Chapter 10 – Additional Consolidation Reporting Issues

P10-30 Computations Involving Tax Allocation

a.

Equity-method journal entries recorded by Broom Manufacturing:

Investment in Satellite Industries

142,500

Income from Satellite Industries

142,500

Record equity-method income for 20X5: $190,000 x 0.75

Cash

112,500

Investment in Satellite Industries

112,500

Record dividends for 20X5: $150,000 x 0.75

b.

Income assigned to noncontrolling interest:

Net income of Satellite Industries

$190,000

Unrealized inventory profit ($30,000 x 0.60)

(18,000)

Unrealized profit on sale of land ($120,000 x 0.60)

(72,000)

Satellite’s realized net income

$100,000

Proportion of stock held by noncontrolling interest

x 0.25

Income to noncontrolling interest

$ 25,000

c.

Consolidated net income and income to controlling Interest:

Operating income of Broom Manufacturing

$700,000

Inventory profits realized in 20X5

20,000

Realized operating income of Broom Manufacturing

$720,000

Realized income of Satellite Industries

100,000

Consolidated income before provision for taxes

$820,000

Provision for income taxes on:

Operating income ($720,000 x 0.40)

$288,000

Income from Satellite Industries ($112,500 x 0.20 x 0.40)

9,000

(297,000)

Consolidated Net Income

$523,000

Income to noncontrolling interest

(25,000)

Income to controlling interest

$498,000

d.

Net assets assigned to noncontrolling interest in consolidated balance sheet at

December 31, 20X5:

Net assets reported by Satellite Industries

$900,000

Less: Unrealized inventory profits ($30,000 x 0.60)

(18,000)

Unrealized profit on land ($120,000 x 0.60)

(72,000)

Realized net assets of Satellite Industries

$810,000

Proportion of stock held by noncontrolling interest

x .25

Net assets assigned to noncontrolling interest

$202,500

P10-31 Worksheet Involving Tax Allocation

a. Consolidation entries:

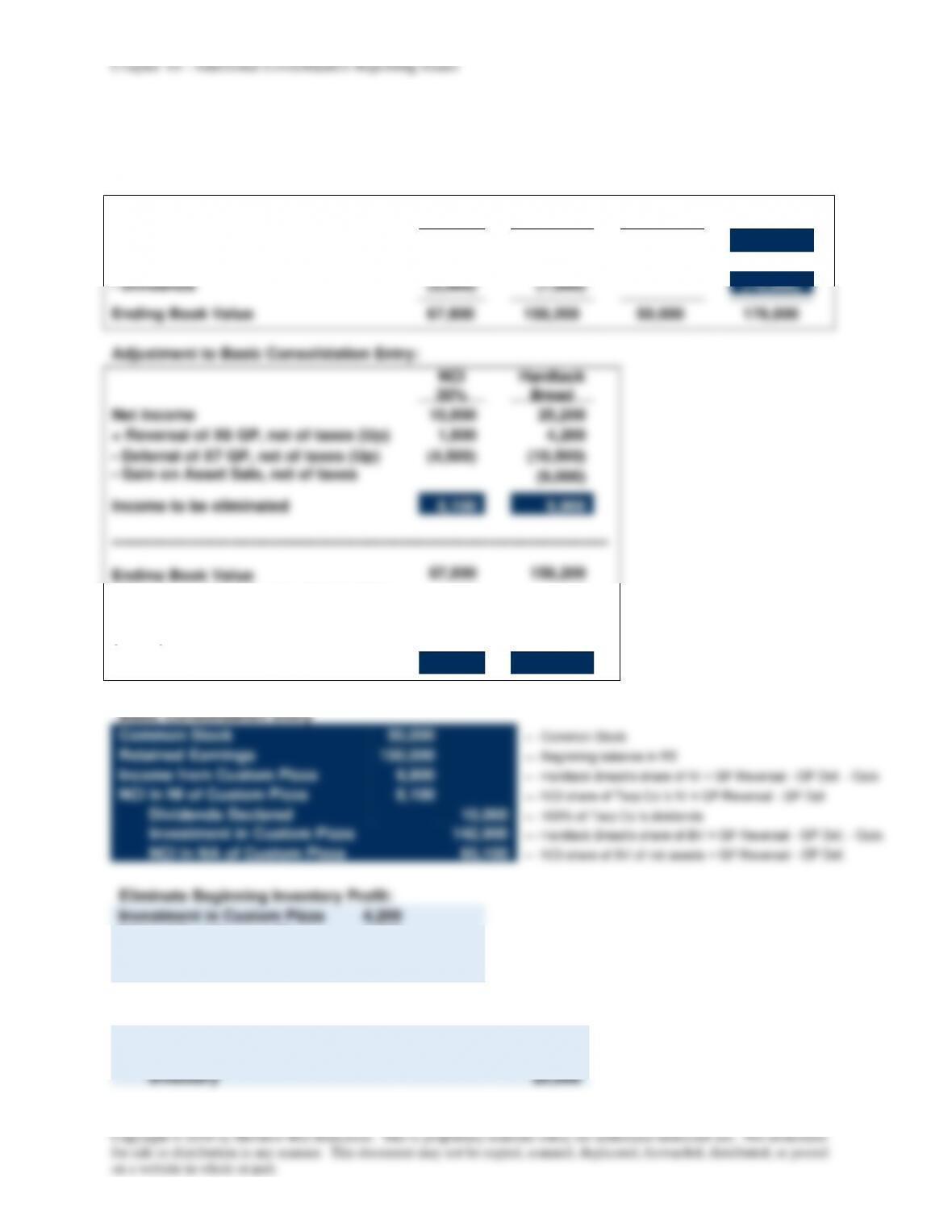

Book Value Calculations:

NCI

30%

+

Hardtack

Bread

=

Common

Stock

+

Retained

Earnings

Original Book Value

60,000

140,000

50,000

150,000

+ Net Income

10,800

25,200

36,000

– Dividends

(3,000)

(7,000)

(10,000)

Ending Book Value

67,800

158,200

50,000

176,000

Adjustment to Basic Consolidation Entry:

NCI

30%

Hardtack

Bread

Net Income

10,800

25,200

+ Reversal of X6 GP, net of taxes (Up)

1,800

4,200

– Deferral of X7 GP, net of taxes (Up)

(4,500)

(10,500)

– Gain on Asset Sale, net of taxes

(Down)

(9,000)

Income to be eliminated

8,100

9,900

————–——–——————–——————–———-———-—————

Ending Book Value

67,800

158,200

+ Reversal of X6 GP, net of taxes (Up)

1,800

4,200

– Deferral of X7 GP, net of taxes (Up)

(4,500)

(10,500)

– Gain on Asset Sale, net of taxes

(Down)

(9,000)

Adjusted Book Value

65,100

142,900

Basic Consolidation Entry

Common Stock

50,000

← Common Stock

Retained Earnings

150,000

← Beginning balance in RE

Income from Custom Pizza

9,900

← Hardtack Bread’s share of NI + GP Reversal – GP Def. – Gain

NCI in NI of Custom Pizza

8,100

← NCI share of Tarp Co.’s NI + GP Reversal – GP Def.

Dividends Declared

10,000

← 100% of Tarp Co.’s dividends

Investment in Custom Pizza

142,900

← Hardtack Bread’s share of BV + GP Reversal – GP Def. – Gain

NCI in NA of Custom Pizza

65,100

← NCI share of BV of net assets + GP Reversal – GP Def.

Eliminate Beginning Inventory Profit:

Investment in Custom Pizza

4,200

NCI in NA of Custom Pizza

1,800

Income Tax Expense

4,000

Cost of Goods Sold

10,000

Eliminate Inventory Purchases:

Sales

120,000

Cost of Goods Sold

95,000

Inventory

25,000

P10-31 (continued)

Eliminate Tax Expense on Unrealized Profit on Inventory Transfer:

Deferred Tax Asset

10,000

Deferred Tax Expense

10,000

Equipment

Accumulated

Depreciation

Custom Pizza

65,000

Actual

0

85,000

100,000

Hardtack Bread

150,000

“As If”

100,000

Eliminate the Gain on Equipment and Correct Asset’s Basis:

Gain on sale

15,000

Equipment

85,000

Accumulated Depreciation

100,000

Eliminate Tax Expense on Unrealized Profit from Asset

Transfer:

Deferred Tax Asset

6,000

Deferred Tax Expense

6,000

P10-31 (continued)

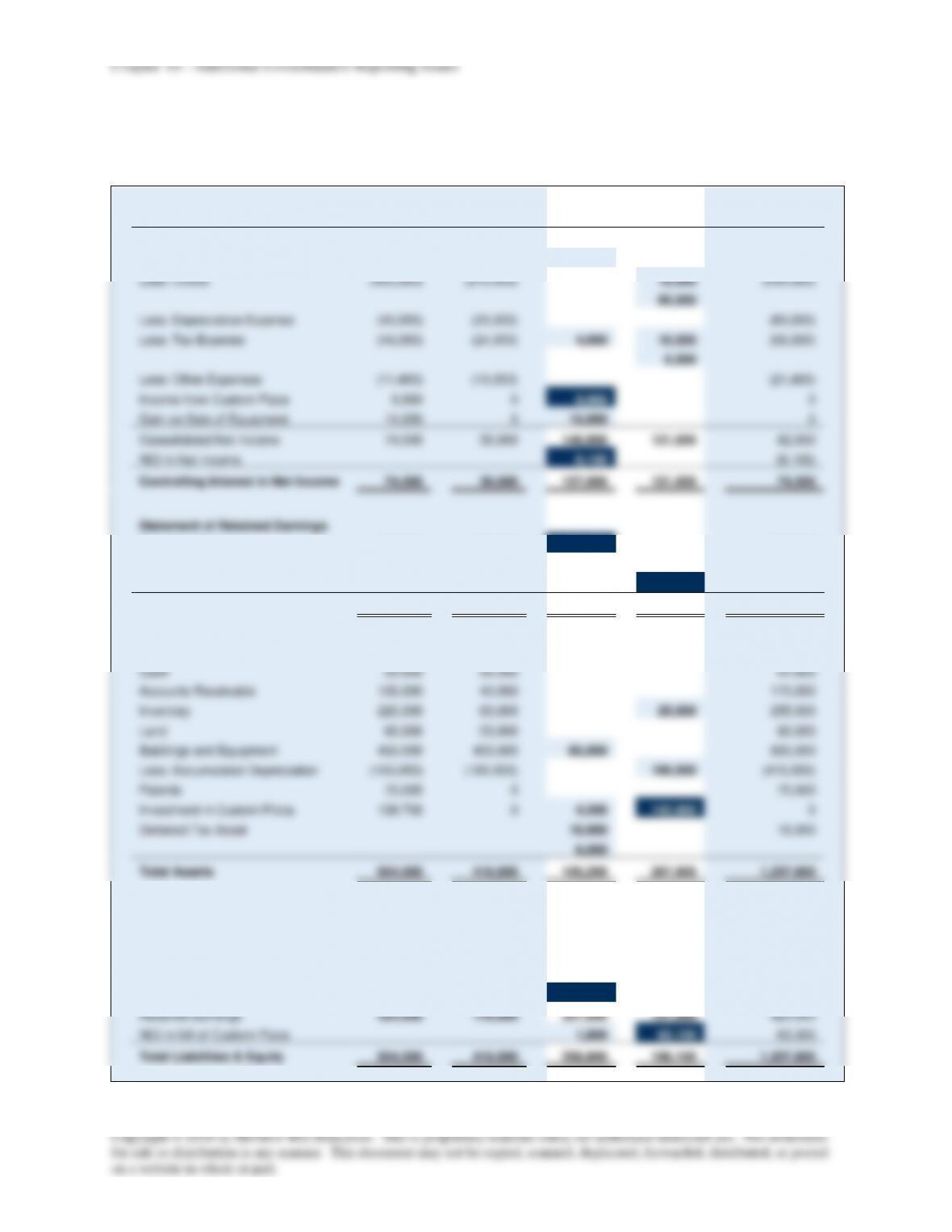

b.

Hardtack

Bread

Custom

Pizza

Consolidation Entries

DR

CR

Consolidated

Income Statement

Sales

580,000

300,000

120,000

760,000

Less: COGS

(435,000)

(210,000)

10,000

(540,000)

95,000

Less: Depreciation Expense

(40,000)

(20,000)

(60,000)

Less: Tax Expense

(44,000)

(24,000)

4,000

10,000

(56,000)

6,000

Less: Other Expenses

(11,400)

(10,000)

(21,400)

Income from Custom Pizza

9,900

0

9,900

0

Gain on Sale of Equipment

15,000

0

15,000

0

Consolidated Net Income

74,500

36,000

148,900

121,000

82,600

NCI in Net Income

8,100

(8,100)

Controlling Interest in Net Income

74,500

36,000

157,000

121,000

74,500

Statement of Retained Earnings

Beginning Balance

370,000

150,000

150,000

370,000

Net Income

74,500

36,000

157,000

121,000

74,500

Less: Dividends Declared

(20,000)

(10,000)

10,000

(20,000)

Ending Balance

424,500

176,000

307,000

131,000

424,500

Balance Sheet

Cash

35,800

56,000

91,800

Accounts Receivable

130,000

40,000

170,000

Inventory

220,000

60,000

25,000

255,000

Land

60,000

20,000

80,000

Buildings and Equipment

450,000

400,000

85,000

935,000

Less: Accumulated Depreciation

(150,000)

(160,000)

100,000

(410,000)

Patents

70,000

0

70,000

Investment in Custom Pizza

138,700

0

4,200

142,900

0

Deferred Tax Asset

10,000

16,000

6,000

Total Assets

954,500

416,000

105,200

267,900

1,207,800

Accounts Payable

40,000

30,000

70,000

Wages Payable

70,000

20,000

90,000

Bonds Payable

200,000

100,000

300,000

Deferred Income Taxes

120,000

40,000

160,000

Common Stock

100,000

50,000

50,000

100,000

Retained Earnings

424,500

176,000

307,000

131,000

424,500

NCI in NA of Custom Pizza

1,800

65,100

63,300

Total Liabilities & Equity

954,500

416,000

358,800

196,100

1,207,800

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

Basic earnings per share

Branch Manufacturing income from operations

$100,000

Short Retail Stores net income

$49,200

Preferred dividends ($100,000 x 0.08)

(8,000)

Earnings available

$41,200

Short shares outstanding

÷20,000

Computed EPS for Short

$ 2.06

Shares held by Branch Manufacturing

x16,000

Contribution to Branch Manufacturing earnings

32,960

Total earnings of Branch Manufacturing

$132,960

Preferred dividends of Branch Manufacturing

(22,000)

Earnings to Branch common shareholders

$110,960

Branch Manufacturing shares outstanding

÷ 15,000

Basic earnings per share

$ 7.40

Diluted earnings per share

Branch Manufacturing income from operations

$100,000

Short Retail Stores net income

$49,200

Assumed conversion of bonds:

$20,000 x 0.60

12,000

Earnings available

$61,200

Short shares outstanding

20,000

Assumed conversion of bonds

8,000

Assumed conversion of preferred

12,000

Total shares

÷40,000

Computed EPS for Short

$ 1.53

Shares held by Branch Manufacturing

x16,000

Contribution to Branch Manufacturing earnings

24,480

Total earnings of Branch Manufacturing

$124,480

Preferred dividends of Branch Manufacturing

(22,000)

Earnings to Branch common shareholders

$102,480

Branch Manufacturing shares outstanding

÷ 15,000

Diluted earnings per share

$ 6.83

P10-33 Comprehensive Earnings per Share

Basic earnings per share

Mighty Corporation operating income

$300,000

Longfellow net income

$115,000

Preferred dividends ($200,000 x 0.11)

(22,000)

Earnings available to common shareholders

$ 93,000

Longfellow shares outstanding

÷ 40,000

Computed EPS for Longfellow

$ 2.325

Shares held by Mighty Corporation

x 32,000

Contribution to Mighty Corporation earnings

74,400

Total earnings of Mighty Corporation

$374,400

Mighty Corporation shares outstanding

÷100,000

Basic earnings per share

$ 3.74

Diluted earnings per share

Mighty Corporation operating income

$300,000

Longfellow net income

$115,000

Assumed conversion of bonds

($500,000 x 0.08) x 0.60

24,000

Earnings available to common

$139,000

Longfellow shares outstanding

40,000

Assumed conversion of bonds

30,000

Assumed conversion of preferred

20,000

Exercise of warrants:

10,000 – [($8 x 10,000) / $40]

8,000

Total shares

÷ 98,000

Computed EPS for Longfellow

$ 1.418

Shares held by Mighty Corporation

x 32,000

Contribution to Mighty Corporation Earnings

45,376

Total earnings of Mighty Corporation

$345,376

Interest savings on assumed conversion

of bonds ($800,000 x 0.10) x 0.60

48,000

$393,376

Mighty Corporation shares

÷125,000

Diluted earnings per share

$

3.15