Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

E4-7 Correction of Error

Required correcting entry:

Investment in Case Products Stock

44,000

Dividend Income

8,000

Income from Case Products

30,000

Retained Earnings

22,000

Addition to account for investment income:

20X6: $16,000

$16,000

20X7: $24,000

24,000

20X8: $32,000

32,000

$72,000

Deduction for dividends received:

20X6: $6,000

$ 6,000

20X7: $8,000

8,000

20X8: $8,000

8,000

(22,000)

Amortization of differential:

Purchase price

$56,000

Proportionate share of book value of net assets

($10,000 + $30,000)

(40,000)

Amount of differential

$16,000

Amortization for 3 years [($16,000 / 8) x 3]

(6,000)

Required correction of investment account

$44,000

Computation of correction of retained earnings of Grand Corporation

Dividend income recorded in 20X6: $6,000

$ 6,000

20X7: $8,000

8,000

($14,000)

Equity-method income in 20X6: ($16,000 – $2,000)

$14,000

20X7: ($24,000 – $2,000)

22,000

36,000

Required correction of retained earnings

$22,000

E4-8 Differential Assigned to Land and Equipment

(1)

Investment in Stafford Corporation Stock

65,000

Cash

65,000

Record purchase of Stafford Stock.

(2)

Cash

4,500

Investment in Stafford Corporation Stock

4,500

Record dividend from Stafford

(3)

Investment in Stafford Corporation Stock

12,000

Income from Stafford

12,000

Record equity-method income

(4)

Income from Stafford

1,000

Investment in Stafford Corporation Stock

1,000

Amortize differential assigned to equipment.

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

4. b – $550,000 = $1,500,000 – [(100,000 + 200,000 + 450,000 +1,000,000) – (300,000 +

5. a – The consolidated balance sheet should only show the retained earnings balance of the

parent company.

E4–11 Multiple-Choice Questions on Consolidation [AICPA Adapted]

1. c – Goodwill is not amortized, but instead is tested for impairment at least annually.

(a) Incorrect. Goodwill is not amortized.

2. a – Goodwill is not amortized, thus no amortization expense is recorded. Because goodwill

was found to be unimpaired, the entire amount of the existing goodwill would be reported.

3. d – All intercompany loans and profits must be eliminated in a consolidation, thus the entire

balances should be eliminated.

4. c – $400,000 = $1,700,000 – $1,300,000

Basic Consolidation Entry

Common stock

20,000

Retained earnings

37,000

Investment in Brown Co.

Excess Value (Differential) Calculations:

=

+

+

Balances

Excess Value (Differential) Reclassification Entry:

Inventory

Buildings & Equipment

Goodwill

E4–12 Consolidation entries with Differential

a.

Equity Method Entries on Tower Corp.’s Books:

Investment in Brown Co.

100,000

Cash

100,000

Record the initial investment in Brown Co.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

57,000

20,000

37,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

E4-12 (continued)

Investment in

Brown Co.

Acquisition Price

100,000

57,000

Basic

43,000

Excess Reclass.

0

b. Journal entries used to record transactions, adjust account balances, and close income

and revenue accounts at the end of the period are recorded in the company’s books and

change the recorded balances. On the other hand, consolidation entries are entered only

in the consolidation worksheet to facilitate the preparation of consolidated financial

statements. As a result, they do not change the balances recorded in the company’s

accounts and must be reentered each time a consolidation worksheet is prepared.

E4–13 Balance Sheet Consolidation

Equity Method Entries on Reed Corp.’s Books:

Investment in Thorne Corp.

395,000

Cash

395,000

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

360,000

120,000

240,000

1/1/X4

Goodwill = 19,000

Identifiable

Excess = 16,000

$395,000

Initial

investment

in Thorne

Corp.

100%

Book value =

360,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-16

Basic Consolidation Entry

Common Stock

120,000

Retained Earnings

240,000

Investment in Thorne Corp.

360,000

Excess Value (Differential) Calculations:

Total

=

Buildings

+

Inventory

+

Goodwill

Balances

35,000

(20,000)

36,000

19,000

Excess Value (Differential) Reclassification Entry:

Inventory

36,000

Goodwill

19,000

Buildings

20,000

Investment in Thorne Corp.

35,000

Investment in

Thorne Corp.

Acquisition Price

395,000

360,000

Basic

35,000

Excess Reclass.

0

E4–14 Acquisition with Differential

a. Goodwill is $60,000, computed as follows:

Book value of Conger’s net assets:

Common stock outstanding

$ 80,000

Retained earnings

130,000

$210,000

Fair value increment:

Land ($100,000 – $80,000)

$ 20,000

Buildings ($400,000 – $220,000)

180,000

200,000

Fair value of net assets

$410,000

Fair value of consideration given

(470,000)

Goodwill

$ 60,000

b.

Equity Method Entries on Road Corp.’s Books:

Investment in Conger Corp.

470,000

Cash

470,000

Record the initial investment in Conger Corp.

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

210,000

80,000

130,000

1/1/X2

Goodwill = 60,000

Identifiable

Excess = 200,000

$470,000

Initial

investment

in Conger

Corp.

100%

Book value =

210,000

Basic Consolidation Entry

Common stock

80,000

Retained earnings

130,000

Investment in Conger Corp.

210,000

Excess Value (Differential) Calculations:

Total

=

Land

+

Buildings

+

Goodwill

Balances

260,000

20,000

180,000

60,000

Excess Value (Differential) Reclassification Entry:

Land

20,000

Buildings

180,000

Goodwill

60,000

Investment in Conger Corp.

260,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

E4–15 Balance Sheet Worksheet with Differential

a.

Equity Method Entries on Blank Corp.’s Books:

Investment in Faith Corp.

189,000

Cash

189,000

Record the initial investment in Faith Corp.

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

150,000

60,000

90,000

Basic Consolidation Entry

Excess Value (Differential) Calculations:

Inventory

+

Balances

Excess Value (Differential) Reclassification Entry:

Inventory

Buildings & Equipment

Investment in Faith Corp.

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

4-19

E4-15 (continued)

Investment in

Faith Corp.

Acquisition Price

189,000

150,000

Basic

39,000

Excess Reclass.

0

Blank

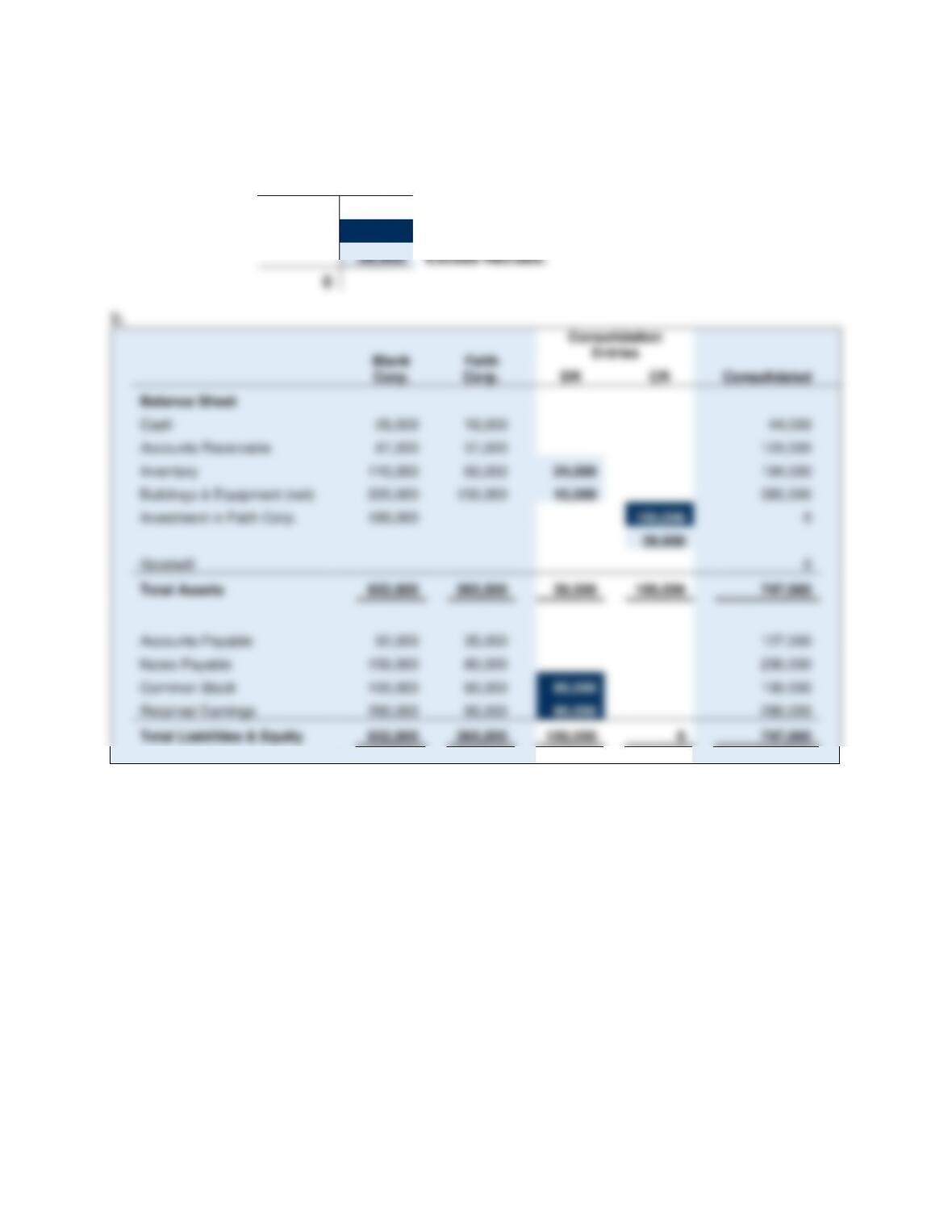

Corp.

Faith

Corp.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

26,000

18,000

44,000

Accounts Receivable

87,000

37,000

124,000

Inventory

110,000

60,000

24,000

194,000

Buildings & Equipment (net)

220,000

150,000

15,000

385,000

Investment in Faith Corp.

189,000

150,000

0

39,000

Goodwill

0

Total Assets

632,000

265,000

39,000

189,000

747,000

Accounts Payable

92,000

35,000

127,000

Notes Payable

150,000

80,000

230,000

Common Stock

100,000

60,000

60,000

100,000

Retained Earnings

290,000

90,000

90,000

290,000

Total Liabilities & Equity

632,000

265,000

150,000

0

747,000

Chapter 04 – Consolidation of Wholly Owned Subsidiaries Acquired at More than Book Value

E4–16 Worksheet for Wholly Owned Subsidiary

a.

Equity Method Entries on Gold Enterprises’ Books:

Investment in Premium Builders

167,000

Cash

167,000

Record the initial investment in Premium Builders

Book Value Calculations:

Total Book

Value

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

150,000

140,000

10,000

Basic Consolidation Entry

Common Stock

140,000

Retained Earnings

10,000

Investment in Premium Builders

Excess Value (Differential) Calculations:

=

+

Inventory

+

Balances

17,000

Excess Value (Differential) Reclassification Entry:

Inventory

Buildings & Equipment