Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4–31 Intercorporate Receivables and Payables

a. Consolidation entries:

Equity Method Entries on Kim Corp.’s Books:

Investment in Normal Co.

305,000

Cash

305,000

Record the initial investment in Normal Co.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Additional

PIC

+

Retained

Earnings

Book value at

acquisition

285,000

150,000

140,000

(5,000)

1/1/X7

Goodwill = 20,000

Identifiable

Excess = 0

$305,000

Initial

investment

in Normal

Co.

100%

Book value =

285,000

Basic Consolidation Entry

Common stock

150,000

Paid-in capital in excess of par

140,000

Retained earnings

5,000

Investment in Normal Co.

285,000

Excess Value (Differential) Calculations:

Total

=

Goodwill

Balances

20,000

20,000

Excess Value (Differential) Reclassification Entry:

Goodwill

20,000

Investment in Normal Co.

20,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-52

P4-31 (continued)

Eliminate Intercompany Accounts:

Bonds Payable

50,000

Investment in Normal Co. Bonds

50,000

Accounts Payable

10,000

Accounts Receivable

10,000

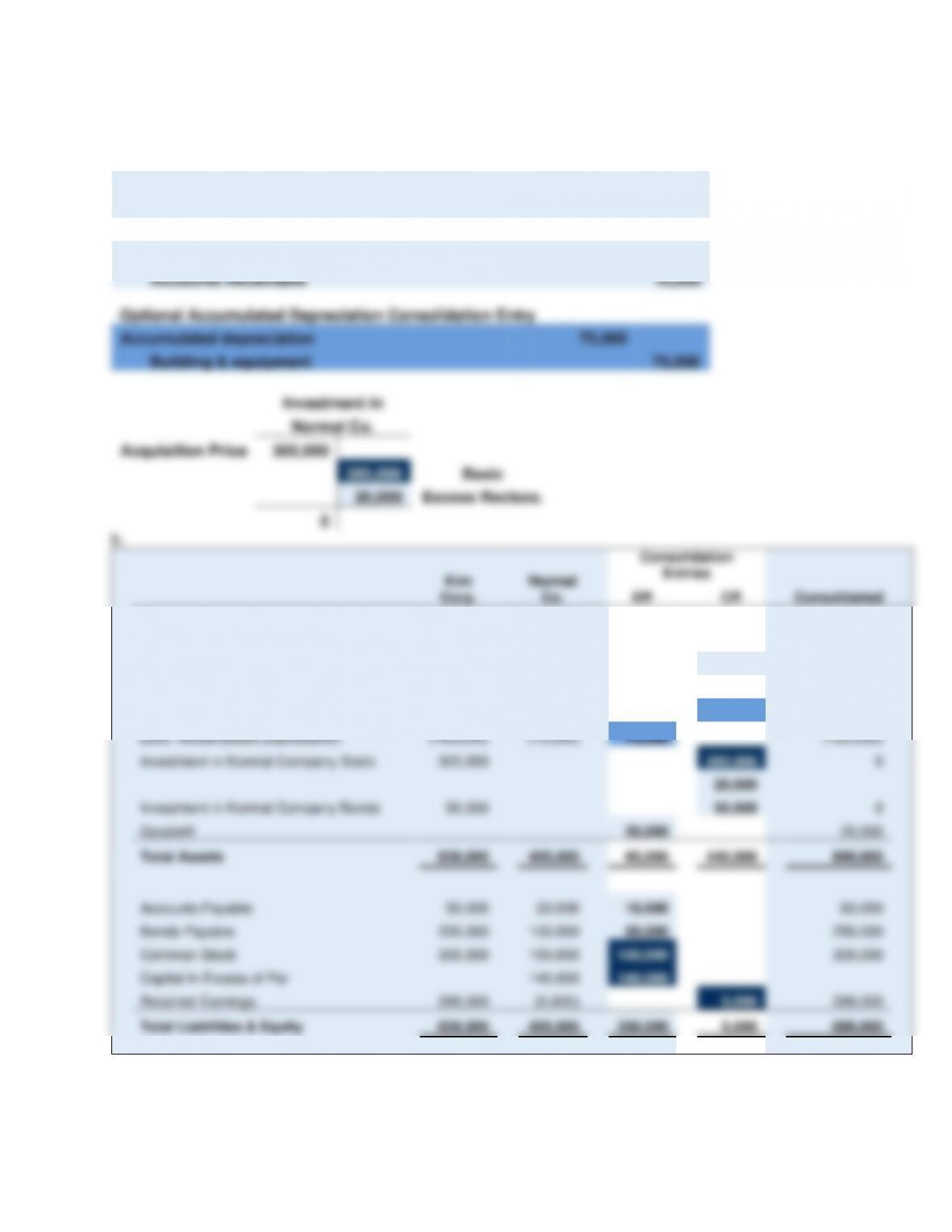

Optional Accumulated Depreciation Consolidation Entry

Accumulated depreciation

75,000

Building & equipment

75,000

Investment in

Normal Co.

Acquisition Price

305,000

285,000

Basic

20,000

Excess Reclass.

0

Kim

Corp.

Normal

Co.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

70,000

35,000

105,000

Accounts Receivable

90,000

65,000

10,000

145,000

Inventory

84,000

80,000

164,000

Buildings & Equipment

400,000

300,000

75,000

625,000

Less: Accumulated Depreciation

(160,000)

(75,000)

75,000

(160,000)

Investment in Normal Company Stock

305,000

285,000

0

20,000

Investment in Normal Company Bonds

50,000

50,000

0

Goodwill

20,000

20,000

Total Assets

839,000

405,000

95,000

440,000

899,000

Accounts Payable

50,000

20,000

10,000

60,000

Bonds Payable

200,000

100,000

50,000

250,000

Common Stock

300,000

150,000

150,000

300,000

Capital in Excess of Par

140,000

140,000

Retained Earnings

289,000

(5,000)

5,000

289,000

Total Liabilities & Equity

839,000

405,000

350,000

5,000

899,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-53

P4–31 (continued)

c.

Kim Corporation and Subsidiary

Consolidated Balance Sheet

January 1, 20X7

Cash

$105,000

Accounts Receivable

145,000

Inventory

164,000

Buildings and Equipment

$625,000

Less: Accumulated Depreciation

(160,000)

465,000

Goodwill

20,000

Total Assets

$899,000

Accounts Payable

$ 60,000

Bonds Payable

250,000

Common Stock

$300,000

Retained Earnings

289,000

589,000

Total Liabilities and Stockholders’ Equity

$899,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

P4–32 Balance Sheet Consolidation

a.

Equity Method Entries on Primary Corp.’s Books:

Investment in Street Co.

650,000

Bonds Payable

650,000

Record the initial investment in Street Co.

b.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Add’l Paid-

In-Capital

+

Retained

Earnings

Book value at

acquisition

478,000

200,000

130,000

148,000

Basic Consolidation Entry

Common Stock

200,000

Additional Paid-in capital

Retained Earnings

148,000

Investment in Street Co.

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-55

P4–32 (continued)

Total

=

Inventory

+

Land

+

Buildings

&

Equipment

+

Patent

+

Disc. on

Bonds

Payable

+

Goodwill

Balances

172,000

4,000

20,000

50,000

40,000

10,000

48,000

Excess Value (Differential) Reclassification Entry:

Inventory

4,000

Land

20,000

Buildings & Equipment

50,000

Patent

40,000

Discount on Bonds Payable

10,000

Goodwill

48,000

Investment in Street

Co.

172,000

Eliminate Intercompany Accounts:

Current Payables

6,500

Receivables

6,500

FYI, the FASB now requires that no allowance accounts be carried forward from the

acquiree in a business combination. However, because of immateriality and the short-

lived nature of the carry forward subsequent to the date of combination, the allowance in

this problem has not been offset against the receivable. If such an offset is desired, the

following consolidation entry would be made:

Allowance for Bad Debts

1,000

Receivables

1,000

However, since receivables are reported net of the allowance, the entry is not shown in the

worksheet included here.

Optional Accumulated Depreciation Consolidation Entry

Accumulated depreciation

220,000

Building & equipment

220,000

Investment in

Street Co.

Acquisition Price

650,000

478,000

Basic

172,000

Excess Reclass.

0

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-56

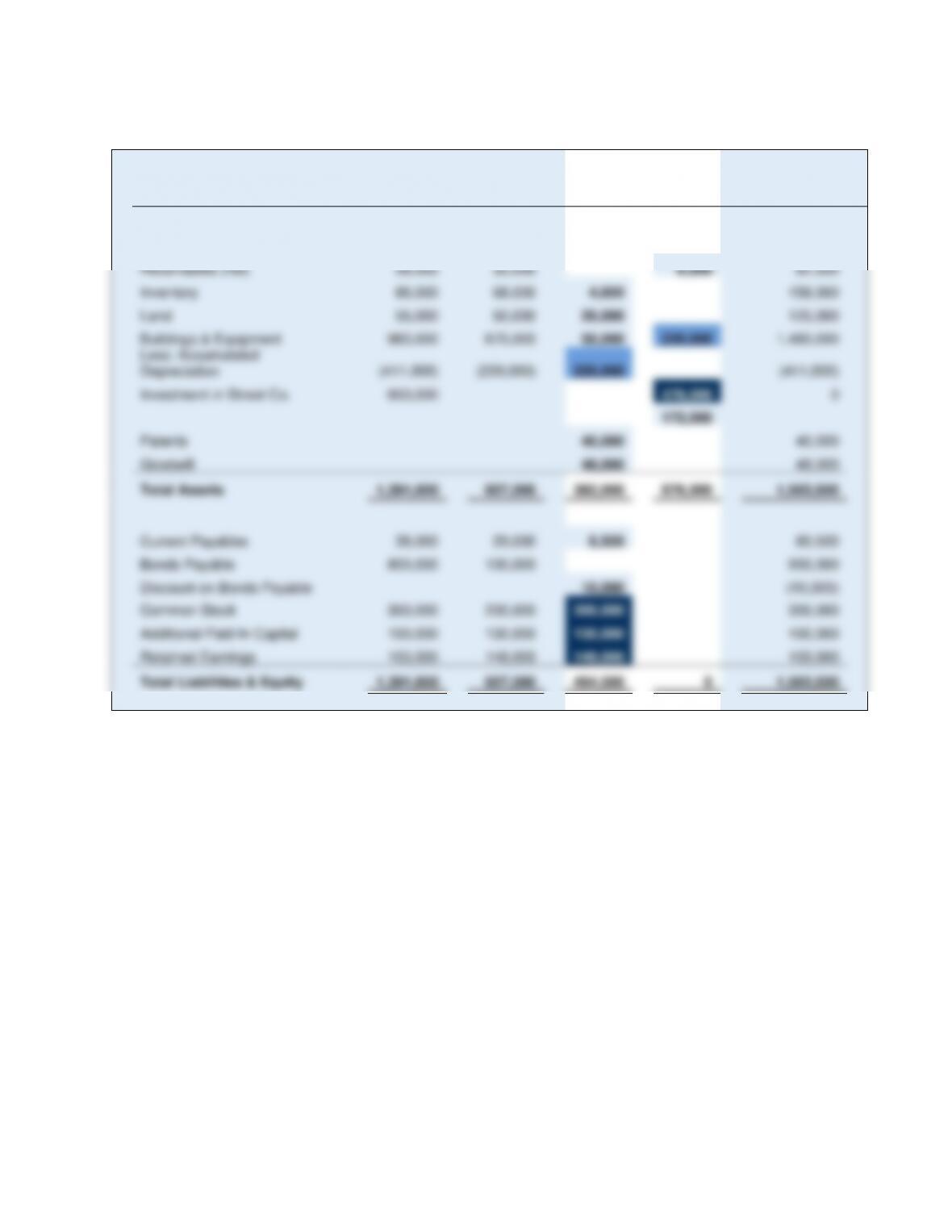

P4–32 (continued)

c.

Primary

Corp.

Street

Co.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

12,000

9,000

21,000

Receivables (net)

39,000

30,000

6,500

62,500

Inventory

86,000

68,000

4,000

158,000

Land

55,000

50,000

20,000

125,000

Buildings & Equipment

960,000

670,000

50,000

220,000

1,460,000

Less: Accumulated

Depreciation

(411,000)

(220,000)

220,000

(411,000)

Investment in Street Co.

650,000

478,000

0

172,000

Patents

40,000

40,000

Goodwill

48,000

48,000

Total Assets

1,391,000

607,000

382,000

876,500

1,503,500

Current Payables

38,000

29,000

6,500

60,500

Bonds Payable

850,000

100,000

950,000

Discount on Bonds Payable

10,000

(10,000)

Common Stock

300,000

200,000

200,000

300,000

Additional Paid-In Capital

100,000

130,000

130,000

100,000

Retained Earnings

103,000

148,000

148,000

103,000

Total Liabilities & Equity

1,391,000

607,000

494,500

0

1,503,500

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-57

P4–32 (continued)

d.

Primary Corporation and Subsidiary

Consolidated Balance Sheet

January 2, 20X8

Cash

$ 21,000

Receivables

$ 65,500

Less: Allowance for Bad Debts

(3,000)

62,500

Inventory

158,000

Land

125,000

Buildings and Equipment

$1,460,000

Less: Accumulated Depreciation

(411,000)

1,049,000

Patent

40,000

Goodwill

48,000

Total Assets

$1,503,500

Current Payables

$ 60,500

Bonds Payable

$ 950,000

Less: Discount on Bonds Payable

(10,000)

940,000

Stockholders’ Equity

Common Stock

$ 300,000

Additional Paid-In Capital

100,000

Retained Earnings

103,000

503,000

Total Liabilities and

Stockholders’ Equity

$1,503,500

P4-33 Consolidation Worksheet at End of First Year of Ownership

a.

Equity Method Entries on Mill Corp.’s Books:

Investment in Roller Co.

128,000

Cash

128,000

Record the initial investment in Roller Co.

Investment in Roller Co.

24,000

Income from Roller Co.

24,000

Record Mill Corp.’s 100% share of Roller Co.’s 20X8 income

Cash

16,000

Investment in Roller Co.

16,000

Record Mill Corp.’s 100% share of Roller Co.’s 20X8 dividend

Income from Roller Co.

7,500

Investment in Roller Co.

7,500

Record amortization of excess acquisition price

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

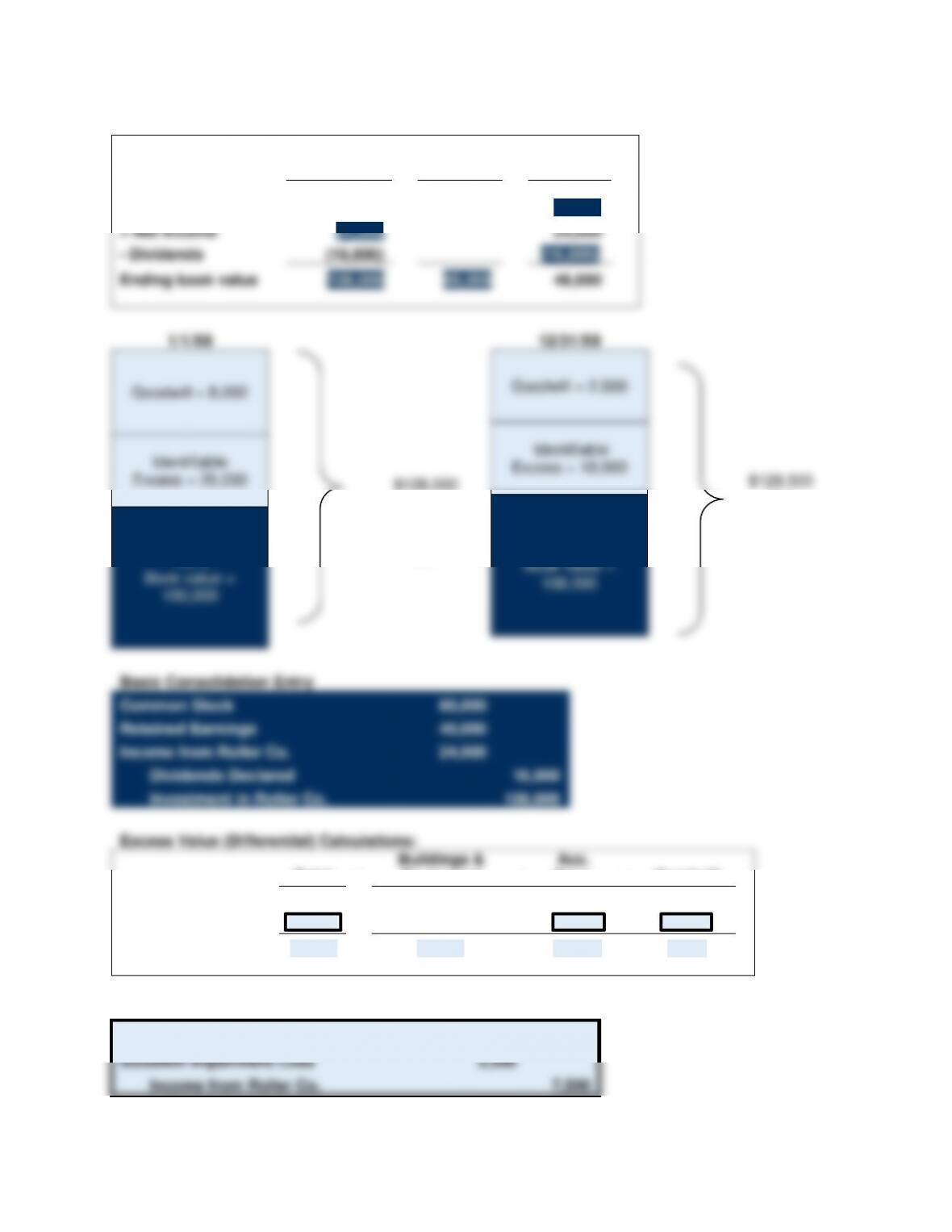

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Beginning book

value

100,000

60,000

40,000

+ Net Income

24,000

24,000

– Dividends

(16,000)

(16,000)

Ending book value

108,000

60,000

48,000

Basic Consolidation Entry

Common Stock

60,000

Retained Earnings

40,000

Income from Roller Co.

24,000

Dividends Declared

16,000

Investment in Roller Co.

108,000

Excess Value (Differential) Calculations:

=

+

+

Beginning balance

Changes

Ending balance

Amortized Excess Value Reclassification Entry:

2,000

5,500

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-59

P4–33 (continued)

Excess Value (Differential) Reclassification Entry:

Buildings & Equipment

20,000

Goodwill

2,500

Accumulated Depreciation

2,000

Investment in Roller Co.

20,500

Optional Accumulated Depreciation Consolidation Entry

Accumulated Depreciation

30,000

Building & Equipment

30,000

Investment in

Income from

Roller Co.

Roller Co.

Acquisition Price

128,000

100% Net Income

24,000

24,000

100% Net Income

16,000

100% Dividends

7,500

Excess Val. Amort.

7,500

Ending Balance

128,500

16,500

Ending Balance

108,000

Basic

24,000

20,500

Excess Reclass.

7,500

0

0

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-60

P4–33 (continued)

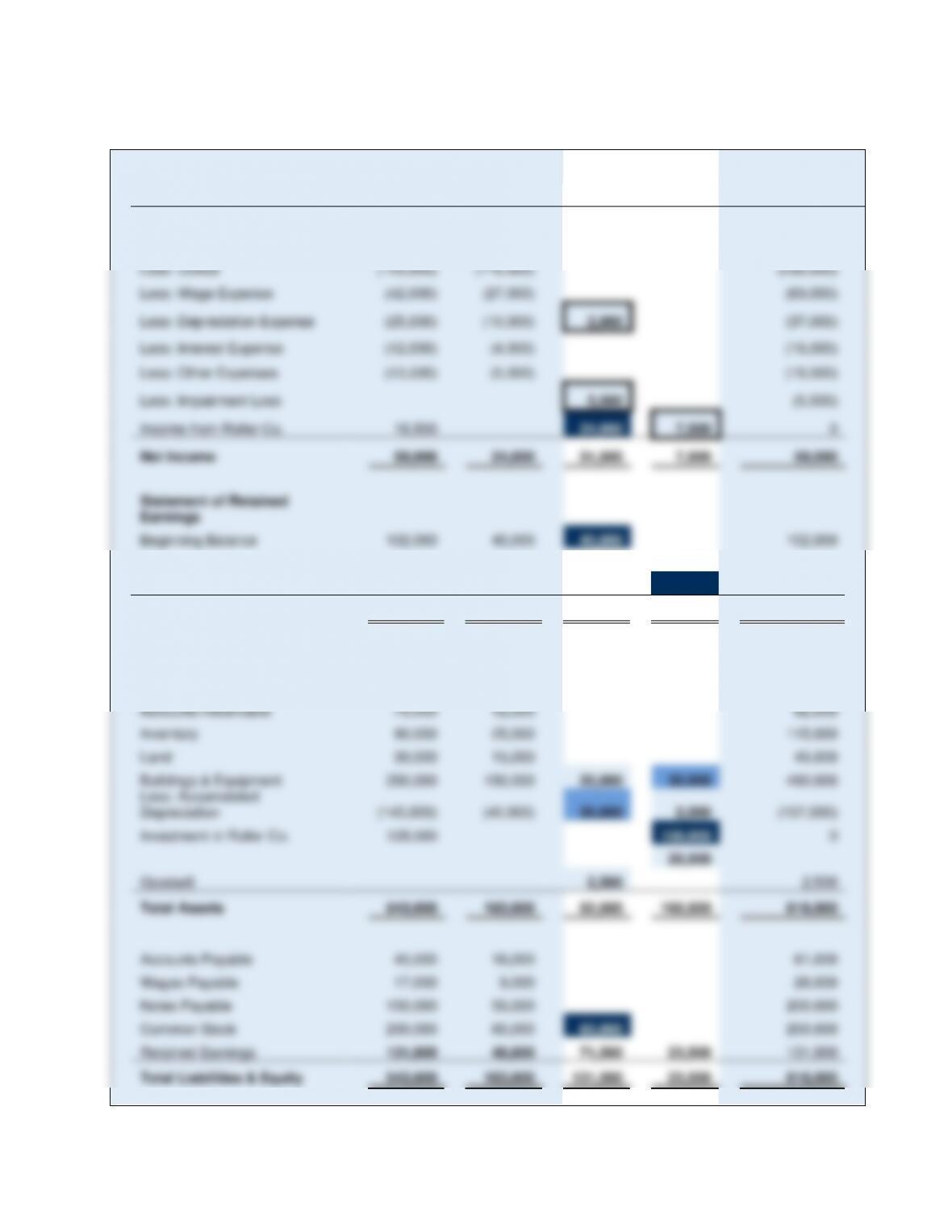

b.

Mill

Corp.

Roller

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

260,000

180,000

440,000

Less: COGS

(125,000)

(110,000)

(235,000)

Less: Wage Expense

(42,000)

(27,000)

(69,000)

Less: Depreciation Expense

(25,000)

(10,000)

2,000

(37,000)

Less: Interest Expense

(12,000)

(4,000)

(16,000)

Less: Other Expenses

(13,500)

(5,000)

(18,500)

Less: Impairment Loss

5,500

(5,500)

Income from Roller Co.

16,500

24,000

7,500

0

Net Income

59,000

24,000

31,500

7,500

59,000

Statement of Retained

Earnings

Beginning Balance

102,000

40,000

40,000

102,000

Net Income

59,000

24,000

31,500

7,500

59,000

Less: Dividends Declared

(30,000)

(16,000)

16,000

(30,000)

Ending Balance

131,000

48,000

71,500

23,500

131,000

Balance Sheet

Cash

19,500

21,000

40,500

Accounts Receivable

70,000

12,000

82,000

Inventory

90,000

25,000

115,000

Land

30,000

15,000

45,000

Buildings & Equipment

350,000

150,000

20,000

30,000

490,000

Less: Accumulated

Depreciation

(145,000)

(40,000)

30,000

2,000

(157,000)

Investment in Roller Co.

128,500

108,000

0

20,500

Goodwill

2,500

2,500

Total Assets

543,000

183,000

52,500

160,500

618,000

Accounts Payable

45,000

16,000

61,000

Wages Payable

17,000

9,000

26,000

Notes Payable

150,000

50,000

200,000

Common Stock

200,000

60,000

60,000

200,000

Retained Earnings

131,000

48,000

71,500

23,500

131,000

Total Liabilities & Equity

543,000

183,000

131,500

23,500

618,000