Chapter 08 – Intercompany Indebtedness

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

CHAPTER 8

INTERCOMPANY INDEBTEDNESS

ANSWERS TO QUESTIONS

Q8-1 A gain or loss on bond retirement is reported by the consolidated entity whenever (a) one

Q8-2 A constructive retirement occurs when the bonds of a company included in the

consolidated entity are purchased by another company included within the consolidated entity.

Q8-3 When bonds sold to an affiliate at par value are not eliminated, bonds payable and bond

investment are misstated in the balance sheet accounts and interest income and interest

Q8-4 Both the bond investment and interest income reported by the purchaser will be

improperly included. Interest expense, bonds payable, and any premium or discount recorded

Q8-5 If the focus is placed on the legal entity, only bonds actually reacquired by the debtor will

be treated as retired. This treatment can lead to incorrect reports for the consolidated entity in

two dimensions, 1) the interest expense/revenue on the bonds and 2) the gain/loss on

Q8-6 The difference in treatment is due to the effect of the transactions on the consolidated

entity. In the case of land sold to another affiliate, a gain has been recorded that is not a gain

from the viewpoint of the consolidated entity. Thus, it must be eliminated in the consolidation

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

C8-1 Recognition of Retirement Gains and Losses

a. When Flood purchases the bonds it establishes an investment account on its books and

Bradley establishes a bond liability and discount account on its books. No entry is made by

Century. When Century purchases the bonds, Century records an investment and Flood

removes the balance in the investment account and records a gain on the sale. Bradley makes

Bradley.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

E8-1 Bond Sale from Parent to Subsidiary

a.

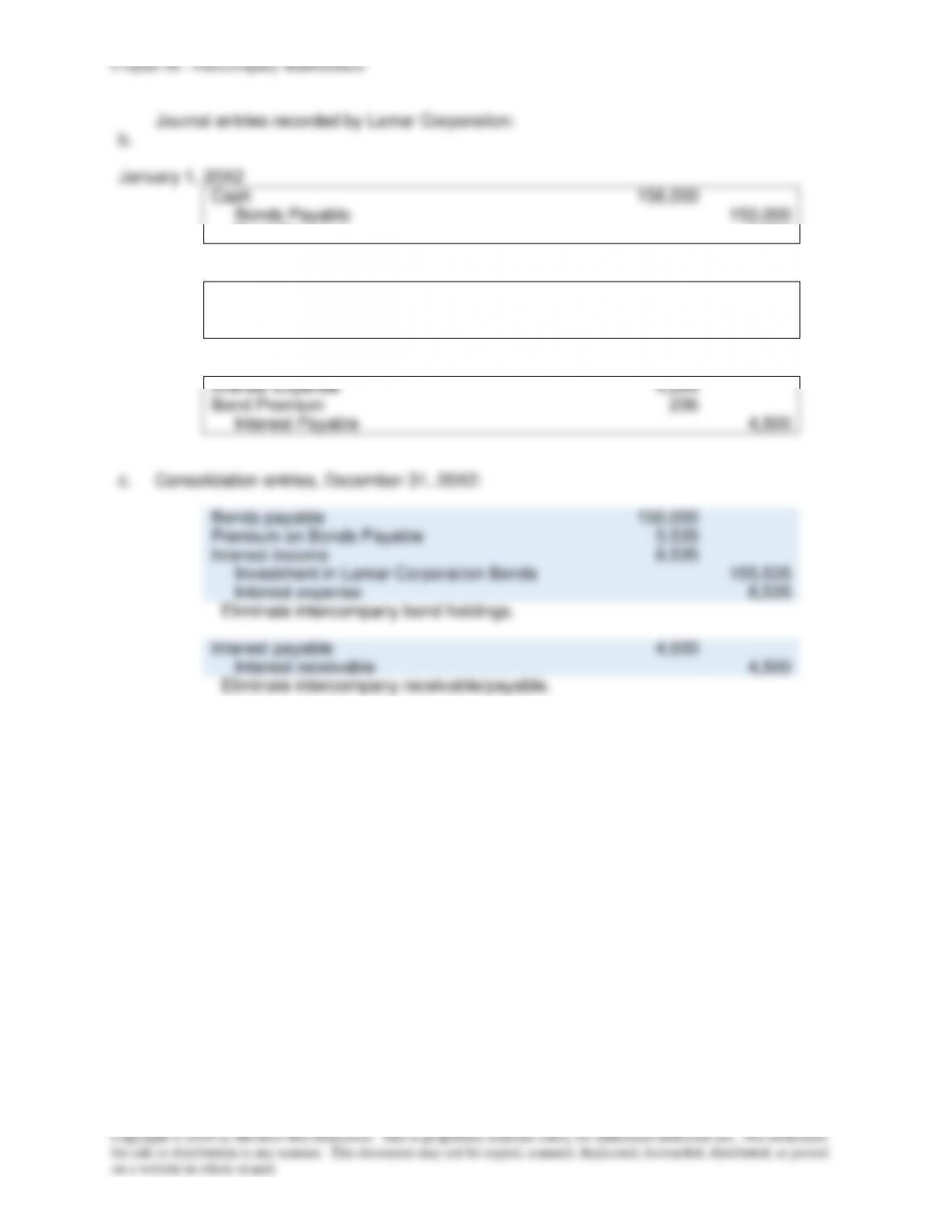

Journal entries recorded by Humbolt Corporation:

January 1, 20X2

Investment in Lamar Corporation Bonds

156,000

Cash

156,000

July 1, 20X2

Cash

4,500

Interest Income

4,271

Investment in Lamar Corporation Bonds

229

December 31, 20X2

Interest Receivable

4,500

Interest Income

4,264

Investment in Lamar Corporation Bonds

236

Chapter 08 – Intercompany Indebtedness

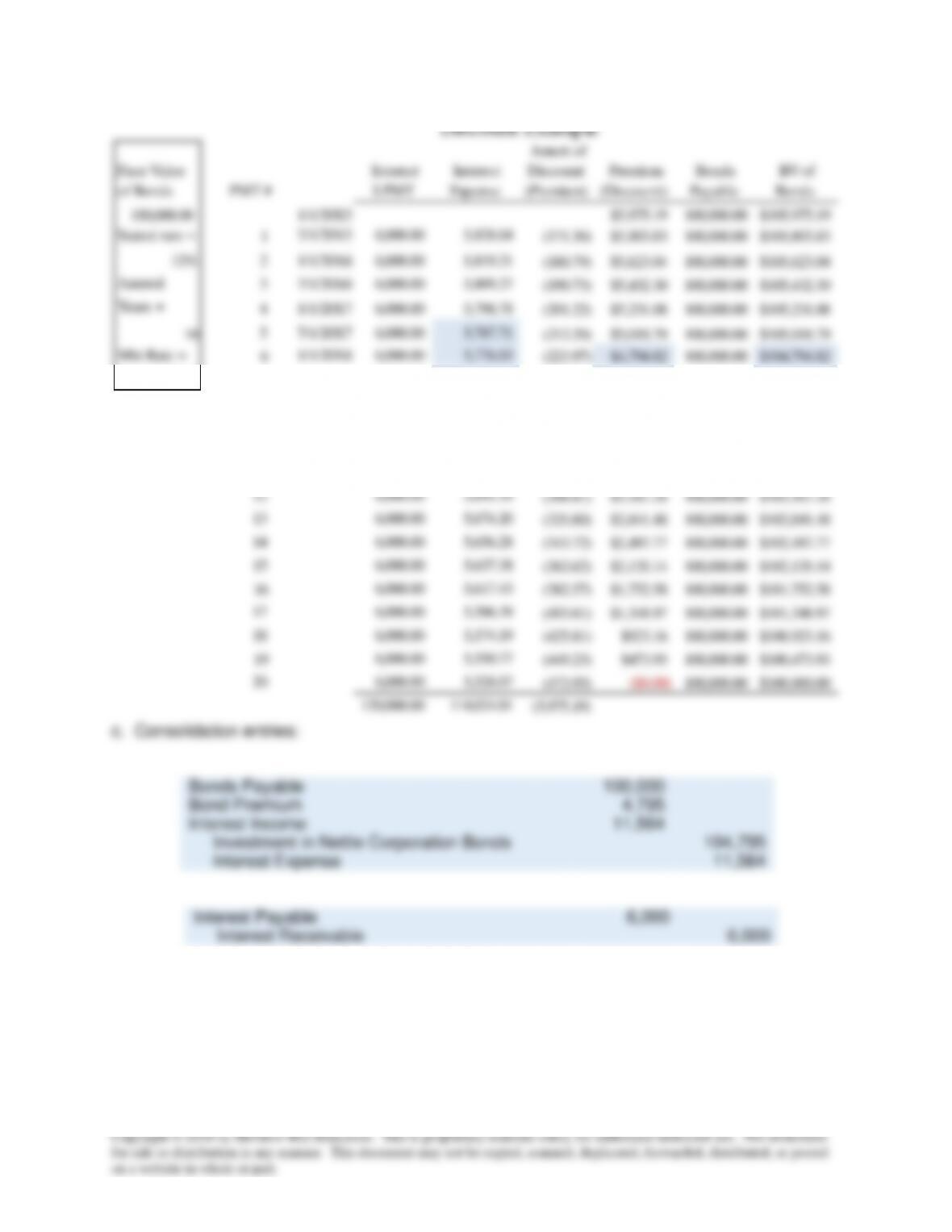

c. Consolidation entries:

Bonds Payable

100,000

Bond Premium

4,795

Interest Income

11,564

Investment in Nettle Corporation Bonds

104,795

Interest Expense

11,564

Interest Payable

6,000

Interest Receivable

6,000

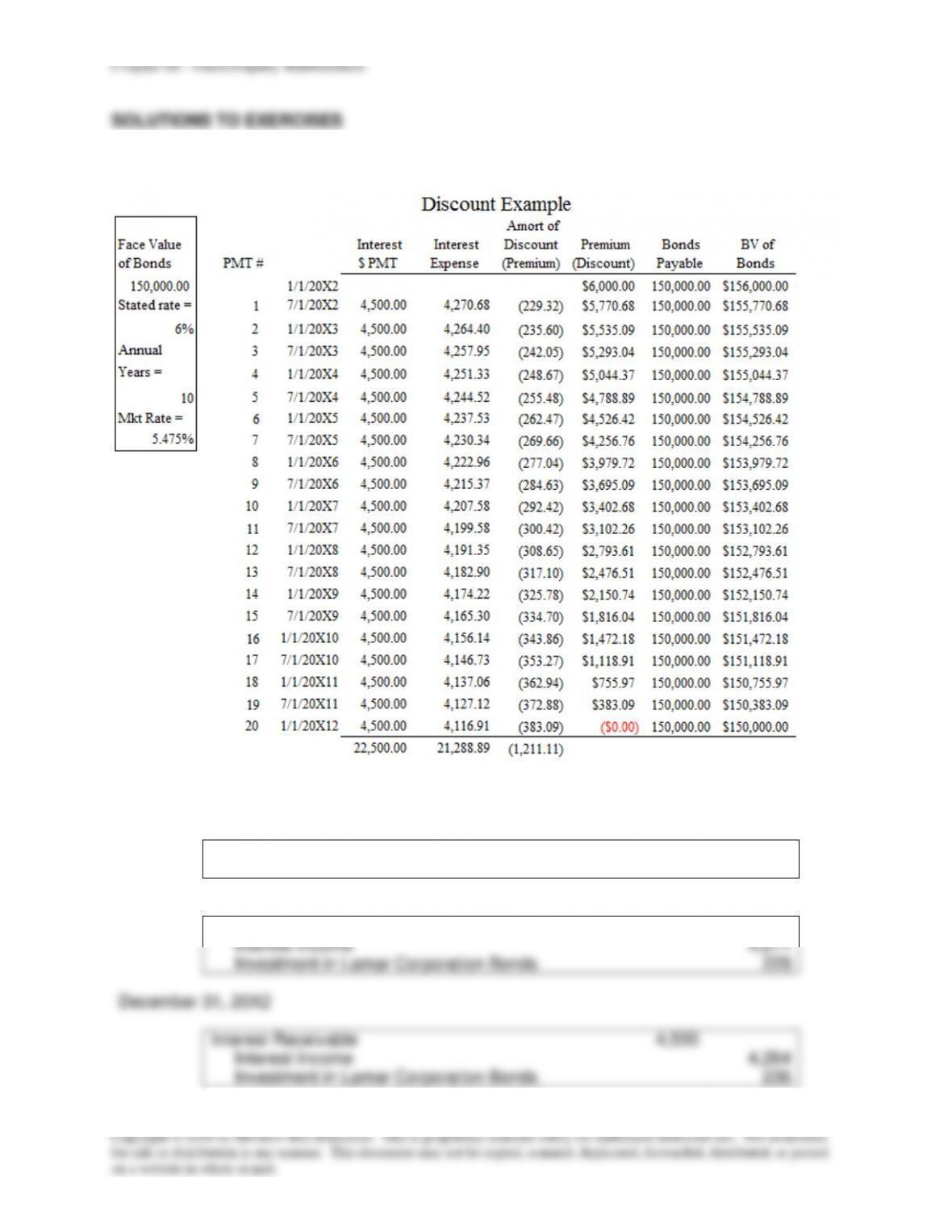

Face Value

of Bonds

PMT #

Interest

$ PMT

Interest

Expense

Amort of

Discount

(Premium)

Premium

(Discount)

Bonds

Payable

BV of

Bonds

100,000.00 1/1/20X5 $5,975.19 100,000.00 $105,975.19

Stated rate = 1 7/1/20X5 6,000.00 5,828.64 (171.36) $5,803.83 100,000.00 $105,803.83

12% 2 1/1/20X6 6,000.00 5,819.21 (180.79) $5,623.04 100,000.00 $105,623.04

Annual 3 7/1/20X6 6,000.00 5,809.27 (190.73) $5,432.30 100,000.00 $105,432.30

Years = 4 1/1/20X7 6,000.00 5,798.78 (201.22) $5,231.08 100,000.00 $105,231.08

10

5 7/1/20X7 6,000.00 5,787.71 (212.29) $5,018.79 100,000.00 $105,018.79

Mkt Rate = 6 1/1/20X8 6,000.00 5,776.03 (223.97) $4,794.82 100,000.00 $104,794.82

11.000% 7 6,000.00 5,763.72 (236.28) $4,558.54 100,000.00 $104,558.54

8 6,000.00 5,750.72 (249.28) $4,309.26 100,000.00 $104,309.26

9 6,000.00 5,737.01 (262.99) $4,046.27 100,000.00 $104,046.27

10 6,000.00 5,722.54 (277.46) $3,768.81 100,000.00 $103,768.81

11

6,000.00 5,707.28 (292.72) $3,476.10 100,000.00 $103,476.10

12 6,000.00 5,691.19 (308.81) $3,167.28 100,000.00 $103,167.28

13 6,000.00 5,674.20 (325.80) $2,841.48 100,000.00 $102,841.48

14 6,000.00 5,656.28 (343.72) $2,497.77 100,000.00 $102,497.77

15 6,000.00 5,637.38 (362.62) $2,135.14 100,000.00 $102,135.14

16

6,000.00 5,617.43 (382.57) $1,752.58 100,000.00 $101,752.58

17 6,000.00 5,596.39 (403.61) $1,348.97 100,000.00 $101,348.97

18 6,000.00 5,574.19 (425.81) $923.16 100,000.00 $100,923.16

19

6,000.00 5,550.77 (449.23) $473.93 100,000.00 $100,473.93

20 6,000.00 5,526.07 (473.93) ($0.00) 100,000.00 $100,000.00

120,000.00 114,024.81 (5,975.19)

Discount Example