Chapter 9 – Consolidation Ownership Issues

E9-16 Sale of Shares by Subsidiary to Nonaffiliate

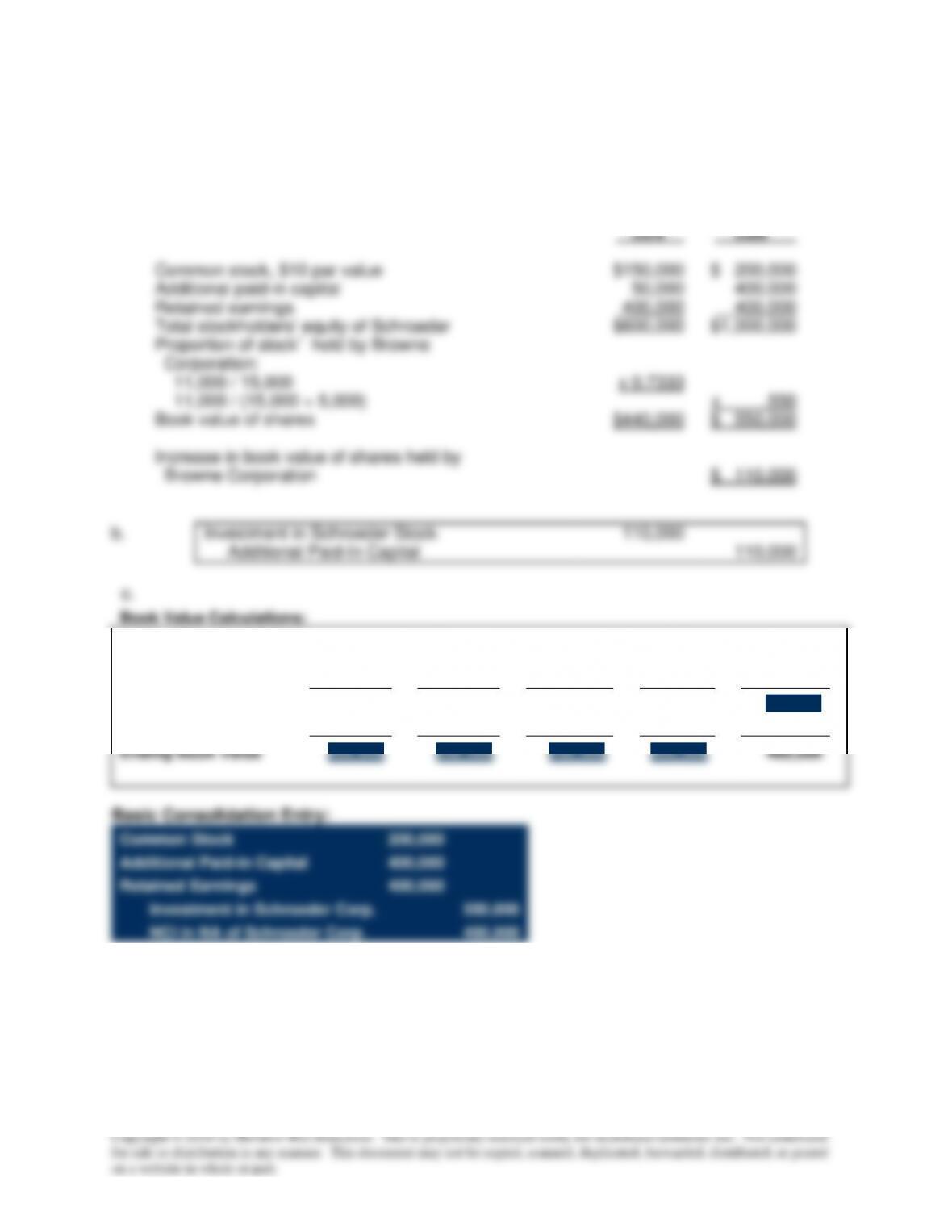

a.

Computation of change in book value of Schroeder Corporation shares held by

Browne Corporation:

Before

After

Sale

Sale

Common stock, $10 par value

$150,000

$ 200,000

Additional paid-in capital

50,000

400,000

Retained earnings

400,000

400,000

Total stockholders‘ equity of Schroeder

$600,000

$1,000,000

Proportion of stock¯ held by Browne

Corporation:

11,000 / 15,000

x 0.7333

11,000 / (15,000 + 5,000)

x .550

Book value of shares

$440,000

$ 550,000

Increase in book value of shares held by

Browne Corporation

$ 110,000

b.

Investment in Schroeder Stock

110,000

Additional Paid-In Capital

110,000

c.

Book Value Calculations:

NCI

26.7/45%

+

Browne

Corp.

73.3/55%

=

Common

Stock

+

Add.

Paid-In

Capital

+

Retained

Earnings

Beginning Book Value

160,000

440,000

150,000

50,000

400,000

New Shares

290,000

110,000

50,000

350,000

Ending Book Value

450,000

550,000

200,000

400,000

400,000

Basic Consolidation Entry:

Common Stock

200,000

Additional Paid-in Capital

400,000

Retained Earnings

400,000

Investment in Schroeder Corp.

550,000

NCI in NA of Schroeder Corp.

450,000

Copyright © 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized

for sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website in whole or part.

P9-17 Multiple-Choice Questions on Preferred Stock Ownership

1.

d –

Book value of shares held by noncontrolling interest:

Preferred stock ($100,000 x 0.30)

$30,000

Common stock [($200,000 + $50,000) x 0.20]

50,000

Total book value

$80,000

2.

b –

Income to noncontrolling preferred shareholders

[($100,000 x 0.10) x 0.30]

$3,000

Income to noncontrolling common shareholders:

Reported net income of Upland Company

$30,000

Income to preferred shareholders

(10,000)

Income to common shareholders

$20,000

Proportion of common stock owned by

noncontrolling interest

x 0.20

4,000

Total income to noncontrolling interest

$7,000

3.

b –

Reported net income of Upland Company

$ 30,000

Operating income of Stacey Company

100,000

Consolidated net income

$130,000

Less: Income to noncontrolling interest

(7,000)

Income to controlling interest

$123,000

4.

c –

Controlling interest:

Common stock

$ 300,000

Retained earnings

350,000

Total controlling interest

$ 650,000

Noncontrolling interest: ($250,000 x 0.20) +

($100,000 x 0.30)

80,000

Total stockholders’ equity

$730,000

5.

a –

All preferred shares of the subsidiary are eliminated in preparing the

consolidated financial statements.

Chapter 9 – Consolidation Ownership Issues

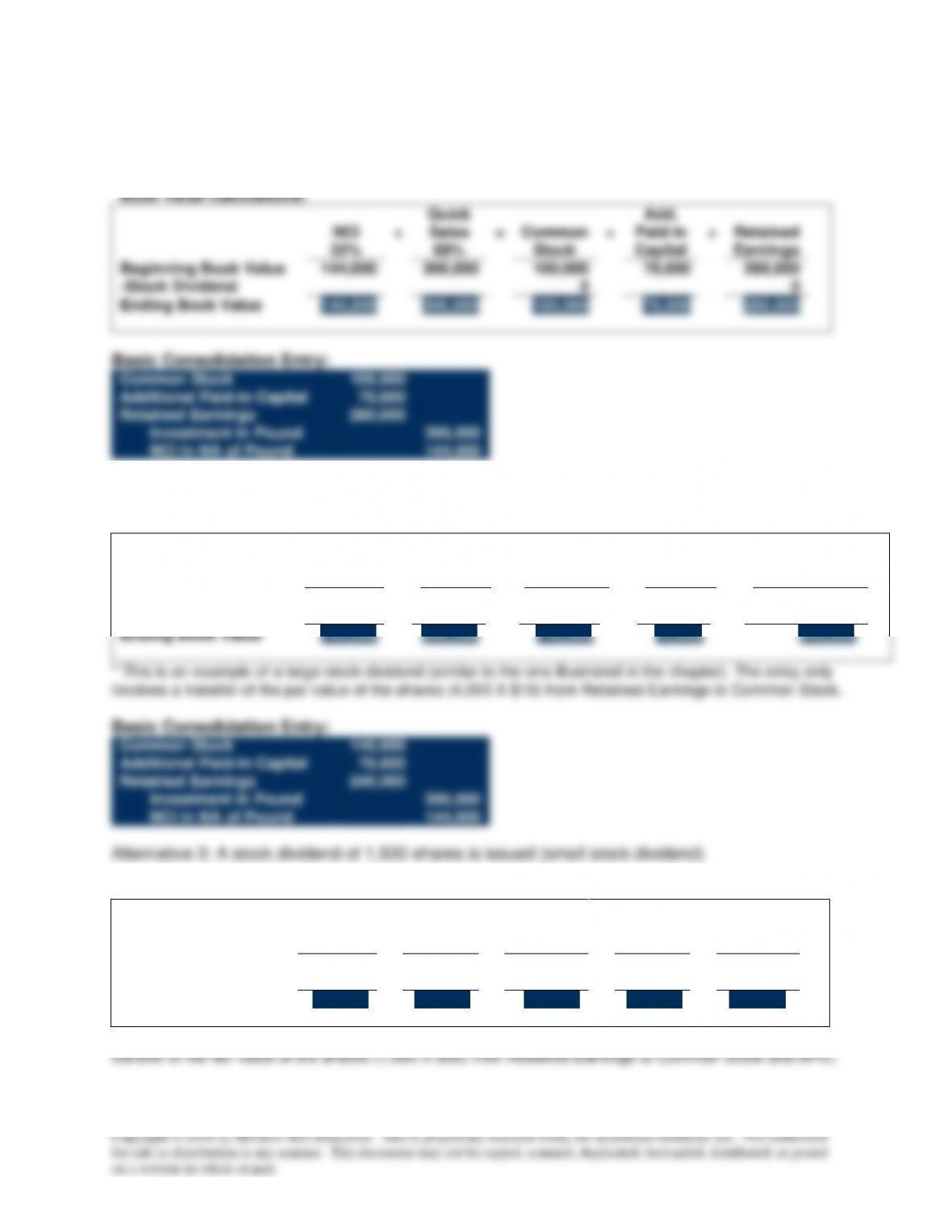

P9–19 Subsidiary Stock Dividend

Alternative 1: Pound Manufacturing stock is split 2:1.

Book Value Calculations:

NCI

32%

+

Quick

Sales

68%

=

Common

Stock

+

Add.

Paid-In

Capital

+

Retained

Earnings

Beginning Book Value

144,000

306,000

100,000

70,000

280,000

-Stock Dividend

0

0

Ending Book Value

144,000

306,000

100,000

70,000

280,000

Book Value Calculations:

NCI 32%

Beginning Book Value

144,000

306,000

-Stock Dividend

40,000

Ending Book Value

144,000

Book Value Calculations:

Quick

68%

Add.

Capital

Beginning Book Value

144,000

306,000

100,000

70,000

-Stock Dividend

60,000

(75,000)*

Ending Book Value

144,000

306,000

115,000

130,000

Consolidated net income and income to controlling

Common Stock

115,000

Additional Paid-in Capital

130,000

Retained Earnings

205,000

Investment in Pound

306,000

NCI in NA of Pound

144,000

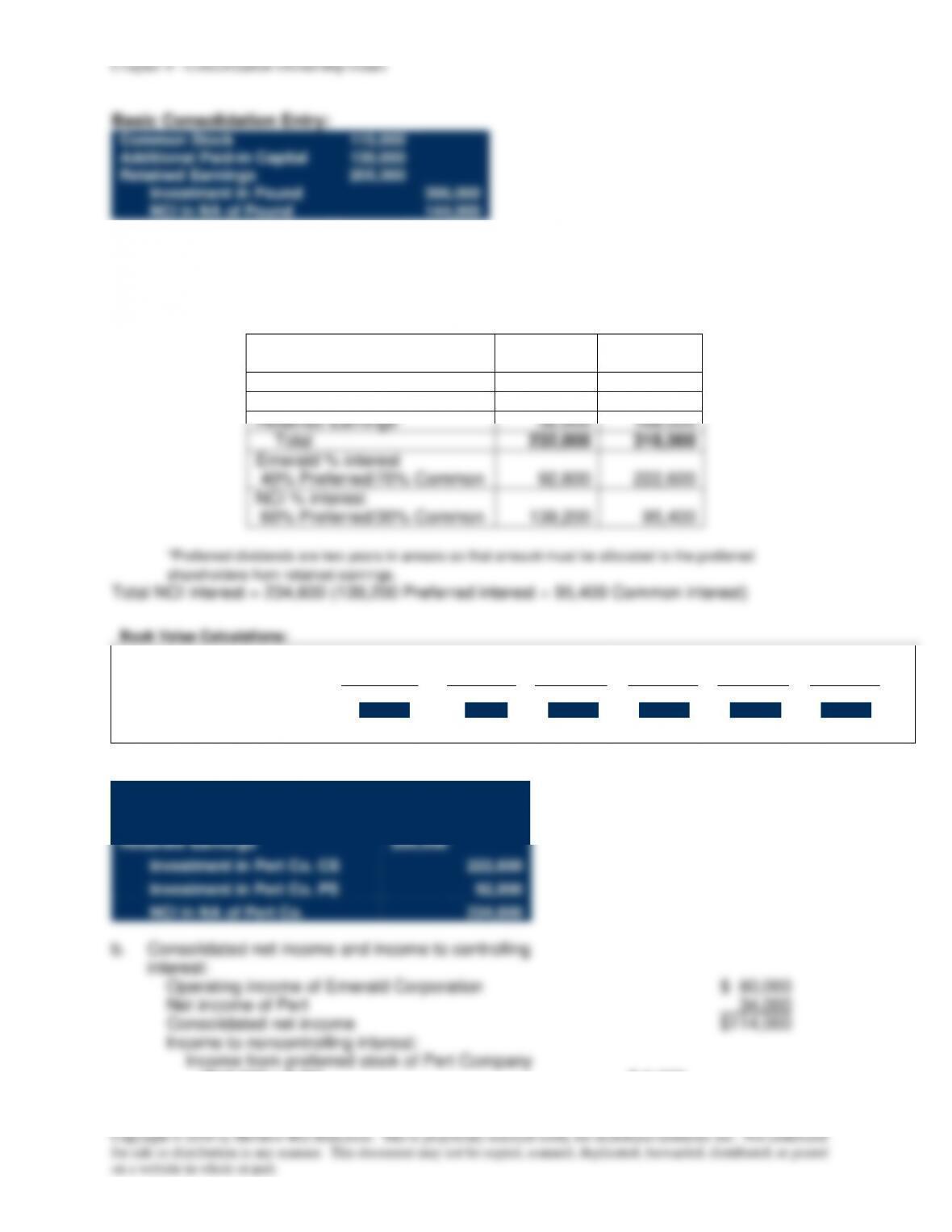

P9-20 Subsidiary Preferred Stock Outstanding

a.Calculation of Preferred/Common Equity

Preferred

Interest

Common

Interest

Preferred Stock

200,000

Common Stock

150,000

Retained Earnings*

32,000

168,000

Total

232,000

318,000

Emerald % interest

40% Preferred/70% Common

92,800

222,600

NCI % interest

60% Preferred/30% Common

139,200

95,400

*Preferred dividends are two years in arrears so that amount must be allocated to the preferred

shareholders from retained earnings.

Total NCI interest = 234,600 (139,200 Preferred interest + 95,400 Common interest)

Book Value Calculations:

NCI

60%/30%

+

Inv. PS

40%

+

Inv. CS

70%

=

Pref.

Stock

+

Com.

Stock

+

Ret.

Earn.

Book Value

234,600

92,800

222,600

200,000

150,000

200,000

Basic Consolidation Entry:

Preferred Stock

200,000

Common Stock

150,000

Retained Earnings

200,000

Investment in Pert Co. CS

222,600

Investment in Pert Co. PS

92,800

NCI in NA of Pert Co.

234,600

Chapter 9 – Consolidation Ownership Issues

[($34,000 – $16,000) x 0.30]

5,400

Income to noncontrolling interest

(15,000)

Income to controlling interest

$ 99,000

Alternate computation of income to controlling interest

Operating income of Emerald Corporation

$80,000

Income from preferred stock of Pert Company

($16,000 x 0.40)

6,400

Income from common stock of Pert Company

[($34,000 – $16,000) x 0.70]

12,600

Income to controlling interest

$99,000

P9-21 Ownership of Subsidiary Preferred Stock

a.

Preferred stockholders’ claim on net assets of Jacobs:

Liquidation value of preferred stock ($101 per share)

$202,000

20X6 dividends in arrears ($200,000 x 0.10)

20,000

Total preferred stockholder claim, December 31, 20X6

$222,000

b.

Book value of Jacobs common shares acquired by Presley:

Total Jacobs stockholders’ equity, December 31, 20X6

$3,155,000

Claim of preferred stockholders

(222,000)

Book value of Jacobs common stock

$2,933,000

Portion acquired by Presley

x 0.60

Book value of common shares acquired by Presley

$1,759,800

c.

Goodwill associated with acquisition of common shares:

Consideration given by Presley to acquire shares

$1,800,000

Fair value of noncontrolling interest in common shares

1,200,000

Total fair value

$3,000,000

Book value of common shares

(2,933,000)

Goodwill

$ 67,000

d.

Income to noncontrolling interest, 20X7:

Jacobs net income

$280,000

Less: impairment of goodwill

(26,000)

Less: 20X7 preferred dividends ($200,000 x 0.10)

(20,000)

Income accruing to common shareholders

$234,000

Noncontrolling common shareholders’ interest

x 0.40

Income to noncontrolling common shareholders

$ 93,600

Preferred dividends to noncontrolling

shareholders ($20,000 x 0.80)

16,000

Total income to noncontrolling shareholders

$109,600

e.

Presley’s income from investment in subsidiary common stock:

Jacobs net income

$280,000