Chapter 08 – Intercompany Indebtedness

P8–16 (continued)

c.

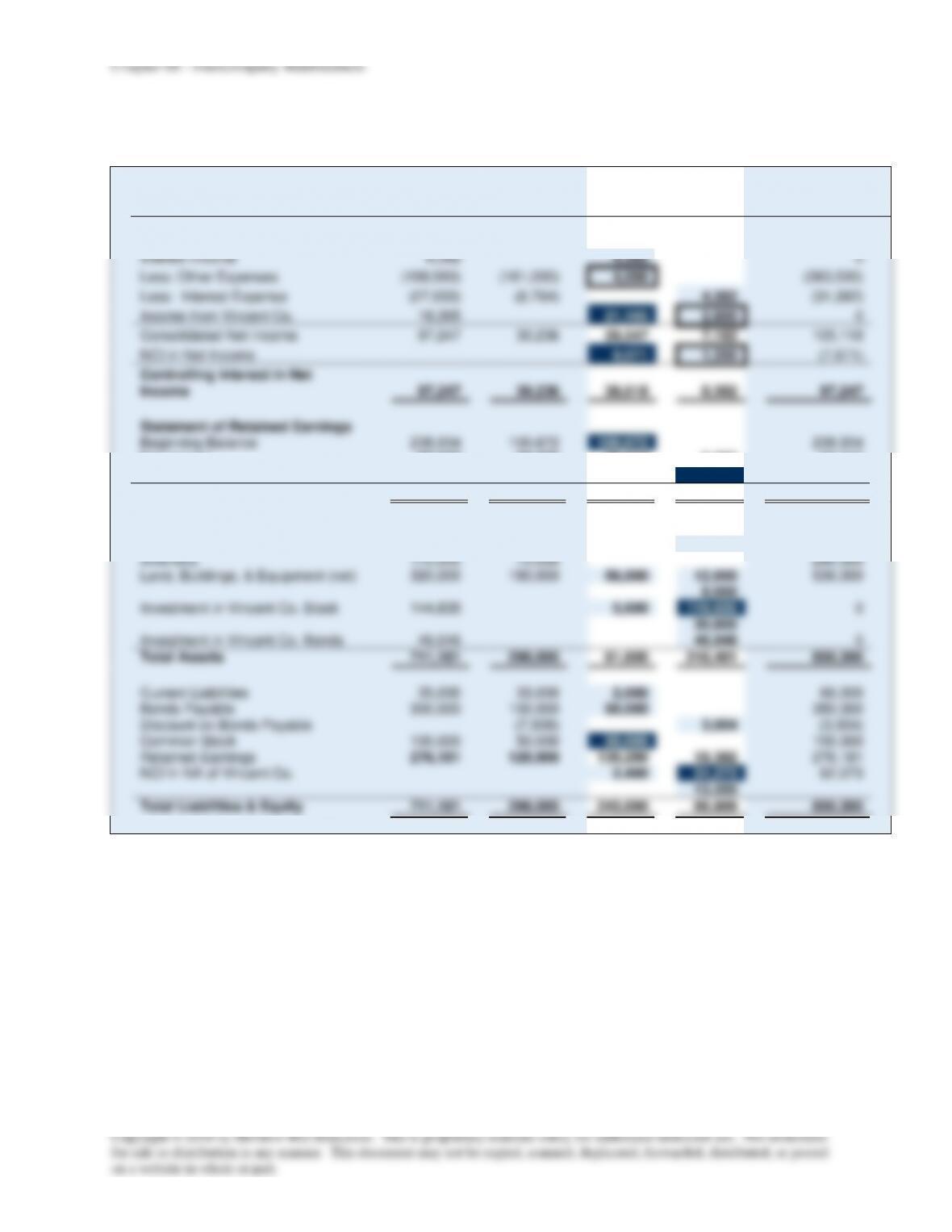

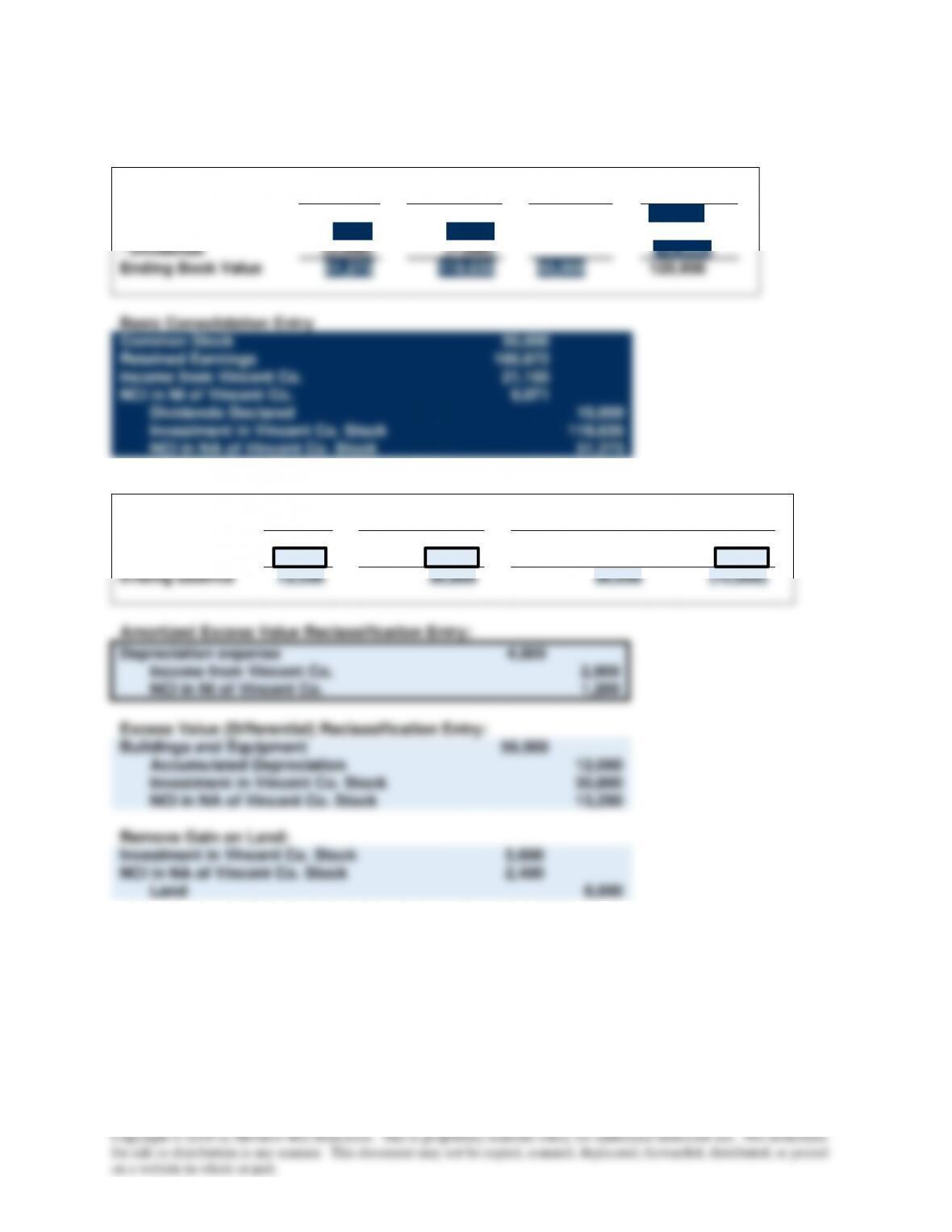

Book Value Calculations:

NCI

30%

+

Fern Corp.

70%

=

Common

Stock

+

Retained

Earnings

Beginning Book Value

45,202

105,470

50,000

100,672

+ Net Income

9,071

21,165

30,236

– Dividends

(3,000)

(7,000)

(10,000)

Ending Book Value

51,273

119,635

50,000

120,908

Basic Consolidation Entry

Common Stock

50,000

Retained Earnings

100,672

Income from Vincent Co.

21,165

NCI in NI of Vincent Co.

9,071

Dividends Declared

10,000

Investment in Vincent Co. Stock

119,635

NCI in NA of Vincent Co. Stock

51,273

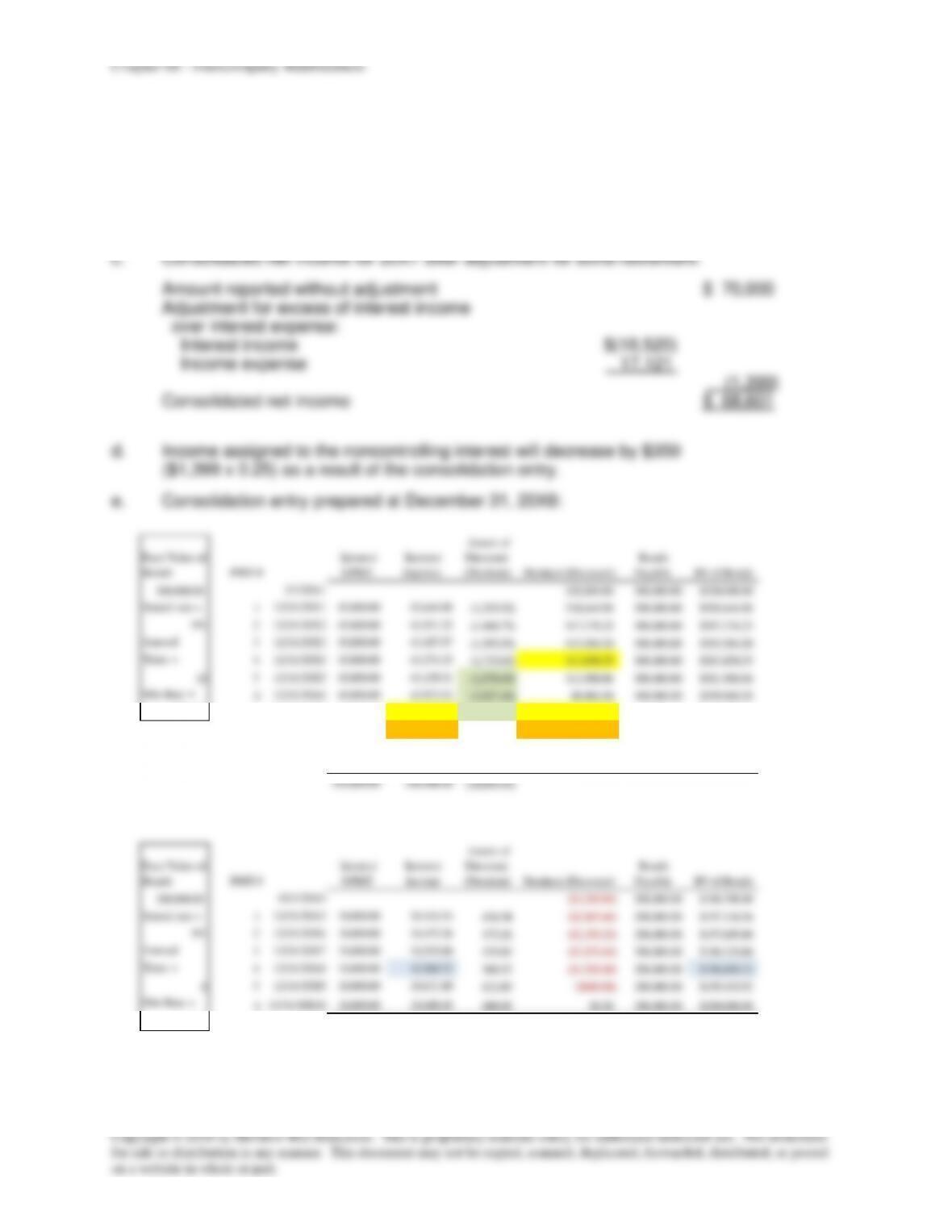

Excess Value (Differential) Calculations:

NCI

30%

+

Fern Corp.

70%

=

Buildings and

Equipment

+

Acc. Depr.

Beg. balance

14,400

33,600

56,000

(8,000)

Changes

(1,200)

(2,800)

(4,000)

Ending balance

13,200

30,800

56,000

(12,000)

Amortized Excess Value Reclassification Entry:

Depreciation expense

4,000

Income from Vincent Co.

2,800

NCI in NI of Vincent Co.

1,200

Excess Value (Differential) Reclassification Entry:

Buildings and Equipment

56,000

Accumulated Depreciation

12,000

Investment in Vincent Co. Stock

30,800

NCI in NA of Vincent Co. Stock

13,200

Remove Gain on Land:

Investment in Vincent Co. Stock

5,600

NCI in NA of Vincent Co. Stock

2,400

Land

8,000