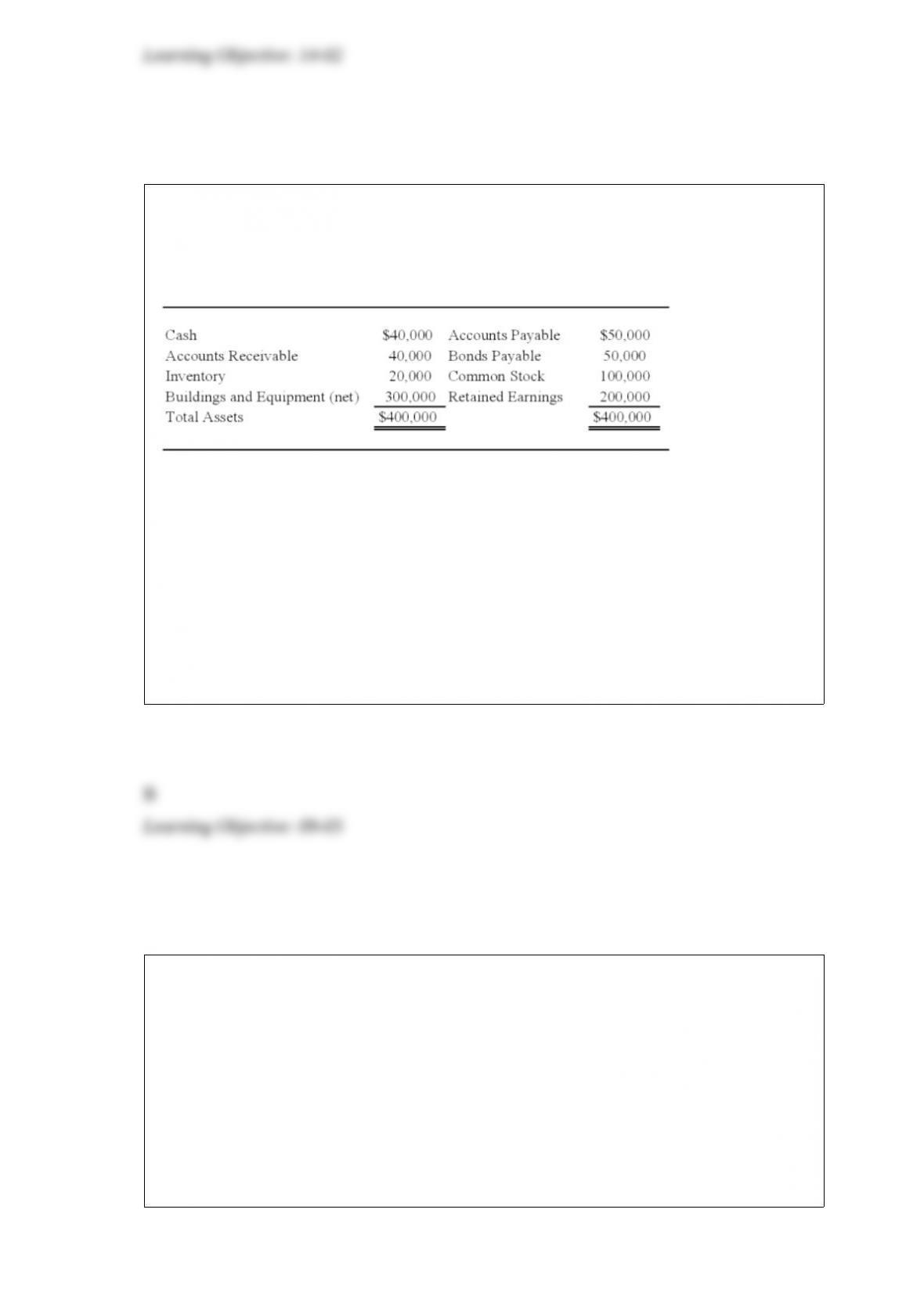

A private, not-for-profit hospital received a contribution of $40,000 on June 15, 20X8.

The donor restricted the contribution to funding research activities currently being

performed by the hospital. For the year ended December 31, 20X8, the hospital spent

$30,000 of the contribution on research activities. The hospital expended the remaining

$10,000 on research activities in January of 20X9.

Refer to the above information. On the statement of operations prepared for the year

ended December 31, 20X8, the events described would:

A. increase operating income by $30,000.

B. have no effect on operating income.

C. increase unrestricted net assets by $30,000.

D. decrease unrestricted net assets by $30,000.

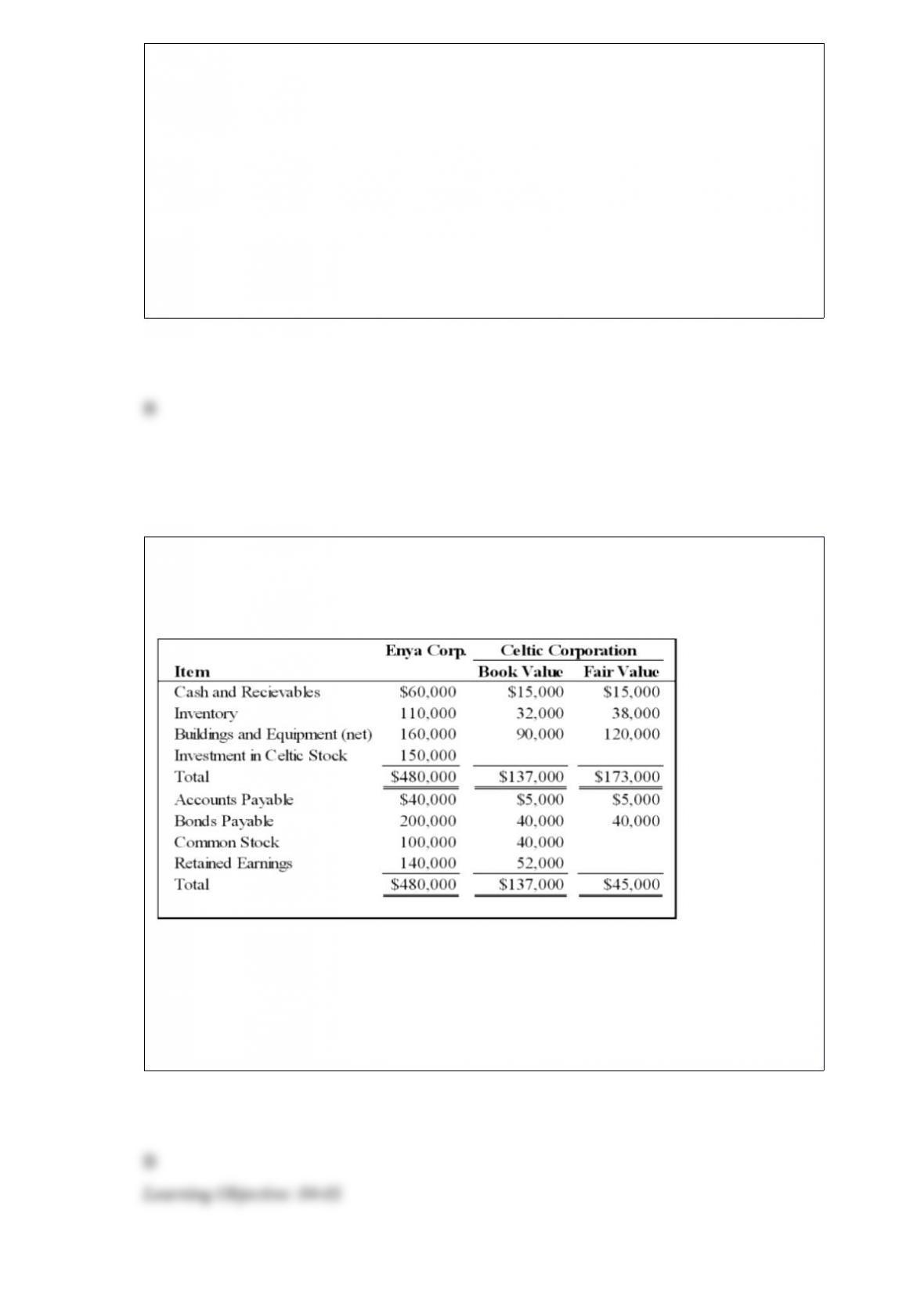

Enya Corporation acquired 100 percent of Celtic Corporation’s common stock on

January 1, 20X9. Summarized balance sheet information for the two companies

immediately after the combination is provided:

Based on the preceding information, the amount of differential associated with the

acquisition is:

A. $0.

B. $58,000.

C. $22,000.

D. $36,000.

Denver Corporation owns 25 percent of the voting shares of Alamos Corporation. In

20X8, Alamos reported net income of $120,000 and paid dividends of $30,000. Denver

uses the equity method to account for this investment. Denver reported taxable income

of $160,000 on its separate operations and has an effective tax rate of 40 percent. There

is an 80 percent exemption on intercompany dividends.

Based on the preceding information, income tax expense for Denver for the year 20X8

will be:

A. $67,000

B. $64,600

C. $64,000

D. $66,400

All of the following are management tools available for a U.S. company to hedge its net

investment in a foreign affiliate except for:

A. Forward exchange contracts

B. Foreign currency commitments

C. Intercompany financing arrangements including intercompany transactions

D. None of the above.

On January 1, 20X6, Climber Corporation acquired 90 percent of Wisden Corporation

for $180,000 cash. Wisden reported net income of $30,000 and dividends of $10,000

for 20X6, 20X7, and 20X8. On January 1, 20X6, Wisden reported common stock

outstanding of $100,000 and retained earnings of $60,000, and the fair value of the

noncontrolling interest was $20,000. It held land with a book value of $30,000 and a

market value of $35,000 and equipment with a book value of $50,000 and a market

value of $60,000 at the date of combination. The remainder of the differential at

acquisition was attributable to an increase in the value of patents, which had a

remaining useful life of five years. All depreciable assets held by Wisden at the date of

acquisition had a remaining economic life of five years. Climber uses the equity method

in accounting for its investment in Wisden.

Based on the preceding information, the increase in the fair value of patents held by

Wisden is:

A. $20,000

B. $25,000

C. $15,000

D. $5,000

Regulation S-X presents the rules for preparing all of the following except:

A. financial statements.

B. footnotes.

C. auditor’s report.

D. management’s discussion.

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. David directly purchases a one-fifth interest

by paying Allen $34,000 and Daniel $10,000. The land account is increased before

David is admitted. By what amount is the land account increased?

A. $40,000

B. $10,000

C. $36,000

D. $20,000

Aaron, a holder of a $200,000 Xenon Inc. bond, collected the interest due on June 30,

20X2, and then sold the bond to Dolphin Inc. for $185,000. On that date the bond

issuer, Xenon, an 80 percent owner of Dolphin, had a $220,000 carrying amount for this

bond.

Based on the information given above, what amount of gain or loss on bond retirement

was recorded during the consolidation process?

A. No gain or loss

B. $35,000 loss

C. $35,000 gain

D. $15,000 loss

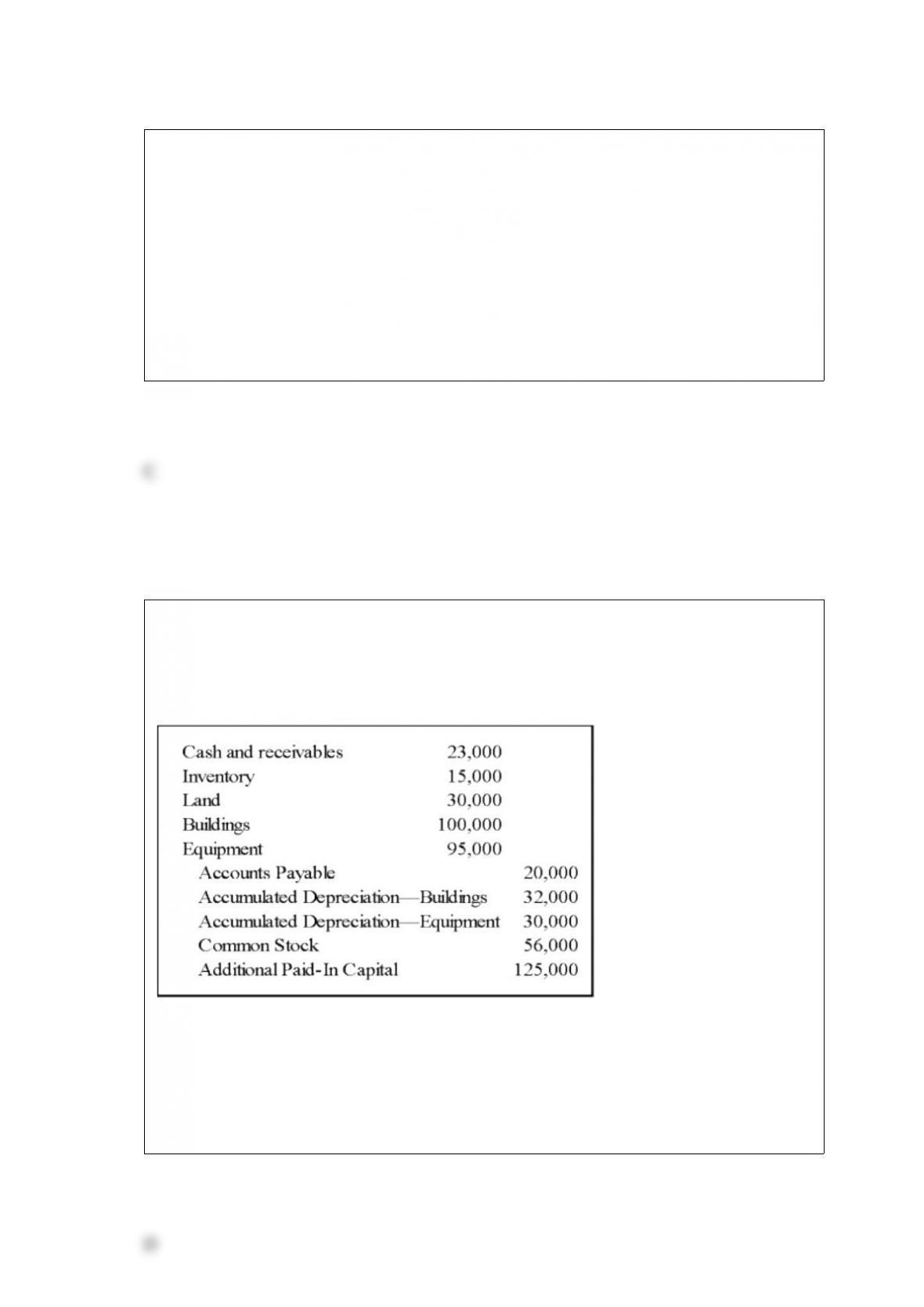

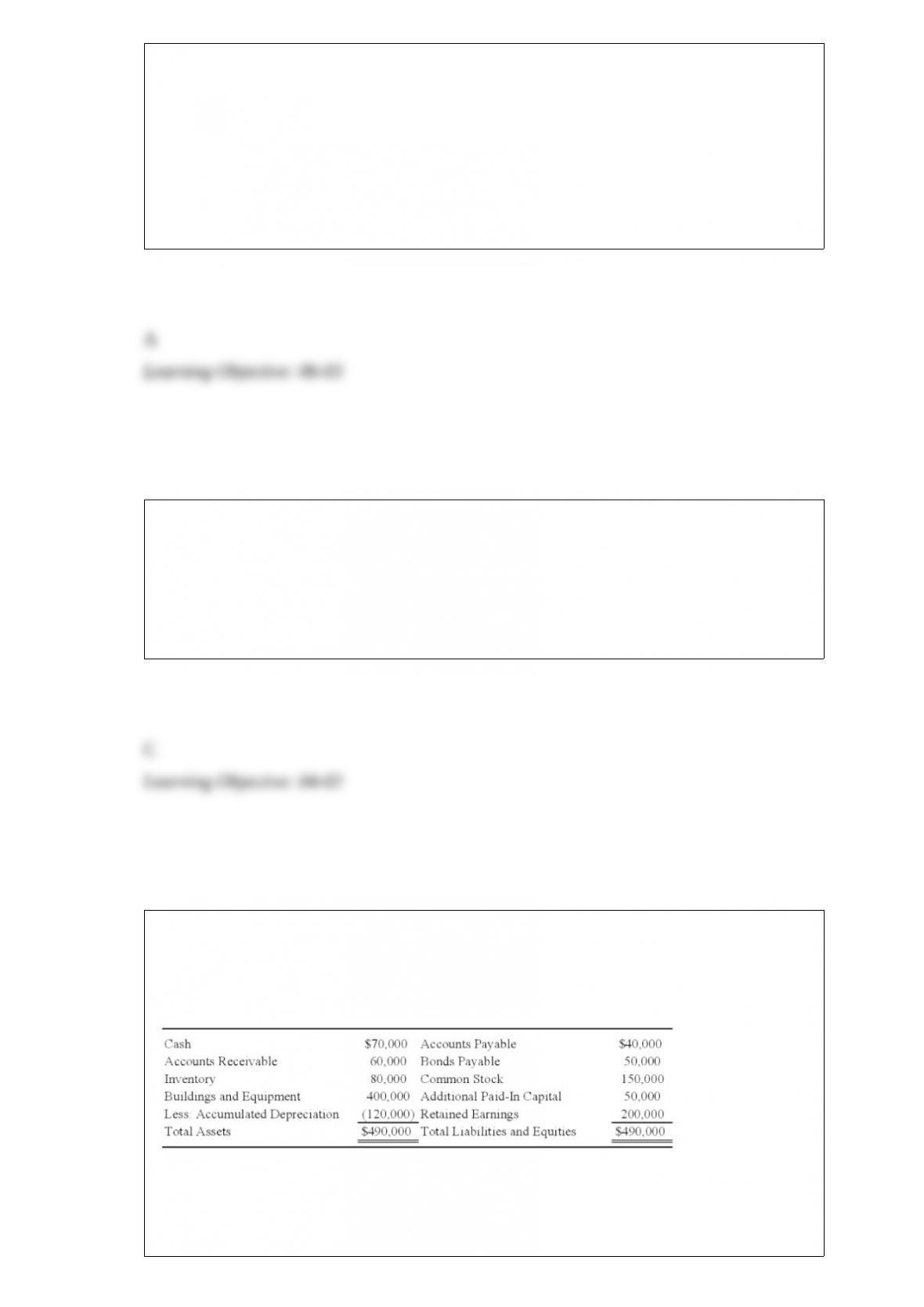

In order to reduce the risk associated with a new line of business, Conservative

Corporation established Spin Company as a wholly owned subsidiary. It transferred

assets and accounts payable to Spin in exchange for its common stock. Spin recorded

the following entry when the transaction occurred:

Based on the preceding information, what was Conservative’s book value of assets

transferred to Spin Company?

A. $243,000

B. $263,000

C. $221,000

D. $201,000

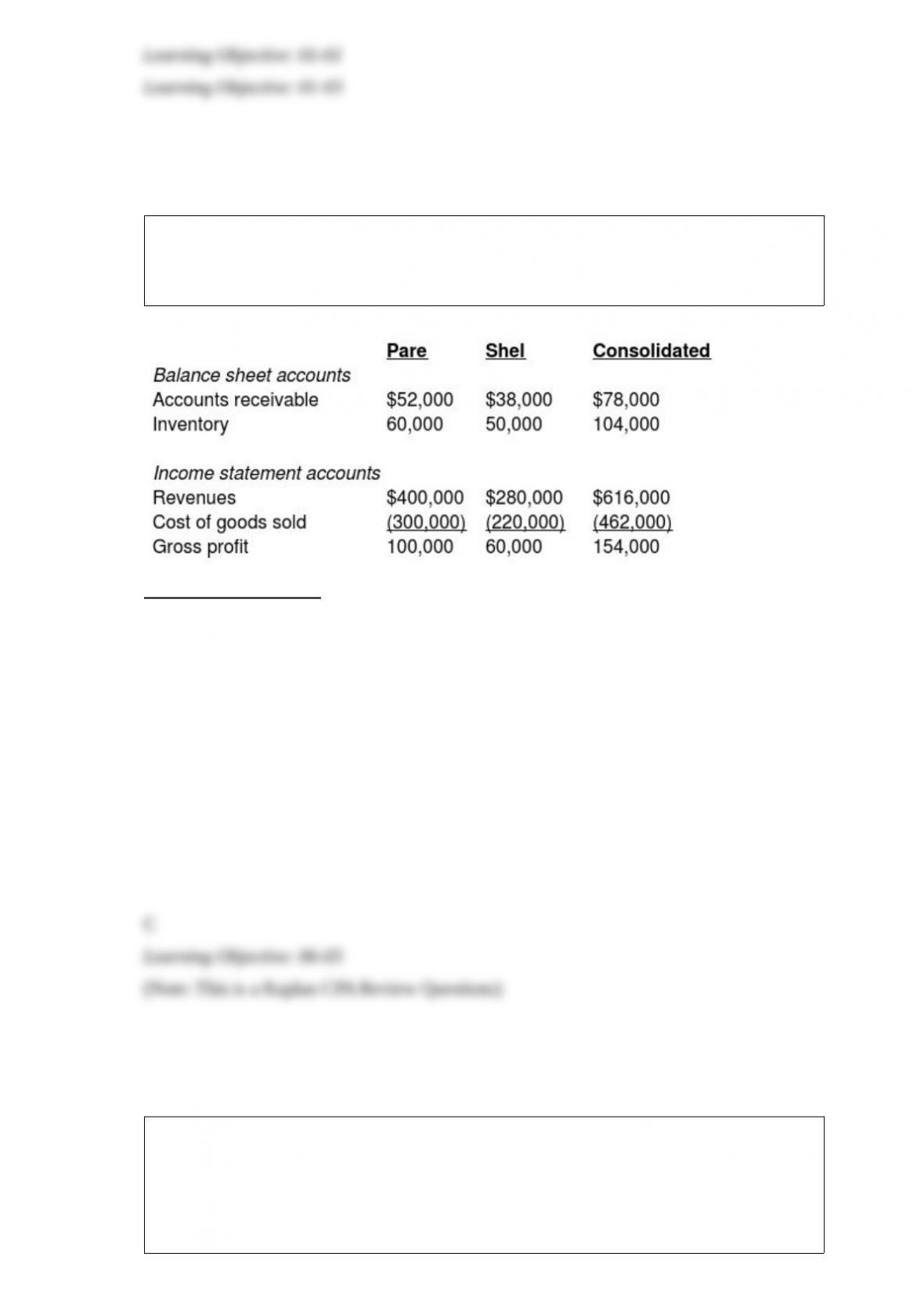

Selected information from the separate and consolidated balance sheets and income

statements of Pare, Inc. and its subsidiary, Shel Co., as of December 31, 20X5, and for

the year then ended is as follows:

Additional information:

During 20X5, Pare sold goods to Shel at the same markup on cost that Pare uses for all

sales.

What was the amount of intercompany sales from Pare to Shel during 20X5?

A. $12,000

B. $6,000

C. $64,000

D. $58,000

On January 1, 20X8, Parent Company acquired 90 percent ownership of Subsidiary

Corporation, at underlying book value. The fair value of the noncontrolling interest at

the date of acquisition was equal to 10 percent of the book value of Subsidiary

Corporation. On Mar 17, 20X8, Subsidiary purchased inventory from Parent for

$90,000. Subsidiary sold the entire inventory to an unaffiliated company for $120,000

on November 21, 20X8. Parent had produced the inventory sold to Subsidiary for

$62,000. The companies had no other transactions during 20X8.

Based on the information given above, what amount of cost of goods sold will be

reported in the 20X8 consolidated income statement?

A. $62,000

B. $120,000

C. $90,000

D. $58,000

When a parent company uses the equity method to account for investments, the

controlling interest in consolidated net income includes all of the following except:

A. The parent’s income from its own operations.

B. The parent company’s share of income from consolidated subsidiaries.

C. The non-controlling interest’s share of income from consolidated subsidiaries.

D. Differential adjustments

Lemon Corporation acquired 80 percent of Bricks Corporation’s common shares on

January 1, 20X7, at underlying book value. At that date, the fair value of the

noncontrolling interest was equal to 20 percent of the book value of Bricks Corporation.

Bricks prepared the following balance sheet as of December 31, 20X8:

On January 1, 20X9, Bricks declares a stock dividend of 9,000 shares on its $5 par

value common stock. The current market price per share of Bricks stock on January 1,

20X9, is $20.

Based on the preceding information, the investment elimination entry required to

prepare a consolidated balance sheet immediately after the stock dividend is issued will

include a debit to Retained Earnings for:

A. $200,000

B. $65,000

C. $155,000

D. $20,000

Which of the following statement is true regarding permanent funds?

A. Permanent funds do not have any donor restrictions when they are established.

B. Permanent funds have a donor restriction on the fund principal but the income from

the fund may be used to benefit the government’s program.

C. Permanent funds have a donor restriction on the income generated from the fund

principal but the principal may be used to benefit the government’s program

D. The cash or accrual basis of accounting may be used to account for a permanent

fund.

Based on the preceding information, what amount will be reported by the company as

cash payments to suppliers for 20X5?

A. $325,000

B. $333,000

C. $358,000

D. $367,000

Neptune Corporation owns 70 percent of Pluto Company’s stock. On July 1, 20X4,

Neptune sold a piece of equipment to Pluto for $56,350. Neptune had purchased this

equipment on January 1, 20X1, for $63,000. The equipment’s original 15-year

estimated total economic life remains unchanged. Both companies use straight-line

depreciation. The equipment’s residual value is considered negligible.

Based on the information provided, while preparing the 20X4 consolidated income

statement, depreciation expense will be

A. credited for $350 in the consolidation entries.

B. debited for $350 in the consolidation entries.

C. credited for $700 in the consolidation entries.

D. debited for $700 in the consolidation entries.

The following information pertains to Sundown’s water and sewer fund, an enterprise

fund, for the year ended June 30, 20X0:

Operating revenues $840,000

Operating expenses—excluding depreciation 610,000

Depreciation expense 50,000

Supplies Inventory 10,000

Cash 130,000

Based upon the information presented, what was the increase in the enterprise fund’s

unrestricted net assets for the fiscal year ended June 30, 20X0?

A. $320,000

B. $310,000

C. $230,000

D. $180,000

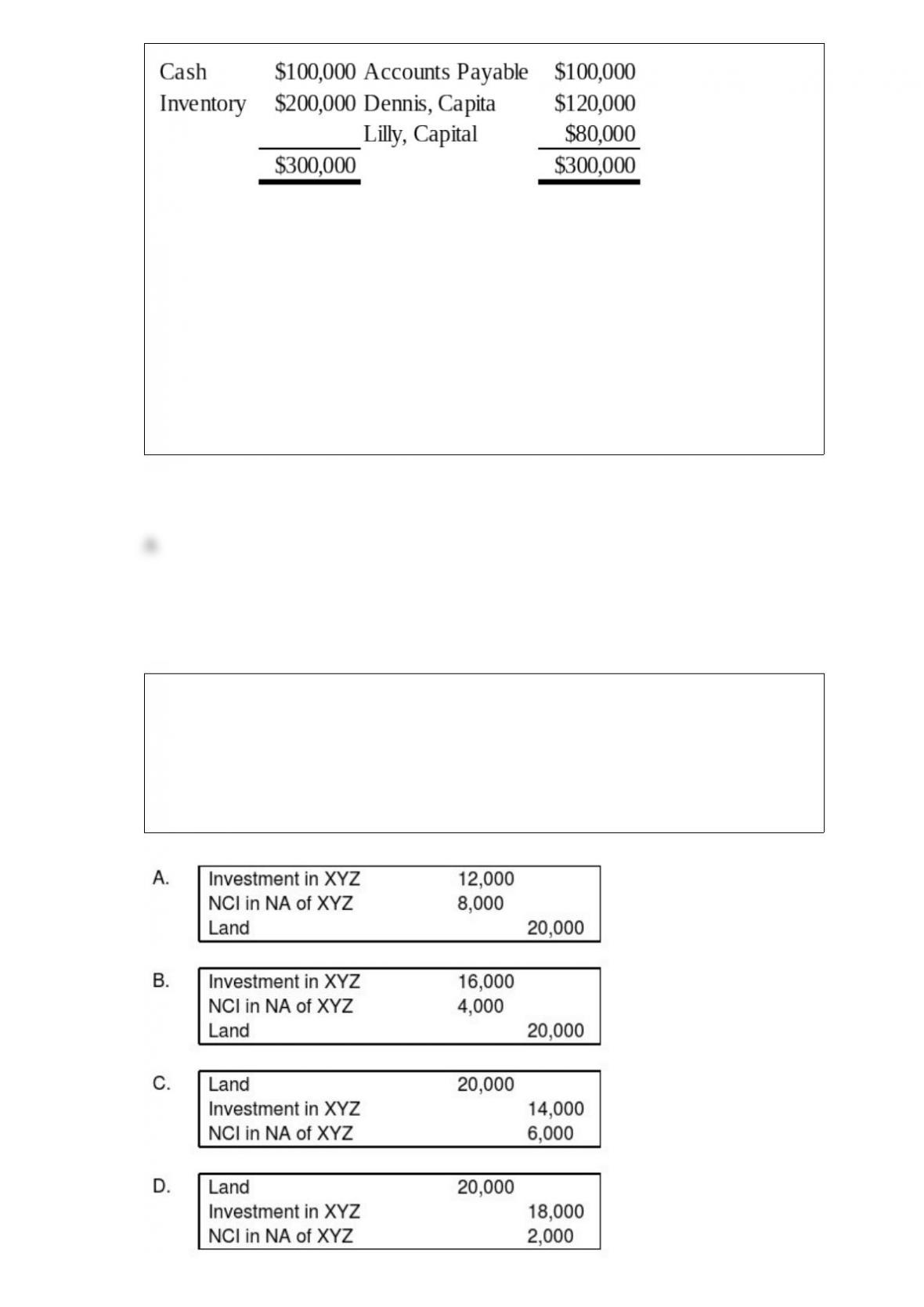

Partners Dennis and Lilly have decided to liquidate their business. The following

information is available:

Dennis and Lilly share profits and losses in a 3:2 ratio. During the first month of

liquidation, half the inventory is sold for $60,000, and $60,000 of the accounts payable

is paid. During the second month, the rest of the inventory is sold for $45,000, and the

remaining accounts payable are paid. Cash is distributed at the end of each month, and

the liquidation is completed at the end of the second month.

Refer to the information provided above. Using a safe payments schedule, how much

cash will be distributed to Lilly at the end of the first month?

A. $24,000

B. $40,000

C. $16,000

D. $64,000

ABC Corporation purchased land on January 1, 20X6, for $50,000. On July 15, 20X8,

it sold the land to its subsidiary, XYZ Corporation, for $70,000. ABC owns 80 percent

of XYZ’s voting shares.

Which worksheet consolidating entry will be made on December 31, 20X9, if XYZ

Corporation had initially purchased the land for $50,000 and then sold it to ABC on

July 15, 20X8, for $70,000?

A. Option A

B. Option B

C. Option C

D. Option D

On January 1, 20X8, Gulfstream Corporation acquired 40 percent of the voting shares

of Hunter Company for $65,000. Hunter reported net income of $45,000 and paid

dividends of $10,000 in 20X8. Gulfstream reported operating income of $50,000 for the

year. There is 80 percent exemption of intercompany dividends and the effective tax

rate is 35 percent. Assume that the equity method is being used.

Based on the preceding information, what would Gulfstream report as income tax

expense for the year?

A. $17,500

B. $18,760

C. $23,800

D. $22,540

Which of the following best describes a “red herring” prospectus?

A. A shortened version of registration Form S-1 available to those companies that

already have publicly traded securities.

B. A prospectus containing material irregularities and deficiencies.

C. Preliminary information provided to investors about an upcoming issue, and issued

between the time a registration statement is presented to the SEC and its effective date.

D. Disclosure in the business press, outlined in red, informing investors of an upcoming

offering.

Vision Corporation acquired 75 percent of the stock of Meta Company on January 1,

20X7, for $225,000. At that date, the fair value of the noncontrolling interest was

$75,000. Meta’s balance sheet contained the following amounts at the time of the

combination:

During each of the next three years, Meta reported net income of $30,000 and paid

dividends of $10,000. On January 1, 20X9, Vision sold 1,500 shares of Meta’s $10 par

value shares for $60,000 in cash. Vision used the fully adjusted equity method in

accounting for its ownership of Meta Company.

Based on the preceding information, in the journal entry recorded by Vision for sale of

shares:

A. Cash will be credited for $60,000.

B. Investment in Meta Stock will be credited for $51,000.

C. Investment in Meta Stock will be credited for $60,000.

D. Additional Paid-in Capital will be credited for $45,000.

Derby Company pays its executives a bonus of 6 percent of income before deducting

the bonus and income taxes. For the quarter ended March 31, 20X8, Derby had income

before the bonus and income tax of $12,000,000. For the year ended December 31,

20X8, Derby estimates that its income before bonus and income taxes will be

$70,000,000. For the quarter ended March 31, 20X8, what is the amount of the bonus

that Derby should deduct on its income statement?

A. $4,200,000

B. $720,000

C. $1,050,000

D. $180,000

Tower Corporation’s controller has just finished preparing a consolidated balance sheet,

income statement, and statement of changes in retained earnings for the year ended

December 31, 20X9. Tower owns 80 percent of Network Corporation’s stock, which it

acquired at underlying book value on November 1, 20X6. At that date, the fair value of

the noncontrolling interest was equal to 20 percent of Network Corporation’s book

value. The following information is available:

Consolidated net income for 20X9 was $160,000.

Network reported net income of $50,000 for 20X9.

Tower paid dividends of $30,000 in 20X9.

Network paid dividends of $10,000 in 20X9.

Tower issued common stock on February, 18, 20X9, for a total of $100,000.

Consolidated wages payable decreased by $6,000 in 20X9.

Consolidated depreciation expense for the year was $15,000.

Consolidated accounts receivable decreased by $20,000 in 20X9.

Bonds payable of Tower with a book value of $102,000 were retired for $100,000 on

December 31, 20X9.

Consolidated amortization expense on patents was $10,000 for 20X9.

Tower sold land that it had purchased for $75,000 to a nonaffiliate for $80,000 on June

10, 20X9.

Consolidated accounts payable decreased by $7,000 during 20X9.

Total purchases of equipment by Tower and Network during 20X9 were $180,000.

Consolidated inventory increased by $36,000 during 20X9.

There were no intercompany transfers between Tower and Network in 20X9 or prior

years except for Network’s payment of dividends. Tower uses the indirect method in

preparing its cash flow statement.

Based on the preceding information, what was the change in cash balance for the

consolidated entity for 20X9?

A. Increase of $49,000

B. Decrease of $66,000

C. Increase of $17,000

D. Increase of $32,000

Rivendell Corporation and Foster Company merged as of January 1, 20X9. To effect the

merger, Rivendell paid finder’s fees of $40,000, legal fees of $13,000, audit fees related

to the stock issuance of $10,000, stock registration fees of $5,000, and stock listing

application fees of $4,000.

Based on the preceding information, under the acquisition method, what amount

relating to the business combination would be expensed?

A. $72,000

B. $19,000

C. $53,000

D. $63,000

Proxy statements are:

A. filed by an entity that acquires a beneficial ownership of more than 5 percent in a

company.

B. interim financial statements need not be audited.

C. materials submitted to shareholders for votes on corporate matters.

D. used to disclose unscheduled material events.

Pilfer Company acquired 90 percent ownership of Scrooge Corporation in 20X7, at

underlying book value. On that date, the fair value of noncontrolling interest was equal

to 10 percent of the book value of Scrooge Corporation. Pilfer purchased inventory

from Scrooge for $90,000 on August 20, 20X8, and resold 70 percent of the inventory

to unaffiliated companies on December 1, 20X8, for $100,000. Scrooge produced the

inventory sold to Pilfer for $67,000. The companies had no other transactions during

20X8.

Based on the information given above, what amount of sales will be reported in the

20X8 consolidated income statement?

A. $90,000

B. $120,000

C. $100,000

D. $67,000

Lemon Corporation acquired 80 percent of Bricks Corporation’s common shares on

January 1, 20X7, at underlying book value. At that date, the fair value of the

noncontrolling interest was equal to 20 percent of the book value of Bricks Corporation.

Bricks prepared the following balance sheet as of December 31, 20X8:

On January 1, 20X9, Bricks declares a stock dividend of 9,000 shares on its $5 par

value common stock. The current market price per share of Bricks stock on January 1,

20X9, is $20.

Begin with information provided, but assume instead that Bricks declared a stock

dividend of 3,000 shares on its $5 par value common stock. The investment elimination

entry required to prepare a consolidated balance sheet immediately after the stock

dividend is issued will include a debit to Additional Paid-In Capital for:

A. $65,000.

B. $95,000.

C. $50,000.

D. $110,000.

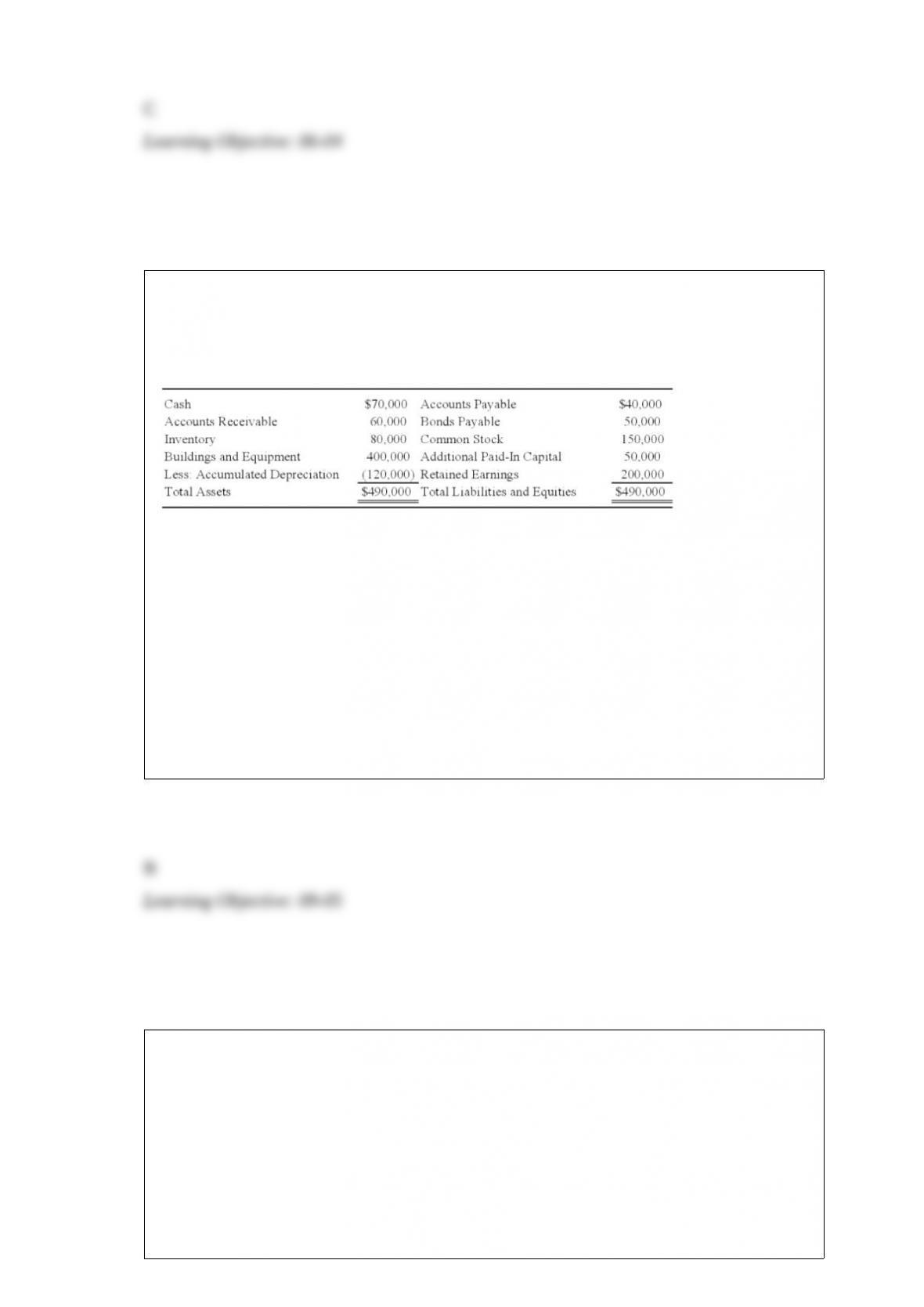

The general ledger of Covington contains the following selected account balances:

Appropriations Control $1,500,000

Reserve for Encumbrances 60,000

Vouchers Payable 80,000

Expenditures 830,000

Covington wants to order additional goods and services before the fiscal year end. What

is the unencumbered balance of the budget that may be expended by Covington?

A. $610,000

B. $670,000

C. $1,360,000

D. $1,440,000