Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-2 Multiple-Choice Questions on Variable Interest Entities

1. c – SPE’s are typically financed primarily by debt, while equity financing is only a small

portion. SPE’s tend to be very highly leveraged.

2. d – A VIE is generally not limited as to the legal form of business that it takes (i.e.

corporation, partnership, joint venture, trust, etc.).

3. a – A primary beneficiary is defined as an enterprise that will absorb the majority of the VIE’s

expected losses, receive a majority of the VIE’s expected residual returns, or both.

However, if one entity receives the residual returns and another absorbs the expected

4. b – The company that has the most at stake is typically required to consolidate the VIE. This

has been defined as the entity receiving a majority of the VIE’s profits, and/or absorbing

the majority of its losses.

E3-3 Multiple-Choice Questions on Consolidated Balances [AICPA Adapted]

1. b – Total book value of net assets is $120,000 (50,000 + 70,000). The amount attributed to

2. b – The consolidated balance in common stock is always equal to the parent’s common

stock and the common stock of the subsidiary is eliminated.

Chapter 03 – The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

(a) Incorrect. The common stock of Kidd Company is eliminated in consolidation.

(c) Incorrect. The only amount to be reported in the consolidated balance sheet is the

amount of common stock on Pare’s books. The common stock is not allocated based on

ownership percentage, but rather is eliminated in its entirety prior to consolidation.

(d) Incorrect. The common stock of Kidd Company is eliminated, and not added to the

common stock balance of the parent.

3. a – Neely directly controls Randle, and indirectly controls Walker as a result of owning 40%

plus an additional 30% as a result of Randle’s ownership of Walker, thus Neely should

consolidate both Randle and Walker.

E3-4 Multiple-Choice Questions on Consolidation Overview

1. d – Consolidation occurs when one company acquires a controlling interest in another

company. This controlling interest is typically defined has owning greater than 50% of the

company.

2. a – The consolidated net earnings contains the net earnings of Aaron as well as the net

earnings of Belle. Thus, the consolidated net earnings are greater than just Aaron’s own

3. b – When the acquisition takes place, X Company only includes the earnings of Y Company

for the portion of the year in which a controlling ownership was held.

(a) Incorrect. Earnings of X Company for the entire year would be included in

4. d – Consolidation typically occurs when greater than 50% of the voting stock is obtained

because the parent company is said to have control over the subsidiary.

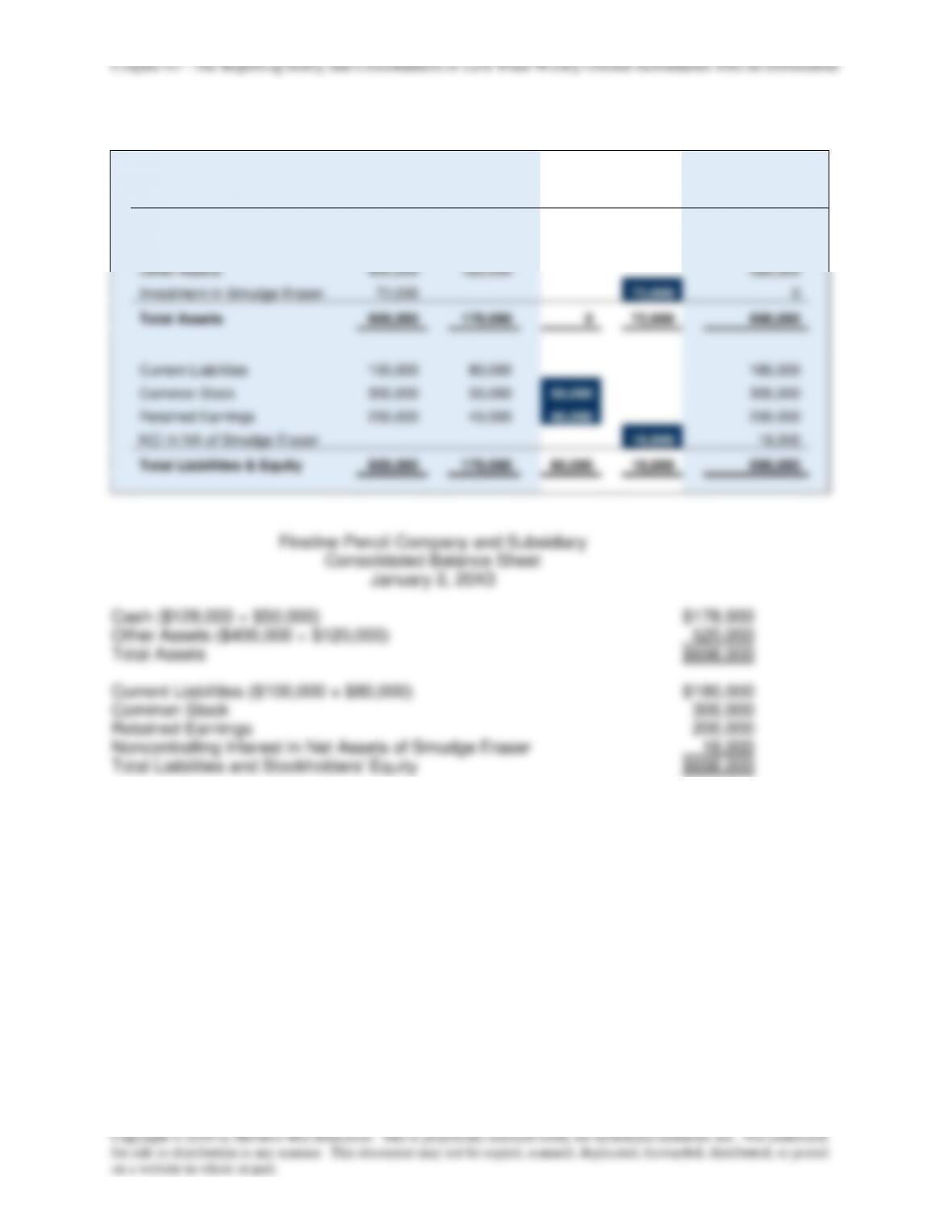

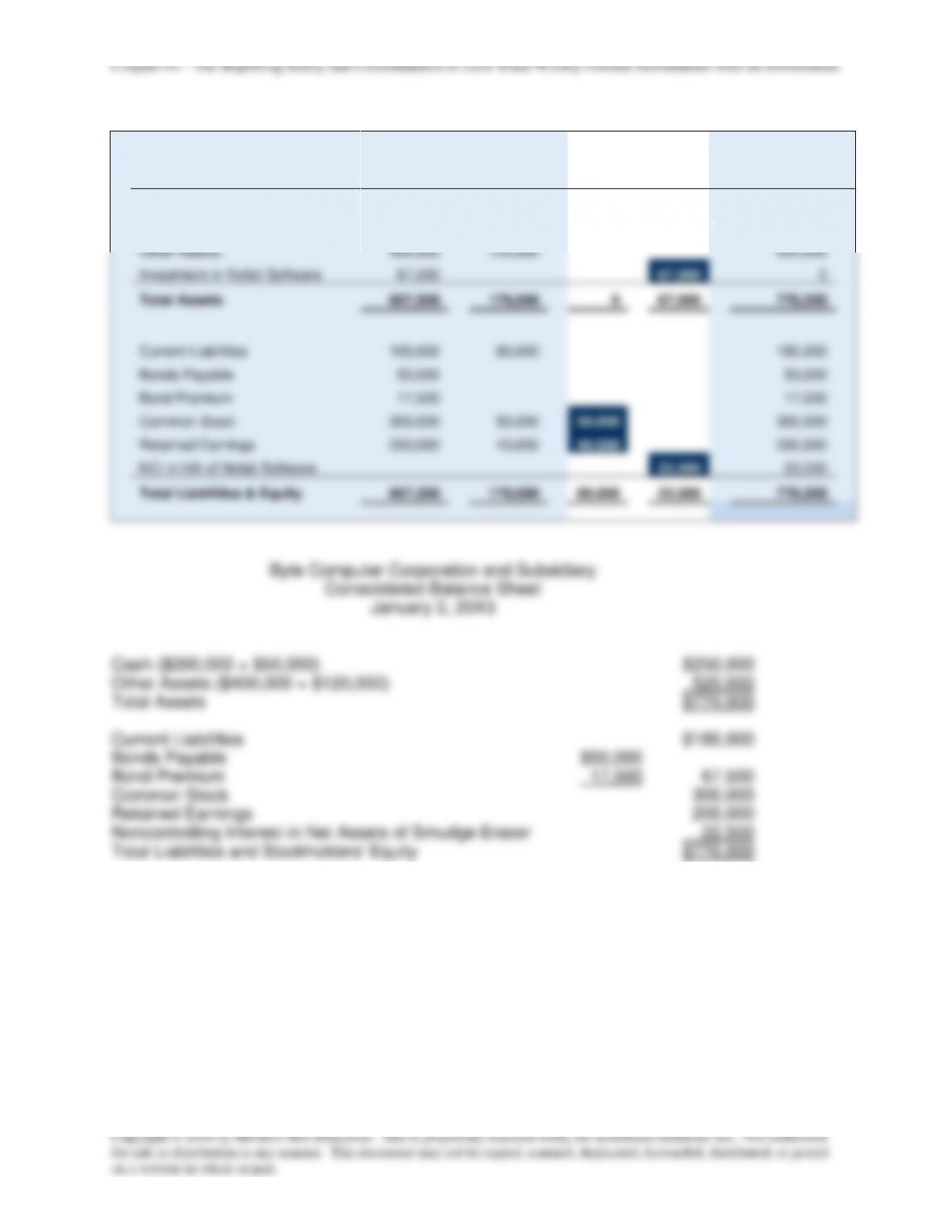

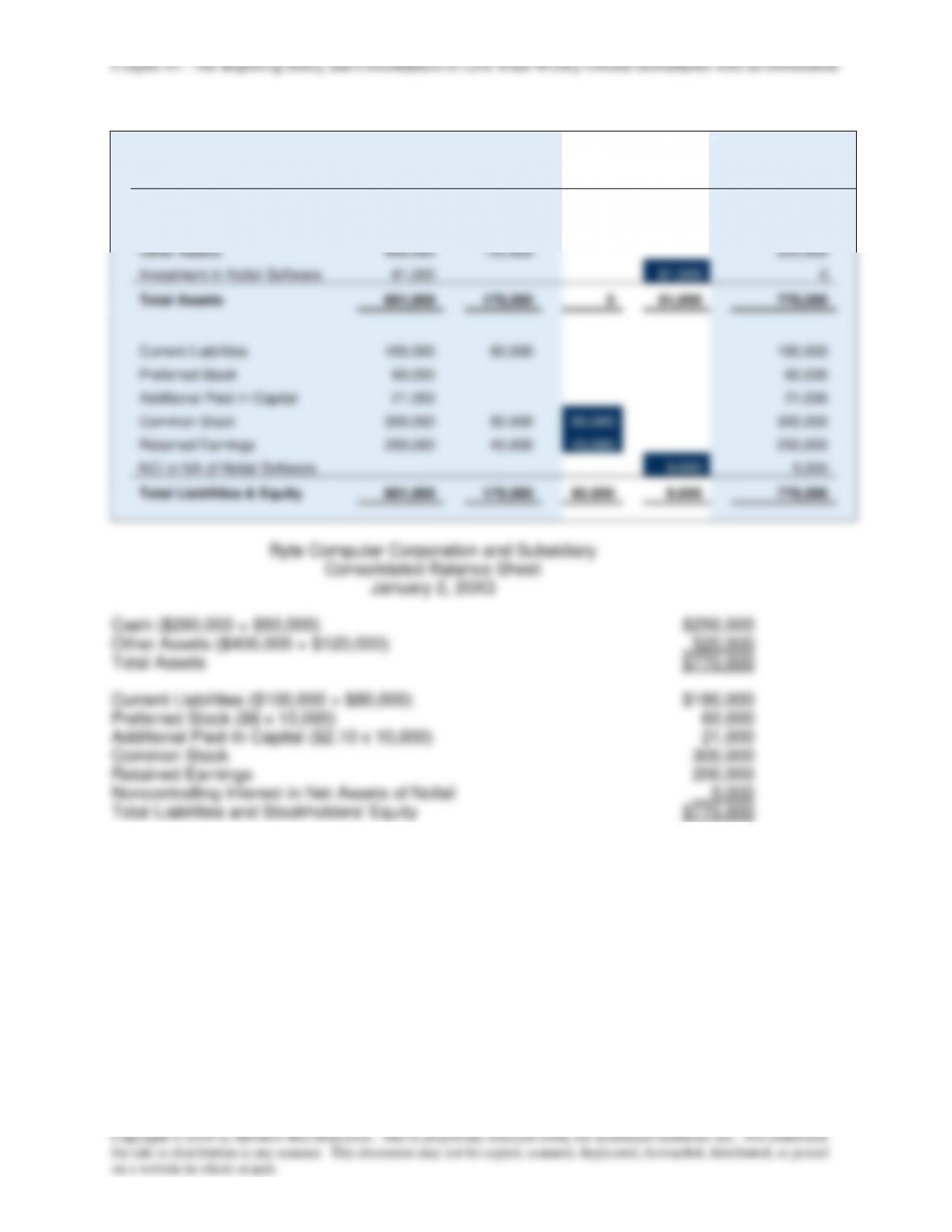

E3-5 Balance Sheet Consolidation

a. $470,000 = $470,000 – $44,000 (cash outlay) + $44,000 (investment)

b. $616,000 = ($470,000 – $44,000 (investment) + $190,000