Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-34 Consolidation Worksheet at End of Second Year of Ownership

a.

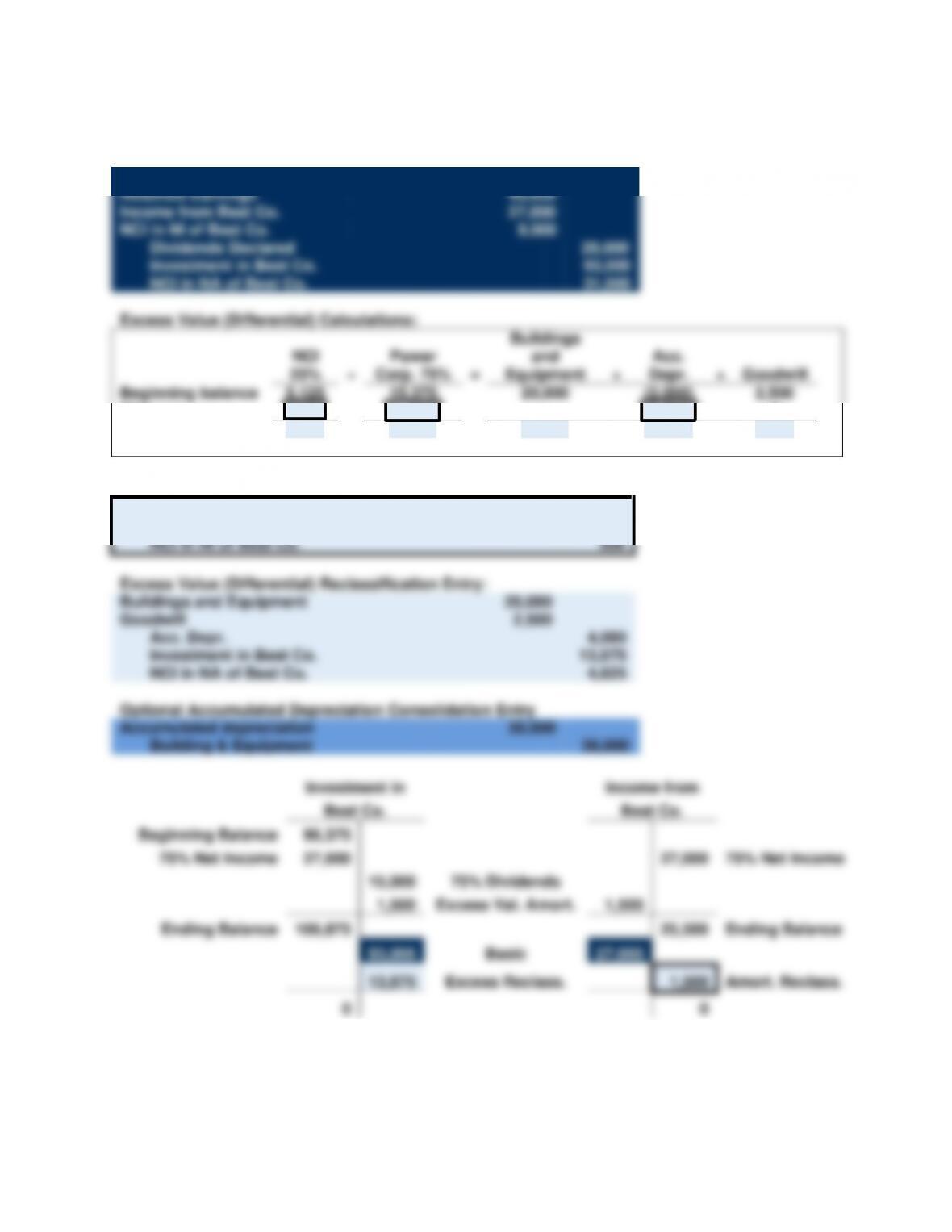

Equity Method Entries on Power Corp.’s Books:

Investment in Best Co.

27,000

Income from Best Co.

27,000

Record Power Corp.’s 75% share of Best Co.’s 20X9 income

Cash

15,000

Investment in Best Co.

15,000

Record Power Corp.’s 75% share of Best Co.’s 20X9 dividend

Income from Best Co.

1,500

Investment in Best Co.

1,500

Record amortization of excess acquisition price

Book Value Calculations:

NCI

25%

+

Power

Corp.

75%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

27,000

81,000

60,000

48,000

+ Net Income

9,000

27,000

36,000

– Dividends

(5,000)

(15,000)

(20,000)

Ending book value

31,000

93,000

60,000

64,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-62

P5-34 (continued)

Basic Consolidation Entry

Common Stock

60,000

Retained Earnings

48,000

Income from Best Co.

27,000

NCI in NI of Best Co.

9,000

Dividends Declared

20,000

Investment in Best Co.

93,000

NCI in NA of Best Co.

31,000

Excess Value (Differential) Calculations:

NCI

25%

+

Power

Corp. 75%

=

Buildings

and

Equipment

+

Acc.

Depr.

+

Goodwill

Beginning balance

5,125

15,375

20,000

(2,000)

2,500

Changes

(500)

(1,500)

(2,000)

0

Ending balance

4,625

13,875

20,000

(4,000)

2,500

Amortized Excess Value Reclassification Entry:

Depreciation Expense

2,000

Income from Best Co.

1,500

NCI in NI of Best Co.

500

Excess Value (Differential) Reclassification Entry:

Buildings and Equipment

20,000

Goodwill

2,500

Acc. Depr.

4,000

Investment in Best Co.

13,875

NCI in NA of Best Co.

4,625

Optional Accumulated Depreciation Consolidation Entry

Accumulated depreciation

30,000

Building & Equipment

30,000

Investment in

Income from

Best Co.

Best Co.

Beginning Balance

96,375

75% Net Income

27,000

27,000

75% Net Income

15,000

75% Dividends

1,500

Excess Val. Amort.

1,500

Ending Balance

106,875

25,500

Ending Balance

93,000

Basic

27,000

13,875

Excess Reclass.

1,500

Amort. Reclass.

0

0

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-63

P5-34 (continued)

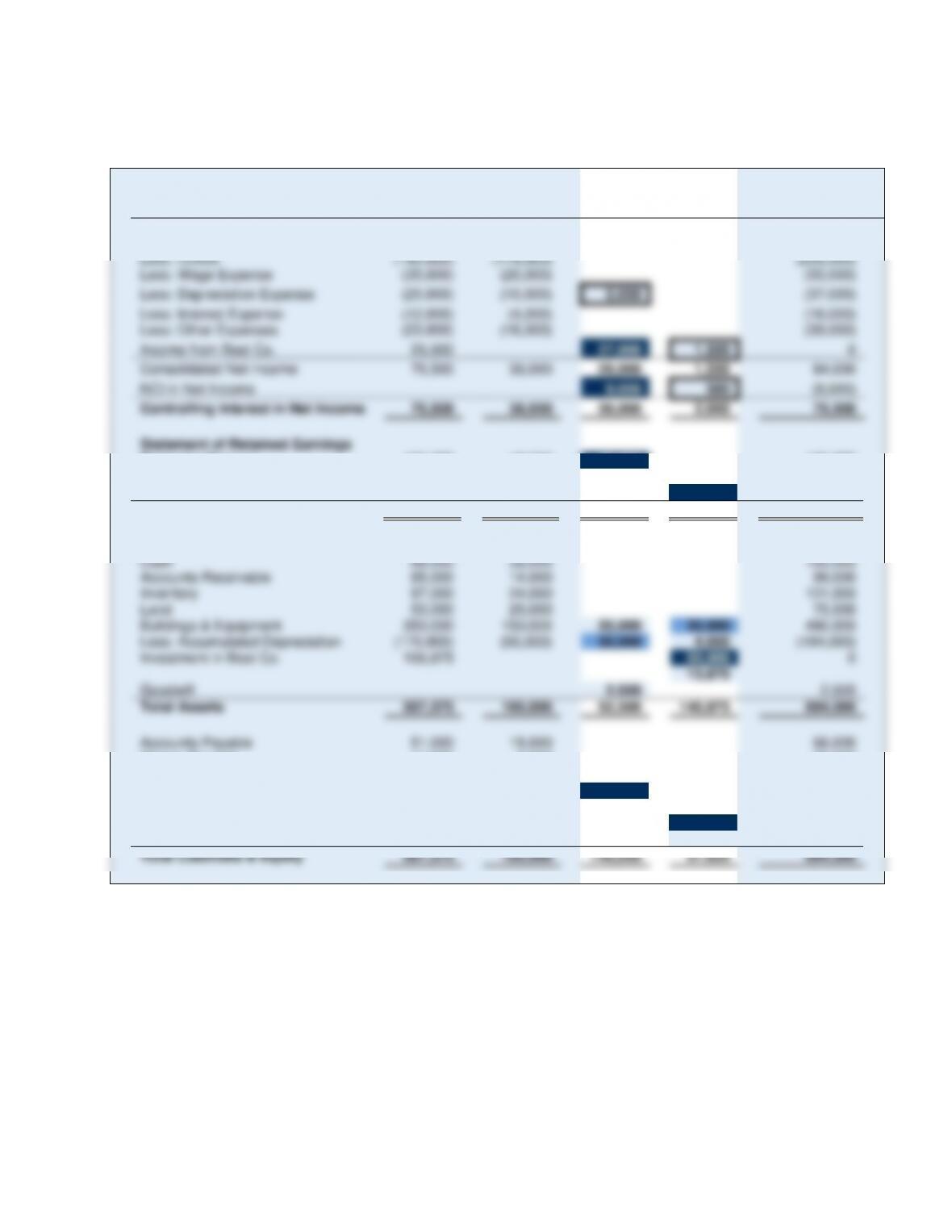

b.

Power

Corp.

Best Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

290,000

200,000

490,000

Less: COGS

(145,000)

(114,000)

(259,000)

Less: Wage Expense

(35,000)

(20,000)

(55,000)

Less: Depreciation Expense

(25,000)

(10,000)

2,000

(37,000)

Less: Interest Expense

(12,000)

(4,000)

(16,000)

Less: Other Expenses

(23,000)

(16,000)

(39,000)

Income from Best Co.

25,500

27,000

1,500

0

Consolidated Net Income

75,500

36,000

29,000

1,500

84,000

NCI in Net Income

9,000

500

(8,500)

Controlling Interest in Net Income

75,500

36,000

38,000

2,000

75,500

Statement of Retained Earnings

Beginning Balance

126,875

48,000

48,000

126,875

Net Income

75,500

36,000

38,000

2,000

75,500

Less: Dividends Declared

(30,000)

(20,000)

20,000

(30,000)

Ending Balance

172,375

64,000

86,000

22,000

172,375

Balance Sheet

Cash

68,500

32,000

100,500

Accounts Receivable

85,000

14,000

99,000

Inventory

97,000

24,000

121,000

Land

50,000

25,000

75,000

Buildings & Equipment

350,000

150,000

20,000

30,000

490,000

Less: Accumulated Depreciation

(170,000)

(50,000)

30,000

4,000

(194,000)

Investment in Best Co.

106,875

93,000

0

13,875

Goodwill

2,500

2,500

Total Assets

587,375

195,000

52,500

140,875

694,000

Accounts Payable

51,000

15,000

66,000

Wages Payable

14,000

6,000

20,000

Notes Payable

150,000

50,000

200,000

Common Stock

200,000

60,000

60,000

200,000

Retained Earnings

172,375

64,000

86,000

22,000

172,375

NCI in NA of Best Co.

31,000

35,625

4,625

Total Liabilities & Equity

587,375

195,000

146,000

57,625

694,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-34 (continued)

c.

Power Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X9

Cash

$100,500

Accounts Receivable

99,000

Inventory

121,000

Land

75,000

Buildings and Equipment

$490,000

Less: Accumulated Depreciation

(194,000)

296,000

Goodwill

2,500

Total Assets

$694,000

Accounts Payable

$ 66,000

Wages Payable

20,000

Notes Payable

200,000

Stockholders’ Equity:

Controlling Interest:

Common Stock

$200,000

Retained Earnings

172,375

Total Controlling Interest

$372,375

Noncontrolling Interest

35,625

Total Stockholders’ Equity

408,000

Total Liabilities and Stockholders’ Equity

$694,000

Power Corporation and Subsidiary

Consolidated Income Statement

Year Ended December 31, 20X9

Sales

$490,000

Cost of Goods Sold

$259,000

Wage Expense

55,000

Depreciation Expense

37,000

Interest Expense

16,000

Other Expenses

39,000

Total Expenses

(406,000)

Consolidated Net Income

$ 84,000

Income to Noncontrolling Interest

(8,500)

Income to Controlling Interest

$

75,500

Power Corporation and Subsidiary

Consolidated Retained Earnings Statement

Year Ended December 31, 20X9

Retained Earnings, January 1, 20X9

$126,875

Income to Controlling Interest, 20X9

75,500

$202,375

Dividends Declared, 20X9

(30,000)

Retained Earnings, December 31, 20X9

$172,375

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5-35 Comprehensive Problem: Differential Apportionment

a.

Equity Method Entries on Mortar Corp.’s Books:

Investment in Granite Co.

173,000

Cash

173,000

Record the initial investment in Granite Co.

Investment in Granite Co.

48,000

Income from Granite Co.

48,000

Record Mortar Corp.’s 80% share of Granite Co.’s 20X7 income

Cash

16,000

Investment in Granite Co.

16,000

Record Mortar Corp.’s 80% share of Granite Co.’s 20X7 dividend

Income from Granite Co.

3,000

Investment in Granite Co.

3,000

Record amortization of excess acquisition price

Book Value Calculations:

NCI

20%

+

Mortar

Corp.

80%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

30,000

120,000

50,000

100,000

+ Net Income

12,000

48,000

60,000

– Dividends

(4,000)

(16,000)

(20,000)

Ending book value

38,000

152,000

50,000

140,000

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-66

P5-35 (continued)

Basic Consolidation Entry

Common Stock

50,000

Retained Earnings

100,000

Income from Granite Co.

48,000

NCI in NI of Granite Co.

12,000

Dividends Declared

20,000

Investment in Granite Co.

152,000

NCI in NA of Granite Co.

38,000

Excess Value (Differential) Calculations:

NCI

20%

+

Mortar

Corp. 80%

=

Buildings &

Equipment

+

Acc.

Depr.

+

Goodwil

l

Beginning balance

13,250

53,000

41,250

0

25,000

Changes

(750)

(3,000)

(3,750)

0

Ending balance

12,500

50,000

41,250

(3,750)

25,000

Amortized Excess Value Reclassification Entry:

Depreciation Expense

3,750

Income from Granite Co.

3,000

NCI in NI of Granite Co.

750

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

41,250

Goodwill

25,000

Acc. Depr.

3,750

Investment in Granite Co.

50,000

NCI in NA of Granite Co.

12,500

Eliminate Intercompany Accounts:

Accounts Payable

16,000

Accounts Receivable

16,000

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

60,000

Building & Equipment

60,000

Investment in

Income from

Granite Co.

Granite Co.

Acquisition Price

173,000

80% Net Income

48,000

48,000

80% Net Income

16,000

80% Dividends

3,000

Excess Val. Amort.

3,000

Ending Balance

202,000

45,000

Ending Balance

152,000

Basic

48,000

50,000

Excess Reclass.

3,000

Amort. Reclass.

0

0

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-67

P5-35 (continued)

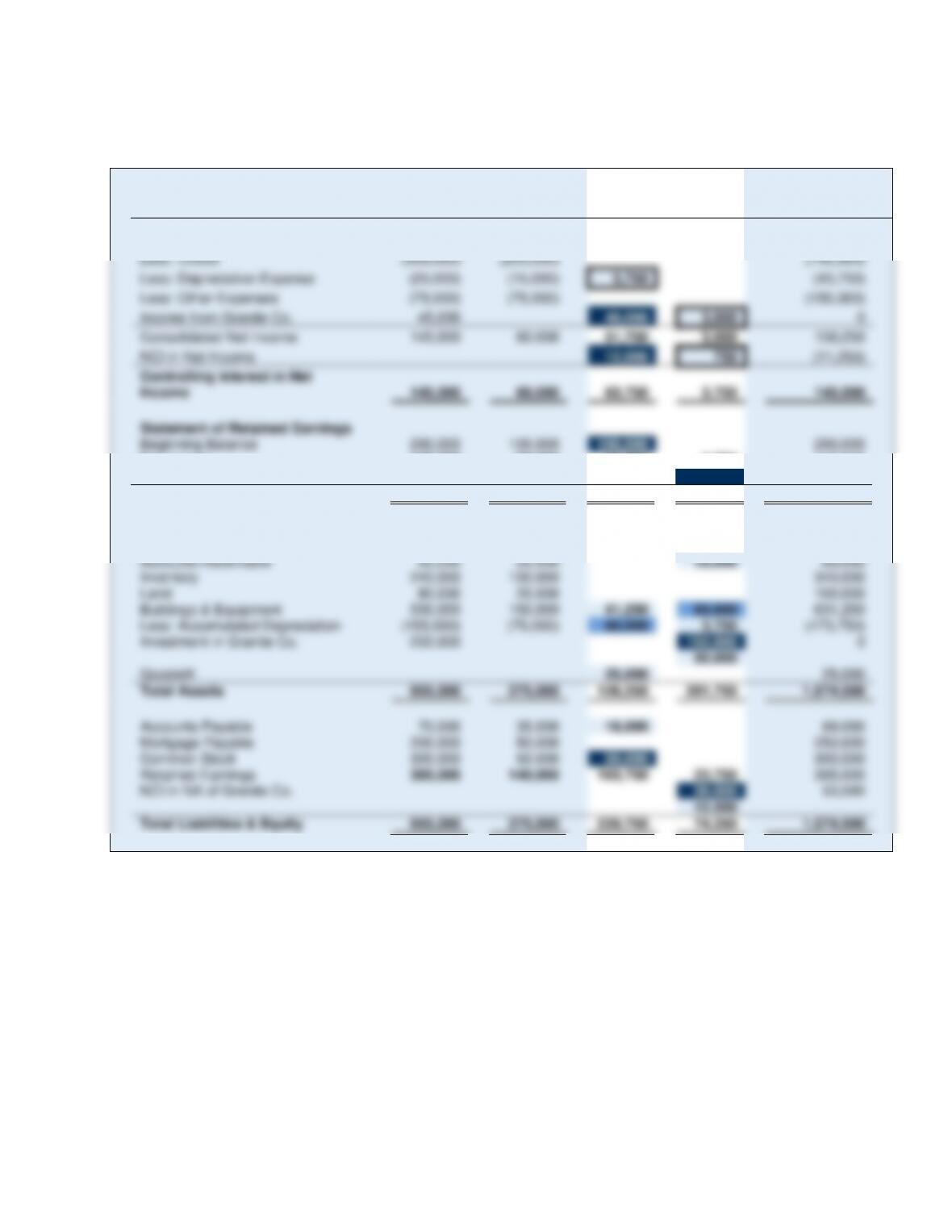

c.

Mortar

Corp.

Granite

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

700,000

400,000

1,100,000

Less: COGS

(500,000)

(250,000)

(750,000)

Less: Depreciation Expense

(25,000)

(15,000)

3,750

(43,750)

Less: Other Expenses

(75,000)

(75,000)

(150,000)

Income from Granite Co.

45,000

48,000

3,000

0

Consolidated Net Income

145,000

60,000

51,750

3,000

156,250

NCI in Net Income

12,000

750

(11,250)

Controlling Interest in Net

Income

145,000

60,000

63,750

3,750

145,000

Statement of Retained Earnings

Beginning Balance

290,000

100,000

100,000

290,000

Net Income

145,000

60,000

63,750

3,750

145,000

Less: Dividends Declared

(50,000)

(20,000)

20,000

(50,000)

Ending Balance

385,000

140,000

163,750

23,750

385,000

Balance Sheet

Cash

38,000

25,000

63,000

Accounts Receivable

50,000

55,000

16,000

89,000

Inventory

240,000

100,000

340,000

Land

80,000

20,000

100,000

Buildings & Equipment

500,000

150,000

41,250

60,000

631,250

Less: Accumulated Depreciation

(155,000)

(75,000)

60,000

3,750

(173,750)

Investment in Granite Co.

202,000

152,000

0

50,000

Goodwill

25,000

25,000

Total Assets

955,000

275,000

126,250

281,750

1,074,500

Accounts Payable

70,000

35,000

16,000

89,000

Mortgage Payable

200,000

50,000

250,000

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

385,000

140,000

163,750

23,750

385,000

NCI in NA of Granite Co.

38,000

50,500

12,500

Total Liabilities & Equity

955,000

275,000

229,750

74,250

1,074,500

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

P5–36 Comprehensive Problem: Differential Apportionment in Subsequent Period.

a.

Equity Method Entries on Mortar Corp.’s Books:

Investment in Granite Co.

36,000

Income from Granite Co.

36,000

Record Mortar Corp.’s 80% share of Granite Co.’s 20X8 income

Cash

20,000

Investment in Granite Co.

20,000

Record Mortar Corp.’s 80% share of Granite Co.’s 20X8 dividend

Income from Granite Co.

11,800

Investment in Granite Co.

11,800

Record amortization of excess acquisition price

Book Value Calculations:

NCI

20%

+

Mortar Corp.

80%

=

Common

Stock

+

Retained

Earnings

Beginning book

value

38,000

152,000

50,000

140,000

+ Net Income

9,000

36,000

45,000

– Dividends

(5,000)

(20,000)

(25,000)

Ending book value

42,000

168,000

50,000

160,000

1/1/X8

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-69

P5–36 (continued)

Basic Consolidation Entry

Common Stock

50,000

Retained Earnings

140,000

Income from Granite Co.

36,000

NCI in NI of Granite Co.

9,000

Dividends Declared

25,000

Investment in Granite Co.

168,000

NCI in NA of Granite Co.

42,000

Excess Value (Differential) Calculations:

NCI

20%

+

Mortar

Corp.

80%

=

Buildings

&

Equipment

+

Acc.

Depr.

+

Goodwill

Beginning balance

12,500

50,000

41,250

(3,750)

25,000

Changes

(2,950)

(11,800)

(3,750)

(11,000)

Ending balance

9,550

38,200

41,250

(7,500)

14,000

Amortized Excess Value Reclassification Entry:

Depreciation Expense

3,750

Goodwill Impairment Loss

11,000

Income from Granite Co.

11,800

NCI in NI of Granite Co.

2,950

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

41,250

Goodwill

14,000

Accumulated Dep.

7,500

Investment in Granite Co.

38,200

NCI in NA of Granite Co.

9,550

Eliminate Intercompany Accounts:

Accounts Payable

9,000

Accounts Receivable

9,000

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

60,000

Building & Equipment

60,000

Investment in

Income from

Granite Co.

Granite Co.

Beginning

Balance

202,000

80% Net Income

36,000

36,000

80% Net Income

20,000

80% Dividends

11,800

Excess Val.

Amort.

11,800

Ending Balance

206,200

24,200

Ending Balance

168,000

Basic

36,000

38,200

Excess Reclass.

11,800

Amort. Reclass.

0

0

Chapter 05 – Consolidation of Less-Than-Wholly Owned Subsidiaries Acquired at More than Book Value

5-70

P5–36 (continued)

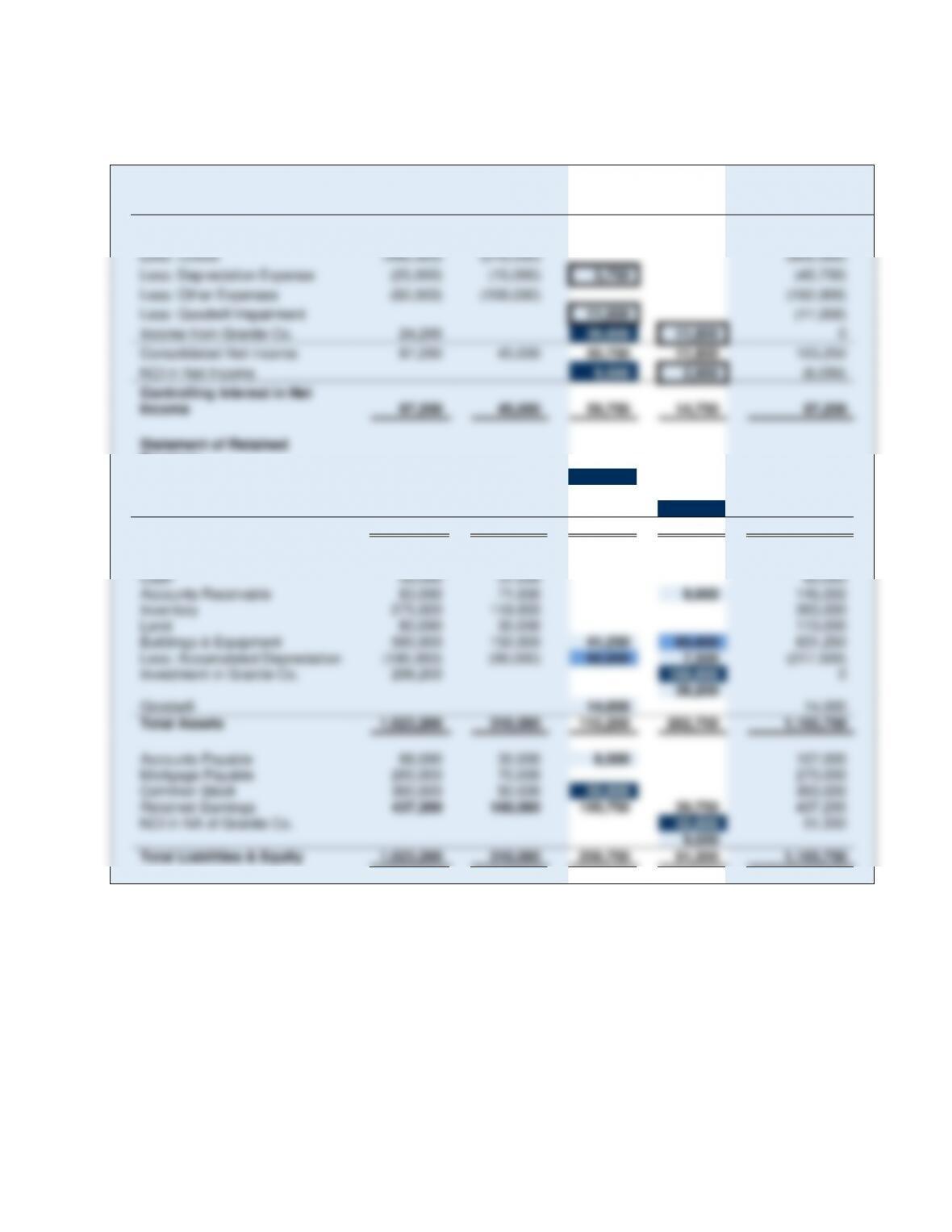

c.

Mortar

Corp.

Granite

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

650,000

470,000

1,120,000

Less: COGS

(490,000)

(310,000)

(800,000)

Less: Depreciation Expense

(25,000)

(15,000)

3,750

(43,750)

Less: Other Expenses

(62,000)

(100,000)

(162,000)

Less: Goodwill Impairment

11,000

(11,000)

Income from Granite Co.

24,200

36,000

11,800

0

Consolidated Net Income

97,200

45,000

50,750

11,800

103,250

NCI in Net Income

9,000

2,950

(6,050)

Controlling Interest in Net

Income

97,200

45,000

59,750

14,750

97,200

Statement of Retained

Earnings

Beginning Balance

385,000

140,000

140,000

385,000

Net Income

97,200

45,000

59,750

14,750

97,200

Less: Dividends Declared

(45,000)

(25,000)

25,000

(45,000)

Ending Balance

437,200

160,000

199,750

39,750

437,200

Balance Sheet

Cash

59,000

31,000

90,000

Accounts Receivable

83,000

71,000

9,000

145,000

Inventory

275,000

118,000

393,000

Land

80,000

30,000

110,000

Buildings & Equipment

500,000

150,000

41,250

60,000

631,250

Less: Accumulated Depreciation

(180,000)

(90,000)

60,000

7,500

(217,500)

Investment in Granite Co.

206,200

168,000

0

38,200

Goodwill

14,000

14,000

Total Assets

1,023,200

310,000

115,250

282,700

1,165,750

Accounts Payable

86,000

30,000

9,000

107,000

Mortgage Payable

200,000

70,000

270,000

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

437,200

160,000

199,750

39,750

437,200

NCI in NA of Granite Co.

42,000

51,550

9,550

Total Liabilities & Equity

1,023,200

310,000

258,750

91,300

1,165,750