Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Suppose the direct foreign exchange rates in U.S. dollars are:

1 Singapore dollar = $0.7025

1 Cyprus pound = $2.5132

Based on the information given above, how many Singapore dollars are required to

purchase goods costing 10,000 US dollars?

A. 7,025

B. 14,235

C. 17,655

D. 2,975

A parent sold land to its partially owned subsidiary during the year at a loss. The

subsidiary continues to hold the land at the end of the year. The amount to be reported

as consolidated net income for the year should equal:

A. the parent's separate operating income, plus the intercompany loss.

B. the parent's separate operating income, plus the intercompany loss, plus the

subsidiary's net income.

C. the parent's separate operating income, minus the intercompany loss.

D. the parent's separate operating income, minus the intercompany loss, plus the

subsidiary's net income.

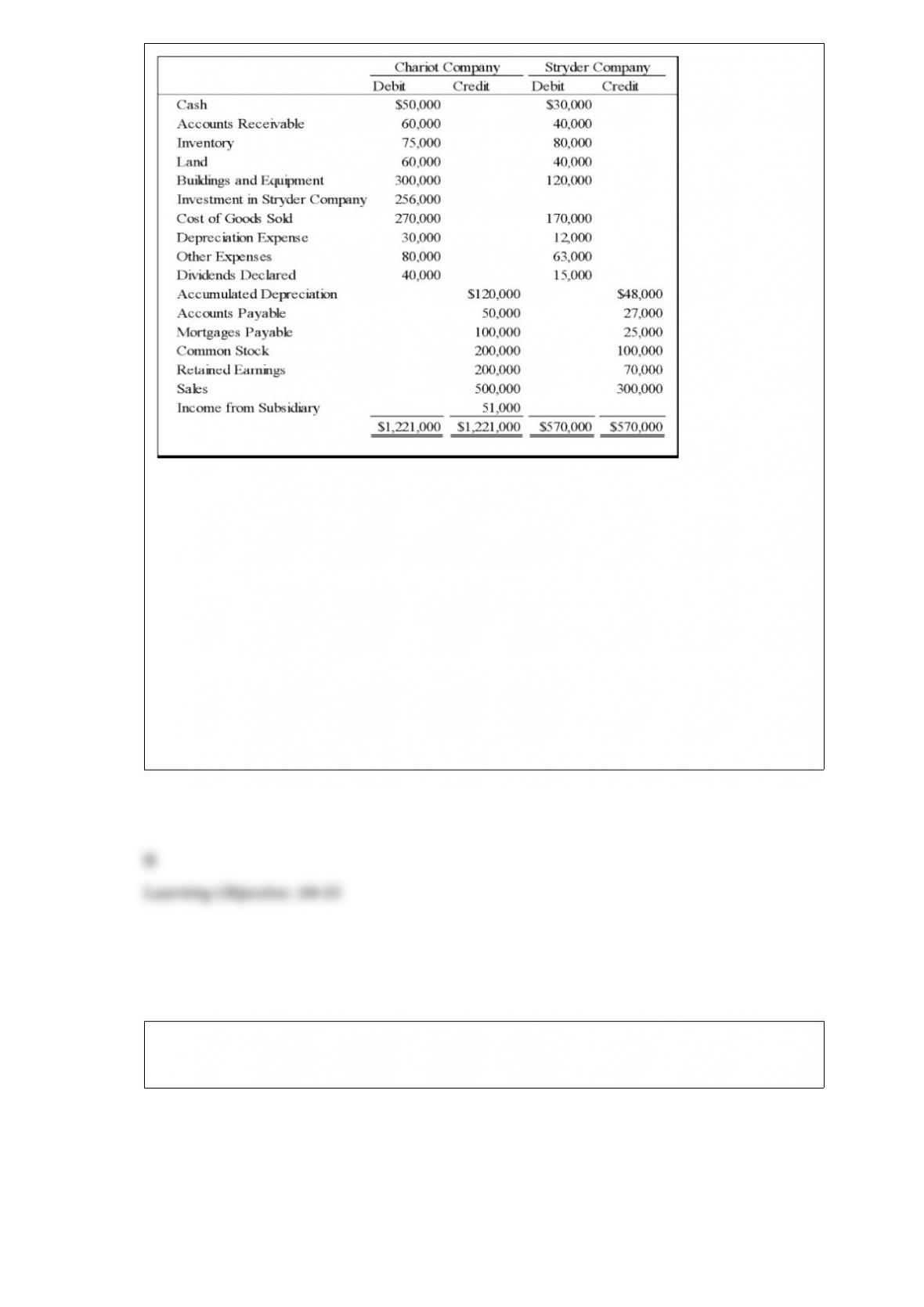

On January 1, 20X8, Chariot Company acquired 100 percent of Stryder Company for

$220,000 cash. The trial balances for the two companies on December 31, 20X8,

included the following amounts:

On the acquisition date, Stryder reported net assets with a book value of $170,000. A

total of $10,000 of the acquisition price is applied to goodwill, which was not impaired

in 20X8. Stryder's depreciable assets had an estimated economic life of 10 years on the

date of combination. The difference between fair value and book value of tangible

assets is related entirely to buildings and equipment. Chariot used the equity method in

accounting for its investment in Stryder. Analysis of receivables and payables revealed

that Stryder owed Chariot $10,000 on December 31, 20X8.

Based on the information provided, the amount of differential assigned to buildings and

equipment that is amortized for the year is:

A. $5,000.

B. $4,000.

C. $10,000.

D. $3,600.

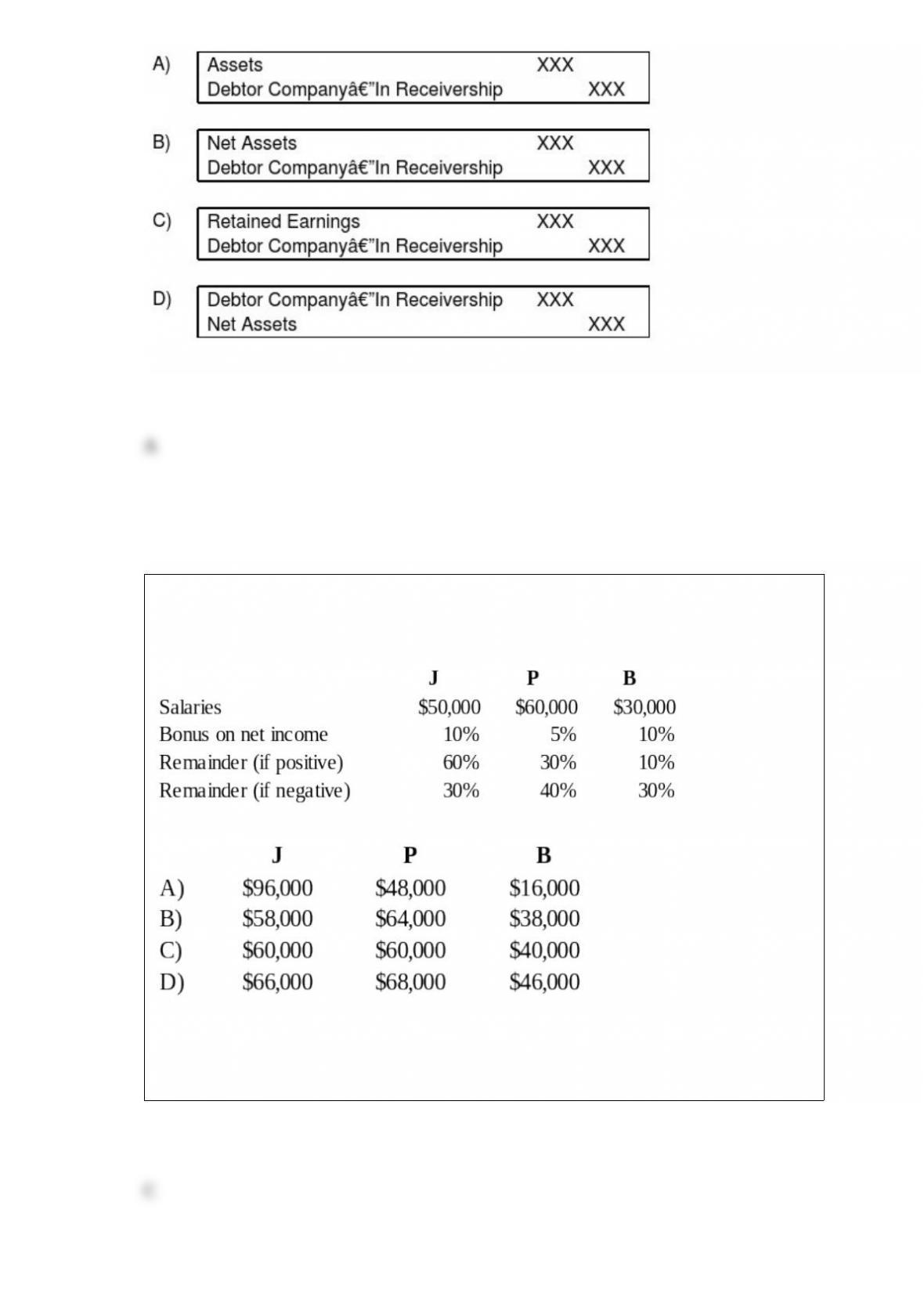

What is the general form of the trustee's opening entry, accepting the assets of the

debtor company?

The JPB partnership reported net income of $160,000 for the year ended December 31,

20X8. According to the partnership agreement, partnership profits and losses are to be

distributed as follows:

How should partnership net income for 20X8 be allocated to J, P, and B?

A. Option A

B. Option B

C. Option C

D. Option D

A loss on the constructive retirement of a parent's bonds by a subsidiary is effectively

recognized in the individual accounting records of the parent and its subsidiary:

I. at the date of constructive retirement.

II. over the remaining term of the bonds.

A. I

B. II

C. Both I and II

D. Neither I nor II

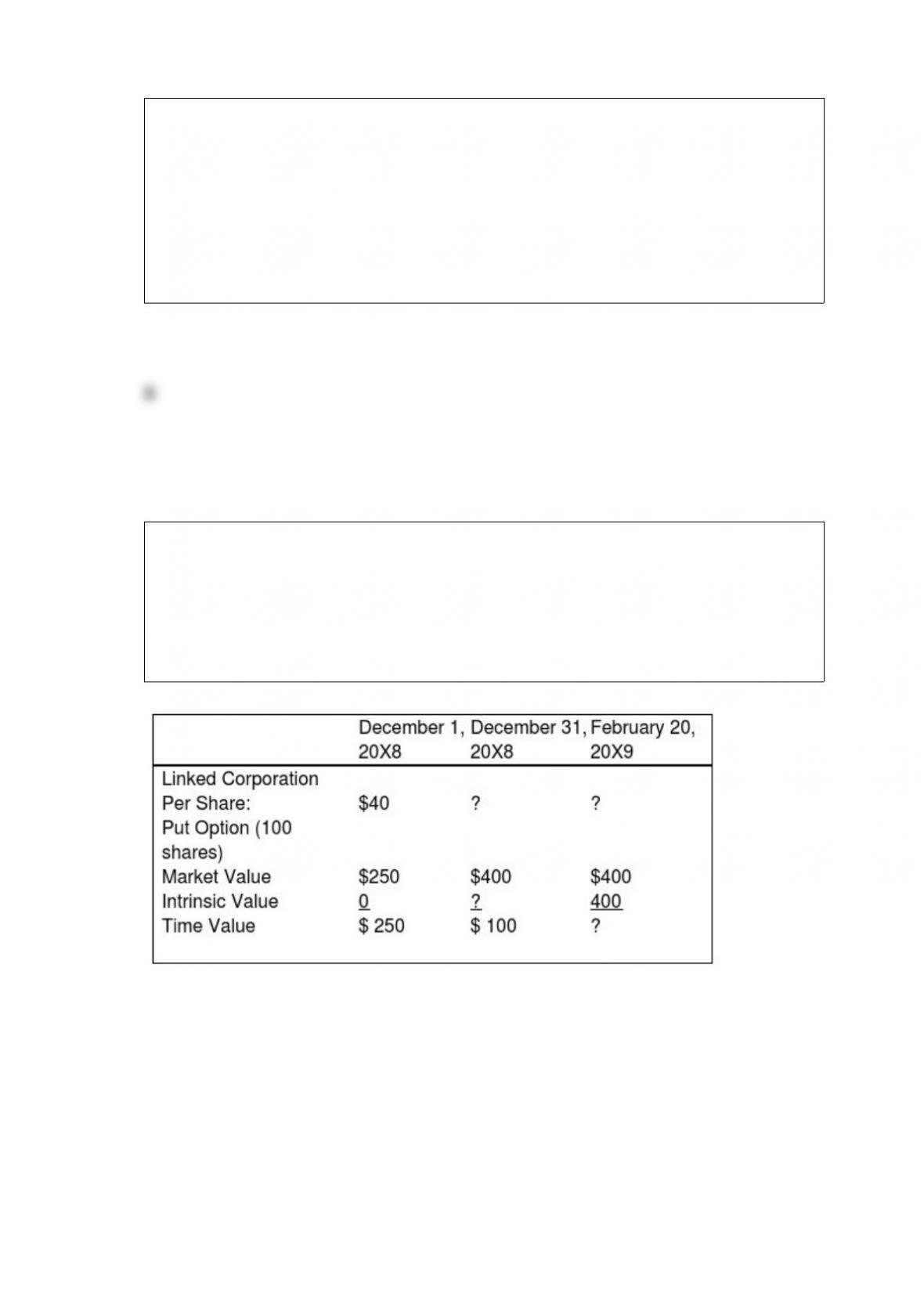

On December 1, 20X8, Winston Corporation acquired 100 shares of Linked

Corporation at a cost of $40 per share. Winston classifies them as available-for-sale

securities. On this same date, it decides to hedge against a possible decline in the value

of the securities by purchasing, at a cost of $250, an at-the-money put option to sell the

100 shares at $40 per share. The option expires on February 20, 20X9. Selected

information concerning the fair values of the investment and the options follow:

Assume that Winston exercises the put option and sells Linked shares on February 20,

20X9.

Based on the preceding information, the journal entry made on December 31, 20X8 to

record decrease in the time value of the options will include:

A. a debit to Loss on Hedge Activity for $150.

B. a credit to Put Option for $300.

C. a debit to Loss on Hedge Activity for $300.

D. a credit to Put Option for $100.

A budgetary comparison schedule presented as required supplementary information for

the general fund should report variances for the difference between:

I. Original budget amounts and final budget amounts

II. Final budget amounts and actual amounts.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

The general fund of Richmond was billed $22,000 on August 15, 20X8, for using the

services of one of its internal service funds (ISF). What accounts should be debited and

credited, respectively, in the general fund on August 15, 20X8, to record this

transaction?

A. Expenditures and Transfer Out to ISF

B. Expenditures and Due to ISF

C. Encumbrances and Due to ISF

D. Encumbrances and Transfer Out to ISF

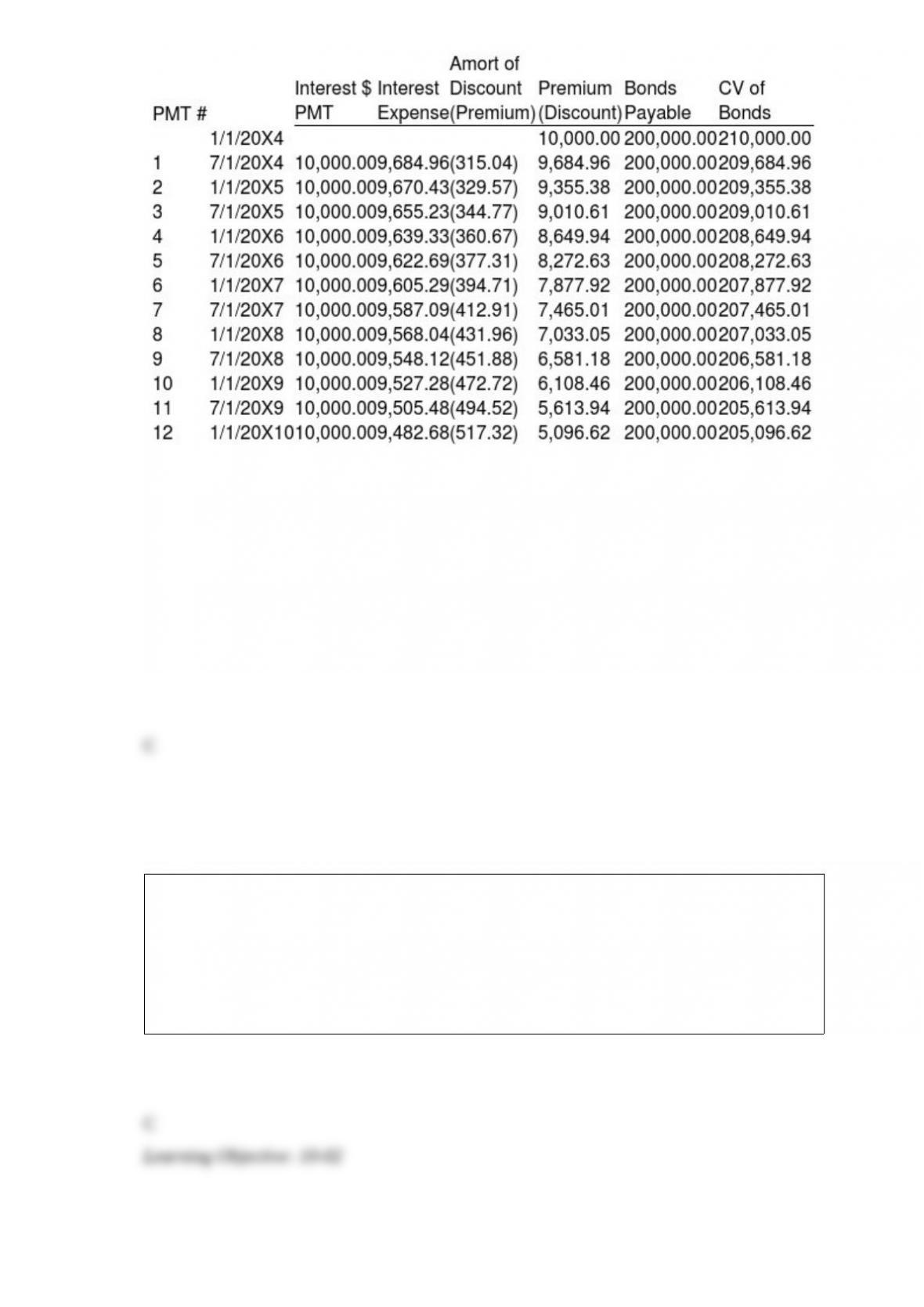

Granite Company issued $200,000 of 10 percent first mortgage bonds on January 1,

20X4, at 105. The bonds mature in 10 years and pay interest semiannually on January 1

and July 1. Mortar Corporation purchased $140,000 of Granite's bonds from the

original purchaser on December 31, 20X8, for $125,000. Mortar owns 75 percent of

Granite's voting common stock. Granite’s partial bond amortization schedule is as

follows:

Based on the information given above, what amount of gain or loss on constructive bond

retirement will be reported in the December 31, 20X8 consolidated financial statements?

A. $8,892 loss

B. $81,108 loss

C. $19,276 gain

D. $81,108 gain

Based on the information provided, what is the consolidated income to the controlling

interest reported for the year 20X4?

A. $275,000

B. $280,000

C. $260,000

D. $200,000

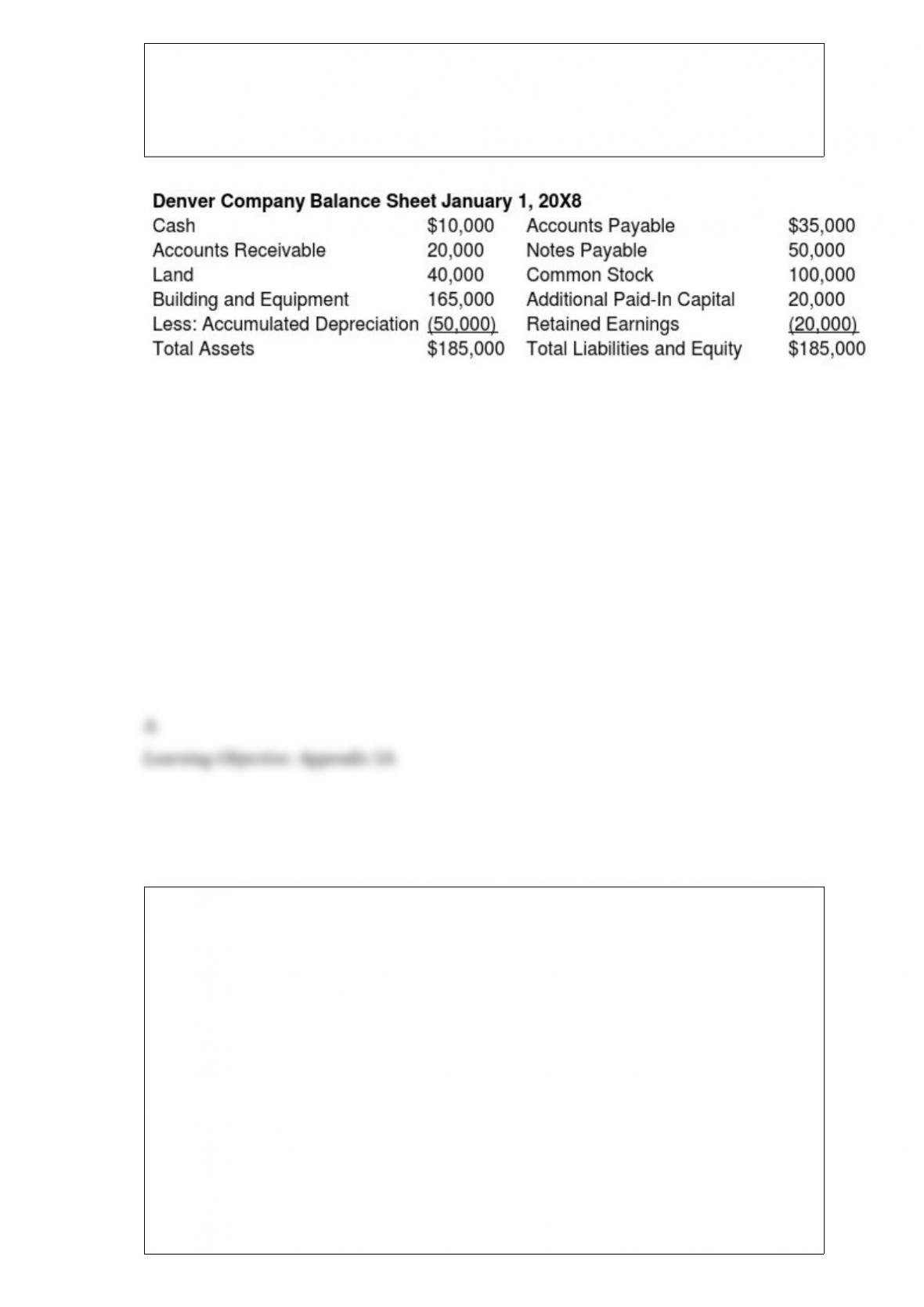

On January 1, 20X8, Colorado Corporation acquired 75 percent of Denver Company's

voting common stock for $90,000 cash. At that date, the fair value of the noncontrolling

interest was $30,000. Denvers's balance sheet at the date of acquisition contained the

following balances:

At the date of acquisition, the reported book values of Denver's assets and liabilities

approximated fair value. Consolidating entries are being made to prepare a consolidated

balance sheet immediately following the business combination.

Based on the preceding information, in the entry to eliminate the investment balance,

A. retained earnings will be credited for $20,000.

B. additional paid-in-capital will be credited for $20,000.

C. retained earnings will be credited for $10,000.

D. noncontrolling interest will be debited for 30,000.

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

"Tombstone ad"

In the AD partnership, Allen's capital is $140,000 and Daniel's is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. What amount will David have to invest to

give him one-fifth percent interest in the capital of the partnership if no goodwill or

bonus is recorded?

A. $60,000

B. $36,000

C. $50,000

D. $45,000

The statement of cash flows for a private not-for-profit performing arts center should

report cash flows according to which of the following classifications?

A. Operating activities, investing activities and financing activities

B. Operating activities, non-capital activities and capital activities.

C. Investing activities, capital activities and financing activities.

D. Financing activities, non-capital activities and capital activities.

Prepare a schedule providing a proof of the translation adjustment using the information

provided below.

Elm City issued a purchase order for supplies with an estimated cost of $5,000. When

the supplies were received, the accompanying invoice indicated an actual price of

$4,950. What amount should Elm debit (credit) to the budgetary fund balance account

after the supplies and invoice were received?

A. $4,950

B. ($50)

C. $50

D. $5,000

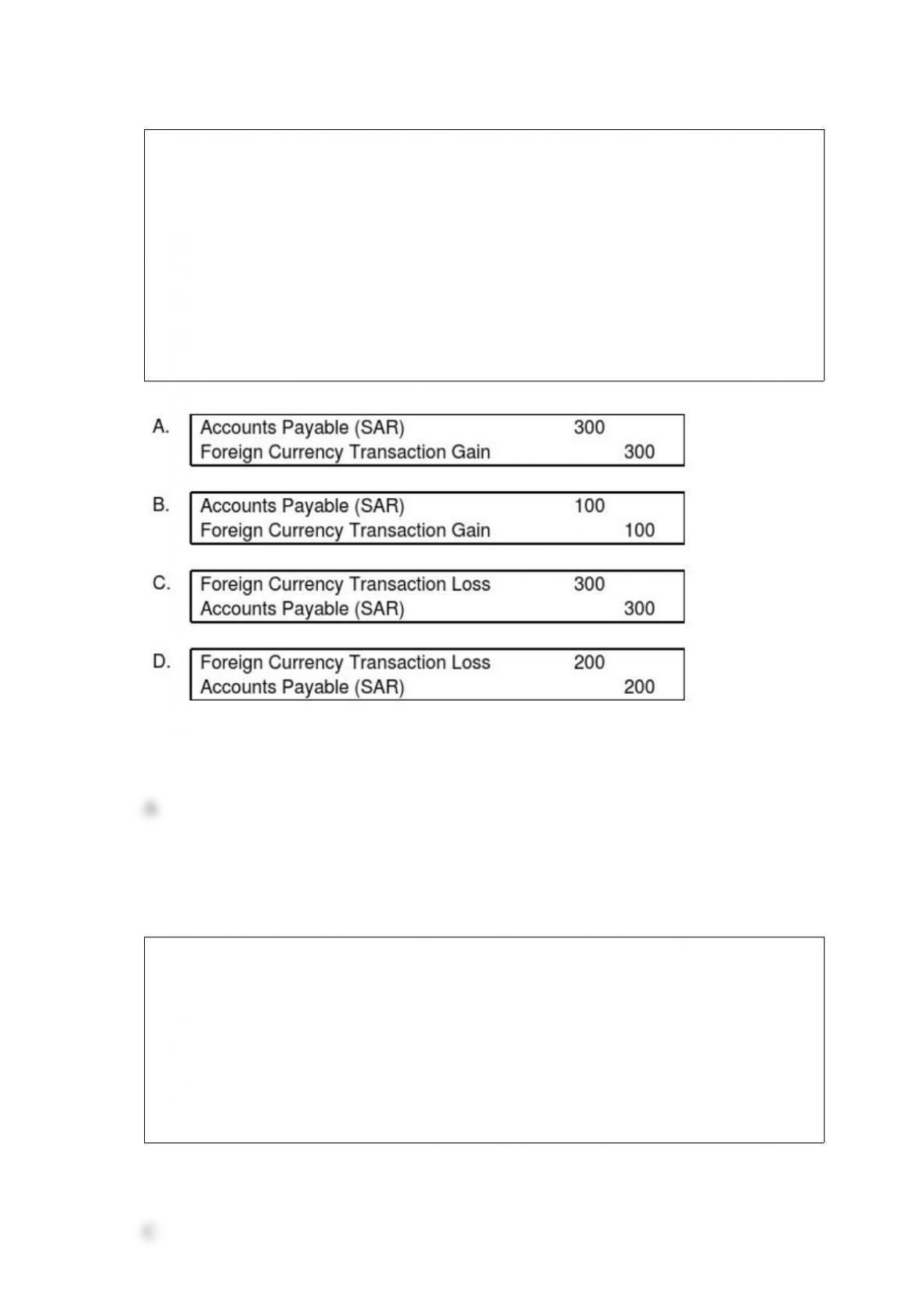

On December 5, 20X8, Texas based Imperial Corporation purchased goods from a

Saudi Arabian firm for 100,000 riyals (SAR), to be paid on January 10, 20X9. The

transaction is denominated in Saudi riyals. Imperial's fiscal year ends on December 31,

and its reporting currency is the U.S. dollar. The exchange rates are:

December 5, 20X8 1 riyal = $0.265

December 31, 20X8 1 riyal = 0.262

January 10, 20X9 1 riyal = 0.264

Based on the preceding information, what journal entry would Imperial make on

December 31, 20X8, to revalue foreign currency payable to equivalent U.S. dollar

value?

Lisa County issued $5,000,000 of general obligation bonds at 101 to finance a capital

project. The $50,000 premium was to be used for payment of principal and interest.

This transaction should be accounted for in the:

A. debt service funds and the general long-term debt account group only.

B. capital projects funds, debt service funds, and the general long-term debt account

group.

C. capital projects funds and debt service funds only.

D. debt service funds only.

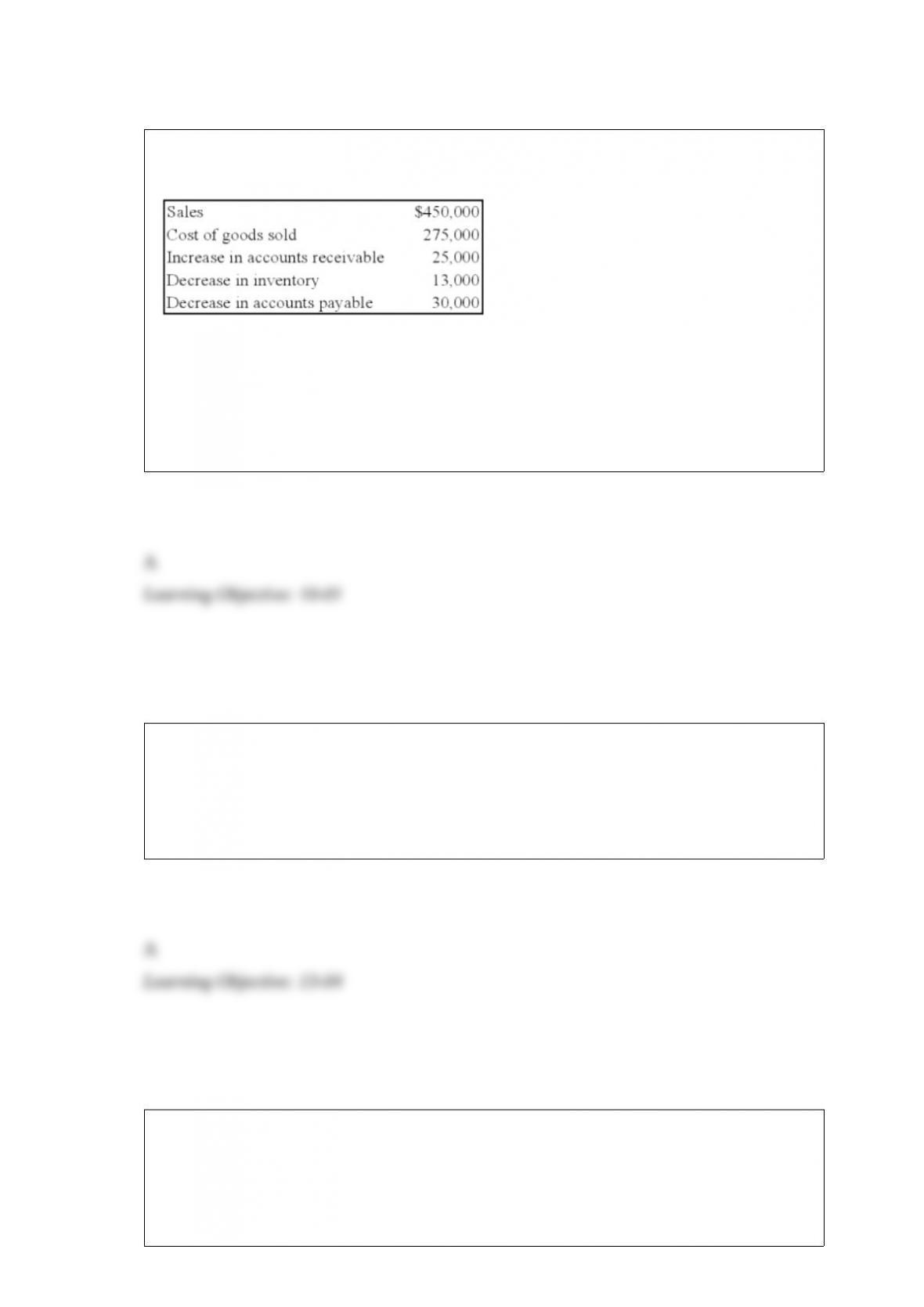

Sigma Company develops and markets organic food products to natural foods retailers.

The following information is available for the company for the year 20X8:

Based on the preceding information, what amount will be reported by the company as

cash payments to suppliers for 20X8?

A. $292,000

B. $305,000

C. $262,000

D. $258,000

ASC 270 uses which view of interim reporting?

A. Integral

B. Discrete

C. Segmental

D. Comprehensive

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital's statement

of operations for the year ended December 31, 20X8.

Transaction: A gain was realized from the sale of endowment investments. The gain is

not expendable.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

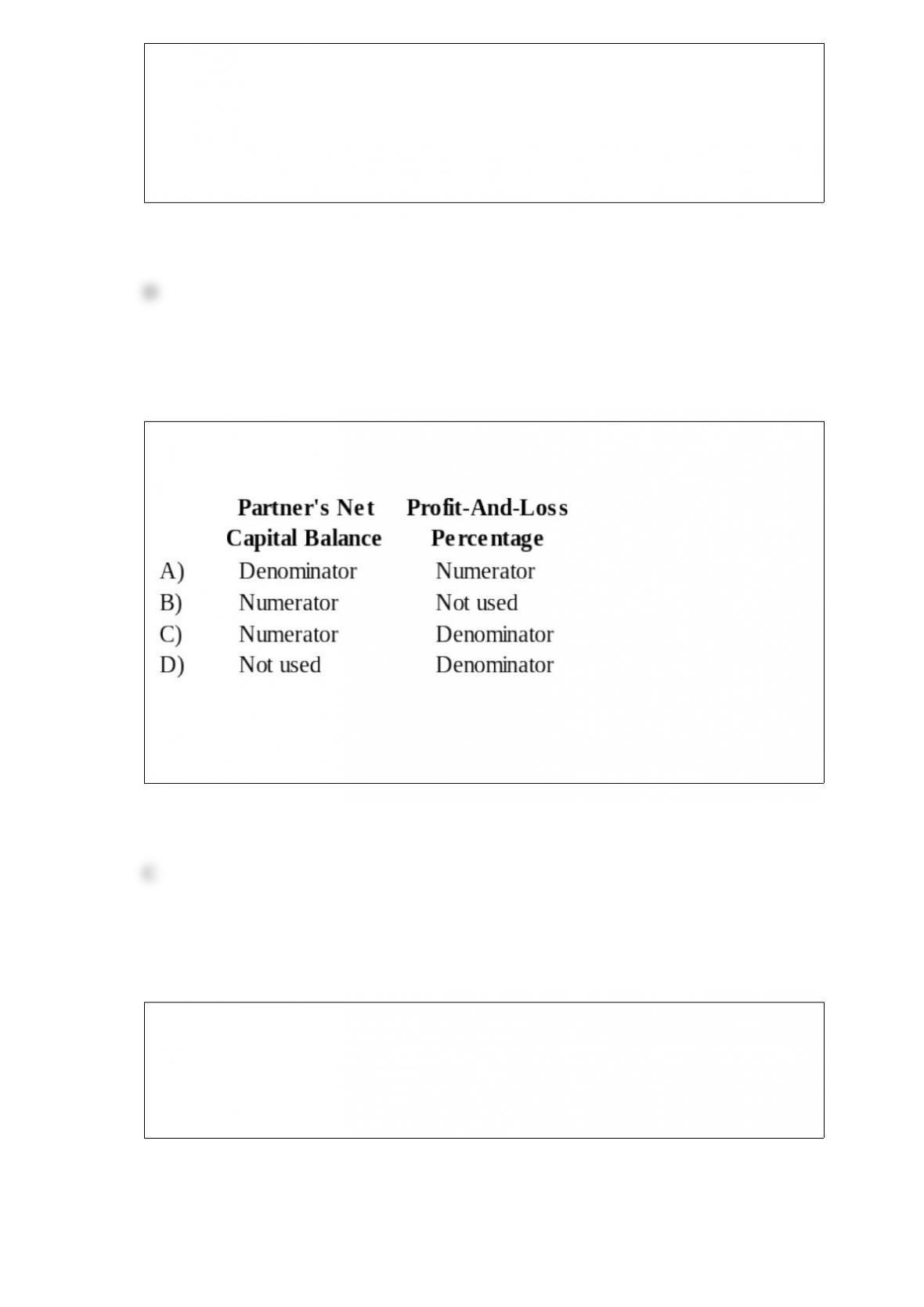

In the computation of a partner's Loss Absorption Power (LAP), the individual partner's

capital balance and profit-and-loss percentage are used in which of the following ways?

A. Option A

B. Option B

C. Option C

D. Option D

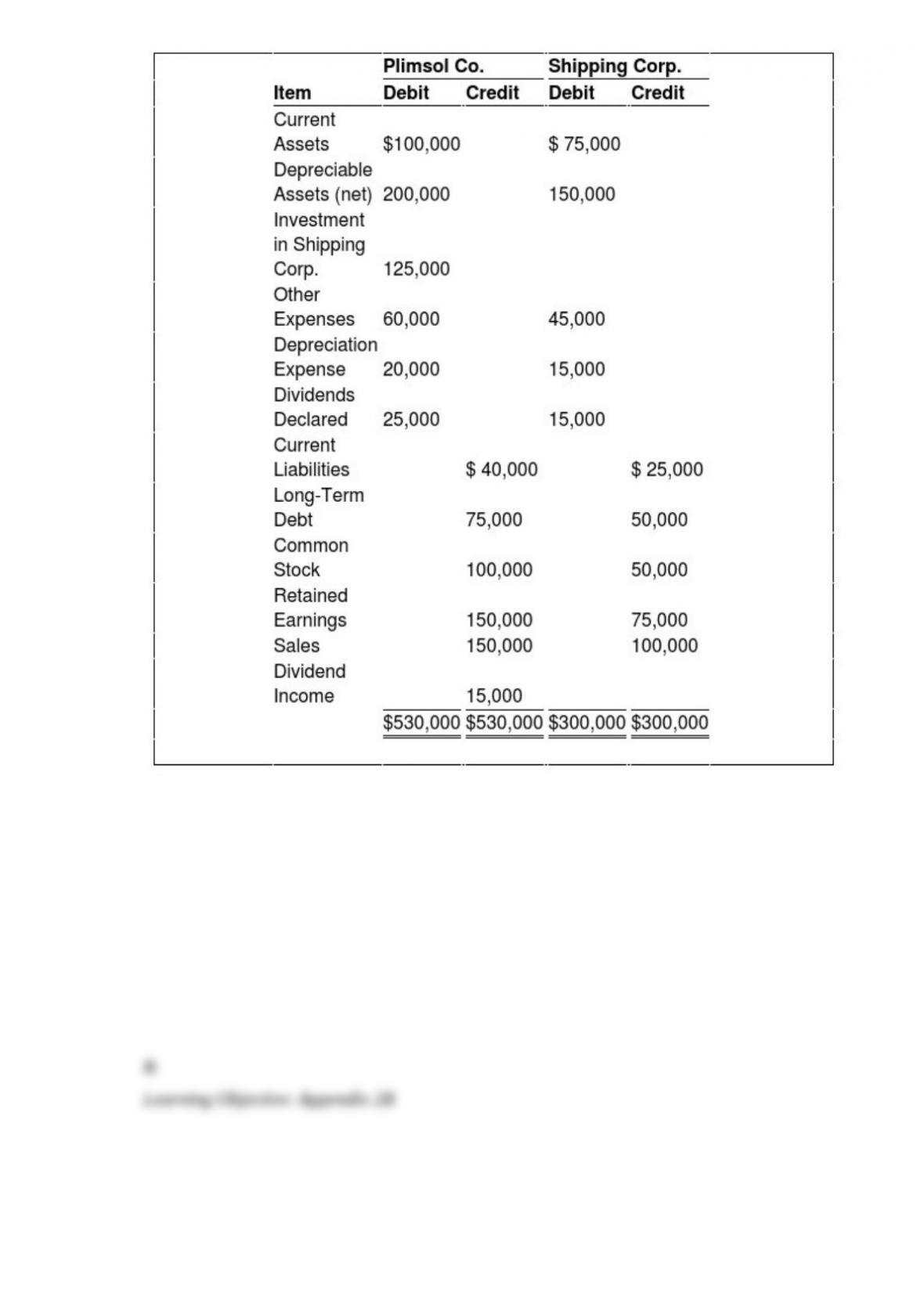

On January 1, 20X4, Plimsol Company acquired 100 percent of Shipping Corporation's

voting shares, at underlying book value. Plimsol uses the cost method in accounting for

its investment in Shipping. Shipping's retained earnings was $75,000 on the date of

acquisition. On December 31, 20X4, the trial balance data for the two companies are as

follows:

Based on the information provided, what amount of total stockholder's equity will be

reported in the consolidated balance sheet prepared on December 31, 20X4?

A. $190,000

B. $335,000

C. $460,000

D. $310,000

Which of the following acts helps businesses raise funds in public capital markets by

minimizing regulatory requirements?

A. Dodd-Frank Wall Street Reform and Consumer Protection Act

B. Foreign Corrupt Practices Act

C. Jumpstart Our Business Startups (JOBS) Act

D. Sarbanes-Oxley Act

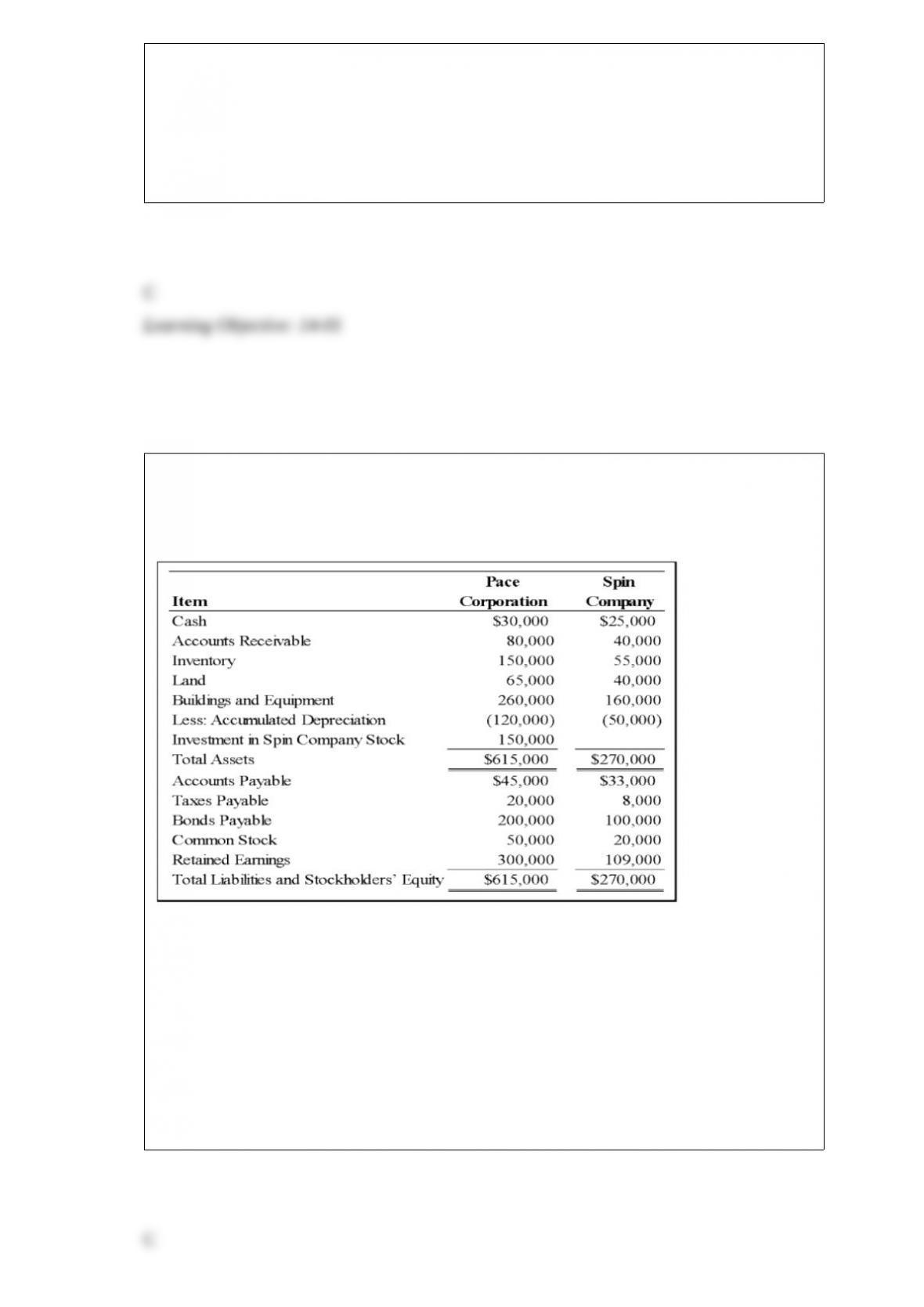

Pace Corporation acquired 100 percent of Spin Company's common stock on January 1,

20X9. Balance sheet data for the two companies immediately following the acquisition

follow:

At the date of the business combination, the book values of Spin's net assets and

liabilities approximated fair value except for inventory, which had a fair value of

$60,000, and land, which had a fair value of $50,000. The fair value of land for Pace

Corporation was estimated at $80,000 immediately prior to the acquisition.

Based on the preceding information, at what amount should total land be reported in the

consolidated balance sheet prepared immediately after the business combination?

A. $130,000

B. $105,000

C. $115,000

D. $120,000

A private, not-for-profit hospital uses a fund structure which includes a general fund

and donor restricted funds. The hospital's revenues from nursing programs and gift

shops should be accounted for in the:

A. specific purpose fund.

B. restricted current fund.

C. general fund.

D. time-restricted fund.

The transactions listed in the following questions occurred in a private, not-for-profit

hospital during 20X8. For each transaction, indicate its effect on the hospital's statement

of operations for the year ended December 31, 20X8.

Transaction: Acquired investments with cash received in the previous item.

Effect on Statement of Operations:

A. Increases operating income.

B. Decreases operating income.

C. The transaction is reported on the statement of operations, but there is no effect on

operating income.

D. The transaction is not reported on the statement of operations.

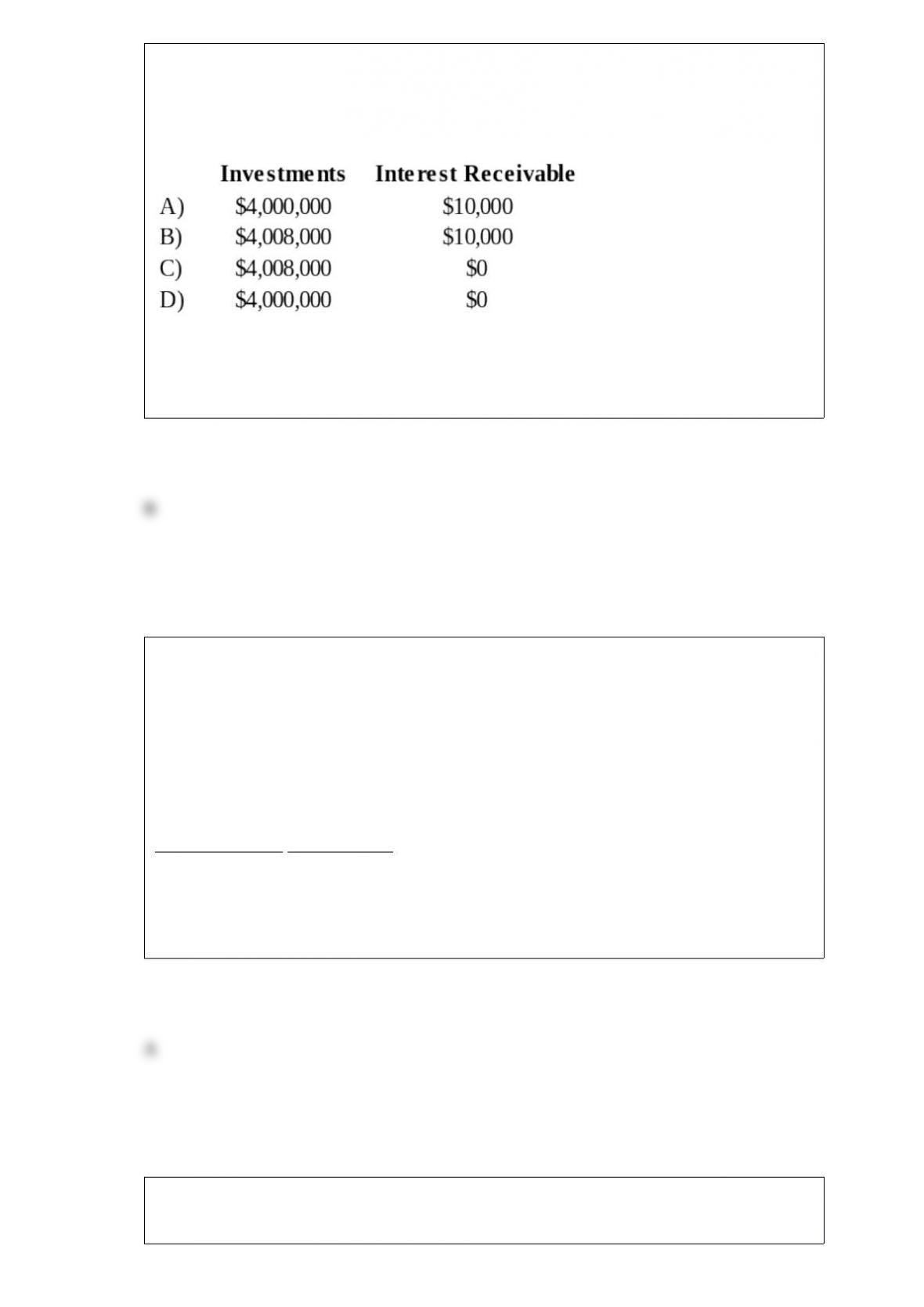

The City of Warwick received $4,000,000 from one of its most prominent citizens

during the year ended June 30, 20X9. The donor stipulated that the $4,000,000 be

invested permanently, and that interest and dividends earned on the investments be used

to support the homeless people of Warwick. During the year ended June 30, 20X9,

dividends received from stock investments amounted to $20,000, while interest

received from bond investments amounted to $40,000. At June 30, 20X9, $10,000 of

interest was earned, but it will not be received until July of 20X9. The fair value of the

securities in which the $4,000,000 was invested had increased $8,000 by June 30,

20X9.

Refer to the above information. On the statement of fiduciary net assets at June 30,

20X9, the nonexpendable trust fund should report investments and interest receivable

of:

A. Option A

B. Option B

C. Option C

D. Option D

Highland Company sold goods to an Egyptian company for 350,000 Egyptian pounds

on December 6, 20X3, with payment due on January 15, 20X4. The exchange rates

were as follows:

December 6, 20X3 1 Egyptian pound = $0.1593

December 31, 20X3 1 Egyptian pound = $0.1612

January 15, 20X4 1 Egyptian pound = $0.1604

Based on the preceding information, which of the following is true of the dollar’s

movement vis--vis the Egyptian pound during the period?

December 6 – 31 January 1 - 15

A. Dollar weakened Dollar strengthened

B. Dollar weakened Dollar weakened

C. Dollar strengthened Dollar strengthened

D. Dollar strengthened Dollar weakened

Mortar Corporation acquired 80 percent of Granite Corporation's voting common stock

on January 1, 20X7. On December 31, 20X8, Mortar received $390,000 from Granite

for equipment Mortar had purchased on January 1, 20X5, for $400,000. The equipment

is expected to have a 10-year useful life and no salvage value. Both companies

depreciate equipment on a straight-line basis.

Based on the preceding information, in the preparation of the 20X8 consolidated

financial statements, equipment will be:

A. debited for $1,000.

B. debited for $10,000.

C. credited for $15,000.

D. debited for $25,000.

Goshen City acquires $36,000 of inventory on November 1, 20X5, having held no

inventory previously. On December 31, 20X5, the end of Goshen City's fiscal year, a

physical count shows $7,000 still in stock. During 20X6, $5,000 of this inventory is

used, resulting in a $2,000 remaining balance of supplies on December 31, 20X6.

Based on the preceding information, which of the following would be the correct

account balances for 20X5 if Goshen City used the purchase method of accounting for

inventories?

Expenditures Inventory of Supplies

A. $36,000 $7,000

B. $29,000 $0

C. $36,000 $0

D. $29,000 $7,000

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Assume that Erin invests $40,000 for a

one-fifth interest. Goodwill is to be recorded. The journal entry to record Erin’s

admission into the partnership will include

A. a credit to cash for $40,000

B. a credit to Erin, Capital for $45,000

C. a credit to Erin, Capital for $40,000

D. a debit to goodwill for $4,000

Based on the information given above, what amount of cost of goods sold will be

reported in the 20X1 consolidated income statement?

A. $13,000

B. $38,000

C. $45,000

D. $58,000

On October 1, 20X7, Chicago Corporation purchased 6,000 shares of Buffalo

Company’s 15,000 outstanding share of common stock for $25 per share. On December

15, 20X7, Buffalo paid $120,000 in dividends to its common stockholders. Buffalo’s

net income for the year ended December 31, 20X7 was $300,000, earned evenly

throughout the year. In its 20X7 income statement, what amount of income from this

investment should Chicago report?

A. $12,000

B. $30,000

C. $48,000

D. $120,000

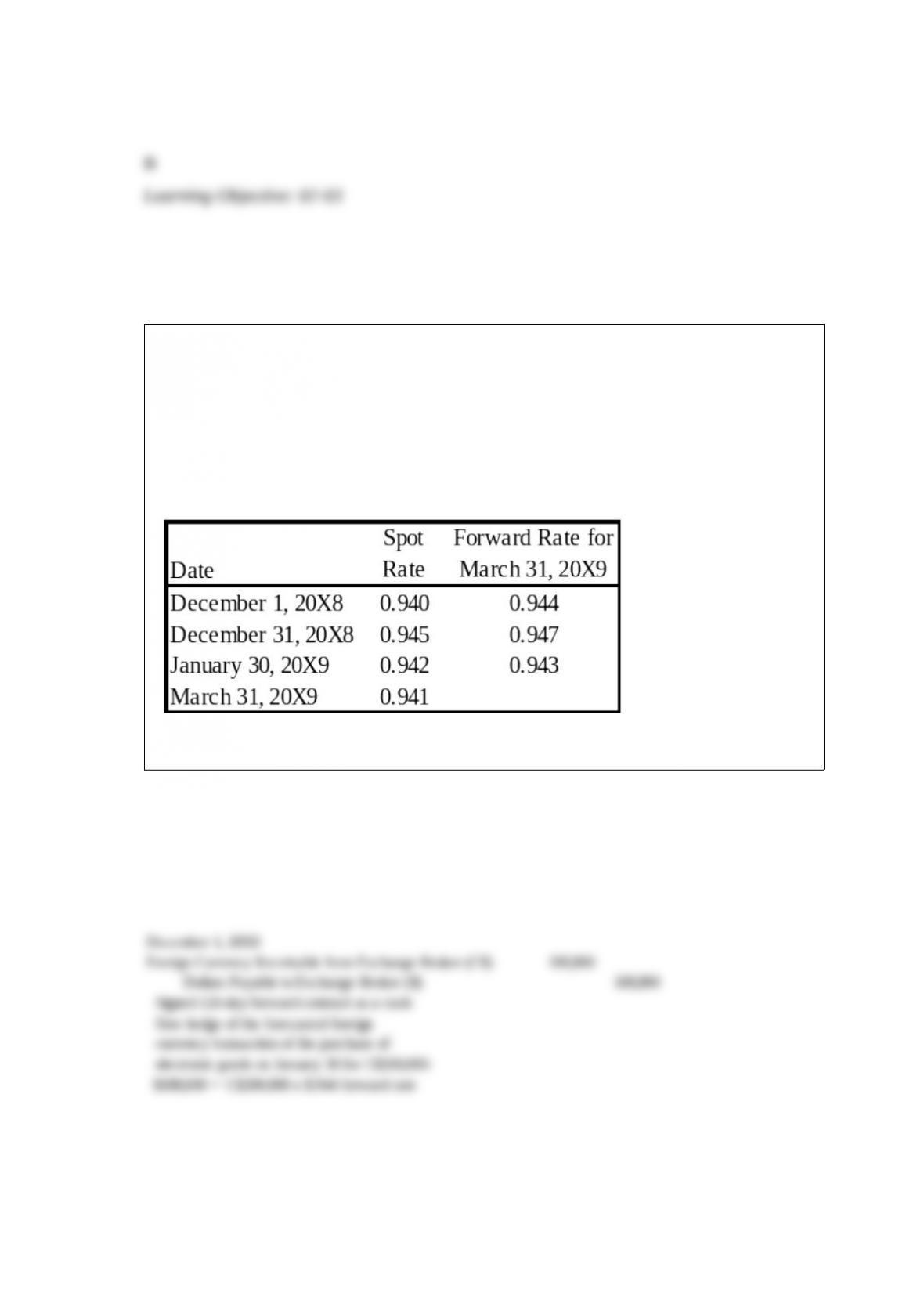

On December 1, 20X8, Denizen Corporation entered into a 120-day forward contract to

purchase 200,000 Canadian dollars (C$). Denizen's fiscal year ends on December 31.

The forward contract was to hedge an anticipated purchase of electronic goods on

January 30, 20X9. The purchase took place on January 30, with payment due on March

31, 20X9. The derivative is designated as a cash flow hedge. The company uses the

forward exchange rate to measure hedge effectiveness. The direct exchange rates

follow:

Required:

Prepare all journal entries for Denizen Corporation.

A partnership may be involved in “Dissociation” or “Dissolution.”

Required:

Describe “Dissociation” and “Dissolution.”

On January 1, 2008, Pace Company acquired all of the outstanding stock of Spin PLC,

a British Company, for $350,000. Spin's net assets on the date of acquisition were

250,000 pounds (). On January 1, 2008, the book and fair values of the Spin's

identifiable assets and liabilities approximated their fair values except for property,

plant, and equipment and trademarks. The fair value of Spin's property, plant, and

equipment exceeded its book value by $25,000. The remaining useful life of Spin's

equipment at January 1, 2008, was 10 years. The remainder of the differential was

attributable to a trademark having an estimated useful life of 5 years. Spin's trial

balance on December 31, 2008, in pounds, follows:

Additional Information

1) Spin uses the FIFO method for its inventory. The beginning inventory was acquired

on December 31, 2007, and ending inventory was acquired on December 26, 2008.

Purchases of 300,000 were made evenly throughout 2008.

2) Spin acquired all of its property, plant, and equipment on March 1, 2006, and uses

straight-line depreciation.

3) Spin's sales were made evenly throughout 2008, and its operating expenses were

incurred evenly throughout 2008.

4) The dividends were declared and paid on November 1, 2008.

5) Pace's income from its own operations was $150,000 for 2008, and its total

stockholders' equity on January 1, 2008, was $1,000,000. Pace declared $50,000 of

dividends during 2008.

6) Exchange rates were as follows:

Assume the U.S. dollar is the functional currency, not the pound.

Required:

1) Prepare a schedule remeasuring the trial balance from British pound into U.S.

dollars.

2) Assume that Pace uses the fully adjusted equity method. Record all journal entries

that relate to its investment in the British subsidiary during 2008. Provide the necessary

documentation and support for the amounts in the journal entries.

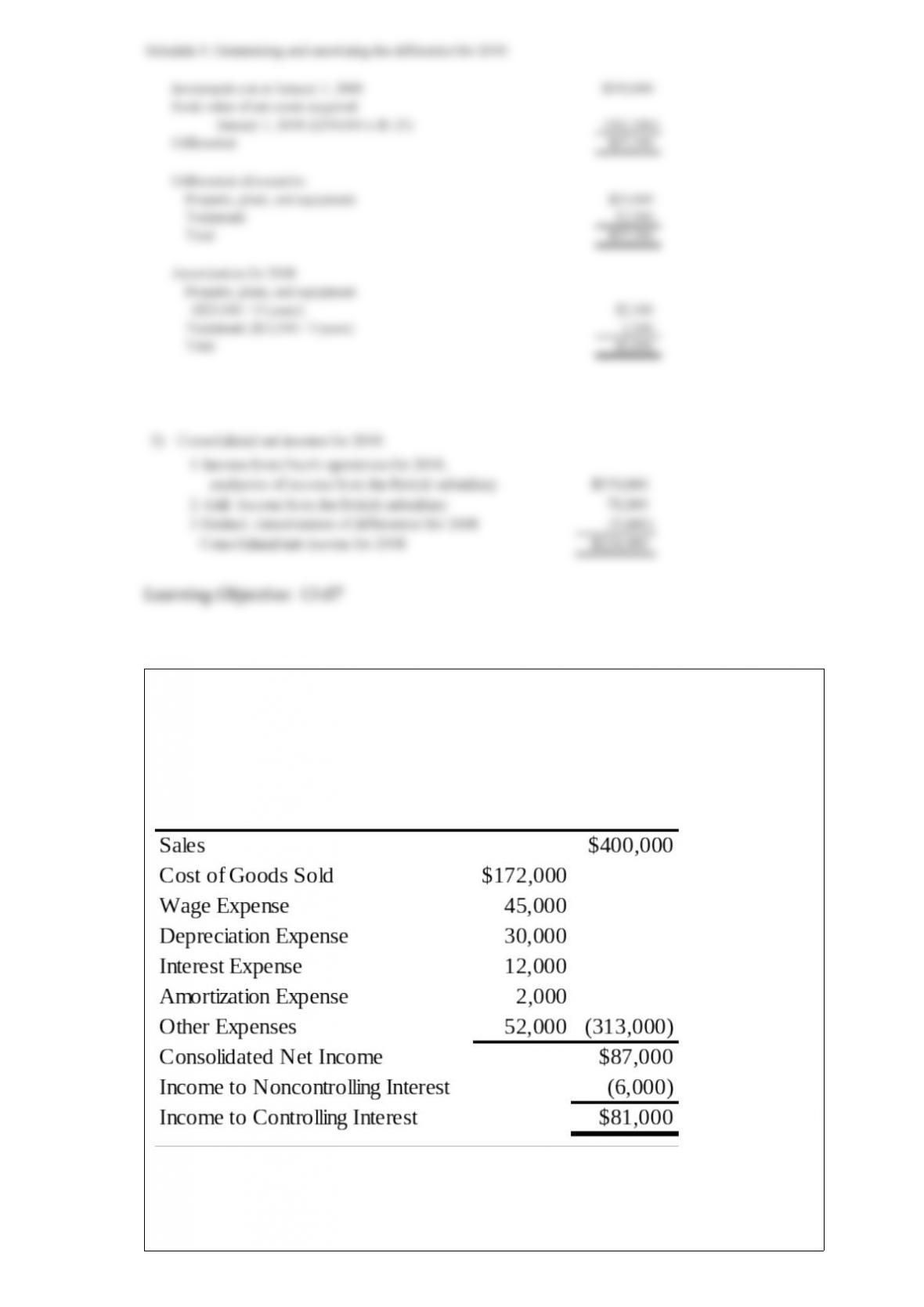

3) Prepare a schedule that determines Pace's consolidated net income for 2008.

Locus Corporation acquired 80 percent ownership of Stereo Company on January 1,

20X6, at underlying book value. At that date, the fair value of the noncontrolling

interest was equal to 20 percent of the book value of Stereo Company. Consolidated

balance sheets at January 1, 20X8, and December 31, 20X8, are as follows:

The consolidated income statement for 20X8 contained the following amounts:

Locus and Stereo paid dividends of $25,000 and $15,000, respectively, in 20X8.

Required:

1) Prepare a worksheet to develop a consolidated statement of cash flows for 20X8

using the indirect method of computing cash flows from operations.

2) Prepare a consolidated statement of cash flows for 20X8.

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Basis of accounting for private NFPs” describes which term listed above?

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Erin directly purchases a one-fifth interest by

paying Jacob $33,000 and Katy $9,000. The land account is increased for its implied

increase in value before Erin is admitted. By what amount is the land account

increased?

A. $20,000

B. $24,000

C. $30,000

D. $36,000

On January 2, 20X2, Kentucky Company acquired 70% of Bluegrass Corporation’s

common stock for $420,000 cash. At the acquisition date, the book values and fair

values of Bluegrass’ assets and liabilities were equal, and the fair value of the

noncontrolling interest was equal to 30% of the total book value of Bluegrass. The

stockholders’ equity accounts of the two companies at the acquisition date are as

follows:

Kentucky Bluegrass

Common Stock ($10 par value) $600,000 $350,000

Additional Paid-In Capital 450,000 50,000

Retained Earnings 250,000 200,000

Total Stockholders’ Equity $1,300,000 $600,000

Noncontrolling interest was assigned income of $15,000 in Kentucky’s consolidated

income statement for 20X2.

Based on the preceding information, what amount will be assigned to noncontrolling

interest on January 2, 20X2, in the consolidated balance sheet?

A. $120,000

B. $126,000

C. $180,000

D. $420,000

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization's statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Acquired equipment with all of the contributions previously received from donors for

equipment purchases.

Cherokee Company reported consolidated revenue of $90,000,000 in 20X5. Cherokee

operates in two geographic areas, domestic and Europe. The following information

pertains to these two areas:

Sales to External Customers Interarea Sales between Affiliates

Domestic $62,000,000 $6,000,000

Europe $28,000,000 $4,000,000

What calculation below is correct to determine if the revenue test is satisfied for the

European operations?

A. $28,000,000/$90,000,000

B. $28,000,000/$100,000,000

C. $32,000,000/$100,000,000

D. $32,000,000/$90,000,000

In the JK partnership, Jacob’s capital is $140,000, and Katy’s is $40,000. They share

income in a 3:2 ratio, respectively. They decide to admit Erin to the partnership. Each of

the following questions is independent of the others.

Refer to the information provided above. Jacob and Katy agree that some of the

inventory is obsolete. The inventory account is decreased before Erin is admitted. Erin

invests $38,000 for a one-fifth interest. What are the capital balances of Jacob and Katy

after Erin is admitted into the partnership?

Jacob Katy

A. $140,000 $40,000

B. $134,000 $36,000

C. $123,200 $28,800

D. $118,400 $25,600