During the fiscal year ended June 30, 20X9, the city of Moorhead constructed a new

courthouse which was budgeted to cost $5,000,000. Moorhead used a capital projects

fund to account for the construction activities. In July of 20X8, a bid was accepted from

Diamond Construction to build the courthouse for $4,800,000. On June 15, 20X9,

Diamond completed construction and submitted a bill to the city for $4,900,000. The

city accepted the bill and paid Diamond the entire amount owed, except for a 10

percentage retainage. On the statement of revenues, expenditures, and changes in fund

balance prepared for the capital projects fund for the year ended June 30, 20X9,

expenditures should be reported at

A. $4,900,000.

B. $4,800,000.

C. $4,410,000.

D. $4,320,000.

In a private, not-for-profit hospital, which fund would record cash and investments

which have been restricted by the governing board for acquisitions of equipment and

construction of a new hospital addition?

A. The plant replacement and expansion fund.

B. The specific purpose fund.

C. The endowment fund.

D. The general fund.

The following transactions were among those reported by Cliff County’s water and

sewer enterprise fund for 20X4:

Proceeds from sale of revenue bonds $5,000,000

Cash received from customer households 3,000,000

Capital contributed by subdividers 1,000,000

In the water and sewer enterprise fund’s statement of cash flows for the year ended

December 31, 20X4, what amount should be reported as cash flows from capital and

related financing activities?

A. $9,000,000

B. $6,000,000

C. $8,000,000

D. $5,000,000

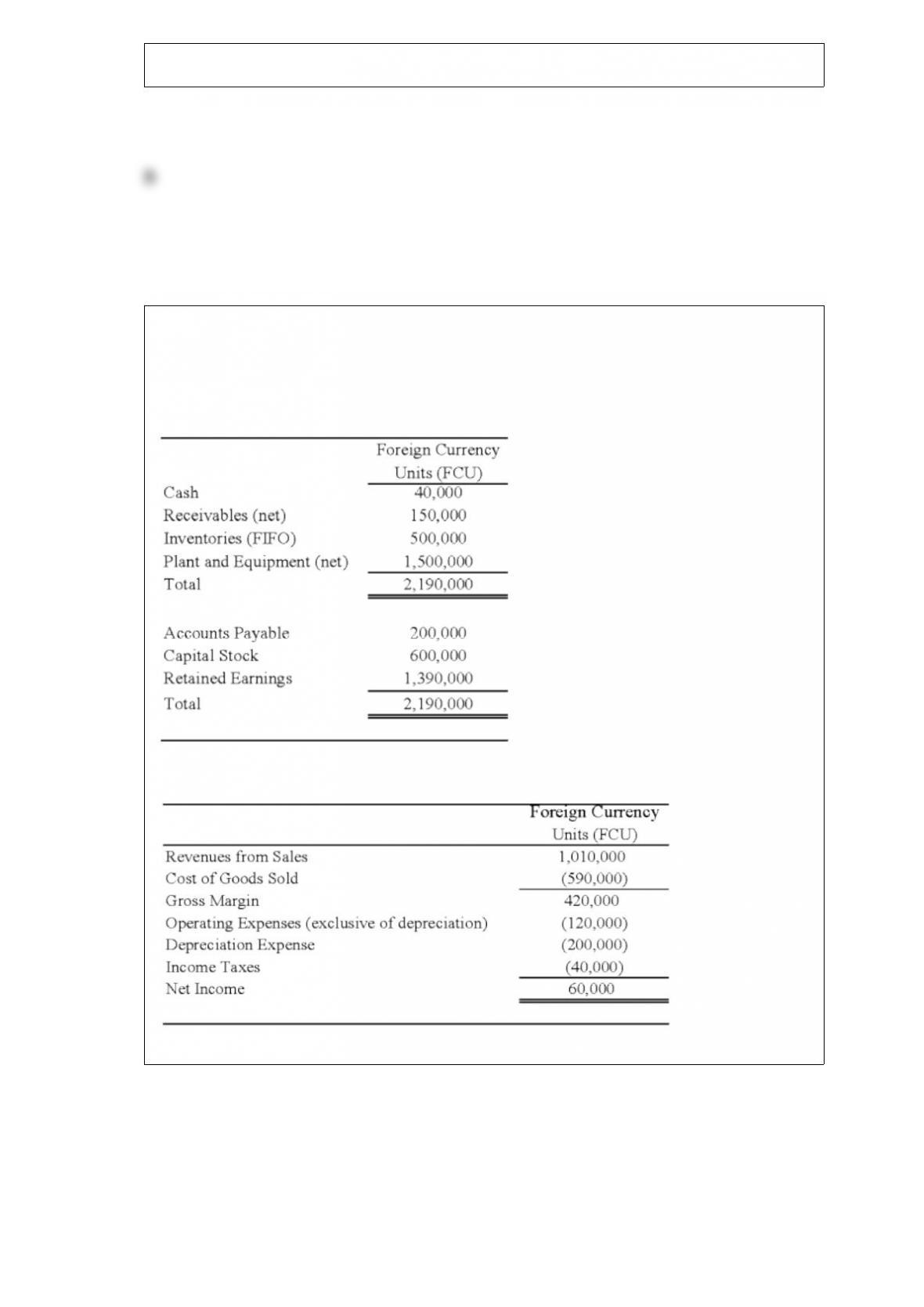

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the U.S. dollar is the functional currency,

what is Johnson’s remeasurement gain (loss) for 20X8? (Assume the ending inventory

was acquired on December 31, 20X8.)

A. $31,000 gain

B. $36,500 loss

C. $22,000 gain

D. $32,000 gain

On December 31, 20X8, Mercury Corporation acquired 100 percent ownership of

Saturn Corporation. On that date, Saturn reported assets and liabilities with book values

of $300,000 and $100,000, respectively, common stock outstanding of $50,000, and

retained earnings of $150,000. The book values and fair values of Saturn’s assets and

liabilities were identical except for land which had increased in value by $10,000 and

inventories which had decreased by $5,000.

Based on the preceding information, what amount of goodwill will be reported if the

acquisition price was $240,000?

A. $0

B. $40,000

C. $15,000

D. $35,000

On January 1, 20X9 Athlon Company acquired 30 percent of the common stock of

Opteron Corporation, at underlying book value. For the same year, Opteron reported net

income of $55,000, which includes an extraordinary gain of 40,000. It did not pay any

dividends during the year. By what amount would Athlon’s investment in Opteron

Corporation increase for the year, if Athlon used the equity method?

A. $0

B. $16,500

C. $4,500

D. $12,000

Miguel Corporation and Forest Company merged as of January 1, 20X3. Miguel paid

finder’s fees of $36,000 and legal fees of $8,000. Miguel also paid audit fees related to

the stock issuance of $12,000, stock registration fees of $7,000, and stock listing

application fees of $3,000.

Based on the preceding information, under the acquisition method

A. $22,000 of stock issue costs are treated as a reduction in the issue price.

B. $22,000 of stock issue costs are expensed.

C. $66,000 of stock issue costs are classified as goodwill.

D. $66,000 of stock issue costs are expensed.

Which of the following transactions of a private voluntary health and welfare

organization would increase temporarily restricted net assets in the statement of

activities for the current year?

I. Received a contribution of $20,000 from a donor in the current year who stipulated

that the money not be spent until the following year.

II. Spent $25,000 for fund raising during the current year from a donation from the

previous year.

A. I only

B. Both I and II

C. II only

D. Neither I nor II

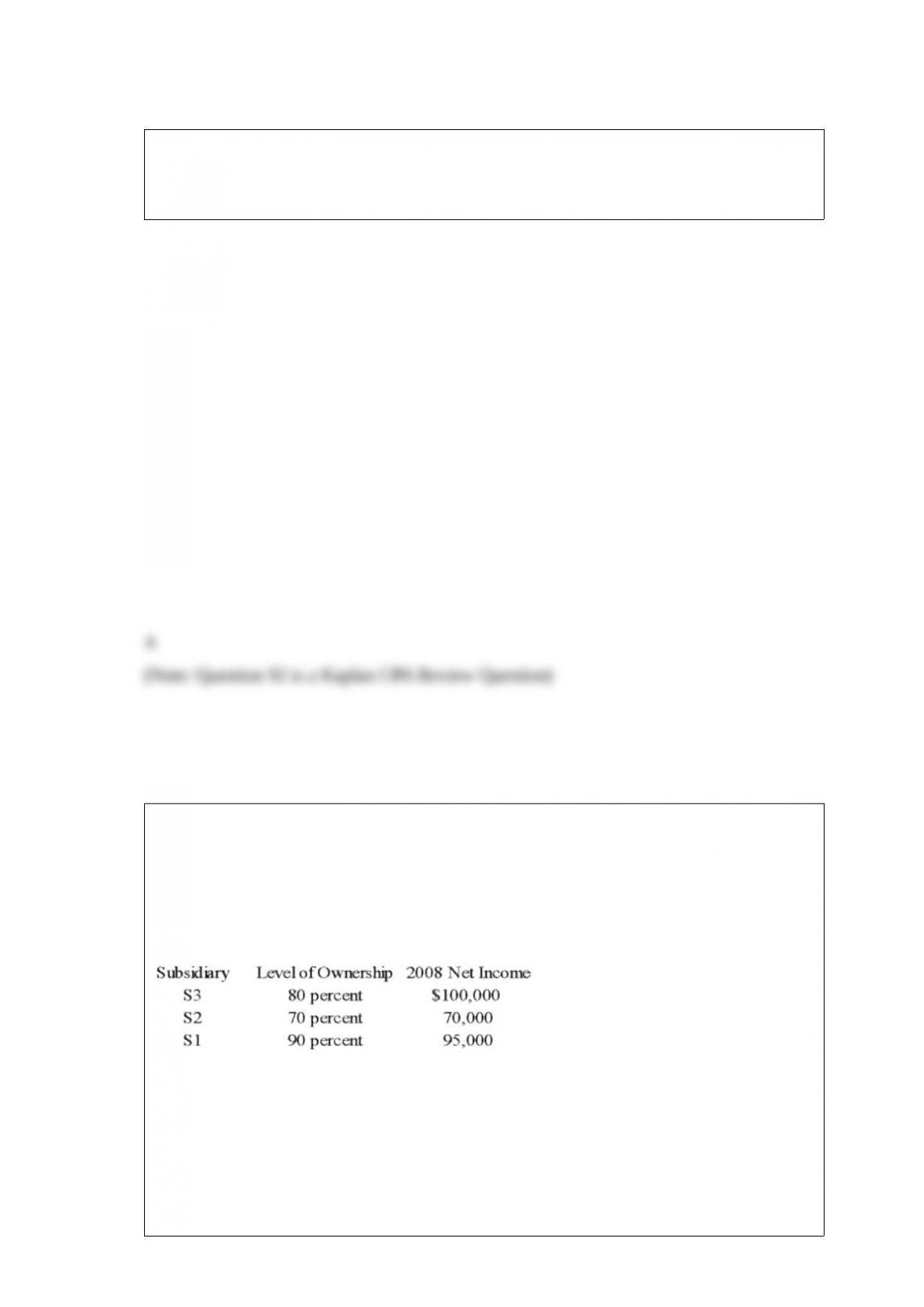

Parent Corporation purchased land from S1 Corporation for $220,000 on December 26,

20X8. This purchase followed a series of transactions between P-controlled

subsidiaries. On February 15, 20X8, S3 Corporation purchased the land from a

nonaffiliate for $160,000. It sold the land to S2 Company for $145,000 on October 19,

20X8, and S2 sold the land to S1 for $197,000 on November 27, 20X8. Parent has

control of the following companies:

Parent reported income from its separate operations of $200,000 for 20X8.

Based on the preceding information, what should be the amount of income assigned to

the controlling shareholders in the consolidated income statement for 20X8?

A. $369,400

B. $405,000

C. $465,000

D. $60,000

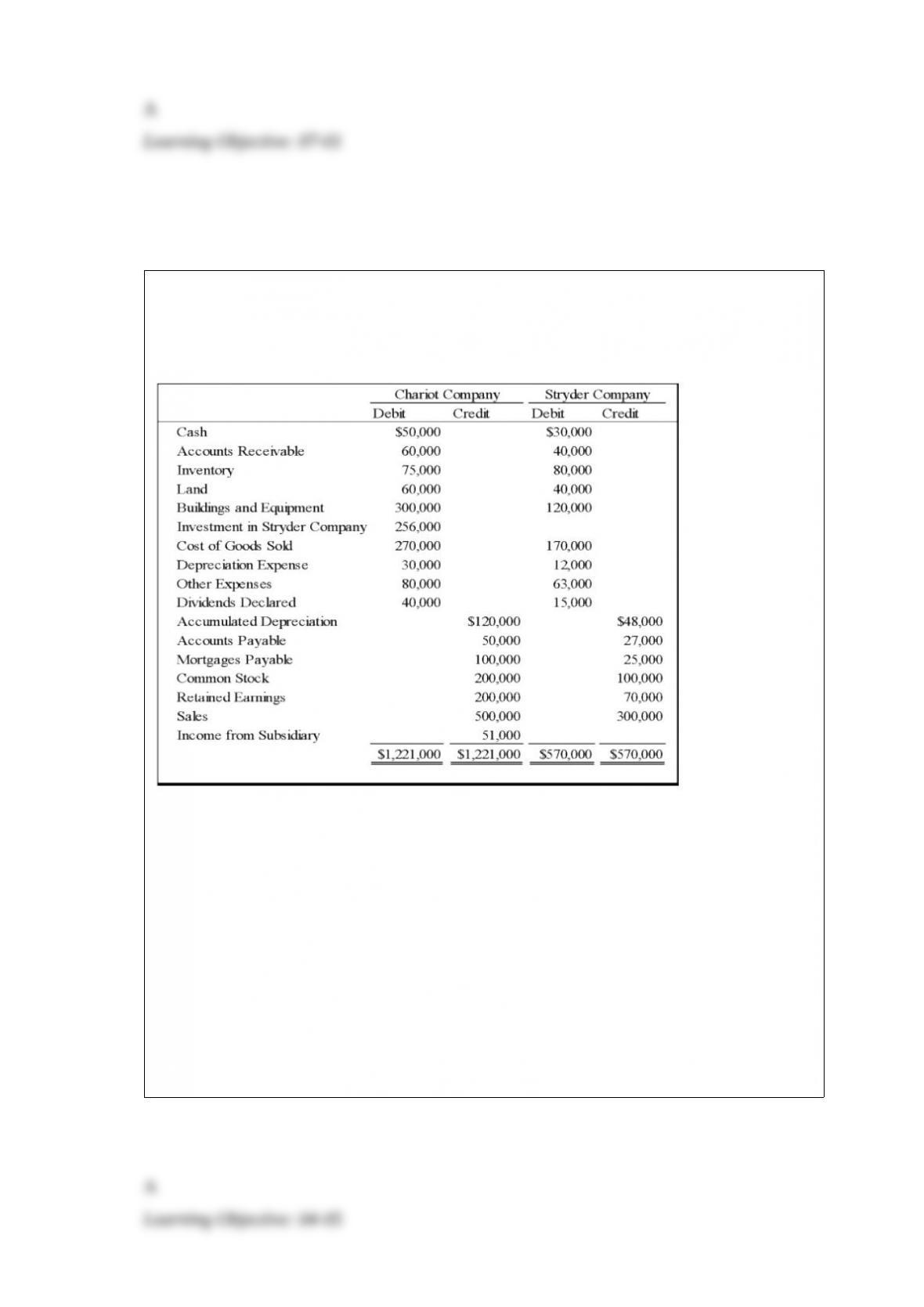

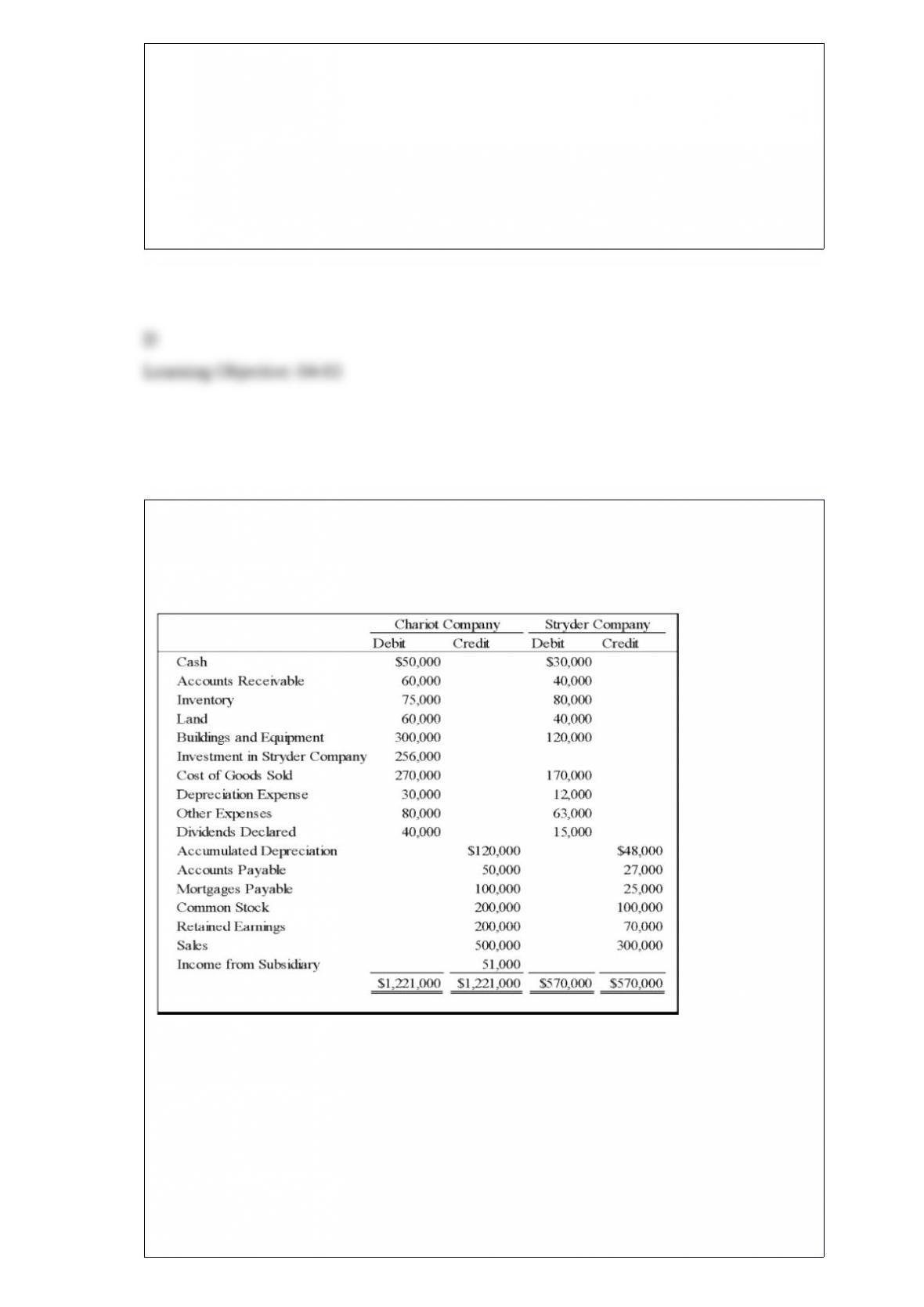

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder’s depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, what amount of retained earnings will be reported

in the consolidated financial statements for the year?

A. $331,000

B. $110,000

C. $441,000

D. $456,000

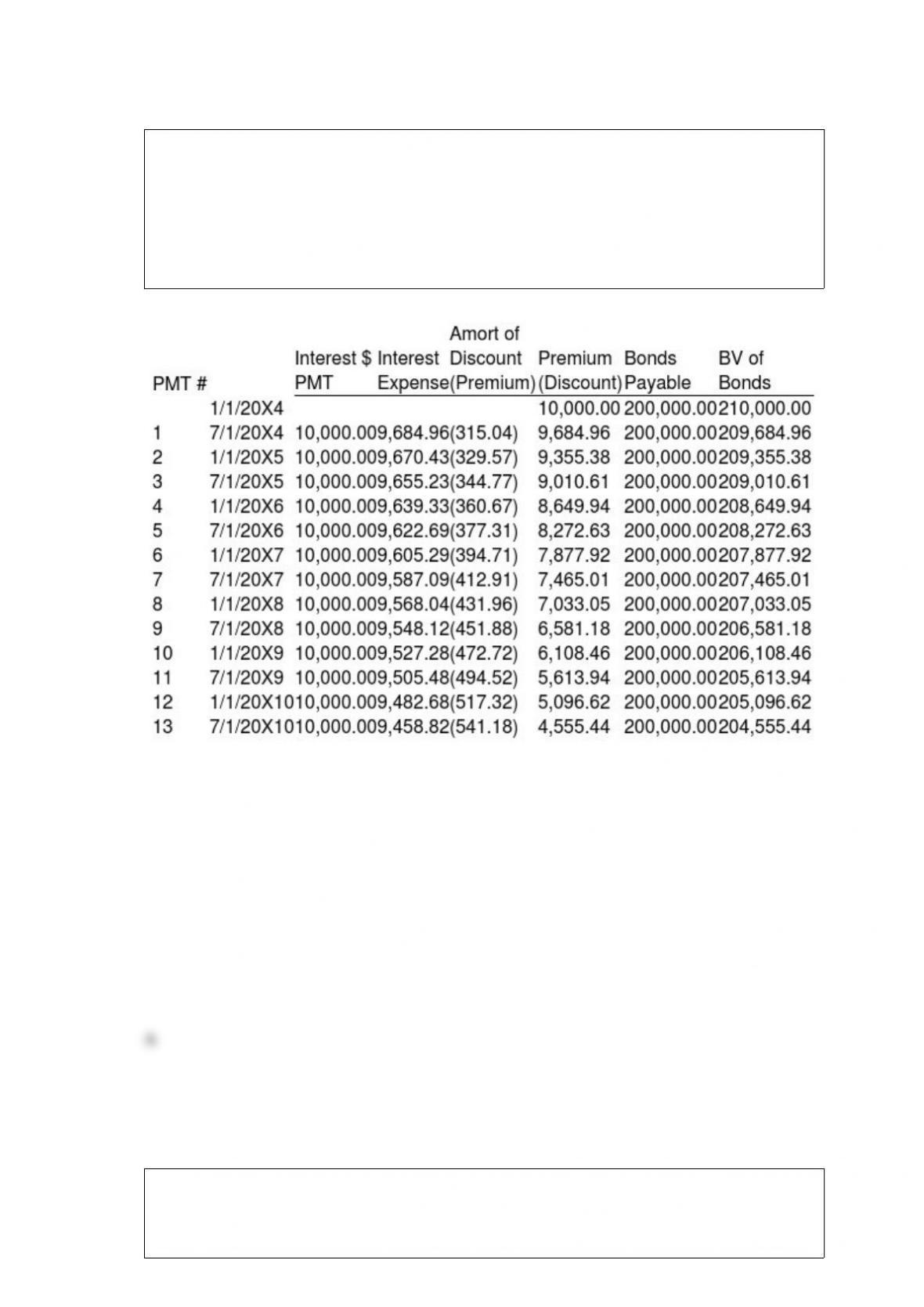

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on January 1, 20X8, for $122,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of interest income will be eliminated

in the preparation of the 20X9 consolidated financial statements?

A. $16,420

B. $11,494

C. $16,103

D. $11,291

Culver owns 80 percent of the common stock of Fowler Company. Culver also

purchases some of Fowler’s bonds directly from Fowler and holds the bonds as a

long-term investment. How is the acquisition of the bonds treated for consolidated

reporting purposes?

A. As a retirement of bonds.

B. As an increase in the Bonds Payable account on Fowler’s books.

C. Everything related to the intercompany bonds is eliminated in the consolidation

worksheet, and nothing related to the bonds appears in the consolidated financial

statements.

D. As an increase in noncurrent assets.

Which of the following observations concerning encumbrances is NOT true?

A. Their purpose is to ensure that the expenditures within a period do not exceed the

budgeted appropriations.

B. They provide a control system and safeguard for governmental unit administrators.

C. They are a unique element of governmental accounting.

D. They are recognized only at the time disbursements are made.

The general fund of Gillette levied property taxes of $400,000 on November 1, 20X8.

However, the property taxes are not collectible until May and August of 20X9. Assume

Gillette reports on the calendar year. On Gillette’s general fund balance sheet at

December 31, 20X8, the property taxes levied on November 1 should:

A. be reported as an asset and as a decrease in unassigned fund balance.

B. be reported as an asset and as an increase in unassigned fund balance.

C. be reported as an asset and as a reservation of fund balance.

D. be reported as an asset and as a deferred revenue.

Zeta Corporation and its subsidiary reported consolidated net income of $320,000 for

the year ended December 31, 20X8. Zeta owns 80 percent of the common shares of its

subsidiary, acquired at book value. Noncontrolling interest was assigned income of

$30,000 in the consolidated income statement for 20X8. What is the amount of separate

operating income reported by Zeta for the year?

A. $170,000

B. $150,000

C. $120,000

D. $200,000

How would a company report a change in an accounting principle made on the last day

of the third quarter?

A. Retrospective application to all pre-change interim periods reported.

B. No change is required.

C. Apply to current and prospective interim periods only.

D. Apply to prospective interim periods only.

Wright Company recently petitioned for bankruptcy and is now in the process of

preparing a statement of affairs. The carrying values and estimated fair values of the

assets of Wright Company are as follows:

Carrying Value Fair Value

Cash $10,000 $10,000

Accounts Receivable 60,000 20,000

Inventory 70,000 40,000

Land 90,000 75,000

Building (net) 200,000 150,000

Equipment (net) 80,000 25,000

Total $510,000 $320,000

Debts of Wright are as follows:

Accounts Payable $40,000

Wages Payable (all have priority) 6,000

Taxes Payable 12,000

Notes Payable (secured by receivables and inventory) 90,000

Interest on Notes Payable 5,000

Bonds Payable (secured by land and buildings) 200,000

Interest on Bonds Payable 8,000

Total $361,000

Based on the preceding information, what is the estimated dividend percentage?

A. 45 percent

B. 55 percent

C. 61 percent

D. 69 percent

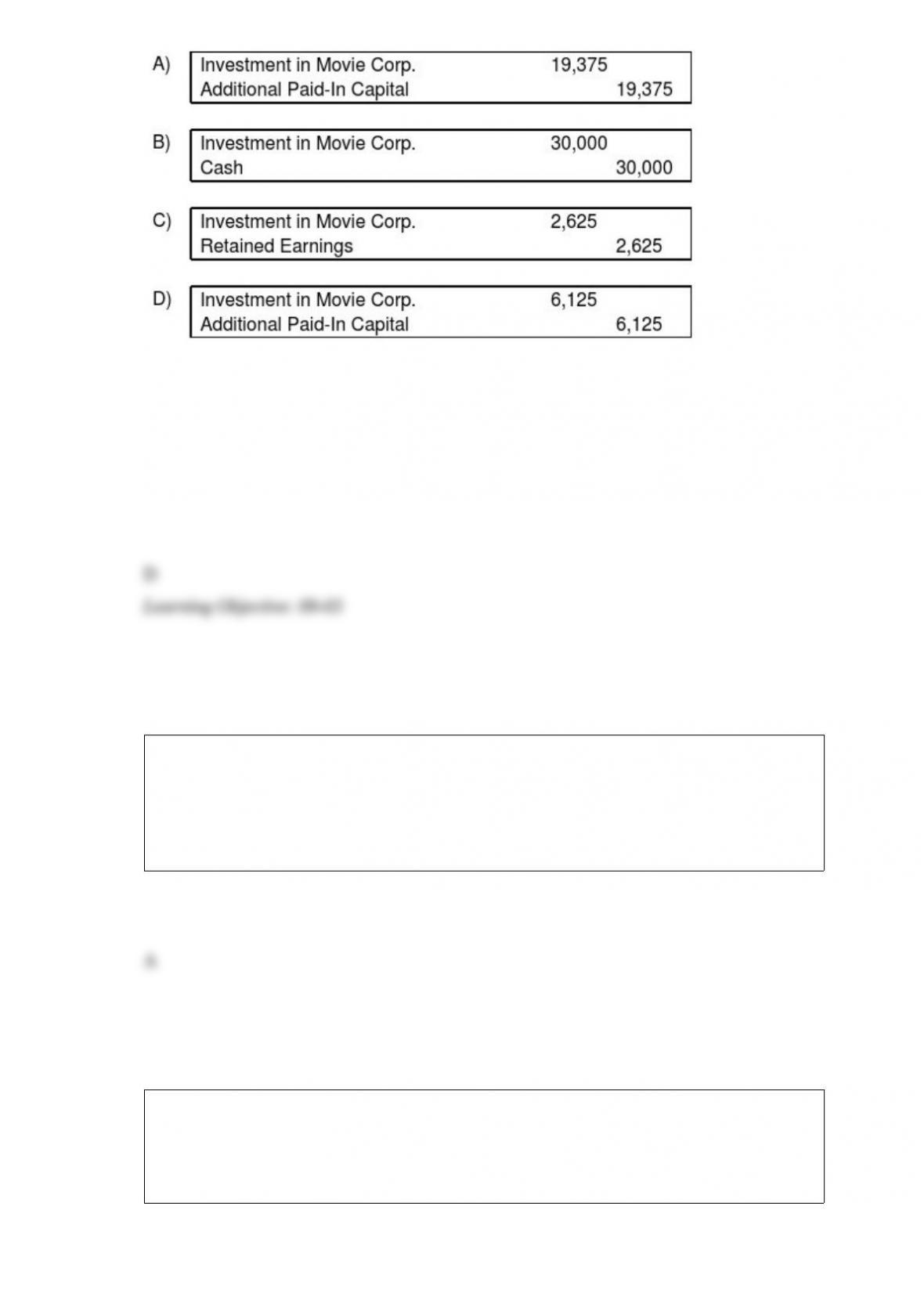

Cinema Company acquired 70 percent of Movie Corporation’s shares on December 31,

20X5, at underlying book value of $98,000. At that date, the fair value of the

noncontrolling interest was equal to 30 percent of the book value of Movie Corporation.

Movie’s balance sheet on January 1, 20X8, contained the following balances:

On January 1, 20X8, Movie acquired 5,000 of its own $2 par value common shares

from Nonaffiliated Corporation for $6 per share.

Based on the preceding information, what will be the journal entry to be recorded on

Cinema Company’s books to recognize the change in the book value of the shares it

holds?

A. Option A

B. Option B

C. Option C

D. Option D

What is the correct sequence in the expenditure process in governmental accounting?

A. Appropriation, Encumbrance, Expenditure, and Disbursement.

B. Encumbrance, Expenditure, Disbursement, and Appropriation.

C. Expenditure, Encumbrance, Disbursement, and Appropriation.

D. Appropriation, Expenditure, Encumbrance, and Disbursement.

On January 2, 20X8, Johnson Company acquired a 100% interest in the capital stock of

Perth Company for $3,100,000. Any excess cost over book value is attributable to a

patent with a 10-year remaining life. At the date of acquisition, Perth’s balance sheet

contained the following information:

Perth’s income statement for 20X8 is as follows:

The balance sheet of Perth at December 31, 20X8, is as follows:

Perth declared and paid a dividend of 20,000 FCU on October 1, 20X8. Spot rates at

various dates for 20X8 follow:

Assume Perth’s revenues, purchases, operating expenses, depreciation expense, and

income taxes were incurred evenly throughout 20X8.

Refer to the above information. Assuming the U.S. dollar is the functional currency,

what is Perth’s net income for 20X8 in U.S. dollars (include the remeasurement gain or

loss in Perth’s net income)?

A. $238,000

B. $228,000

C. $219,500

D. $202,000

Neptune Corporation owns 70 percent of Pluto Company’s stock. On July 1, 20X4,

Neptune sold a piece of equipment to Pluto for $56,350. Neptune had purchased this

equipment on January 1, 20X1, for $63,000. The equipment’s original 15-year

estimated total economic life remains unchanged. Both companies use straight-line

depreciation. The equipment’s residual value is considered negligible.

Based on the information provided, in the preparation of the 20X5 consolidated income

statement, depreciation expense will be

A. debited for $350 in the consolidation entries.

B. credited for $350 in the consolidation entries.

C. debited for $700 in the consolidation entries.

D. credited for $700 in the consolidation entries.

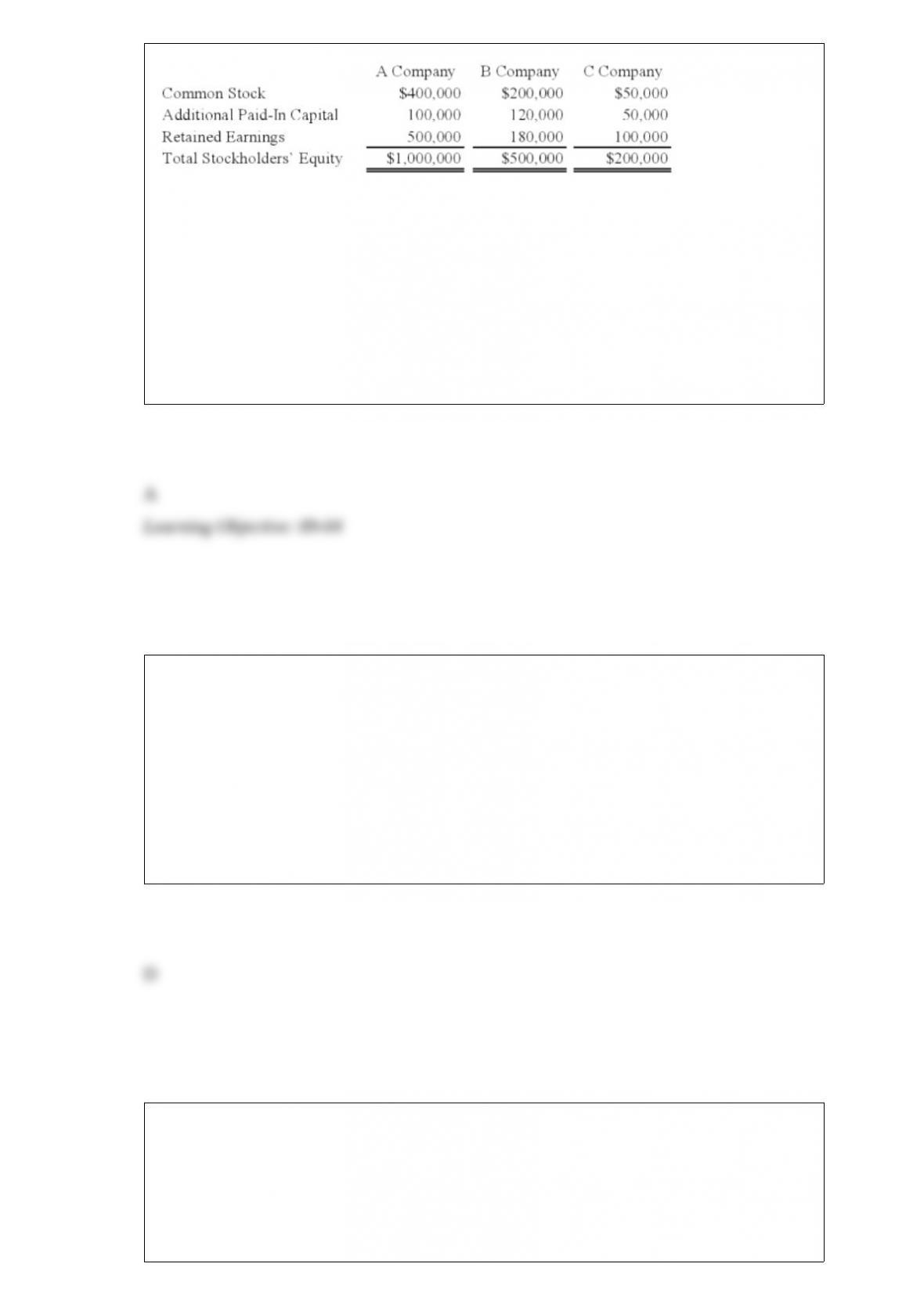

On January 1, 20X9, A Company acquired 85 percent of B Company’s voting common

stock for $425,000. At that date, the fair value of the noncontrolling interest of B

Company was $75,000. Immediately after A Company acquired its ownership, B

Company acquired 75 percent of C Company’s stock for $150,000. The fair value of the

noncontrolling interest of C Company was $50,000 at that date. At January 1, 20X9, the

stockholders’ equity sections of the balance sheets of the companies were as follows:

During 20X9, A Company reported operating income of $175,000 and paid dividends

of $50,000. B Company reported operating income of $125,000 and paid dividends of

$40,000. C Company reported net income of $100,000 and paid dividends of $25,000.

Based on the information provided, what amount of income will be assigned to the

noncontrolling interest in the consolidated income statement for 20X9?

A. $55,000

B. $25,000

C. $30,000

D. $43,750

Which of the following statements best describes limited partnerships?

A. In an LLP, there must be at least one general partner that is personally liable for the

obligations of the partnership and has management responsibilities.

B. There are no general or limited partners in a LP; each partner has the rights and

duties of a general partner, but limited legal liability.

C. The identifier LP or LLP need not be included in the name or identification of a

limited partnership.

D. If the presumption of control by the general partner can be overcome, the partner

would account for its investment using the equity method of accounting.

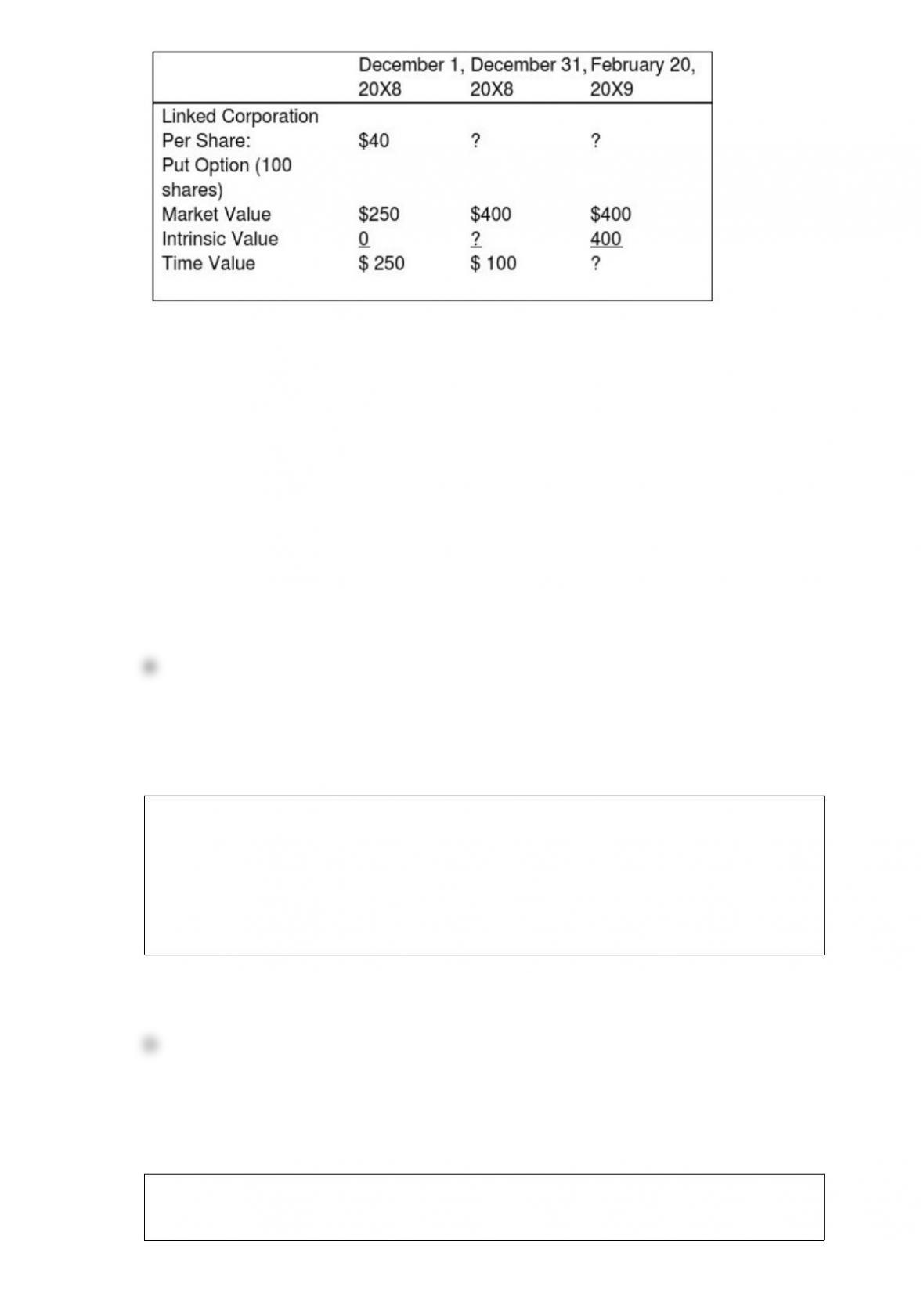

On December 1, 20X8, Winston Corporation acquired 100 shares of Linked

Corporation at a cost of $40 per share. Winston classifies them as available-for-sale

securities. On this same date, it decides to hedge against a possible decline in the value

of the securities by purchasing, at a cost of $250, an at-the-money put option to sell the

100 shares at $40 per share. The option expires on February 20, 20X9. Selected

information concerning the fair values of the investment and the options follow:

Assume that Winston exercises the put option and sells Linked shares on February 20,

20X9.

Based on the preceding information, what is the market price of Linked Corporation stock

on December 31, 20X8?

A. $40

B. $37

C. $36

D. $38

All of the following are elements of the statement of financial condition for state and

local governments with the exception of:

A. Assets and Liabilities

B. Deferred inflow and outflow of resources

C. Net position

D. Inflow and outflow of resources

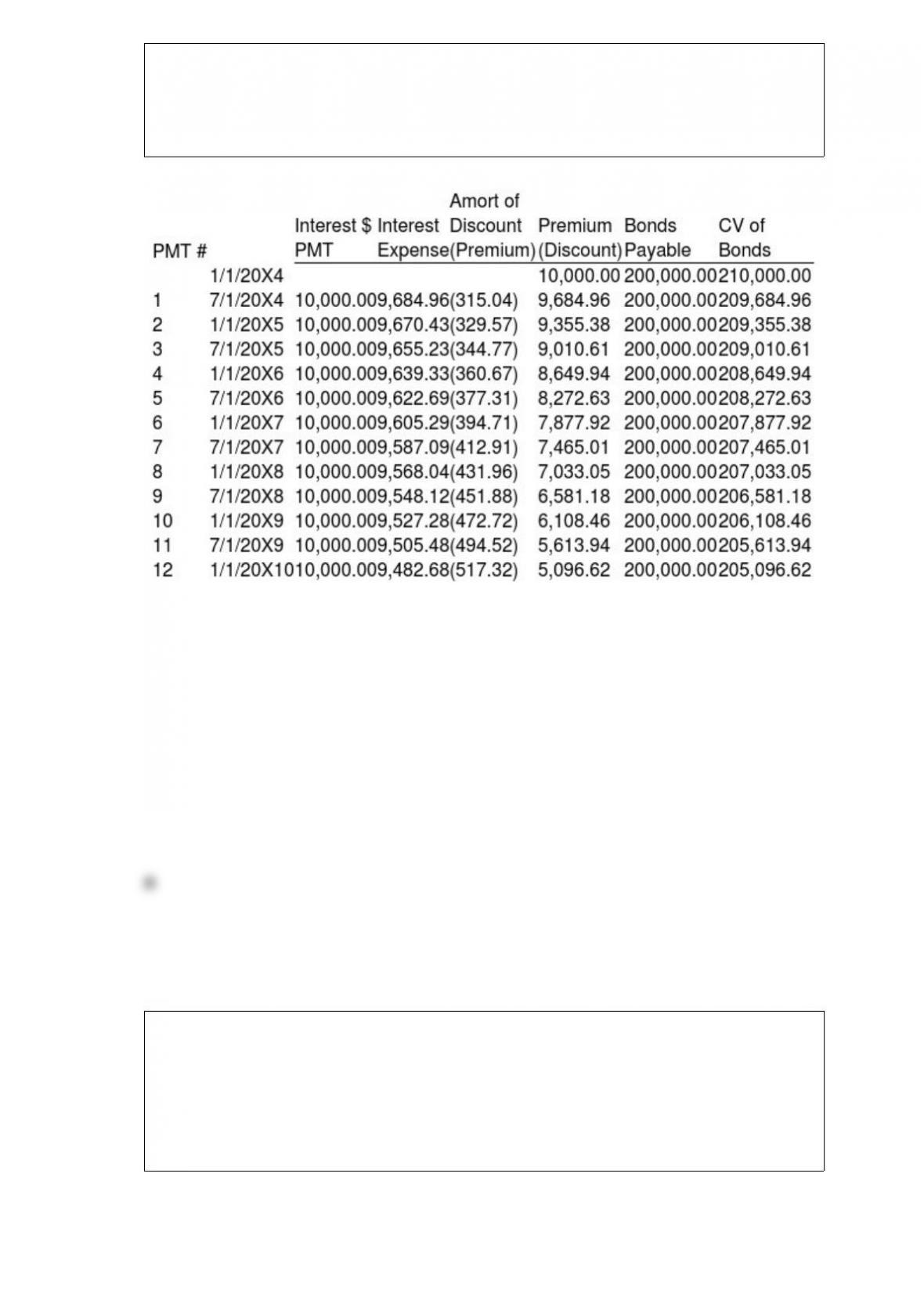

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on December 31, 20X8, for $125,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of premium on bonds payable will be

eliminated in the preparation of the December 31, 20X9 consolidated financial statements?

A. $5,097

B. $3,568

C. $5,614

D. $3,930

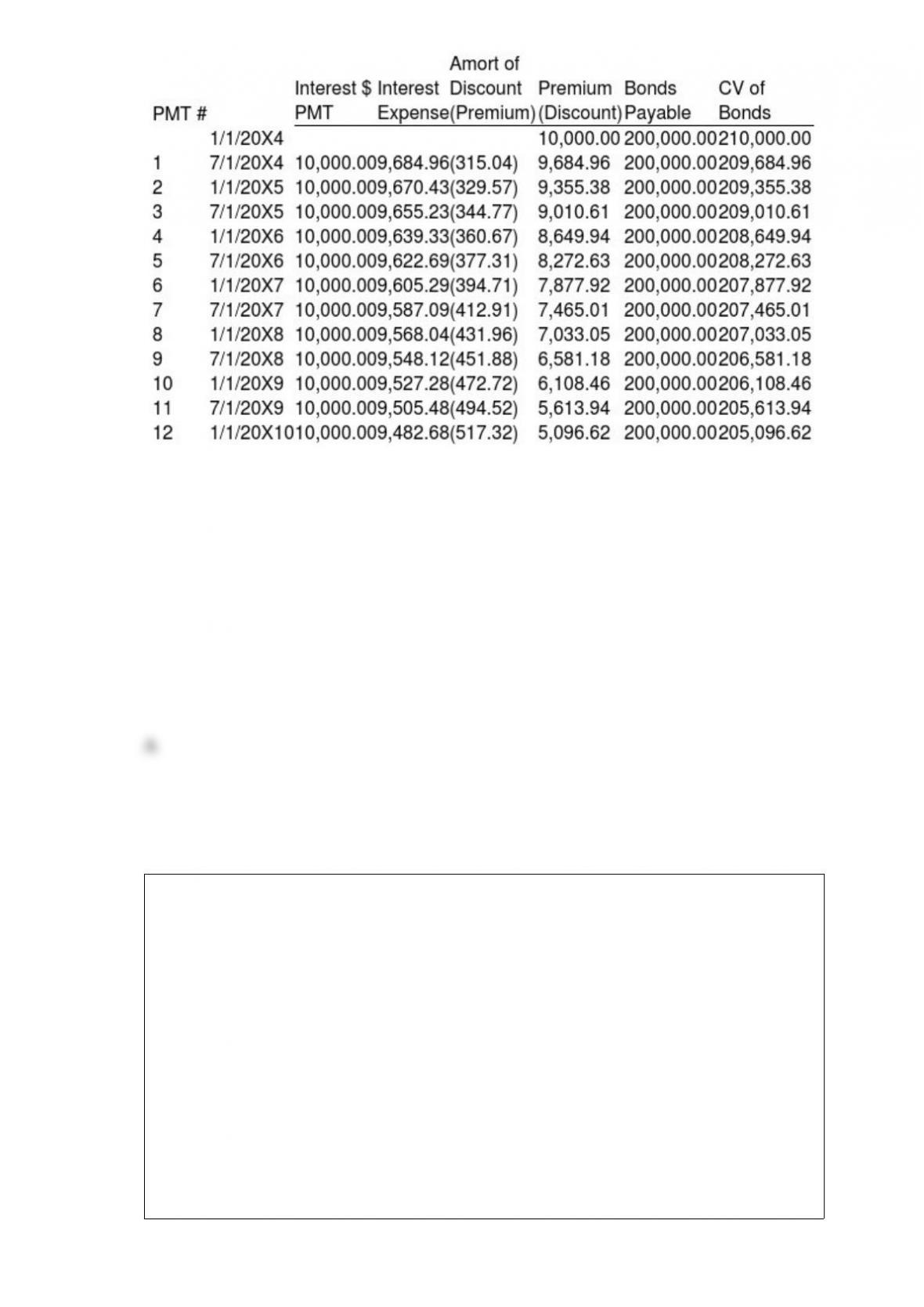

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite’s bonds from the

original purchaser on December 31, 20X8, for $125,000. Mortar owns 75 percent of

Granite’s voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of premium on bonds payable will be

eliminated in the preparation of the December 31, 20X8 consolidated financial statements?

A. $4,276

B. $6,108

C. $6,581

D. $4,607

Tinitoys, Inc., a domestic company, purchased inventory from a Brazilian company for

500,000 Brazilian reals (Br. reals) on May 1, 20X2. Payment is due on June 30, 20X2.

On May 1, 20X2, Tinitoys also entered into a 60-day forward contract to purchase

500,000 Brazilian reals. The forward contract is not designated as a hedge. Tinitoys’

fiscal year ends on May 31. The direct exchange rates were as follows:

Spot Rate Forward Rate

May 1, 20X2 $0.523 $0.525 (60 days)

May 31, 20X2 $0.516 $0.52 (30 days)

June 30, 20X2 $0.508

Based on the preceding information, the entries on June 30, 20X2, include a

A. debit to Dollars Payable to Exchange Broker, $262,500.

B. credit to Cash, $254,000.

C. credit to Premium on Forward Contract, $6,000.

D. credit to Foreign Currency Receivable from Exchange Broker, $262,500.

Winner Corporation acquired 80 percent of the common shares and 70 percent of the

preferred shares of First Corporation at underlying book value on January 1, 20X9. At

that date, the fair value of the noncontrolling interest in First’s common stock was equal

to 20 percent of the book value of its common stock. First’s balance sheet at the time of

acquisition contained the following balances:

The preferred shares are cumulative and have a 10 percent annual dividend rate and are

four years in arrears on January 1, 20X9. All of the $5 par value preferred shares are

callable at $6 per share. During 20X9, First reported net income of $100,000 and paid

no dividends.

Based on the preceding information, the amount assigned to noncontrolling

stockholders’ share of preferred stock interest in the preparation of a consolidated

balance sheet on January 1, 20X9, is:

A. $40,000

B. $42,000

C. $36,000

D. $48,000

Consolidated net income may include the parent’s separate operating income plus the

parent’s share of the subsidiary’s reported net income:

A. plus the unrealized profit on upstream intercompany sales of inventory made during

the current year.

B. plus the profit realized this year from upstream intercompany sales of inventory

made last year.

C. plus unrealized profit on downstream intercompany sales of inventory made during

the current year.

D. minus the parent’s share of profit realized this year from upstream intercompany

sales of inventory made last year.

A statutory consolidation is a type of business combination in which:

A. one of the combining companies survives and the other loses its separate identity.

B. one company acquires the voting shares of the other company and the two

companies continue to operate as separate legal entities.

C. two publicly traded companies agree to share a board of directors.

D. each of the combining companies is dissolved and the net assets of both companies

are transferred to a newly created corporation.

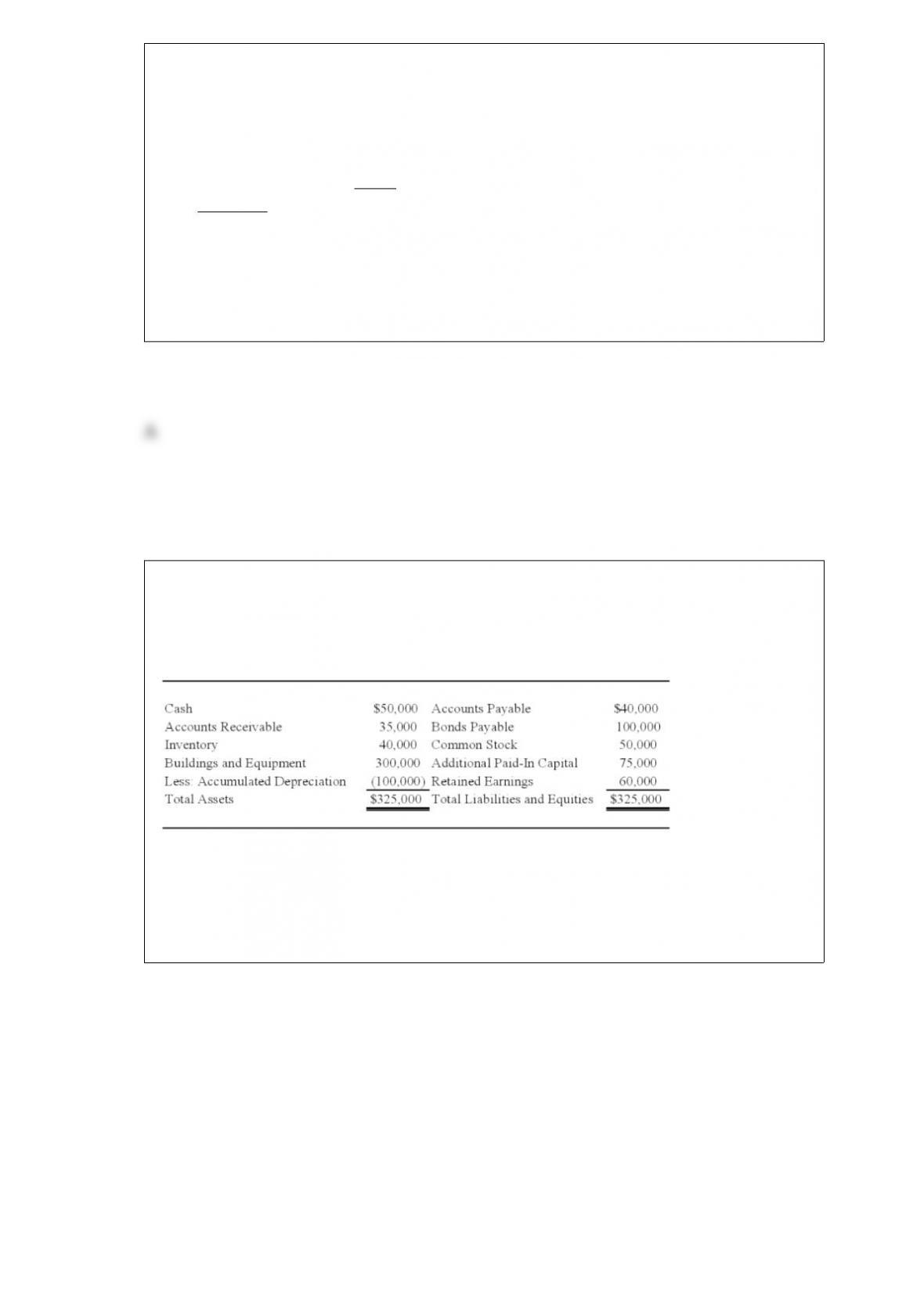

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, what is the differential associated with the

acquisition?

A. $15,000

B. $20,000

C. $22,000

D. $37,000

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder’s depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, the differential associated with this acquisition is:

A. $36,000.

B. $40,000.

C. $10,000.

D. $50,000.

Pone Company purchased 100 percent of Sone Inc. on January 1, 20X9 for $625,000.

Sone reported earnings of $76,000 and declared dividends of $8,000 during 20X9.

Based on the preceding information and assuming Pone uses the equity method to

account for its investment in Sone, what is the balance in Pone’s Investment in Sone

account on December 31, 20X9, prior to consolidation?

A. $617,000

B. $625,000

C. $633,000

D. $693,000

Peter Architectural Services owns 100 percent of Smith Manufacturing. During the

course of 20X8 Peter provides $100,000 of architectural services associated with

Smith’s new manufacturing facility, which will open January 4, 20X9, and has a 5 year

useful life. Explain the impact providing this service has on Peter Architectural

Services’ 20X8 and 20X9 consolidated financial statements.

Rivendell Corporation and Foster Company merged as of January 1, 20X9. To effect the

merger, Rivendell paid finder’s fees of $40,000, legal fees of $13,000, audit fees related

to the stock issuance of $10,000, stock registration fees of $5,000, and stock listing

application fees of $4,000.

Based on the preceding information, under the acquisition method:

A. $72,000 of stock issue costs are treated as goodwill.

B. B. $19,000 of stock issue costs are treated as a reduction in the issue price.

C. C. $19,000 of stock issue costs are expensed.

D. D. $72,000 of stock issue costs are expensed.

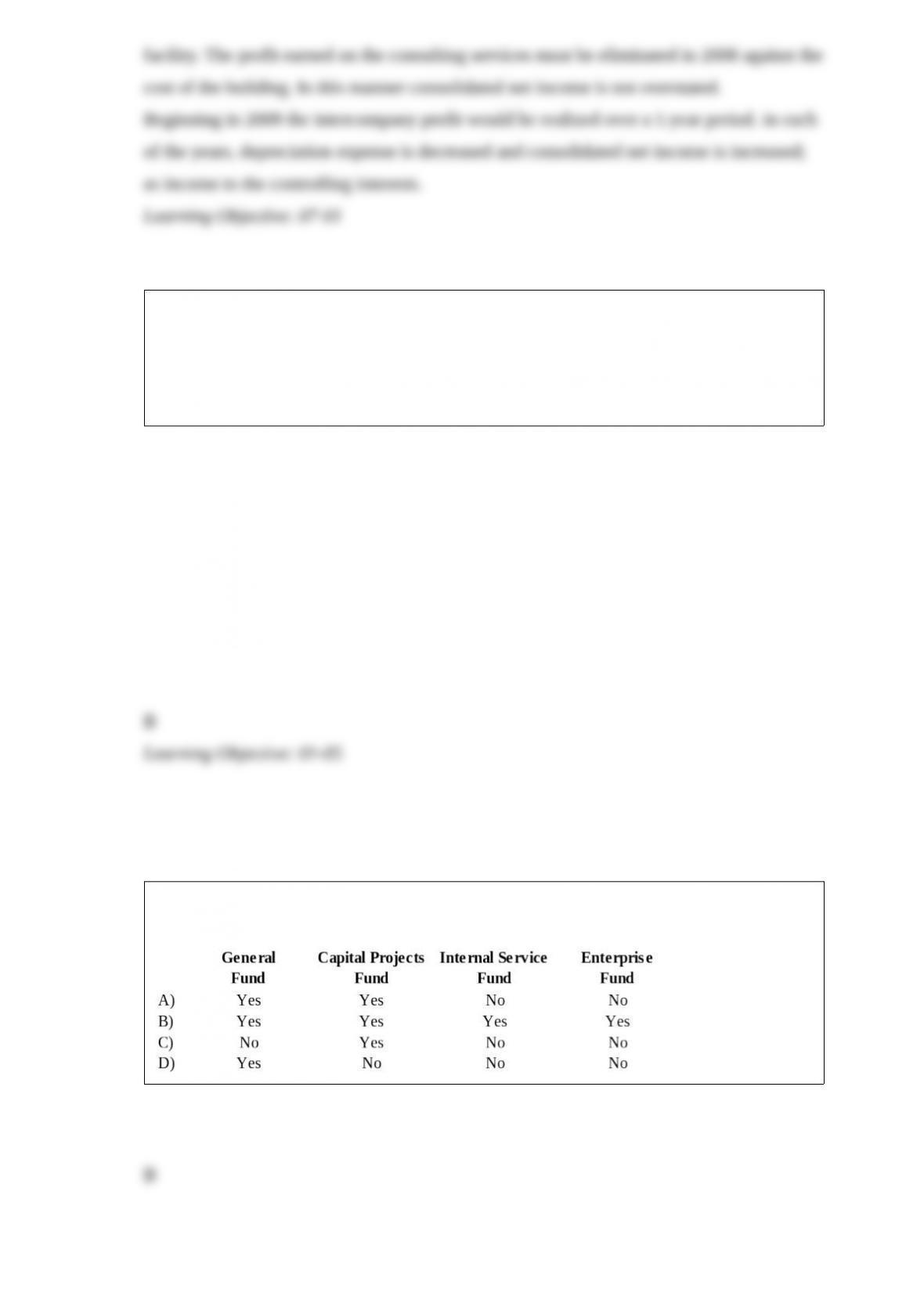

The government-wide financial statements prepared for a municipality should include

assets acquired by the following funds:

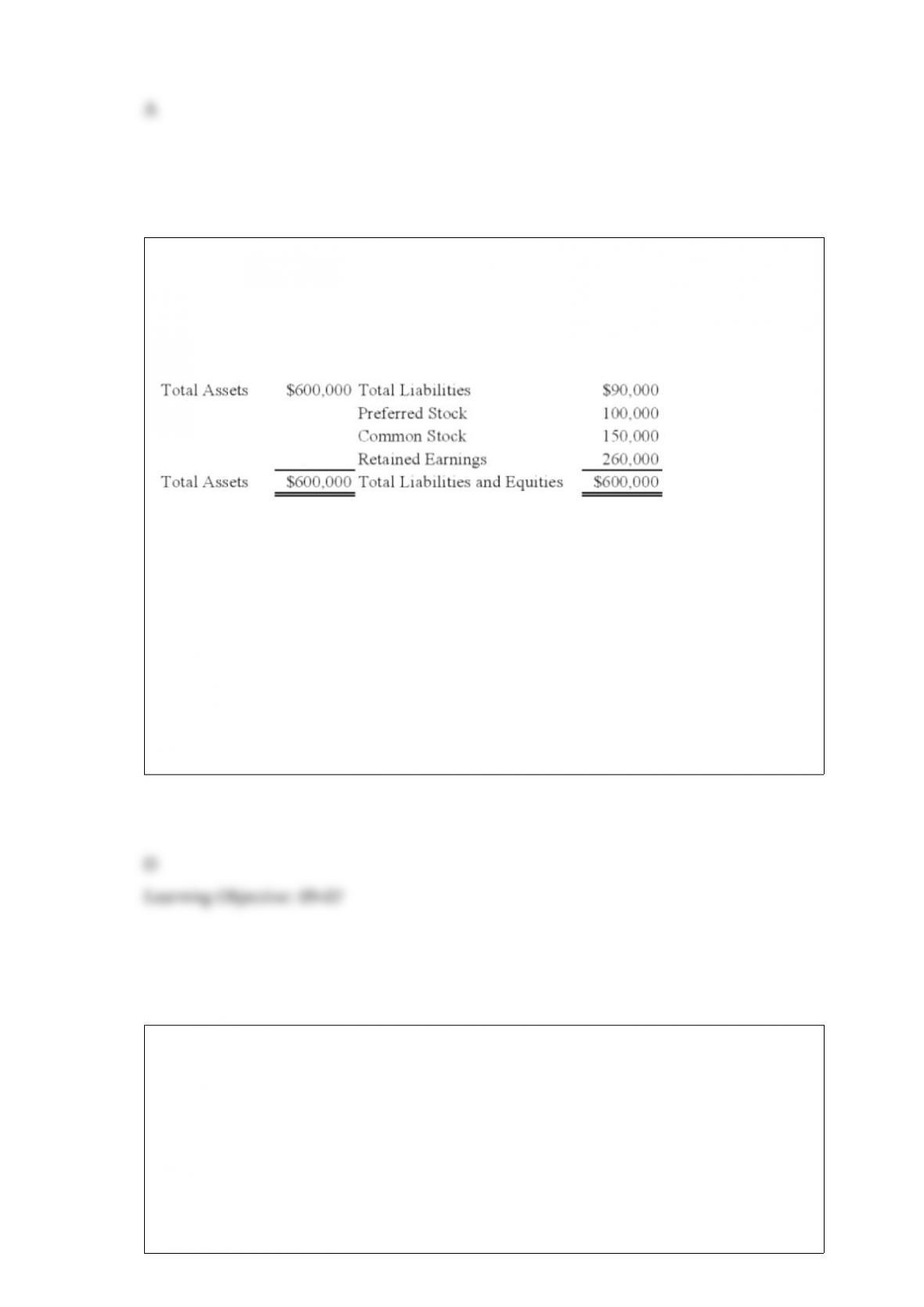

The following condensed balance sheet is presented for the partnership of H, I, and J

who share profits and losses in the ration of 4:3:3, respectively:

Cash $50,000

Other Assets 300,000

Total $350,000

Liabilities $80,000

H, Capital 150,000

I, Capital 70,000

J, Capital 50,000

Total $350,000

The partners agree to liquidate the partnership after selling the other assets.

Refer to the above information. If the other assets are sold for $140,000 and all partners

are personally insolvent, how much should I receive upon liquidation?

A. $0

B. $2,000

C. $6,600

D. $22,000

A stock dividend of 2,000 shares on its $5 par value common stock

The current market price per share of Agro stock on January 1, 20X9, is $15.

Required:

Give the investment elimination entry required to prepare a consolidated balance sheet

at the close of business on January 1, 20X9, for each of the alternative transactions

under consideration by Agro Corporation.

On January 2, 20X2, Kentucky Company acquired 70% of Bluegrass Corporation’s

common stock for $420,000 cash. At the acquisition date, the book values and fair

values of Bluegrass’ assets and liabilities were equal, and the fair value of the

noncontrolling interest was equal to 30% of the total book value of Bluegrass. The

stockholders’ equity accounts of the two companies at the acquisition date are as

follows:

Kentucky Bluegrass

Common Stock ($10 par value) $600,000 $350,000

Additional Paid-In Capital 450,000 50,000

Retained Earnings 250,000 200,000

Total Stockholders’ Equity $1,300,000 $600,000

Noncontrolling interest was assigned income of $15,000 in Kentucky’s consolidated

income statement for 20X2.

Based on the preceding information, what will be the amount of net income reported by

Bluegrass Corporation in 20X2?

A. $45,000

B. $50,000

C. $75,000

D. $105,000

Paco Company acquired 100 percent of the stock of Garland Corp. on December 31,

20X8. The stockholder’s equity section of Garland’s balance sheet at that date is as

follows:

Paco financed the acquisition by using $880,000 cash and giving a note payable for

$400,000. Book value approximated fair value for all of Garland’s assets and liabilities

except for buildings which had a fair value $60,000 more than its book value and a

remaining useful life of 10 years. Any remaining differential was related to goodwill. Paco

has an account payable to Garland in the amount of $30,000.

Required:

1) Present all consolidating entries needed to prepare a consolidated balance sheet

immediately following the acquisition.

2) What additional consolidating entry must be prepared at December 31, 20X9?

The CFO of a “Not-for-Profit” hospital is making a presentation at your college. The

presentation is for Business and Health-Science majors. During the presentation the

CFO mentions assets being reported “above the line.” On the way out your roommate a

health-science major asks, you an accounting major, to explain what the CFO was

referring to. What do you respond?

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Reported as an expenditure of the fund using plant and equipment” describes which

term listed above?

The following condensed balance sheet is presented for the partnership of Dunn, Lott,

and Tyler who share profits and losses in the ratio of 7:2:1, respectively.

Cash $30,000

Other assets 150,000

$180,000

Liabilities $60,000

Dunn, Capital 50,000

Lott, Capital 40,000

Tyler, Capital 30,000

$180,000

The partners agreed that the partnership would be liquidated after selling the other

assets. All partners are personally insolvent. What would each of the partners receive if

the other assets are sold for $70,000?

Dunn Lott Tyler

A. $6,000 $24,000 $22,000

B. $0 $21,000 $19,000

C. $50,000 $40,000 $30,000

D. $0 $20,000 $20,000

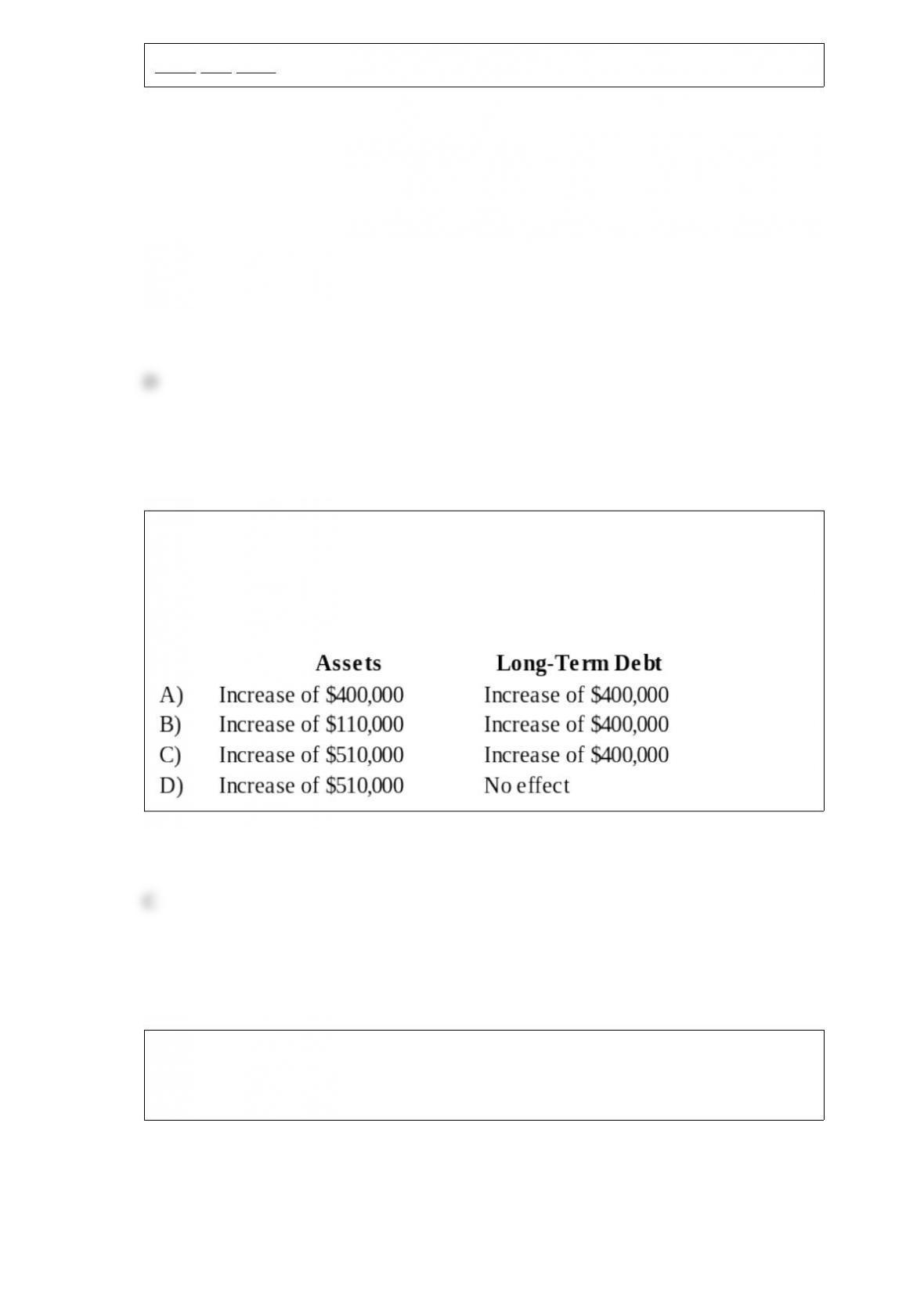

During the fiscal year ended June 30, 20X9, an enterprise fund of St. Cloud acquired

computer equipment costing $110,000 on account and issued $400,000 of long-term

bonds. Revenues of the enterprise fund will be used to repay bond interest and

principal. What effect did these transactions have on St. Cloud’s enterprise fund assets

and long-term debt?

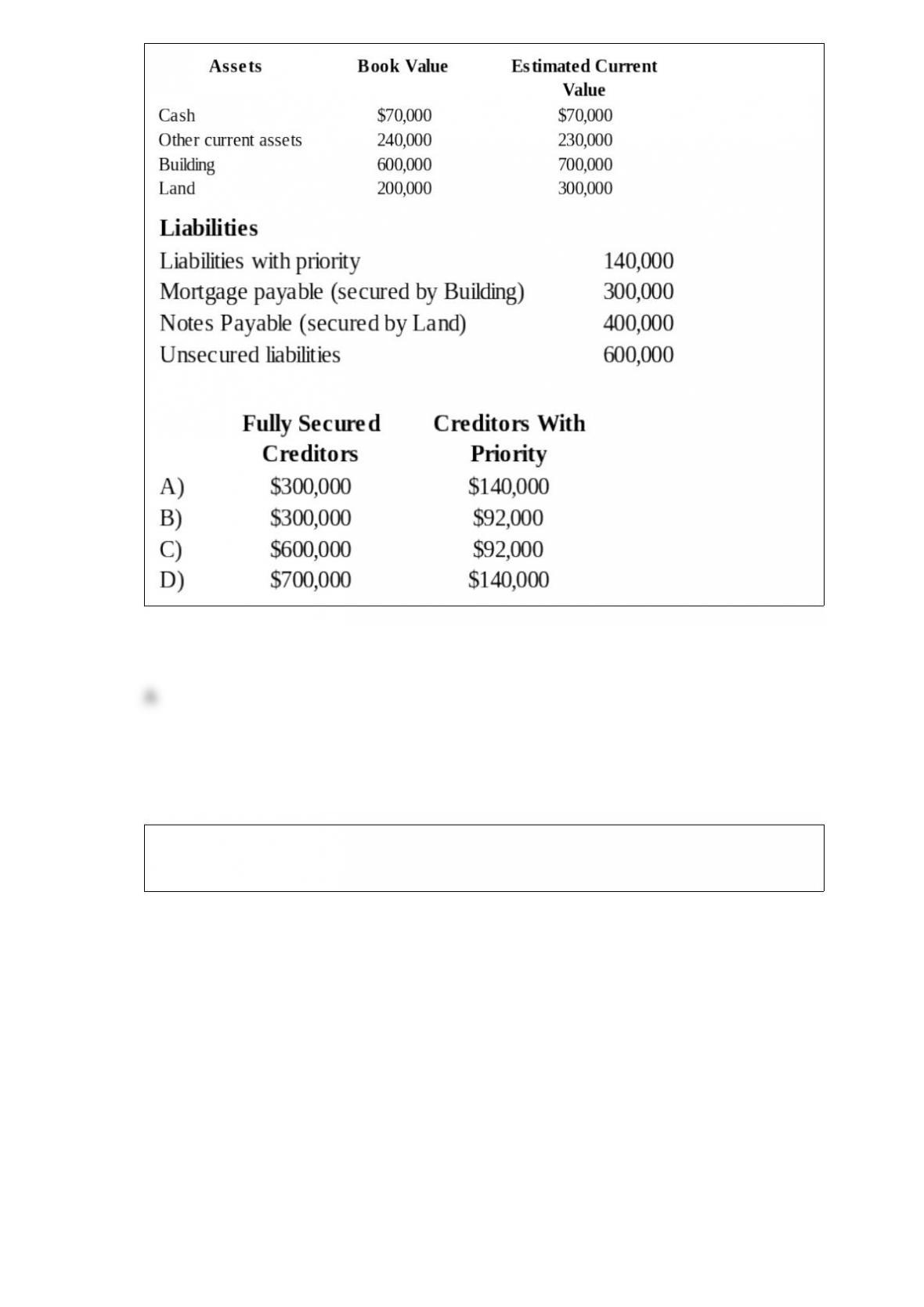

Eagle Company recently petitioned for bankruptcy and is now in the process of

preparing a statement of affairs. The following information has been assembled for this

statement:

What amount will be paid to the fully secured creditors and the creditors with priority?

Boycott Company holds 75 percent ownership of Fred Corporation. The consolidated

balance sheets as of December 31, 20X8, and December 31, 20X9, are as follows:

The 20X9 consolidated income statement contained the following amounts:

Boycott acquired its investment in Fred on January 1, 20X6, for $120,000. At that date,

the fair value of the noncontrolling interest was $40,000, and Fred reported net assets of

$130,000. A total of $20,000 of the differential was assigned to goodwill. The

remainder of the differential was assigned to equipment with a remaining life of 10

years from the date of combination.

Boycott sold $100,000 of bonds on December 31, 20X9, to assist in generating

additional funds. Fred reported net income of $20,000 for 20X9 and paid dividends of

$10,000. Boycott reported 20X9 equity-method net income of $75,000 paid dividends

of $20,000 for the year.

Required:

1) Prepare a worksheet to develop a consolidated statement of cash flows for 20X9

using the indirect method of computing cash flows from operations.

2) Prepare a consolidated statement of cash flows for 20X9.

Siera, Lani, and Cecilia are partners in an equipment leasing business that has not been

able to generate the type of revenue expected by the partners. They share profits and

losses in a ratio of 5:3:2, respectively. They have decided to liquidate the business and

have sold all the assets except for one piece of heavy machinery. All the partners are

personally insolvent. The machinery has a book value of $120,000, and the partners

have capital balances as follows:

Siera, Capita $40,000

Lani, Capital $20,000

Cecilia, Capital $30,000

Each of the following is an independent case.

Refer to the information given above. What amount of cash will each partner receive as

a liquidating distribution if the machinery is sold for $51,000?

Siera Lani Cecilia

A. $5,000 $0 $16,000

B. $5,000 $700 $16,000

C. $5,500 $0 $16,200

D. $5,500 $700 $16,200