Chapter 16 – Partnerships: Liquidation

16–21

E16-8 (continued):

Based on practical approach:

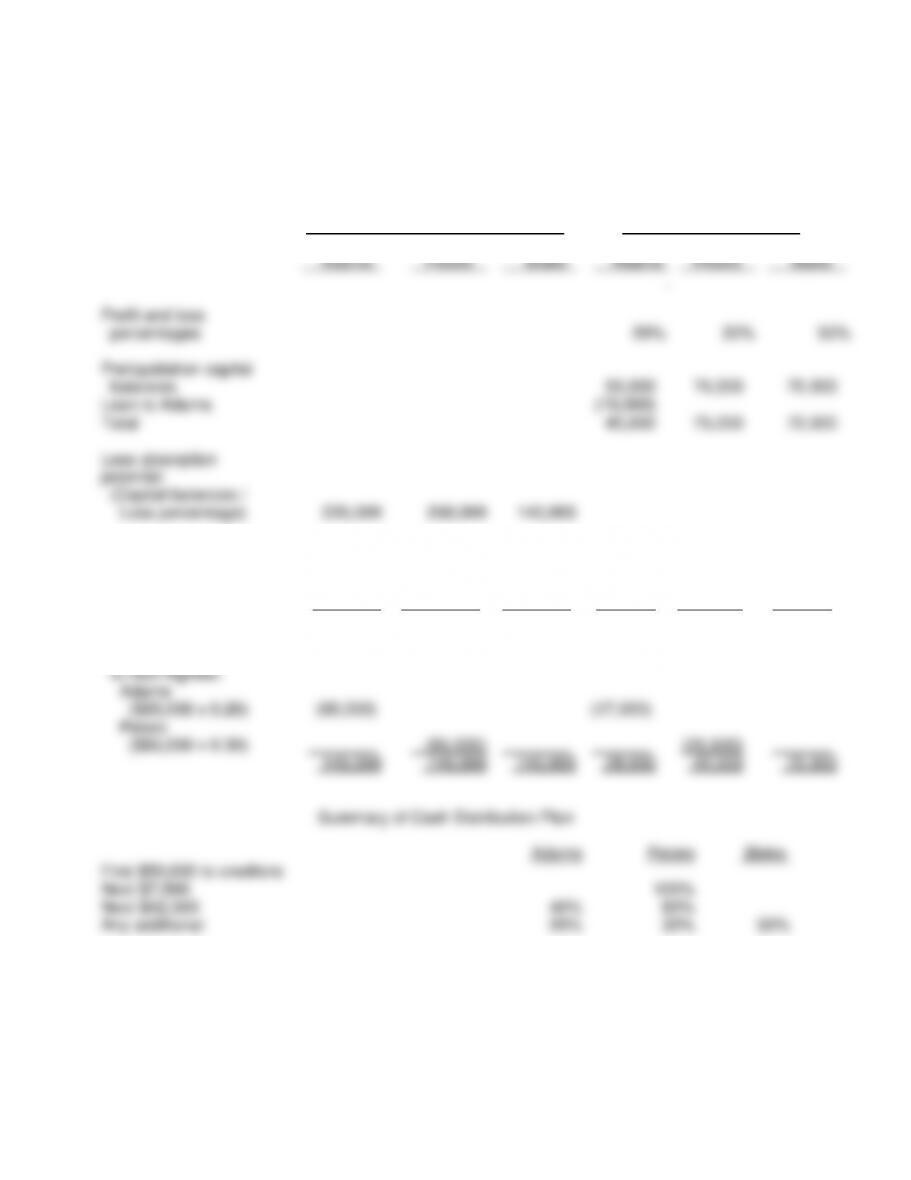

APB Partnership

Cash Distribution Plan

Loss Absorption Potential

Capital Accounts

Adams

Peters

Blake

Adams

Peters

Blake

Profit and loss

percentages

20%

30%

50%

Preliquidation capital

balances

55,000

75,000

70,000

Loan to Adams

(10,000)

Total

45,000

75,000

70,000

Loss absorption

potential

(Capital balances /

Loss percentage)

225,000

250,000

140,000

Decrease highest LAP

to next highest:

Adams

($25,000 x 0.30)

(25,000)

(7,500)

225,000

225,000

140,000

45,000

67,500

70,000

Decrease LAPs

to next highest:

Adams

($85,000 x 0.20)

(85,000)

(17,000)

Peters

($85,000 x 0.30)

(85,000)

(25,500)

140,000

140,000

140,000

28,000

42,000

70,000

Summary of Cash Distribution Plan

Adams

Peters

Blake

First $50,000 to creditors

Next $7,500

100%

Next $42,500

40%

60%

Any additional

20%

30%

50%

Chapter 16 – Partnerships: Liquidation

16–22

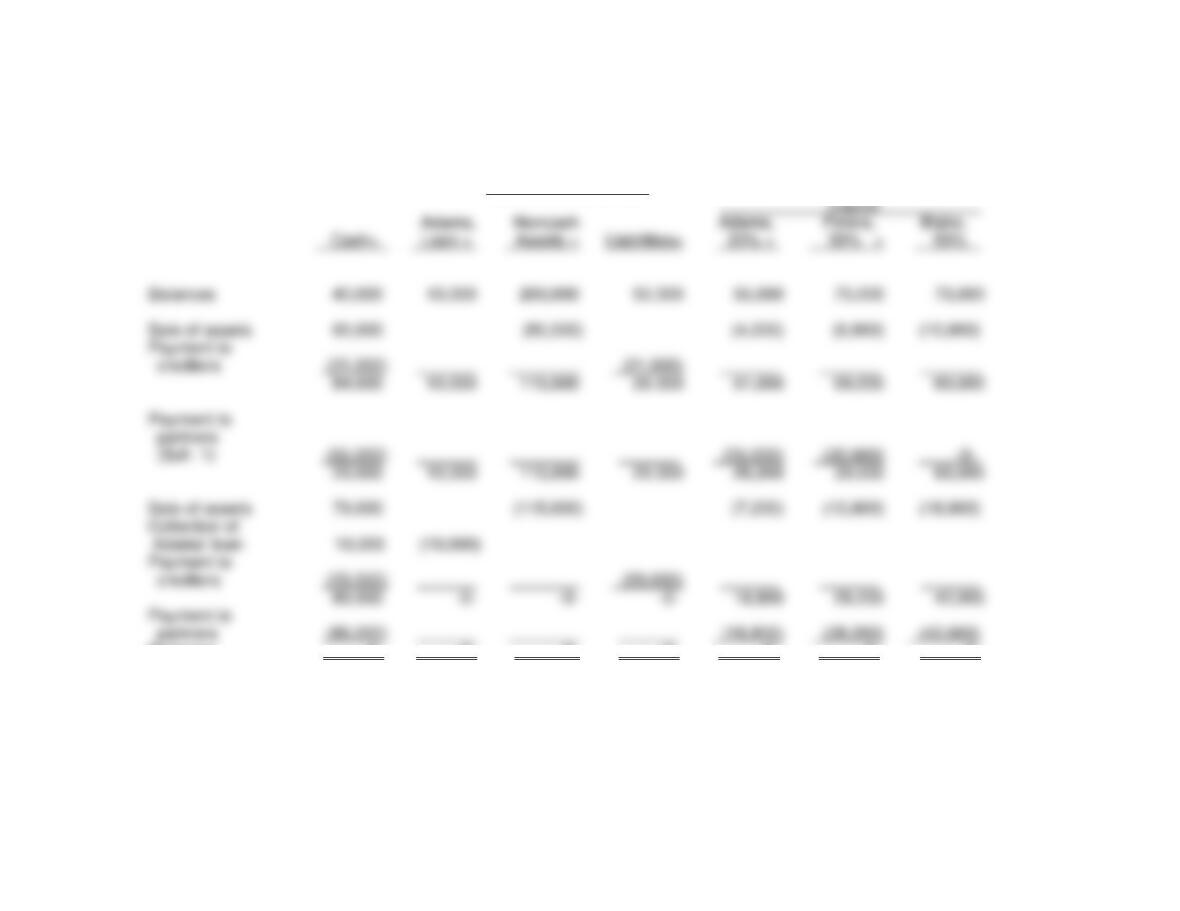

16-9 Confirmation of Cash Distribution Plan

Based on strict observance of UPA 1997:

APB Partnership

Statement of Partnership Realization and Liquidation

Installment Liquidation

Capital

Adams,

Noncash

Adams,

Peters,

Blake,

Cash+

Loan +

Assets =

Liabilities+

20% +

30% +

50%

Balances

40,000

10,000

200,000

50,000

55,000

75,000

70,000

Sale of assets

65,000

(85,000)

(4,000)

(6,000)

(10,000)

Payment to

creditors

(21,000)

(21,000)

84,000

10,000

115,000

29,000

51,000

69,000

60,000

Payment to

partners

(Sch. 1)

(55,000)

(25,000)

(30,000)

-0-

29,000

10,000

115,000

29,000

26,000

39,000

60,000

Sale of assets

79,000

(115,000)

(7,200)

(10,800)

(18,000)

Collection of

Adams’ loan

10,000

(10,000)

Payment to

creditors

(29,000)

(29,000)

89,000

-0-

-0-

-0-

18,800

28,200

42,000

Payment to

partners

(89,000)

(18,800)

(28,200)

(42,000)

Balances

-0-

-0–

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–23

E16-9 (continued)

Schedule 1:

APB Partnership

Schedule of Safe Payments to Partners

Adams

Peters

Blake

20%__

30% __

50%__

Capital balances, end of first month

51,000

69,000

60,000

Possible loss of $125,000 on noncash

assets ($10,000 loan and $115,000 other)

(25,000)

(37,500)

(62,500)

26,000

31,500

(2,500)

Allocate Blake’s potential deficit:

2,500

20/50 x $2,500

(1,000)

30/50 x $2,500

_______

__(1,500)

___ __

Safe payment to partners

(25,000)

(30,000)

-0-

Chapter 16 – Partnerships: Liquidation

16–24

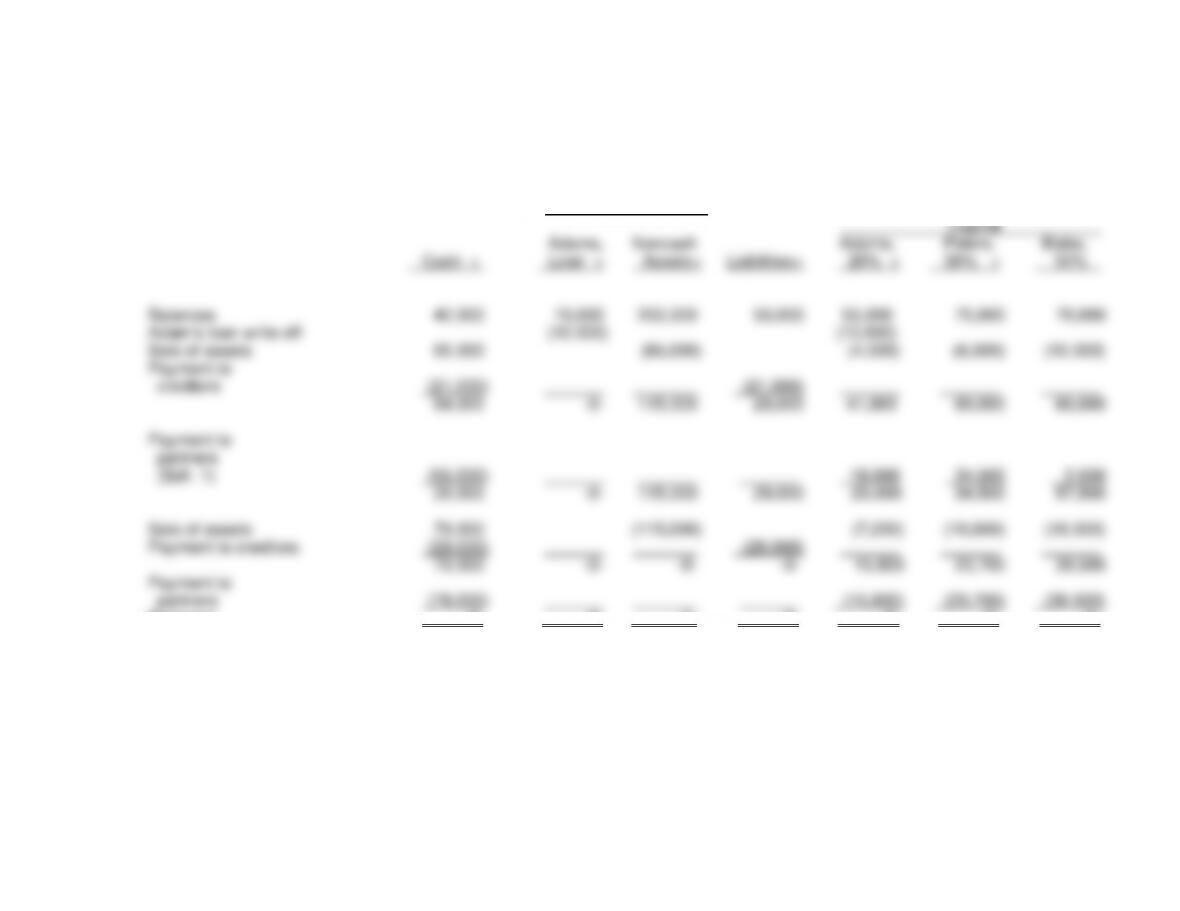

E16-9 (continued)

Based on practical approach:

APB Partnership

Statement of Partnership Realization and Liquidation

Installment Liquidation

Capital

Adams,

Noncash

Adams,

Peters,

Blake,

Cash +

Loan +

Assets=

Liabilities+

20% +

30% +

50%

Balances

40,000

10,000

200,000

50,000

55,000

75,000

70,000

Adam’s loan write-off

(10,000)

(10,000)

Sale of assets

65,000

(85,000)

(4,000)

(6,000)

(10,000)

Payment to

creditors

(21,000)

(21,000)

84,000

-0-

115,000

29,000

41,000

69,000

60,000

Payment to

partners

(Sch. 1)

(55,000)

18,000

34,500

2,500

29,000

-0-

115,000

29,000

23,000

34,500

57,500

Sale of assets

79,000

(115,000)

(7,200)

(10,800)

(18,000)

Payment to creditors

(29,000)

(29,000)

79,000

-0-

-0-

-0-

15,800

23,700

39,500

Payment to

partners

(79,000)

(15,800)

(23,700)

(39,500)

Balances

-0-

-0–

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–25

E16-9 (continued)

Schedule 1:

APB Partnership

Schedule of Safe Payments to Partners

Adams

Peters

Blake

20%__

30% __

50%__

Capital balances, end of first month

41,000

69,000

60,000

Possible loss of $115,000 on assets

(23,000)

(34,500)

(57,500)

18,000

34,500

2,500

Safe payment to partners

(18,000)

(34,500)

(2,500)

Chapter 16 – Partnerships: Liquidation

16–26

E16-10* Incorporation of a Partnership

a.

Partnership’s Books

(1)

Alice, Capital ($11,200 x 0.60)

6,720

Betty, Capital ($11,200 x 0.40)

4,480

Accounts Receivable

800

Inventory

3,200

Equipment

7,200

To record revaluation of assets.

(2)

Investment in A & B Corporation Stock

85,200

Accounts Payable

17,200

Cash

8,000

Accounts Receivable

21,600

Inventory

32,800

Equipment

40,000

To record transfer of net assets to A & B corporation.

(3)

Alice, Capital ($62,400 – $6,720)

55,680

Betty, Capital ($34,000 – $4,480)

29,520

Investment in A & B Corporation Stock

85,200

To record distribution of stock to prior partners.

b.

A & B Corporation‘s Books

Cash

8,000

Accounts Receivable

21,600

Inventory

32,800

Equipment

40,000

Accounts Payable

17,200

Common Stock

71,000

Additional Paid-In Capital

14,200

To record receipt of net assets from partnership.

Chapter 16 – Partnerships: Liquidation

16–27

E16-11A Multiple-Choice Questions on Personal Financial Statements [AICPA

Adapted]

1. b

2. a

3. a –

10,000 shares x ($25 – $10)

=

$150,000 options fair value

x 0.65 net-of-tax rate

$ 97,500 value, net-of–tax

+400,000 pre-option net worth

$497,500 net worth

4. d

5. a

6. c

7. b

8. c

9. d – 95,500 + 3,400 = 98,900

10. b

11. d – 125,000 – 50,000 = 75,000

Chapter 16 – Partnerships: Liquidation

16–28

E16-12A Personal Financial Statements

Leonard and Michelle

Statement of Changes in Net Worth

For the Year Ended August 31, 20X3

Realized increases in net worth:

Salaries

$ 44,300

Farm income

6,700

Dividends and interest income

1,400

$ 52,400

Realized decreases in net worth:

Income taxes

$ 11,400

Personal expenditures

43,500

Loss on sale of marketable securities

300

(1)

Interest expense

4,600

(2)

$(59,800)

Net realized decrease in net worth

$ (7,400)

Unrealized increases in net worth:

Residence

$ 7,300

Investment in Farm

9,300

(3)

$ 16,600

Unrealized decreases in net worth:

Marketable securities

$ 400

(1)

Increase in estimated income taxes

on the difference between the

estimated current values of assets

and liabilities and their tax bases

3,200

$ 3,600

Net unrealized increase in net worth

$ 13,000

Net increase in net worth:

Realized and unrealized changes in net worth

$ 5,600

Net worth at beginning of period

60,800

Net worth at end of period

$ 66,400

(1) Realized loss: $11,000 – $10,700 = $300

Unrealized loss on remaining securities:

($16,300 – $11,000) – $4,900 = $400

(2) Mortgage payable: $76,000 – $71,000 = $5,000 principal payment

$9,000 paid – $5,000 = $4,000 interest payment

Life insurance loan: $4,000 x 0.15 = $600 interest payment

(3) Unrealized holding gain on farm land

$9,900

Unrealized holding loss on net farm equipment

($22,400 – $9,000) – $14,000

(600)

$9,300

Chapter 16 – Partnerships: Liquidation

16–29

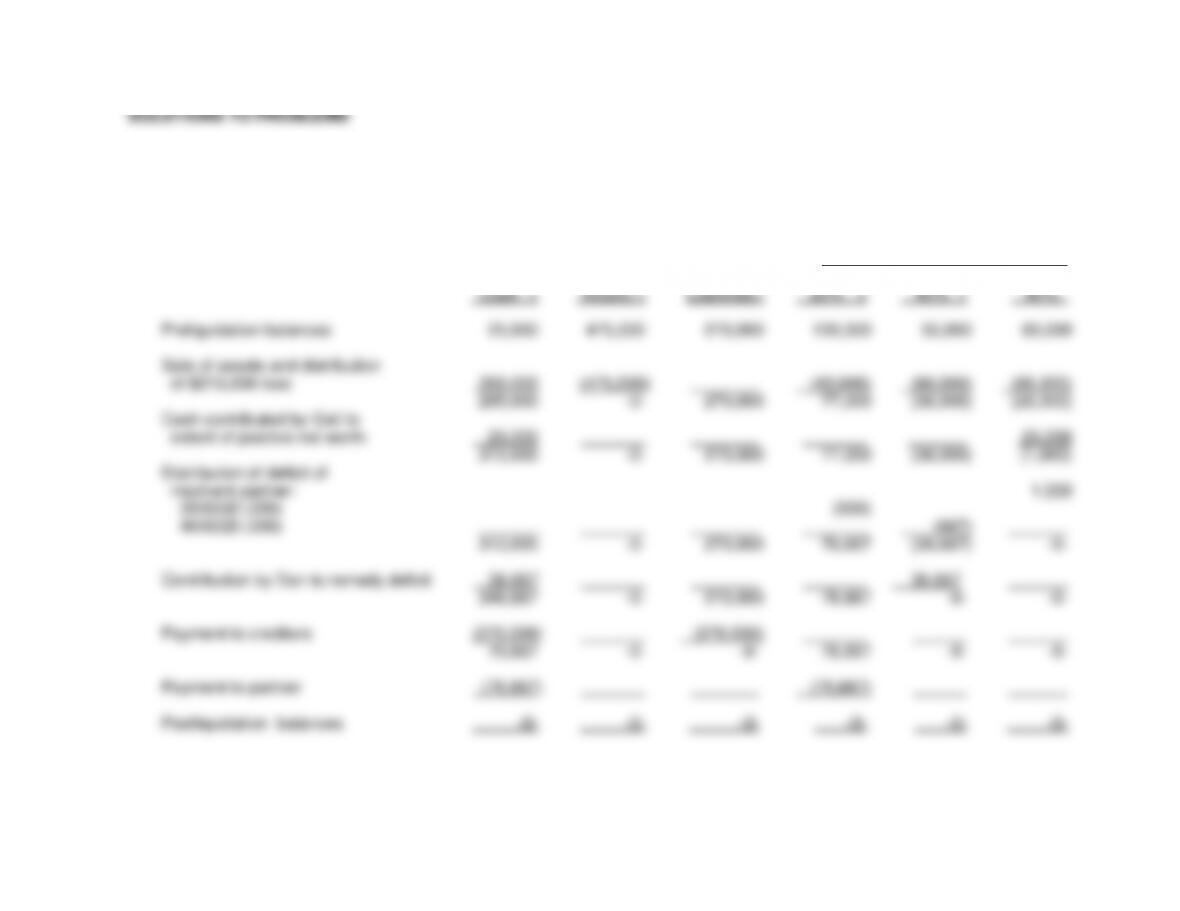

P16-13 Lump-Sum Liquidation

a.

CDG Partnership

Statement of Realization and Liquidation

Lump-sum Liquidation on December 10, 20X6

Capital Balances

Noncash

Carlos

Dan

Gail

Cash +

Assets =

Liabilities+

20% +

40% +

40%

Preliquidation balances

25,000

475,000

270,000

120,000

50,000

60,000

Sale of assets and distribution

of $215,000 loss

260,000

(475,000)

(43,000)

(86,000)

(86,000)

285,000

-0-

270,000

77,000

(36,000)

(26,000)

Cash contributed by Gail to

extent of positive net worth

25,000

25,000

310,000

-0-

270,000

77,000

(36,000)

(1,000)

Distribution of deficit of

insolvent partner:

1,000

20/60($1,000)

(333)

40/60($1,000)

(667)

310,000

-0-

270,000

76,667

(36,667)

-0-

Contribution by Dan to remedy deficit

36,667

36,667

346,667

-0-

270,000

76,667

-0-

-0-

Payment to creditors

(270,000)

(270,000)

76,667

-0-

-0-

76,667

-0-

-0-

Payment to partner

(76,667)

(76,667)

Postliquidation balances

-0-

-0-

-0-

-0-

-0-

-0-

Chapter 16 – Partnerships: Liquidation

16–30

P16-13 (continued)

b.

CDG Partnership

Net Worth of Partners

December 10, 20X6

Carlos

Dan

Gail

Personal assets, excluding

partnership capital interests

250,000

300,000

350,000

Personal liabilities

(230,000)

(240,000)

(325,000)

Personal net worth, excluding

partnership capital interests, Dec. 1, 20X6

20,000

60,000

25,000

Contribution to partnership

(36,667)

(25,000)

Liquidating distribution from partnership

76,667

-0-

-0-

Net worth, December 10, 20X6

96,667

23,333

-0-

This computation assumes that no other events occurred in the 10-day period that changed any of the partners’ personal

assets and personal liabilities. In practice, the accountant must be sure that a computation of net worth is current and timely.

The table shows the effects of the transactions between the partnership and each partner. A presumption of this table is

that the personal creditors of Dan or Gail would not seek court action to block the settlement transactions with the

partnership. Upon winding up and liquidation, the partnership does not have any priority to the partner’s personal assets.

Thus, the personal creditors may seek to block the transactions with the partnership in order to provide more resources from

which they can be paid. A partner who fails to remedy his or her deficit can be sued by the other partners who had to make

additional contributions or even by a partnership creditor if the failed partner is liable to the partnership creditor. But those

claims are not superior to the other claims to the partner’s individual assets.

When accountants provide professional services to partnerships and to its partners, the accountant should expect, at

some time, legal suits involving the partnership and/or individual partners. A strong and thorough understanding of the legal

and accounting foundations of partnerships will be very important to that accountant.