Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–10

P5-20

LO 5-1

10 min.

E

Acquisition Price

Students must determine the acquisition price given two separate situations.

Additionally, students are required to determine the amount assigned to the

noncontrolling interest at the date of acquisition.

P5-21

LO 5-1

15 min.

M

Multiple-Choice Questions on Applying the Equity Method

[AICPA Adapted] Four multiple-choice questions are included. Primary

emphasis is placed on the computation of investment income and the appropriate

account balances under equity-method reporting.

P5-22

LO 5-1

15 min.

M

Amortization of Differential

Journal entries made by an investor during the year are required assuming the

equity method of accounting for the investment.

P5-23

LO 5-1

15 min.

M

Computation of Account Balances

Students must calculate investment income and investment account balances

assuming (a) the equity method is used and (b) the cost method is used. Goodwill

is included.

P5-24

LO 5-1,

LO 5-2

20 min.

H

Complex Differential

The amount of investment income and the balance in the investment account is

required assuming the equity method is used in accounting for the investment.

Amortization of inventory, buildings and equipment, and patents included.

P5-25

LO 5-1

20 min.

M

Equity Entries with Differential

The entry to record a purchase using an exchange of common stock and entries

for two years under equity-method reporting are required. The ending investment

account balance also must be computed. The differential is assigned to buildings

and equipment and goodwill.

P5-26

LO 5-1

15 min.

M

Equity Entries with Differential

Equity-method journal entries must be prepared and the carrying value of the

investment computed following a purchase of shares. The differential is assigned

to inventory, buildings and equipment, and goodwill.

P5-27

LO 5-1

30 min.

M

Additional Ownership Level

Net income must be calculated and all journal entries made for investments

involving three entities.

P5-28

LO 5-1

15 min.

M

Correction of Error

An investor incorrectly applies the equity method. An entry is necessary to

correct the accounts involved.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–11

P5-29

LO 5-2

45 min.

M

Majority-Owned Subsidiary Acquired at More than Book Value

Students must provide the consolidation entries needed to prepare a consolidated

balance sheet immediately following a business combination in which the

subsidiary is acquired at an amount greater than book value. A consolidated

balance sheet worksheet and a consolidated balance sheet must also be prepared.

An intercompany receivable/payable is involved.

P5-30

LO 5-2

30 min.

M

Balance Sheet Consolidation of Majority-Owned Subsidiary

Students must provide the entry to record the business combination on the books

of the parent. Consolidation entries, a consolidated balance sheet worksheet, and

a consolidated balance sheet must also be prepared.

P5-31

LO 5-1,

LO 5-2

40 min.

M

Incomplete Data

Students must interpret and derive amounts and relationships between a parent

company and its subsidiary, based on incomplete and missing data.

P5-32

LO 5-2

10 min.

E

Income and Retained Earnings

Information on operating income and dividend payments is given for the parent

and subsidiary. Net income and retained earnings reported by the parent and

subsidiary, consolidated net income, and consolidated retained earnings must be

computed.

P5-33

LO 5-2

40 min.

M

Wp

Consolidation Worksheet at End of First Year of Ownership

Trial balance information is given for the parent and majority owned subsidiary

at the end of the first year of ownership. The differential is assigned to buildings

and equipment and goodwill. Consolidation entries and completion of a three-

part worksheet are required.

P5-34

LO 5-2

40 min.

M

Consolidation Worksheet at End of Second Year of Ownership

Trial balance information is given for the parent and majority owned subsidiary

at the end of the second year of ownership. The differential is assigned to

buildings and equipment and goodwill. Consolidation entries, a three-part

consolidation worksheet, and a balance sheet, income statement, and retained

earnings statement are required.

P5-35

LO 5-2

50 min.

H

Comprehensive Problem: Differential Apportionment

Parent company entries, consolidation entries, and a consolidation worksheet are

required at the end of the first year of ownership for a majority-held subsidiary.

The differential is assigned to buildings and equipment and to goodwill.

P5-36

LO 5-2

55 min.

M

Comprehensive Problem: Differential Apportionment in Subsequent Period

Students must prepare equity method journal entries made by the parent during

second year after acquisition of a partially owned subsidiary involving a

differential. A three-part consolidation work paper and consolidation entries for

the end of the year are also required.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–12

P5-37

LO 5-4

45 min

H

Subsidiary with Other Comprehensive Income in Year of Acquisition

The subsidiary reports other comprehensive income during the first year of

ownership. Consolidation entries, a three-part consolidation worksheet, and a

consolidated balance sheet, income statement, and statement of comprehensive

income must be prepared.

P5-38

LO 5-4

45 min.

H

Subsidiary with Other Comprehensive Income in Year Following

Acquisition

The subsidiary reports other comprehensive income in the first and second years

of ownership. Consolidation entries and a three-part consolidation worksheet

must be prepared at the end of the second year.

P5-39

LO 5-2

50 min.

M

Comprehensive Problem: Majority-Owned Subsidiary

Parent company entries, consolidation entries, and a consolidation worksheet are

required at the end of the fifth year of ownership. Majority ownership is held and

the differential is assigned to buildings and equipment.

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–13

OTHER RESOURCES

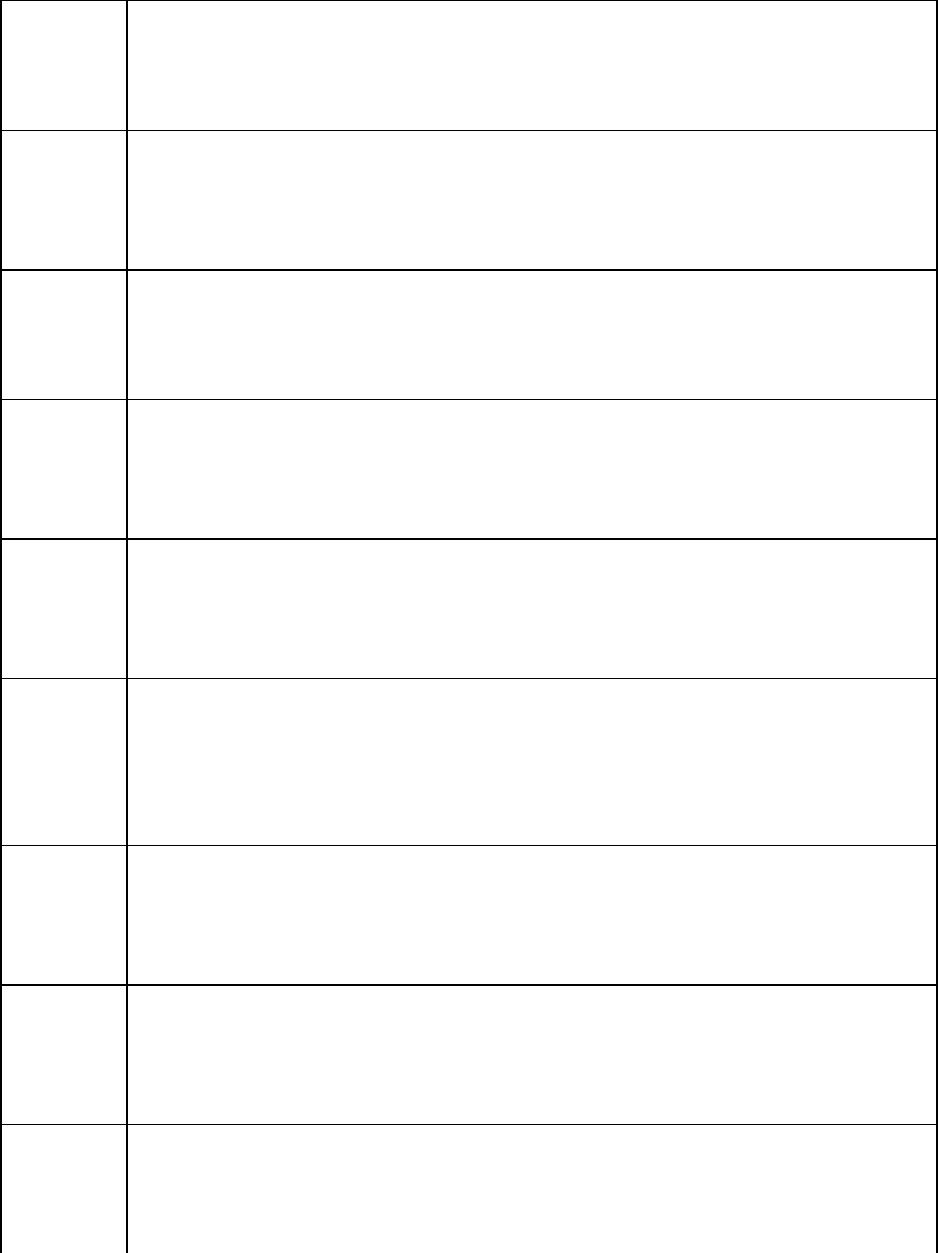

EXERCISES NO. 1 and 2 BASICS OF CONSOLIDATION

1. On January 1, 20X9, Parent Corporation acquired 90 percent of Small Corporation’s stock for

$324,000 cash. At that date, the noncontrolling interest had a fair value of $36,000. At that date

Small had $150,000 of stock outstanding and reported retained earnings of $140,000. The fair

values of all of Small’s assets approximated their fair values except one of its buildings whose

fair value exceeded its book value by $50,000. The remaining economic life for all Small’s

depreciable assets was ten years on the date of combination. The amount of the differential

assigned to goodwill is not impaired. Small reported net income of $56,000 in 20X9 and

declared no dividends.

Required

a. Give the consolidation entries needed to prepare a consolidated balance sheet immediately

after Parent acquired Small Corporation stock.

b. Give all consolidation entries needed to prepare a full set of consolidated financial statements

for 20X9.

a. Consolidation entries, January 1, 20X9:

Book Value Calculations:

NCI

10%

+

Parent Corp.

90%

=

Common

Stock

+

Retained

Earnings

Ending Book Value

29,000

261,000

150,000

140,000

Basic consolidation entry:

Common Stock

150,000

Retained Earnings

140,000

Investment in Small Corp.

261,000

NCI in NA of Small Corp.

29,000

Excess Value (Differential) Calculations:

NCI

10%

+

Parent Corp.

90%

=

Buildings

+

Goodwill

Beginning balance

7,000

63,000

50,000

20,000

Excess value (differential) reclassification entry:

Buildings

50,000

Goodwill

20,000

Investment in Small Corp.

63,000

NCI in NA of Small Corp.

7,000

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–14

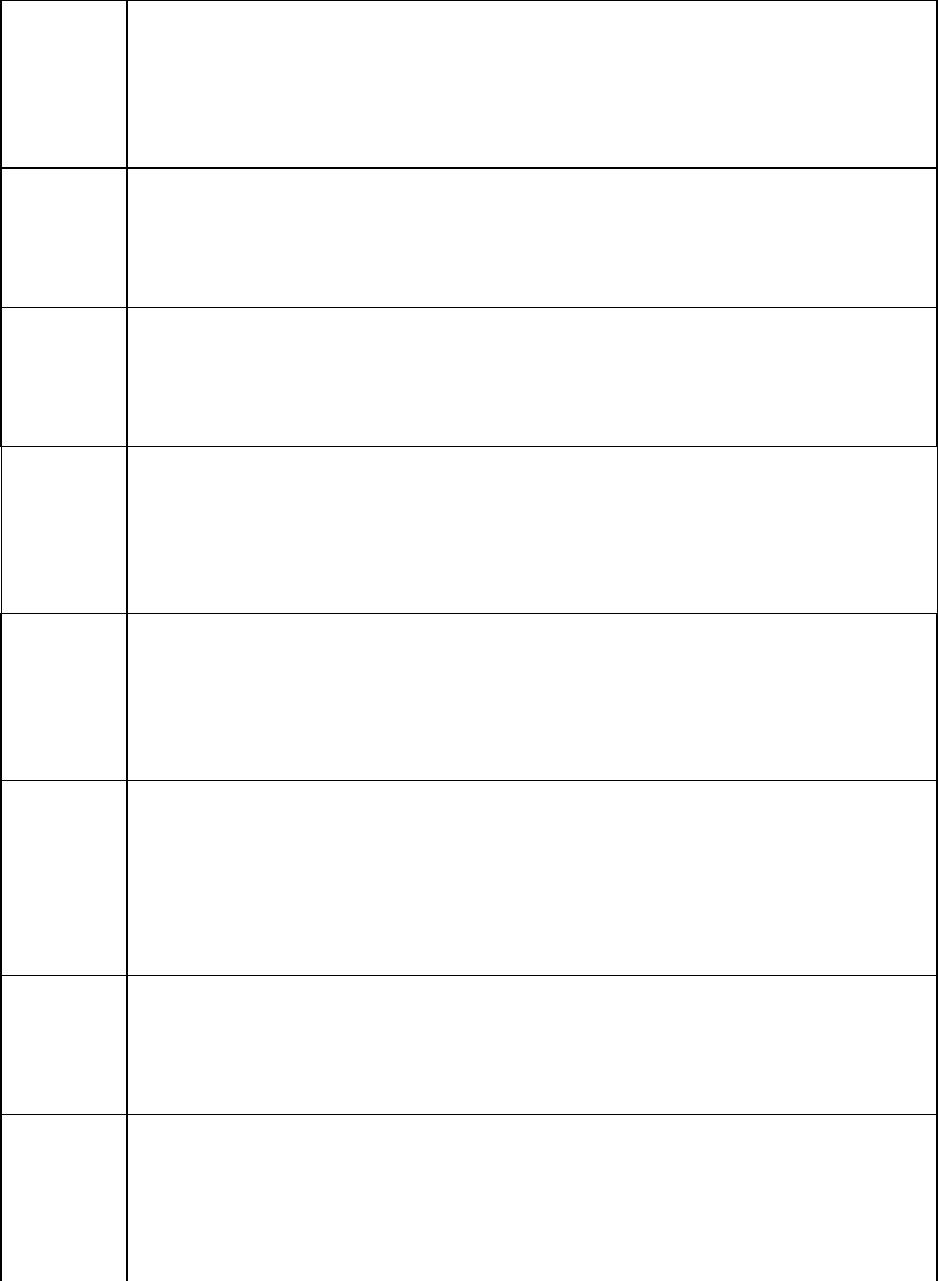

b. Consolidation entries, December 31, 20X9:

Book Value Calculations:

NCI

10%

+

Parent Corp.

90%

=

Common

Stock

+

Retained

Earnings

Beginning Book

Value

29,000

261,000

150,000

140,000

+ Net Income

5,600

50,400

56,000

Ending Book Value

34,600

311,400

150,000

196,000

Basic consolidation entry:

Common Stock

150,000

Retained Earnings

140,000

Income from Small Corp.

50,400

NCI in NI of Small Corp.

5,600

Investment in Small Corp.

311,400

NCI in NA of Small Corp.

34,600

Excess Value (Differential) Calculations:

NCI

10%

+

Parent

Corp.

90%

=

Buildings

+

Accumulated

Depreciation

+

Goodwill

Beginning balance

7,000

63,000

50,000

0

20,000

Changes

(500)

(4,500)

(5,000)

Ending balance

6,500

58,500

50,000

(5,000)

20,000

Amortized excess value reclassification entry:

Depreciation Expense

5,000

Income from Small Corp.

4,500

NCI in NI of Small Corp.

500

Excess value (differential) reclassification entry:

Buildings

50,000

Goodwill

20,000

Accumulated Depreciation

5,000

Investment in Small Corp.

58,500

NCI in NA of Small Corp.

6,500

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–15

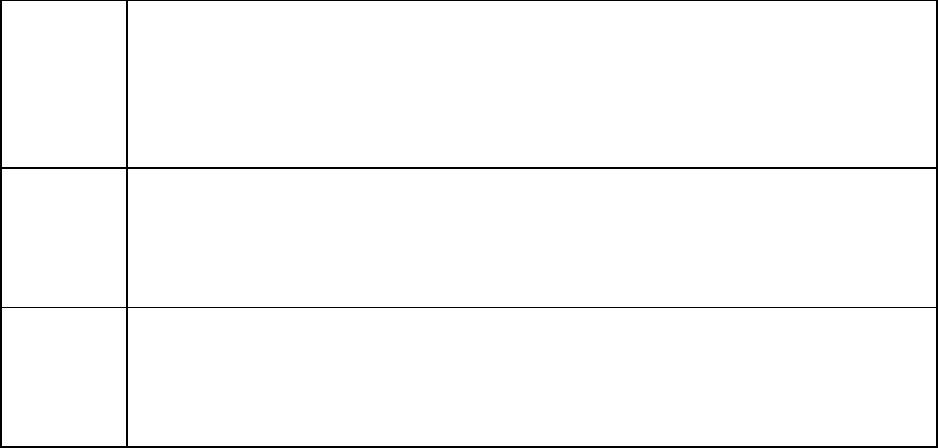

2. Parent Corporation acquired 75 percent of Signature Company’s voting stock on January 1,

20X9, at underlying book value. The fair value of the noncontrolling interest was equal to 20

percent of the book value of Signature at that date. Parent uses the fully adjusted equity method

in accounting for its ownership of Signature during 20X9. On December 31, 20X9, the trial

balances of the two companies are as follows:

Required:

a. Give all consolidation entries required as of December 31, 20X9, to prepare consolidated

financial statements.

b. Prepare a three-part consolidation worksheet.

c. Prepare a consolidated balance sheet, income statement, and retained earnings statement for

20X9.

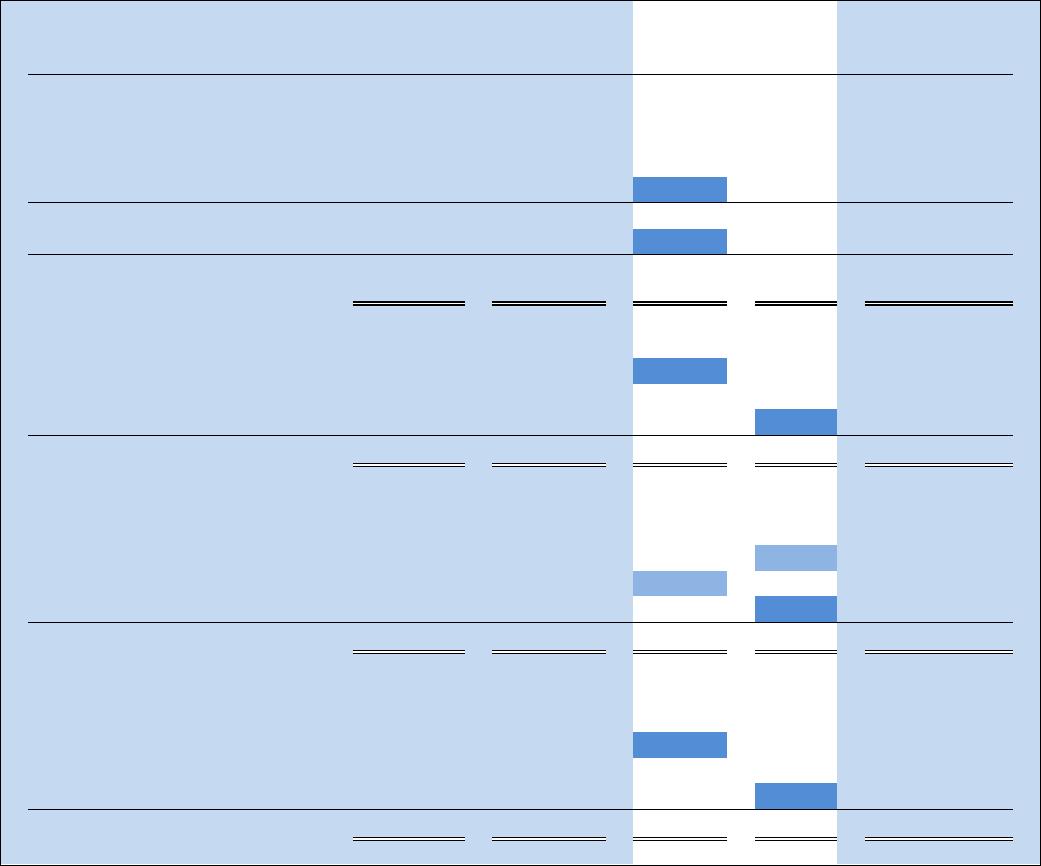

Parent Corporation Signature Company

Item Debit Credit Debit Credit

Current Assets 125,250 75,000

Depreciable Assets 250,000 180,000

Investment in Signature Co. Stock 71,250

Depreciation Expense 35,000 18,000

Other Expenses 90,000 60,000

Dividends Declared 30,000 12,000

Accumulated Depreciation 75,000 60,000

Current Liabilities 75,000 25,000

Long-Term Debt 50,000 75,000

Common Stock 100,000 50,000

Retained Earnings 135,000 35,000

Sales 150,000 100,000

Income from Subsidiary 16,500

601,500 601,500 345,000 345,000

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–16

a)

Book Value Calculations:

NCI

25%

+

Parent Corp.

75%

=

Common

Stock

+

Retained

Earnings

Beginning Book

Value

21,250

63,750

50,000

35,000

+ Net Income

5,500

16,500

22,000

– Dividends

(3,000)

(9,000)

(12,000)

Ending Book Value

23,750

71,250

50,000

45,000

Basic consolidation entry:

Common Stock

50,000

Retained Earnings

35,000

Income from Signature Co.

16,500

NCI in NI of Signature Co.

5,500

Dividends declared

12,000

Investment in Signature Co.

71,250

NCI in NA of Signature Co.

23,750

Optional accumulated depreciation consolidation

entry:

Accumulated Depreciation

42,000

Depreciable Assets

42,000

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–17

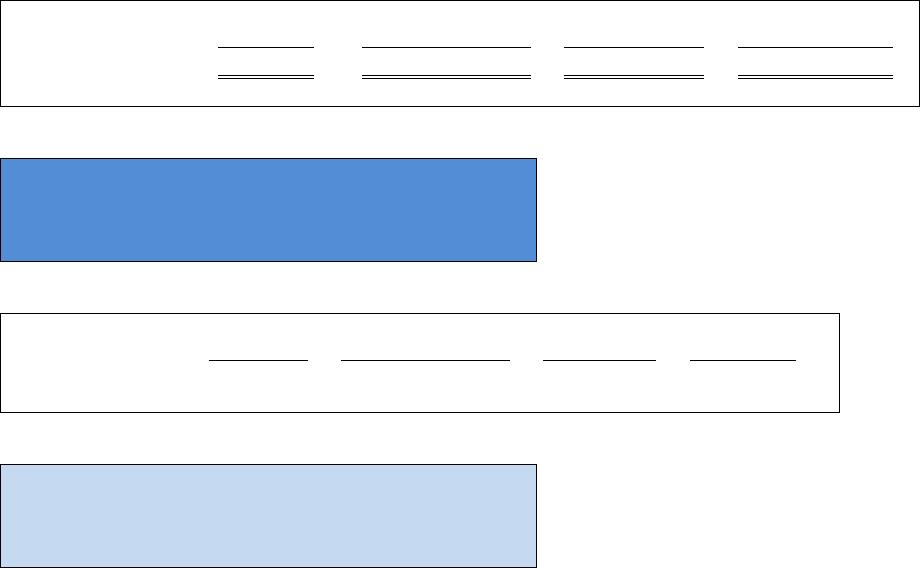

b)

Parent

Corp.

Signature

Co.

Consolidation

Entries

DR

CR

Consolidated

Income Statement

Sales

150,000

100,000

250,000

Less: Depreciation Expense

(35,000)

(18,000)

(53,000)

Less: Other Expenses

(90,000)

(60,000)

(150,000)

Income from Signature Co.

16,500

0

16,500

0

Consolidated Net Income

41,500

22,000

16,500

0

47,000

NCI in Net Income

5,500

(5,500)

Controlling Interest in Net

Income

41,500

22,000

22,000

0

41,500

Statement of Retained Earnings

Beginning Balance

135,000

35,000

35,000

135,000

Net Income

41,500

22,000

22,000

0

41,500

Less: Dividends Declared

(30,000)

(12,000)

12,000

(30,000)

Ending Balance

146,500

45,000

57,000

12,000

146,500

Balance Sheet

Current Assets

125,250

75,000

200,250

Depreciable Assets

250,000

180,000

42,000

388,000

Less: Accumulated Depreciation

(75,000)

(60,000)

42,000

(93,000)

Investment in Signature Co.

71,250

0

71,250

0

Total Assets

371,500

195,000

18,000

89,250

495,250

Current Liabilities

75,000

25,000

100,000

Long-Term Debt

50,000

75,000

125,000

Common Stock

100,000

50,000

50,000

100,000

Retained Earnings

146,500

45,000

57,000

12,000

146,500

NCI in NA of Signature Co.

23,750

23,750

Total Liabilities & Equity

371,500

195,000

107,000

35,750

495,250

Chapter 05 – CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED SUBSIDIARIES

5–18

c)

Parent Corporation and Subsidiary

Consolidated Balance Sheet

December 31, 20X9

Current Assets

$200,250

Depreciable Assets

$388,000

Less: Accumulated Depreciation

(93,000)

295,000

Total Assets

$495,250

Current Liabilities

$100,000

Long-Term Debt

125,000

Stockholders’ Equity

Controlling Interest

Common Stock

$100,000

Retained Earnings

146,500

Total Controlling Interest

$246,500

Noncontrolling Interest

23,750

Total Stockholders’ Equity

270,250

Total Liabilities and Stockholders’ Equity

$495,250

Sales $250,000

Depreciation $53,000

Other Expenses 150,000

Total Expenses (203,000)

Consolidated Net Income $47,000

Income to Noncontrolling Interest (5,500)

Income to Controlling Interest $41,500

Parent Corporation and Subsidiary

Consolidated Income Statement

Year Ended December 31, 20X9

Retained Earnings, January 1, 20X9 $135,000

Income to Controlling Interest, 20X9 41,500

$176,500

Dividends Declared, 20X9 (30,000)

Retained Earnings, December 31, 20X9 $146,500

Proud Corporation and Subsidiary

Consolidated Retained Earnings Statement

Year Ended December 31, 20X9