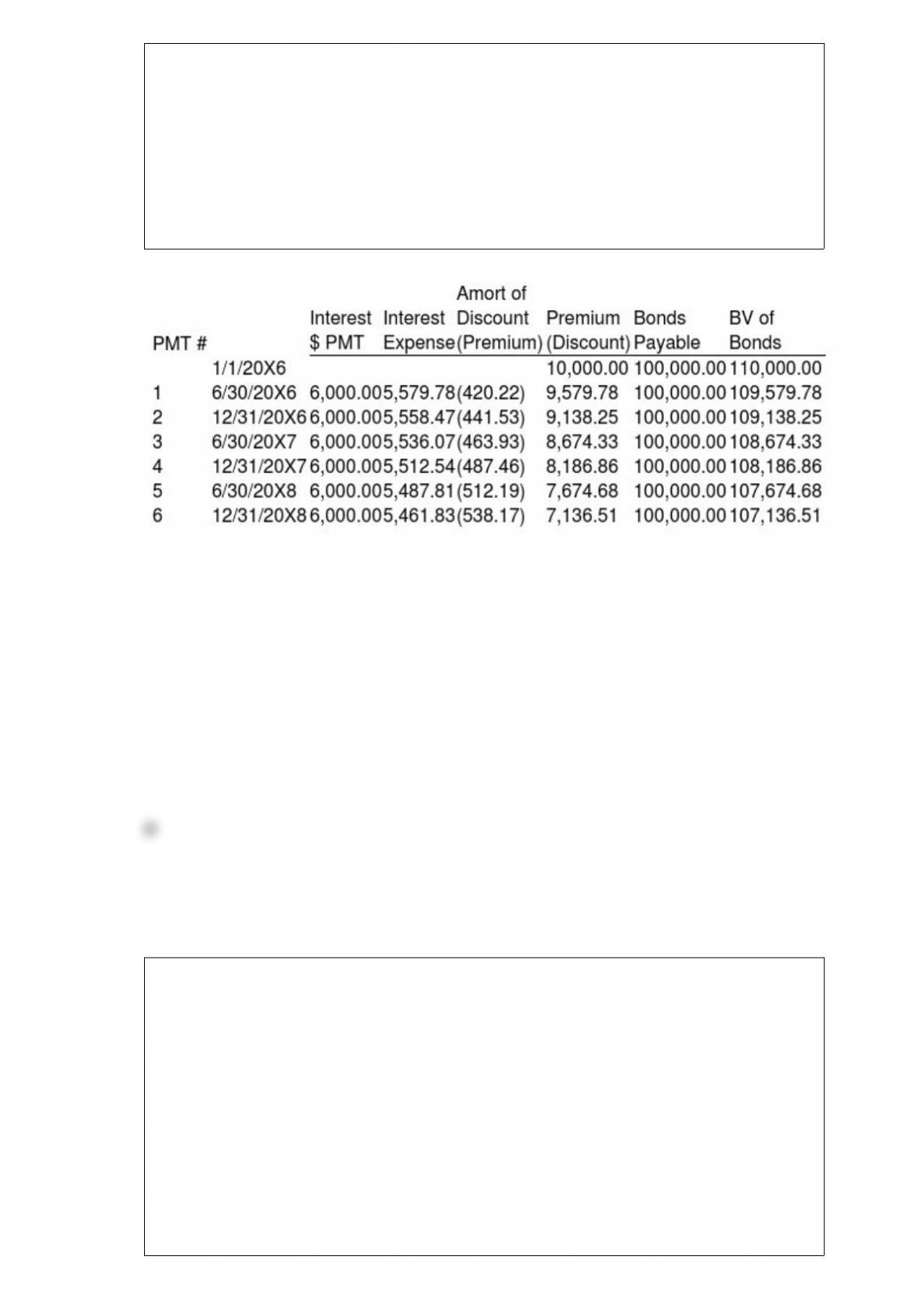

Hunter Corporation holds 80 percent of the voting shares of Moss Company. On

January 1, 20X8, Moss purchased $100,000 par value 12 percent Hunter bonds from

Cruse Corporation for $115,000. Hunter originally issued the bonds to Cruse on January

1, 20X6, for $110,000. The bonds have an 8-year maturity from the date of issue and

pay interest semiannually on June 30 and December 31 each year. Moss’ reported net

income of $65,000 for 20X8, and Hunter reported income (excluding income from

ownership of Moss’s stock) of $90,000. Hunter’s partial bond amortization schedule is

as follows:

Based on the information given above, what amount of interest income does Moss record

on its individual books for 20X8?

A. $10,950

B. $8,002

C. $9,410

D. $10,002

Barcode Corporation acquired 70% of the common stock of a Russian company on

January 1, 20X6. The goodwill associated with this acquisition was $12,520. Exchange

rates at various dates during 20X6 follow:

January 1, 20X6 1 ruble = $0.0313

December 31, 20X6 1 ruble = $0.0308

Average for 20X6 1 ruble = $0.031

Goodwill suffered an impairment of 25 percent during the year. If the functional

currency is the Russian ruble, how much goodwill impairment loss should be reported

on Barcode’s consolidated statement of income for 20X6?

A. $3,130

B. $3,100

C. $3,090

D. $3,080

Light Corporation owns 80 percent of Sound Company’s voting shares. On January 1,

20X7, Sound sold bonds with a par value of $300,000 when the market rate was 7

percent. Light purchased two thirds of the bonds; the remainder was sold to

nonaffiliates. The bonds mature in ten years and pay an annual interest rate of 6 percent.

Interest is paid semiannually on June 30 and Dec 31.

Based on the information given above, what amount of interest income will Light

Corporation recognize on December 31, 20X8 relative to the interest received on that

day, in its separate financial statements?

A. $13,023

B. $13,096

C. $6,538

D. $6,557

Which of the following statements is (are) correct about the funds used by

governmental entities?

A. I only

B. II only

C. I and II

D. Neither I nor II

Net assets restricted as to time or purpose should be classified as:

I. temporarily restricted.

II. permanently restricted.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

Which of the following accounts could be found in the general ledger of a partnership?

A. Option A

B. Option B

C. Option C

D. Option D

The partnership of X and Y shares profits and losses in the ratio of 60 percent to X and

40 percent to Y. For the year 20X8, partnership net income was double X’s withdrawals.

Assume X’s beginning capital balance was $80,000, and ending capital balance (after

closing) was $140,000. Partnership net income for the year was:

A. $120,000.

B. $300,000.

C. $500,000.

D. $600,000.

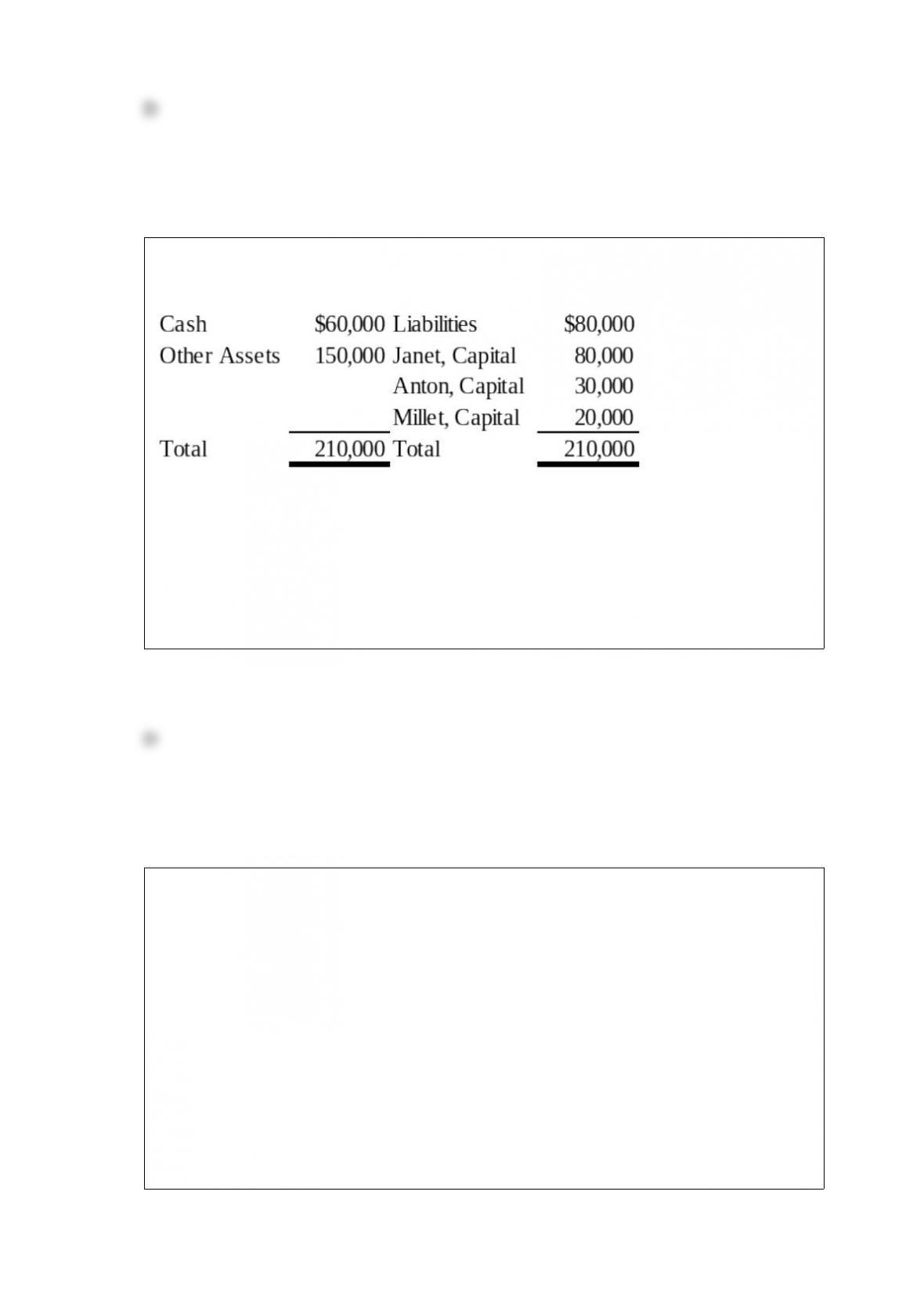

The balance sheet given below is presented for the partnership of Janet, Anton, and

Millet:

The partners share profits and losses in the ratio of 5:3:2, respectively. The partners

agreed to dissolve the partnership after selling the other assets for $50,000. On

dissolution of the partnership, Janet should receive:

A. $0.

B. $80,000.

C. $10,000.

D. $30,000.

Grant, Inc. acquired 30 percent of South Co.’s voting stock for $200,000 on January 2,

20X4. Grant’s 30 percent interest in South gave Grant the ability to exercise significant

influence over South’s operating and financial policies. During 20X4, South earned

$80,000 and paid dividends of $50,000. South reported earnings of $100,000 for the six

months ended June 30, 20X5, and $200,000 for the year ended December 31, 20X5. On

July 1, 20X5, Grant sold half of its stock in South for $150,000 cash. South paid

dividends of $60,000 on October 1, 20X5.

What amount should Grant include in its 20X4 income statement as a result of the

investment?

A. $15,000

B. $24,000

C. $50,000

D. $80,000

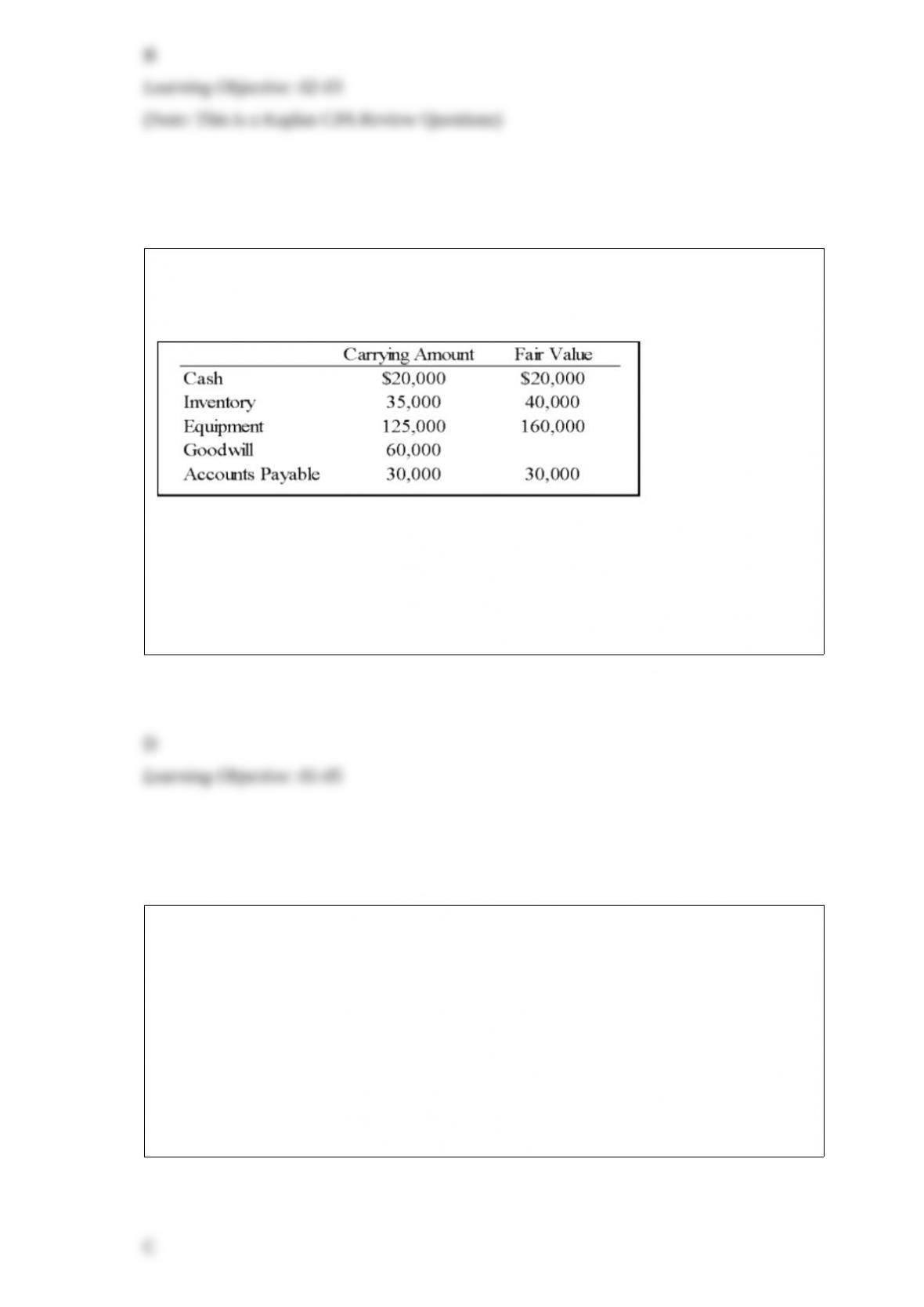

Following its acquisition of the net assets of Dan Company, Empire Company assigned

goodwill of $60,000 to one of the reporting divisions. Information for this division

follows:

Based on the preceding information, what amount of goodwill impairment will be

recognized for this division if its fair value is determined to be $195,000?

A. $5,000

B. $30,000

C. $60,000

D. $55,000

The income tax expense applicable to the second quarter’s income statement is

determined by:

A. dividing the estimated annual income tax expense by four and allocating the amount

to the second quarter.

B. multiplying the effective income tax rate times the income before tax for the second

quarter.

C. subtracting the income tax expense applicable to the first quarter from the income

tax expense applicable to the first two quarters.

D. subtracting the income tax liability applicable to the first quarter from the income tax

liability applicable to the first two quarters.

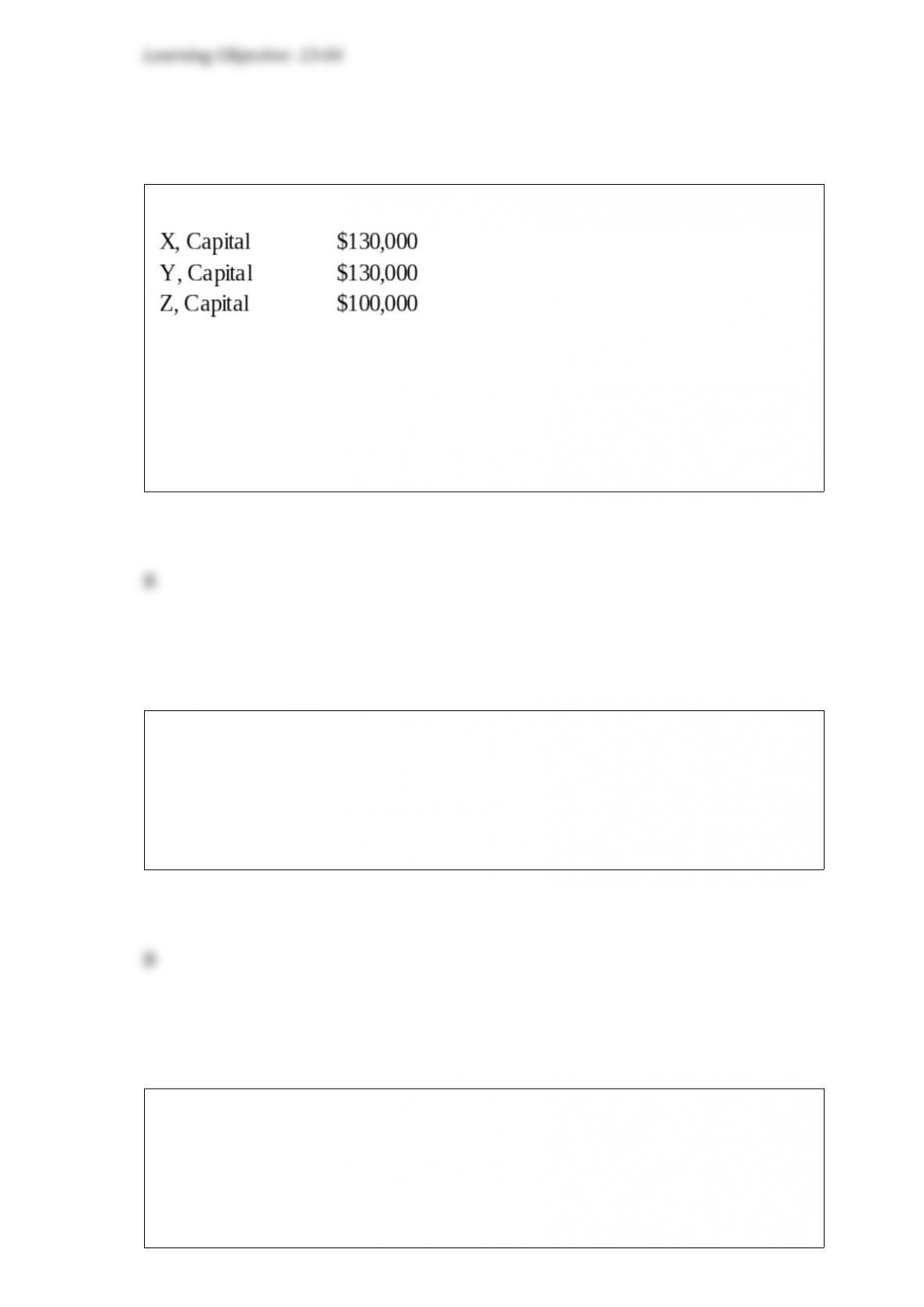

The capital balances, prior to the liquidation of the XYZ partnership, were as follows:

X, Y, and Z share profits and losses in the ratio of 5:3:2. As a result of a loan, the

partnership owes Y $80,000. Using the information above, which partner has the

highest Loss Absorption Power (LAP) prior to liquidation?

A. X

B. Y

C. Z

D. Both X and Y

Based on the preceding information, the entry to revalue the foreign currency payable

to current U.S. dollar value on May 31 will include a

A. credit to Foreign Currency Transaction Gain for $350.

B. credit to Foreign Currency Transaction Gain for $200.

C. debit to Foreign Currency Transaction Loss for $550.

D. debit to Foreign Currency Transaction Loss for $350.

Parent Corporation owns 90 percent of Subsidiary 1 Company’s stock and 75 percent of

Subsidiary 2 Company’s stock. During 20X8, Parent sold inventory purchased in 20X7

for $48,000 to Subsidiary 1 for $60,000. Subsidiary 1 then sold the inventory at its cost

of $60,000 to Subsidiary 2. Prior to December 31, 20X8, Subsidiary 2 sold $45,000 of

inventory to a nonaffiliate for $67,000 and held $15,000 in inventory at December 31,

20X8.

Based on the information given above, what amount of inventory must be eliminated

from the consolidated balance sheet for 20X8?

A. $2,400

B. $9,000

C. $12,000

D. $3,000

A donor agrees to contribute $5,000 per year at the end of each of the next five years to

a voluntary health and welfare organization. The donor did not place any use

restrictions on the amount pledged. The stream of the payments is discounted at 6

percent. The first payment of $5,000 is received at the end of the first year. The present

value factor for a five-payment annuity due on June 30, 20X9, at 6 percent is 4.2124.

Based on the preceding information, at the end of the first year, the pledge increased

unrestricted net assets by:

A. $25,000.

B. $21,062.

C. $4,212.

D. $5,000.

Based on the preceding information, what amount will be reported by the company as

cash received from customers during the year?

A. $590,000

B. $585,000

C. $575,000

D. $560,000

Company A holds 70 percent of the voting shares of Company B. During 20X8,

Company B sold land with a book value of $125,000 to Company A for $150,000.

Company A continues to hold the land at the end of the year. The companies file

separate tax returns and are subject to a 40 percent tax rate. Assume that Company A

uses the fully adjusted equity method in accounting for its investment in Company B.

Use the information given, but also assume that Company A holds the land at the end of

20X9. The consolidating entry relating to the intercorporate sale of land to be entered in

the consolidation worksheet prepared at the end of 20X9 will include a debit to

Investment in Company B for:

A. $4,500.

B. $7,500.

C. $15,000.

D. $10,500.

Consolidated financial statements are being prepared for Behemoth Corporation and its

two wholly-owned subsidiaries that have intercompany loans of $50,000 and

intercompany profits of $100,000. How much of these intercompany loans and profits

should be eliminated?

A. intercompany loans – $0; intercompany profits – $0

B. intercompany loans – $50,000; intercompany profits – $0

C. intercompany loans – $50,000; intercompany profits – $100,000

D. intercompany loans – $0; intercompany profits – $100,000

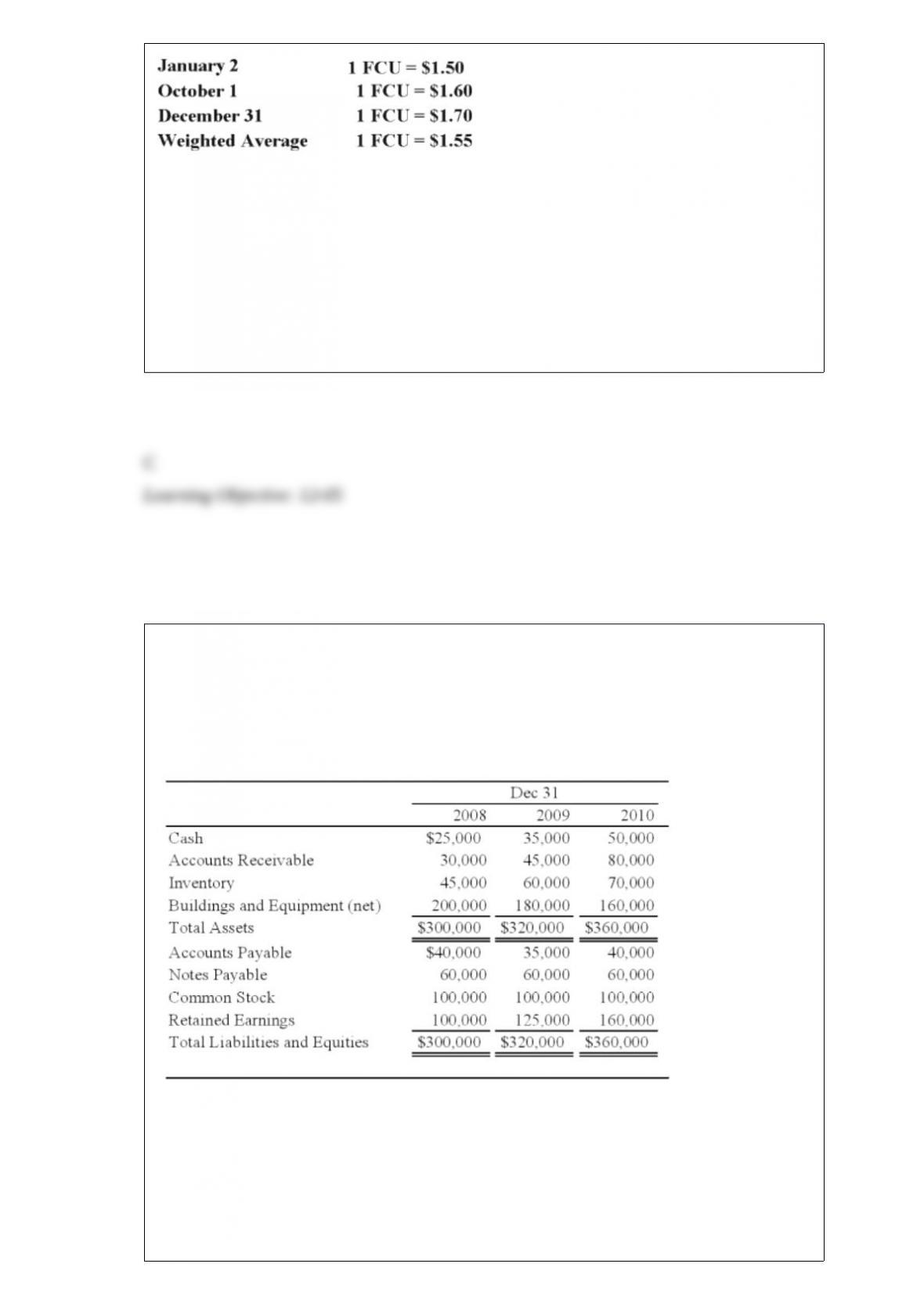

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming Perth’s local currency is the functional

currency, what is the balance in Johnson’s investment in foreign subsidiary account at

December 31, 2008?

A. $3,216,500

B. $3,560,000

C. $3,568,300

D. $3,577,694

Perfect Corporation acquired 70 percent of Trevor Company’s shares on December 31,

2008, for $140,000. At that date, the fair value of the noncontrolling interest was

$60,000. On January 1, 2010, Perfect acquired an additional 10 percent of Trevor’s

common stock for $32,500. Summarized balance sheets for Trevor on the dates

indicated are as follows:

Trevor paid dividends of $10,000 in each of the three years. Perfect uses the fully

adjusted equity method in accounting for its investment in Trevor and amortizes all

differentials over 5 years against the related investment income. All differentials are

assigned to patents in the consolidated financial statements.

Based on the preceding information, what was the balance in Perfect’s Investment in

Trevor Company Stock account on December 31, 2010?

A. $211,500

B. $218,000

C. $173,000

D. $216,000

Jupiter Corporation’s consolidated cash flow statement for the year ended December 31,

20X8, reported operating cash inflows of $160,000, financing cash outflows of

$90,000, and investing cash outflows $55,000, and an ending cash balance of $75,000.

Jupiter acquired 75 percent of Ganymede Company’s common stock on July 1, 20X6, at

book value. At that date, the fair value of the noncontrolling interest was equal to 25

percent of Ganymede Company’s book value. Ganymede reported net income of

$20,000, paid dividends of $8,000 in 20X8, and is included in Jupiter’s consolidated

statements. Jupiter paid dividends of $25,000 in 20X8. The indirect method is used in

computing cash flow from operations.

Based on the information provided, what was the consolidated cash balance at January

1, 20X8?

A. $60,000

B. $85,000

C. $15,000

D. $380,000

On January 1, 20X6, Nichols Corporation issued 10-year bonds at par to unrelated

parties. The bonds have a 10% stated rate, face value of $300,000, and pay interest

every June 30 and December 31. On December 31, 20X9, Harn Corporation purchased

all of Nichols’ bonds in the open market at a $6,000 discount. Harn is Nichols’ 80

percent owned subsidiary. Harn uses the effective interest method of amortization. The

consolidated income statement for the year 20X9 should report with respect to the

bonds:

I. interest expense of $30,000.

II. an extraordinary gain of $6,000.

A. I

B. II

C. Either I or II

D. Neither I nor II

Mint Corporation has several transactions with foreign entities. Each transaction is

denominated in the local currency unit of the country in which the foreign entity is

located. On October 1, 20X8, Mint purchased confectionary items from a foreign

company at a price of LCU 5,000 when the direct exchange rate was 1 LCU = $1.20.

The account has not been settled as of December 31, 20X8, when the exchange rate has

decreased to 1 LCU = $1.10. The foreign exchange gain or loss on Mint’s records at

year-end for this transaction will be:

A. $500 loss

B. $500 gain

C. $378 gain

D. $5,500 loss

Wakefield Company uses a perpetual inventory system. In August, it sold 2,000 units

from its LIFO-base inventory, which had originally cost $35 per unit. The replacement

cost is expected to be $45 per unit. The company is planning to reduce its inventory and

expects to replace only 1,500 of these units by December 31, the end of its fiscal year.

The company replaced 1,500 units in November at an actual cost of $50 per unit.

Based on the preceding information, in the entry in August to record the sale of the

2,000 units:

A. Cost of Goods Sold will be debited for $70,000.

B. Inventory will be credited for $85,000.

C. Excess of Replacement Cost over LIFO Cost of Inventory Liquidation will be

credited for $15,000.

D. Excess of Replacement Cost over LIFO Cost of Inventory Liquidation will be

credited for $67,000.

Which of the following items should not be included as revenue for a state government?

A. Property taxes levied in the current fiscal year.

B. Private property for which a state takes custody when the legal owner cannot be

found.

C. Amounts received from other financing sources.

D. Fines and licensing fees for which amounts cannot be budgeted.

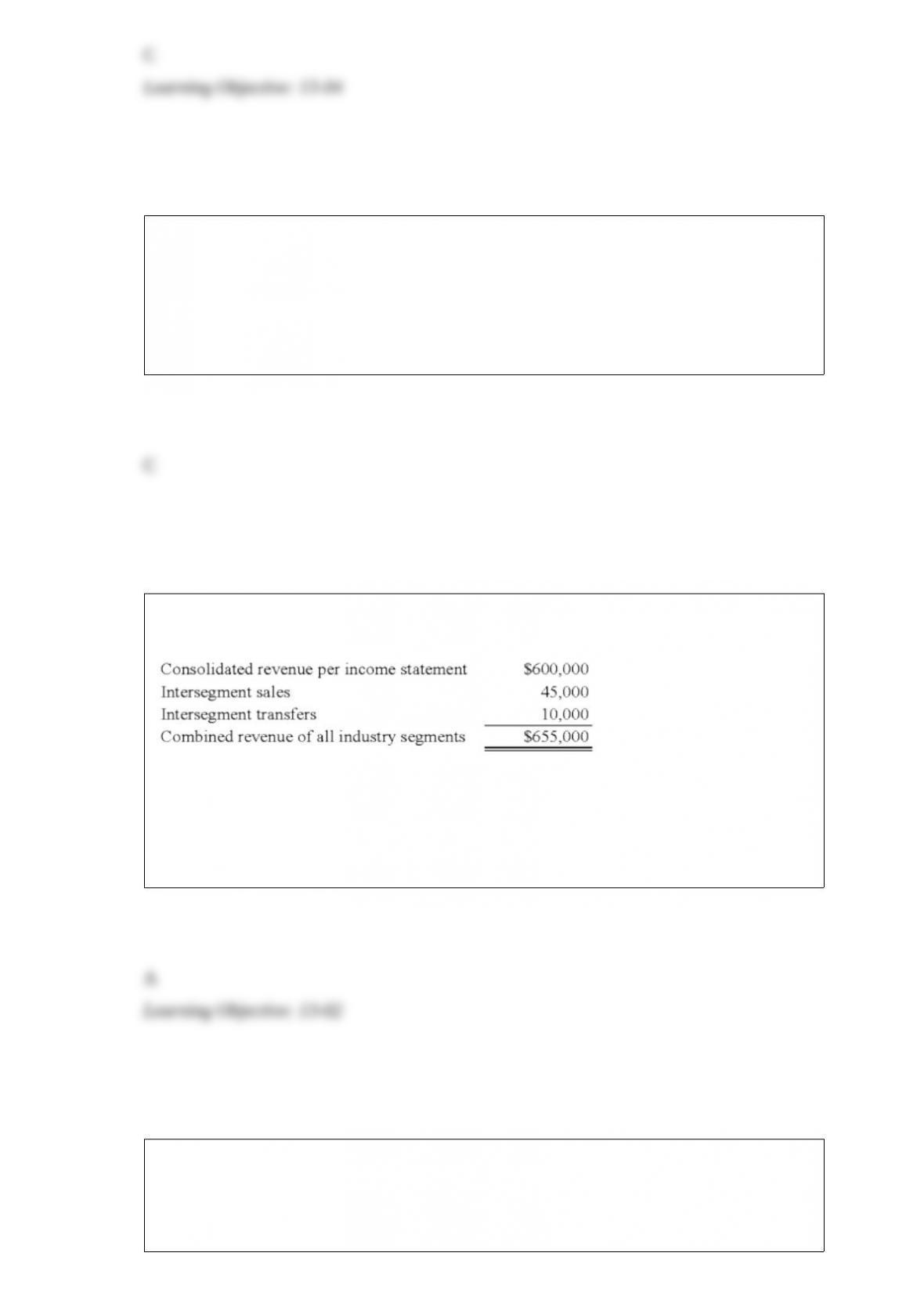

Trimester Corporation’s revenue for the year ended December 31, 20X8, was as

follows:

Trimester has a reportable operating segment if that segment’s revenue exceeds:

A. $65,500

B. $60,000

C. $64,500

D. $61,000

When a capital projects fund transfers a premium from the issuance of general

obligation bonds to another fund, the transfer should be accounted for as which type of

interfund transaction or transfer?

A. As a loan.

B. As an interfund transfer.

C. As revenue.

D. As a reimbursement.

Typically, the plan of reorganization must be approved by at least _____ of all creditors,

who must hold at least _____ of the dollar amount of the outstanding debt.

A. one-third; half

B. two-thirds; half

C. half; one-third

D. half; two-thirds

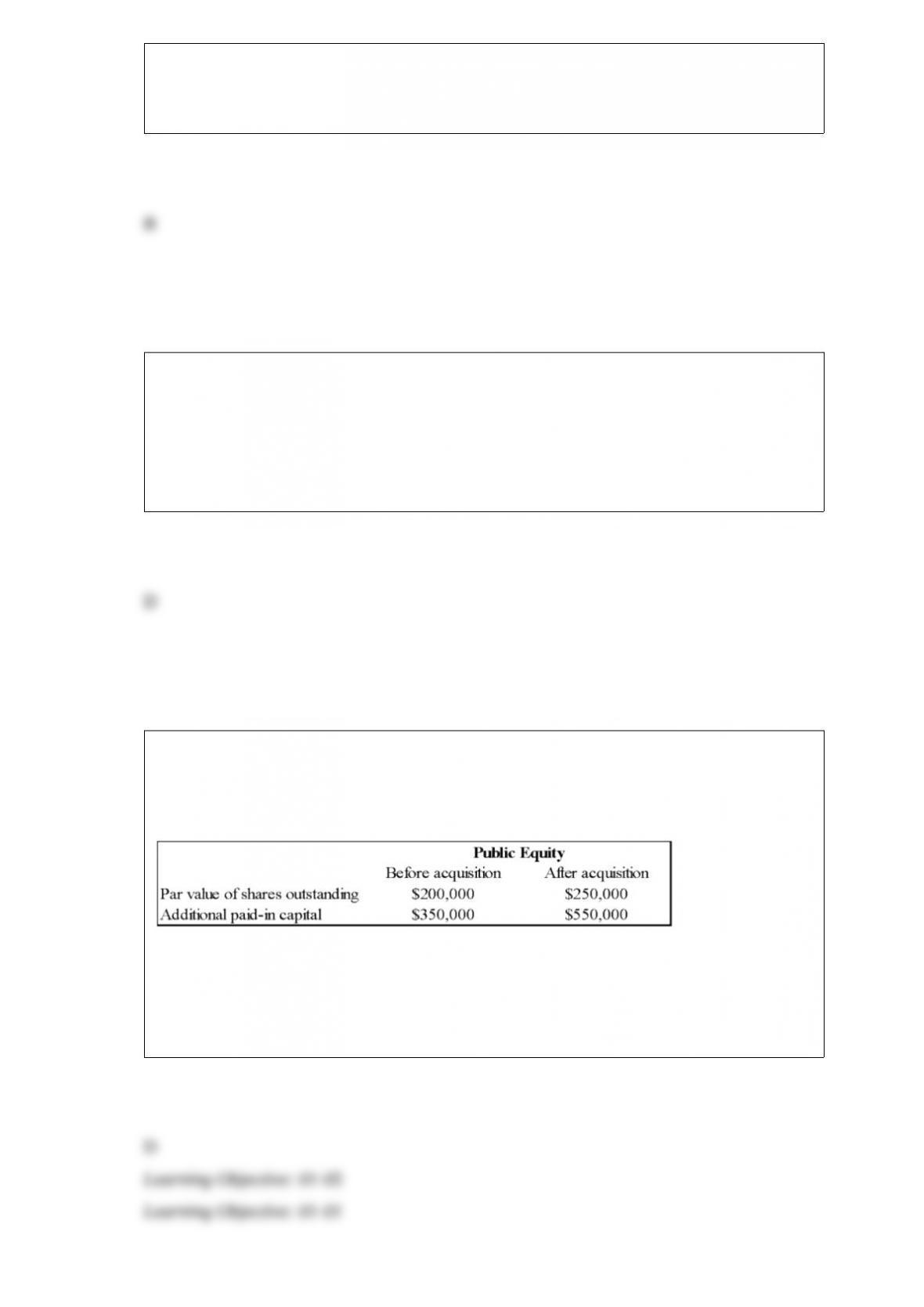

Public Equity Corporation acquired Lenore Company through an exchange of common

shares. All of Lenore’s assets and liabilities were immediately transferred to Public

Equity. Public’s common stock was trading at $20 per share at the time of exchange.

Following selected information is also available.

Based on the preceding information, what is the par value of Public’s common stock?

A. $10

B. $1

C. $5

D. $4

Schedule 13D is filed

A. by entities that acquire a beneficial ownership of more than 5 percent of a class of

registered equity securities.

B. to broadly report material information that is being provided to securities analysts,

selected institutional investors, or others.

C. to disclose material items related to asset-backed securities such as a bond issue.

D. by management to report the existence and effectiveness of the company’s internal

control over financial reporting.

Which of the following forms is the most comprehensive registration statement?

A. Form S-1

B. Form F-2

C. Form S-3

D. Form S-2