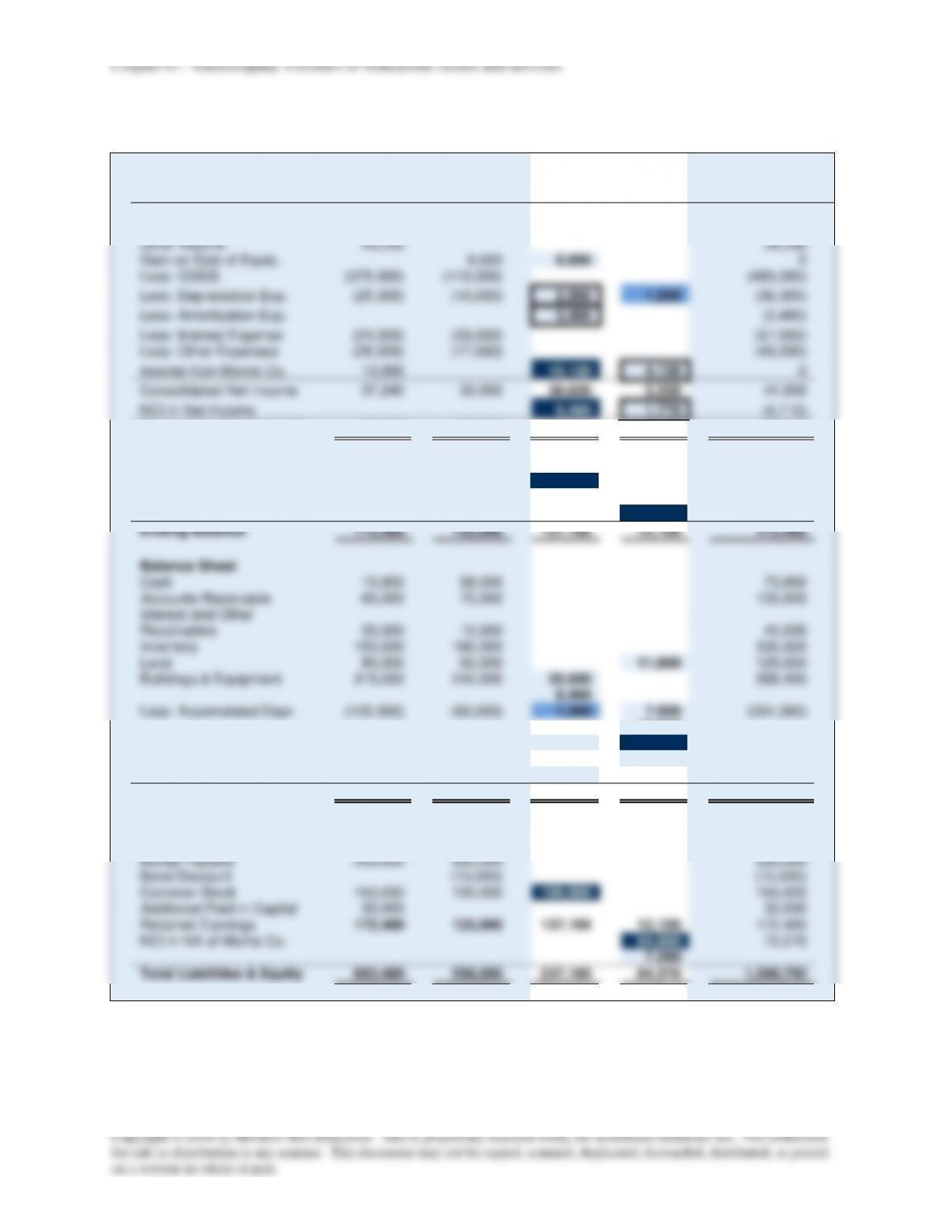

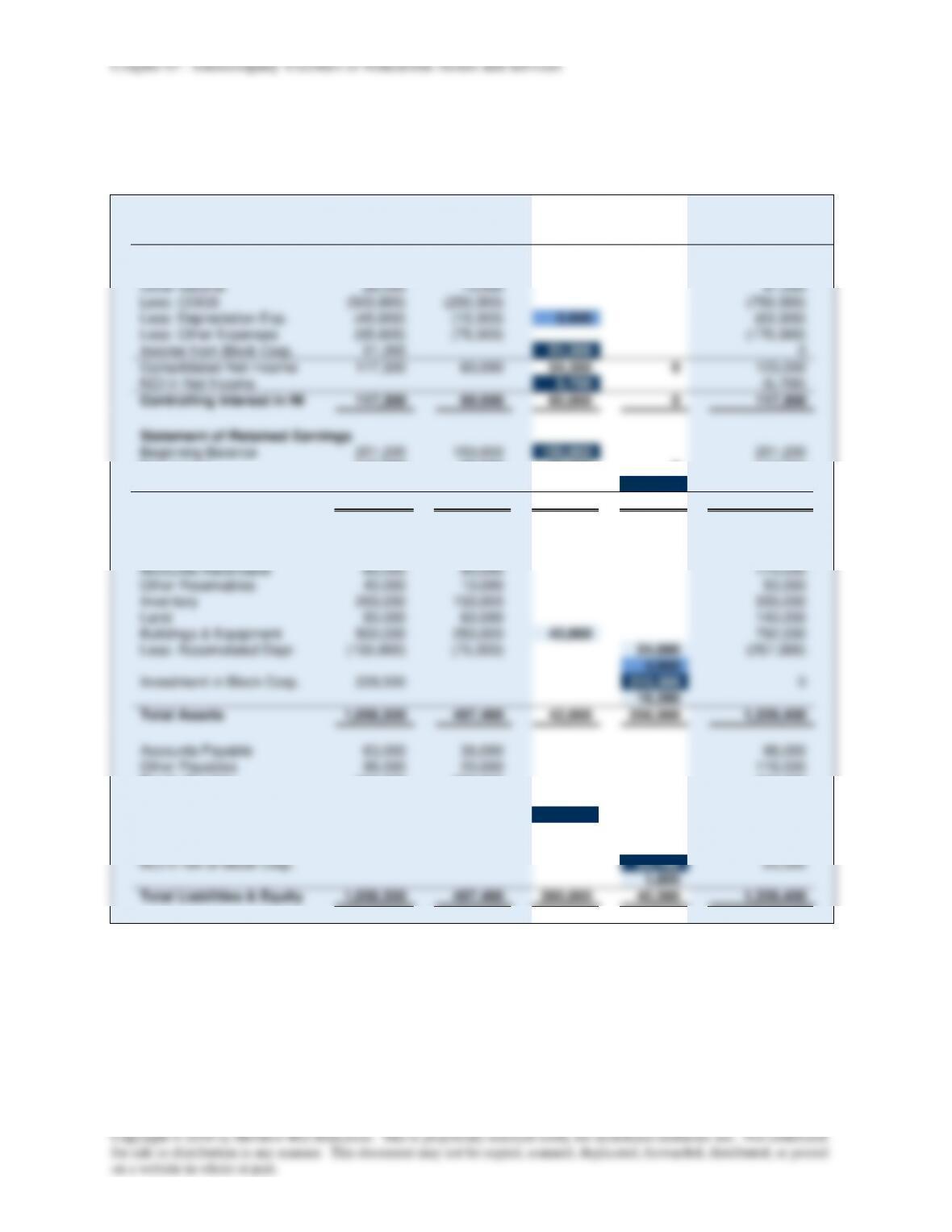

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

P7–35 (continued)

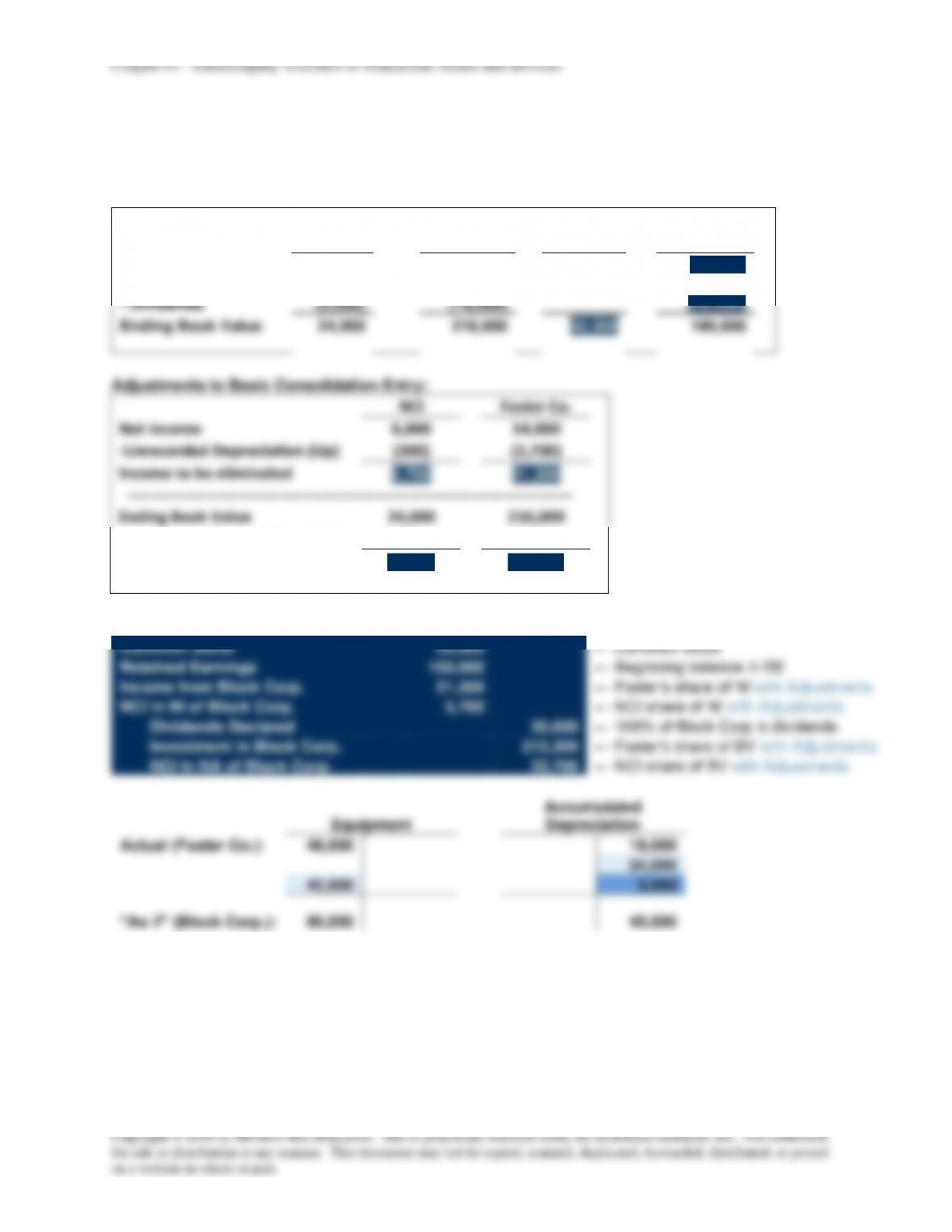

Adjustments to Basic Consolidation Entry:

NCI

Topp Corp.

Net Income

9,000

21,000

– Gain on Equip (Up)

(2,880)

(6,720)

+Extra Depreciation (Up)

360

840

Income to be eliminated

6,480

15,120

———————————————————-—————————

Ending Book Value

67,500

157,500

– Gain on Equip (Up)

(2,880)

(6,720)

+Extra Depreciation (Up)

360

840

Adjusted Book Value

64,980

151,620

108,000

242,000

Basic Consolidation Entry

Common Stock

100,000

← Common Stock

Retained Earnings

100,000

← Beginning balance RE

Income from Morris Co.

15,120

← Topp’s share of NI with Adjustments

NCI in NI of Morris Co.

6,480

← NCI share of NI with Adjustments

Dividends Declared

5,000

← 100% of Morris Co.’s dividends

Investment in Morris Co.

151,620

← Topp’s share of BV with Adjustments

NCI in NA of Morris Co.

64,980

← NCI share of BV with Adjustments

Excess Value (Differential) Calculations:

NCI

30%

+

Topp

Corp.

70%

=

Buildings &

Equipment

+

Copyright

+

Acc.

Depr.

Beginning balance

9,060

21,140

25,000

10,200

(5,000)

Changes

(1,770)

(4,130)

(3,400)

(2,500)

Ending balance

7,290

17,010

25,000

6,800

(7,500)

Amortized Excess Value Reclassification Entry:

Amortization Expense

3,400

Depreciation Expense

2,500

Income from Morris Co.

4,130

NCI in NI of Morris Co.

1,770

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

25,000

Copyright

6,800

Acc. Depr.

7,500

Investment in Morris Co.

17,010

NCI in NA of Morris Co.

7,290

Eliminate Gain on Purchase of Land

Investment in Morris Co.

11,000

Land

11,000

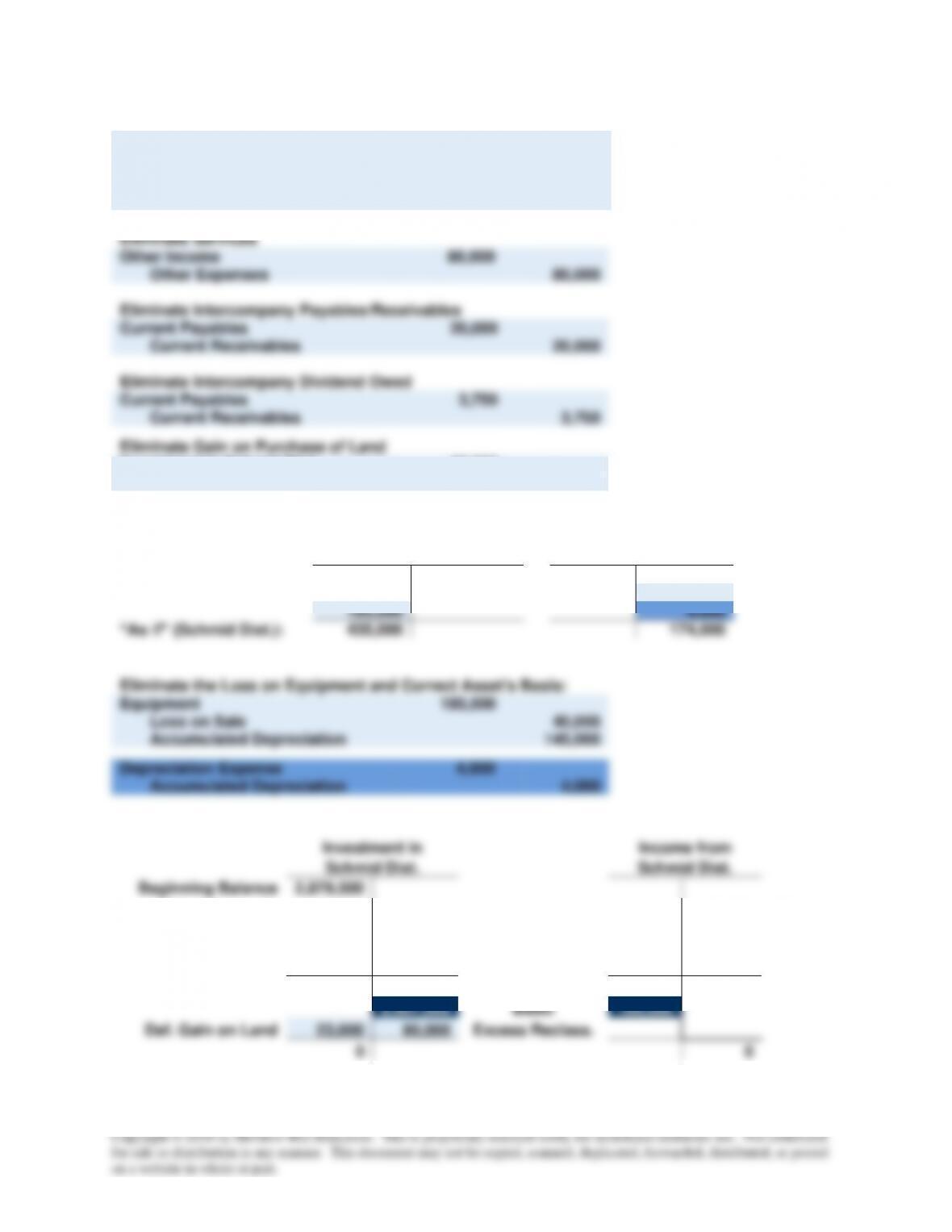

Chapter 07 – Intercompany Transfers of Noncurrent Assets and Services

Excess Value (Differential) Reclassification Entry:

Land

56,000

Goodwill

64,000

Investment in Schmid Dist.

90,000

NCI in NA of Schmid Dist.

30,000

Eliminate Services

Other Income

80,000

Other Expenses

80,000

Eliminate Intercompany Payables/Receivables

Current Payables

20,000

Current Receivables

20,000

Eliminate Intercompany Dividend Owed

Current Payables

3,750

Current Receivables

3,750

Eliminate Gain on Purchase of Land

Investment in Schmid Dist.

23,000

Land

23,000

Equipment

Accumulated

Depreciation

Actual (Rossman Corp.):

250,000

25,000

145,000

185,000

4,000

“As if” (Schmid Dist.):

435,000

174,000

Eliminate the Loss on Equipment and Correct Asset’s Basis:

Equipment

185,000

Loss on Sale

40,000

Accumulated Depreciation

145,000

Depreciation Expense

4,000

Accumulated Depreciation

4,000

Investment in

Income from

Schmid Dist.

Schmid Dist.

Beginning Balance

2,879,500

75% Net Income

82,500

82,500

75% Net Income

15,000

75% Dividends

Def. Loss on

Equipment

30,000

3,000

Realize Loss

3,000

30,000

Def. Loss on

Equipment

Ending Balance

2,974,000

109,500

Ending Balance

2,907,000

Basic

109,500

Def. Gain on Land

23,000

90,000

Excess Reclass.

0

0

P7-38 (continued)