Burrough Corporation paid $80,000 to acquire all of Helyar Company’s net assets.

Helyar reported assets with a book value of $60,000 and fair value of $98,000 and

liabilities with a book value and fair value of $23,000 on the date of combination.

Burrough also paid $3,000 to a search firm for finder’s fees related to the acquisition.

What amount will be recorded as goodwill by Burrough Corporation while recording its

investment in Helyar?

A. $0

B. $5,000

C. $8,000

D. $13,000

Unrestricted current funds of a private university designated by the governing board for

a specific future purpose should be reported as part of:

A. unrestricted net assets.

B. temporarily restricted net assets.

C. board-restricted net assets.

D. term endowments.

Small-Town Retail owns 70 percent of Supplier Corporation’s common stock. For the

current financial year, Small-Town and Supplier reported sales of $450,000 and

$300,000 and expenses of $290,000 and $240,000, respectively.

Based on the preceding information, what is the amount of net income to be reported in

the consolidated income statement for the year under the proprietary theory approach?

A. $210,000

B. $202,000

C. $160,000

D. $200,000

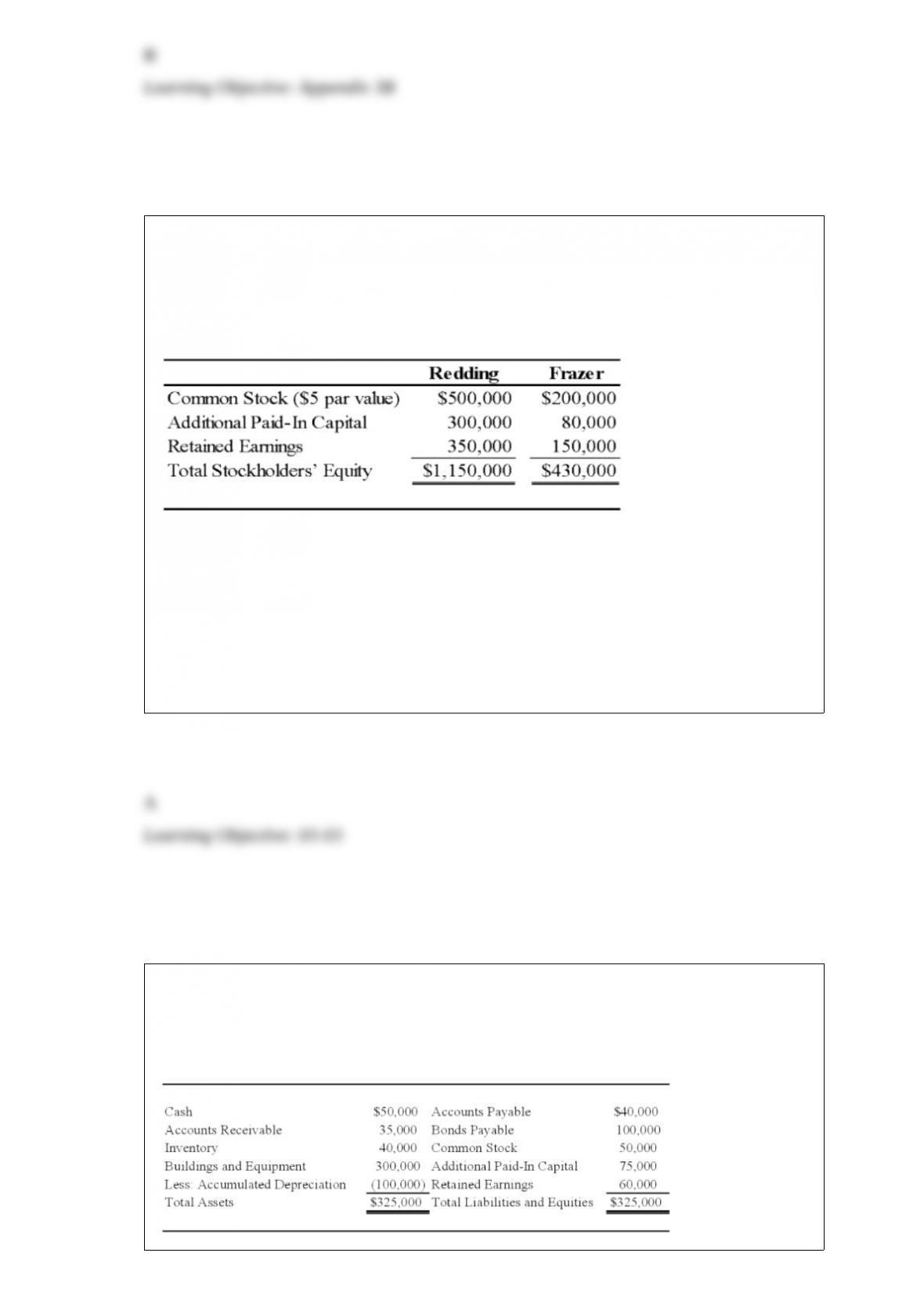

On January 3, 20X9, Redding Company acquired 80 percent of Frazer Corporation’s

common stock for $344,000 in cash. At the acquisition date, the book values and fair

values of Frazer’s assets and liabilities were equal, and the fair value of the

noncontrolling interest was equal to 20 percent of the total book value of Frazer. The

stockholders’ equity accounts of the two companies at the acquisition date are:

Noncontrolling interest was assigned income of $11,000 in Redding’s consolidated

income statement for 20X9.

Based on the preceding information, what amount will be assigned to the

noncontrolling interest on January 3, 20X9, in the consolidated balance sheet?

A. $86,000

B. $44,000

C. $68,800

D. $50,000

Cinema Company acquired 70 percent of Movie Corporation’s shares on December 31,

20X5, at underlying book value of $98,000. At that date, the fair value of the

noncontrolling interest was equal to 30 percent of the book value of Movie Corporation.

Movie’s balance sheet on January 1, 20X8, contained the following balances:

On January 1, 20X8, Movie acquired 5,000 of its own $2 par value common shares

from Nonaffiliated Corporation for $6 per share.

Based on the preceding information, what is the increase in the book value of the equity

attributable to the parent as a result of the repurchase of shares by Movie Corporation?

A. $19,375

B. $6,125

C. $2,625

D. $9,000

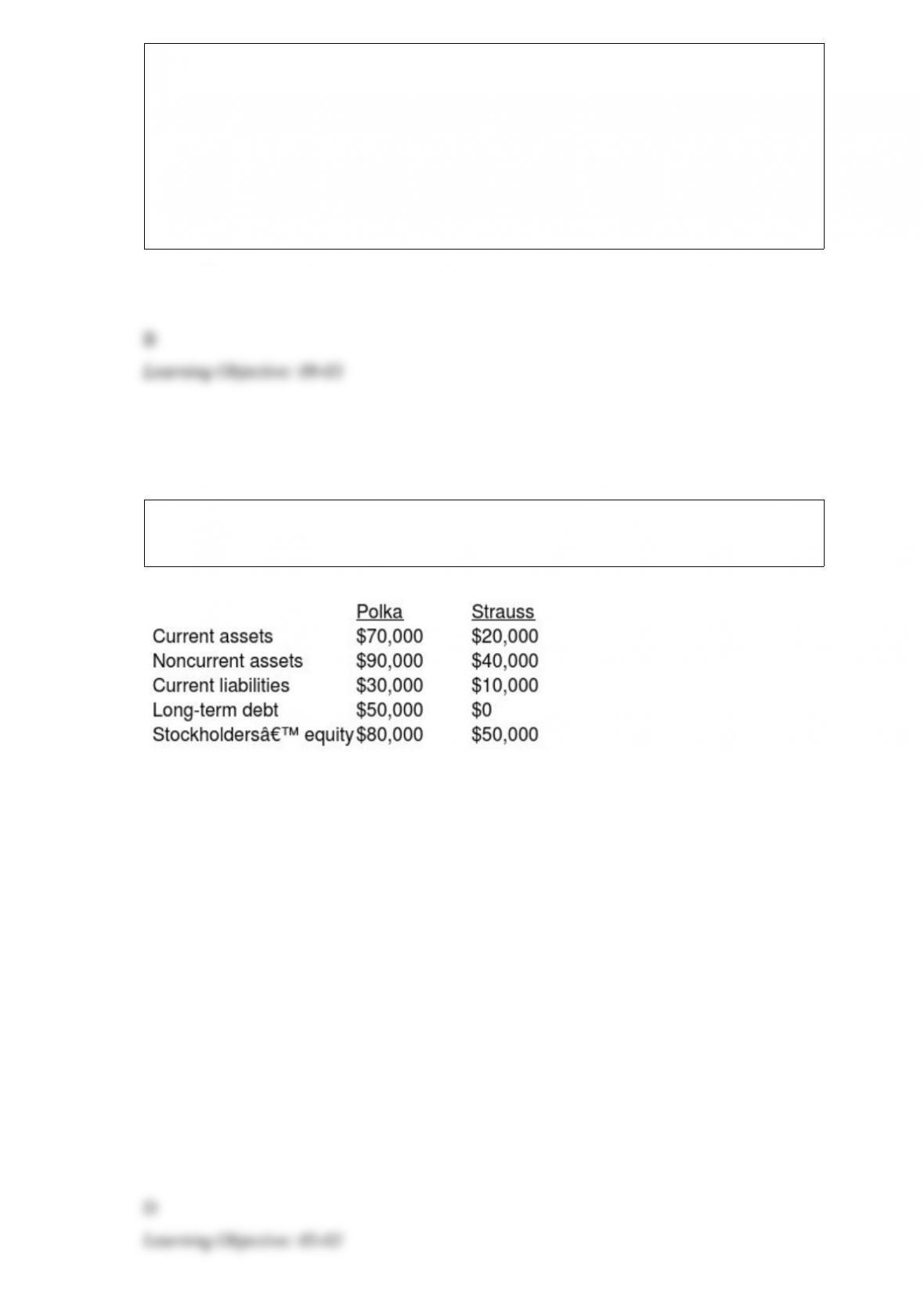

On January 1, 20X6, Polka Co. (Polka) and Strauss Co. (Strauss) had condensed

balance sheets as follows:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the

outstanding common shares of Strauss. This debt is payable in ten equal annual principal

and accrued interest payments beginning December 30, 20X6. On the acquisition date, the

fair value of Strauss was $100,000, and the excess cost of the investment over Strauss’s

carrying amount of acquired net assets should be allocated 60% to inventory and 40% to

goodwill.

Noncurrent liabilities on the January 2, 20X6, consolidated balance sheet should be:

A. $109,000

B. $55,000

C. $104,000

D. $131,000

Beta Company acquired 100 percent of the voting common shares of Standard Video

Corporation, its bitter rival, by issuing bonds with a par value and fair value of

$150,000. Immediately prior to the acquisition, Beta reported total assets of $500,000,

liabilities of $280,000, and stockholders’ equity of $220,000. At that date, Standard

Video reported total assets of $400,000, liabilities of $250,000, and stockholders’ equity

of $150,000. Included in Standard’s liabilities was an account payable to Beta in the

amount of $20,000, which Beta included in its accounts receivable.

Based on the preceding information, what amount of total assets did Beta report in its

balance sheet immediately after the acquisition?

A. $500,000

B. $650,000

C. $750,000

D. $900,000

According to ASC 958, the statement of financial position of a private university

should report the excess of the university’s assets over its liabilities as:

A. fund balance.

B. unrestricted and restricted fund balance.

C. retained earnings.

D. unrestricted, temporarily restricted, and permanently restricted net assets.

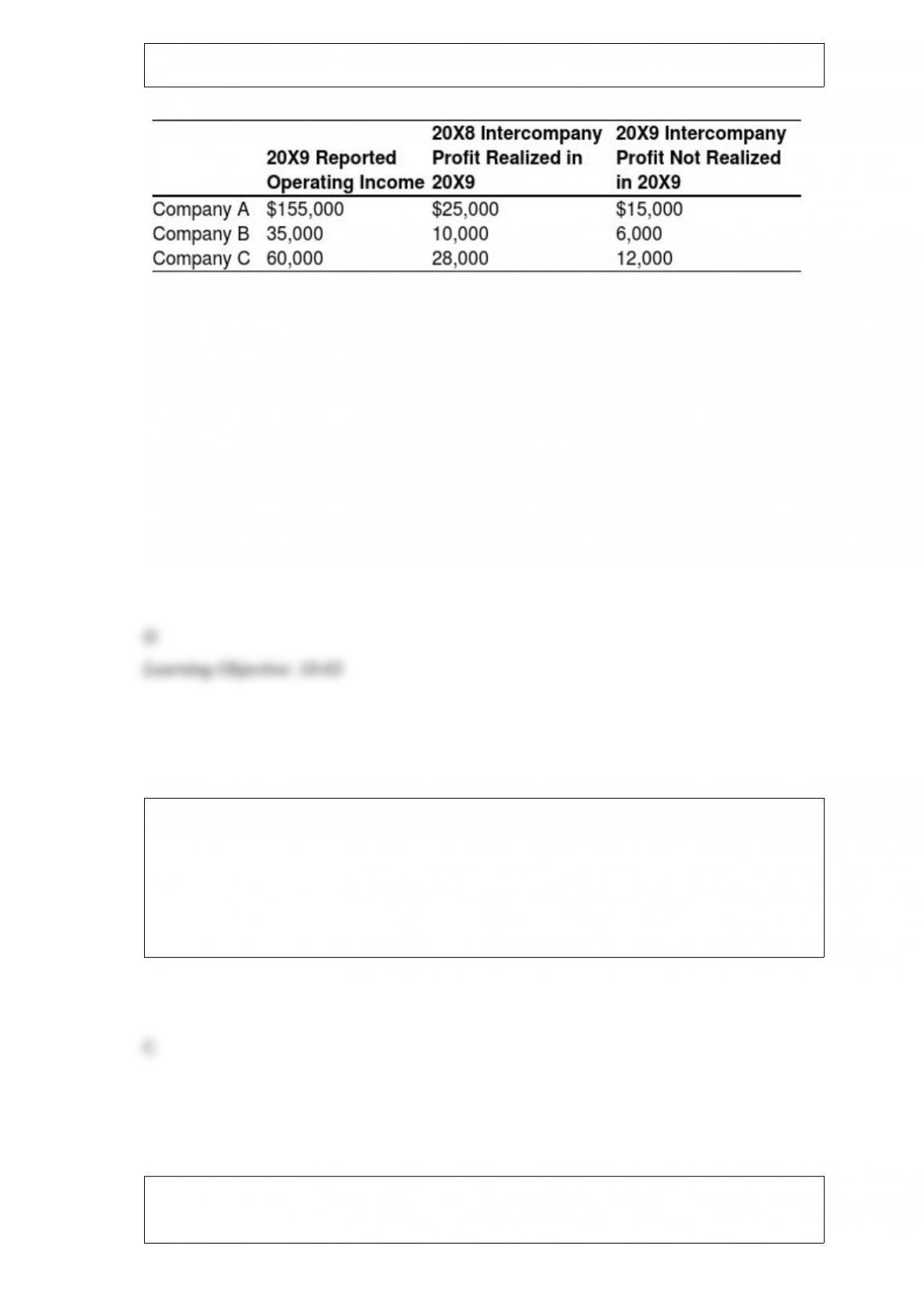

Company A owns 85 percent of Company B’s stock and 80 percent of Company C’s

stock. All acquisitions were made at book value. The fair values of noncontrolling

interests at the time of acquisition were equal to the proportionate share of the book

values of the companies. The companies file a consolidated tax return each year and in

20X9 paid a total tax of $112,000. Each company is involved in a number of

intercompany inventory transfers each period. Information on the companies’ activities

for 20X9 is as follows:

Company A does not record income tax expense on income from subsidiaries because a

consolidated tax return is filed.

Based on the information provided, what amount of income tax expense should be

assigned to Company C?

A. $24,000

B. $35,200

C. $19,200

D. $30,400

On the statement of revenues, expenditures, and changes in fund balance for a capital

projects fund, proceeds of general obligation bonds should be reported:

A. in the revenue section of the statement.

B. as a direct addition to the beginning balance of unreserved fund balance.

C. in the other financing sources (uses) section of the statement.

D. as a subtraction from construction expenditures.

Under a composition agreement,

A. creditors agree to accept less than the face amount of their claims.

B. debtors in financial difficulty transfer assets “without recourse.”

C. a creditors’ committee is initiated with a plan of settlement proposed by the debtor.

D. the debtor petitions for relief in a bankruptcy court.

The preparation of which of the following items is covered by Regulation S-K?

A. Descriptions of business

B. Pro forma disclosures

C. Schedules

D. Reports of accountants

Blue Company owns 70 percent of Black Company’s outstanding common stock. On

December 31, 20X8, Black sold equipment to Blue at a price in excess of Black’s

carrying amount, but less than its original cost. On a consolidated balance sheet at

December 31, 20X8, the carrying amount of the equipment should be reported at:

A. Blue’s original cost.

B. Black’s original cost.

C. Blue’s original cost less Black’s recorded gain.

D. Blue’s original cost less 70 percent of Black’s recorded gain.

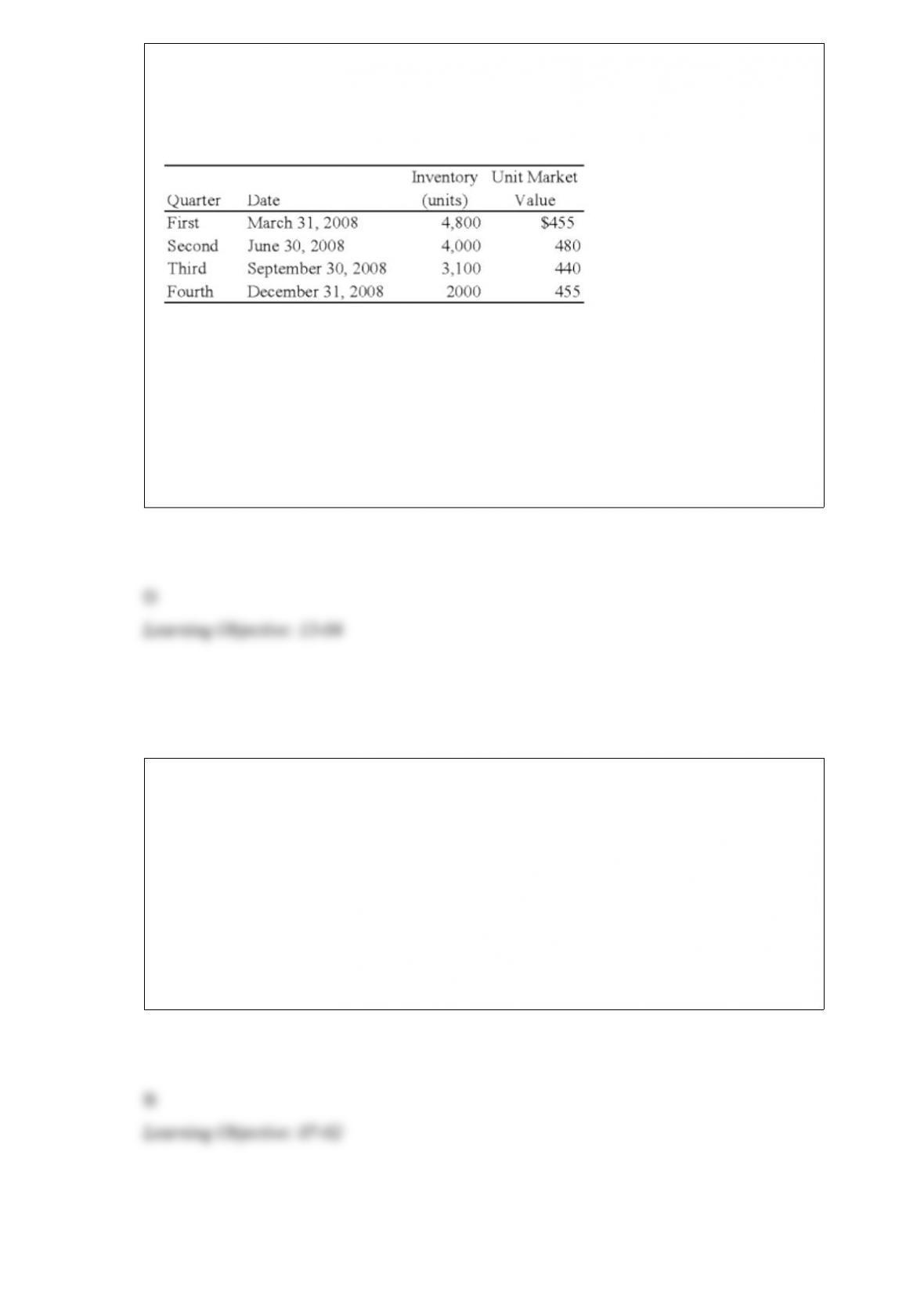

Forge Company, a calendar-year entity, had 6,000 units in its beginning inventory for

20X8. On December 31, 20X7, the units had been adjusted down to $470 per unit from

an actual cost of $510 per unit. It was the lower of cost or market. No additional units

were purchased during 20X8. The following additional information is provided for

20X8:

Forge does not have sufficient experience with the seasonal market for its inventory

units and assumes that any reductions in market value during the year will be

permanent.

Based on the preceding information, the cost of goods sold for the year 20X8, is:

A. $2,080,000

B. $1,880,000

C. $1,835,000

D. $1,910,000

A wholly owned subsidiary sold land to its parent during the year at a gain. The parent

continues to hold the land at the end of the year. The amount to be reported as

consolidated net income for the year should equal:

A. the parent’s separate operating income, plus the subsidiary’s net income.

B. the parent’s separate operating income, plus the subsidiary’s net income, minus the

intercompany gain.

C. the parent’s separate operating income, plus the subsidiary’s net income, plus the

intercompany gain.

D. the parent’s net income, plus the subsidiary’s net income, minus the intercompany

gain.

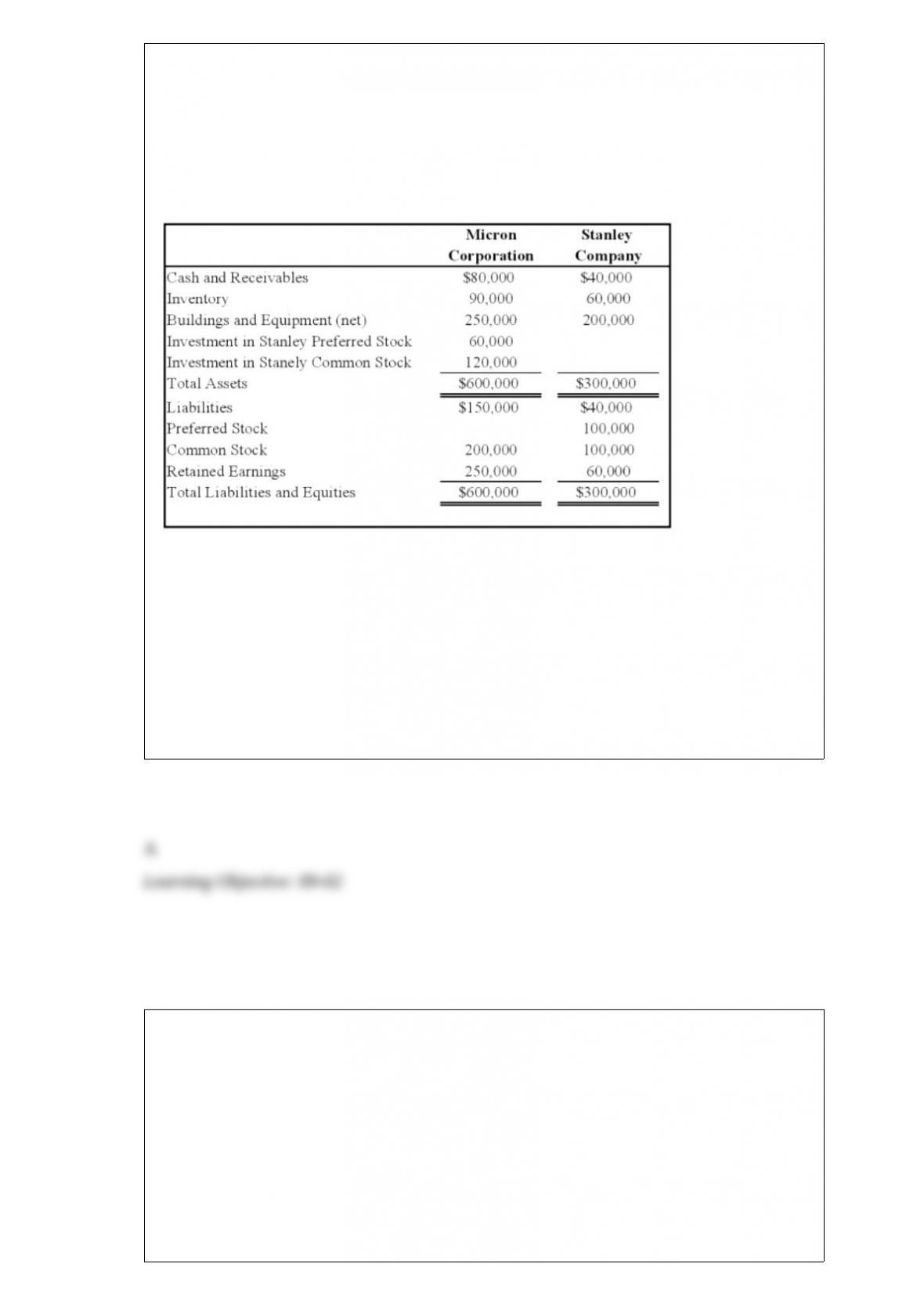

Micron Corporation owns 75 percent of the common shares and 60 percent of the

preferred shares of Stanley Company, all acquired at underlying book value on January

1, 20X8. At that date, the fair value of the noncontrolling interest in Stanley’s common

stock was equal to 25 percent of the book value of its common stock. The balance

sheets of Micron and Stanley immediately after the acquisition contained these

balances:

Stanley’s preferred stock pays a 12 percent dividend and is cumulative. For 20X8,

Stanley reports net income of $40,000 and pays no dividends. Micron reports income

from its separate operations of $75,000 and pays dividends of $30,000 during 20X8.

Based on the preceding information, what is the total stockholders’ equity reported in

the consolidated balance sheet as of January 1, 20X8?

A. $450,000

B. $530,000

C. $490,000

D. $370,000

In cases of operations located in highly inflationary economies:

A. The reporting currency of the U.S. parent—the U.S. dollar—should be used as the

foreign entity’s functional currency.

B. The foreign currency should be used as the functional currency with a footnote to the

financials displaying what the earnings would have been using the U.S. dollar as the

functional currency.

C. The foreign currency should be used as the functional currency with a single line

item—foreign translation—reporting the adjustment using the U.S. dollar as the

functional currency.

D. None of the above.

A voluntary health and welfare organization received a $300,000 contribution on April

15, 20X9, from a donor who stipulated the donation be invested permanently in stocks

and bonds. The donor further stipulated earnings from the investments be spent

according to the wishes of the governing board of the voluntary health and welfare

organization. Earnings from the investments for the year ended June 30, 20X9,

amounted to $6,000. How would the voluntary health and welfare organization report

this information for the year ended June 30, 20X9?

A. Increase in permanently restricted net assets of $306,000.

B. Increase in permanently restricted net assets of $300,000, and in temporarily

restricted net assets of $6,000.

C. Increase in permanently restricted net assets of $300,000, and in unrestricted net

assets of $6,000.

D. Increase in permanently restricted net assets of $300,000, and in board-designated

net assets of $6,000.

On January 1, 20X7, Yang Corporation acquired 25 percent of the outstanding shares of

Spiel Corporation for $100,000 cash. Spiel Company reported net income of $75,000

and paid dividends of $30,000 for both 20X7 and 20X8. The fair value of shares held

by Yang was $110,000 and $105,000 on December 31, 20X7 and 20X8 respectively.

Based on the preceding information, what amount will be reported by Yang as balance

in investment in Spiel on December 31, 20X8, if it used the equity method of

accounting?

A. $108,250

B. $118,750

C. $100,000

D. $122,500

Investment income for not-for-profit entities may include:

I. interest from debt investments.

II. dividends from equity investments.

III. changes in the fair values of both debt and equity investments.

A. I only

B. I and II only

C. I and III only

D. I, II, and III

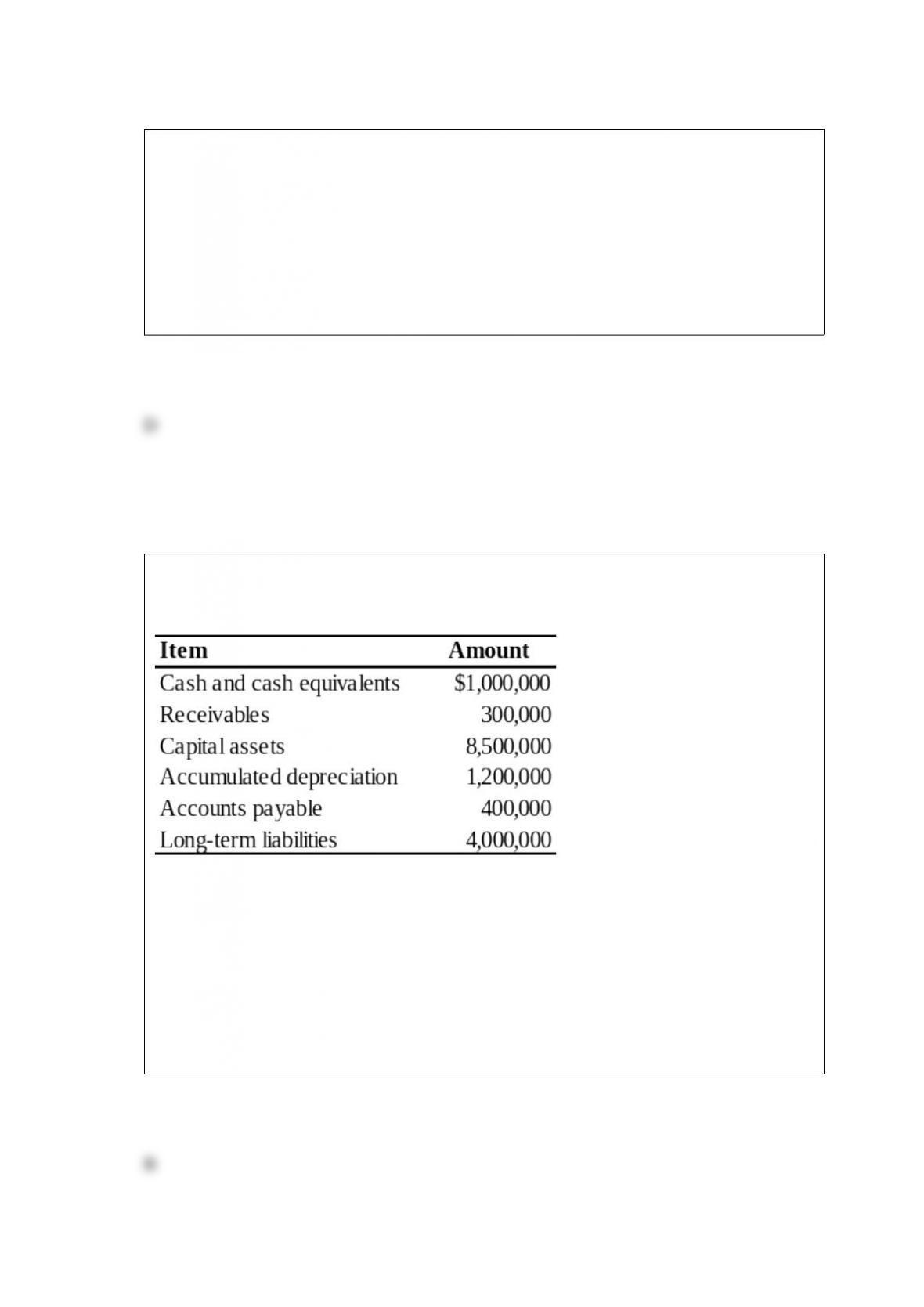

Riviera Township reported the following data for its governmental activities for the year

ended June 30, 20X9:

Additional information available is as follows:

All of the long-term debt was used to acquire capital assets. Cash of $475,000 is

restricted for debt service.

Based on the preceding information, on the statement of net assets prepared at June 30,

20X9, what amount should be reported for total net assets?

A. $2,425,000

B. $4,200,000

C. $2,900,000

D. $3,625,000

On January 1, 20X7, Yang Corporation acquired 25 percent of the outstanding shares of

Spiel Corporation for $100,000 cash. Spiel Company reported net income of $75,000

and paid dividends of $30,000 for both 20X7 and 20X8. The fair value of shares held

by Yang was $110,000 and $105,000 on December 31, 20X7 and 20X8 respectively.

Based on the preceding information, what amount will be reported by Yang as balance

in investment in Spiel on December 31, 20X8, if it used the fair value option to account

for its investment in Spiel?

A. $105,000

B. $118,750

C. $100,000

D. $122,500

What is defined as a condition in which a company is unable to meet debts as the debts

mature?

A. Deficit

B. Liability

C. Insolvency

D. Credit squeeze

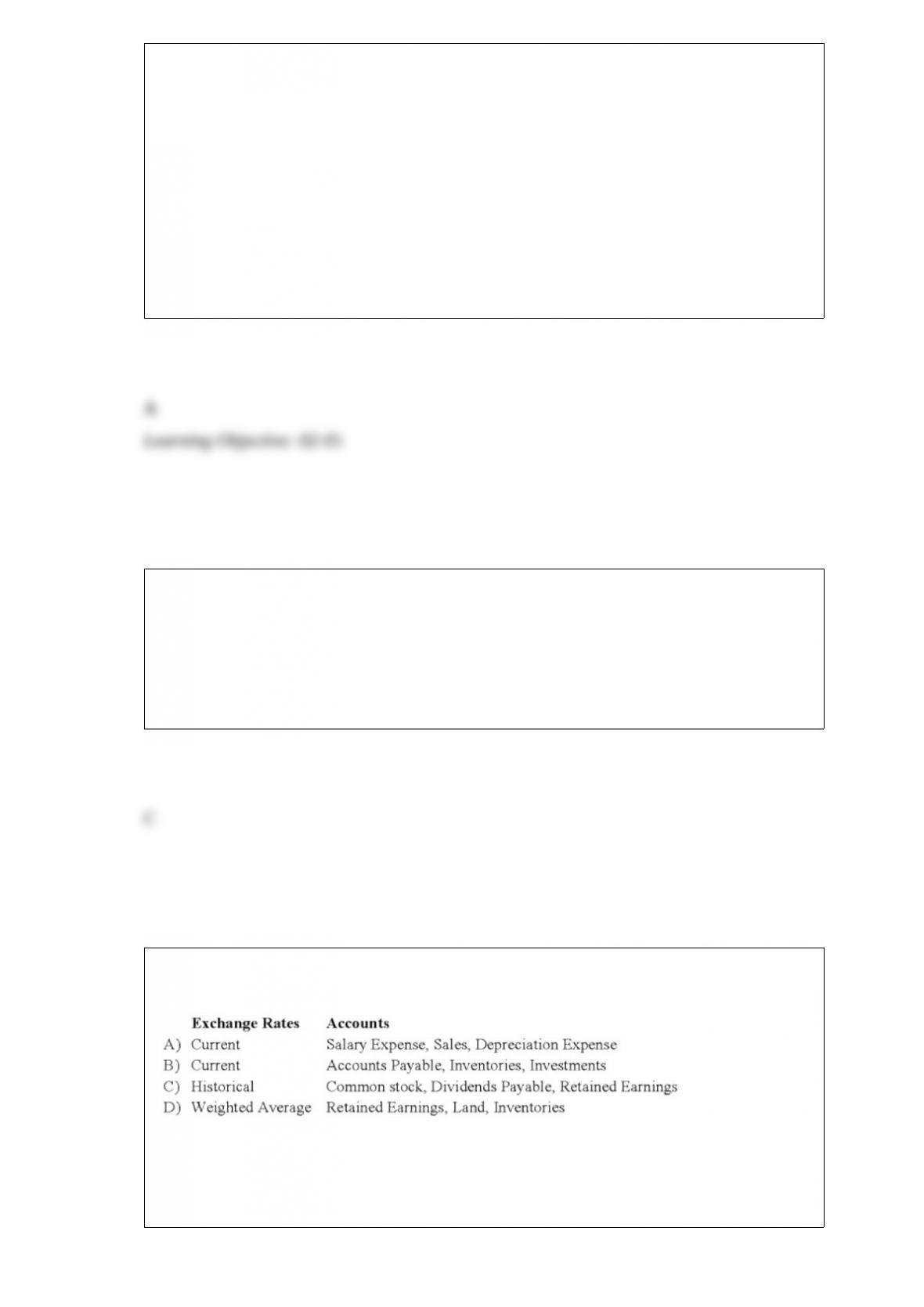

Which combination of accounts and exchange rates is correct for the translation of a

foreign entity’s financial statements from the functional currency to U.S. dollars?

A. Option A

B. Option B

C. Option C

D. Option D

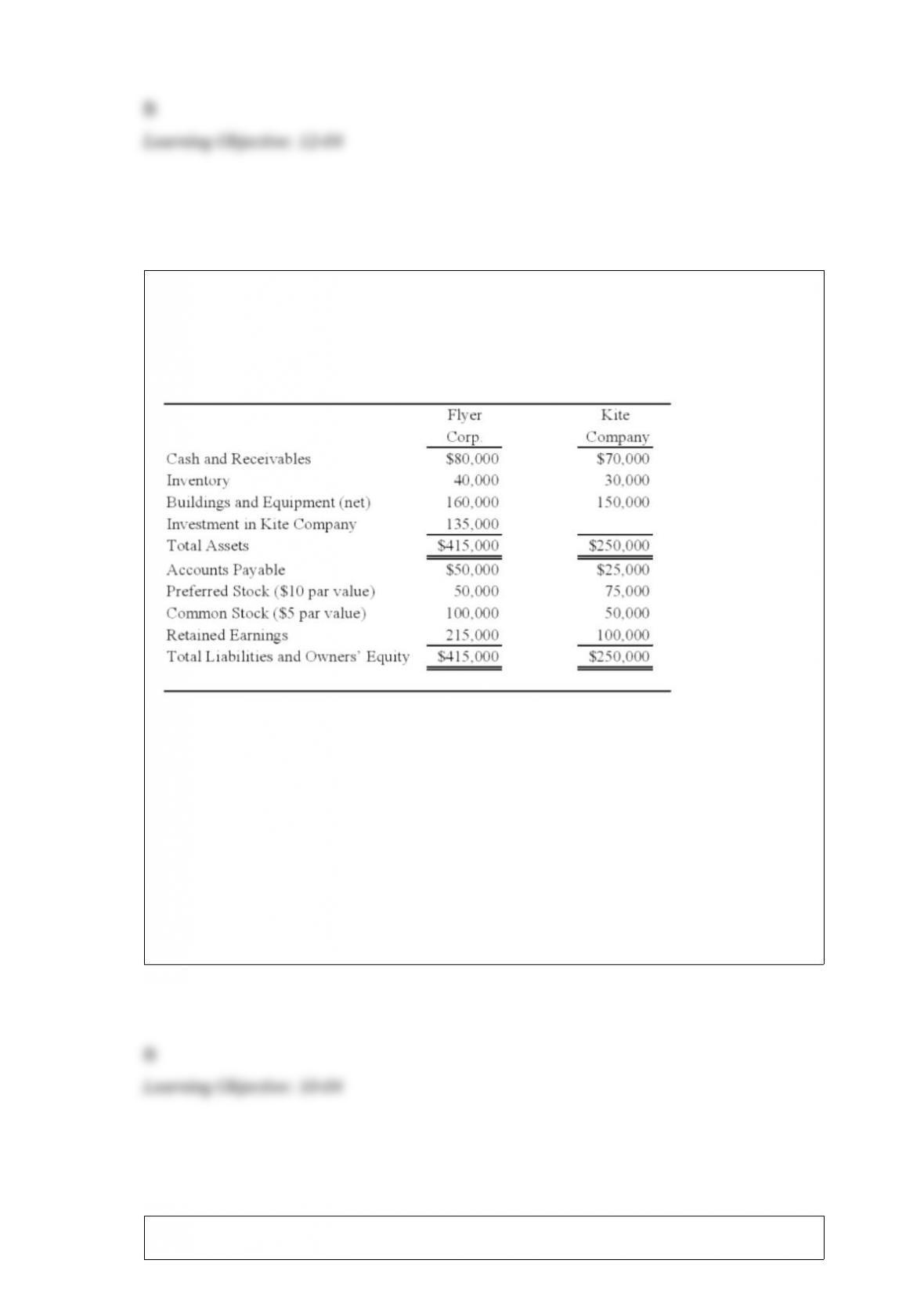

Flyer Corporation holds 90 percent of Kite Company’s common shares but none of its

preferred shares. On the date of acquisition, the fair value of the noncontrolling interest

was equal to 10 percent of the book value of Kite Company. Summary balance sheets

for the companies on December 31, 20X8, are as follows:

Flyer’s preferred pays a 8 percent annual dividend, and Kite’s preferred pays a 10

percent dividend. Kite’s preferred shares can be converted into 20,000 shares of

common stock at any time. Kite reported net income of $35,000 and paid a total of

$10,000 of dividends in 20X8. Flyer reported income from its separate operations of

$80,000 and paid total dividends of $25,000 in 20X8.

Based on the information provided, what is the diluted earnings per share for the

consolidated entity for 20X8?

A. 4.53

B. 4.33

C. 4.00

D. 3.80

The following related entries were recorded in sequence in the general fund of a

municipality:

1. ENCUMBRANCES CONTROL $12,000

BUDGETARY FUND BALANCE $12,000

2. BUDGETARY FUND BALANCE $12,000

ENCUMBRANCES CONTROL $12,000

3. Expenditures control $12,350

Vouchers payable $12,350

The sequence of entries indicates that

A. Encumbrances were anticipated but later failed to materialize and were reversed. A

liability of $12,350 was incurred.

B. An adverse event was foreseen and a reserve of $12,000 was created; later the reserve

was cancelled and a liability for the item was acknowledged.

C. An order was placed for goods or services estimated to cost $12,000; the actual cost was

$12,350 for which a liability was acknowledged upon receipt.

D. The first entry was erroneous and was reversed; a liability of $12,350 was

acknowledged.

The City of Fargo issued general obligation bonds to finance construction of a new fire

station. The bonds were issued at a discount. Which of the following is true?

I. The amount expended for the improvement must be decreased.

II. The general fund must make up the difference to the face value of the bonds.

III. A debt service fund must make up the difference to the face value of the bonds.

A. I only

B. Either I or III

C. Either II or III

D. Either I or II

Based on the information given above, what amount of investment in bonds will be

eliminated in the preparation of the 20X3 consolidated financial statements?

A. $257,248

B. $300,000

C. $395,766

D. $400,784

The CRT partnership has decided to terminate operations and to liquidate the

partnership assets. There are no partner loans, and all partners have positive capital

balances. Gains and losses on liquidation and cash distributions to partners should be

allocated as follows:

A. Option A

B. Option B

C. Option C

D. Option D

West, Inc. holds 100 percent of the common stock of Coast Company, an investment

acquired for $680,000. Immediately following the combination, West’s net assets have a

book value of $1,150,000 and a fair value of $1,390,000. The book value and the fair

value of Coast’s net assets on the date of combination are $400,000 and $550,000,

respectively. Immediately following the combination, a consolidated balance sheet is

prepared.

Based on the information given above, at what amount will West’s investment in Coast

stock be reported in the consolidated balance sheet?

A. $0

B. $400,000

C. $440,000

D. $480,000

A voluntary health and welfare organization reports pledges receivable on its statement

of financial position at the present value of the future cash collections. How is the

increase in the present value of the pledges receivable, which is due to the passage of

time, reported on the voluntary health and welfare organization’s statement of

activities?

A. As interest income-temporarily restricted.

B. As an increase in pledges receivable-temporarily restricted.

C. As an increase in contributions-temporarily restricted.

D. As an increase in deferred revenue-temporarily restricted.

The costs of enterprise fund activities are recovered

A. from special tax levies.

B. from federal or state governmental grants.

C. by user charges.

D. by private donations.

The costs of a building being constructed by a capital projects fund should be debited,

or charged, to which of the following accounts in the capital projects fund?

A. Expenditures.

B. Building.

C. Construction in Progress.

D. Other Financing Uses.