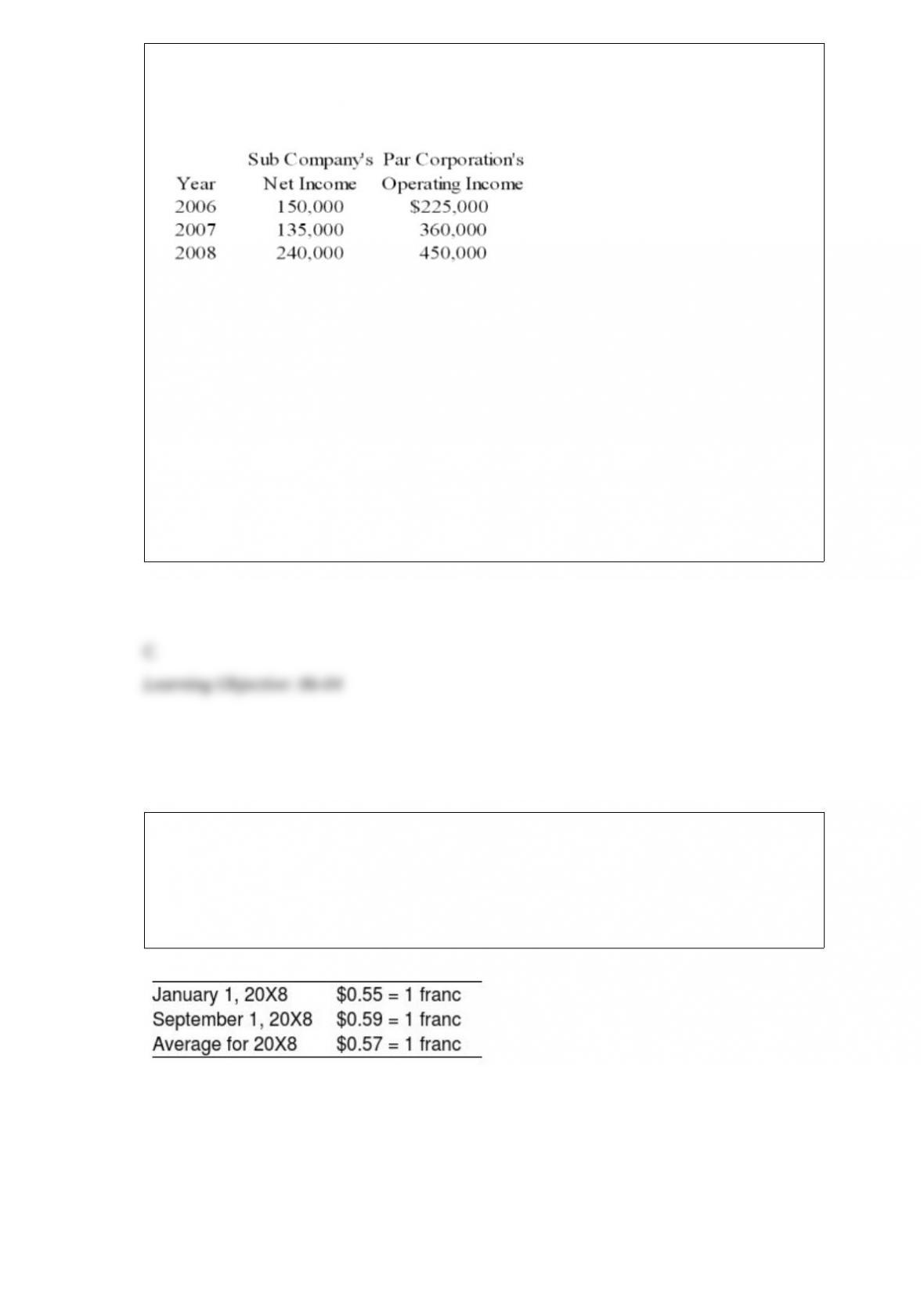

Sub Company sells all its output at 20 percent above cost to Par Corporation. Par

purchases its entire inventory from Sub. The incomes reported by the companies over

the past three years are as follows:

Sub Company sold inventory for $300,000, $262,500 and $337,500 in the years 20X6,

20X7, and 20X8 respectively. Par Company reported ending inventory of $105,000,

$157,500 and $180,000 for 20X6, 20X7, and 20X8 respectively. Par acquired 70

percent of the ownership of Sub on January 1, 20X6, at underlying book value. The fair

value of the noncontrolling interest at the date of acquisition was equal to 30 percent of

the book value of Sub Company.

Based on the information given above, what will be the consolidated net income for

20X7?

A. $495,000

B. $317,750

C. $486,250

D. $690,000

53. Elan, a U.S. corporation, completed the December 31, 20X8, foreign currency

translation of its 70 percent owned Swiss subsidiary’s trial balance using the current rate

method. The translation resulted in a debit adjustment of $25,000. The subsidiary had

reported net income of 800,000 Swiss francs for 20X8 and paid dividends of 50,000

Swiss francs on September 1, 20X8. The translation rates for the year were:

The January 1 balance of the Investment in the Swiss subsidiary account was $1,600,000.

Elan acquired its interest in the Swiss subsidiary at book value with no differential or

goodwill recorded at acquisition.

Elan’s Investment in Swiss subsidiary account at December 31, 20X8, is:

A. $1,881,050.

B. $1,916,050.

C. $1,923,950.

D. $2,051,500.

On January 1, 20X8, William Company acquired 30 percent of eGate Company’s

common stock, at underlying book value of $100,000. eGate has 100,000 shares of $2

par value, 5 percent cumulative preferred stock outstanding. No dividends are in

arrears. eGate reported net income of $150,000 for 20X8 and paid total dividends of

$72,000. William uses the equity method to account for this investment.

Based on the preceding information, what amount of investment income will William

Company report from its investment in eGate for the year?

A. $45,000

B. $42,000

C. $62,000

D. $35,000

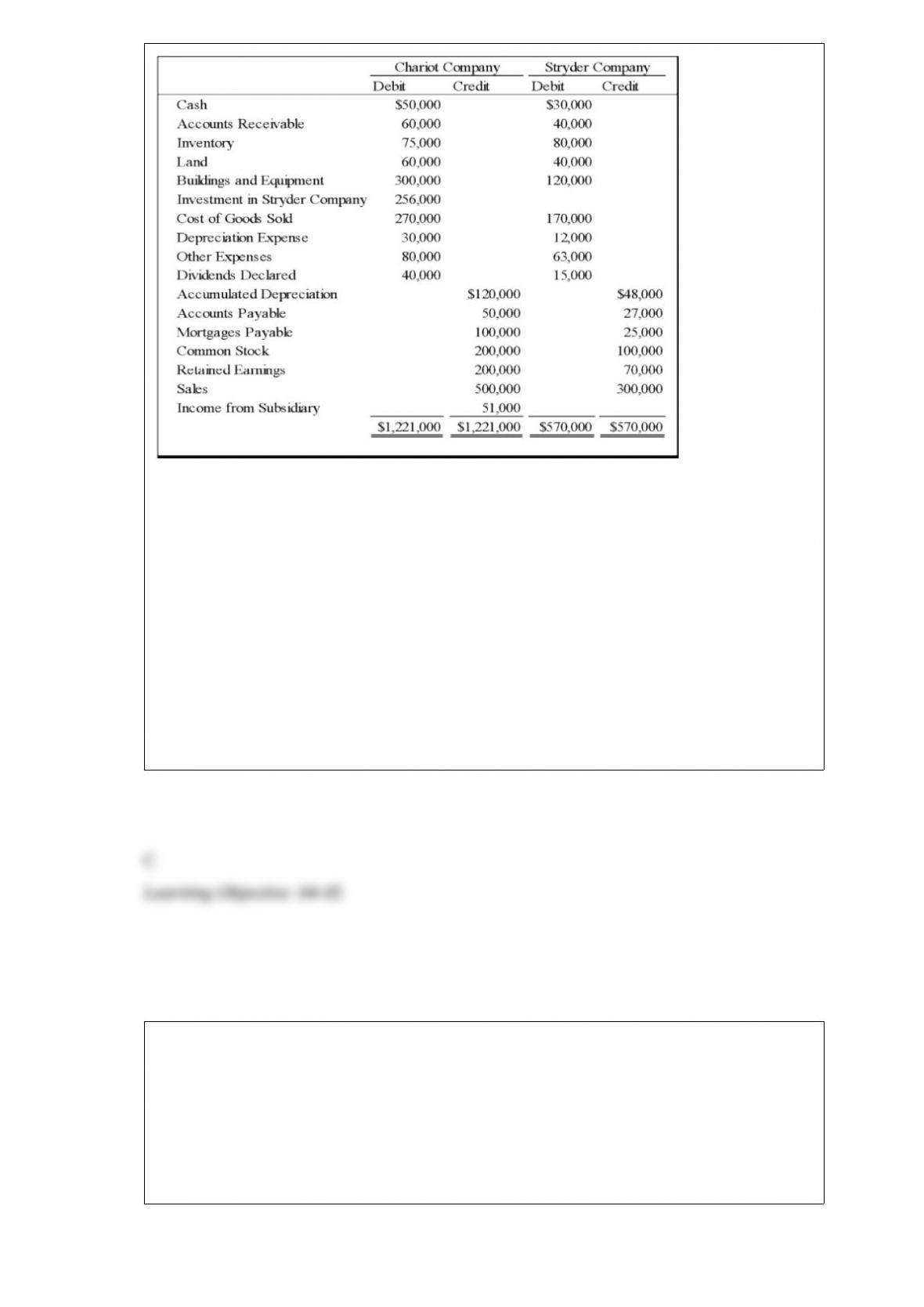

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder’s depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, what amount of total assets will be reported in the

consolidated balance sheet for the year?

A. $895,000

B. $801,000

C. $723,000

D. $1,111,000

In which of the following situations do accounting standards not require that the

financial statements of the parent and subsidiary be consolidated:

A. A corporation creates a new 100 percent owned subsidiary

B. A corporation purchases 90 percent of the voting stock of another company

C. A corporation has both control and majority ownership of an unincorporated

company

D. A corporation owns less-than a controlling interest in an unincorporated company

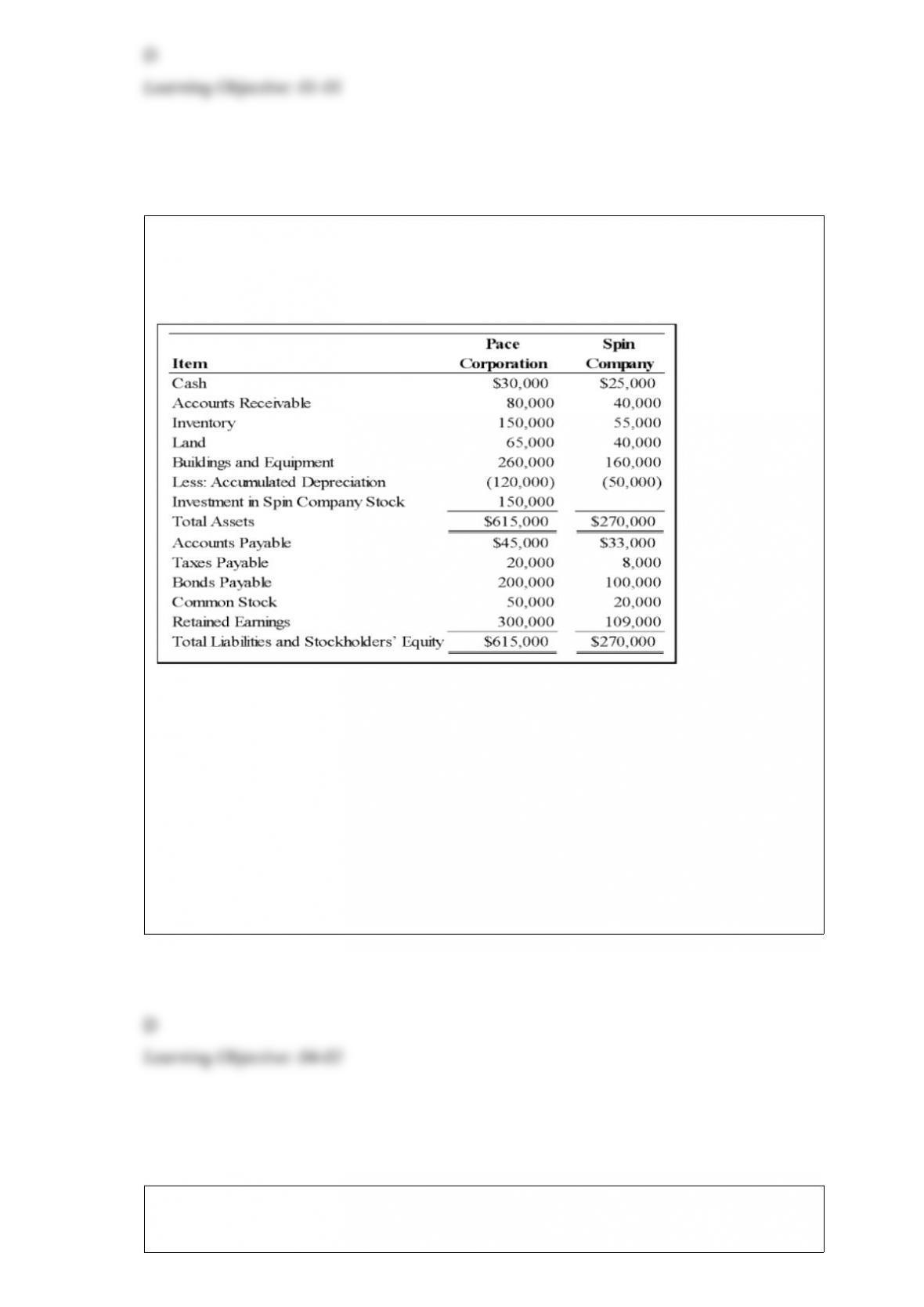

Pace Corporation acquired 100 percent of Spin Company’s common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, what amount of total stockholder’s equity will be

reported in the consolidated balance sheet prepared immediately after the business

combination?

A. $300,000

B. $479,000

C. $315,000

D. $350,000

On January 1, 20X7, Yang Corporation acquired 25 percent of the outstanding shares of

Spiel Corporation for $100,000 cash. Spiel Company reported net income of $75,000

and paid dividends of $30,000 for both 20X7 and 20X8. The fair value of shares held

by Yang was $110,000 and $105,000 on December 31, 20X7 and 20X8 respectively.

Based on the preceding information, what amount will be reported by Yang as income

from its investment in Spiel for 20X7 if it used the fair value option to account for its

investment in Spiel?

A. $17,500

B. $12,500

C. $11,250

D. $7,500

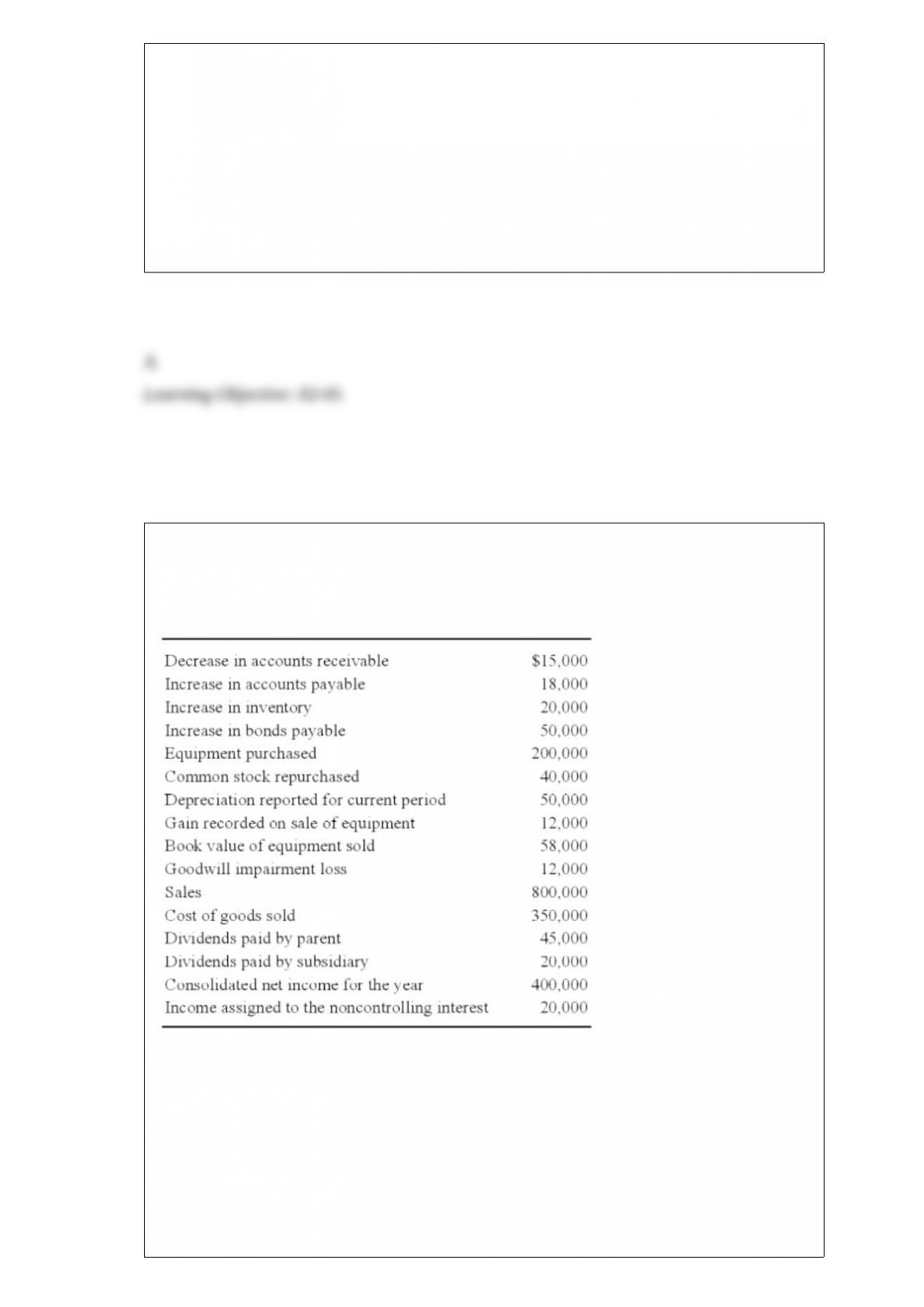

New Life Corporation has just finished preparing a consolidated balance sheet, income

statement, and statement of changes in retained earnings for 20X9. The following items

are proposed for inclusion in the consolidated cash flow statement:

New Life holds 75 percent of the voting stock of Shane Pharmaceuticals, acquired at

book value on June 21, 20X6. On the date of the acquisition, the fair value of the

noncontrolling interest was equal to 25 percent of the book value of Shane.

Based on the preceding information, what amount will be reported in the consolidated

cash flow statement as net cash provided by operating activities for 20X9?

A. $350,000

B. $463,000

C. $335,000

D. $421,000

The Canadian subsidiary of a U.S. company reported cost of goods sold of 50,000 C$,

for the current year ended December 31. The beginning inventory was 15,000 C$, and

the ending inventory was 10,000 C$. Spot rates for various dates are as follows:

Date beginning inventory was acquired $1.08 = 1C$

Rate at beginning of the year $1.10 = 1C$

Weighted average rate for the year $1.12 = 1C$

Date ending inventory was acquired $1.13 = 1C$

Assuming the Canadian dollar is the functional currency of the Canadian subsidiary, the

translated amount of cost of goods sold that should appear in the consolidated income

statement is

A. $50,000

B. $55,300

C. $56,000

D. $56,500

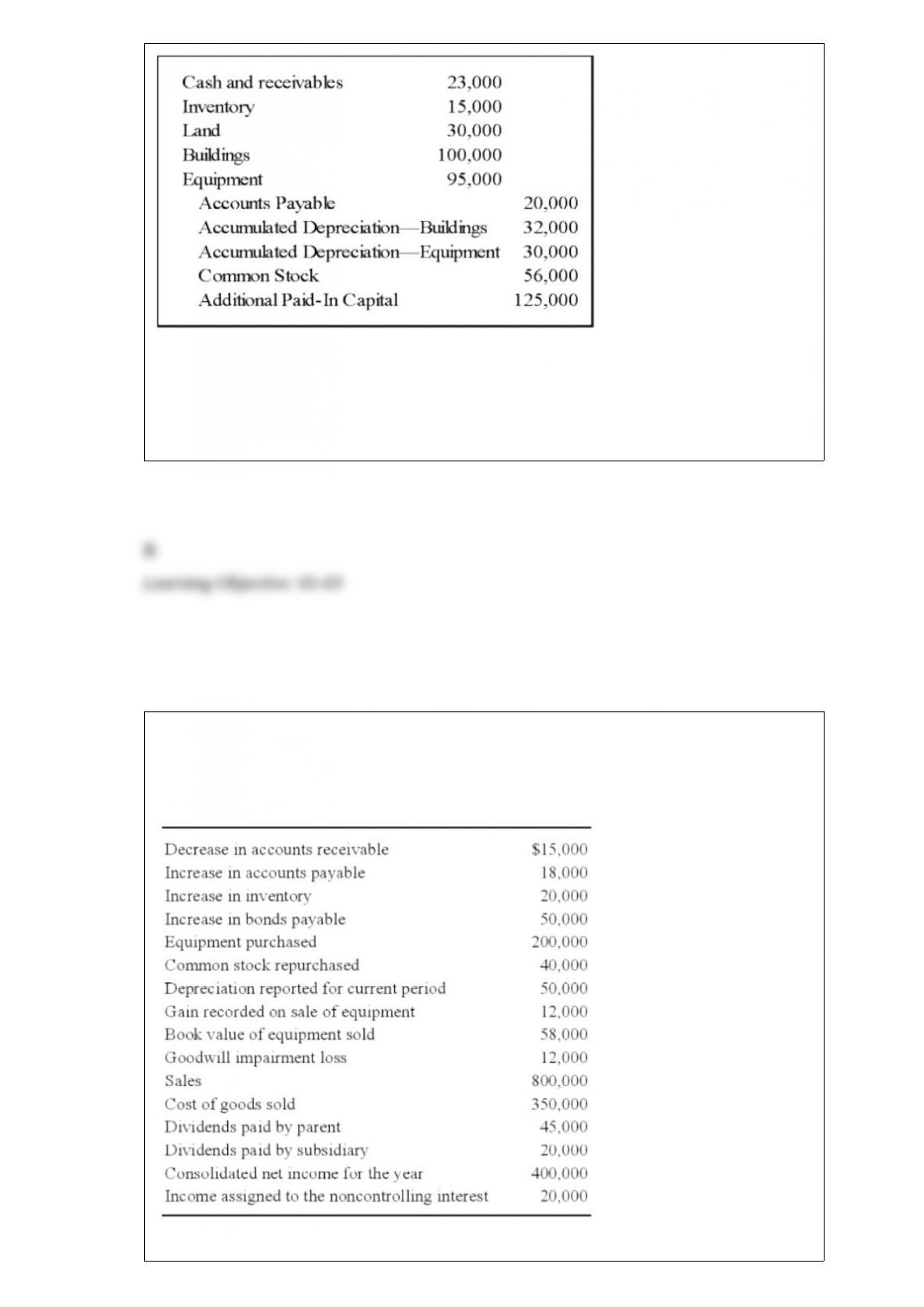

In order to reduce the risk associated with a new line of business, Conservative

Corporation established Spin Company as a wholly owned subsidiary. It transferred

assets and accounts payable to Spin in exchange for its common stock. Spin recorded

the following entry when the transaction occurred:

Based on the preceding information, immediately after the transfer,

A. Conservative’s total assets decreased by $23,000.

B. Conservative’s total assets decreased by $20,000.

C. Conservative’s total assets increased by $56,000.

D. Conservative’s total assets remained the same.

New Life Corporation has just finished preparing a consolidated balance sheet, income

statement, and statement of changes in retained earnings for 20X9. The following items

are proposed for inclusion in the consolidated cash flow statement:

New Life holds 75 percent of the voting stock of Shane Pharmaceuticals, acquired at

book value on June 21, 20X6. On the date of the acquisition, the fair value of the

noncontrolling interest was equal to 25 percent of the book value of Shane.

Based on the preceding information, assuming that New Life uses the direct method of

computing cash flows from operating activities, what amount will be reported by the

company as cash payments to suppliers for 20X9?

A. $350,000

B. $348,000

C. $312,000

D. $352,000

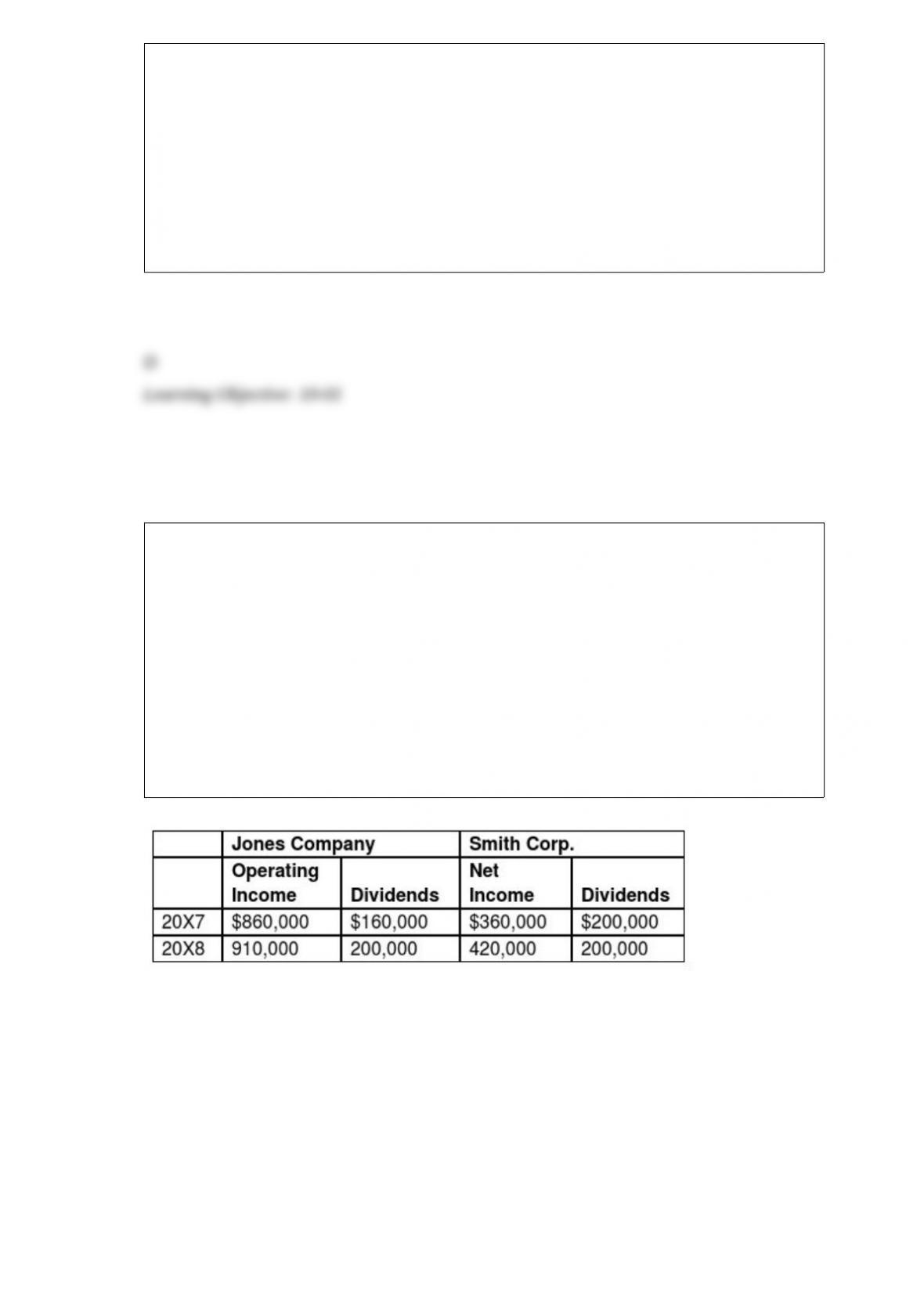

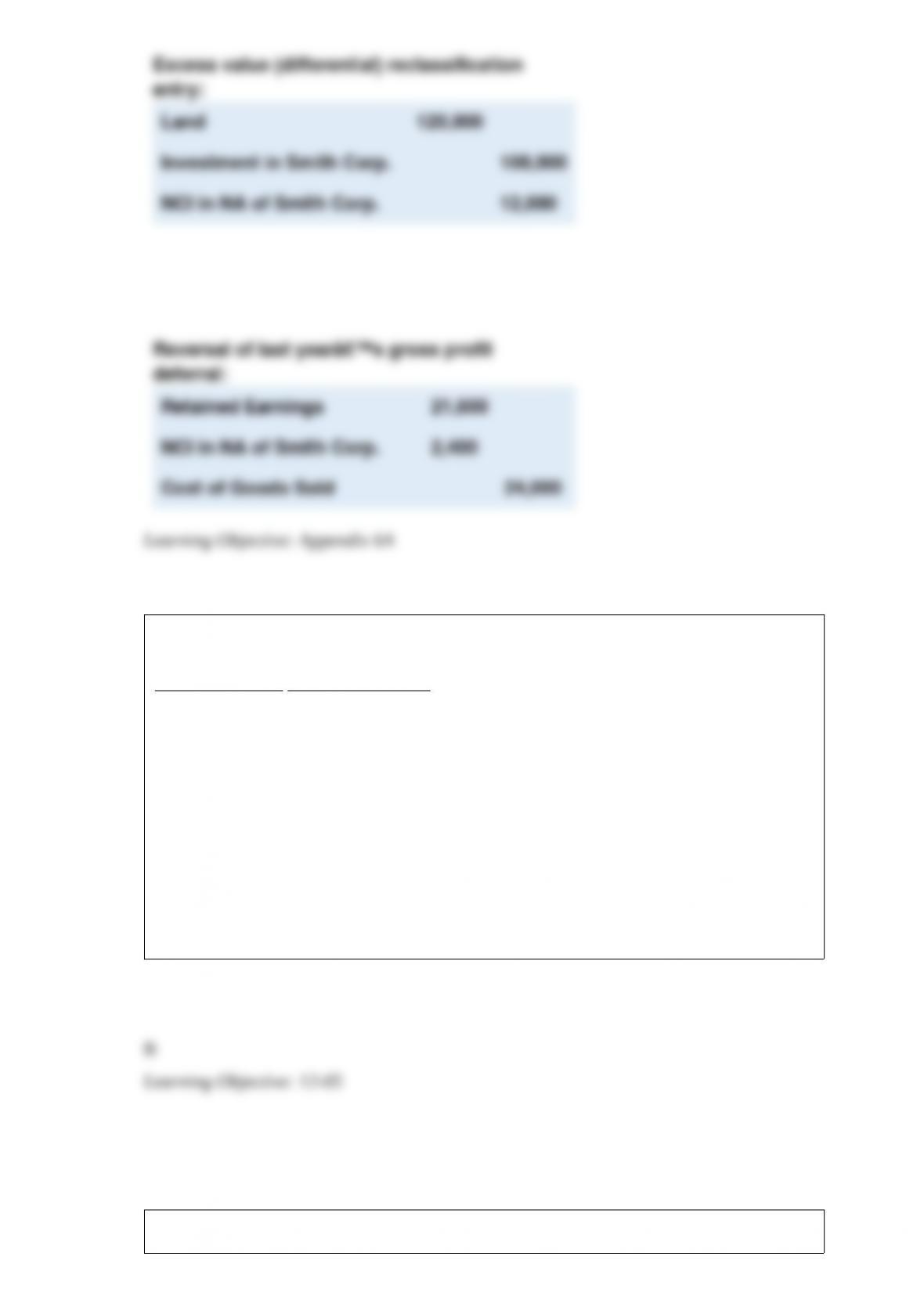

On January 1, 20X7, Jones Company acquired 90 percent of the outstanding common

stock of Smith Corporation for $1,242,000. On that date, the fair value of

noncontrolling interest was equal to $138,000. The entire differential was related to

land held by Smith. At the date of acquisition, Smith had common stock outstanding of

$520,000, additional paid-in capital of $200,000, and retained earnings of $540,000.

During 20X7, Smith sold inventory to Jones for $440,000. The inventory originally cost

Smith $360,000. By year-end, 30 percent was still in Jones’ ending inventory. During

20X8, the remaining inventory was resold to an unrelated customer. Both Jones and

Smith use perpetual inventory systems.

Income and dividend information for both Jones and Smith for 20X7 and 20X8 are as

follows:

Assume Jones uses the modified equity method to account for its investment in Smith.

Required:

a. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X7.

b. Present the worksheet consolidation entries necessary to prepare consolidated financial

statements for 20X8.

Certain balance sheet accounts of a foreign subsidiary of Rowan, Inc. (Rowan) at

December 31, 20X6, have been translated into U.S. dollars as follows:

At current rates At historical rates

Note receivable, long-term $240,000 $200,000

Prepaid rent $85,000 $80,000

Patent $150,000 $170,000

The subsidiary’s functional currency is the currency of the country in which it is

located.

What total amount should be included in Rowan’s December 31, 20X6 consolidated

balance sheet for the above accounts?

A. $450,000

B. $475,000

C. $455,000

D. $495,000

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On January 1, 20X8, Mortar received $350,000 from Granite for

equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment is

expected to have a 10-year useful life and no salvage value. Both companies depreciate

equipment on a straight-line basis.

Based on the preceding information, the gain on sale of equipment recorded by Mortar

for 20X8 is:

A. $70,000.

B. $65,000.

C. $50,000.

D. $40,000.

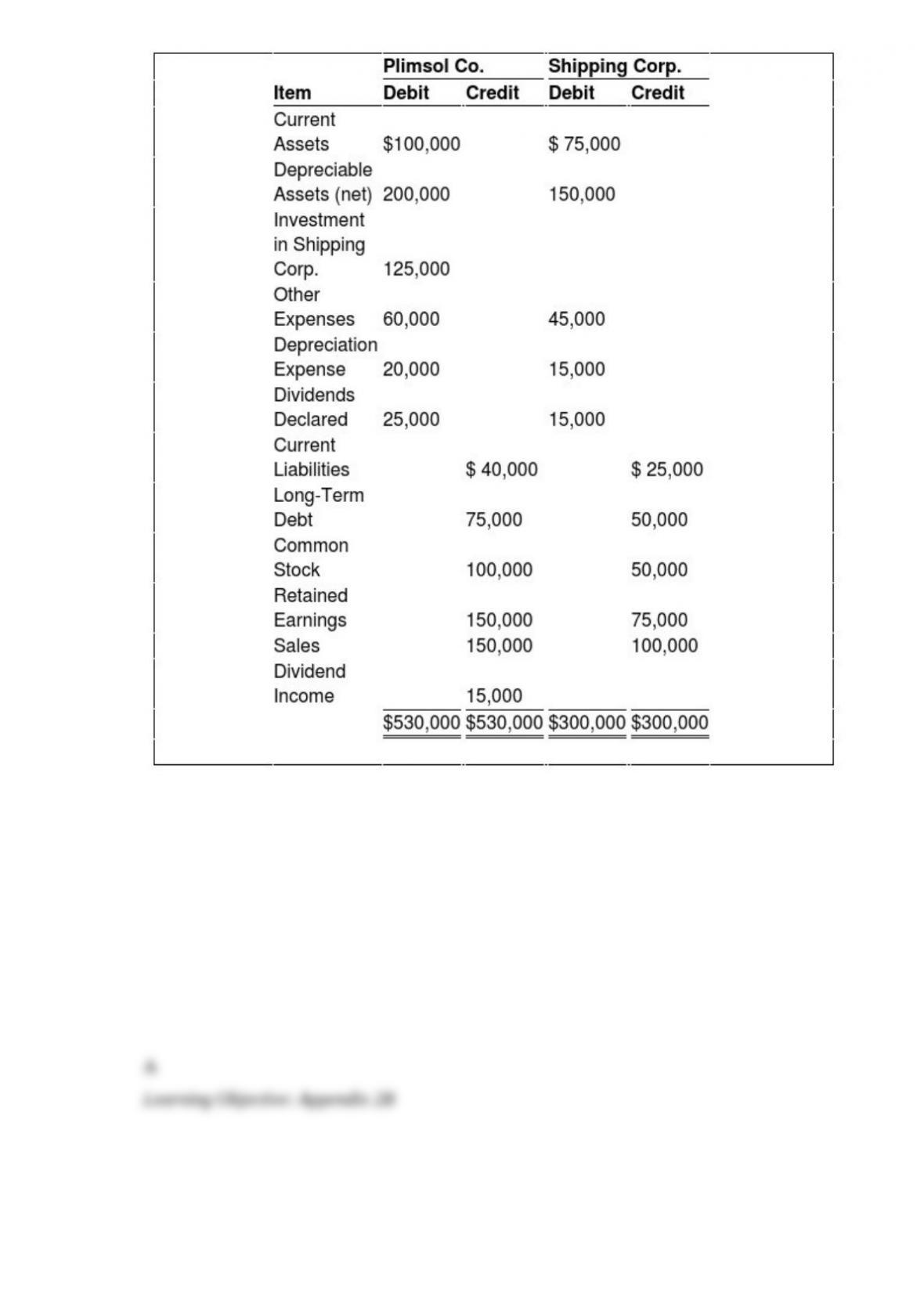

On January 1, 20X4, Plimsol Company acquired 100 percent of Shipping Corporation’s

voting shares, at underlying book value. Plimsol uses the cost method in accounting for

its investment in Shipping. Shipping’s retained earnings was $75,000 on the date of

acquisition. On December 31, 20X4, the trial balance data for the two companies are as

follows:

Based on the information provided, what amount of retained earnings will be reported in

the consolidated balance sheet prepared on December 31, 20X4?

A. $235,000

B. $210,000

C. $310,000

D. $225,000

Aaron, a holder of a $200,000 Xenon Inc. bond, collected the interest due on June 30,

20X2, and then sold the bond to Dolphin Inc. for $185,000. On that date the bond

issuer, Xenon, an 80 percent owner of Dolphin, had a $220,000 carrying amount for this

bond.

Based on the information given above, what was the effect of Dolphin’s purchase of

Xenon’s bonds on the noncontrolling interest amount reported in Xenon’s June 30,

20X2 consolidated balance sheet?

A. $3,000 increase

B. $7,000 decrease

C. $7,000 increase

D. No effect

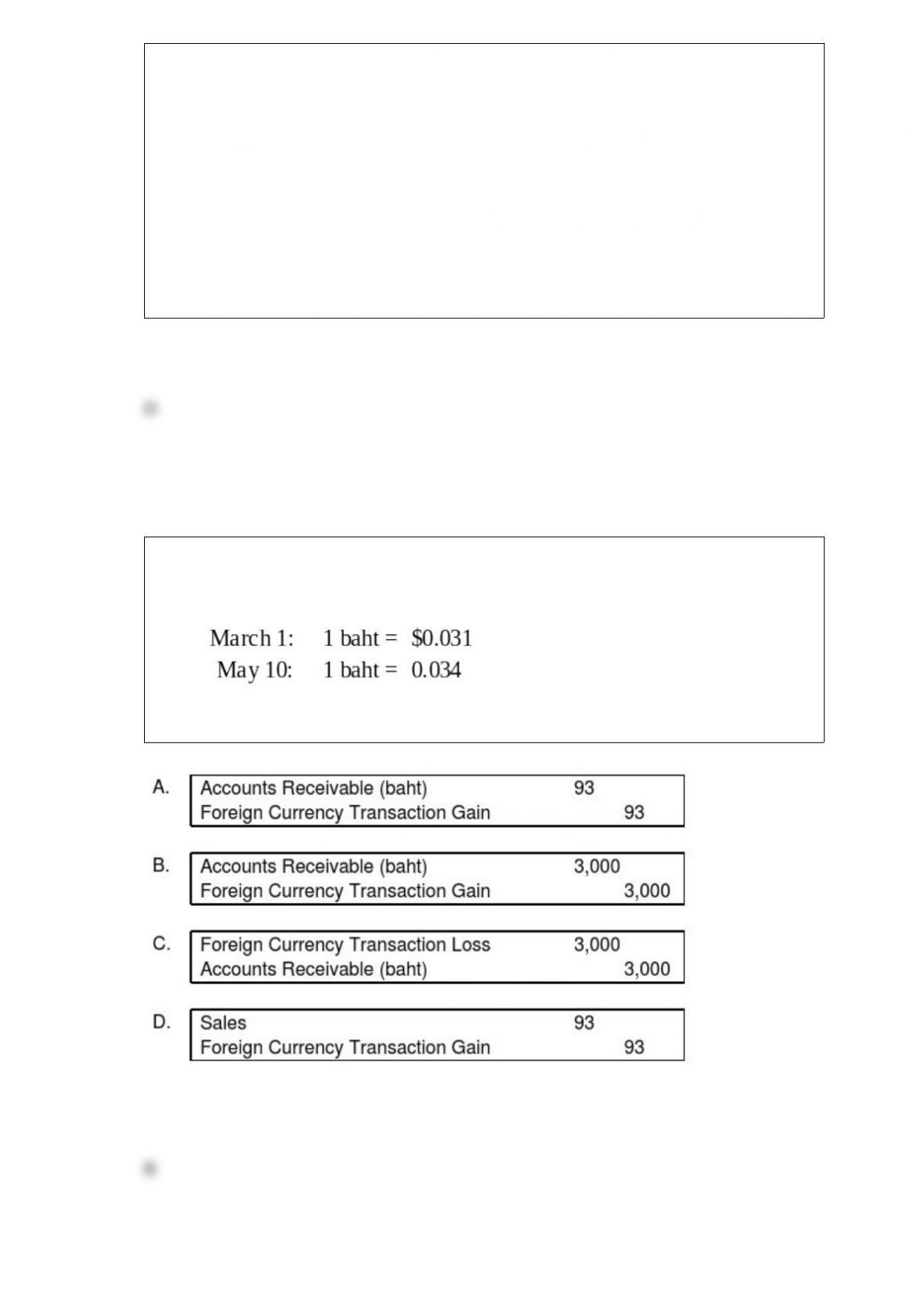

On March 1, 20X8, Wilson Corporation sold goods for a U.S. dollar equivalent of

$31,000 to a Thai company. The transaction is denominated in Thai baht. The payment

is received on May 10. The exchange rates were:

What entry is required to revalue foreign currency payable to U.S. dollar equivalent

value on May 10?

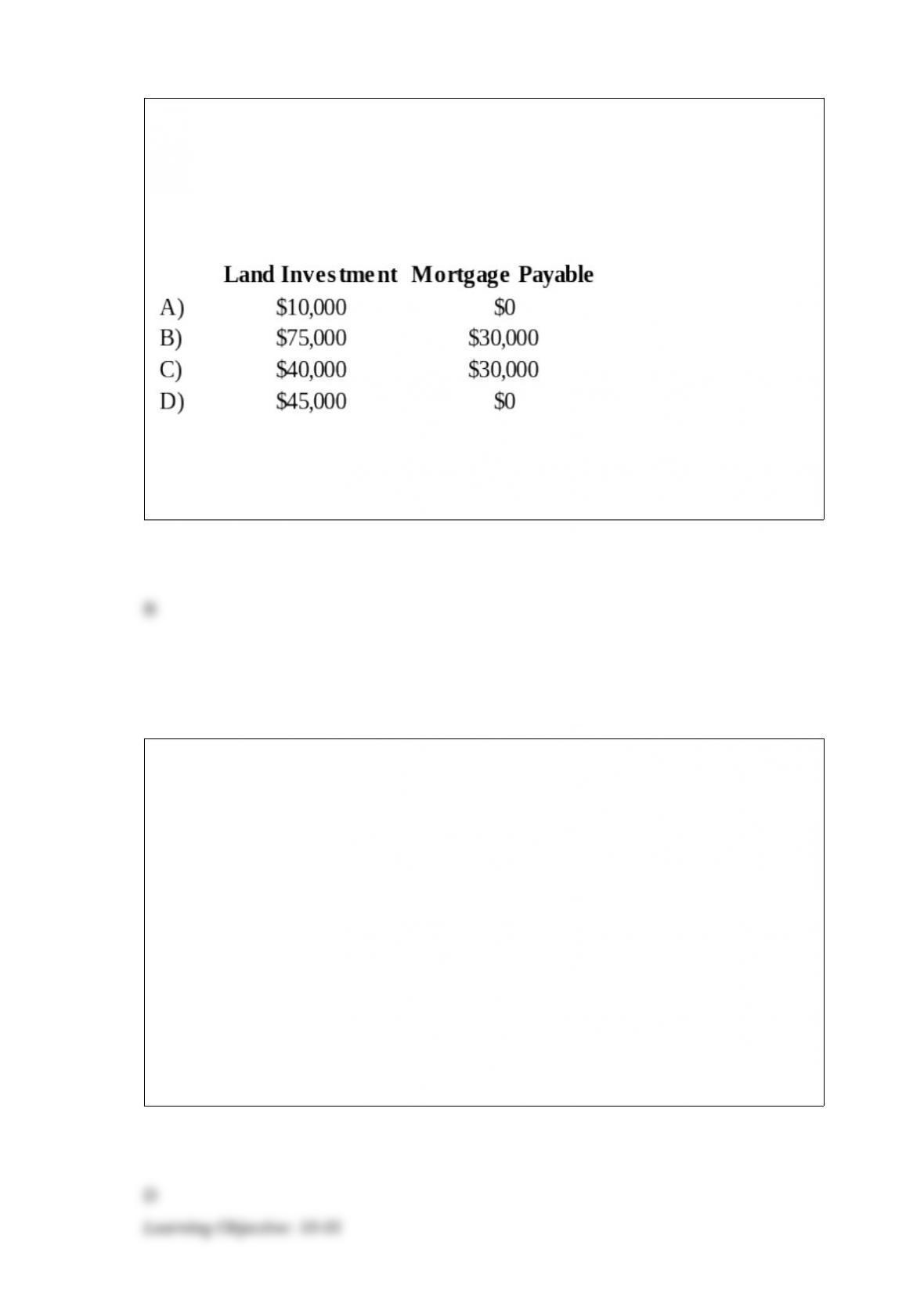

On December 31, 20X8, Mr. and Mrs. Williams owned a parcel of land held as an

investment. The land was purchased for $40,000 in 20X6, and was encumbered by a

mortgage with a principal balance of $30,000 at December 31, 20X8. On this date the

fair value of the land was $75,000. In the Williams’ December 31, 20X8, personal

statement of financial condition, at what amount should the land investment and

mortgage payable be reported?

A. Option A

B. Option B

C. Option C

D. Option D

Winter Corporation’s consolidated cash flow statement for the year ended December

31, 20X2, reported operating cash inflows of $100,000, financing cash inflows of

$30,000, investing cash outflows of $120,000, and an ending cash balance of $50,000.

Winter acquired 60 percent of Snowboard Company’s common stock on April 1, 20X0

at book value. At that date, the fair value of the noncontrolling interest was equal to 40

percent of Snowboard’s book value. Snowboard reported net income of $30,000, paid

dividends of $20,000 in 20X2, and is included in Winter’s consolidated statements.

Winter paid dividends of $40,000 in 20X2. The indirect method is used in computing

cash flows from operations.

Based on the information provided, what was the consolidated cash balance at January

1, 20X2?

A. $300,000

B. $100,000

C. $60,000

D. $40,000

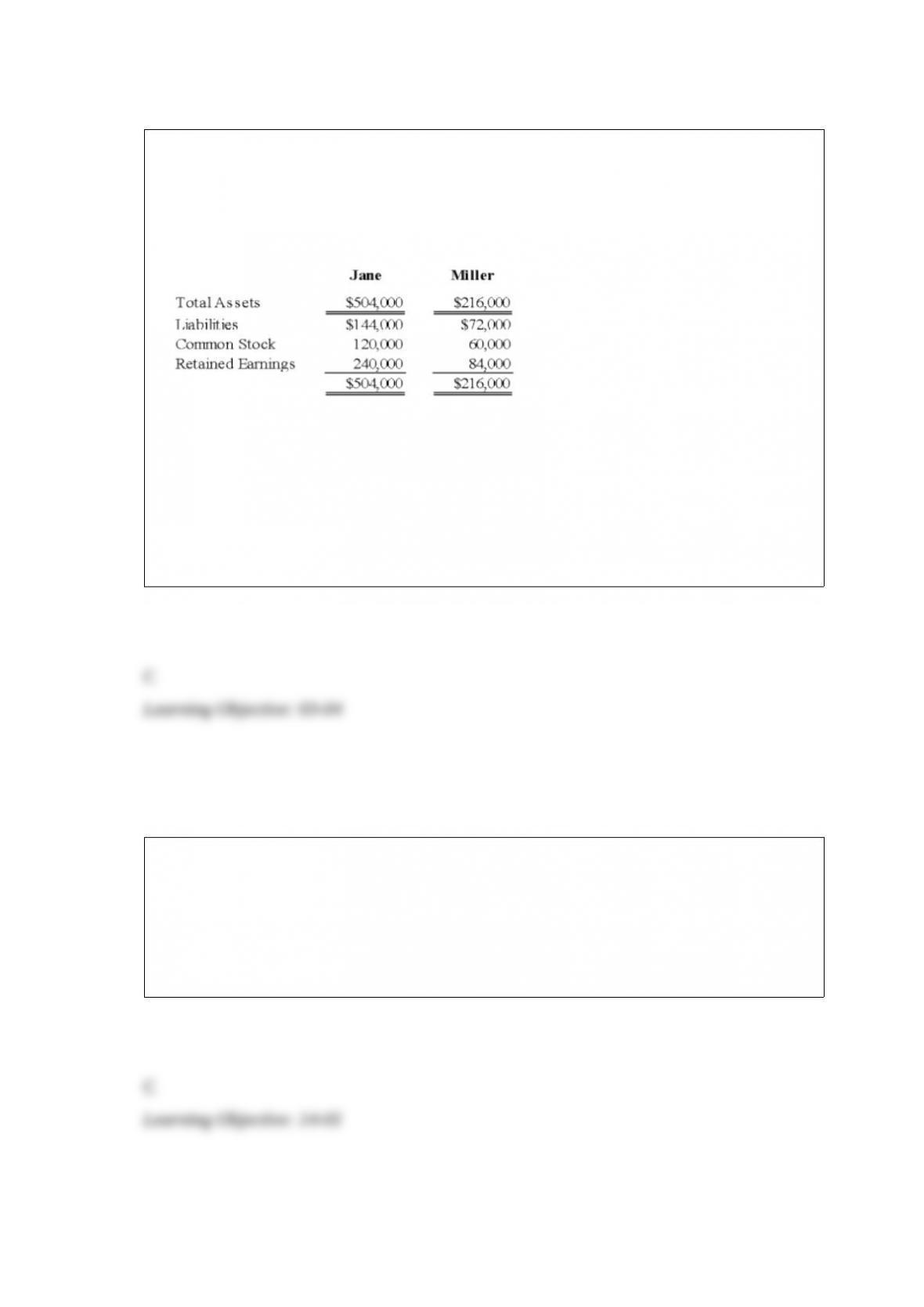

On January 3, 20X9, Jane Company acquired 75 percent of Miller Company’s

outstanding common stock for cash. The fair value of the noncontrolling interest was

equal to a proportionate share of the book value of Miller Company’s net assets at the

date of acquisition. Selected balance sheet data at December 31, 20X9, are as follows:

Based on the preceding information, what amount should be reported as noncontrolling

interest in net assets in Jane Company’s December 31, 20X9, consolidated balance

sheet?

A. $90,000

B. $54,000

C. $36,000

D. $0

Which regulation resulted in the creation of the Public Company Accounting Oversight

Board?

A. Investment Advisers Act

B. Securities Investor Protection Act

C. Sarbanes-Oxley Act

D. Trust Indenture Act

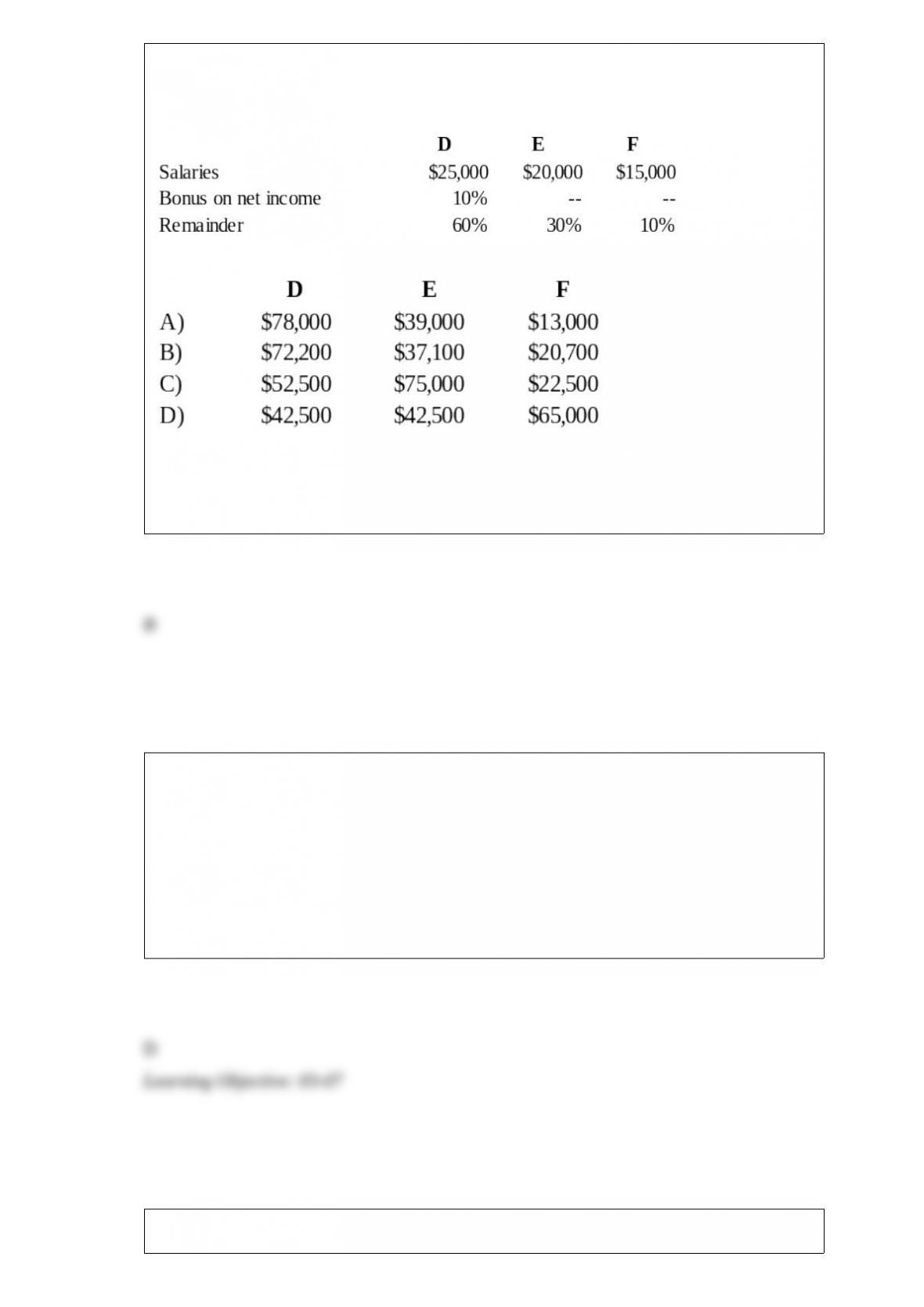

The DEF partnership reported net income of $130,000 for the year ended December 31,

20X8. According to the partnership agreement, partnership profits and losses are to be

distributed as follows:

How should partnership net income for 20X8 be allocated to D, E, and F?

A. Option A

B. Option B

C. Option C

D. Option D

All of the following statements accurately describe Special Purpose Entities (SPEs)

except for:

A. SPEs are corporations, trust or partnerships created for a single specified purpose.

B. SPEs usually have no substantive operations and are used for financing operations.

C. SPEs are used for asset securitization, risk sharing and taking advantage of tax

statues.

D. A variable interest entity (VIE) is a type of SPE with a limited number of equity

investors.

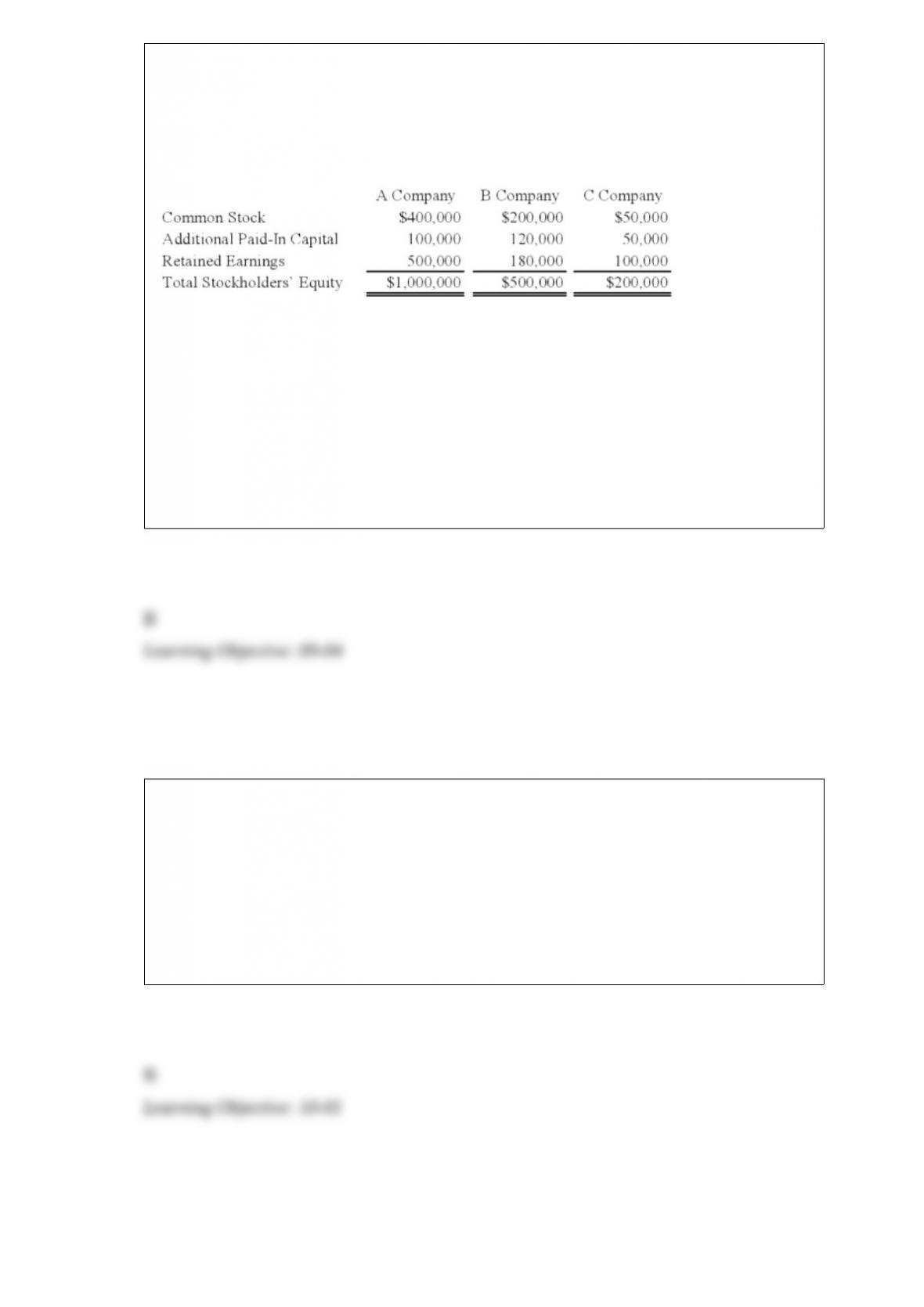

On January 1, 20X9, A Company acquired 85 percent of B Company’s voting common

stock for $425,000. At that date, the fair value of the noncontrolling interest of B

Company was $75,000. Immediately after A Company acquired its ownership, B

Company acquired 75 percent of C Company’s stock for $150,000. The fair value of the

noncontrolling interest of C Company was $50,000 at that date. At January 1, 20X9, the

stockholders’ equity sections of the balance sheets of the companies were as follows:

During 20X9, A Company reported operating income of $175,000 and paid dividends

of $50,000. B Company reported operating income of $125,000 and paid dividends of

$40,000. C Company reported net income of $100,000 and paid dividends of $25,000.

Based on the information provided, what amount of income will be assigned to the

controlling interest in the consolidated income statement for 20X9?

A. $400,000

B. $345,000

C. $285,000

D. $175,000

Which of the following observations concerning the comparisons between the direct

and indirect approaches of presenting a cash flow statement is true?

A. The final number of cash flows from operating activities is different under the two

approaches.

B. The direct approach provides a clearer picture of cash flows related to operations.

C. Authoritative bodies have generally expressed a preference for the indirect method.

D. A separate reconciliation of operating cash flows and net income is required under

the indirect approach.

Under GASB 34, capital assets and non-current debt are:

A. reported in the government-wide statement of net assets.

B. reported in the fixed asset and long-term debt group of accounts.

C. reported in the governmental funds balance sheet.

D. no longer reported under GASB 34.

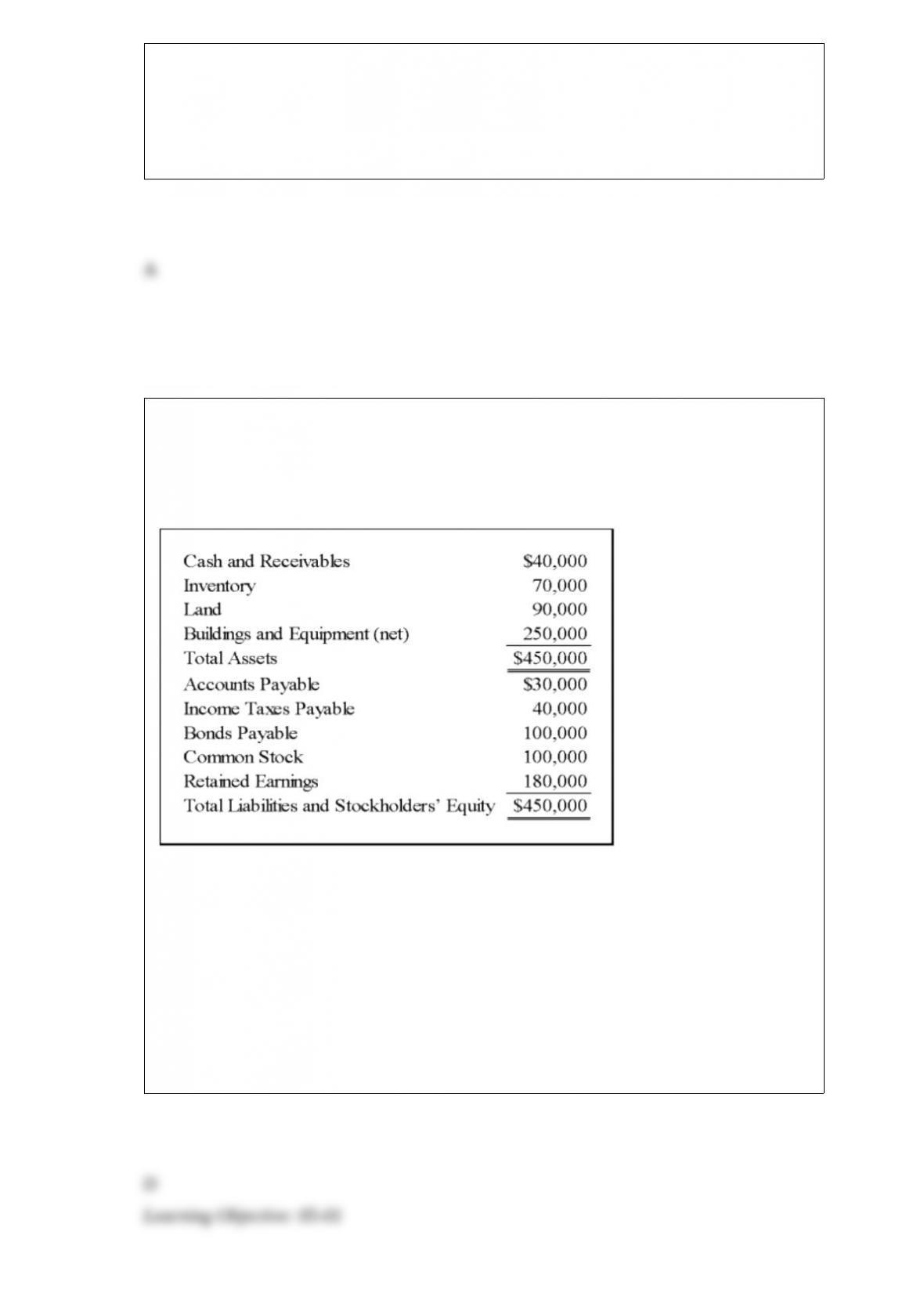

Bristle Corporation acquired 75 percent of Silver Corporation’s common stock on

December 31, 20X8, for $300,000. The fair value of the noncontrolling interest at that

date was determined to be $100,000. Silver’s balance sheet immediately before the

combination reflected the following balances:

A careful review of the fair value of Silver’s assets and liabilities indicated that

inventory, land, and buildings and equipment (net) had fair values of $65,000,

$100,000, and, $300,000 respectively. Goodwill is assigned proportionately to Bristle

and the noncontrolling shareholders.

Based on the preceding information, what amount of land will be included in the

consolidated balance sheet immediately following the acquisition?

A. $0

B. $10,000

C. $90,000

D. $100,000

On January 1, 20X6, Climber Corporation acquired 90 percent of Wisden Corporation

for $180,000 cash. Wisden reported net income of $30,000 and dividends of $10,000

for 20X6, 20X7, and 20X8. On January 1, 20X6, Wisden reported common stock

outstanding of $100,000 and retained earnings of $60,000, and the fair value of the

noncontrolling interest was $20,000. It held land with a book value of $30,000 and a

market value of $35,000 and equipment with a book value of $50,000 and a market

value of $60,000 at the date of combination. The remainder of the differential at

acquisition was attributable to an increase in the value of patents, which had a

remaining useful life of five years. All depreciable assets held by Wisden at the date of

acquisition had a remaining economic life of five years. Climber uses the equity method

in accounting for its investment in Wisden.

Based on the preceding information, what balance would Climber report as its

investment in Wisden at January 1, 20X9?

A. $251,100

B. $224,100

C. $215,100

D. $234,000

A special revenue fund should be used in which of the following situations for a state

government?

A. For sales taxes which are to be distributed to towns, cities, villages, etc. of the state.

B. For the proceeds of general obligation bonds which are to be used to construct major

long-lived fixed assets.

C. For gasoline taxes which are to be used exclusively to repair state roads and bridges.

D. For investments donated by a prominent citizen which are to be invested

permanently, with income being used to support homeless people.

On December 5, 20X8, Texas based Imperial Corporation purchased goods from a

Saudi Arabian firm for 100,000 riyals (SAR), to be paid on January 10, 20X9. The

transaction is denominated in Saudi riyals. Imperial’s fiscal year ends on December 31,

and its reporting currency is the U.S. dollar. The exchange rates are:

December 5, 20X8 1 riyal = $0.265

December 31, 20X8 1 riyal = 0.262

January 10, 20X9 1 riyal = 0.264

Based on the preceding information, what was the overall foreign currency gain or loss

on the accounts payable transaction?

A. $300 loss

B. $200 loss

C. $100 gain

D. $200 gain