Chapter 10 – Additional Consolidation Reporting Issues

E10-6 Direct Method Cash Flow Statement

Consolidated Enterprises Inc. and Subsidiary

Consolidated Statement of Cash Flows

For the Year Ended December 31, 20X3

Cash Flows from Operating Activities:

Cash Received from Customers

$ 923,000

(a)

Cash Payments to Suppliers

(378,000)

(b)

Net Cash Provided by Operating Activities

$ 545,000

Cash Flows from Investing Activities:

Equipment Purchased

$(380,000)

Sale of Equipment

45,000

Net Cash Used in Investing Activities

(335,000)

Cash Flows from Financing Activities:

Sale of Bonds

$120,000

Repurchase of Common Stock

(35,000)

Dividends Paid:

To Parent Company Shareholders

(60,000)

To Noncontrolling Shareholders

(6,000)

Net Cash Provided by Financing Activities

19,000

Net Increase in Cash

$ 229,000

(a) $923,000 = $900,000 + $23,000

(b) $378,000 = $368,000 – $5,000 + $15,000

Consolidated Net Income

$464,000

Adjustments for noncash items:

Depreciation Expense

$73,000

Goodwill Impairment Loss

3,000

Gain on Sale of Equipment

(8,000)

Changes in operating assets and liabilities:

Decrease in Accounts Receivable

23,000

Increase in Inventory

(15,000)

Increase in Accounts Payable

5,000

Total Adjustments

81,000

Net Cash Provided by Operating Activities

$545,000

E10-7 Analysis of Consolidated Cash Flow Statement

a.

Dividends paid to noncontrolling interest

$ 6,000

Proportion of stock held by noncontrolling interest

÷ .40

Total dividends paid by Jones Delivery

$15,000

b.

When bonds are sold at a premium the annual cash payment is greater than

reported interest expense. The amount of premium amortized must therefore be

deducted from net income in determining the cash flow from operations.

c.

An increase in accounts receivable means that cash collections have been less

than sales for the period. The amount of the increase must be deducted from

operating income to determine the amount of cash actually made available from

current period operations.

d.

Dividends paid to noncontrolling shareholders are reported as a cash outflow in

the cash flow statement because they represent funds that have been distributed

during the period and are no longer available to the consolidated entity. On the

other hand, these same dividends are omitted from the retained earnings

statement. Only the income to the parent company shareholders is included in the

consolidated retained earnings statement and only dividends to the parent

company shareholders are deducted in deriving the ending consolidated retained

earnings balance.

e.

The loss occurred on a sale to a nonaffiliate. All profits and losses on sales to

affiliates are eliminated in the period of intercompany sale and are considered

realized as the equipment is depreciated by the purchasing affiliate.

E10-8 Midyear Acquisition

a.

The retained earnings balance reported for the consolidated entity as of January 1,

20X1, would be $400,000.

b.

Separate earnings of Yarn Manufacturing

$140,000

Net income reported by Spencer Corporation

$60,000

Portion of year ownership was held by Yarn

x 4/12

Income earned following acquisition

20,000

Consolidated net income

$160,000

Income to noncontrolling interest ($20,000 x .05)

(1,000)

Income to controlling interest

$159,000

c.

Consolidated retained earnings, January 1, 20X1

$400,000

Income to controlling interest

159,000

Dividends paid by Yarn Manufacturing

(80,000)

Consolidated retained earnings, December 31, 20X1

$479,000

d.

Purchase price on August 30, 20X1

$503,500

Equity method income

19,000

Dividends received from Spencer ($25,000 x .95)

(23,750)

Balance in investment account December 31, 20X1

$498,750

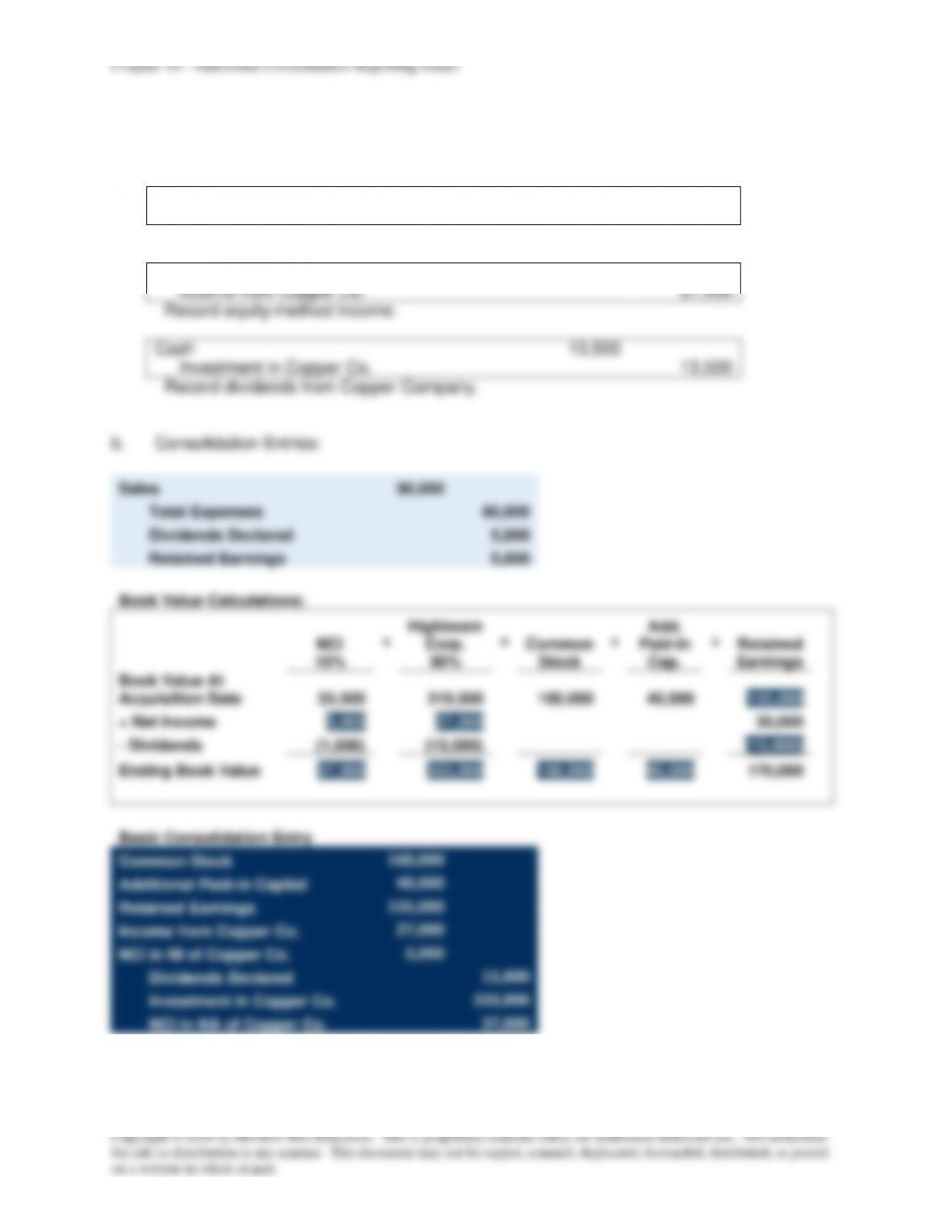

E10-9 Purchase of Shares at Midyear

a.

Journal entries recorded by Highbeam in 20X2:

Investment in Copper Co.

319,500

Cash

319,500

Record purchase of Copper Company Stock.

Investment in Copper Co.

27,000

Income from Copper Co.

27,000

Record equity-method income.

Cash

13,500

Investment in Copper Co.

13,500

Record dividends from Copper Company.

b.

Consolidation Entries:

E10-10 Deferred Tax Assets and Liabilities Arising in Acquisition

Fair Value

$28,000

Tax Basis

30,000

Book-Tax Difference (future deductible difference)

Deferred Tax Asset

2,000

x 0.40

800

Land:

Fair Value

$40,000

Tax Basis

10,000

Book-Tax Difference (future taxable difference)

Deferred Tax Liability

30,000

x 0.40

12,000

Fair Value

$15,000

Tax Basis

5,000

Book-Tax Difference (future taxable difference)

Deferred Tax Liability

10,000

x 0.40

4,000

Bond Payable:

Fair Value

$115,000

Tax Basis

120,000

Book-Tax Difference (future taxable difference)

Deferred Tax Liability

5,000

x 0.40

2,000

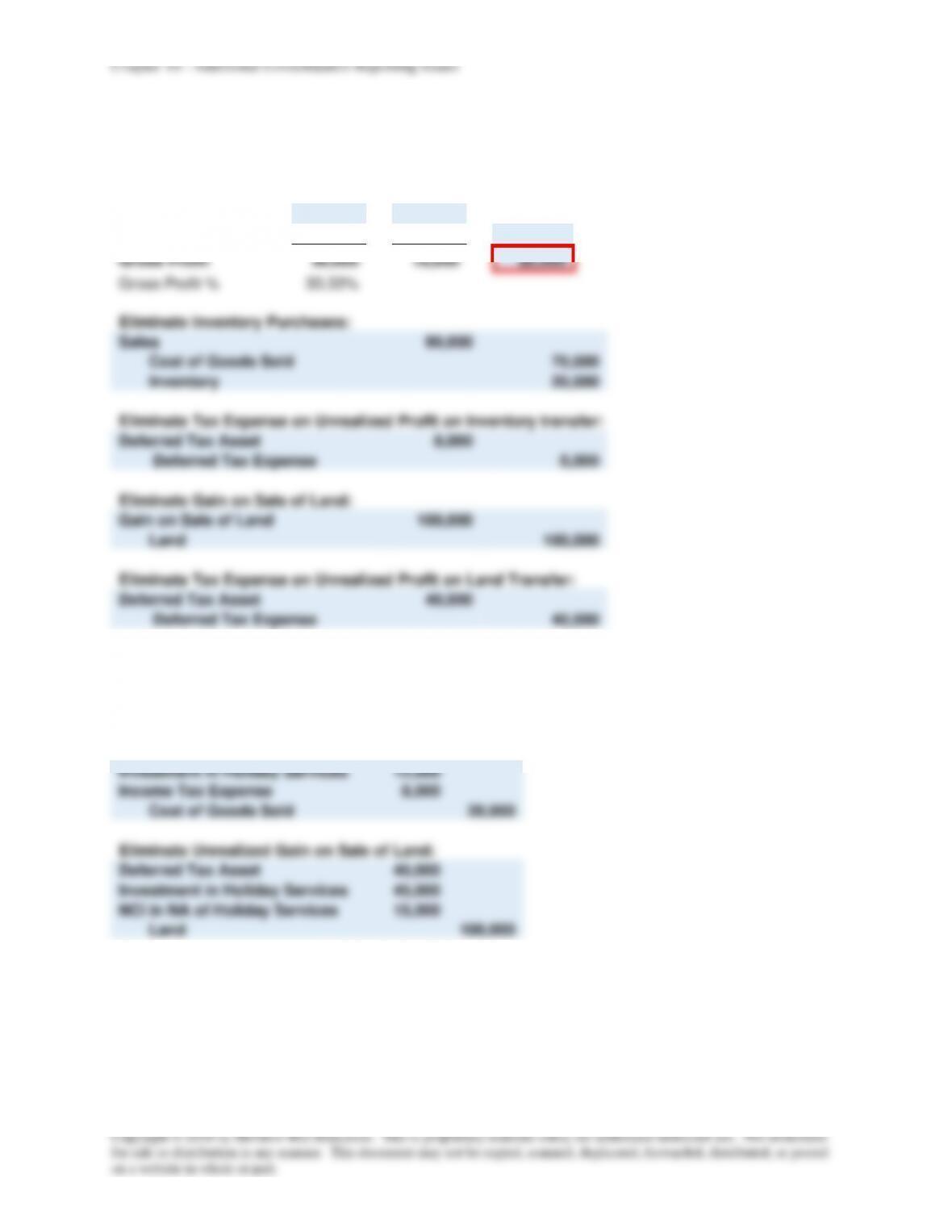

E10-11 Tax Deferral on Gains and Losses

Consolidation entries, December 31, 20X7:

Total

=

Re-sold

+

Ending

Inventory

Sales

90,000

30,000

60,000

COGS

60,000

20,000

40,000

Gross Profit

30,000

10,000

20,000

Gross Profit %

33.33%

Eliminate Inventory Purchases:

Sales

90,000

Cost of Goods Sold

70,000

Inventory

20,000

Eliminate Tax Expense on Unrealized Profit on Inventory transfer:

Deferred Tax Asset

8,000

Deferred Tax Expense

8,000

Eliminate Gain on Sale of Land:

Gain on Sale of Land

100,000

Land

100,000

Eliminate Tax Expense on Unrealized Profit on Land Transfer:

Deferred Tax Asset

40,000

Deferred Tax Expense

40,000

E10-12 Unrealized Profits in Prior Year

Consolidation entries, December 31, 20X8:

Eliminate Beginning InventoryPprofit:

Investment in Holiday Services

12,000

Income Tax Expense

8,000

Cost of Goods Sold

20,000

Eliminate Unrealized Gain on Sale of Land:

Deferred Tax Asset

40,000

Investment in Holiday Services

45,000

NCI in NA of Holiday Services

15,000

Land

100,000

E10-13 Allocation of Income Tax Expense

a.

Allocation of tax expense incurred in 20X5:

Winter

Ray Guard

Block

Item

Corporation

Corporation

Company

Reported operating income

$100,000

$50,000

$30,000

20X4 profits realized in 20X5

40,000

20,000

Unrealized profits in 20X5

sales

(10,000)

(20,000)

(10,000)

Realized income before tax

$130,000

$30,000

$40,000

Income tax assigned:

($130,000 / $200,000) x $80,000

$ 52,000

($30,000 / $200,000) x $80,000

$12,000

($40,000 / $200,000) x $80,000

$16,000

b.

Computation of consolidated net income and income to controlling interest:

Realized income before tax:

Winter Corporation

$130,000

Ray Guard Corporation

30,000

Block Company

40,000

Consolidated income before tax

$200,000

Income tax expense

(80,000)

Consolidated net income

$120,000

Income to noncontrolling interests:

Ray Guard Corporation ($30,000 – $12,000) x 0.20

$ 3,600

Block Company ($40,000 – $16,000) x 0.10

2,400

(6,000)

Income to controlling interest

$114,000

E10-14 Effect of Preferred Stock on Earnings per Share

Because both companies paid preferred dividends in 20X1 and neither issue is convertible, only

one basic consolidated earnings per share number will be reported for 20X1:

Operating income of Amber Corporation

$ 59,000

Net income of Newtop Company

$45,000

Less: Preferred dividends

(5,000)

Earnings available to Newtop common shareholders

40,000

Consolidated net income

$99,000

Less: Income to noncontrolling interest ($40,000 x .30)

(12,000)

Income to common shareholders of Amber Corporation

$87,000

Less: Preferred dividends of Amber Corporation

(9,000)

Earnings available to common shareholders

$78,000

Consolidated earnings per share for 20X1

($78,000 / 12,000 shares)

$6.50

E10-15 Effect of Convertible Bonds on Earnings per Share

Basic earnings per share:

Operating income of Crystal Corporation

$45,000

Contribution to consolidated EPS from Evans Company

($30,000 / 10,000) x 6,000 shares

18,000

Earnings available to common shareholders

$63,000

Consolidated earnings per share for 20X2

($63,000 / 30,000 shares)

$2.10

Diluted earnings per share:

Operating income of Crystal Corporation

$45,000

Contribution to consolidated EPS from Evans Company:

$30,000 + $12,000 (a)

x 6,000 shares

10,000 shares + 10,000 shares

12,600

Earnings available to common shareholders

$57,600

Consolidated earnings per share for 20X2

($57,600 / 30,000 shares)

$1.92

(a) $12,000 = ($200,000 x 0.10) x (1 – 0.40)

E10-16 Effect of Convertible Preferred Stock on Earnings per Share

Basic earnings per share:

Operating income of Eagle Corporation

$60,000

Contribution to consolidated EPS from Standard Company:

$45,000 – $12,000

x 8,000 shares

10,000 shares

26,400

Earnings available to shareholders

$86,400

Preferred dividends of Eagle Corporation

(16,000)

Earnings available to common shareholders

$70,400

Consolidated earnings per share for 20X1

($70,400 / 10,000 shares)

$7.04

Diluted earnings per share:

Operating income of Eagle Corporation

$60,000

Contribution to consolidated EPS from Standard Company:

$45,000

x 8,000 shares

10,000 shares + 15,000 shares

14,400

Earnings available to shareholders

$74,400

Preferred dividends of Eagle Corporation

(16,000)

Earnings available to common shareholders

$58,400

Consolidated earnings per share for 20X1

($58,400 / 10,000 shares)

$5.84

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

P10-17 Direct Method Computation of Cash Flows

Car Corporation and Subsidiary

Operating Cash Flows

For the Year Ended December 31, 20X1

Cash Flows from Operating Activities:

Cash Received from Customers

$533,000

Cash Payments to Suppliers

(268,000)

Net Cash Provided by Operating Activities

$265,000

Computation of payments received from customers

Sales of Car Corporation

$400,000

Sales to outside parties by Bus Company ($240,000 – $100,000)

140,000

Increase in Car Corporation accounts receivable

(9,000)

Decrease in Bus Company’s accounts receivable

2,000

Payments received from customers

$533,000

Computation of payments to suppliers

Cost of goods sold by Car Corporation excluding sale of

inventory purchased from Bus Company ($235,000 – $40,000)

$195,000

Cost of goods sold on sales by Bus Company

to outside parties ($105,000 – $70,000)

35,000

Cost of goods sold on intercompany sales

resold in period ($70,000 x 0.40)

28,000

Decrease in Car Corporation inventory

(22,000)

Increase in Bus Company inventory

16,000

Decrease in accounts payable of Car Corporation

31,000

Increase in accounts payable of Bus Company

(15,000)

Payment made to suppliers

$268,000

P10-18 Preparing a Statement of Cash Flows

a.

Metal Corporation and Ocean Company

Consolidated Cash Flow Worksheet

Year Ended December 31, 20X3

Balance

Balance

Item

1/1/X3

Debit

Credit

12/31/X3

Cash

68,500

(a) 32,000

100,500

Accounts Receivable

82,000

(b) 15,000

97,000

Inventory

115,000

(c) 8,000

123,000

Land

45,000

(d) 10,000

55,000

Buildings and Equipment

515,000

(e) 35,000

550,000

Patents

5,000

(f) 1,000

4,000

830,500

929,500

Accumulated Depreciation

186,500

(g)

36,500

223,000

Accounts Payable

61,000

(h)

5,000

66,000

Wages Payable

26,000

(i)

6,000

20,000

Notes Payable

250,000

(j) 15,000

265,000

Common Stock

150,000

150,000

Retained Earnings

130,000

(k) 30,000

(l) 74,500

174,500

Noncontrolling Interest

27,000

(m)

5,000

(l)

9,000

31,000

830,500

141,000

141,000

929,500

Cash Flows from Operating Activities:

Consolidated Net Income

(l) 83,500

Depreciation Expense

(g) 36,500

Amortization of Patent

(f)

1,000

Changes in Operating Assets and Liabilities:

Increase in Accounts Receivable

(b) 15,000

Increase in Inventory

(c) 8,000

Increase in Accounts Payable

(h) 5,000

Decrease in Wages Payable

(i)

6,000

Cash Flows from Investing Activities:

Purchase of Land

(d) 10,000

Purchase of Buildings and Equipment

(e) 35,000

Cash Flows from Financing Activities:

Increase in Notes Payable

(j)

15,000

Dividends Paid:

To Metal Corporation Shareholders

(k) 30,000

To Ocean Company Shareholders

(m)

5,000

Increase in Cash

(a) 32,000

141,000

141,000