Chapter 06 – Intercompany Inventory Transactions

6.

b –

14 years = ($28,000 / [(28,000 – $20,000) / 4 years]

E6-3 Multiple Choice – Consolidated Income Statement

1.

c –

The only sales recorded are sales to non-affiliates.

2.

b –

The amount of cost of goods sold is the cost at

which Blue had produced the inventory.

3.

c –

Total income ($86,000 – $47,000)

$39,000

Income assigned to noncontrolling

interest [0.40($86,000 – $60,000)]

(10,400)

Consolidated net income assigned

to controlling interest

$28,600

E6-4 Multiple-Choice Questions — Consolidated Balances

1.

c –

The only sales recorded are sales to non-affiliates.

2.

a –

Amount paid by Lorn Corporation

$120,000

Unrealized profit

(45,000)

Actual cost

$ 75,000

Portion sold

x 0.80

Cost of goods sold

$ 60,000

3.

e –

Consolidated sales

$140,000

Cost of goods sold

(60,000)

Consolidated net income

$ 80,000

Income to Dresser’s noncontrolling

interest:

Sales

$120,000

Reported cost of sales

(75,000)

Report income

$ 45,000

Portion realized

x 0.80

Realized net income

$ 36,000

Portion to Noncontrolling

Interest

x 0.30

Income to noncontrolling

Interest

(10,800)

Income to controlling interest

$ 69,200

4.

a –

Inventory reported by Lorn

$ 24,000

Unrealized profit ($45,000 x .20)

(9,000)

Ending inventory reported

$ 15,000

E6-5 Multiple-Choice Questions — Consolidated Income Statement

1.

a –

$20,000 = $30,000 x [($48,000 – $16,000) / $48,000]

2.

d –

Sales reported by Movie Productions Inc.

$67,000

Cost of goods sold ($30,000 x 2/3)

(20,000)

Consolidated net income

$47,000

3.

a –

$7,000 = [($67,000 – $32,000) x 0.20]

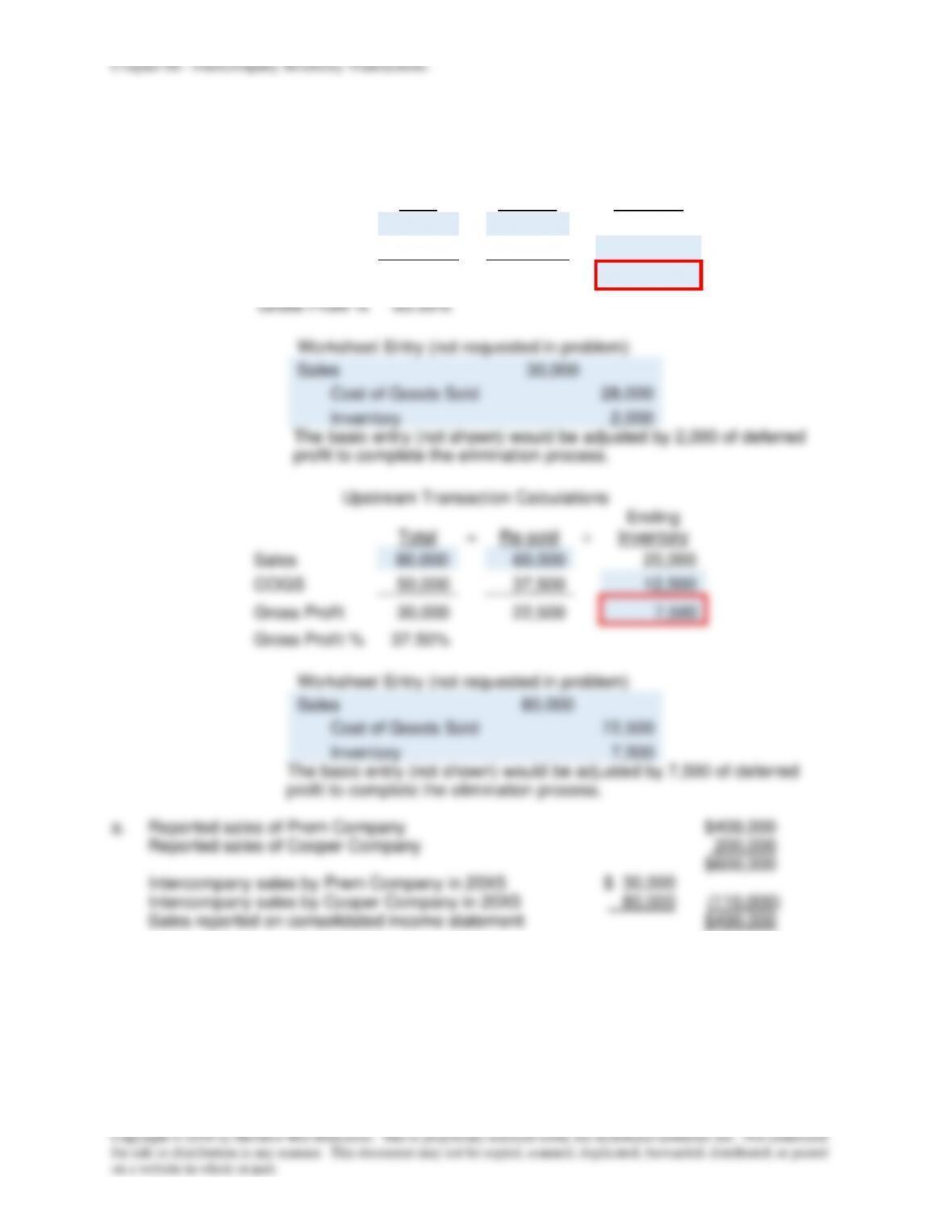

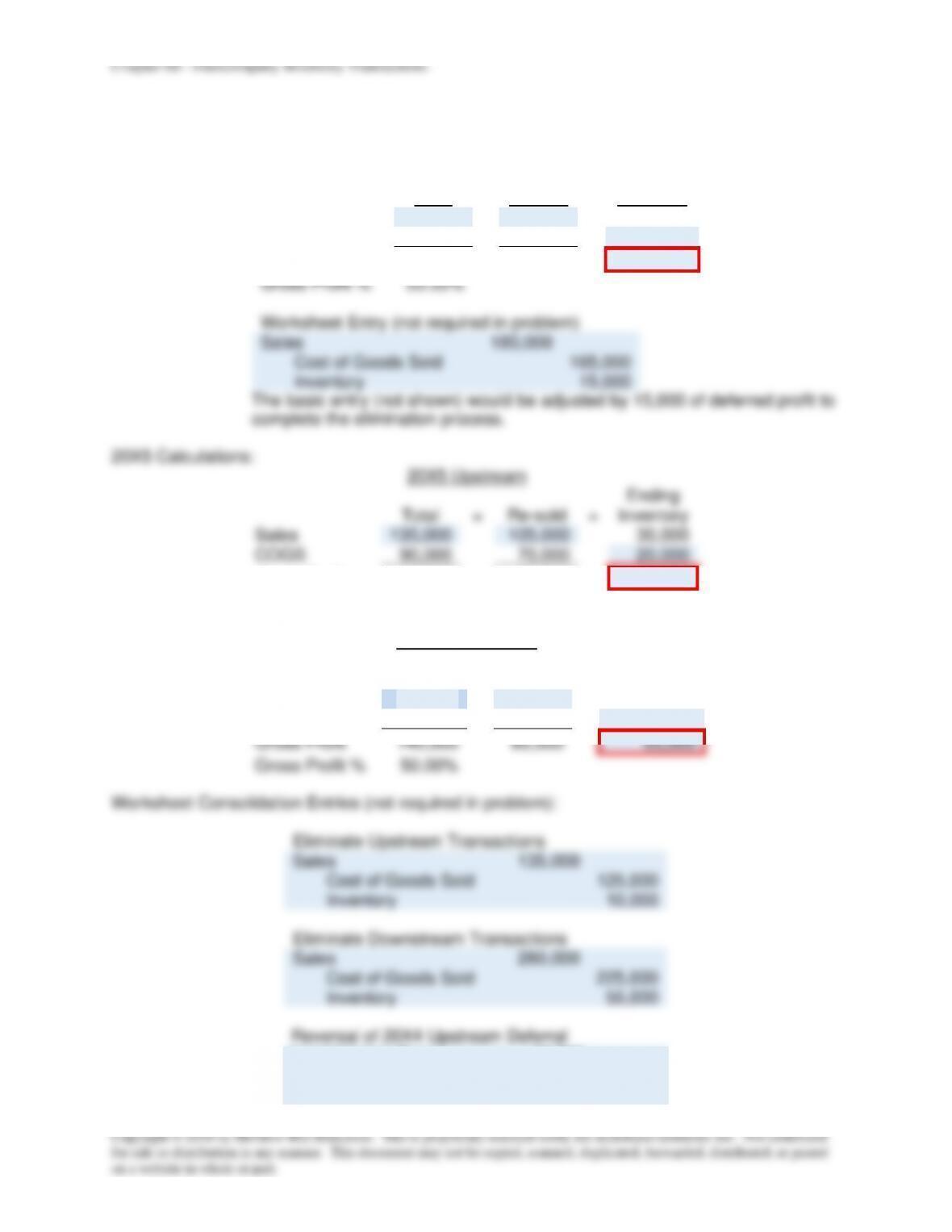

Chapter 06 – Intercompany Inventory Transactions

The basic entry (not shown) would be adjusted by 65,000 of deferred

E6-12 (continued)

a.

Consolidated net income for 20X4:

Operating income of Hollow Corporation

$160,000

Net income of Surg Corporation

90,000

$250,000

Less: Unrealized profit — Surg Corporation

(15,000)

Consolidated net income

$235,000

b.

Inventory balance, December 31, 20X5:

Inventory reported by Hollow Corporation

$ 30,000

Unrealized profit on books of Surg

Corporation

($135,000 – $90,000) x ($30,000/$135,000)

(10,000)

$20,000

Inventory reported by Surg Corporation

$110,000

Unrealized profit on books of Hollow

Corporation

($280,000 – $140,000) x ($110,000/$280,000)

(55,000)

55,000

Inventory, December 31, 20X5

$75,000

c.

Consolidated cost of goods sold for 20X5:

COGS on sale of inventory on hand January 1, 20X5

$45,000 x ($120,000 / $180,000)

$ 30,000

COGS on items purchased from Surg in 20X5

($135,000 – $30,000) x ($90,000 / $135,000)

70,000

COGS on items purchased from Hollow in 20X5

($280,000 – $110,000) x ($140,000 / $280,000)

85,000

Total cost of goods sold

$185,000

d.

Income assigned to controlling interest:

Operating income of Hollow Corporation

$220,000

Net income of Surg Corporation

85,000

$305,000

Add: Inventory profit of prior year realized in 20X5

15,000

Less:

Unrealized inventory profit — Surg Corporation

(10,000)

Unrealized inventory profit — Hollow Corporation

(55,000)

Income to noncontrolling interest

($85,000 + $15,000 – $10,000) x 0.30

(27,000)

Income assigned to controlling interest

$228,000