Chapter 02 – Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with no Differential

5. d – Since these are liquidating dividends they would decrease the investment account under

the cost method and decrease the investment account under the equity method.

6. d – The amount of dividends not in excess would be considered dividend income.

(a) Incorrect. There would be at least some dividend income recorded.

E2-2 Multiple-Choice Questions on Intercorporate Investments

1. b – Equity method reporting is used when an investor gains significant influence over the

operating and financing decisions of the investee. Typically, this is satisfied by

maintaining 20% or more of the voting stock, but can also be obtained by other

2. c – Under the equity method, net income from the investee causes an increase to the

investment, while dividends declared by the investee causes a reduction.

(a) Incorrect. This simply represents the historical cost of the investment. It must be

E2-3 Multiple-Choice Questions on Applying Equity Method

1. d – $250,000 + ($100,000 x 0.30) – ($10,000 x 0.30) = $277,000

2. c – 20X9 investment income: $650,000 * 30% = $195,000, 20X8 adjustment: ($600,000 *

3. d – Because income is greater than the amount of dividends declared, the equity method

would have resulted in a higher balance in the investment account, net earnings, and

retained earnings than under the cost method.

4. d – Under the equity method, dividends by the investee are recorded with a credit to the

investment account, not to dividend revenue. By wrongly classifying this entry, the

investment is overstated, and retained earnings are also overstated.

E2-4 Cost versus Equity Reporting

a. Winston Corporation net income – cost method:

20X2

$100,000

+

.40($30,000)

$112,000

20X3

$ 60,000

+

.40($60,000)

84,000

20X4

$250,000

+

.40($20,000

+

$25,000)a

268,000

a Dividends paid from undistributed earnings of prior years

($70,000 + $40,000 – $30,000 – $60,000 = $20,000)

and $25,000 earnings of current period.

b. Winston Corporation net income – equity method:

20X2

$100,000

+

.40($70,000)

$128,000

20X3

$ 60,000

+

.40($40,000)

76,000

20X4

$250,000

+

.40($25,000)

260,000

E2-5 Acquisition Price

Balance at date of acquisition:

a. Cost method $54,000 + $2,800 = $56,800

Change in Investment Account

Year

Net Income

Dividends

Cost Method

Equity Method

20X1

$ 8,000

$15,000

$(2,800)

$(2,800)

20X2

12,000

10,000

800

20X3

20,000

10,000

______

4,000

Change in account balance

$(2,800)

$ 2,000

E2-6 Investment Income

a. (1) Ravine Corporation net income under Cost Method:

20X6

$140,000

+

0.30($20,000)

=

$146,000

20X7

$ 80,000

+

0.30($40,000)

=

$ 92,000

20X8

$220,000

+

0.30($20,000 + $10,000)a

=

$229,000

20X9

$160,000

+

0.30($20,000)

=

$166,000

a Dividends paid from undistributed earnings of prior years

($30,000 + $50,000 – $20,000 – $40,000= $20,000) and $10,000

earnings of current period.

(2) Ravine Corporation net income under Equity Method:

20X6

$140,000

+

0.30($30,000)

=

$149,000

20X7

$ 80,000

+

0.30($50,000)

=

$ 95,000

20X8

$220,000

+

0.30($10,000)

=

$223,000

20X9

$160,000

+

0.30($40,000)

=

$172,000

b. Journal entries recorded by Ravine Corporation in 20X8:

(1) Cost method:

Cash

12,000

Dividend Income

9,000

Investment in Valley Stock

3,000

(2) Equity method:

Cash

12,000

Investment in Valley Stock

12,000

Investment in Valley Stock

3,000

Income from Valley

3,000

E2-7 Investment Value

The following amounts would be reported as the carrying value of Port’s investment in Sund:

20X2

$184,500

=

$180,000

+

($40,000 x 0.30)

–

($25,000 x 0.30)

20X3

$193,500

=

$184,500

+

($30,000 x 0.30)

20X4

$195,000

=

$193,500 + ($5,000 x 0.30)

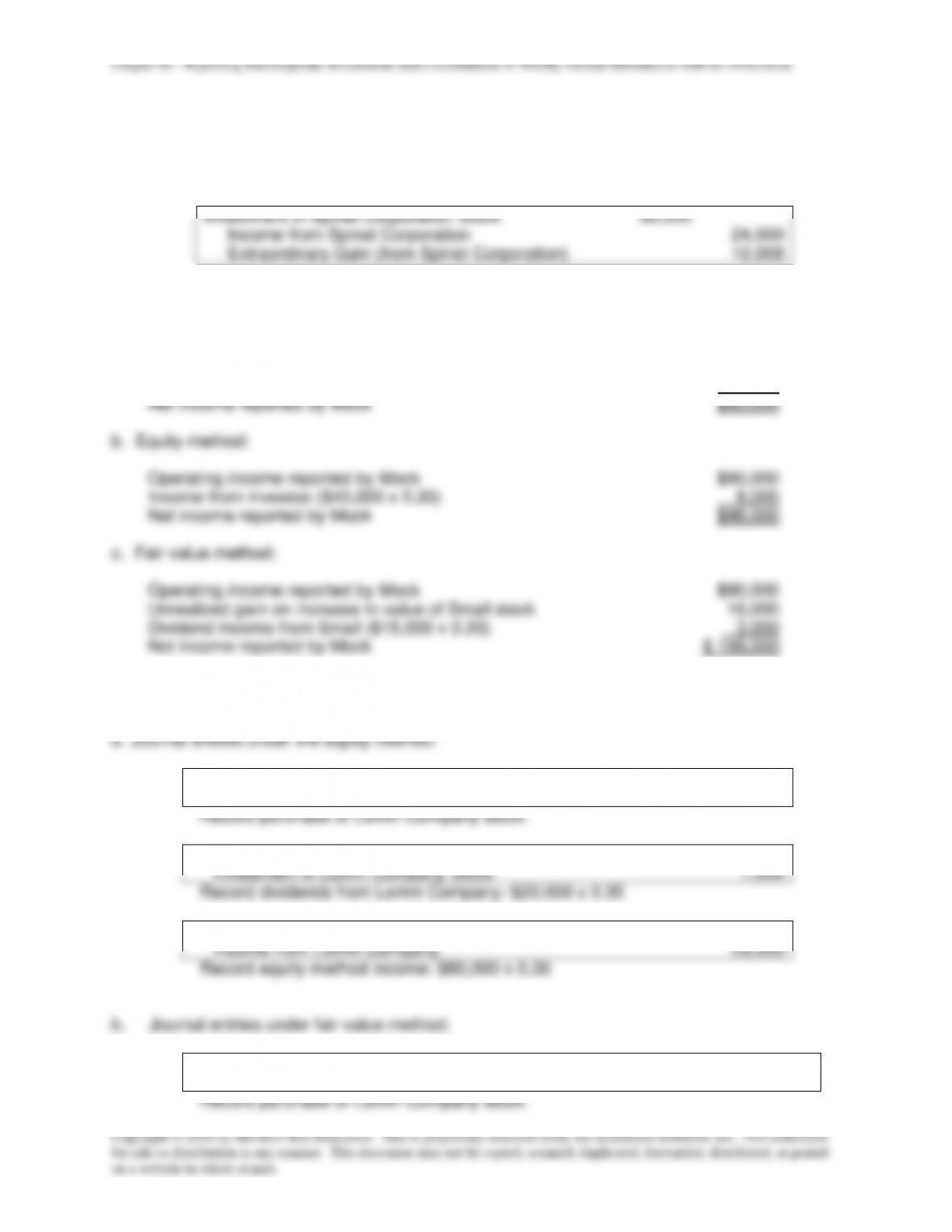

E2-8A Income Reporting

Journal entry recorded by Grandview Company:

Investment in Spinet Corporation Stock

36,000

Income from Spinet Corporation

24,000

Extraordinary Gain (from Spinet Corporation)

12,000

E2-9 Fair Value Method

a. Cost method:

Operating income reported by Mock

$90,000

Dividend income from Small ($15,000 x 0.20)

3,000

Net income reported by Mock

$93,000

Operating income reported by Mock

$90,000

Income from investee ($40,000 x 0.20)

8,000

Net income reported by Mock

$98,000

Operating income reported by Mock

$90,000

Unrealized gain on increase in value of Small stock

16,000

Dividend income from Small ($15,000 x 0.20)

3,000

Net income reported by Mock

$ 109,000

E2-10 Fair Value Recognition

(1)

Investment in Lomm Company Stock

140,000

Cash

140,000

Record purchase of Lomm Company stock.

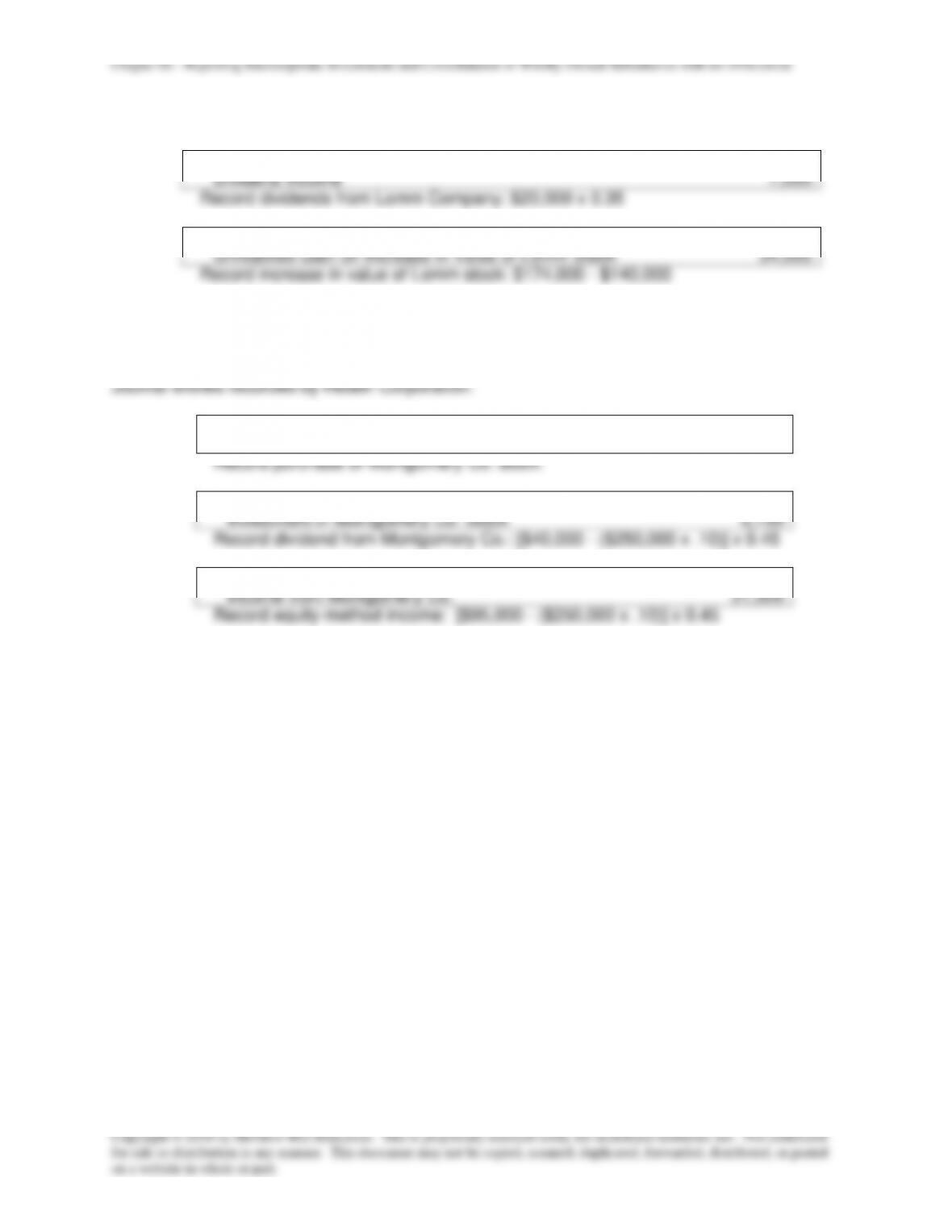

(2)

Cash

7,000

Investment in Lomm Company Stock

7,000

Record dividends from Lomm Company: $20,000 x 0.35

(3)

Investment in Lomm Company Stock

28,000

Income from Lomm Company

28,000

Record equity-method income: $80,000 x 0.35

(1)

Investment in Lomm Company Stock

140,000

Cash

140,000

Record purchase of Lomm Company stock.

(2)

Cash

7,000

Dividend Income

7,000

Record dividends from Lomm Company: $20,000 x 0.35

(3)

Investment in Lomm Company Stock

34,000

Unrealized Gain on Increase in Value of Lomm Stock

34,000

Record increase in value of Lomm stock: $174,000 – $140,000

E2–11A Investee with Preferred Stock Outstanding

(1)

Investment in Montgomery Co. Stock

288,000

Cash

288,000

Record purchase of Montgomery Co. stock.

(2)

Cash

6,750

Investment in Montgomery Co. Stock

6,750

Record dividend from Montgomery Co.: [$40,000 – ($250,000 x .10)] x 0.45

(3)

Investment in Montgomery Co. Stock

31,500

Income from Montgomery Co.

31,500

Record equity-method income: [$95,000 – ($250,000 x .10)] x 0.45

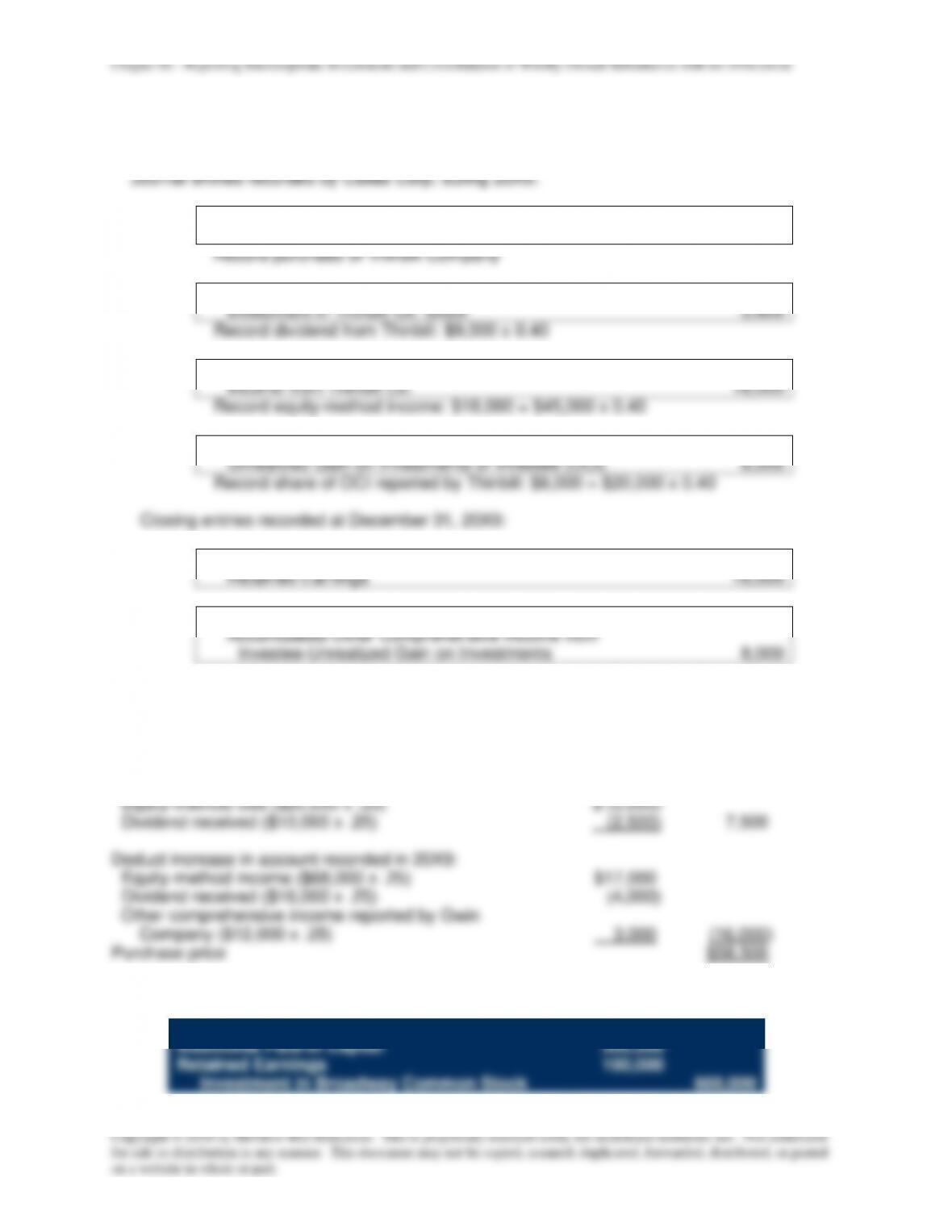

E2–12A Other Comprehensive Income Reported by Investee

(1)

Investment in Thinbill Co. Stock

380,000

Cash

380,000

Record purchase of Thinbill Company

(2)

Cash

3,600

Investment in Thinbill Co. Stock

3,600

Record dividend from Thinbill: $9,000 x 0.40

(3)

Investment in Thinbill Co. Stock

18,000

Income from Thinbill Co.

18,000

Record equity-method income: $18,000 = $45,000 x 0.40

(4)

Investment in Thinbill Co. Stock

8,000

Unrealized Gain on Investments of Investee (OCI)

8,000

Record share of OCI reported by Thinbill: $8,000 = $20,000 x 0.40

Closing entries recorded at December 31, 20X9:

(5)

Income from Thinbill Co.

18,000

Retained Earnings

18,000

(6)

Unrealized Gain on Investments of Investee (OCI)

8,000

Accumulated Other Comprehensive Income from

Investee-Unrealized Gain on Investments

8,000

E2–13A Other Comprehensive Income Reported by Investee

Investment account balance reported by Baldwin Corp.

$67,000

Add decrease in account recorded in 20X8:

Equity-method loss ($20,000 x .25)

$ (5,000)

Dividend received ($10,000 x .25)

(2,500)

7,500

Deduct increase in account recorded in 20X9:

Equity-method income ($68,000 x .25)

$17,000

Dividend received ($16,000 x .25)

(4,000)

Other comprehensive income reported by Gwin

Company ($12,000 x .25)

3,000

(16,000)

Purchase price

$58,500

E2-14 Basic Consolidation Entry

Common Stock – Broadway Corporation

200,000

Additional Paid-In Capital

300,000

Retained Earnings

100,000

Investment in Broadway Common Stock

600,000

E2-15 Balance Sheet Worksheet

a.

Equity Method Entries on Blank’s Books:

Investment in Faith

150,000

Cash

150,000

Record the initial investment in Faith

12/31/X2

Goodwill = 0

Identifiable

excess = 0

$150,000

Initial

investment in

Faith

Book value =

CS + RE =

150,000

Book Value Calculations:

Total

Book Value

=

Common

Stock

+

Retained

Earnings

Ending book value

150,000

60,000

90,000

Basic Consolidation Entry

Common stock

60,000

Retained earnings

90,000

Investment in Faith

150,000

Optional accumulated depreciation consolidation entry

Accumulated depreciation

30,000

Buildings & equipment

30,000

(Since the buildings and equipment are reported net of accumulated depreciation on the

balance sheet, this entry will not affect the worksheet. However, if sufficient information had

been given, this entry would have made a difference in the worksheet balances for Buildings

and Equipment and Accumulated Depreciation. Additionally, this entry would impact any

footnote disclosure of the details of Buildings and Equipment.)

E2-15 (continued)

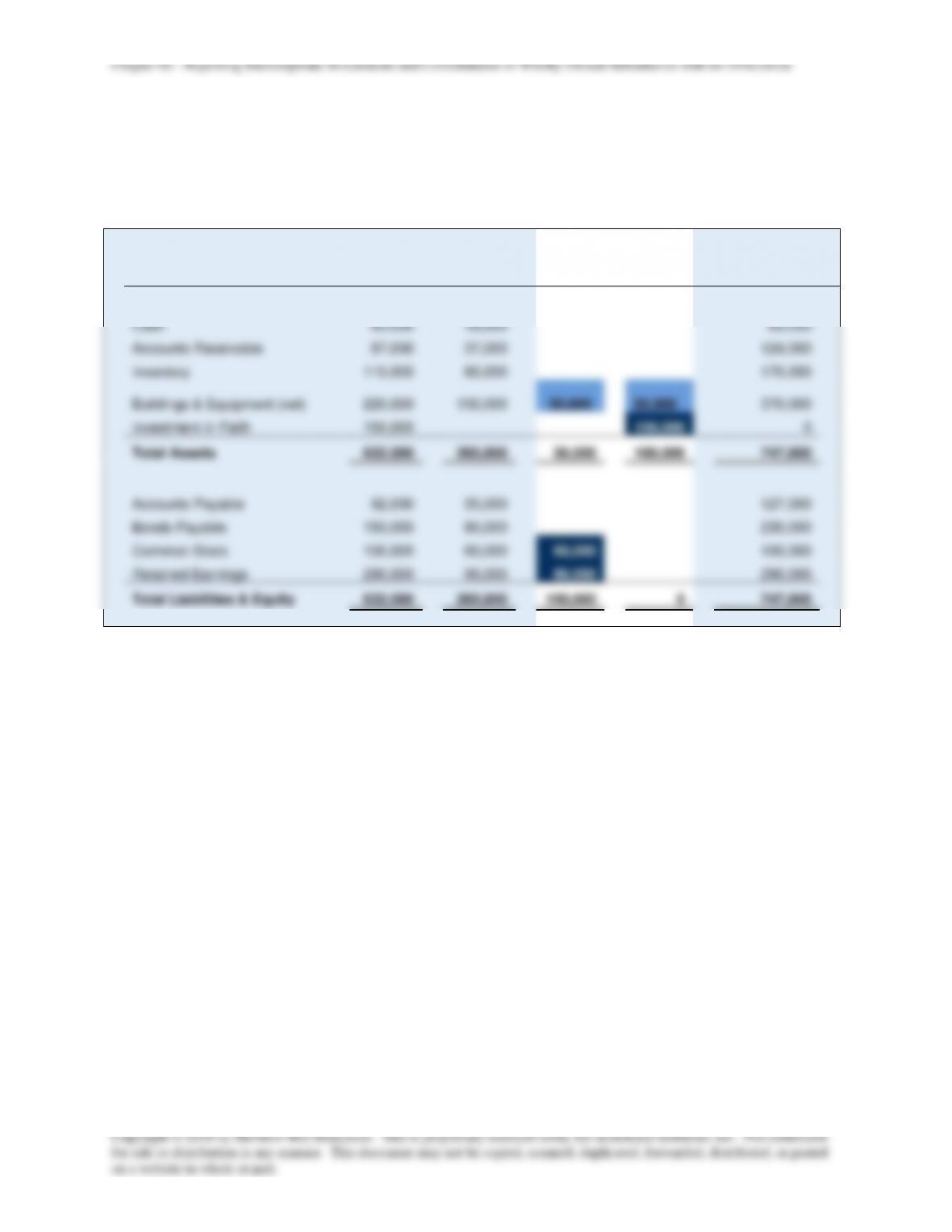

b.

Blank

Faith

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

65,000

18,000

83,000

Accounts Receivable

87,000

37,000

124,000

Inventory

110,000

60,000

170,000

Buildings & Equipment (net)

220,000

150,000

30,000

30,000

370,000

Investment in Faith

150,000

150,000

0

Total Assets

632,000

265,000

30,000

180,000

747,000

Accounts Payable

92,000

35,000

127,000

Bonds Payable

150,000

80,000

230,000

Common Stock

100,000

60,000

60,000

100,000

Retained Earnings

290,000

90,000

90,000

290,000

Total Liabilities & Equity

632,000

265,000

150,000

0

747,000

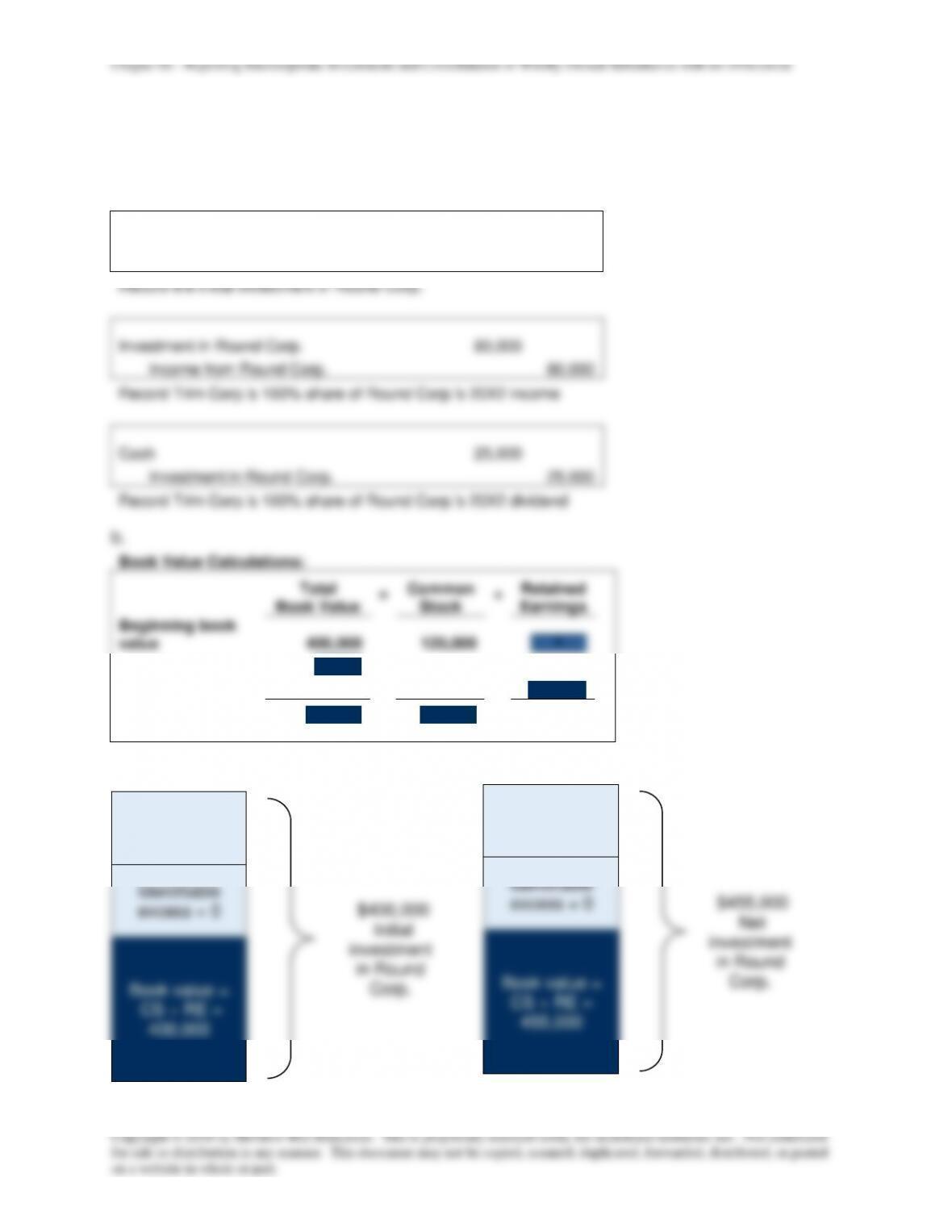

E2-16 Consolidation Entries for Wholly Owned Subsidiary

a.

Equity Method Entries on Trim Corp.’s Books:

Investment in Round Corp.

400,000

Cash

400,000

Record the initial investment in Round Corp.

Investment in Round Corp.

80,000

Income from Round Corp.

80,000

Record Trim Corp.’s 100% share of Round Corp.’s 20X2 income

Cash

25,000

Investment in Round Corp.

25,000

Record Trim Corp.’s 100% share of Round Corp.’s 20X2 dividend

Book Value Calculations:

Total

Book Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

400,000

120,000

280,000

+ Net Income

80,000

80,000

– Dividends

(25,000)

(25,000)

Ending book value

455,000

120,000

335,000

1/1/X2

Goodwill = 0

Identifiable

excess = 0

$400,000

Initial

investment

in Round

Corp.

Book value =

CS + RE =

400,000

12/31/X2

Goodwill = 0

Identifiable

excess = 0

$455,000

Net

investment

in Round

Corp.

Book value =

CS + RE =

455,000