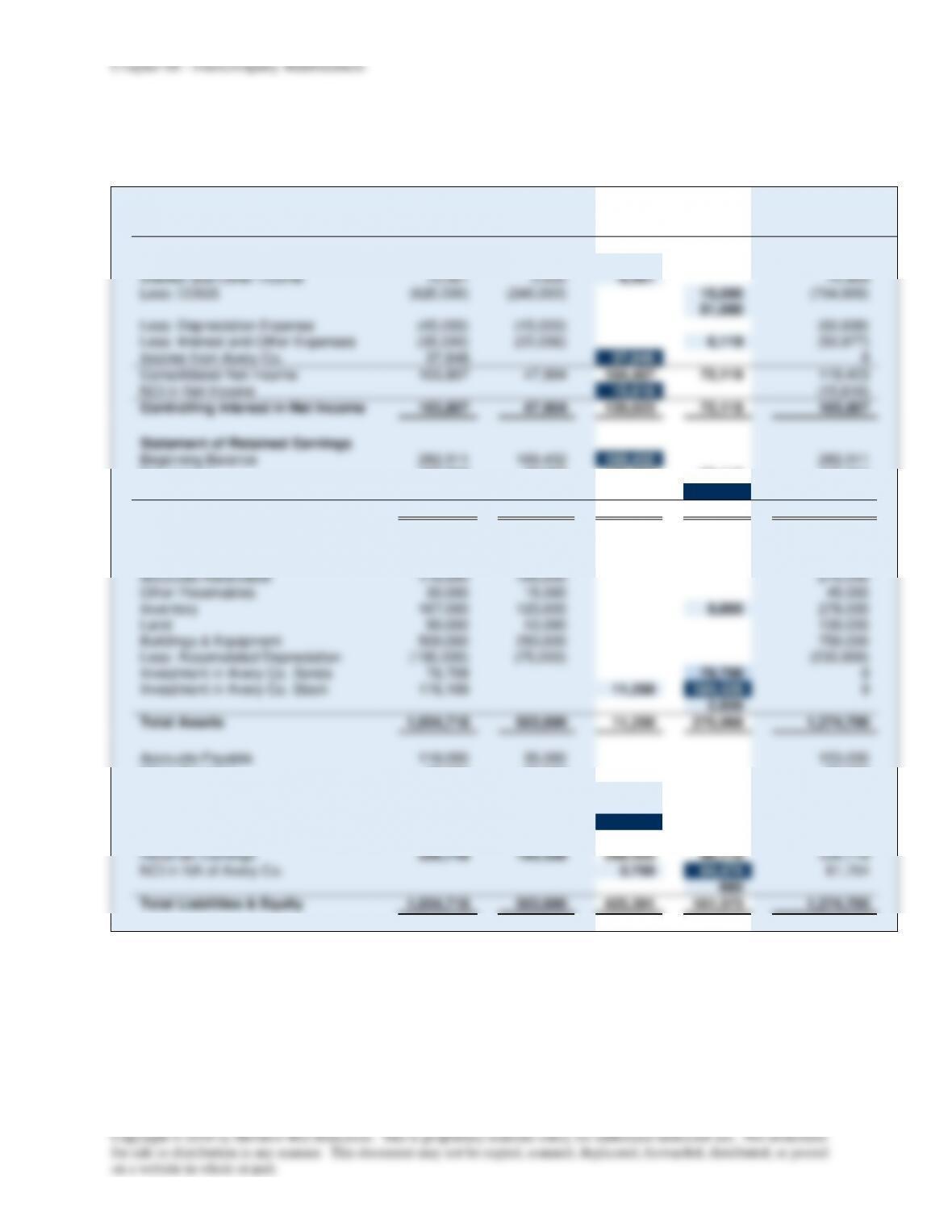

Chapter 08 – Intercompany Indebtedness

P8-24 Consolidation Worksheet — Year after Retirement

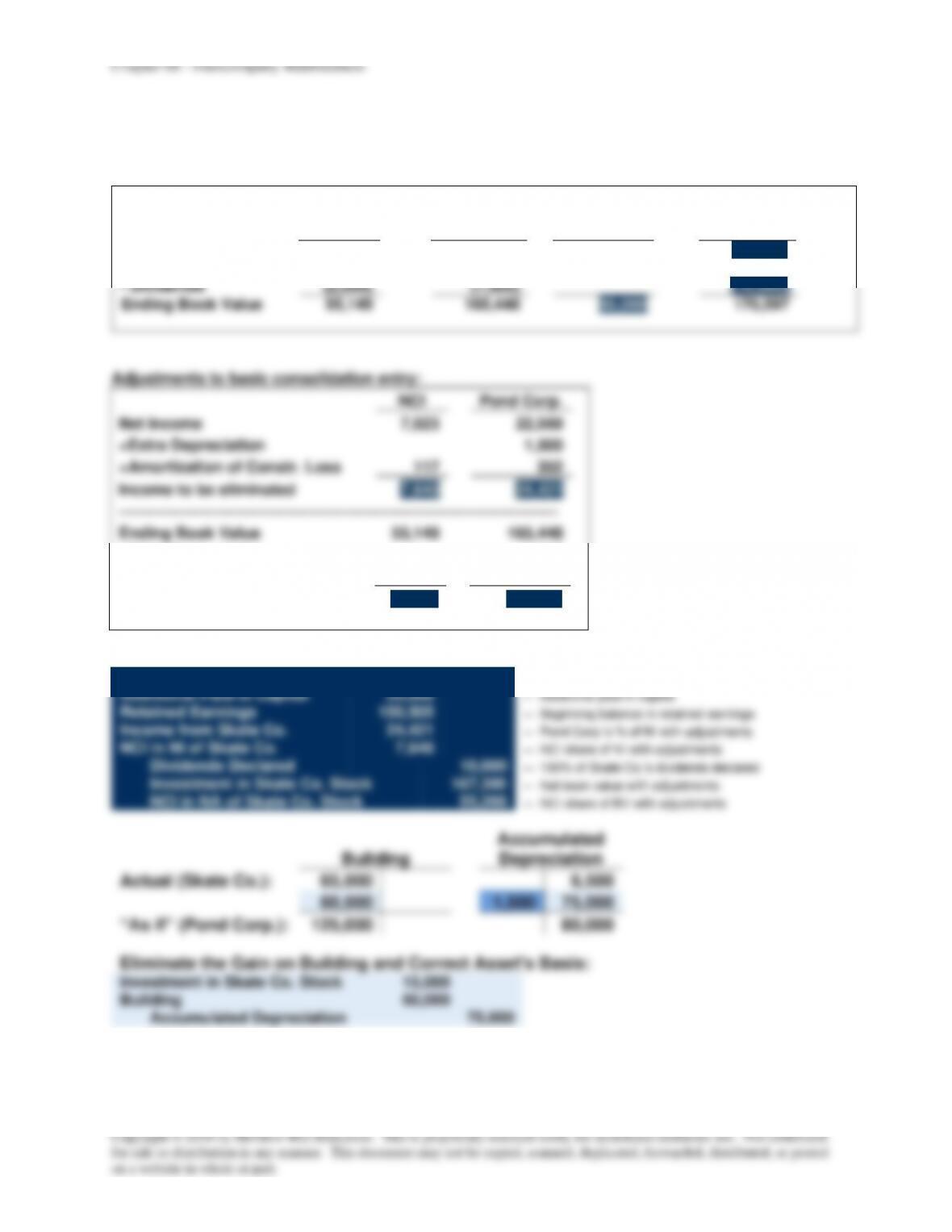

a.

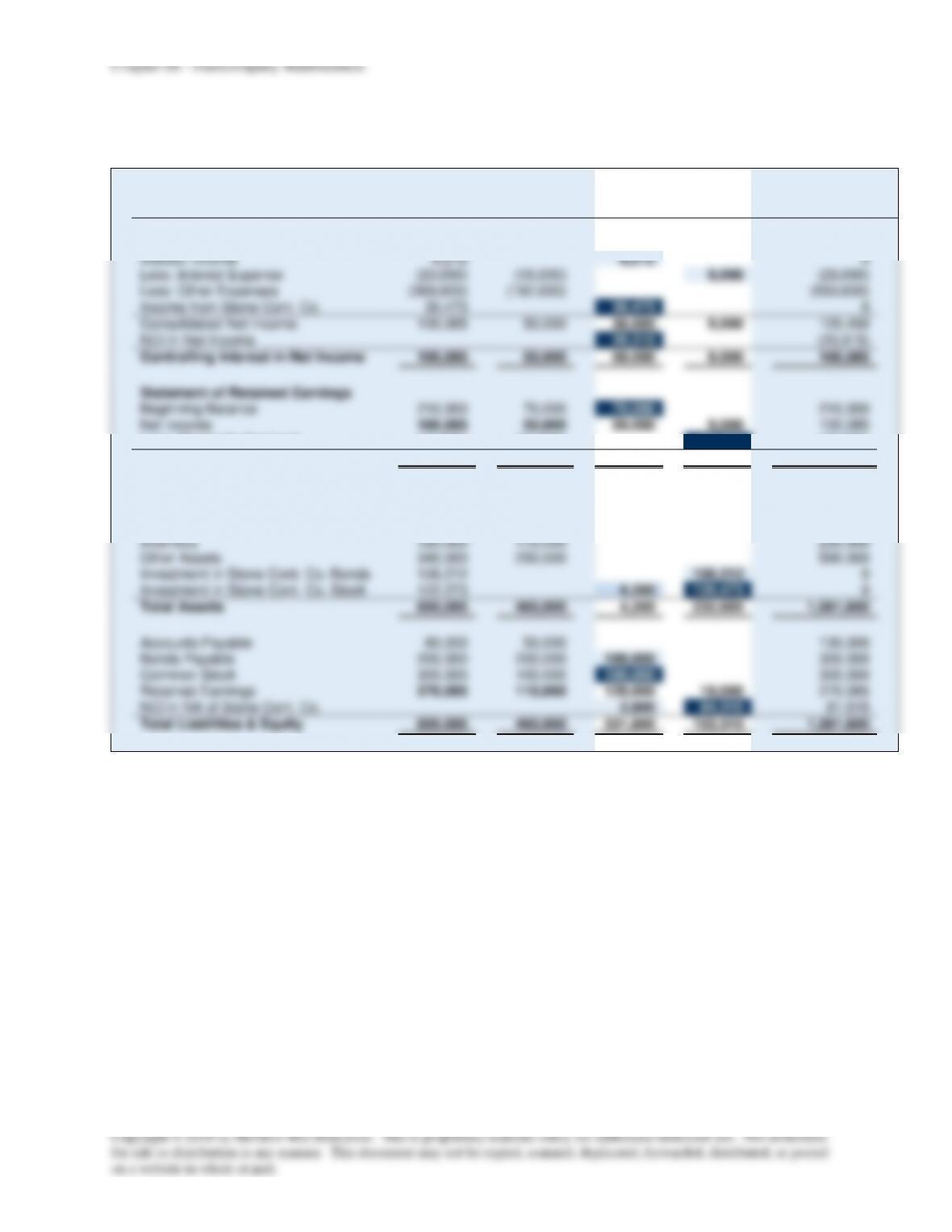

Book Value Calculations:

NCI

40%

+

Bennett

Corp.

60%

=

Common

Stock

+

Retained

Earnings

Beginning Book Value

68,000

102,000

100,000

70,000

+ Net Income

20,000

30,000

50,000

– Dividends

(4,000)

(6,000)

(10,000)

Ending Book Value

84,000

126,000

100,000

110,000

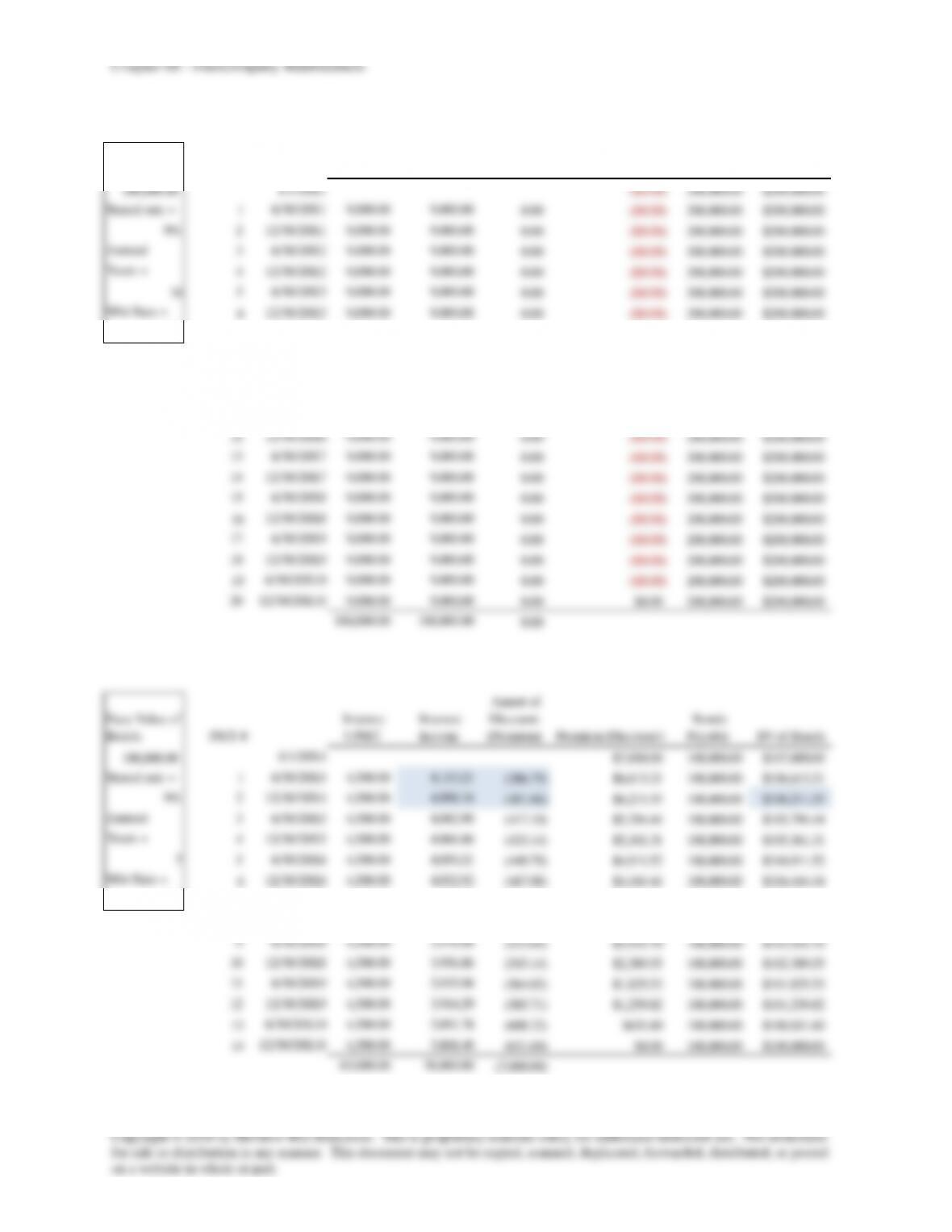

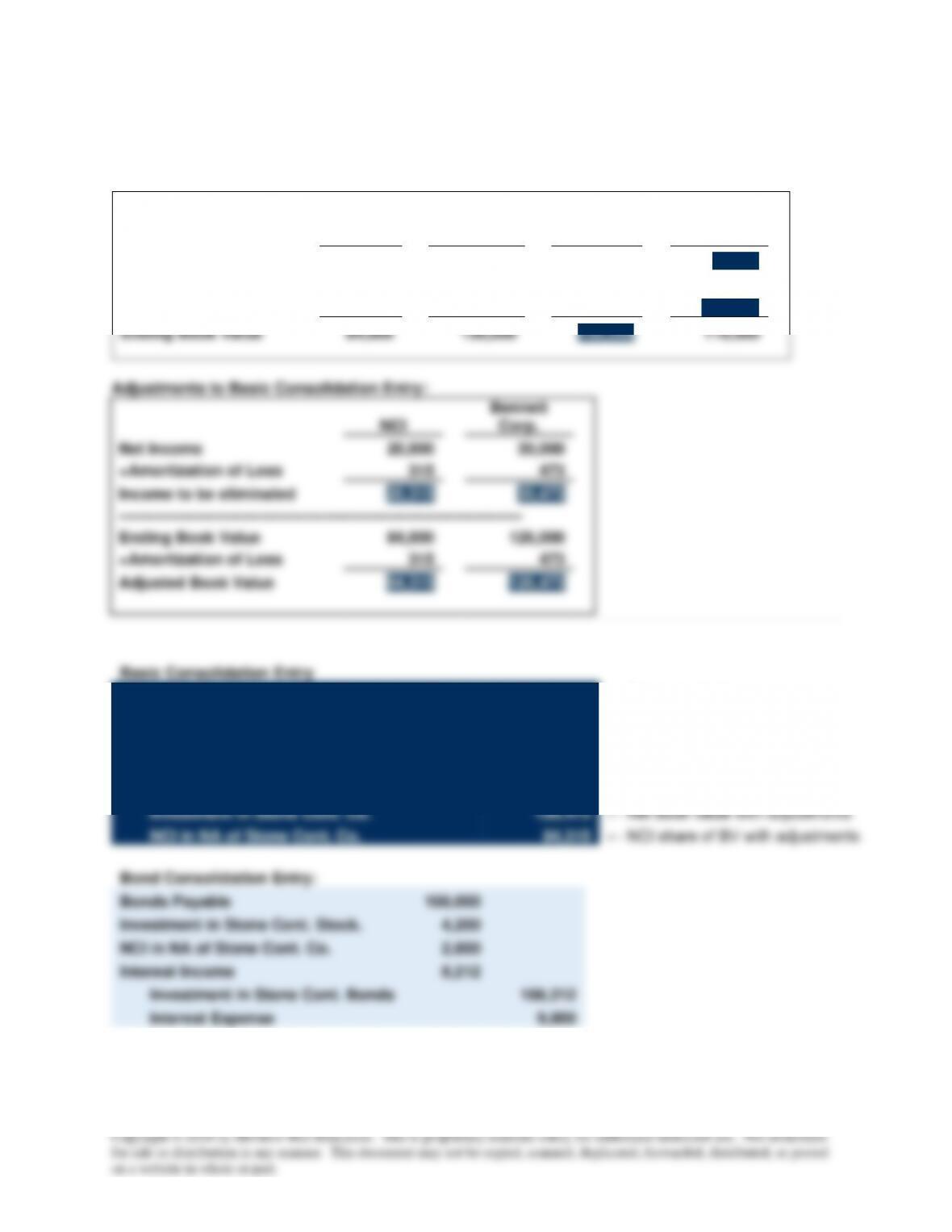

NCI

Bennett

Corp.

Net Income

20,000

30,000

+Amortization of Loss

315

473

Income to be eliminated

20,315

30,473

————————–——–——————————–————

Ending Book Value

84,000

126,000

+Amortization of Loss

315

473

Adjusted Book Value

84,315

126,473

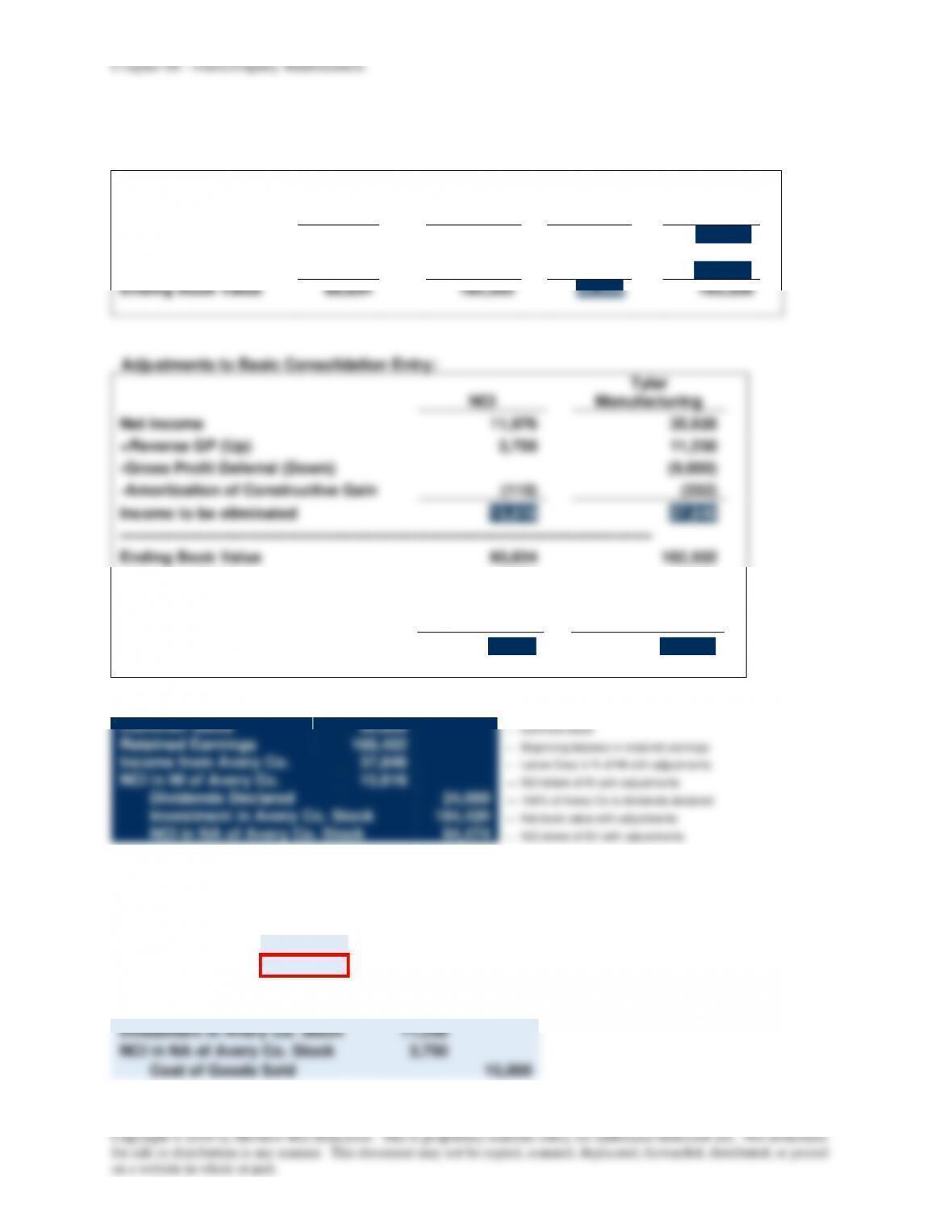

Basic Consolidation Entry

Common Stock

100,000

← Common stock

Retained Earnings

70,000

← Beginning balance in retained earnings

Income from Stone Cont. Co.

30,473

← Bennett’s % of NI with adjustments

NCI in NI of Stone Cont. Co.

20,315

← NCI share of NI with adjustments

Dividends Declared

10,000

← 100% of Stone Cont. Co.’s dividends

Investment in Stone Cont. Co.

126,473

← Net book value with adjustments

NCI in NA of Stone Cont. Co.

84,315

← NCI share of BV with adjustments

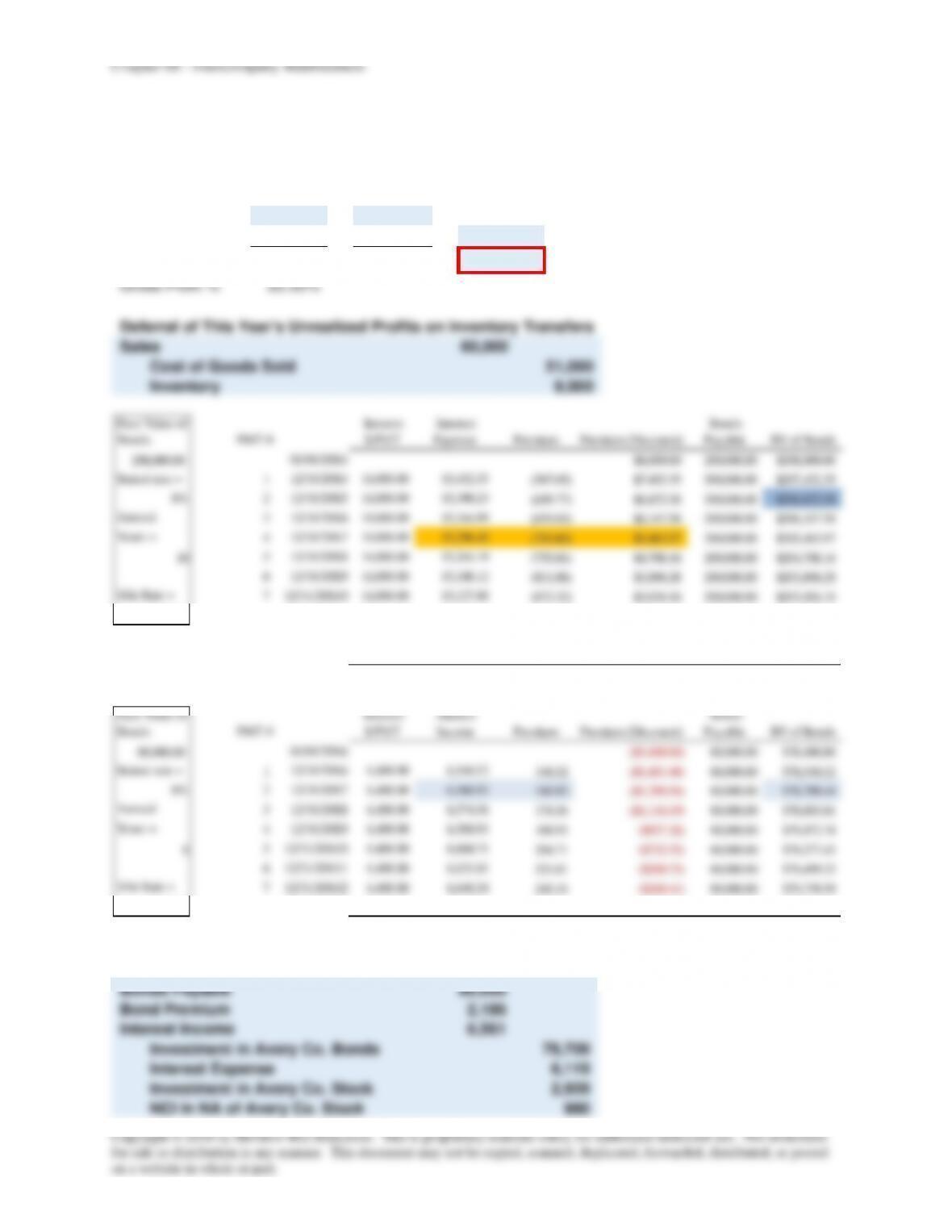

Bond Consolidation Entry:

Bonds Payable

100,000

Investment in Stone Cont. Stock.

4,200

NCI in NA of Stone Cont. Co.

2,800

Interest Income

8,212

Investment in Stone Cont. Bonds

106,212

Interest Expense

9,000