ABC Corporation owns 75 percent of XYZ Company’s voting shares. During 20X8,

ABC produced 50,000 chairs at a cost of $79 each and sold 35,000 chairs to XYZ for

$90 each. XYZ sold 18,000 of the chairs to unaffiliated companies for $117 each prior

to December 31, 20X8, and sold the remainder in early 20X9 to unaffiliated companies

for $130 each. Both companies use perpetual inventory systems.

Based on the information given above, what amount of cost of goods sold did ABC

record in 20X8?

A. $2,765,000

B. $1,620,000

C. $1,422,000

D. $2,963,000

South Company is a subsidiary of North Company and is located in Malaysia, where

the currency is the ringgit. Data on South’s inventory and purchases are as follows:

Inventory, January 1, 20X4 30,000 ringgits

Purchases during 20X4 80,000 ringgits

Inventory, December 31, 20X4 20,000 ringgits

The beginning inventory was acquired during the fourth quarter of 20X3, and the

ending inventory was acquired during the fourth quarter of 20X4. Purchases were made

evenly during 20X4. Exchange rates were as follows:

Fourth quarter of 20X3 1 ringgit = $0.319

January 1, 20X4 1 ringgit = $0.318

Average during 20X4 1 ringgit = $0.315

Fourth quarter of 20X4 1 ringgit = $0.313

December 31, 20X4 1 ringgit = $0.31

Based on the preceding information and assuming the U.S. dollar is the functional

currency, what is the amount of South’s costs of goods sold remeasured in U.S. dollars?

A. $28,480

B. $28,510

C. $28, 540

D. $28,570

If a company changes the method it uses to compute the allowance for uncollectible

accounts receivable because more recent information has become available, how is this

change in method is accounted for?

A. The change is only reported in the current period in which the change is made

B. The change is reported in all future periods affected by the change

C. Previously issued financial statements are not adjusted by the change

D. All of the above are correct ways to account for the change

In a statement of realization and liquidation, unusual revenue items are reported under:

A. assets.

B. extraordinary items.

C. supplementary items.

D. These are never reported.

Blue Ridge Township uses the consumption method of accounting for its inventory of

supplies. On the December 31, 20X7 balance sheet for the general fund, the township

reported $10,000 of supplies inventory. During 20X8, expenditures for supplies

amounted to $40,000, and, at December 31, 20X8, unused supplies totaled $7,000. In

the adjusting entry for supplies at December 31, 20X8,

A. Expenditures should be credited for $3,000.

B. Expenditures should be debited for $3,000.

C. Fund Balance—Nonspendable should be debited for $7,000.

D. Fund Balance—Nonspendable should be credited for $7,000.

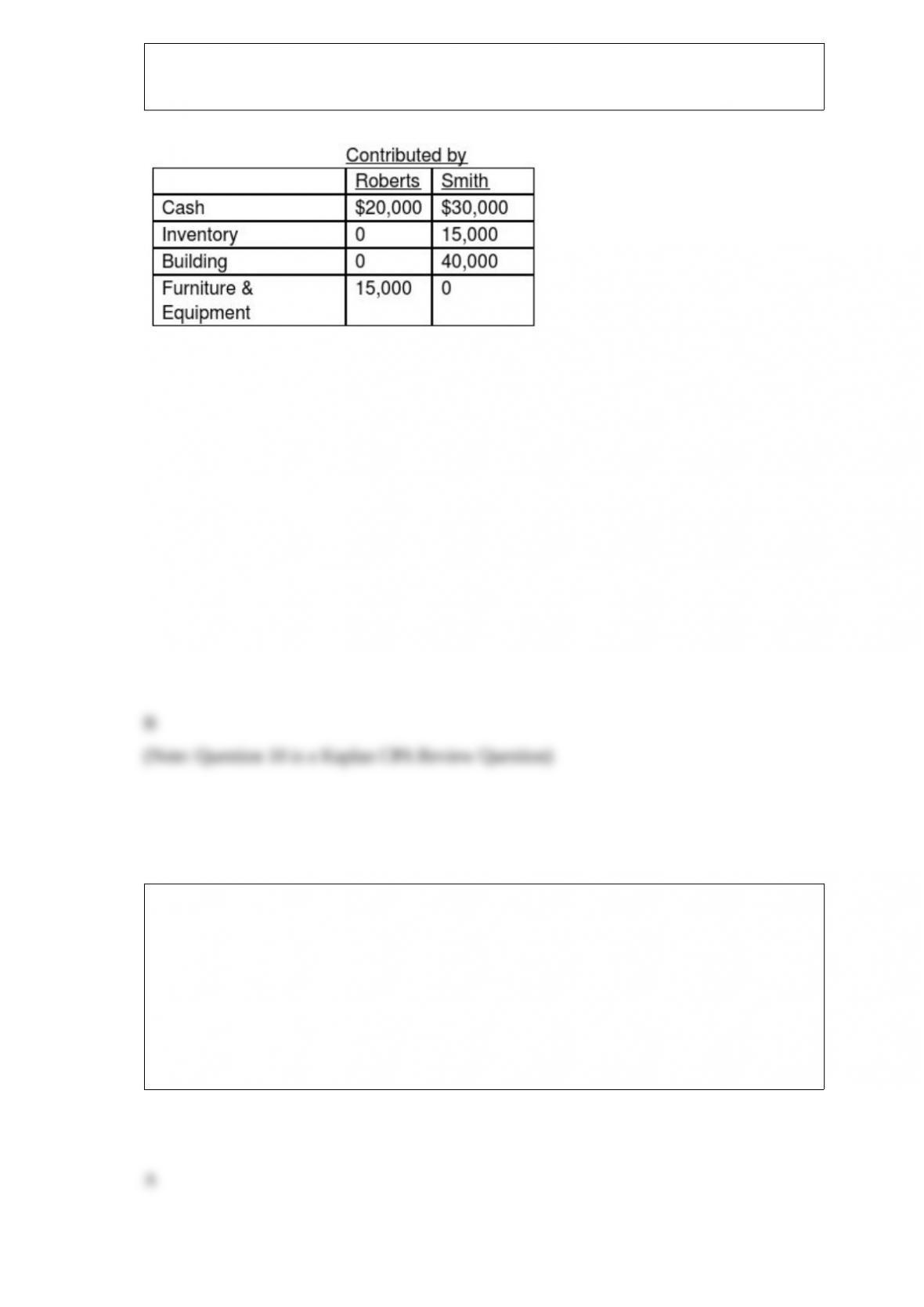

Roberts and Smith drafted a partnership agreement that lists the following assets

contributed at the partnership’s formation:

The building is subject to a mortgage of $10,000, which the partnership has assumed. The

partnership agreement also specifies that profits and losses are to be distributed evenly.

What amounts should be recorded as capital for Roberts and Smith at the formation of the

partnership?

Roberts Smith

A. $35,000 $85,000

B. $35,000 $75,000

C. $55,000 $55,000

D. $60,000 $60,000

Bridger Hospital, which is operated by a religious organization, provides charity care

for the indigent living in the region served by the hospital. How should Bridger report

the amount of its charity care on its financial statements?

A. In the notes to the financial statements only.

B. As unrestricted revenues on the statement of operations.

C. As net patient service revenue and as an expense, equal to the net patient service

revenue, on the statement of operations.

D. As temporarily restricted revenue on the statement of operations.

Which of the following statements best describes accounting for a partnership?

A. A partnership may be a profit or a nonprofit entity.

B. A partnership may use federal income tax rules to account for transactions in their

journals and ledger accounts.

C. A partnership’s equity section contains both capital and retained earnings accounts.

D. A partnership may only distribute money through a dividend payment.

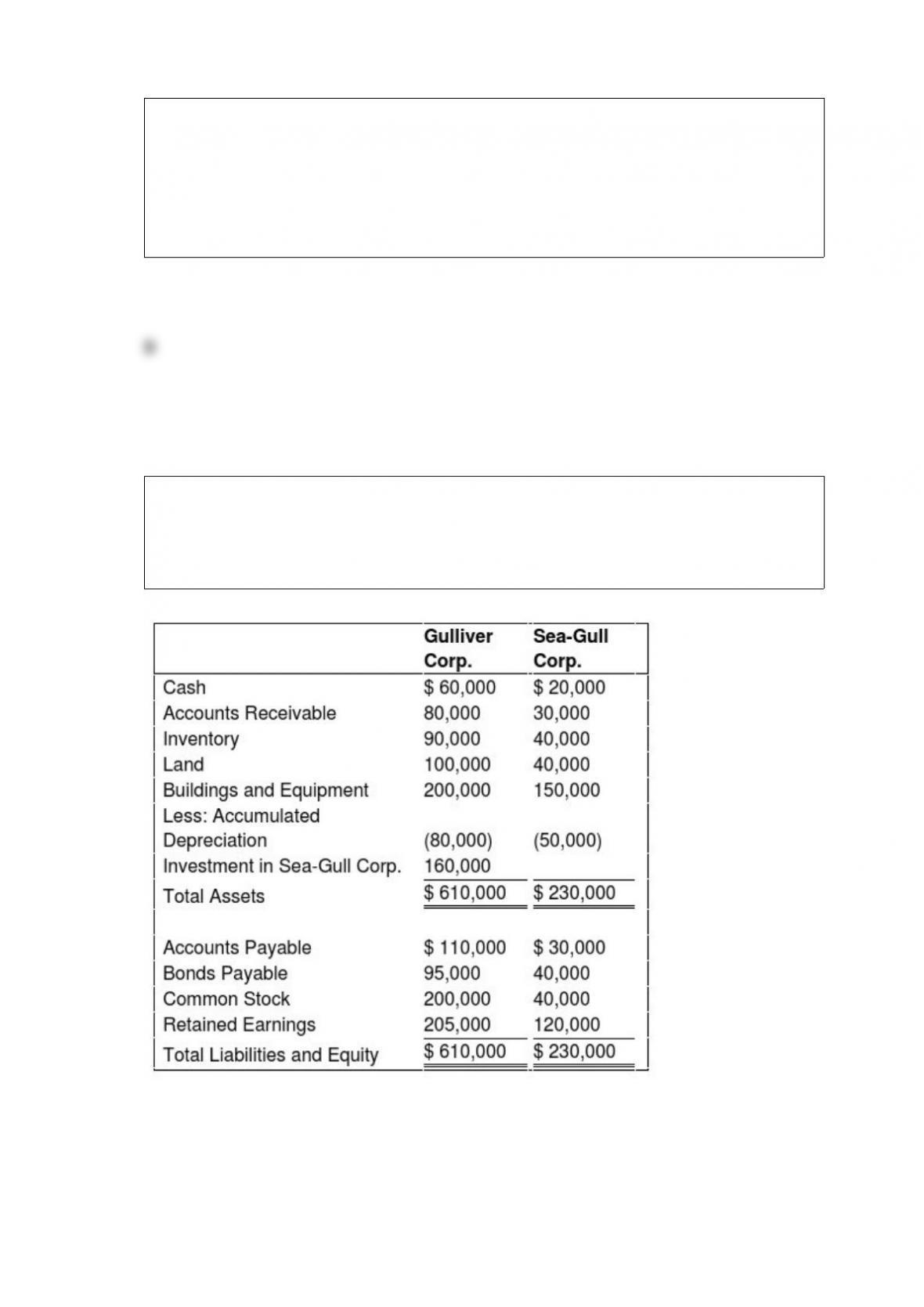

On January 1, 20X9, Gulliver Corporation acquired 80 percent of Sea-Gull Company’s

common stock for $160,000 cash. The fair value of the noncontrolling interest at that

date was determined to be $40,000. Data from the balance sheets of the two companies

included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Sea-Gull’s net assets and

liabilities approximated fair value except for inventory, which had a fair value of $45,000,

and land, which had a fair value of $60,000.

Based on the preceding information, what amount will be reported as total stockholders’

equity in the consolidated balance sheet prepared immediately after the business

combination?

A. $445,000

B. $205,000

C. $565,000

D. $550,000

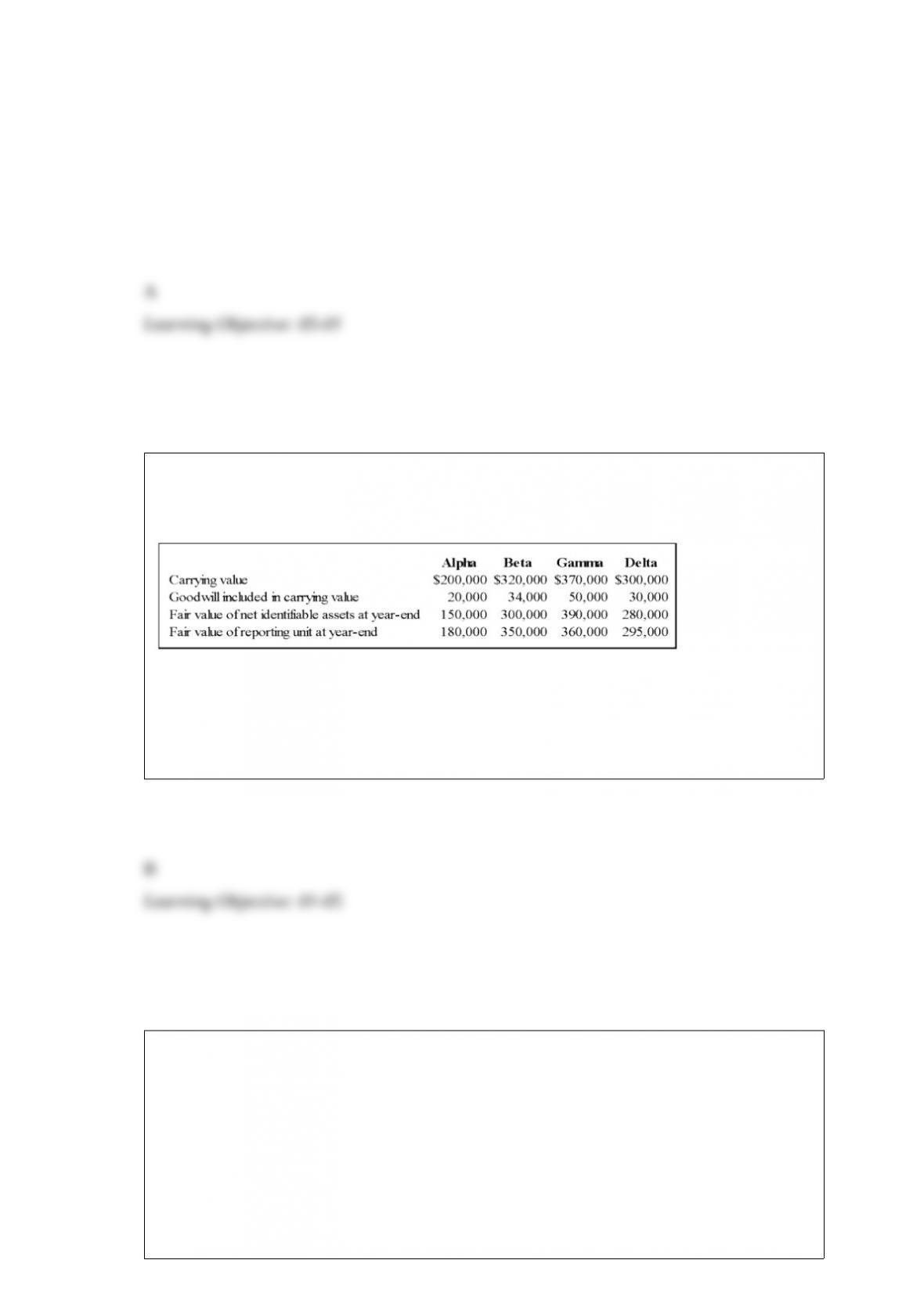

Pursuing an inorganic growth strategy, Wilson Company acquired Venus Company’s net

assets and assigned them to four separate reporting divisions. Wilson assigned total

goodwill of $134,000 to the four reporting divisions as given below:

Based on the preceding information, for Delta:

A. no goodwill should be reported at year-end.

B. goodwill impairment of $15,000 should be recognized at year-end.

C. goodwill impairment of $20,000 should be recognized at year-end.

D. goodwill of $30,000 should be reported at year-end.

Hilldale Corporation purchased land on January 1, 20X0, for $60,000. On August 7,

20X2, it sold the land to its subsidiary, Allen Corporation, for $35,000. Hilldale owns

60 percent of Allen’s voting shares

Based on the preceding information, what will be the worksheet consolidation entry to

remove the effects of the intercompany sale of land in preparing the consolidated

financial statements for 20X3?

A. Investment in Allen 25,000

Land 25,000

B. Land 15,000

Investment in Allen 15,000

C. Investment in Allen 15,000

Land 15,000

D. Land 25,000

Investment in Allen 25,000

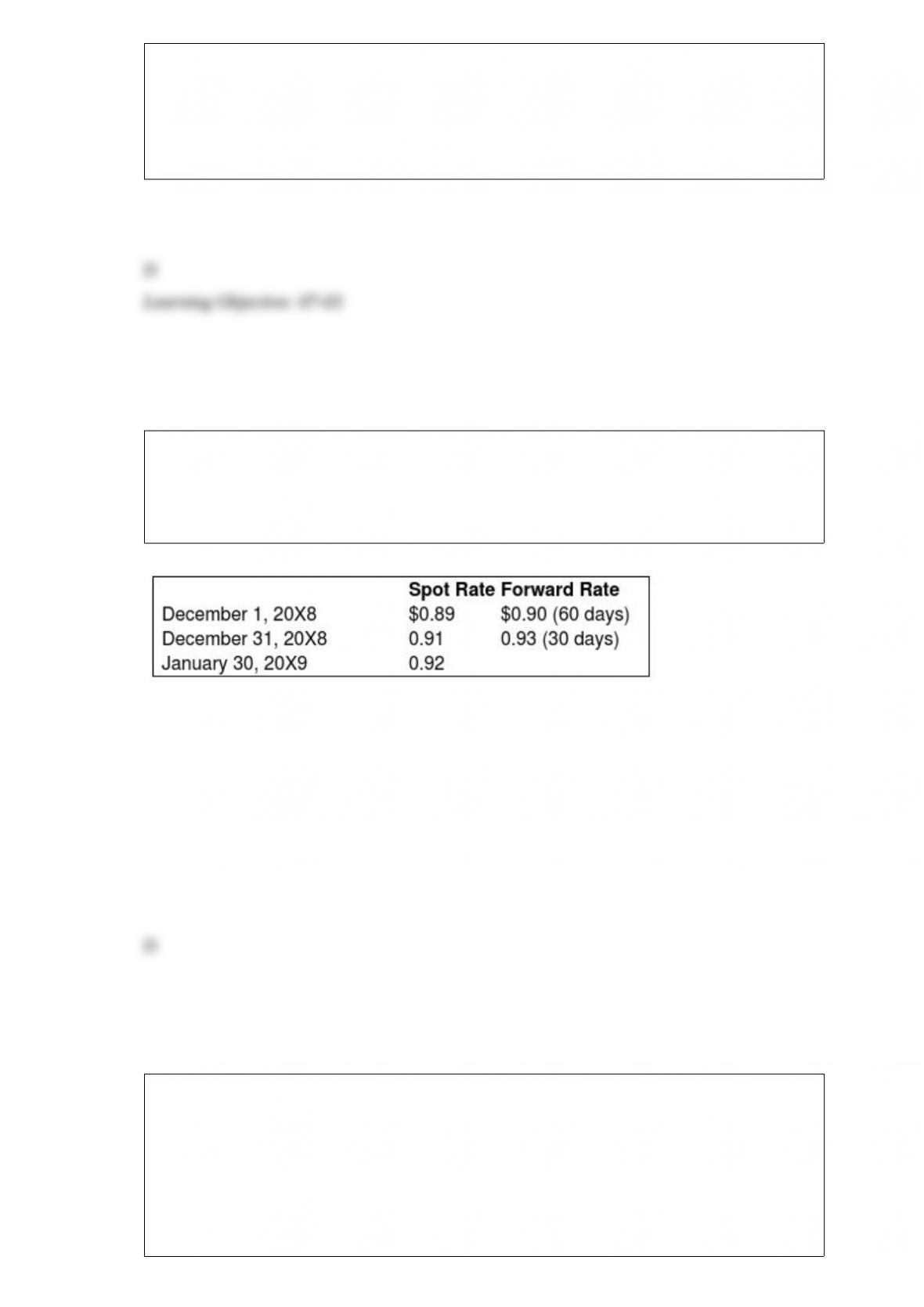

Taste Bits Inc. purchased chocolates from Switzerland for 200,000 Swiss francs (SFr)

on December 1, 20X8. Payment is due on January 30, 20X9. On December 1, 20X8, the

company also entered into a 60-day forward contract to purchase 100,000 Swiss francs.

The forward contract is not designated as a hedge. The rates were as follows:

Based on the preceding information, the entries on January 30, 20X9, include a:

A. Debit to Dollars Payable to Exchange Broker, $184,000.

B. Credit to Foreign Currency Transaction Gain, $4,000.

C. Credit to Foreign Currency Receivable from Exchange Broker, $180,000.

D. Debit to Foreign Currency Units (SFr), $184,000.

The term “restricted” as used in university accounting refers to a constraint on the use

of funds which has been:

I. internally imposed.

II. externally imposed.

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Rohan Corporation holds assets with a fair value of $150,000 and a book value of

$125,000 and liabilities with a book value and fair value of $50,000. What balance will

be assigned to the noncontrolling interest in the consolidated balance sheet if Helms

Company pays $90,000 to acquire 75 percent ownership in Rohan and goodwill of

$20,000 is reported?

A. $50,000

B. $30,000

C. $40,000

D. $20,000

Mortar Corporation acquired 80 percent of Granite Corporation’s voting common stock

on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite

for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment

is expected to have a 10-year useful life and no salvage value. Both companies

depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X9 consolidated

financial statements, equipment will be:

A. debited for $1,000.

B. debited for $10,000.

C. credited for $15,000.

D. debited for $25,000.

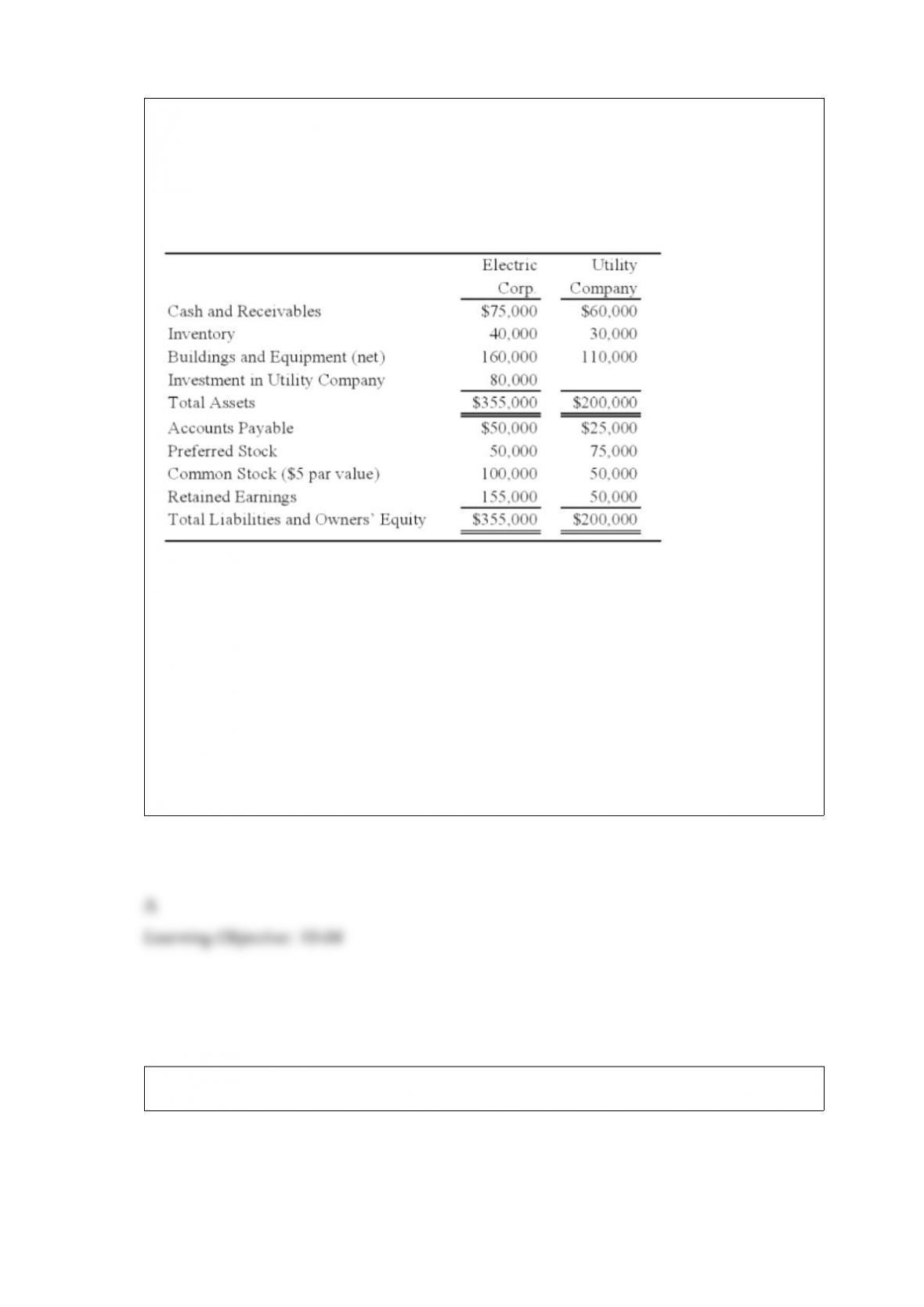

Electric Corporation holds 80 percent of Utility Company’s voting common shares,

acquired at book values, but none of its preferred shares. At the date of acquisition, the

fair value of the noncontrolling interest was equal to 20 percent of the book value of

Utility Company. Summary balance sheets for the companies on December 31, 20X8,

are as follows:

Neither of the preferred issues is convertible. Electric’s preferred pays a 8 percent

annual dividend, and Utility’s preferred pays a 12 percent dividend. Utility reported net

income of $30,000 and paid a total of $10,000 of dividends in 20X8. Electric reported

income from its separate operations of $70,000 and paid total dividends of $25,000 in

20X8.

Based on the preceding information, what is the amount of earnings available to

common shareholders reported in the consolidated financial statements for the year?

A. $101,800

B. $104,500

C. $112,300

D. $115,000

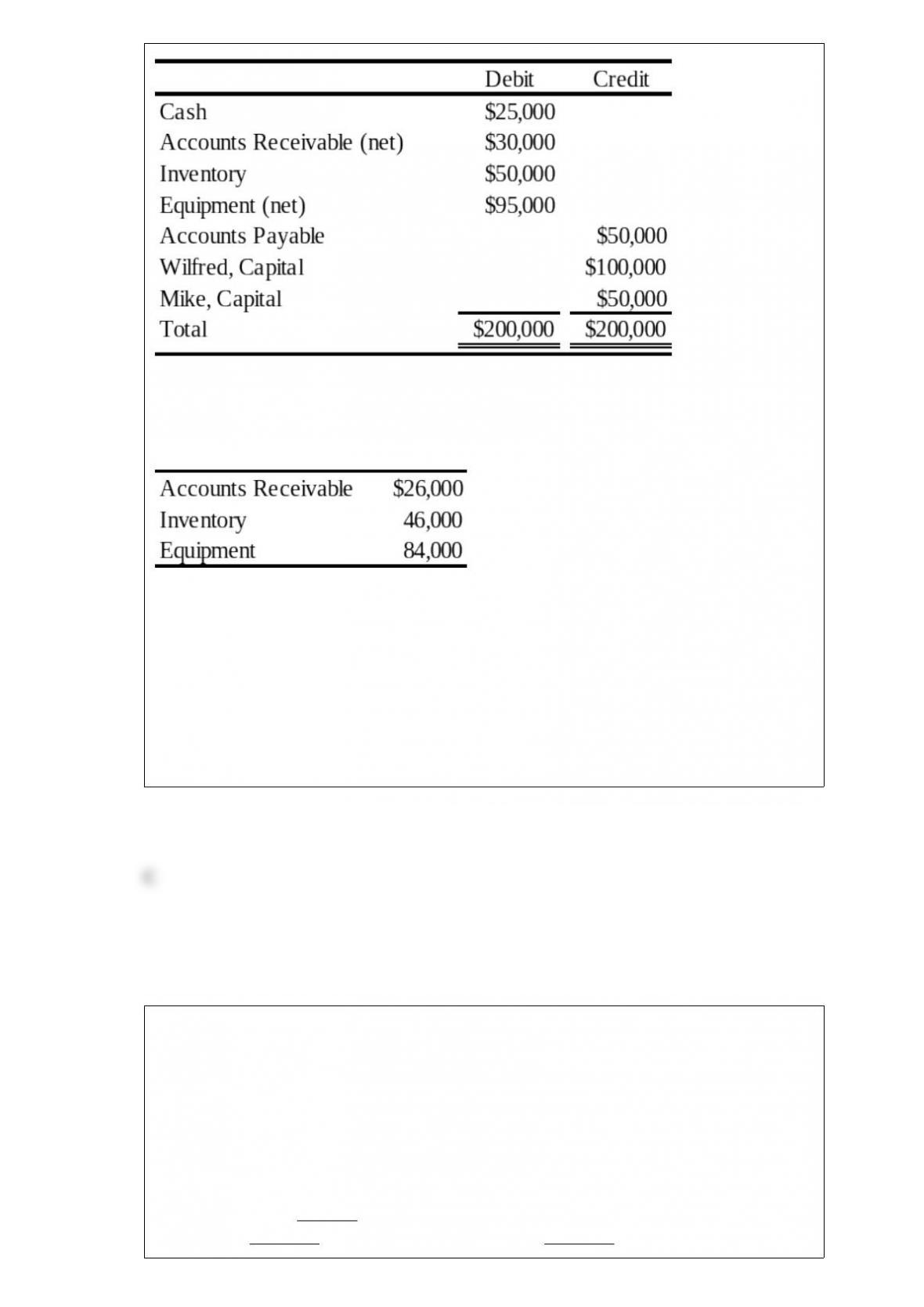

The trial balance of WM Partnership is as follows:

Wilfred and Mike decide to incorporate their partnership. The partnership’s books will

be closed, and new books will be used for W & M Corporation. The following

additional information is available:

1) The estimated fair values of the assets follow:

2)All assets and liabilities are transferred to the corporation.

3) The common stock is $10 par. Wilfred and Mike receive a total of 10,000 shares.

4) The partners share profits and losses in the ratio 7:3.

Based on the preceding information, the journal entry on the partnership’s books to

record distribution of stock to prior partners will include a debit to Wilfred, Capital for:

A. $140,000.

B. $91,700.

C. $86,700.

D. $126,700.

Wally Corporation acquired 70 percent of the common shares and 60 percent of the

preferred shares of Safety Corporation at underlying book value on January 1, 20X6. At

that date, the fair value of the noncontrolling interest in Safety’s common stock was

equal to 30 percent of the book value of its common stock. Safety’s balance sheet at the

time of acquisition contained the following balances:

Assets $700,000 Liabilities $110,000

Preferred Stock 100,000

Common Stock 200,000

Retained Earnings 290,000

Total Assets $700,000 Total Liabilities and Equities $700,000

The preferred shares are cumulative and have an 8 percent annual dividend rate and are

three years in arrears on January 1, 20X6. All of the $10 par value preferred shares are

callable at $12 per share. During 20X6, Safety reported net income of $80,000 and paid

no dividends.

Based on the preceding information, what is the portion of Safety’s retained earnings

assignable to its preferred shareholders on January 1, 20X6?

A. $52,000

B. $44,000

C. $36,000

D. $28,000

If Push Company owned 51 percent of the outstanding common stock of Shove

Company, which reporting method would be appropriate?

A. Cost method

B. Consolidation

C. Equity method

D. Merger method

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Customary Review

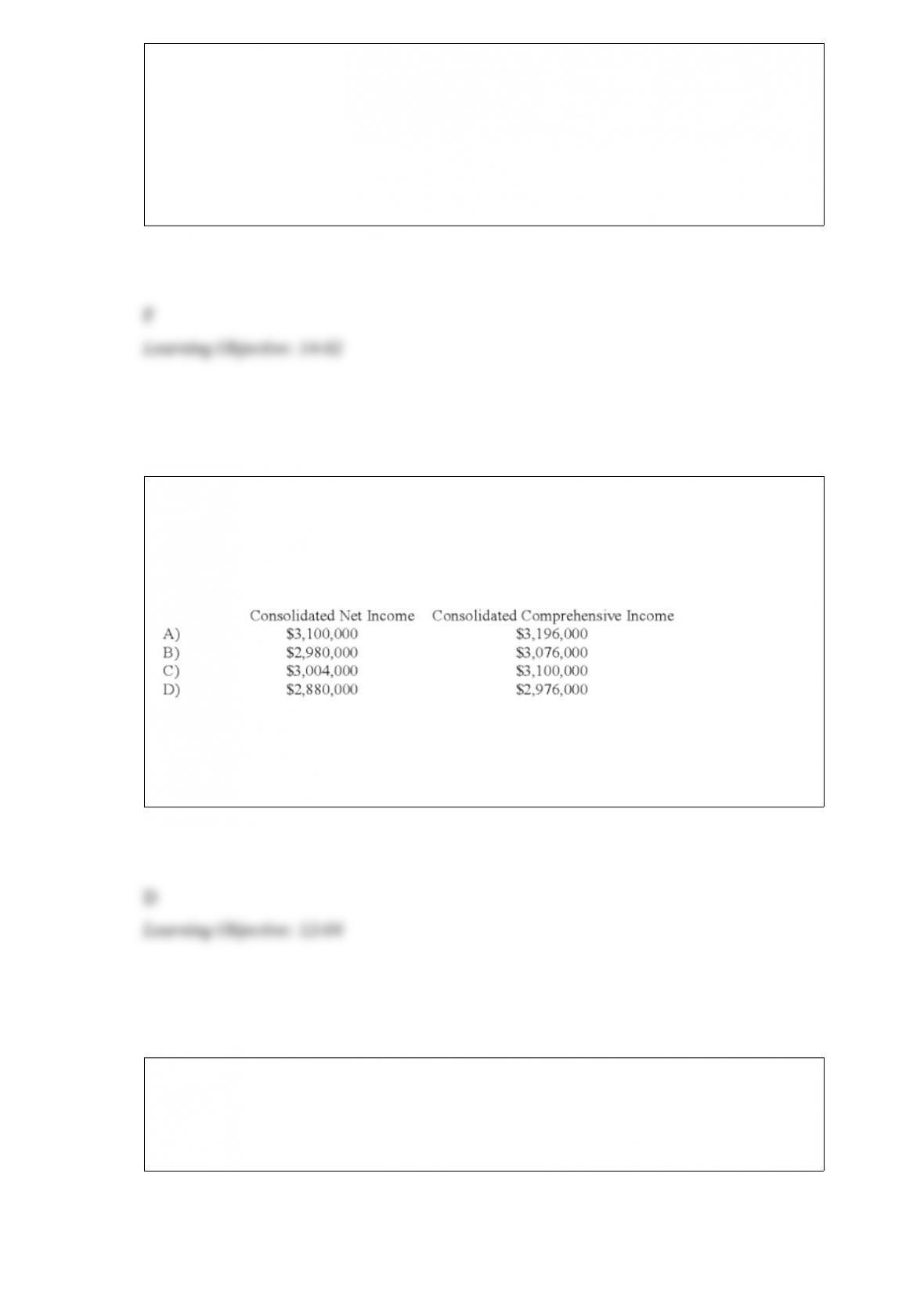

Seattle, Inc. owns an 80 percent interest in a Portuguese subsidiary. For 20X8, Seattle

reported income from operations of $2.0 million. The Portuguese company’s income

from operations, after foreign currency translation, was $1.1 million. The foreign

currency translation adjustment was $120,000 (credit). Consolidated net income and

consolidated comprehensive income for the year are:

A. Option A

B. Option B

C. Option C

D. Option D

Catalyst Corporation acquired 90 percent of Trigger Corporation’s common stock on

September 30, 20X8 for $225,000. At that date, the fair value of the noncontrolling

interest was $25,000. On January 1, 20X8, Trigger reported the following stockholders’

equity balances:

Trigger reported net income of $80,000 in 20X8, earned uniformly throughout the year,

and declared and paid dividends of $10,000 on June 30 and $30,000 on December 31,

20X8. Catalyst reported retained earnings of $250,000 on January 1, 20X8, and had

20X8 income of $120,000 from its separate operations. Catalyst paid dividends of

$50,000 on December 31, 20X8. Catalyst accounts for its investment in Trigger

Corporation using the fully adjusted equity method.

Based on the information provided, what is the consolidated net income reported for the

year 20X8?

A. $120,000

B. $138,000

C. $140,000

D. $192,000

The general fund of Wold Township ordered office furniture for the mayor’s office on

August 1, 20X8. The office furniture was estimated to cost $12,000. The office

furniture was received on September 1, 20X8, with the actual cost being $11,800.

Which of the following accounts decreased on September 1, 20X8?

A. Encumbrances only.

B. Expenditures only.

C. Encumbrances and Budgetary Fund Balance—Assigned for Encumbrances.

D. Expenditures and Budgetary Fund Balance—Assigned for Encumbrances.

Which organization has the authority to establish generally accepted accounting

principles for state and local government entities?

A. The National Council on Governmental Accounting

B. The Governmental Accounting Standards Board

C. The Financial Accounting Standards Board

D. The Municipal Officers Finance Organization

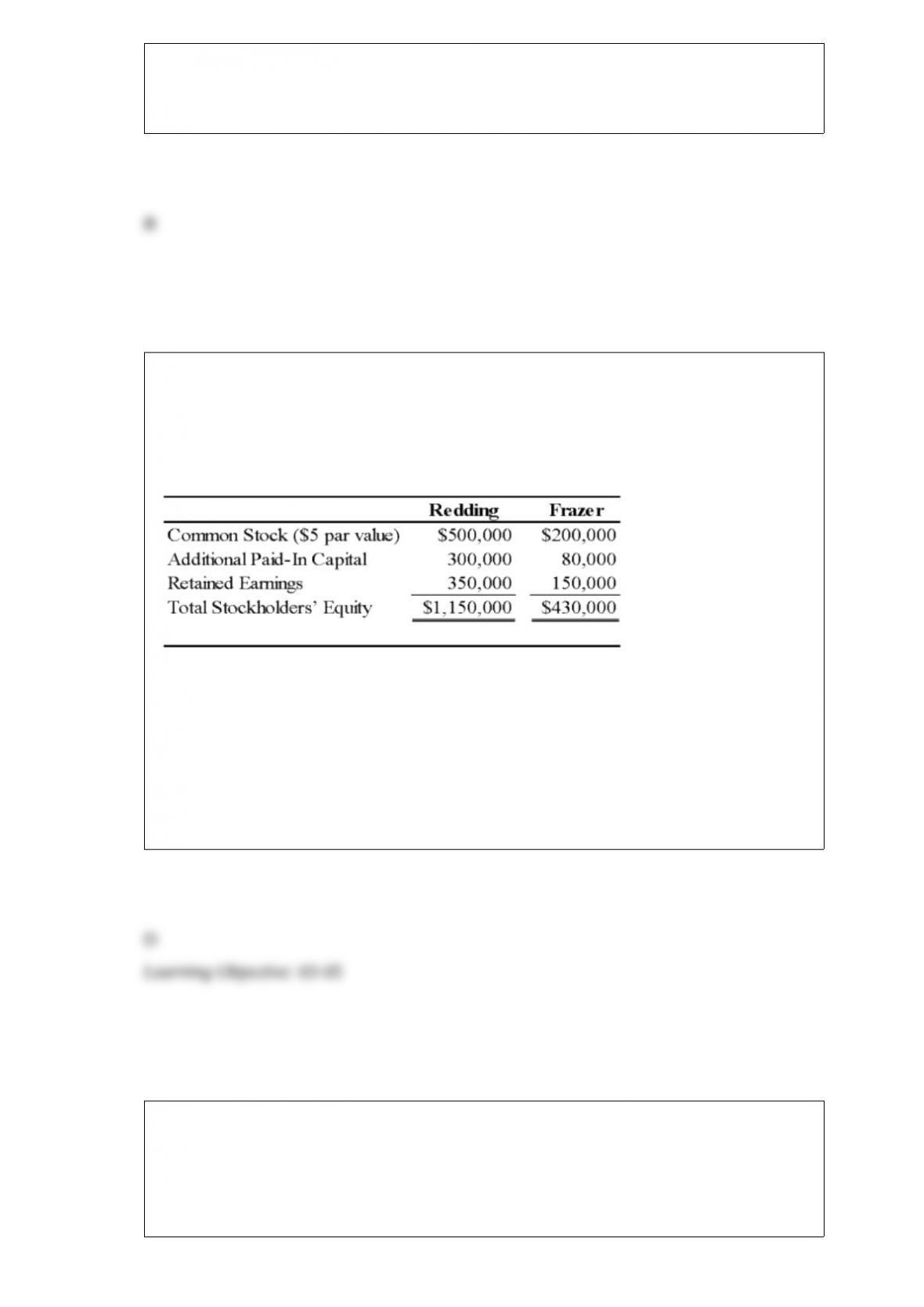

On January 3, 20X9, Redding Company acquired 80 percent of Frazer Corporation’s

common stock for $344,000 in cash. At the acquisition date, the book values and fair

values of Frazer’s assets and liabilities were equal, and the fair value of the

noncontrolling interest was equal to 20 percent of the total book value of Frazer. The

stockholders’ equity accounts of the two companies at the acquisition date are:

Noncontrolling interest was assigned income of $11,000 in Redding’s consolidated

income statement for 20X9.

Based on the preceding information, what is the total stockholders’ equity in the

consolidated balance sheet as of January 3, 20X9?

A. $1,580,000

B. $1,064,000

C. $1,150,000

D. $1,236,000

Myway Company sold equipment to a Canadian company for 100,000 Canadian dollars

(C$) on January 1, 20X9 with settlement to be in 60 days. On the same date, Myway

entered into a 60-day forward contract to sell 100,000 Canadian dollars at a forward

rate of 1 C$ = $.94 in order to manage its exposed foreign currency receivable. The

forward contract is not designated as a hedge. The spot rates were:

Based on the preceding information, had Myway not used the forward exchange

contract, net income for the year would have:

A. increased by $1,000.

B. increased by $500.

C. decreased by $1,000.

D. decreased by $1,500.

According to the latest GASB exposure draft, which of the following is the only

governmental fund type that may report an unassigned fund balance?

A. General fund

B. Special revenue fund

C. Capital projects fund

D. Permanent fund

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, what amount of retained earnings will be reported

in the consolidated balance sheet prepared immediately after the business combination?

A. $200,000

B. $212,000

C. $350,000

D. $488,000

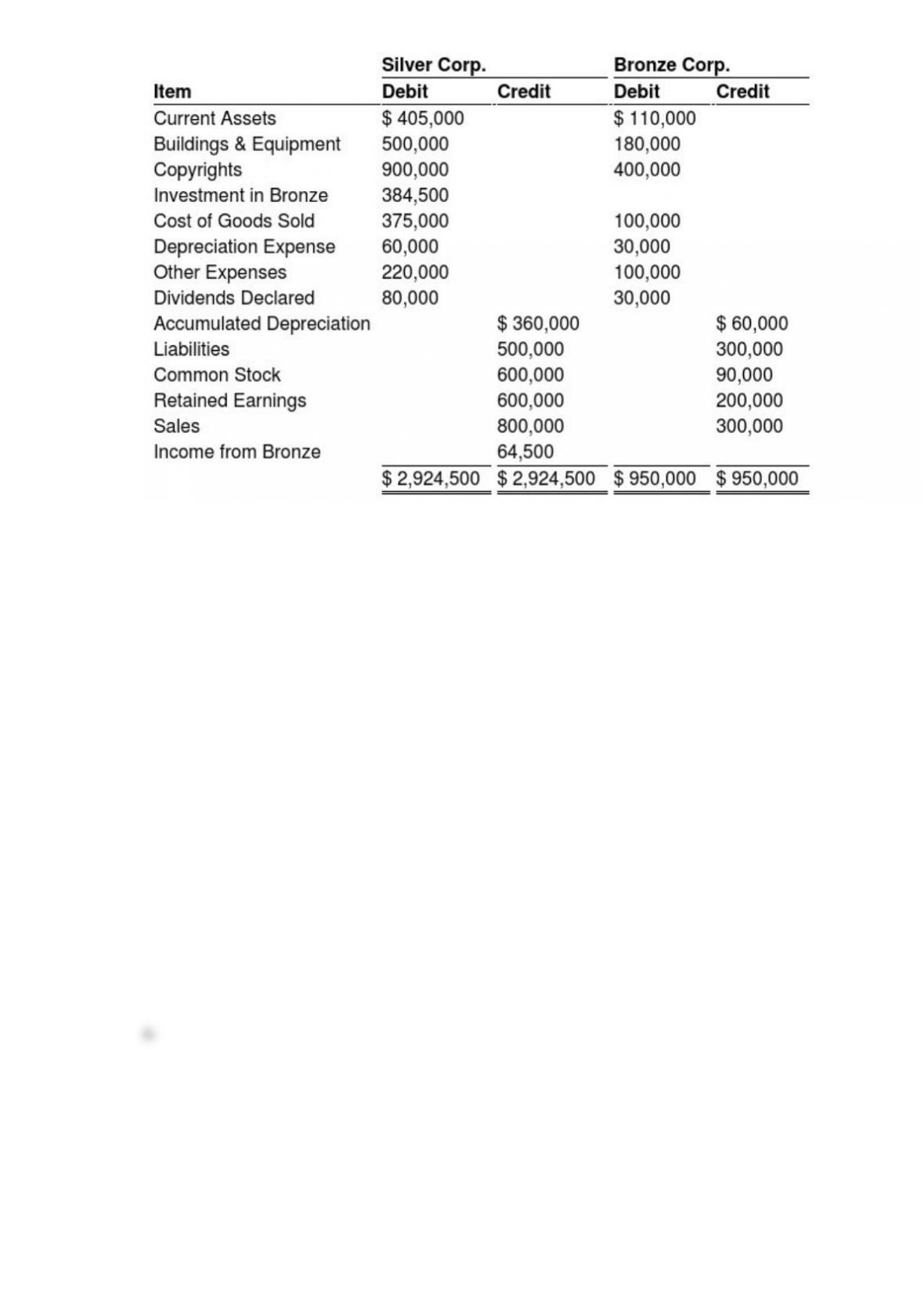

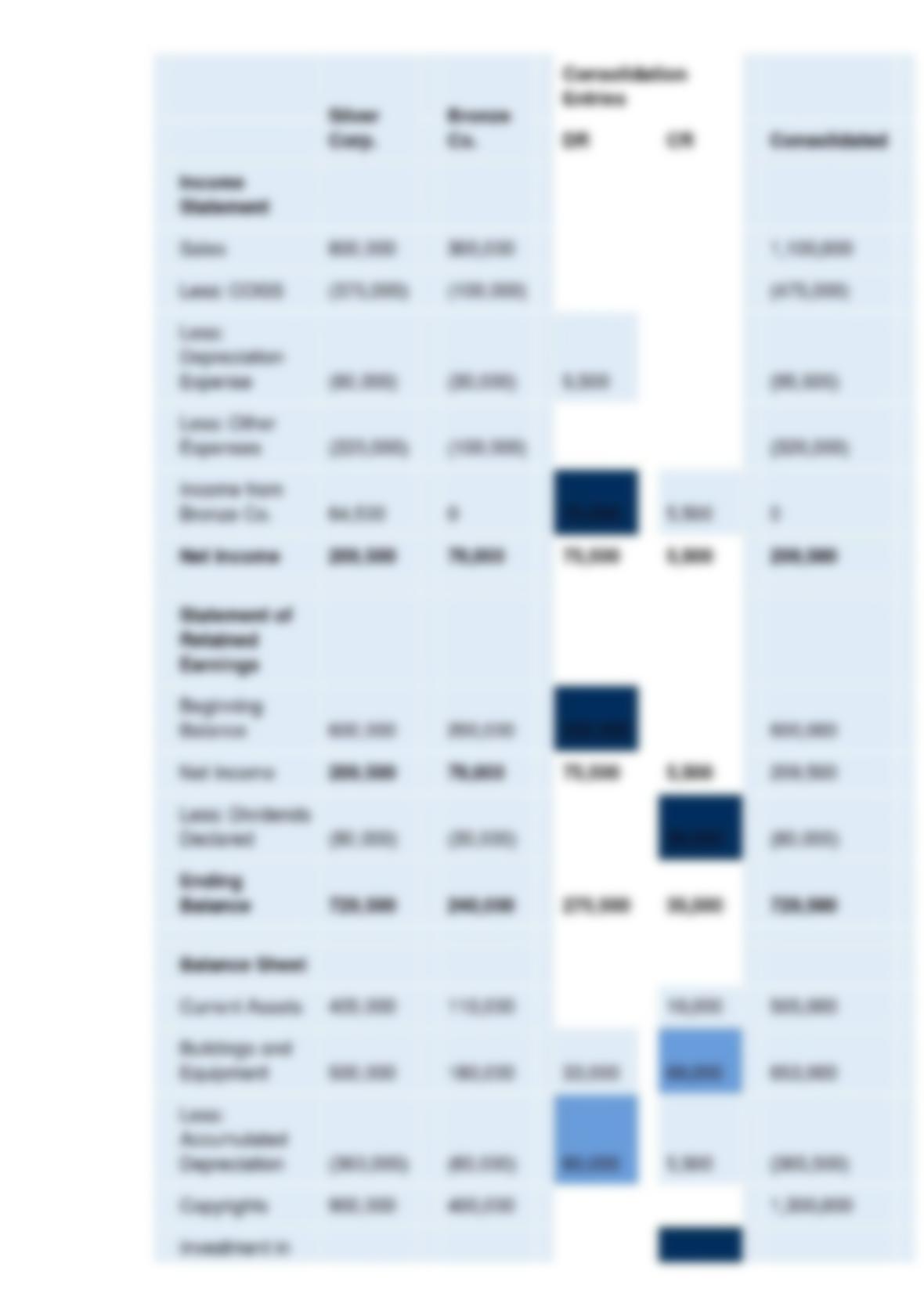

Silver Corporation acquired 100 percent of Bronze Company on January 1, 20X5, for

$350,000. Following are selected account balances from Silver and Bronze Corporation

as of December 31, 20X5:

Additional Information:

1) On January 1, 20X5 the fair market value of Bronze’s assets equaled their book value

with the exception of Plant Assets (with an estimated economic life of 6 years) which had

a fair market value in excess in Bronze’s depreciable assets of $33,000.

2) Silver used the equity-method in accounting for its investment in Bronze.

3) Detailed analysis of receivables and payables showed that Bronze owed Silver $10,000

on December 31, 20X5.

Required:

a. Give all journal entries recorded by Silver with regard to its investment in Bronze during

20X5.

b. Give all consolidating entries needed to prepare a full set of consolidated financial

statements for 20X5.

c. Prepare a three-part consolidation worksheet as of December 31, 20X5.

The general fund of Battle Creek budgeted a transfer to its capital projects fund for

$110,000 to be used in operations during the year ended June 20, 20X9. On September

15, 20X8, the general fund transferred $110,000 to the capital projects fund. What

account should be debited in the general fund on September 15 to record this transfer?

A. Appropriations

B. Expenditures

C. Budgetary Fund Balance—Assigned For Encumbrances

D. Other Financing Uses—Transfer Out to Capital Projects Fund

_____ have liens, or security interests, on specific assets.

A. Secured creditors

B. Creditors with priority

C. Unsecured creditors

D. Assured creditors

Based on the information provided, what is the balance of Ceafoam’s investment in

Trump Corporation as of December 31, 20X4?

A. $360,000

B. $380,000

C. $388,000

D. $395,000

A state government collected income taxes of $8,000,000 for the benefit of one of its

cities that imposes an income tax on its residents. The state remitted these collections

periodically to the city. The state should account for the $8,000,000 in the

A. General fund.

B. Agency funds.

C. Internal service funds.

D. Special assessment funds.

Company Pea owns 90 percent of Company Essone which in turn owns 80 percent of

Company Esstwo. Company Esstwo owns 100 percent of Company Essthree.

Consolidated financial statements should be prepared to report the financial status and

results of operations for:

A. Pea.

B. Pea plus Essone.

C. Pea plus Essone plus Esstwo.

D. Pea plus Essone plus Esstwo plus Essthree.