Chapter 16 – Partnerships: Liquidation

16–31

P16-14 Installment Liquidation [AICPA Adapted]

ABC Partnership

Statement of Partnership Realization and Liquidation

For the period from January 1, 20X1, through March 31, 20X1

Capital Balances

Other

Accounts

Art

Bru

Chou

Cash +

Assets =

Payable +

50% +

30% +

20%

Balances before liquidation, January 1, 20X1

18,000

307,000

53,000

88,000

110,000

74,000

January transactions:

1.

Collection of accounts receivable at a loss

of $15,000

51,000

(66,000)

(7,500)

(4,500)

(3,000)

2.

Sale of inventory at a loss of $14,000

38,000

(52,000)

(7,000)

(4,200)

(2,800)

3.

Liquidation expenses paid

(2,000)

(1,000)

(600)

(400)

4.

Share of credit memorandum

(3,000)

1,500

900

600

5.

Payments to creditors

(50,000)

(50,000)

55,000

189,000

-0-

74,000

101,600

68,400

Safe payments to partners (Schedule 1)

(45,000)

(26,600)

(18,400)

10,000

189,000

-0-

74,000

75,000

50,000

February transactions:

6.

Liquidation expenses paid

(4,000)

(2,000)

(1,200)

(800)

6,000

189,000

-0-

72,000

73,800

49,200

Safe payments to partners (Schedule 2)

-0-

-0-

-0-

-0-

6,000

189,000

-0-

72,000

73,800

49,200

March transactions:

8.

Sale of M&Eq. at a loss of $43,000

146,000

(189,000)

(21,500)

(12,900)

(8,600)

9.

Liquidation expenses paid

(5,000)

(2,500)

(1,500)

(1,000)

147,000

-0-

-0-

48,000

59,400

39,600

10. Payments to partners

(147,000)

(48,000)

(59,400)

(39,600)

Balances at end of liquidation, March 31, 20X1

-0-

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–32

P16-14 (continued)

ABC Partnership

Schedules of Safe Payments to Partners

Art

Bru

Chou

Schedule 1: January 31, 20X1

50%

30%

20%

Capital balances

74,000

101,600

68,400

Possible loss:

Other assets ($189,000) and possible

liquidation costs ($10,000)

(99,500)

(59,700)

(39,800)

(25,500)

41,900

28,600

Absorption of Art’s potential deficit balance

25,500

Bru: ($25,500 x 3/5 = $15,300)

(15,300)

Chou: ($25,500 x 2/5 = $10,200)

(10,200)

Safe payment, January 31, 20X1

-0-

26,600

18,400

Schedule 2: February 27, 20X1

Capital balances

72,000

73,800

49,200

Possible loss:

Other assets ($189,000) and possible

liquidation costs ($6,000)

(97,500)

(58,500)

(39,000)

(25,500)

15,300

10,200

Absorption of Art’s potential deficit balance:

25,500

Bru: ($25,500 x 3/5 = $15,300)

(15,300)

Chou: ($25,500 x 2/5 = $10,200)

(10,200)

Safe payment, February 27, 20X1

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–33

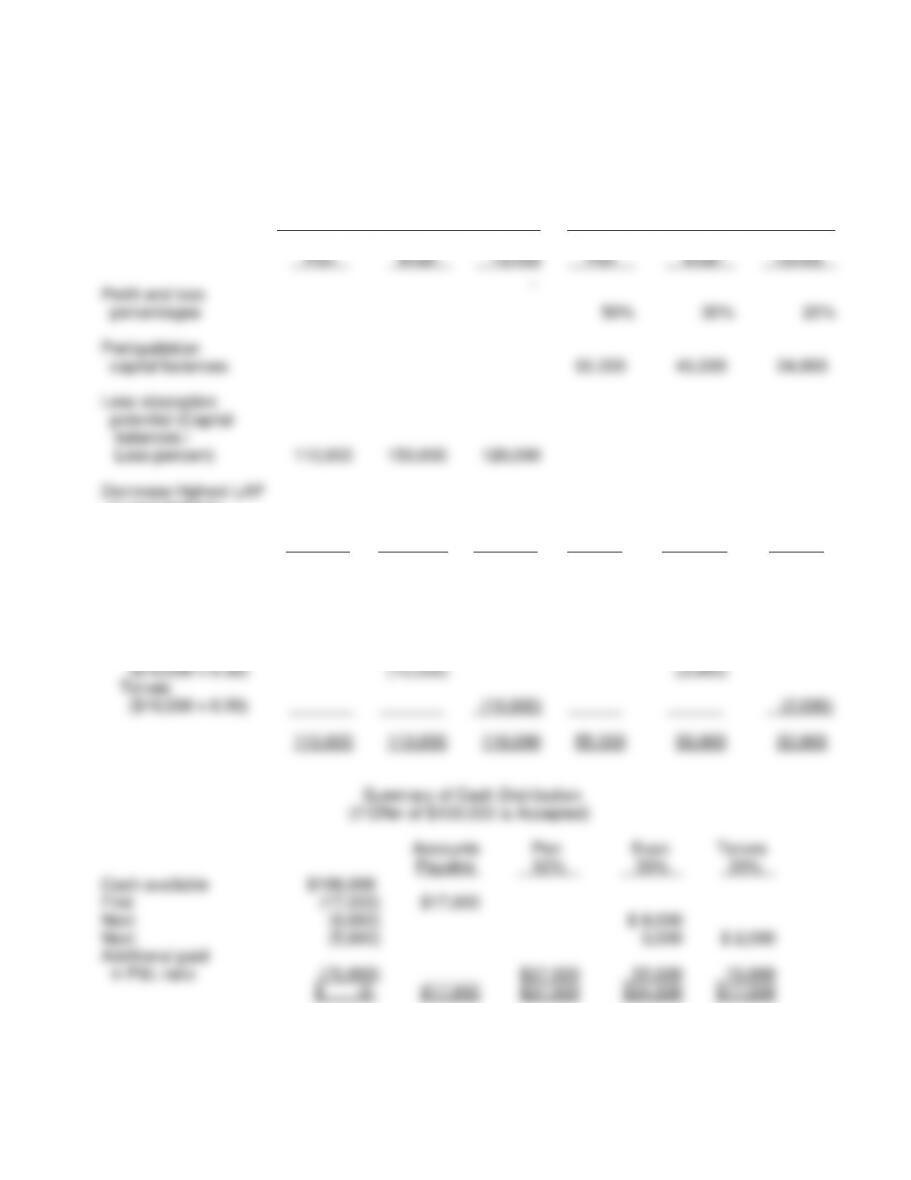

P16-15 Cash Distribution Plan

PET Partnership

Cash Distribution Plan

June 30, 20X1

Loss Absorption Potential

Capital Accounts

Pen

Evan

Torves

Pen

Evan

Torves

Profit and loss

percentages

50%

30%

20%

Preliquidation

capital balances

55,000

45,000

24,000

Loss absorption

potential (Capital

balances /

Loss percent)

110,000

150,000

120,000

Decrease highest LAP

to next highest:

Evan

($30,000 x 0.30)

(30,000)

(9,000)

110,000

120,000

120,000

55,000

36,000

24,000

Decrease LAPs

to next highest:

Evan

($10,000 x 0.30)

(10,000)

(3,000)

Torves

($10,000 x 0.20)

(10,000)

(2,000)

110,000

110,000

110,000

55,000

33,000

22,000

Summary of Cash Distribution

(If Offer of $100,000 is Accepted)

Accounts

Pen

Evan

Torves

Payable

50%

30%

20%

Cash available

$106,000

First

(17,000)

$17,000

Next

(9,000)

$ 9,000

Next

(5,000)

3,000

$ 2,000

Additional paid

in P&L ratio

(75,000)

______

$37,500

22,500

15,000

$ -0-

$17,000

$37,500

$34,500

$17,000

Chapter 16 – Partnerships: Liquidation

16–34

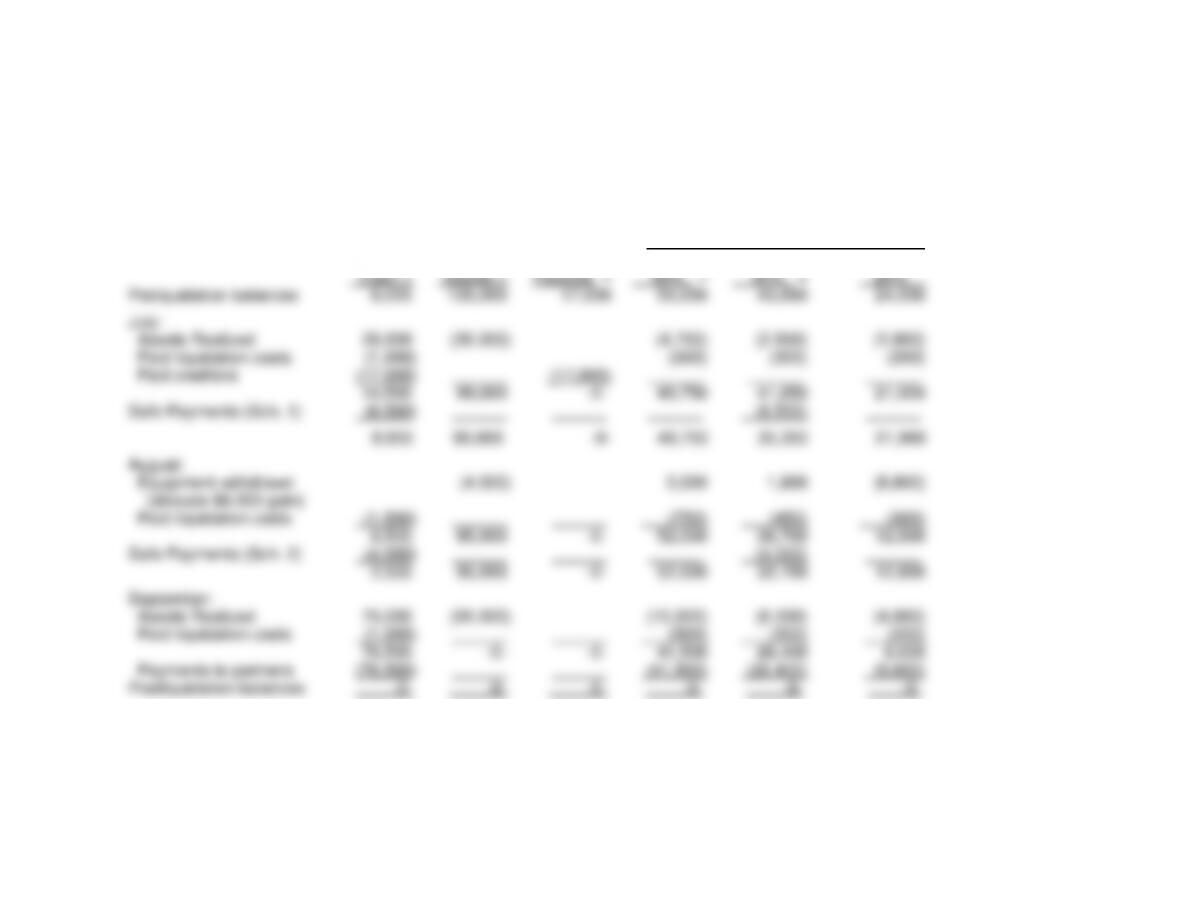

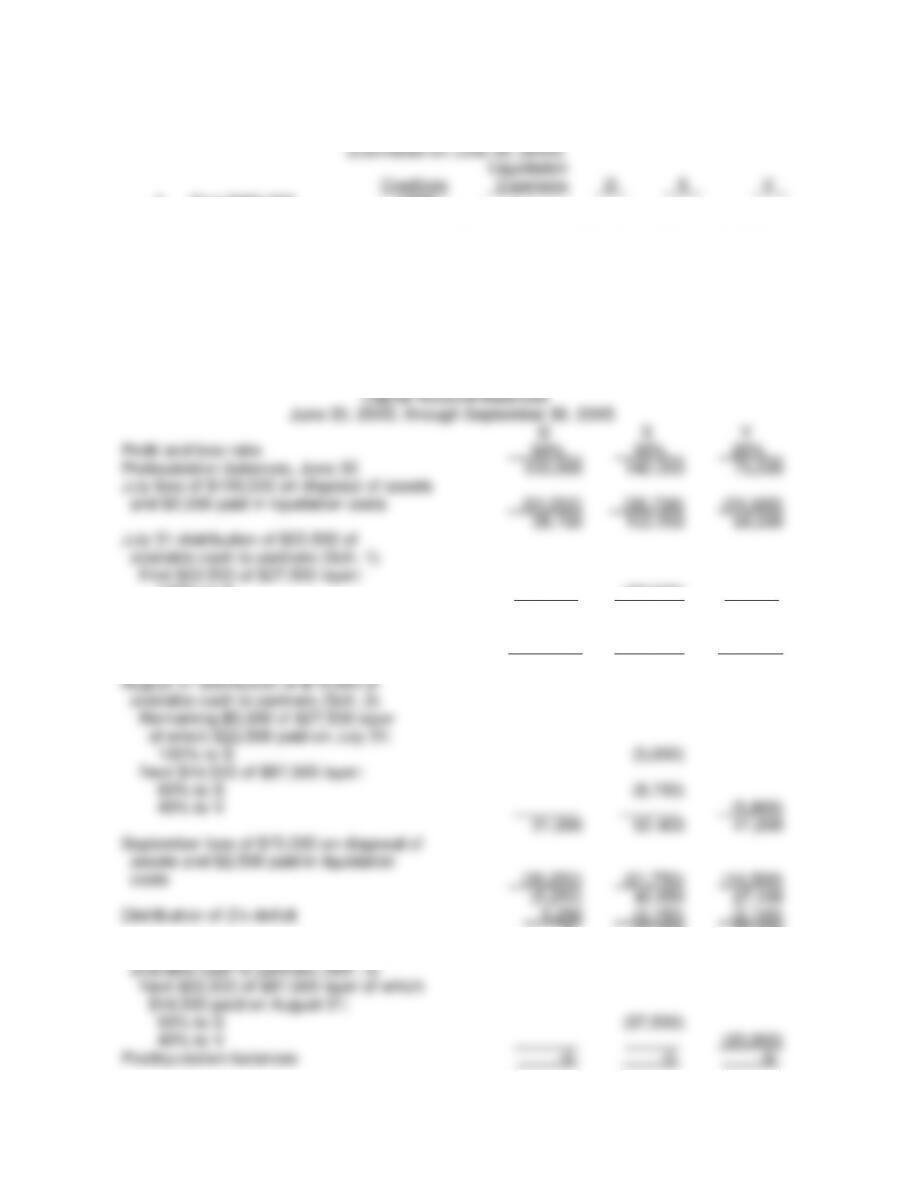

P16-16 Installment Liquidation

PET Partnership

Statement of Partnership Liquidation and Realization

From July 1, 20X1, through September 30, 20X1

Capital

Noncash

Accounts

Pen

Evan

Torves

Cash +

Assets =

Payable +

50% +

30% +

20%

Preliquidation balances

6,000

135,000

17,000

55,000

45,000

24,000

July:

Assets Realized

26,500

(36,000)

(4,750)

(2,850)

(1,900)

Paid liquidation costs

(1,000)

(500)

(300)

(200)

Paid creditors

(17,000)

(17,000)

14,500

99,000

-0-

49,750

41,850

21,900

Safe Payments (Sch. 1)

(6,500)

(6,500)

8,000

99,000

-0-

49,750

35,350

21,900

August:

Equipment withdrawn

(4,000)

3,000

1,800

(8,800)

(allocate $6,000 gain)

Paid liquidation costs

(1,500)

(750)

(450)

(300)

6,500

95,000

-0-

52,000

36,700

12,800

Safe Payments (Sch. 2)

(4,000)

(4,000)

2,500

95,000

-0-

52,000

32,700

12,800

September:

Assets Realized

75,000

(95,000)

(10,000)

(6,000)

(4,000)

Paid liquidation costs

(1,000)

(500)

(300)

(200)

76,500

-0-

-0-

41,500

26,400

8.600

Payments to partners

(76,500)

(41,500)

(26,400)

(8,600)

Postliquidation balances

-0-

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–35

P16-16 (continued)

PET Partnership

Schedules of Safe Payments to Partners

Pen

Evan

Torves

Schedule 1: July 31, 20X1

50%

30%

20%

Capital balances

49,750

41,850

21,900

Possible loss on noncash assets ($99,000)

(49,500)

(29,700)

(19,800)

Cash retained ($8,000)

(4,000)

(2,400)

(1,600)

(3,750)

9,750

500

Absorption of Pen‘s potential deficit

3,750

Evan: $3,750 x 0.30/0.50

(2,250)

Torves: $3,750 x 0.20/0.50

(1,500)

-0-

7,500

(1,000)

Absorption of Torves’ potential deficit

1,000

Evan: $1,000 x 0.30/0.30

(1,000)

Safe payment

-0-

6,500

-0-

Schedule 2: August 31, 20X1

Capital balances

52,000

36,700

12,800

Possible loss on noncash assets ($95,000)

(47,500)

(28,500)

(19,000)

Cash retained ($2,500)

(1,250)

(750)

(500)

3,250

7,450

(6,700)

Absorption of Torves’ potential deficit

6,700

Pen: $6,700 x 0.50/0.80

(4,188)

Evan: $6,700 x 0.30/0.80

(2,512)

(938)

4,938

-0-

Absorption of Pen‘s potential deficit

938

Evan: $938 x 0.30/0.30

(938)

Safe payment

-0-

4,000

-0-

Chapter 16 – Partnerships: Liquidation

16–36

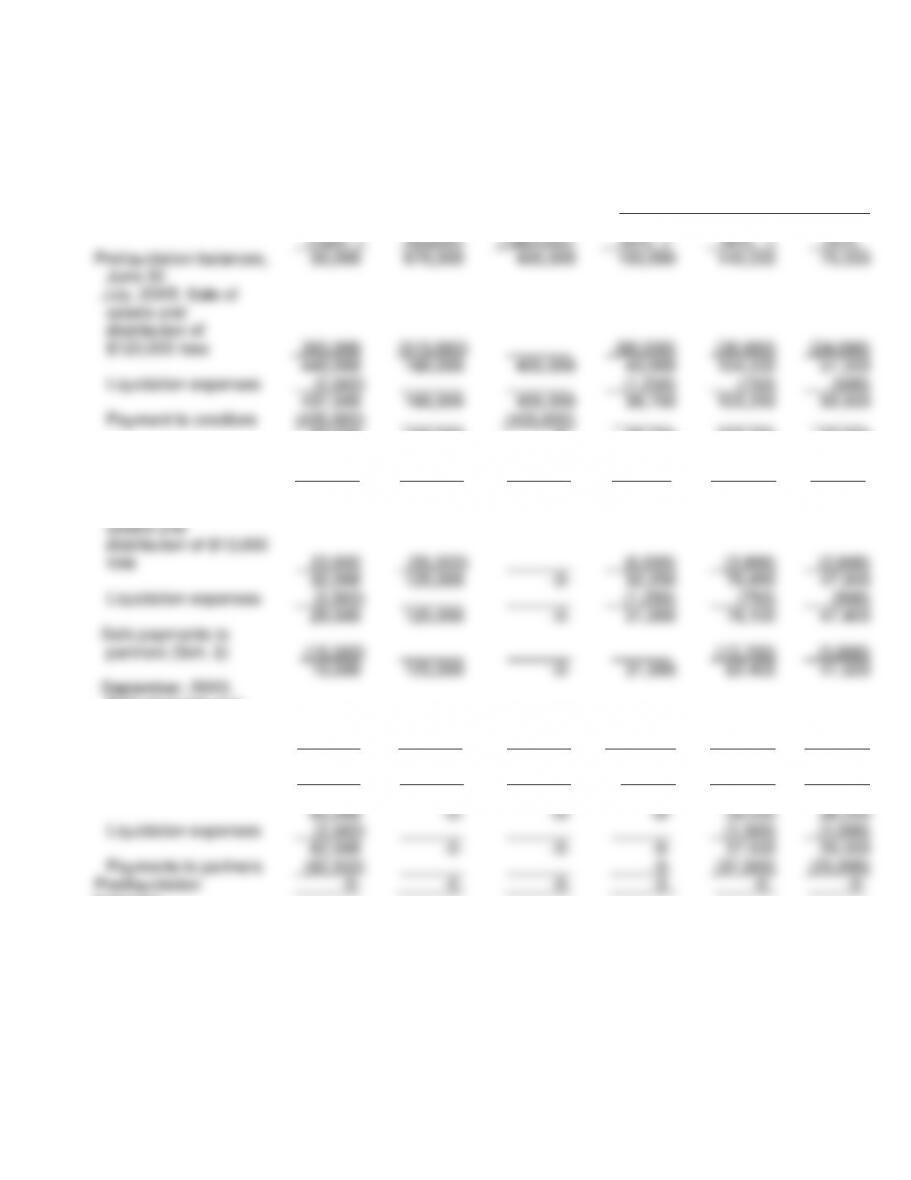

P16-17 Installment Liquidation

DSV Partnership

Statement of Partnership Realization and Liquidation — Installment Liquidation

From July 1, 20X5, through September 30, 20X5

Capital Balances

Noncash

D

S

V

Cash +

Assets=

Liabilities+

50% +

30% +

20%

Preliquidation balances,

June 30

50,000

670,000

405,000

100,000

140,000

75,000

July, 20X5: Sale of

assets and

distribution of

$120,000 loss

390,000

(510,000)

(60,000)

(36,000)

(24,000)

440,000

160,000

405,000

40,000

104,000

51,000

Liquidation expenses

(2,500)

(1,250)

(750)

(500)

437,500

160,000

405,000

38,750

103,250

50,500

Payment to creditors

(405,000)

(405,000)

32,500

160,000

-0-

38,750

103,250

50,500

Safe payments to

partners (Sch. 1)

(22,500)

(22,500)

10,000

160,000

-0-

38,750

80,750

50,500

August, 20X5: Sale of

assets and

distribution of $13,000

loss

22,000

(35,000)

(6,500)

(3,900)

(2,600)

32,000

125,000

-0-

32,250

76,850

47,900

Liquidation expenses

(2,500)

(1,250)

(750)

(500)

29,500

125,000

-0-

31,000

76,100

47,400

Safe payments to

partners (Sch. 2)

(19,500)

(13,700)

(5,800)

10,000

125,000

-0-

31,000

62,400

41,600

September, 20X5:

Sale of assets and

distribution of $70,000

loss

55,000

(125,000)

(35,000)

(21,000)

(14,000)

65,000

-0-

-0-

(4,000)

41,400

27,600

Allocate D’s deficit to S

and V

4,000

(2,400)

(1,600)

65,000

-0-

-0-

-0-

39,000

26,000

Liquidation expenses

(2,500)

(1,500)

(1,000)

62,500

-0-

-0-

-0-

37,500

25,000

Payments to partners

(62,500)

-0-

(37,500)

(25,000)

Postliquidation

balances

-0-

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–37

P16-17 (continued)

DSV Partnership

Schedule of Safe Payments to Partners

D

S

V

Schedule 1, July 31, 20X5:

50%

30%

20%

Capital balances, July 31,

Before cash distribution

38,750

103,250

50,500

Assume full loss of $160,000 on

remaining noncash assets and

$10,000 in possible future

liquidation expenses

(85,000)

(51,000)

(34,000)

(46,250)

52,250

16,500

Assume D’s potential deficit

must be absorbed by S and V:

46,250

30/50 x $46,250

(27,750)

20/50 x $46,250

(18,500)

-0-

24,500

(2,000)

Assume V’s potential deficit

must be absorbed by S completely

(2,000)

2,000

Safe payments to partners

on July 31, 20X5

-0-

22,500

-0-

Schedule 2, August 31, 20X5:

Capital balances, August 31, before cash

distribution

31,000

76,100

47,400

Assume full loss of $125,000 on remaining

noncash assets and$10,000 in possible

liquidation expenses

(67,500)

(40,500)

(27,000)

(36,500)

35,600

20,400

Assume D’s potential deficit must be absorbed

by S and V:

36,500

30/50 x $36,500

(21,900)

20/50 x $36,500

(14,600)

Safe payments to partners

-0-

13,700

5,800

Chapter 16 – Partnerships: Liquidation

16–38

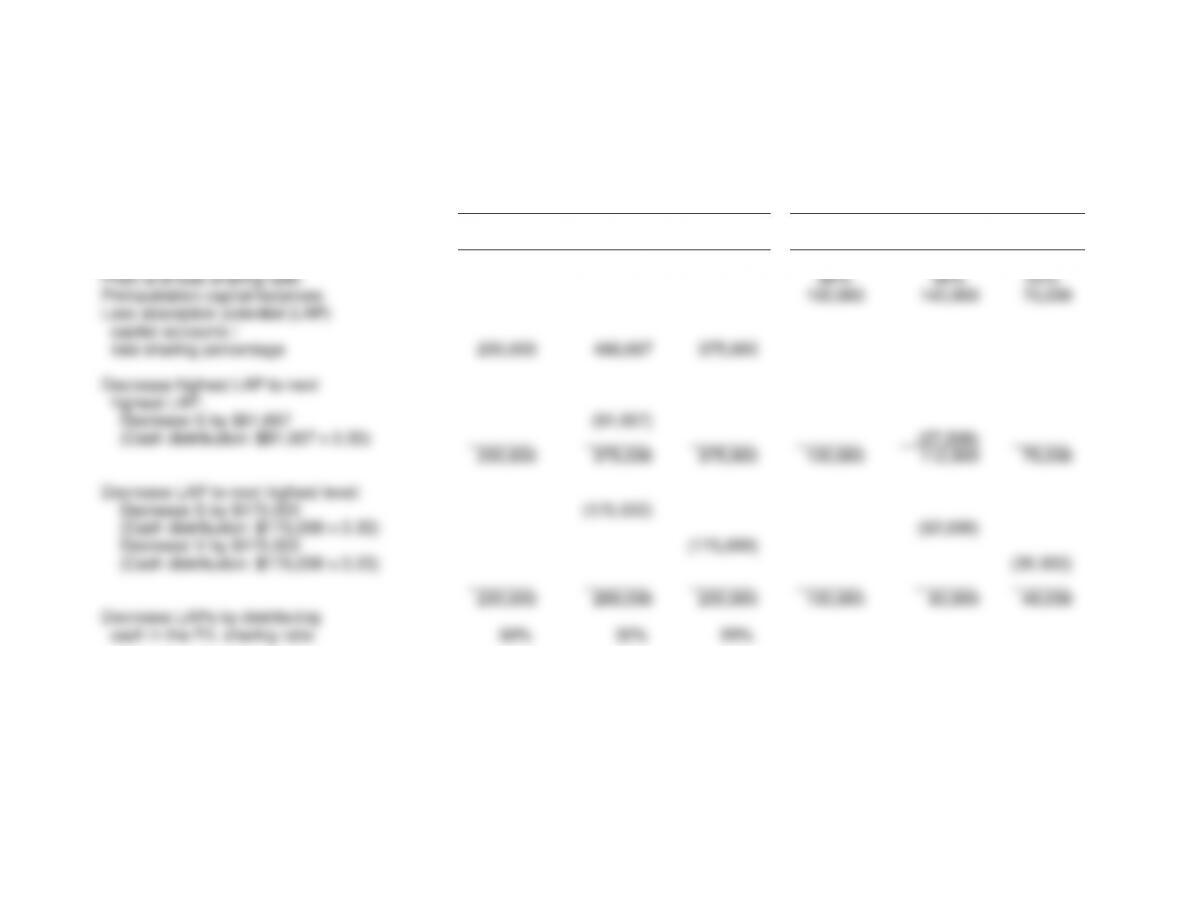

P16-18 Cash Distribution Plan

DSV Partnership

Cash Distribution Plan

June 30, 20X5

Loss Absorption Potential

Capital Accounts

D

S

V

D

S

V

Profit and loss sharing ratio

50%

30%

20%

Preliquidation capital balances

100,000

140,000

75,000

Loss absorption potential (LAP)

capital accounts /

loss sharing percentage

200,000

466,667

375,000

Decrease highest LAP to next

highest LAP:

Decrease S by $91,667

(91,667)

(Cash distribution: $91,667 x 0.30)

(27,500)

200,000

375,000

375,000

100,000

112,500

75,000

Decrease LAP to next highest level:

Decrease S by $175,000

(175,000)

(Cash distribution: $175,000 x 0.30)

(52,500)

Decrease V by $175,000

(175,000)

(Cash distribution: $175,000 x 0.20)

(35,000)

200,000

200,000

200,000

100,000

60,000

40,000

Decrease LAPs by distributing

cash in the P/L sharing ratio

50%

30%

20%

Chapter 16 – Partnerships: Liquidation

16–39

P16-18 (continued)

Summary of Cash Distribution Plan

(Estimated on June 30, 20X5)

Liquidation

Creditors

Expenses

D

S

V

1.

First $405,000

100%

2.

Next $10,000

100%

3.

Next $27,500

100%

4.

Next $87,500

60%

40%

5.

Any additional distributions

in the partners’ profit

and loss ratio

50%

30%

20%

b. Confirmation of cash distribution plan

DSV Partnership

Capital Account Balances

June 30, 20X5, through September 30, 20X5

D

S

V

Profit and loss ratio

50%

30%

20%

Preliquidation balances, June 30

100,000

140,000

75,000

July loss of $120,000 on disposal of assets

and $2,500 paid in liquidation costs

(61,250)

(36,750)

(24,500)

38,750

103,250

50,500

July 31 distribution of $22,500 of

available cash to partners (Sch. 1)

First $22,500 of $27,500 layer:

100% to S

(22,500)

38,750

80,750

50,500

August loss of $13,000 on disposal of

assets and $2,500 paid in liquidation costs

(7,750)

(4,650)

(3,100)

31,000

76,100

47,400

August 31 distribution of $19,500 of

available cash to partners (Sch. 2)

Remaining $5,000 of $27,500 layer

of which $22,500 paid on July 31:

100% to S

(5,000)

Next $14,500 of $87,500 layer:

60% to S

(8,700)

40% to V

(5,800)

31,000

62,400

41,600

September loss of $70,000 on disposal of

assets and $2,500 paid in liquidation

costs

(36,250)

(21,750)

(14,500)

(5,250)

40,650

27,100

Distribution of D’s deficit

5,250

(3,150)

(2,100)

-0-

37,500

25,000

September 30 distribution of $62,500 of

available cash to partners (Sch. 3)

Next $62,500 of $87,500 layer of which

$14,500 paid on August 31:

60% to S

(37,500)

40% to V

(25,000)

Postliquidation balances

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–40

P16-18 (continued)

Schedule 1, July 31, 20X5: Computation of $22,500 of cash available to be distributed to

partners on July 31, 20X5:

Cash balance, July 1, 20X5

$ 50,000

Cash from sale of noncash assets

390,000

Less: Payment of actual liquidation expenses

(2,500)

Less: Payments to creditors

(405,000)

Less: Amount held for possible

future liquidation expenses

(10,000)

Cash available to partners, July 31, 20X5

$ 22,500

Schedule 2, August 31, 20X5: Computation of $19,500 of cash available to be distributed

to partners on August 31, 20X5:

Cash balance, August 1, 20X5

$10,000

Cash from sale of noncash assets

22,000

Less: Payment of actual liquidation expenses

(2,500)

Less: Amount held for possible

future liquidation expenses

(10,000)

Cash available to partners, August 31, 20X5

$ 19,500

Schedule 3, September 30, 20X5: Computation of $62,500 of cash available to be

distributed to partners on September 30, 20X5:

Cash balance, September 1, 20X5

$10,000

Cash received from sale of noncash assets

55,000

Less: Payment of actual liquidation expenses

(2,500)

Cash available to partners, September 30, 20X5

$62,500