Chapter 5 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES ACQUIRED AT

MORE THAN BOOK VALUE

CHAPTER 5

CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

ACQUIRED AT MORE THAN BOOK VALUE

IMPORTANT NOTE TO INSTRUCTORS

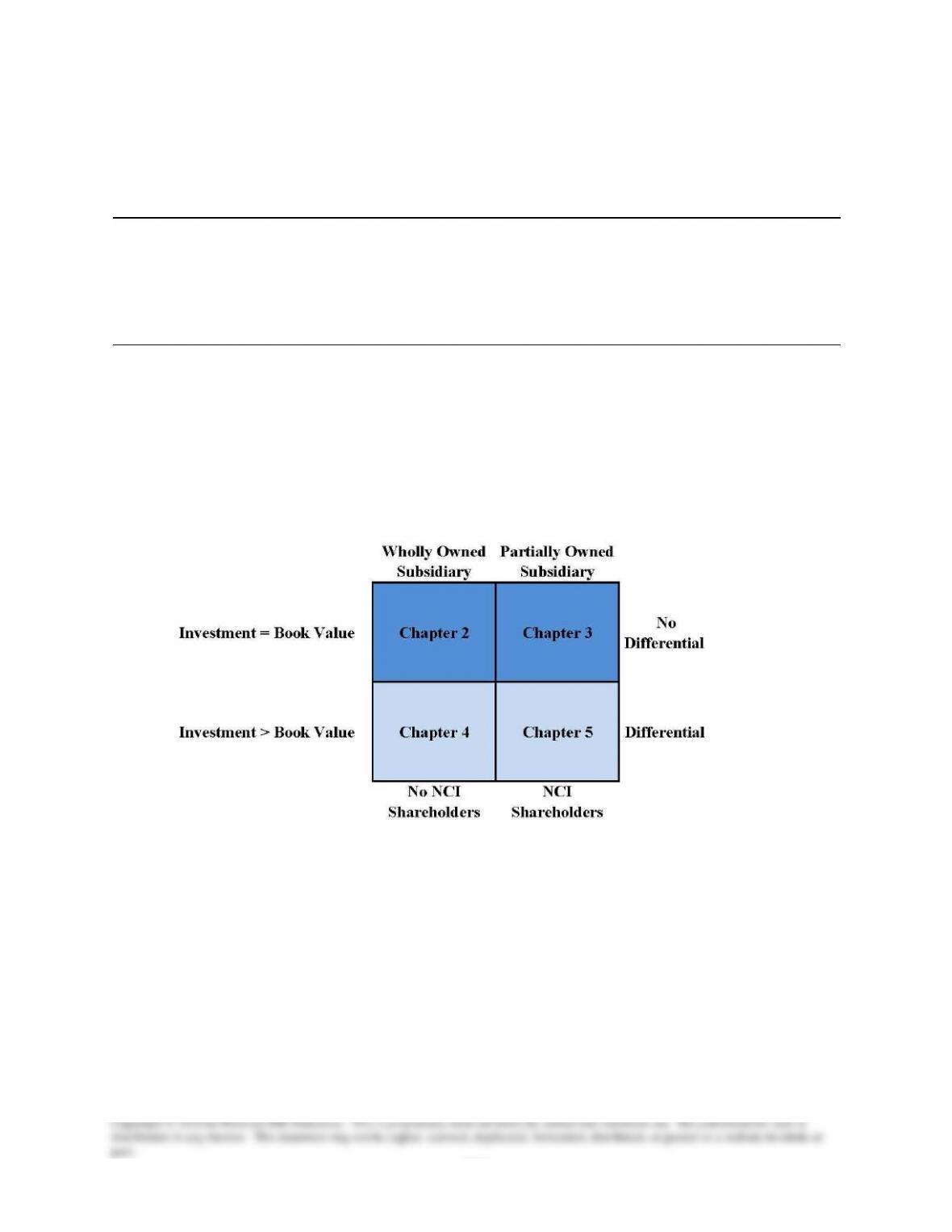

The 11th edition uses a building block approach to our coverage of consolidation in

chapters 2 through 5. Chapter 2 introduces our coverage of consolidation in the most basic

setting when the subsidiary is either created or purchased at an amount equal to the book value of

the subsidiary’s underlying net assets.

Chapter 3 explains how the basic consolidation process changes when the parent

company owns less than 100 percent of the subsidiary. Chapter 4 shows how the consolidation

process differs when the parent company acquires the subsidiary for an amount greater (or less)

than the book value of the subsidiary’s net assets. Finally, Chapter 5 presents the most complex

consolidation scenario (where the parent owns less than 100 percent of the subsidiary’s

outstanding voting stock and the acquisition price is not equal to the book value of the

subsidiary’s net assets). In order to facilitate this new approach, we emphasize that this edition

includes consolidation entries used to facilitate the elimination of the investment in a subsidiary

in two steps: (1) first the book value portion of the investment and income from the subsidiary

are eliminated and (2) then the differential portion of the investment and income from subsidiary

are eliminated with separate entries. We believe this approach is more intuitive for students.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-2

OVERVIEW OF CHAPTER 5

Chapter 5 presents the preparation of consolidated financial statements for less-than-

wholly-owned subsidiaries. When a subsidiary is less than wholly owned, the general approach

to consolidation is the same as discussed in Chapter 4 for wholly owned subsidiaries, but the

consolidation procedures must be modified slightly to recognize the noncontrolling interest.

Also, the computation of consolidated net income and retained earnings must allow for the claim

of the noncontrolling interest.

The noncontrolling shareholders of a subsidiary have a claim on the income and assets of

that subsidiary. In simple cases, the income that accrues to the noncontrolling interest is the

noncontrolling stockholders’ proportionate share of the subsidiary’s net income, and their claim

on assets is equal to their proportionate share of the subsidiary’s net assets.

The chapter also illustrates the consolidation process and resulting financial statements

when other comprehensive income is reported by the subsidiary. It also presents journal entries

recorded by the parent and subsidiary. The subsidiary’s other comprehensive income items

should also be allocated between the controlling and noncontrolling interests.

When the subsidiary reports other comprehensive income, the worksheet can be prepared

in the standard manner, with one modification. The standard three-part consolidation worksheet

can be modified to provide an additional section that includes the other comprehensive income of

the subsidiary and the parent’s share of the subsidiary’s other comprehensive income.

The parent company includes income from the subsidiary in its income statement and

adjusts the balance in the investment account for the investment income recorded and dividends

received when it uses the equity method in accounting for its investment. If the cost method is

used, the parent records dividend income for its portion of dividends received from the

subsidiary and different consolidation entries are needed in preparing the consolidated financial

statements.

Appendix 5A discusses additional considerations including negative retained earnings of

subsidiary at acquisition; other stockholders’ equity accounts; and the subsidiary’s disposal of

differential-related assets.

LEARNING OBJECTIVES

When students finish studying this chapter, they should be able to:

LO 5-1 Understand and explain how the consolidation process differs when the subsidiary is

less-than-wholly owned and there is a differential.

LO 5-2 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential.

LO 5-3 Understand and explain what happens when a parent company ceases to consolidate

a subsidiary.

LO 5-4 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential and other

comprehensive income.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-3

SYNOPSIS OF CHAPTER 5

Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at

More than Book Value

Cisco Acquires a Controlling Interest in Nuova

LO 5-1 Understand and explain how the consolidation process differs when the subsidiary is

less- than-wholly owned and there is a differential

A Noncontrolling Interest in Conjunction with a Differential

Consolidated Balance Sheet with Majority-Owned Subsidiary

LO 5-2 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential.

Consolidated Financial Statements with a Majority-Owned Subsidiary

Initial Year of Ownership

Second Year of Ownership

LO 5-3 Understand and explain what happens when a parent company ceases to consolidate

a subsidiary.

Discontinuance of Consolidation

LO 5-4 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential and other

comprehensive income.

Treatment of Other Comprehensive Income

Modification of the Consolidation Worksheet

Adjusting Entry Recorded by Subsidiary

Adjusting Entry Recorded by Parent Company

Consolidation Worksheet—Second Year following Combination

Consolidation Procedures

Consolidation Worksheet—Comprehensive Income in Subsequent Years

Appendix 5A

Additional Consolidations Details

Negative Retained Earnings of a Subsidiary at Acquisition

Other Stockholders’ Equity Accounts

Subsidiary’s Disposal of Differential Related Assets

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-4

NOTES ON POWERPOINT SLIDES

We have attempted to provide PowerPoint slides that will be useful to a broad set of users. Since

instructors often have different styles and preferences, we have attempted to include slides that

will accommodate different approaches and that can be adapted to classes with different levels of

preparation. For example, some instructors prefer to introduce the material before students have

read the chapter. We have tried to facilitate these types of introductory discussions by including

slides that replicate key points from the chapter. Other instructors expect students to have read

the chapter and attempted homework problems before coming to class. As a result, they may not

find it useful to review all of the topics in the chapter or to include slides that simply review

many of the details they expect students to study before class. However, instructors following

this approach often like to use sample exercises and problems built into the slides that allow

them to have extended discussions or to facilitate group interaction in class.

If instructors elect to spend two class periods on the same subject, they might find a combination

of both styles to be useful by first introducing foundational material before students have read

the chapter and studied the topic, followed by an extended discussion the next class period after

students have read the chapter and attempted homework problems.

We have tried to develop slides that can facilitate a flexible approach to allow instructors to

select the slides that best match their objectives and style for class discussions. This is the reason

we are including over 100 slides for some chapters in the text. We do not expect all instructors

to use all slides, but the slide files should help support different teaching approaches and allow

instructors to select the subset of slides that best matches their specific discussion objectives.

The slides are organized by learning objective. We have included a slide at the beginning of

each learning objective to show where the new material begins. Instructors may or may not want

to use these learning objective slides in class. We provide them primarily as a way of organizing

the material. We also include short multiple choice questions at the end of most learning

objectives. Some instructors find it useful to pause periodically during class to assess students’

level of understanding. For this reason, we include several “practice quiz questions” that can be

used throughout class discussions to engage students, help them focus on key points, or to

facilitate group interaction. Finally, we provide longer exercises and problems that many

instructors find useful in assessing understanding and encouraging group learning.

LO 5-1 Understand and explain how the consolidation process differs when the subsidiary is

less-than-wholly owned and there is a differential.

• Slides 3-4 briefly summarize how consolidation procedures differ when the

subsidiary is less-than-wholly owned.

• Slides 5-12 illustrate an example of the consolidation procedure for a less-than –

wholly owned subsidiary. Since the investment in Sub is acquired on the balance

sheet date, no income has been earned. Thus, there is no need for a consolidated

income statement or statement of retained earnings. We find that the preparation

of a consolidated balance sheet allows students to understand one aspect of the

differential (the balance sheet side) before getting too deep in the income

statement effects. We find it useful to provide full-page handouts (or an Excel

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-5

Template) for slides 5, 7 and 8 so that students can walk through the analyses in

small groups. We often go through slides 5-11 slowly, pausing to allow students

to work one step at a time before showing them correct answers. We then have

them complete the worksheet (slide 12) while working in a small group. If we are

short on time, we opt to quickly go through this worksheet with the entire class

and save “group time” for the “full–blown” worksheet later in this set of slides.

• Slides 13-16 include a second illustration of the basic calculations for a less-than-

wholly owned subsidiary.

LO 5-2 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential.

• Slides 20-31 walk students through the consolidation process during the first year

following acquisition.

• Slides 32-43 walk students through the consolidation process during the second year

following acquisition.

• Slides 44-56 are a group exercise which allows students to practice the consolidation

process for a less-than-wholly-owned subsidiary at the date of acquisition.

• Slides 57-58 summarize the differences in the consolidation entries that are unique to

the less-than-wholly-owned subsidiary consolidation as a quick reminder for students

and preparation for Group Exercise 2.

• Slides 59-76 return to the previous example to slowly walk students through the

consolidation during the first year of acquisition. This is a critical example for helping

students to understand all of the detail for a positive differential and partial

ownership. We tend to have students work one step ahead of the slides and reveal one

portion of the solution at a time to make sure they stay on track. After working

through all of the foundational steps, we have students complete the consolidation

worksheet in their groups (and sometimes have them turn in their solution as a “group

quiz”). Note that the book value calculations on slide 63 lead directly to the basic

consolidation entry. The bottom row of the excess value calculations on slide 65 leads

to the excess value reclassification entry and the middle row of the excess value

calculations leads to the amortized excess value reclassification entry.

LO 5-3 Understand and explain what happens when a parent company ceases to consolidate

a subsidiary.

• Slides 78-84 explain and illustrate the accounting for situations in which the parent

ceases to consolidate a subsidiary.

LO 5-4 Make calculations and prepare consolidation entries for the consolidation of a

partially owned subsidiary when there is a complex positive differential and other

comprehensive income.

• Slides 93-97 explain and briefly illustrate how the consolidation differs when the

subsidiary has other comprehensive income.

Appendix 5A Additional Consolidations Details

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-6

• Slides 99-103 briefly cover the additional considerations: subsidiary valuation,

negative retained earnings, other stockholders’ equity accounts and the disposal of

differential-related assets.

TEACHING IDEAS

1. Students could be asked to “prove” the amounts provided in their Fortune 100 company’s

annual report for noncontrolling interest on the consolidated balance sheet and on the

consolidated income statement. Reconciliation of these amounts is usually possible by

reading the information available in the footnotes. Some students may find that these

amounts cannot be reconciled from the information presented. If that is the case, student

should suggest additional disclosures that would make the calculation of the non–

controlling interest amounts possible.

2. Each student could be asked to determine the percentage of ownership of the subsidiaries

for a Fortune 100 company. This can be determined by access to Moody’s and is

sometimes disclosed in the company’s annual report. An indirect method to determine the

extent of the parent company’s ownership percentage of the subsidiaries could be used to

determine the magnitude of the noncontrolling interest on the consolidated balance sheet.

Students could be asked the question: Why do most parent companies acquire 100

percent ownership of the subsidiary when 51 percent would grant them economic

control? What are the economic reasons supporting more than a 51 percent ownership

level?

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-7

DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS

C5-1

LO 5-2

15 min.

M

Consolidation Worksheet Preparation

This case requires a basic understanding of the way in which four of the pieces of

information included in the consolidation worksheet are developed and used.

C5-2

LO 5-2

25 min.

M

Consolidated Income Presentation

Students must prepare a memorandum explaining how consolidated net income is

computed and the procedures used to allocate income to the parent company and

noncontrolling shareholders. Authoritative reference need to be included. In

addition, students must prepare an analysis showing the income statement

amounts actually reported for two years.

C5-3

LO 5-1

25 min.

M

Pro-Rata Consolidation

Students must research the authoritative literature to determine whether the

company should account for its joint venture investment using the equity method

or a pro rata consolidation. A memorandum that reports findings and provides the

necessary supporting references is required.

C5-4

LO 5-1

15 min.

M

Consolidation Procedures

Five questions are presented in this case. The questions focus on why

consolidation entries are needed, which balances must be eliminated, and the

ways in which particular consolidated balances are computed.

C5-5

LO 5-1

25 min.

M

Changing Accounting Standards: Monsanto Company

Students have to determine how Monsanto Company reported its subsidiary

noncontrolling interest in its 2007 consolidated financial statements, and

comment on the company’s treatment of its subsidiary noncontrolling interest

They also have to identify various aspects of the company’s special purpose or

variable interest entities.

E5-1

LO 5-1,

LO 5-2

15 min.

E

Multiple-Choice Questions on Consolidation Process

Four multiple-choice questions are used to cover basic issues dealing with the

preparation of consolidated statements subsequent to the date of combination.

E5-2

LO 5-1,

LO 5-2

15 min.

E

Multiple-Choice Questions on Consolidation

[AICPA Adapted] Five multiple-choice questions are used to cover additional

issues associated with the preparation of consolidated statements subsequent to

the date of combination.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-8

E5-3

LO 5-2

10 min.

E

Consolidation Entries with Differential

A basic set of balance sheet consolidation entries must be prepared. Assignment

of a differential is required.

E5-4

LO 5-2

15 min.

E

Computation of Consolidated Balances

Students must calculate the appropriate amounts to be included in the

consolidated balance sheet immediately following the acquisition for six items,

including goodwill.

E5-5

LO 5-2

15 min.

E

Balance Sheet Worksheet

Based on the balance sheets of the two companies immediately after the

acquisition, students should prepare and complete a consolidated balance sheet

worksheet.

E5-6

LO 5-2

30 min.

M

Majority-Owned Subsidiary Acquired at Higher than Book Value

The consolidation entries, a consolidated balance sheet worksheet and

consolidated balance sheet are required. Intercompany receivable/payable

adjustment is required.

E5-7

LO 5-2

15 min.

E

Consolidation with Noncontrolling Interest

Consolidation entries needed to prepare a consolidated balance sheet immediately

following the business combination are required. Differential is assigned to

inventory, buildings, and goodwill.

E5-8

LO 5-2

20 min.

M

Multiple-Choice Questions on Balance Sheet Consolidation

Given the balance sheets of the parent and subsidiary at the date of acquisition,

seven multiple-choice questions cover the computation of various consolidated

balances. The parent holds majority ownership in the subsidiary.

E5-9

LO 5-2

20 min.

M

Majority Owned Subsidiary with Differential

Students must prepare the equity method journal entries made during the year by

the parent and also the consolidation entries necessary to prepare the consolidated

financial statements given a differential between cost and book values of the

underlying net assets.

E5-10

LO 5-1,

LO 5-2

20 min.

E

Differential Assigned to Amortizable Asset

The investment account balance at the end of the first period of ownership must

be calculated. Students should also prepare the consolidation entries needed to

prepare consolidated financial statements at the end of the first year of

ownership. The differential is assigned to an intangible asset.

E5-11

LO 5-2

25 min.

M

Consolidation after One Year of Ownership

Consolidation entries to prepare a consolidated balance sheet worksheet at the

date of acquisition and to prepare a full set of consolidated statements at the end

of the first year of ownership are required. The subsidiary is majority-owned and

the differential is assigned to buildings and equipment and goodwill.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5-9

E5-12

LO 5-1,

LO 5-2

25 min.

M

Consolidation Following Three Years of Ownership

Information on subsidiary net income and dividends is presented for a three year

period. The differential is assigned to land, equipment, and patents. Students have

to calculate the increase in value of patents. The consolidation entries to prepare

a consolidated balance sheet at the date of acquisition, the investment account

balance at the end of the second year 2, equity-method entries recorded by the

parent in the third year, and the consolidation entries needed at the end of the

third year to prepare a three-part consolidation worksheet are also required.

E5-13

LO 5-2

40 min.

H

Consolidation Worksheet for Majority-Owned Subsidiary

A consolidation worksheet and consolidated statements are required for a

majority-owned subsidiary. No differential is involved.

E5-14

LO 5-2

40 min.

M

Consolidation Worksheet for Majority-Owned Subsidiary for Second Year

Consolidation journal entries and a three-part work paper must be prepared for a

wholly-owned subsidiary for the second year after acquisition.

E5-15

LO 5-4

20 min

M

Preparation of Stockholders’ Equity Section with Other Comprehensive

Income

Subsidiary net income, other comprehensive income, and dividends paid are

given for two years. Parent company operating income and dividends are also

given. Consolidated net income and comprehensive income must be computed

for each year and the stockholders’ equity section of the consolidated balance

sheet prepared at the end of the second year.

E5-16

LO 5-4

20 min.

M

Consolidation Entries for Subsidiary with Other Comprehensive Income

Subsidiary net income, comprehensive income, and dividends are given. Equity-

method entries recorded by the parent and consolidation entries needed to prepare

a complete set of financial statements at the end of the year are required.

E5-17A

15 min.

E

Consolidation of Subsidiary with Negative Retained Earnings

Students must prepare the consolidation entry immediate after acquisition of an

80% interest in a subsidiary with a negative retained earnings balance.

E5-18A

30 min.

M

Complex Assignment of Differential

Parent company entries under the equity method and the consolidation entries

involving a differential allocation to several current and long-term assets as well

as notes payable are required.

P5-19

LO 5-1

10 min.

E

Reported Balances

Students compute the reported balances immediately following the acquisition.