Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

ABC, a holder of a $400,000 XYZ Inc. bond, collected the interest due on June 30,

20X8, and then sold the bond to DEF Inc. for $365,000. On that date the bond issuer,

XYZ, a 90 percent owner of DEF, had a $450,000 carrying amount for this bond.

Based on the information given above, what was the effect of DEF's purchase of XYZ's

bond on the noncontrolling interest amount reported in XYZ's June 30, 20X8,

consolidated balance sheet?

A. No effect

B. $35,000 increase

C. $8,500 decrease

D. $8,500 increase

Parent Corporation purchased land from S1 Corporation for $220,000 on December 26,

20X8. This purchase followed a series of transactions between P-controlled

subsidiaries. On February 15, 20X8, S3 Corporation purchased the land from a

nonaffiliate for $160,000. It sold the land to S2 Company for $145,000 on October 19,

20X8, and S2 sold the land to S1 for $197,000 on November 27, 20X8. Parent has

control of the following companies:

Parent reported income from its separate operations of $200,000 for 20X8.

Based on the preceding information, what amount of gain or loss on sale of land should

be reported in the consolidated income statement for 20X8?

A. $60,000

B. $0

C. $75,000

D. $23,000

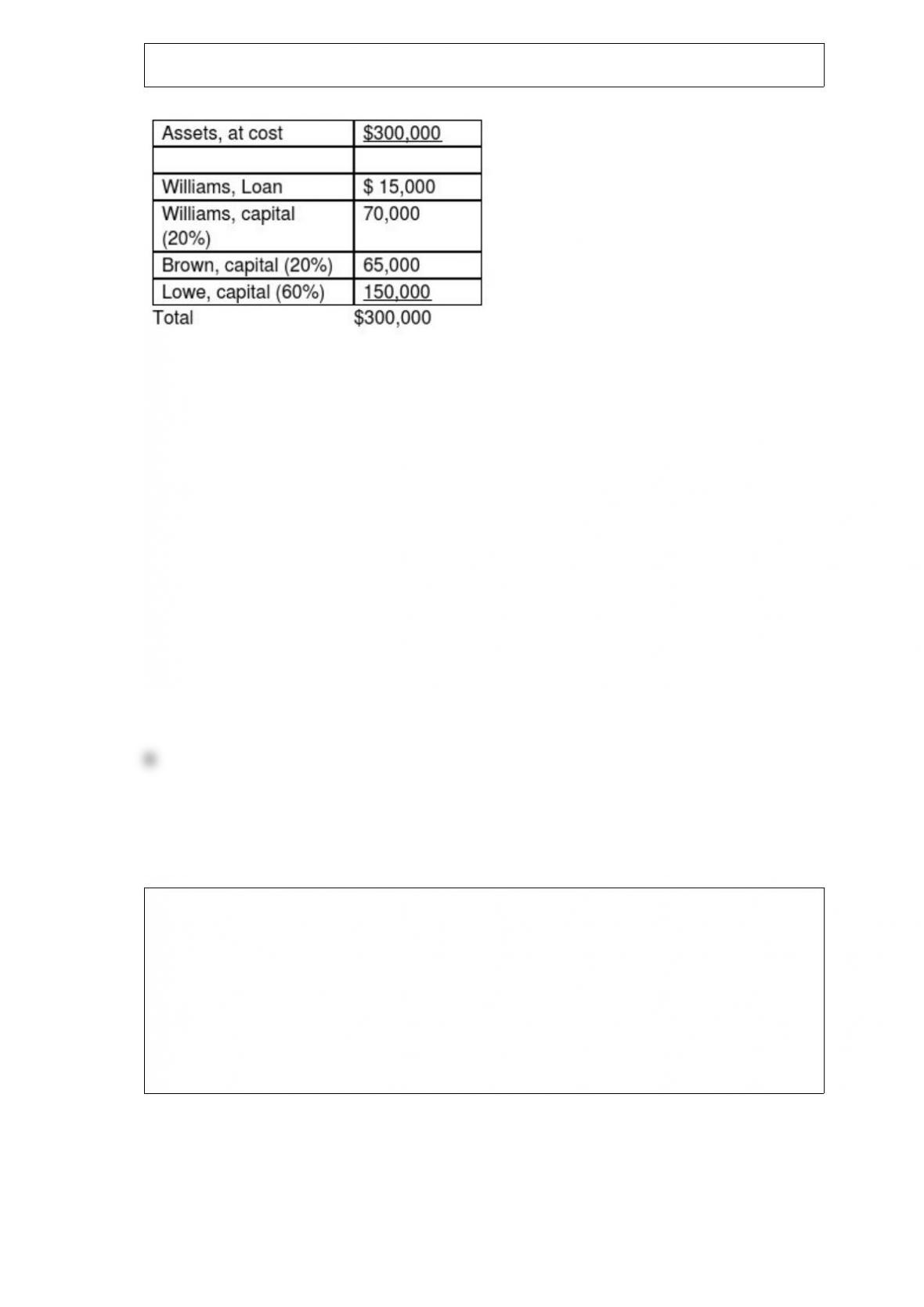

On June 30, the balance sheet for the partnership of Williams, Brown and Lowe,

together with their respective profit and loss ratios, was as follows:

Williams has decided to retire from the partnership and by mutual agreement the assets are

to be adjusted to their fair value of $360,000 at June 30. It was agreed that the partnership

would pay Williams $102,000 cash for his partnership interest exclusive of his loan which

is to be repaid in full. No goodwill is to be recorded in this transaction. After William's

retirement, and before the loan is repaid, what are the capital account balances of Brown

and Lowe, respectively?

A. $65,000 and $150,000

B. $72,000 and $171,000

C. $73,000 and $174,000

D. $77,000 and $186,000

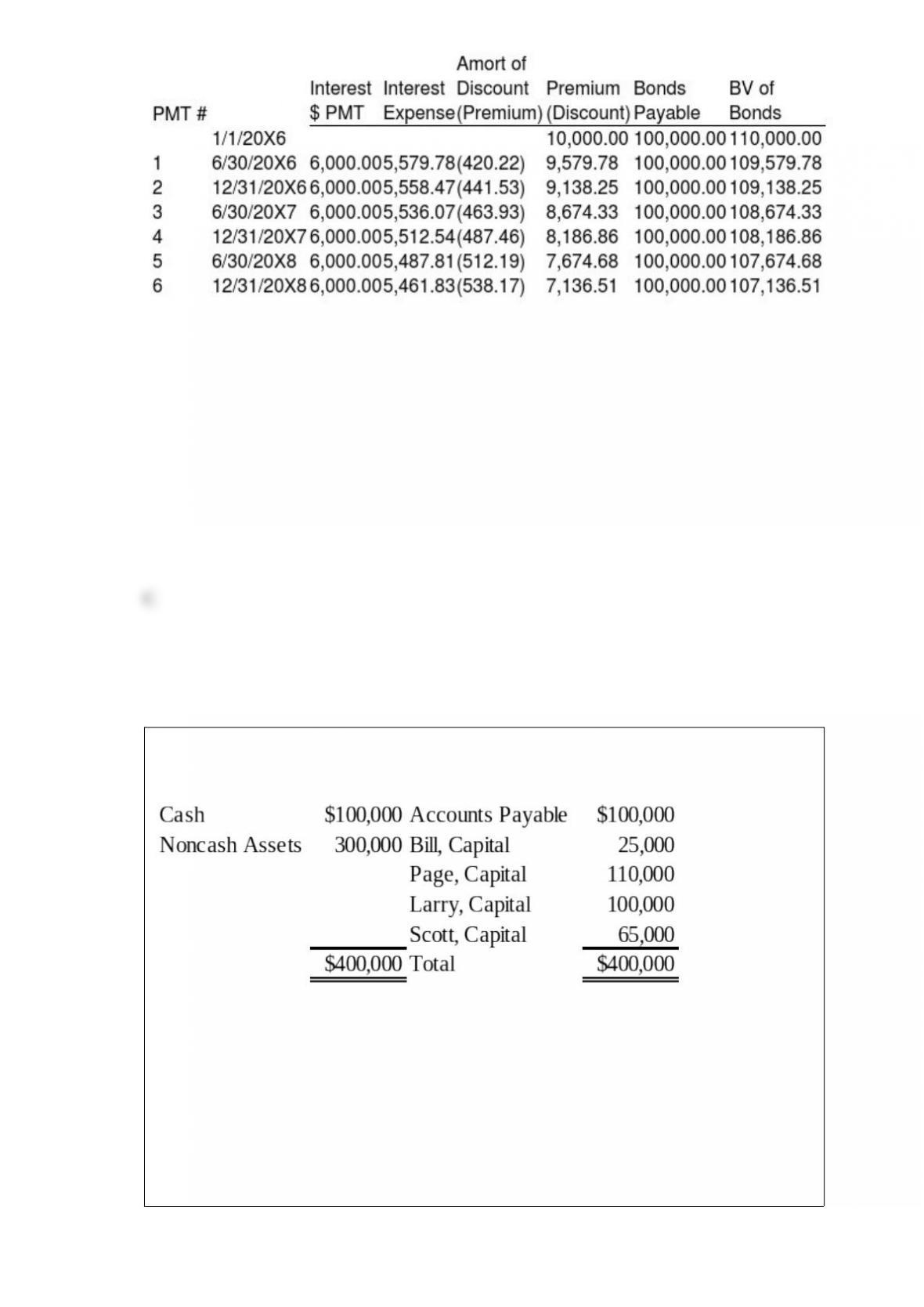

Hunter Corporation holds 80 percent of the voting shares of Moss Company. On

January 1, 20X8, Moss purchased $100,000 par value 12 percent Hunter bonds from

Cruse Corporation for $115,000. Hunter originally issued the bonds to Cruse on January

1, 20X6, for $110,000. The bonds have an 8-year maturity from the date of issue and

pay interest semiannually on June 30 and December 31 each year. Moss' reported net

income of $65,000 for 20X8, and Hunter reported income (excluding income from

ownership of Moss's stock) of $90,000. Hunter’s partial bond amortization schedule is

as follows:

Based on the information given above, what amount of consolidated net income should be

reported for 20X8?

A. $147,240

B. $134,240

C. $149,134

D. $136,134

Bill, Page, Larry, and Scott have decided to terminate their partnership. The

partnership's balance sheet at the time they decide to wind up is as follows:

During the winding up of the partnership, the other assets are sold for $150,000 and the

accounts payable are paid. Page and Larry are personally solvent, but Bill and Scott are

personally insolvent. The partners share profits and losses in the ratio of 3:2:1:4.

Based on the preceding information, what amount will be paid out to Bill upon

liquidation of the partnership?

A. $0

B. $5,000

C. $25,000

D. $2,500

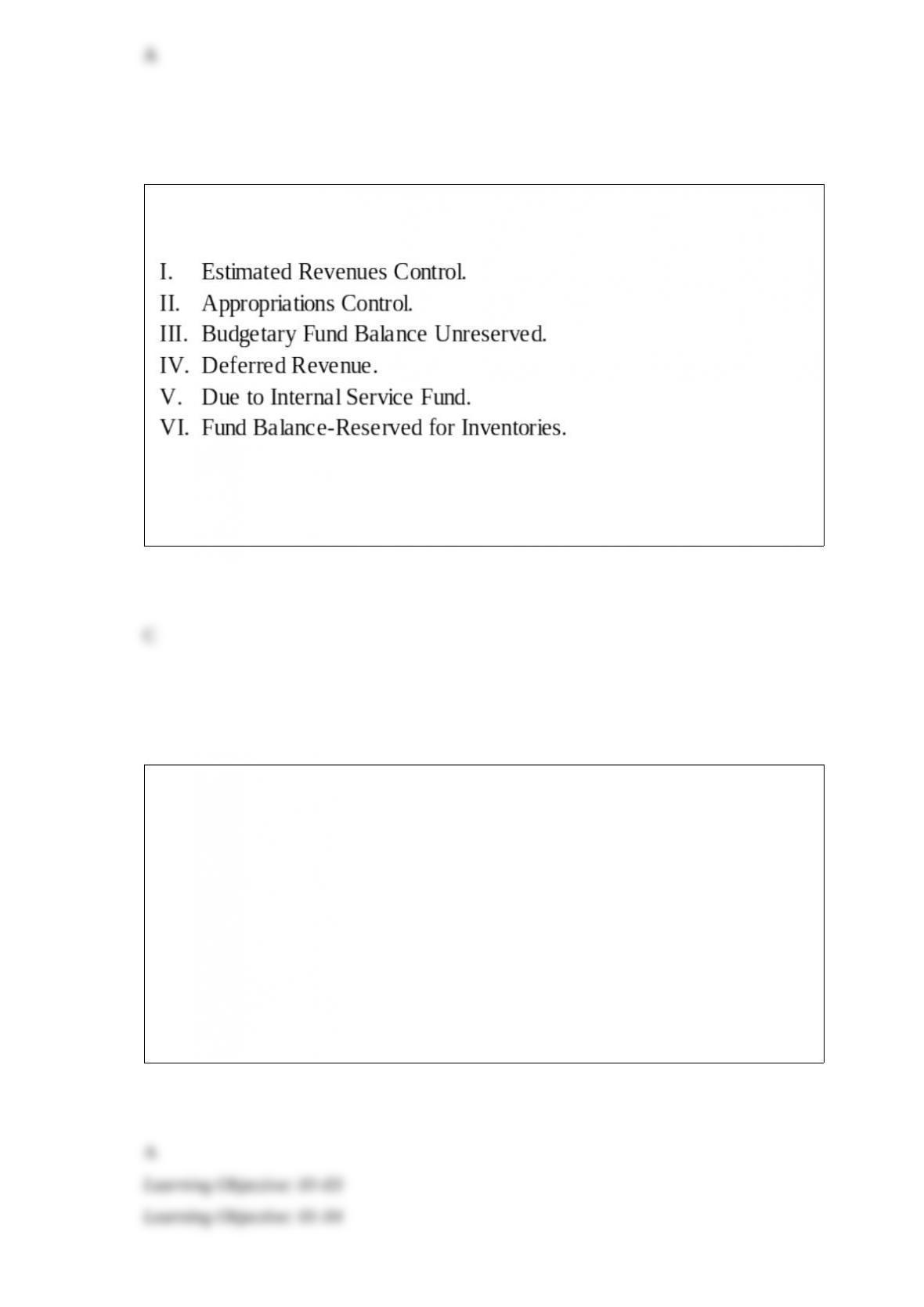

Which accounts described below would have non-zero balances after the accounts are

closed in the general fund of a state or local government?

A. I, II, III.

B. I, II, IV.

C. IV, V, VI.

D. III, IV, V.

At its inception, Peacock Company purchased land for $50,000 and a building for

$220,000. After exactly 4 years, it transferred these assets and cash of $75,000 to a

newly created subsidiary, Selvick Company, in exchange for 25,000 shares of Selvick’s

$5 par value stock. Peacock uses straight-line depreciation. When purchased, the

building had a useful life of 20 years with no expected salvage value. An appraisal at

the time of the transfer revealed that the building has a fair value of $250,000.

Based on the information provided, at the time of the transfer, Selvick Company should

record

A. the building at $220,000 and accumulated depreciation of $44,000.

B. the building at $220,000 with no accumulated depreciation.

C. the building at $176,000 with no accumulated depreciation.

D. the building at $250,000 with no accumulated depreciation.

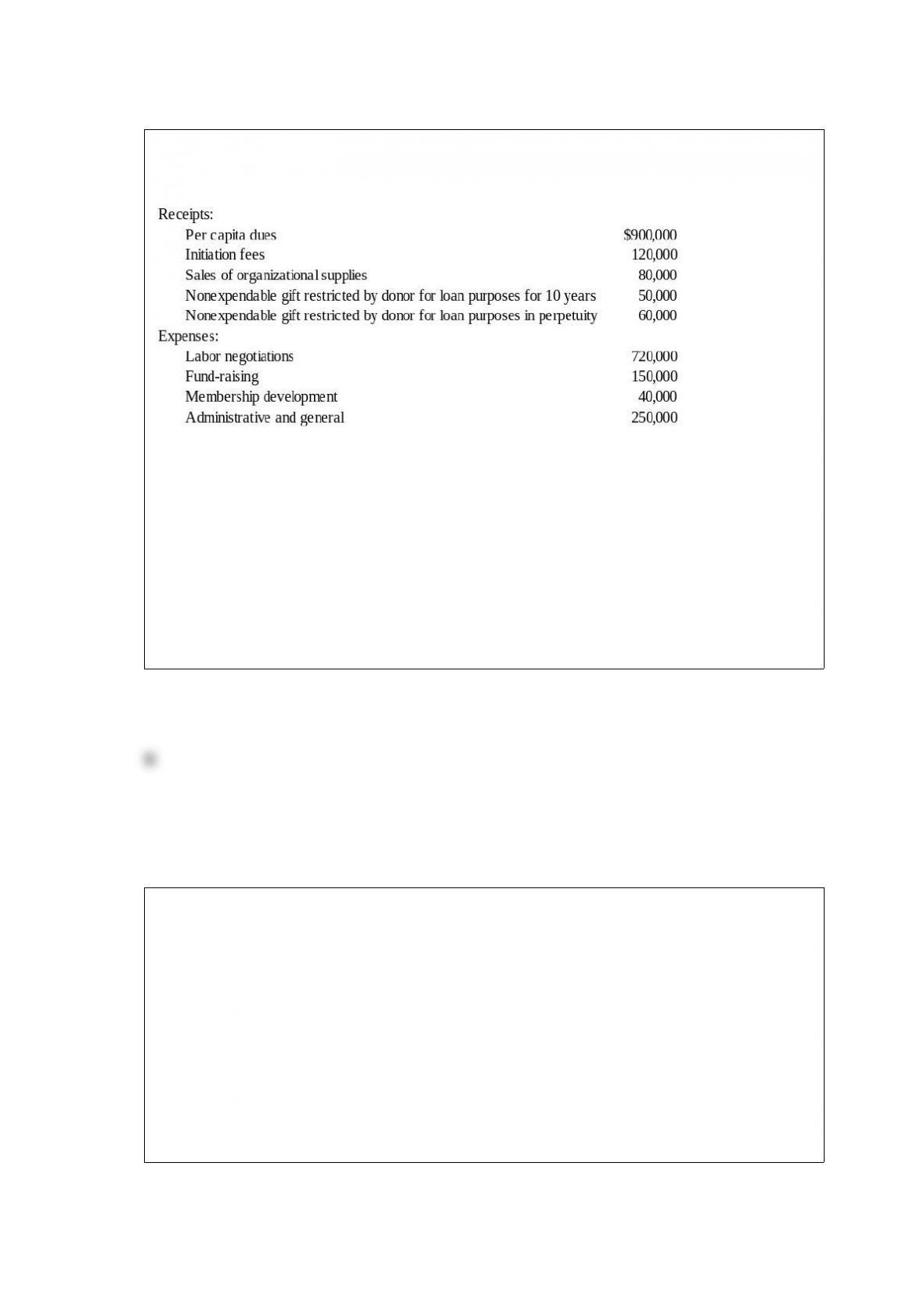

Golden Path, a labor union, had the following receipts and expenses for the year ended

December 31, 20X8:

The union's constitution provides that 12 percent of the per capita dues be designated

for the strike insurance fund to be distributed for strike relief at the discretion of the

union's executive board.

Based on the information provided, in Golden Path's statement of activities for the year

ended December 31, 20X8, what amount should be reported under the classification of

revenue from unrestricted funds?

A. $980,000

B. $1,100,000

C. $1,210,000

D. $1,020,000

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units

from its LIFO-base inventory, which had originally cost $35 per unit. The replacement

cost is expected to be $45 per unit. The company is planning to reduce its inventory and

expects to replace only 1,500 of these units by December 31, the end of its fiscal year.

The company replaced 1,500 units in November at an actual cost of $50 per unit.

Based on the preceding information, in the entry to record the replacement of the 1,500

units in November, Cost of Goods Sold will be debited for:

A. $52,500.

B. $22,500.

C. $15,000.

D. $7,500.

Patch Corporation purchased land from Sub1 Corporation for $350,000 on December 3,

20X5. This purchase followed a series of transactions between Patch-controlled

subsidiaries. On January 23, 20X5, Sub3 Corporation purchased the land from a

nonaffiliate for $240,000. It sold the land to Sub2 Company for $220,000 on July 15,

20X5, and Sub2 sold the land to Sub1 for $305,000 on September 5, 20X5. Patch has

control of the following companies:

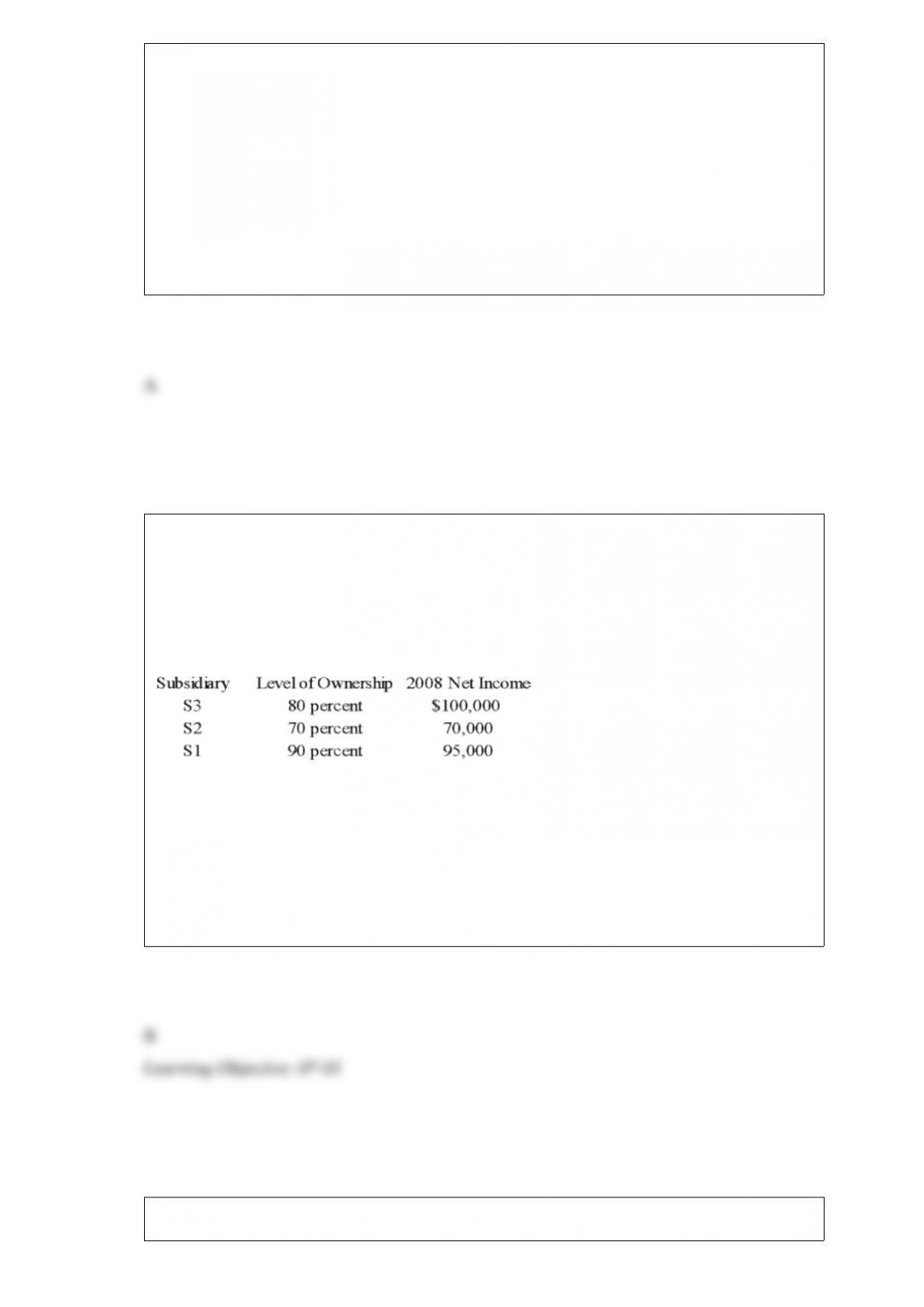

Subsidiary Level of Ownership 20X5 Net Income

Sub3 60 percent $60,000

Sub2 90 percent $140,000

Sub1 70 percent $90,000

Patch reported income from its separate operations of $345,000 for 20X5.

Based on the preceding information, what amount of gain or loss on the sale of land

should be reported in the consolidated income statement for 20X5?

A. $0

B. $20,000 loss

C. $110,000 gain

D. $130,000 gain

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, at what amount should the land be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $135,000

B. $140,000

C. $150,000

D. $155,000

Which of the following funds are classified as fiduciary funds?

A. Agency and Special revenue funds.

B. Internal service and Enterprise funds.

C. Private-purpose trust and Agency funds.

D. Capital projects and Debt service funds.

For which of the following reporting units is the preparation of combined financial

statements most appropriate?

A. A corporation and a foreign subsidiary with nonintegrated homogeneous operations.

B. A corporation and a majority-owned subsidiary with nonhomogeneous operations.

C. Several corporations with related operations owned by one individual.

D. Several corporations with related operations with some common individual owners.

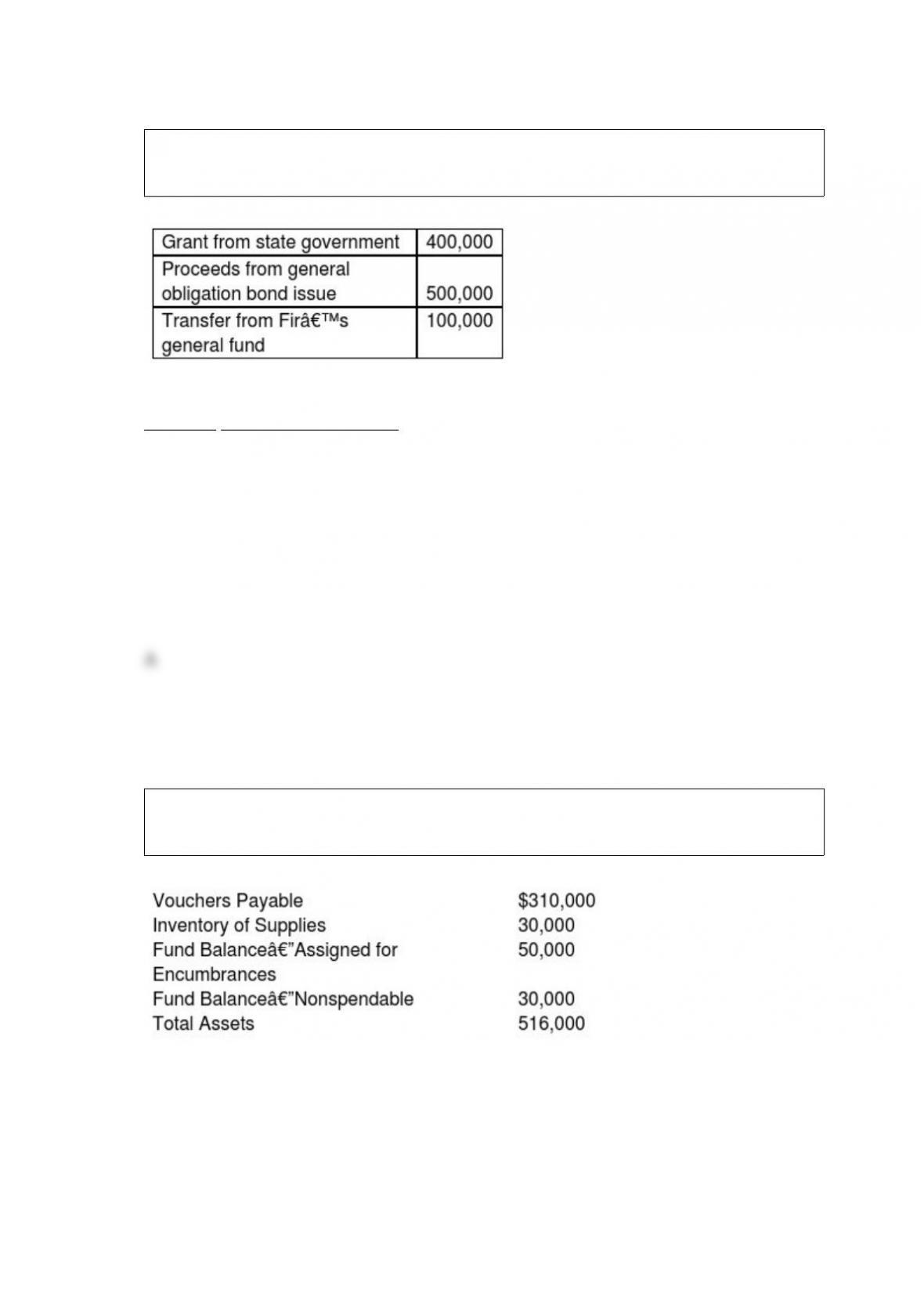

Financing for the renovation of Fir City's municipal park, begun and completed during

20X4, came from the following sources:

In its 20X4 capital projects fund operating statement, Fir should report these amounts as:

Revenues Other financing sources

A. $ 400,000 $ 600,000

B. $ 0 $1,000,000

C. $1,000,000 $ 0

D. $ 900,000 $ 100,000

The following information was obtained from the general fund balance sheet of Lincoln

County on June 30, 20X2, the close of its fiscal year:

On June 30, 20X2, what was Lincoln's unassigned fund balance in its general fund?

A. $96,000

B. $126,000

C. $176,000

D. $206,000

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock

on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for

equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is

expected to have a 10-year useful life and no salvage value. Both companies depreciate

equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X8 consolidated

financial statements, equipment will be:

A. debited for $50,000.

B. debited for $40,000.

C. credited for $70,000.

D. debited for $25,000.

The statement of financial position for a private not-for-profit college should show

separate dollar amounts for

A. Unrestricted net assets, temporarily restricted net assets, and permanently restricted

net assets.

B. All accounts in its equity section.

C. Unrestricted net assets only.

D. Unrestricted net assets and temporarily restricted net assets.

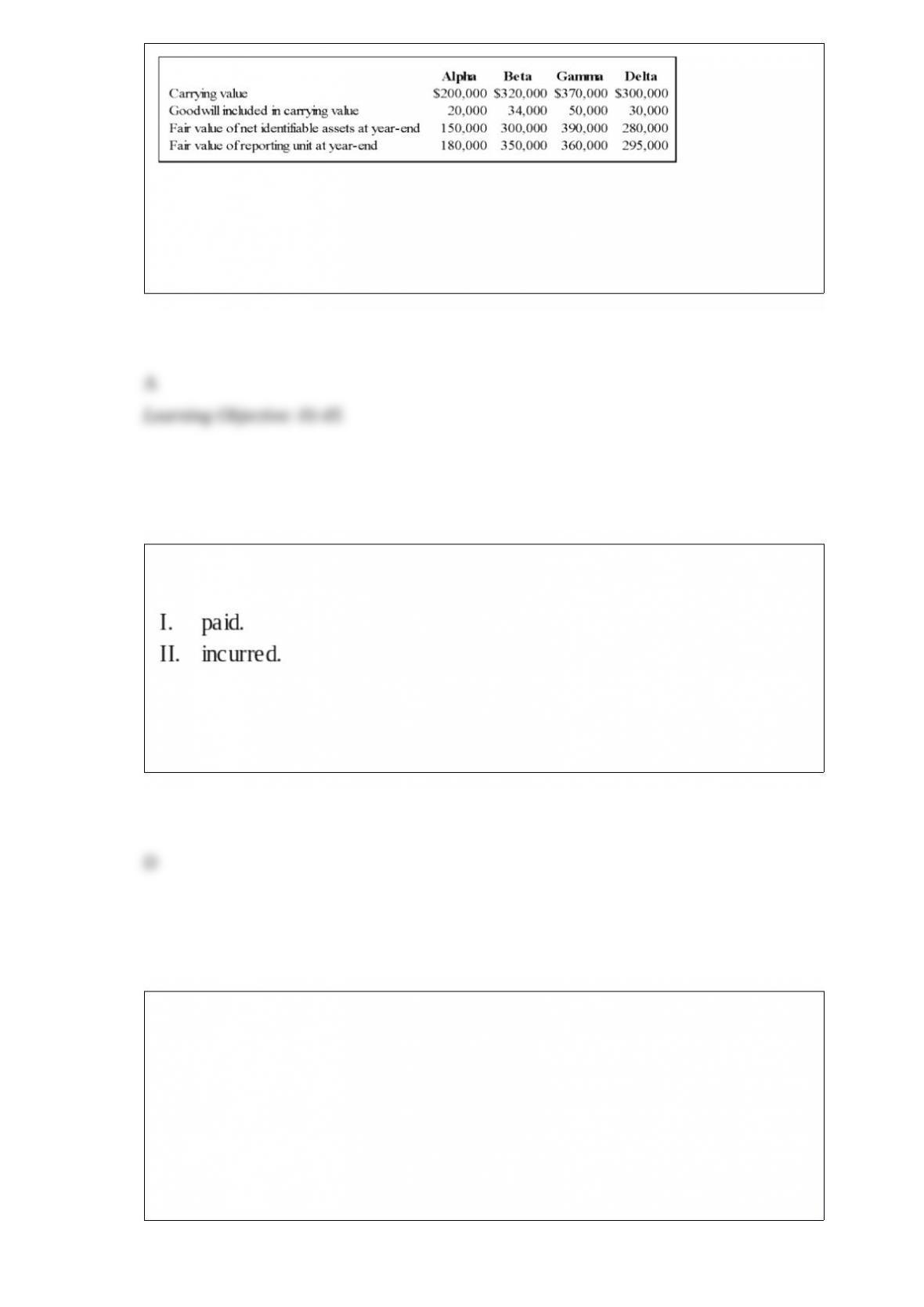

Pursuing an inorganic growth strategy, Wilson Company acquired Venus Company's net

assets and assigned them to four separate reporting divisions. Wilson assigned total

goodwill of $134,000 to the four reporting divisions as given below:

Based on the preceding information, for Gamma:

A. no goodwill should be reported at year-end.

B. goodwill impairment of $30,000 should be recognized at year-end.

C. goodwill impairment of $20,000 should be recognized at year-end.

D. goodwill of $30,000 should be reported at year-end.

Under the modified accrual basis of accounting for the general fund, expenditures

should be recognized in the period in which the related liability is:

A. I only

B. II only

C. Both I and II

D. Neither I nor II

As of May 30, 20X9, the debt service fund of Cody had accumulated $52,000 of assets

in a debt service fund to pay the principal of its currently maturing serial bonds. On

June 1, 20X9, $50,000 of serial bonds matured and were paid with the resources

accumulated in the debt service fund. In Cody's debt service fund, Matured Bonds

Payable was debited for $50,000 and:

A. Cash was credited for $50,000.

B. Due to General Fund was credited for $50,000.

C. Investments was credited for $50,000.

D. Reserve for Encumbrances was credited for $50,000.

A newly created subsidiary sold all of its inventory to its parent at a profit in its first

year of existence. The parent, in turn, sold all but 20 percent of the inventory to

unaffiliated companies, recognizing a profit. The parent had no other sales during the

year. The amount that should be reported as cost of goods sold in this year’s

consolidated income statement should be:

A. 80 percent of the amount reported as intercompany sales by the subsidiary.

B. 80 percent of the amount reported as cost of goods sold by the subsidiary.

C. the amount reported as cost of goods sold by the parent minus unrealized profit in

the ending inventory of the parent.

D. 80 percent of the amount reported as cost of goods sold by the parent.

Patch Corporation purchased land from Sub1 Corporation for $350,000 on December 3,

20X5. This purchase followed a series of transactions between Patch-controlled

subsidiaries. On January 23, 20X5, Sub3 Corporation purchased the land from a

nonaffiliate for $240,000. It sold the land to Sub2 Company for $220,000 on July 15,

20X5, and Sub2 sold the land to Sub1 for $305,000 on September 5, 20X5. Patch has

control of the following companies:

Subsidiary Level of Ownership 20X5 Net Income

Sub3 60 percent $60,000

Sub2 90 percent $140,000

Sub1 70 percent $90,000

Patch reported income from its separate operations of $345,000 for 20X5.

Based on the preceding information, at what amount should the land be reported in the

consolidated balance sheet as of December 31, 20X5?

A. $220,000

B. $240,000

C. $305,000

D. $350,000

Plummet Corporation reported the book value of its net assets at $400,000 when Zenith

Corporation acquired 100 percent ownership. The fair value of Plummet's net assets

was determined to be $510,000 on that date.

Based on the preceding information, what amount of goodwill will be reported in

consolidated financial statements presented immediately following the combination if

Zenith paid $500,000 for the acquisition?

A. $0

B. $50,000

C. $150,000

D. $40,000

On September 30, 20X8, Wilfred Company sold inventory to Jackson Corporation, its

Canadian subsidiary. The goods cost Wilfred $30,000 and were sold to Jackson for

$40,000, payable in Canadian dollars. The goods are still on hand at the end of the year

on December 31. The Canadian dollar (C$) is the functional currency of the Canadian

subsidiary. The exchange rates follow:

Based on the preceding information, at what amount is the inventory shown on the

consolidated balance sheet for the year?

A. $45,000

B. $30,000

C. $40,000

D. $35,000

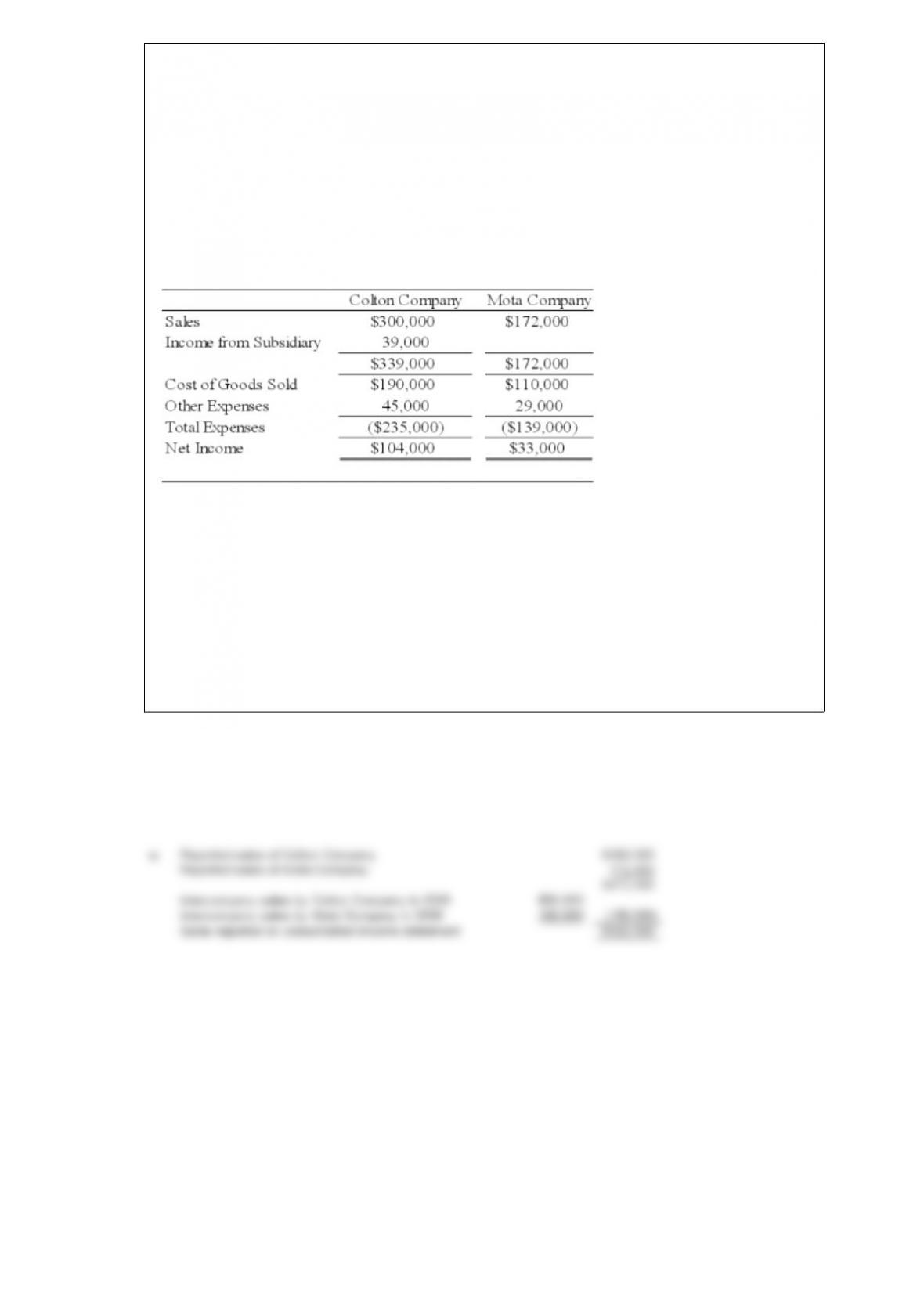

Colton Company acquired 80 percent ownership of Mota Company's voting shares on

January 1, 2008, at underlying book value. The fair value of the noncontrolling interest

on that date was equal to 20 percent of the book value of Mota Company. During 2008,

Colton purchased inventory for $30,000 and sold the full amount to Mota Company for

$50,000. On December 31, 2008, Mota's ending inventory included $10,000 of items

purchased from Colton. Also in 2008, Mota purchased inventory for $80,000 and sold

the units to Colton for $100,000. Colton included $30,000 of its purchase from Mota in

ending inventory on December 31, 2008. Summary income statement data for the two

companies revealed the following:

Required:

a. Compute the amount to be reported as sales in the 20X8 consolidated income

statement.

b. Compute the amount to be reported as cost of goods sold in the 20X8 consolidated

income statement.

c. What amount of income will be assigned to the noncontrolling shareholders in the

20X8 consolidated income statement?

d. What amount of income will be assigned to the controlling interest in the 20X8

consolidated income statement?

On December 31, 20X5, Paris Corporation acquired 60 percent of Sanlo Company’s

common stock for $180,000. At that date, the fair value of the noncontrolling interest

was $120,000. Of the $45,000 differential, $5,000 related to the increased value of

Sanlo’s inventory, $15,000 related to the increased value of its land, and $10,000 related

to the increased value of its equipment that had a remaining life of five years from the

date of combination. Sanlo sold all inventory it held at the end of 20X5 during 20X6.

The land to which the differential related was also sold during 20X6 for a large gain. In

20X6, Sanlo reported net income of $40,000 but paid no dividends. Paris accounts for

its investment in Sanlo using the equity method.

Based on the preceding information, the amount of goodwill reported in the

consolidated financial statements prepared immediately after the combination is

A. $9,000

B. $15,000

C. $27,000

D. $45,000

Under which nonjudicial action do creditors agree to assist the debtor in managing the

most efficient payment of creditors' claims?

A. Debt restructuring arrangement

B. Creditors' committee management

C. Transfer of assets

D. Composition agreement

Tinitoys, Inc., a domestic company, purchased inventory from a Brazilian company for

500,000 Brazilian reals (Br. reals) on May 1, 20X2. Payment is due on June 30, 20X2.

On May 1, 20X2, Tinitoys also entered into a 60-day forward contract to purchase

500,000 Brazilian reals. The forward contract is not designated as a hedge. Tinitoys’

fiscal year ends on May 31. The direct exchange rates were as follows:

Spot Rate Forward Rate

May 1, 20X2 $0.523 $0.525 (60 days)

May 31, 20X2 $0.516 $0.52 (30 days)

June 30, 20X2 $0.508

Based on the preceding information, the entries on May 31, 20X2, include a

A. credit to Foreign Currency Payable to Exchange Broker, $3,500.

B. debit to Foreign Currency Transaction Loss, $3,500.

C. credit to Foreign Currency Receivable from Exchange Broker, $2,500.

D. credit to Foreign Currency Receivable from Exchange Broker, $260,000.

Which of the following observations is true of the shelf registration rule?

A. It is an option available to all listed companies.

B. Shelf registration is limited to 25 percent of the company's currently outstanding

stock.

C. It allows private placements of an unlimited amount of securities.

D. It allows large companies to select the optimal time to sell their stock.

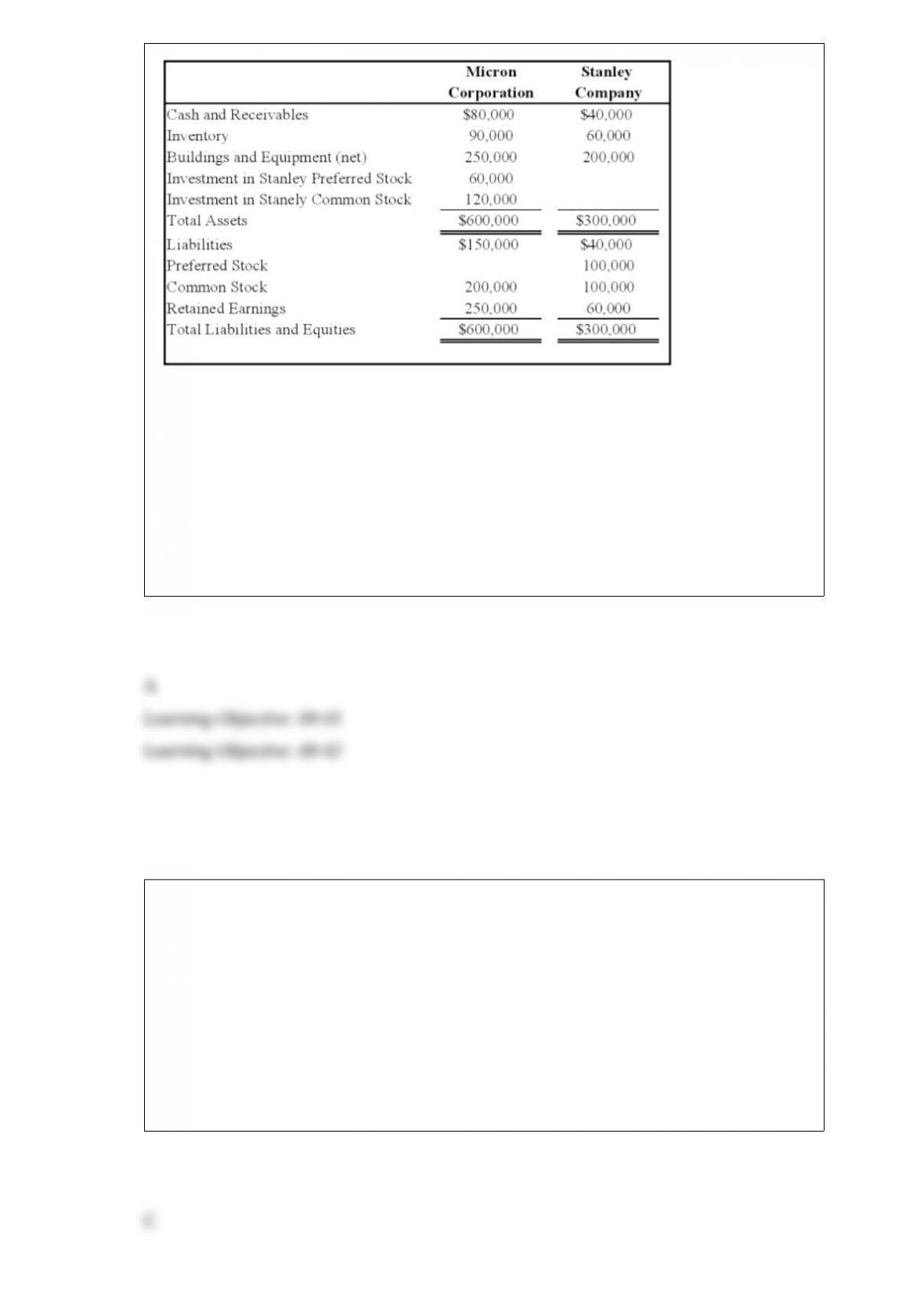

Micron Corporation owns 75 percent of the common shares and 60 percent of the

preferred shares of Stanley Company, all acquired at underlying book value on January

1, 20X8. At that date, the fair value of the noncontrolling interest in Stanley's common

stock was equal to 25 percent of the book value of its common stock. The balance

sheets of Micron and Stanley immediately after the acquisition contained these

balances:

Stanley's preferred stock pays a 12 percent dividend and is cumulative. For 20X8,

Stanley reports net income of $40,000 and pays no dividends. Micron reports income

from its separate operations of $75,000 and pays dividends of $30,000 during 20X8.

Based on the preceding information, what is the total noncontrolling interest reported in

the consolidated balance sheet as of January 1, 20X8?

A. $80,000

B. $40,000

C. $50,000

D. $60,000

On September 22, 20X1, Yumi Corp. purchased merchandise from an unaffiliated

foreign company for 10,000 units of the foreign company's local currency. On that date,

the spot rate was $.55. Yumi paid the bill in full, six months later, on March 20, 20X2,

when the spot rate was $.65. The spot rate was $.70 on December 31, 20X1. What

amount should Yumi report as a foreign currency transaction loss in its income

statement for the year ended December 31, 20X1?

A. $500

B. $0

C. $1,500

D. $1,000

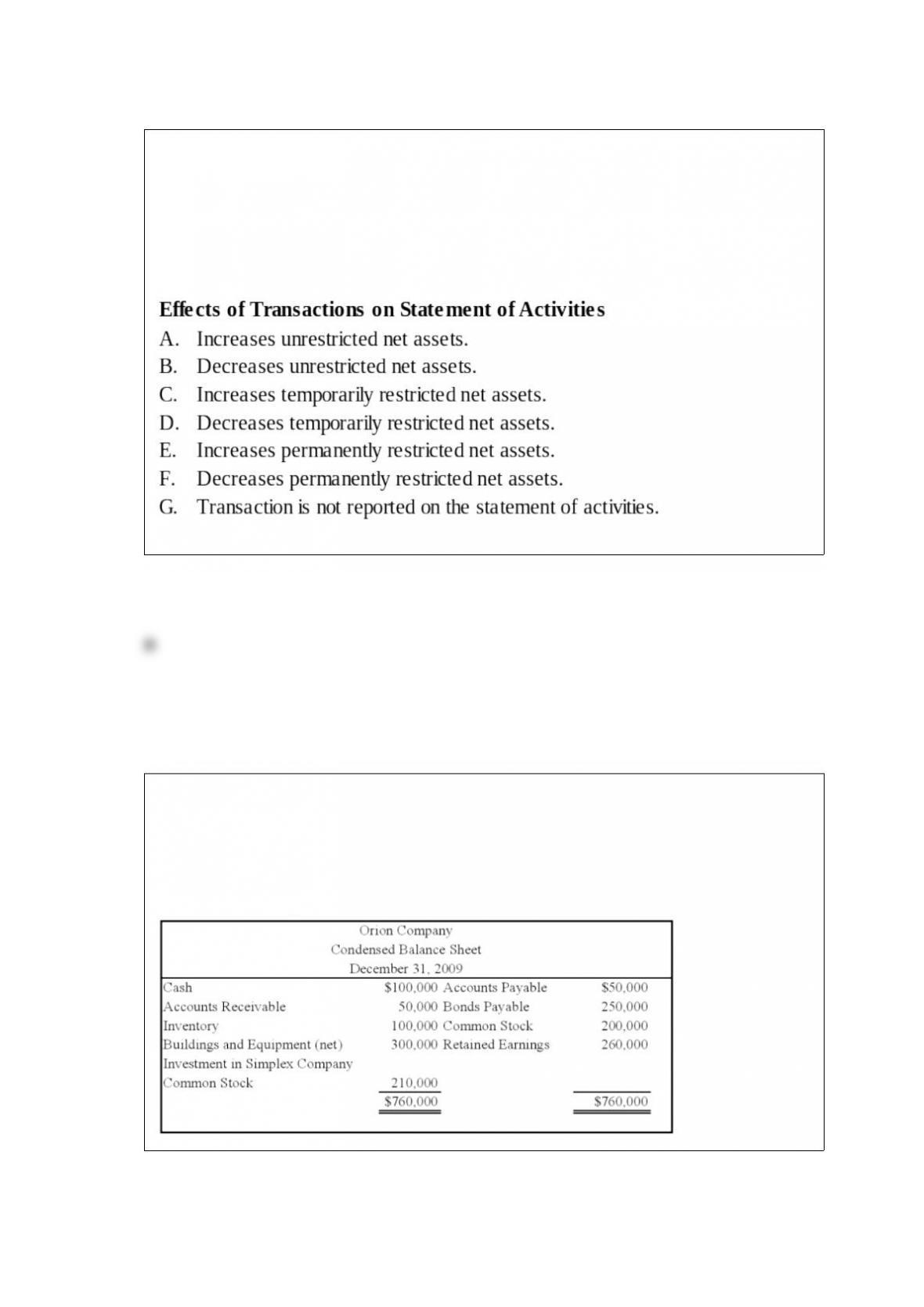

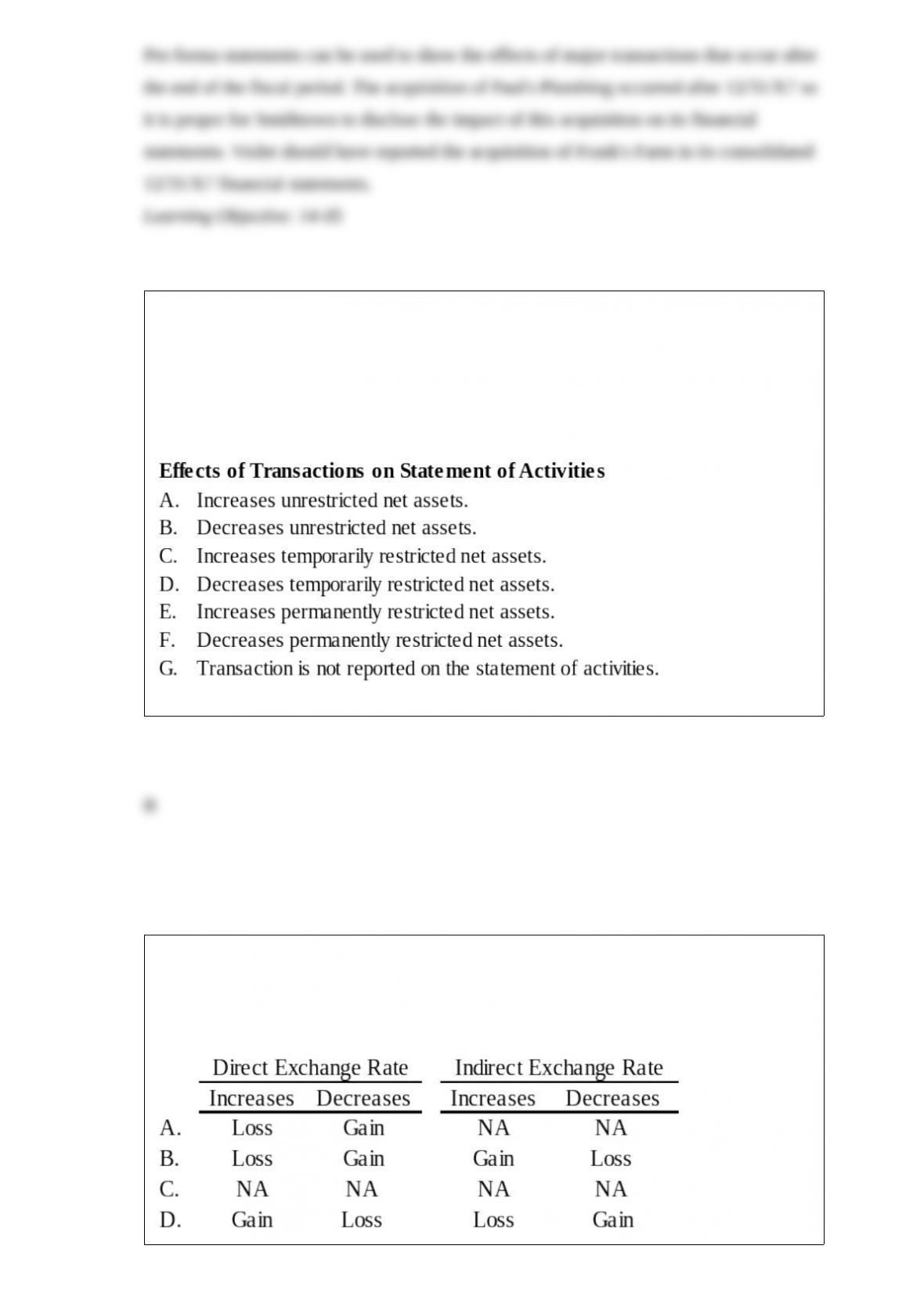

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization's statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Incurred fund-raising costs.

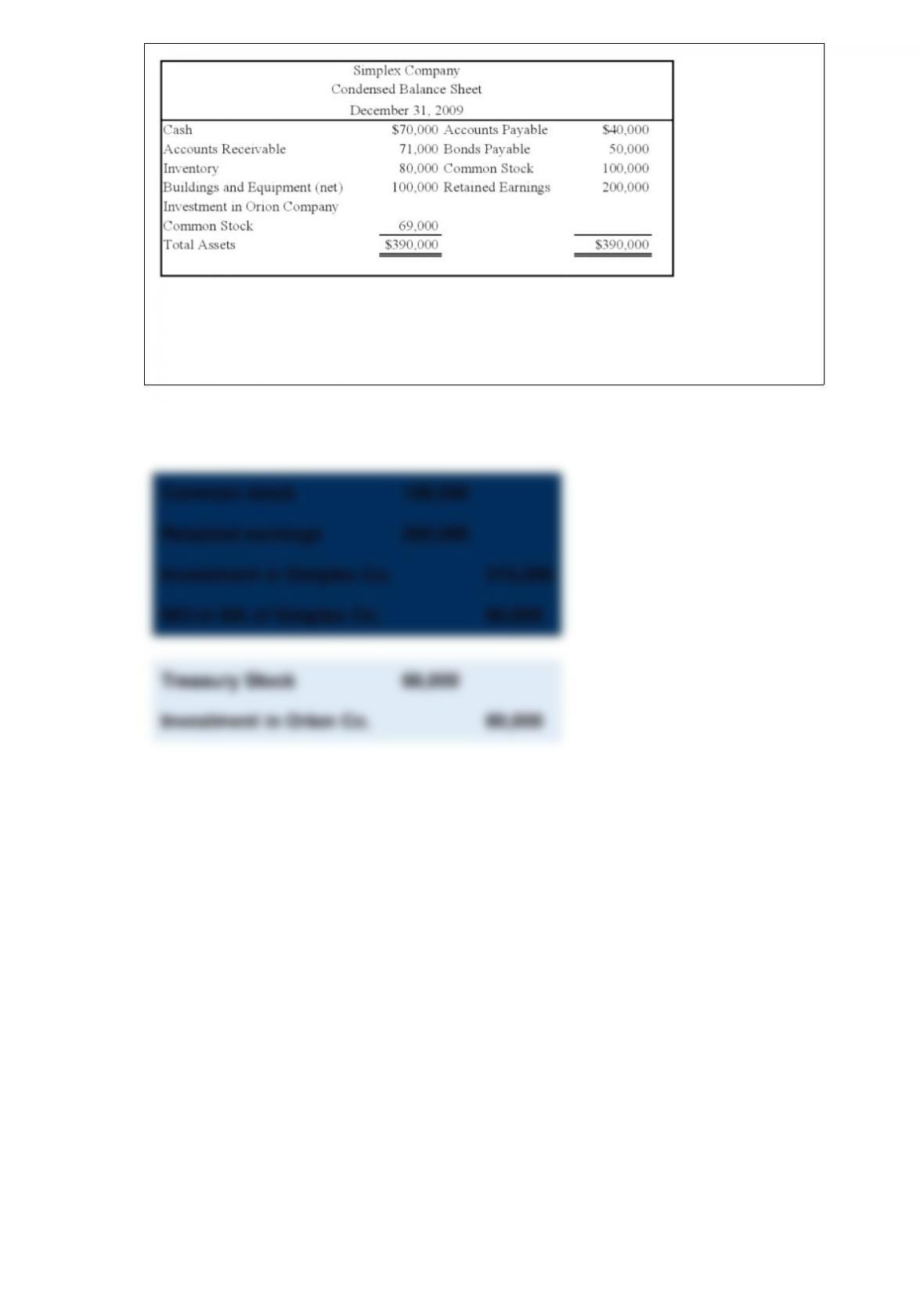

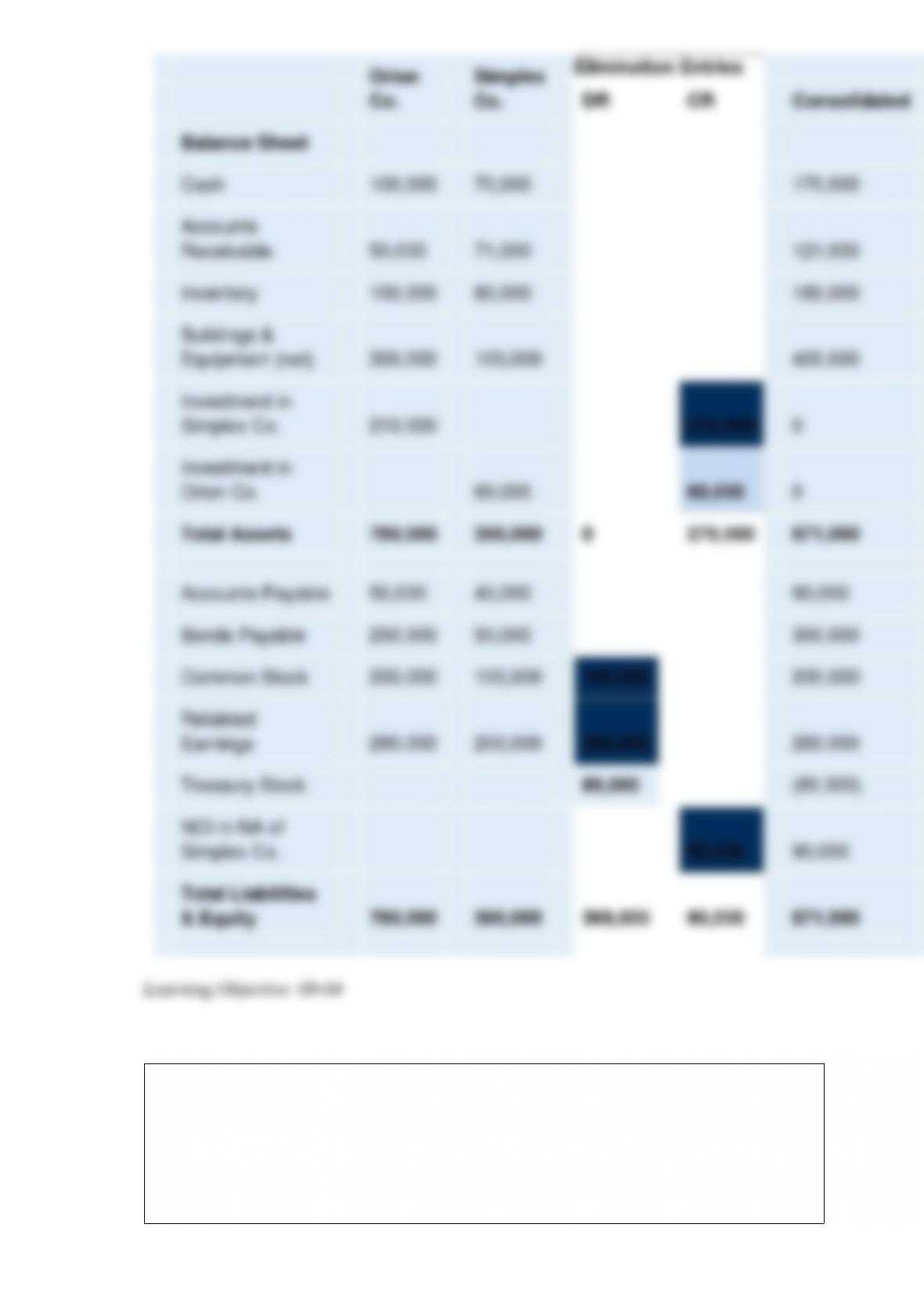

On January 1, 2008, Orion Company acquired 70 percent of Simplex Company's stock

at underlying book value. At that date, the fair value of the noncontrolling interest was

equal to 30 percent of the book value of Simplex Company. On December 31, 2009,

Simplex acquired 15 percent of Orion's stock. Balance sheets for the two companies on

December 31, 2009, are as follows:

Required:

Assuming that the treasury stock method is used in reporting Orion's shares held by

Simplex, prepare the elimination entries and a consolidated balance sheet worksheet for

December 31, 2009.

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization's statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Received a multi-year pledge, with cash being received this year and for the next 4

years. Donors did not place any use restrictions on how the pledges were to be spent.

Listen and Hear are thinking of dissolving their partnership. Listen has a friend who

told him to complete a “lump-sum” liquidation. Hear wants to complete an

“installment” liquidation. They have come to you for advice. What do you recommend

and Why?

Heavy Company sold metal scrap to a Brazilian company for 200,000 Brazilian reals on

December 1, 20X8, with payment due on January 20, 20X9. The exchange rates were:

December 1, 20X8 1 real = $0.5435

December 31, 20X8 1 real = 0.5192

January 20, 20X9 1 real = 0.5305

Based on the preceding information, which of the following is true of dollar's

movement vis--vis Brazilian real during the period?

A cash dividend returns assets to the stockholders while reducing corporate liquidity.

Why are not all cash dividends considered to be "liquidating dividends"? In your

response include a discussion of how an investor accounts for a liquidating dividend.

Big Company acquired 75 percent of Little Company's stock at underlying book value

on January 1, 20X8. At that date, the fair value of the noncontrolling interest was equal

to 25 percent of the book value of Little Company. Little Company reported shares

outstanding of $350,000 and retained earnings of $100,000. During 20X8, Little

Company reported net income of $60,000 and paid dividends of $3,000. In 20X9, Little

Company reported net income of $90,000 and paid dividends of $15,000. The following

transactions occurred between Big Company and Little Company in 20X8 and 20X9:

Little Co. sold equipment to Big Co. for a $42,000 gain on December 31, 20X8. Little

Co. had originally purchased the equipment for $140,000 and it had a carrying value of

$28,000 on December 31, 20X8. At the time of the purchase, Big Co. estimated that the

equipment still had a seven-year remaining useful life.

Big sold land costing $90,000 to Old Company on June 28, 20X9, for $110,000.

Required:

Give all consolidating entries needed to prepare a consolidation worksheet for 20X9

assuming that Big Co. uses the modified equity method to account for its investment in

Old Company.

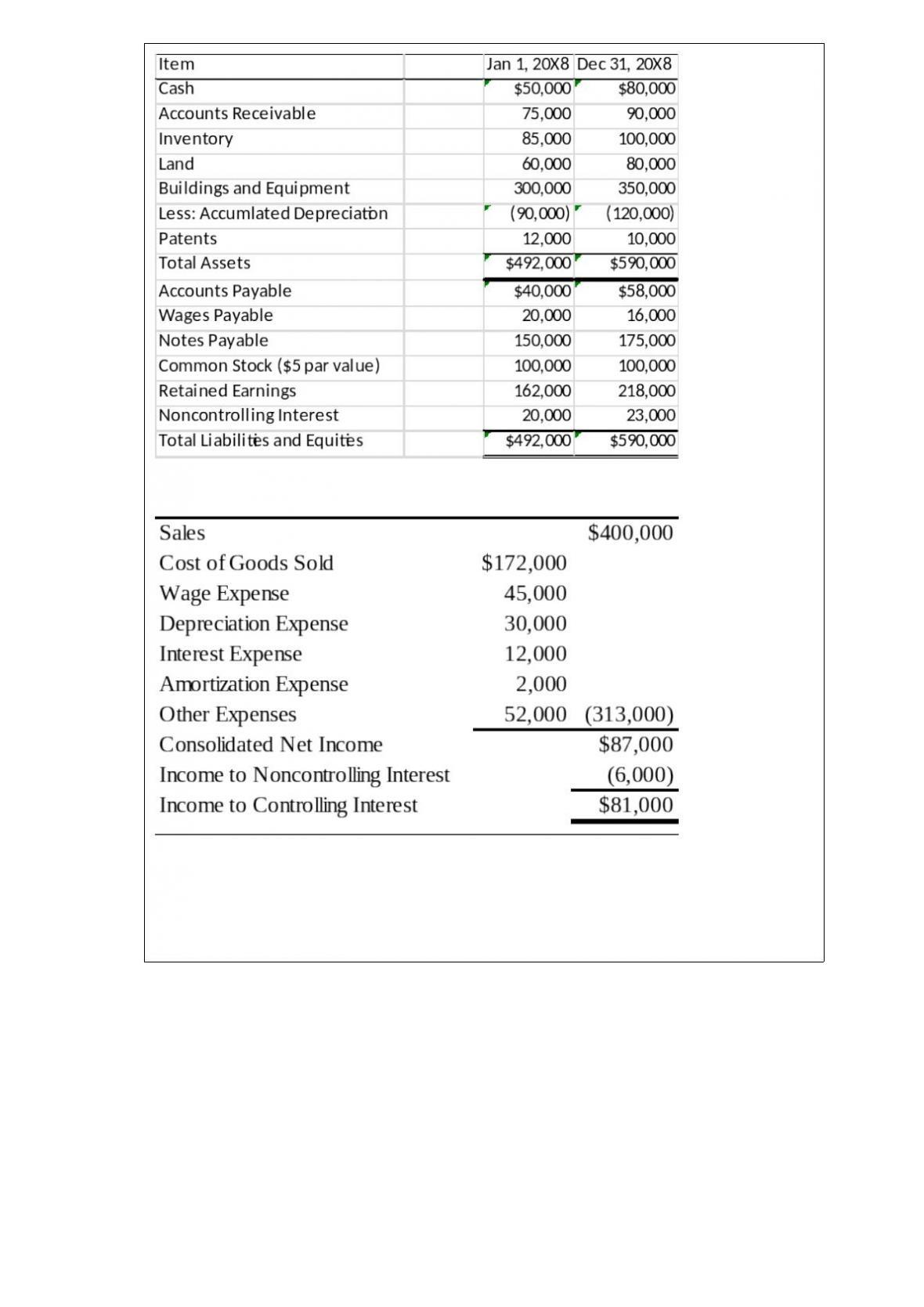

Locus Corporation acquired 80 percent ownership of Stereo Company on January 1,

20X6, at underlying book value. At that date, the fair value of the noncontrolling

interest was equal to 20 percent of the book value of Stereo Company. Consolidated

balance sheets at January 1, 20X8, and December 31, 20X8, are as follows:

The consolidated income statement for 20X8 contained the following amounts:

Locus and Stereo paid dividends of $25,000 and $15,000, respectively, in 20X8.

Required:

1) Prepare a worksheet to develop a consolidated statement of cash flows for 20X8

using the direct method of computing cash flows from operations.

2) Prepare a consolidated statement of cash flows for 20X8.

PeopleMag sells a plot of land for $100,000 to Seven Star Company, its 100 percent

owned subsidiary, on January 1, 20X7. The cost of the land was $75,000, when it was

purchased in 20X6. In 20X9, Seven Star sells the land to Hot Properties Inc., an

unrelated entity, for $120,000. How is the land reported in the consolidated financial

statements for 20X7, 20X8 and 20X9?

The PQ partnership has the following plan for the distribution of partnership net income

(loss):

Required:

Calculate the distribution of partnership net income (loss) for each independent

situation below (for each situation, assume the average capital balance of P is $140,000

and of Q is $240,000).

1) Partnership net income is $360,000.

2) Partnership net income is $240,000.

3) Partnership net loss is $40,000.

On December 1, 20X8, Secure Company bought a 90-day forward contract to purchase

200,000 euros (€) at a forward rate of €1 = $1.35 when the spot rate was $1.33. Other

exchange rates were as follows:

Required

1) Prepare all journal entries related to Secure Company's foreign currency speculation

from December 1, 20X8, through March 1, 20X9, assuming the fiscal year ends on

December 31, 20X8.

2) Did the company gain or lose on its purchase of the forward contract?

Smithtown Distributors acquired Paul's Plumbing on January 15, 20X8. Violet Flowers

acquired Frank's Farm on January 1, 20X7. In the 12/31/X7 financial statements filed

with the SEC, Smithtown included a Pro Forma disclosure and Violet did not. If both

acquisitions account for 100% of the common stock of the company acquired and are

considered to be material, then can both filings be considered proper?

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization's statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Depreciation expense for the year was recorded.

Chicago based Corporation X has a number of exporting transactions with companies

based in Sweden. Exporting activities result in receivables. If the settlement currency is

the Swedish Krona, which of the following will happen by changes in the direct or

indirect exchange rates?

Binary Company acquired 75 percent ownership of Fordham Corporation in 20X5, at

underlying book value. On that date, the fair value of the noncontrolling interest was

equal to 25 percent of the book value of Fordham Corporation. Binary purchased

inventory from Fordham for $150,000 on July 24, 20X6, and resold 90 percent of the

inventory to unaffiliated companies on November 11, 20X6, for $160,000. Fordham

produced the inventory sold to Binary for $120,000. The companies had no other

transactions during 20X6.

Based on the information given above, what amount of sales will be reported in the

20X6 consolidated income statement?

A. $120,000

B. $135,000

C. $150,000

D. $160,000

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Basis for measuring contributions” describes which term listed above?