Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP

15-7

DESCRIPTIONS OF CASES, EXERCISES, AND PROBLEMS

C15-1

LO 15-1,

LO 15-5

30 min.

E

Partnership Agreement

This case points out the necessity for a partnership agreement and focuses on the

need to define the accounting treatment of salaries and bonuses.

C15-2

LO 15-6

30 min.

M

Comparisons of Bonus, Goodwill, and Asset Revaluation Methods

Students are asked to evaluate and discuss the three alternative methods of

accounting for the admission of a new partner.

C15-3

LO 15-1

45 min.

M

Uniform Partnership Act Issues

Research case requiring reference to the UPA 1997 to address several specific

partnership issues.

C15-4

LO 15-1

20 min.

M

Defining Partners’ Authority

Students are to prepare a memo to discuss the rights of each partner to engage in

transactions on behalf of the partnership and how a partnership can restrict a

partner’s authority to engage in specific types of transactions.

C15-5

LO 15-4,

LO 15-5

25 min.

M

Preferences for Using GAAP for Partnership Accounting

Students are to prepare a memo to discuss the use of generally accepted

accounting principles (GAAP) for a partnership while admitting a new member

into the partnership.

E15-1

LO 15-3

15 min.

E

Multiple-Choice on Initial Investment [AICPA Adapted]

Five multiple-choice questions on the accounting for initial investments for

various cases.

E15-2

LO 15-5

20 min.

E

Division of Income—Multiple Bases

Income distribution schedules are required for a multiple base illustration for two

different income amounts. One of the amounts results in a deficit that must be

distributed.

E15-3

LO 15-5

30 min.

M

Division of Income—Interest on Capital Balances

Students must compute the average capital balances during the period in order to

determine the amount of interest that will be distributed to each partner as part of

an income distribution.

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP

15-8

E15-4

LO 15-5

25 min.

M

Distribution of Partnership Income and Preparation of a Statement of

Partners’ Capital

Students are asked to distribute partnership net income, prepare the statement of

partners’ capital, and then analyze the effects of changes in the partners’ salaries.

E15-5

LO 15-1

through

LO 15-6

20 min.

E

Matching Terms

Thirteen terms are presented for which students must match the appropriate

description.

E15-6

LO 15-6

30 min.

M

Admission of a Partner

Journal entries are required for several alternative investment amounts and

percentage of capital amounts. Students must compute the proportionate book

value received under the alternatives.

E15-7

LO 15-6

40 min.

H

Admission of a Partner

Six independent cases of investment amounts and methods of recording the

admission of a new partner must be analyzed and journal entries for each of the

six cases are required.

E15-8

LO 15-6

25 min.

M

Multiple-Choice Questions on the Admission of a Partner

Eight questions presenting different types of admission situations, including

direct purchase.

E15-9

LO 15-6

30 min.

M

Withdrawal of a Partner

Journal entries are required for each of three alternative methods of accounting

for the withdrawal of a partner. The bonus method is contrasted with recognizing

just the retired partner’s portion of goodwill and with recognizing all the implied

goodwill.

E15-10

LO 15-6

25 min.

M

Retirement of a Partner

Six cases are presented for which students must determine the method used to

account for the retirement of a partner.

P15-11

LO 15-6

60 min.

H

Admission of a Partner

Seven alternatives are examined for accounting for the admission of a new

partner to a partnership. Students must provide the journal entries required for

each of the seven alternatives.

P15-12

LO 15-5

50 min.

H

Division of Income

Students are asked to prepare income distribution schedules for three alternative

distribution plans. The plans include interest on average capital, which must be

computed, salaries, and bonuses.

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP

15-9

P15-13

LO 15-6

45 min.

M

Determining a New Partner’s Investment Cost

Students are presented with seven independent cases for which they must

determine the amount of investment required of a new partner. The cases include

bonus, goodwill, and revaluation of assets.

P15-14

LO 15-5

50 min.

H

Division of Income

Students are asked to prepare income distribution schedules for three alternative

distribution plans. One of the distribution plans requires the final distribution of a

deficit created in an earlier stage of the income distribution process. Alternative

bonus plans are used.

P15-15

LO 15-6

50 min.

H

Withdrawal of a Partner under Various Alternatives

Journal entries are required to record the withdrawal of a partner under seven

independent alternatives including revaluing net assets and recording goodwill.

P15-16

LO 15-5,

LO 15-6

30 min.

M

Multiple-Choice Questions—Initial Investments, Division of Income,

Admission and Retirement of a Partner [AICPA Adapted]

Nine multiple-choice questions on a variety of partnership issues including

accounting for the creation of a partnership, division of income, and accounting

for the withdrawal of a partner recording a bonus or goodwill.

P15-17

LO 15-3

through

LO 15-6

60 min.

H

Partnership Formation, Operation, and Changes in Ownership

A comprehensive problem requiring journal entries to record the formation and

operation of a partnership, preparation of the partnership’s income statement and

balance sheet, and recording of the admission of a new partner.

P15-18A

30 min.

M

Initial Investments and Tax Bases [AICPA Adapted]

Students are required to compare GAAP accounting and tax accounting for the

initial contribution of several long-term assets including a building that is subject

to a mortgage. Instructors not wishing to cover the tax method may assign

requirement a of the problem only.

P15-19

LO 15-3

through

LO 15-6

50 min.

M

Formation of a Partnership and Allocation of Profit and Loss

This is a two-part problem involving a new partnership formed by two sole

proprietors. Part I requires that students prepare a classified balance sheet

immediately after formation of the new entity. Part II requires that students

prepare an income statement, a schedule showing the allocation of partnership

income, and calculate partners’ capital balances at the end of the first year after

the partnership was formed. In addition, students must calculate what partnership

income must be so that each partner receives the same income.

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP

15–10

OTHER RESOURCES Chapter 15

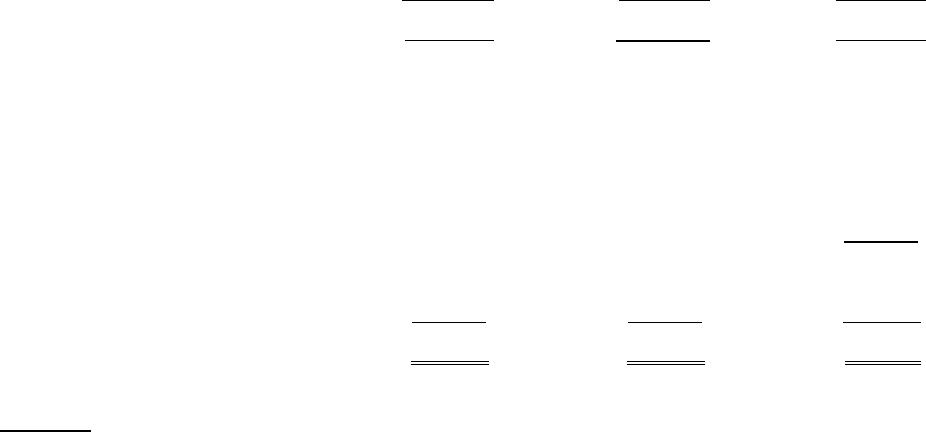

Allocation of Income/Loss

Allocate income/loss before taxes (partnerships don’t pay taxes) follow the partnership

agreement with regard to:

interest on capital balances

salaries to partners

bonus to partners

residual in profit and loss sharing ratio (assume equal unless otherwise stated)

Example:

Partners A and B share profits and losses in ratio of 3:2

Partner A receives a salary of $20,000 and Partner B of $14,000. Partner A receives a

bonus of 10% of net income after deducting the bonus. Interest of 10% is paid on average

capital balances of $70,000 for A and $90,000 for B. Profits for the period are $44,000.

Partners

A

B

Total

Profit percentage

60%

40%

100%

Net income

$ 44,000

Salary

$20,000

$14,000

(34,000)

Bonus**

4,000

(4,000)

Interest

7,000

9,000

(16,000)

Residual (Deficit)

(10,000)

Allocate in P&L ratio

(6,000)

(4,000)

10,000

Total

$25,000

$19,000

$ -0-

** Bonus

B

=

.10 (NI-B)

B

=

.10NI-.10B

1.1B

=

.10NI

1.1B

=

.10 (44,000)

1.1B

=

4,400

B

=

4,000

Chapter 15 – PARTNERSHIPS: FORMATION, OPERATION, AND CHANGES IN MEMBERSHIP

15–11

Overview of Accounting for Admission of a New Partner

PARTNERSHIPS: CHANGES IN MEMBERSHIP

New partners proportion

of the partnership’s book

value

=

Prior capital of

present partners

+

Investment of

new partner

X

Percentage of

capital to new

partner

Step 1: Compare

Proportionate Book

Value and Investment of

New Partner

Step 2: Alternative Methods

to Account for Admission

Key Observations

Investment cost greater

than Book value

1. Revalue net assets up to

market value and allocate

to prior partners.

2. Record unrecognized

goodwill and allocate to

prior partners.

3. Assign bonus to prior

partners.

• Prior partners receive asset

valuation increase, goodwill, or

bonus indicated by the excess of

new partner’s investment over

book value of the capital share

initially assignable to new

partner.

• Recording asset valuation

increase or prior partners’

goodwill increases total resulting

partnership capital.

Investment cost equal to

Book value

1. No revaluations, bonus, or

goodwill.

• No additional allocations

necessary because new partner

will receive a capital share equal

to the amount invested.

• Total resulting partnership

capital equals prior partners’

capital plus investment of new

partner.

Investment cost less than

Book value

1. Revalue net assets down

to market value and

allocate to prior partners.

2. Recognize goodwill

brought in by new

partner.

3. Assign bonus to new

partner.

• Prior partners are assigned the

reduction of asset values

occurring before admission of

the new partner. Alternatively,

new partner is assigned goodwill

or bonus as part of admission

incentive.

• Recording asset valuation

decrease reduces total resulting

capital, while recording new

partner’s goodwill increases total

resulting capital.