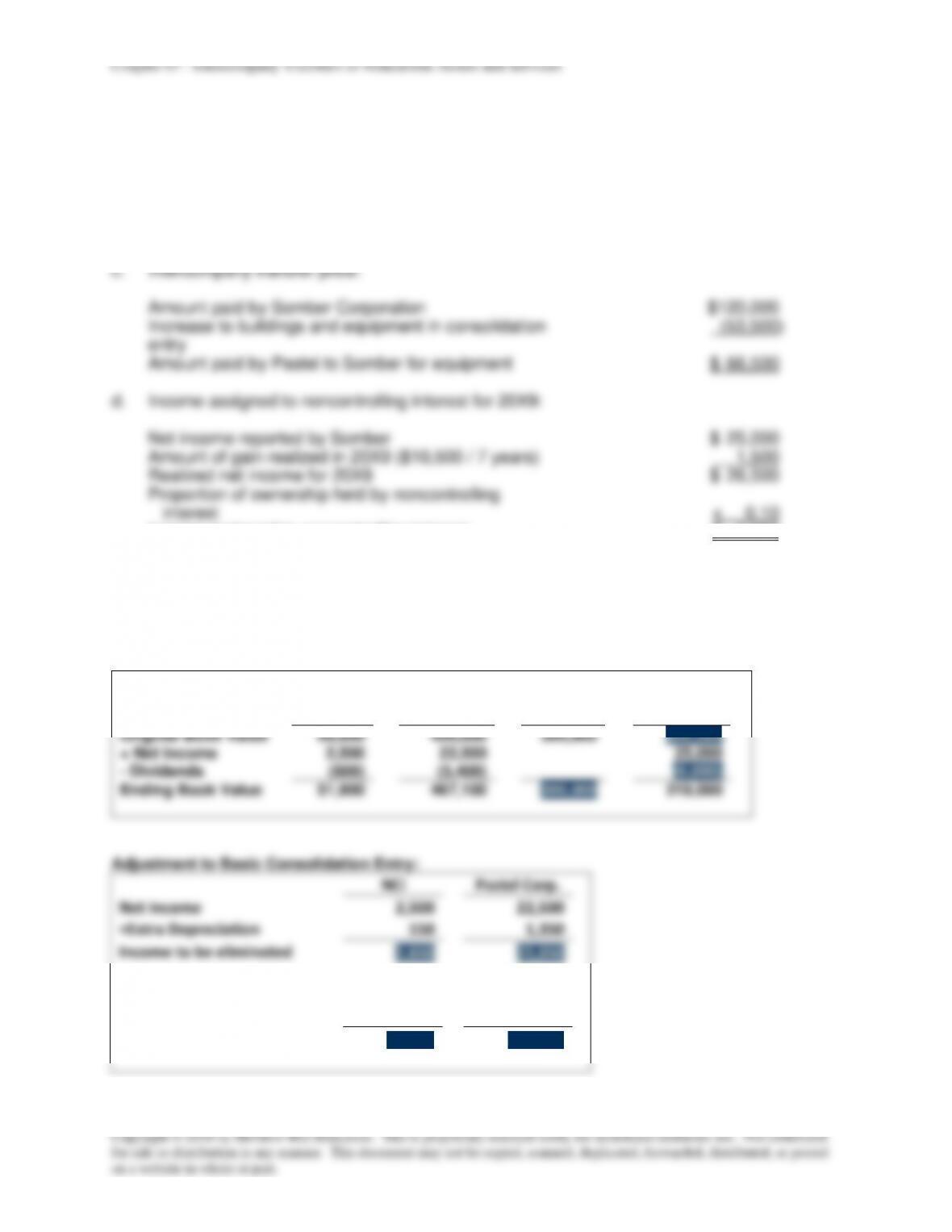

Eliminate the Loss on Building and Correct Asset’s Basis:

Building

156,000

Investment in Transom Co.

25,200

NCI in NA of Transom Co.

10,800

Accumulated Depreciation

120,000

Depreciation Expense

4,000

Accumulated Depreciation

4,000

The basic entry (not shown) would be adjusted by 4,000 to reverse the

loss deferral and complete the elimination process.

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

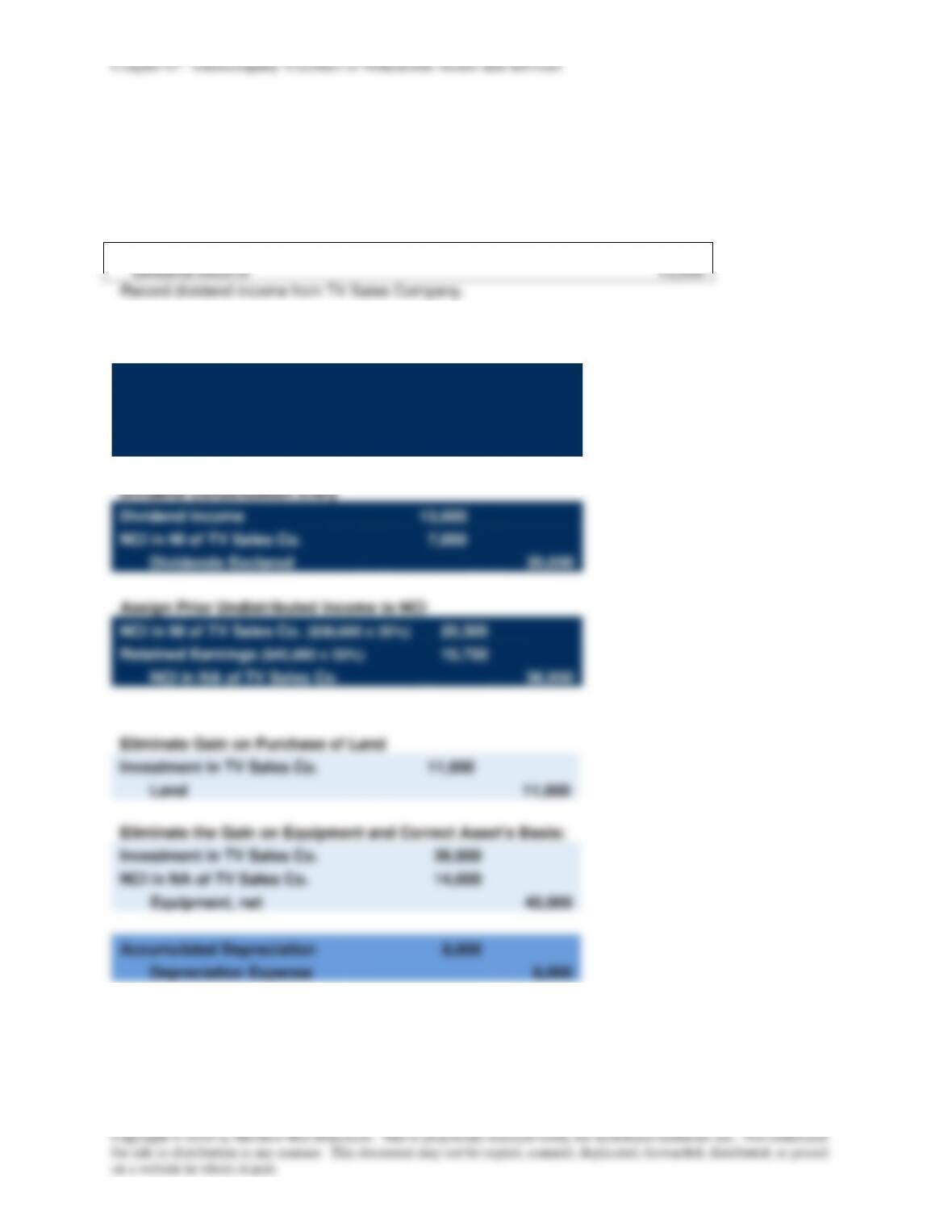

Eliminate Gain on Purchase of Land

Investment in TV Sales Co.

11,000

Land

11,000

Eliminate the Gain on Equipment and Correct Asset’s Basis:

Investment in TV Sales Co.

26,000

NCI in NA of TV Sales Co.

14,000

Equipment, net

40,000

Accumulated Depreciation

8,000

Depreciation Expense

8,000

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

P7-24 Computation of Consolidated Net Income

a.

Separate operating income of Petime Corporation

$34,000

Reported net income of United Grain Company

$19,000

Unrealized profit of sale of land

(7,000)

Realized income for 20X4

$12,000

Amortization of differential ($10,000 / 10 years)

( 1,000)

$11,000

Proportion of ownership held by Petime

x 0.90

Income attributable to controlling interest

9,900

Income to controlling interest

$43,900

b.

Separate operating income of Petime Corporation

$34,000

Reported net income by United Grain Company

$19,000

Amortization of differential ($10,000 / 10 years)

( 1,000)

$18,000

Proportion of stock held by Petime

x 0.90

Income attributable to controlling interest

16,200

Unrealized profit on sale of land

(7,000)

Income to controlling interest

$43,200

Reported income will decrease by $700. In the upstream case the unrealized profit

($7,000) is apportioned to both majority ($6,300) and noncontrolling ($700)

shareholders. In the downstream case, it is apportioned entirely to the majority

shareholders ($7,000).

P7-25 Subsidiary Net Income

a.

Toll Corporation’s reported net income for 20X4 was $94,400:

Income assigned to noncontrolling shareholders

$17,500

Add: Unrealized profit on building ($20,000 x 0.25)

5,000

Amortization of differential ($4,400 x 0.25)

1,100

Income assigned to noncontrolling interest before

adjustment

$23,600

Proportion of stock held by noncontrolling interest

÷ 0.25

Reported income of Toll

$94,400

Computation of annual amortization:

Fair value of consideration given by Bold

$348,000

Fair value of noncontrolling interest

116,000

Total fair value

$464,000

Book value of Toll’s assets:

Common stock

$150,000

Retained earnings

270,000

Total book value

(420,000)

Differential paid by Bold

$ 44,000

Number of years in amortization period

÷ 10

Annual amortization

$4,400