Chapter 11 – Multinational Accounting: Foreign Currency Transactions And Financial Instruments

E11-10 (continued)

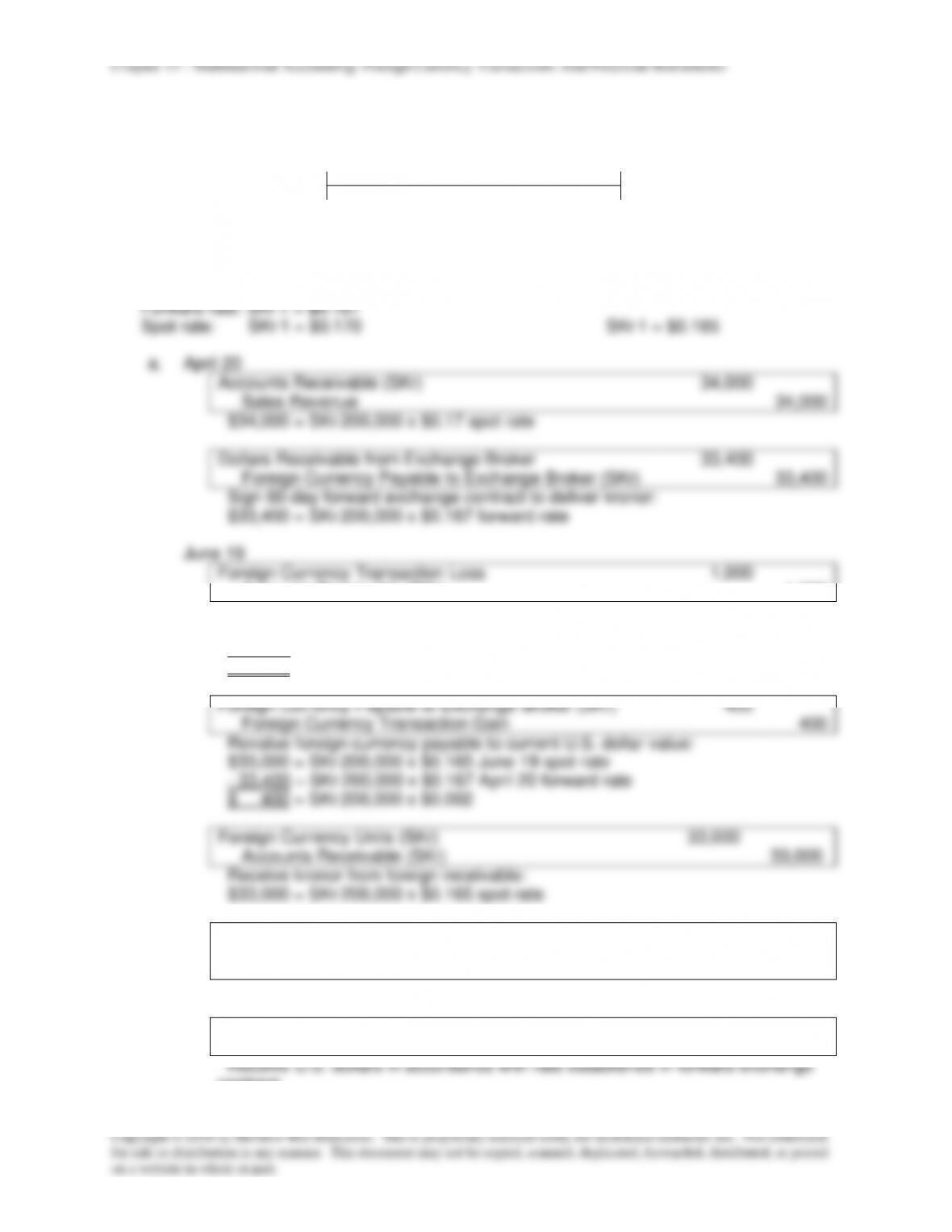

February 14, 20X8

Foreign Currency Transaction Loss

700

Foreign Currency Receivable from Exchange Broker (SFr)

700

Revalue foreign currency receivable to current equivalent U.S. dollar value:

$96,600 = SFr 140,000 x $0.69 Feb. 14, 20X8, spot rate

– 97,300 = SFr 140,000 x $0.695 Dec. 31, 20X7, forward rate

$ 700 = SFr 140,000 x ($0.69 – $0.695)

Accounts Payable (SFr)

1,400

Foreign Currency Transaction Gain

1,400

Revalue foreign currency accounts payable to current U.S. dollar value:

$96,600 = SFr 140,000 x $0.69 Feb. 14, 20X8, spot rate

– 98,000 = SFr 140,000 x $0.70 Dec. 31, 20X7, spot rate

$ 1,400 = SFr 140,000 x ($0.69 – $0.70)

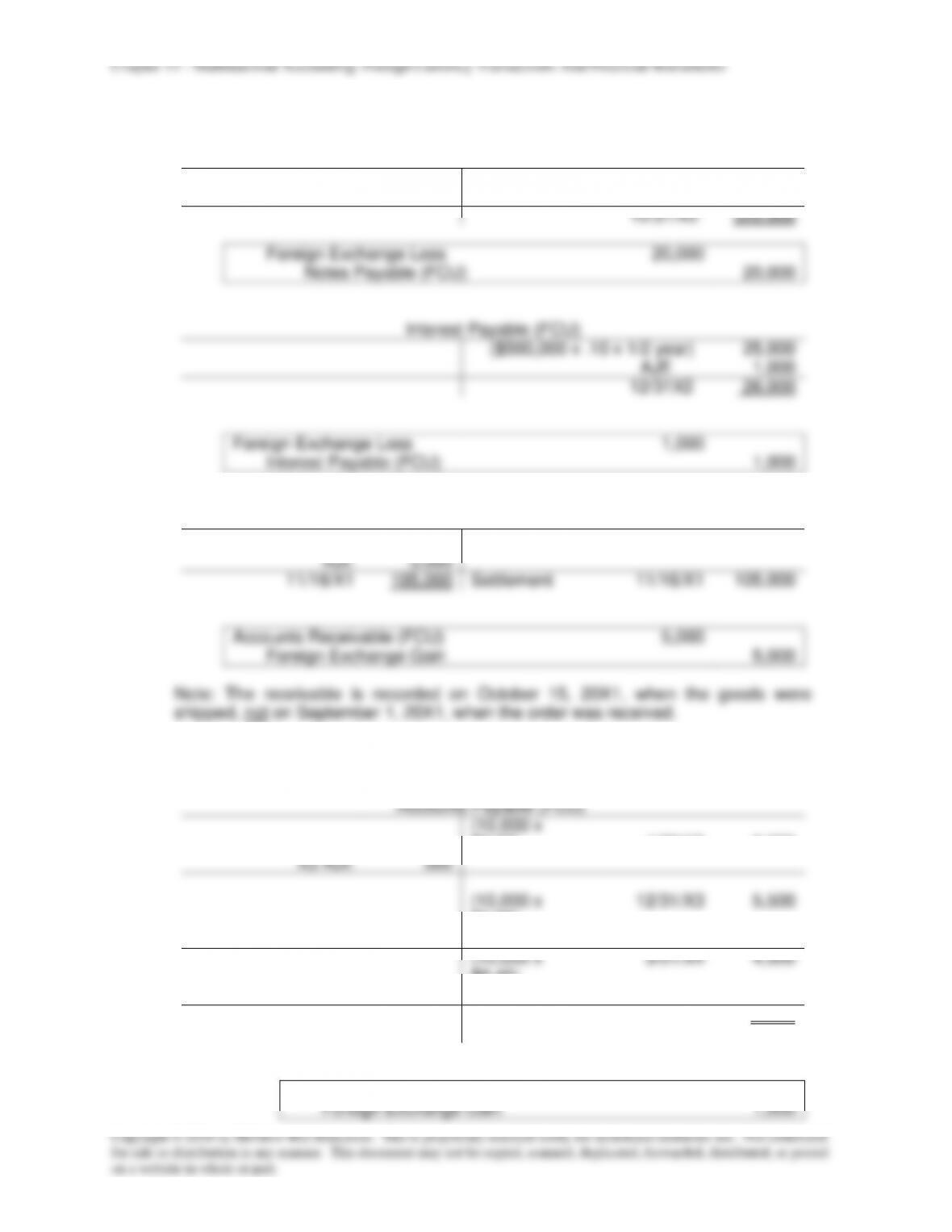

Dollars Payable to Exchange Broker ($)

93,800

Cash

93,800

Pay U.S. dollars to exchange broker for forward contract.

Foreign Currency Units (SFr)

96,600

Foreign Currency Receivable from Exchange Broker (SFr)

96,600

Receive francs from exchange broker:

$96,600 = SFr 140,000 x $0.69 spot rate

Accounts Payable (SFr)

96,600

Foreign Currency Units (SFr)

96,600

Settle foreign currency payable.

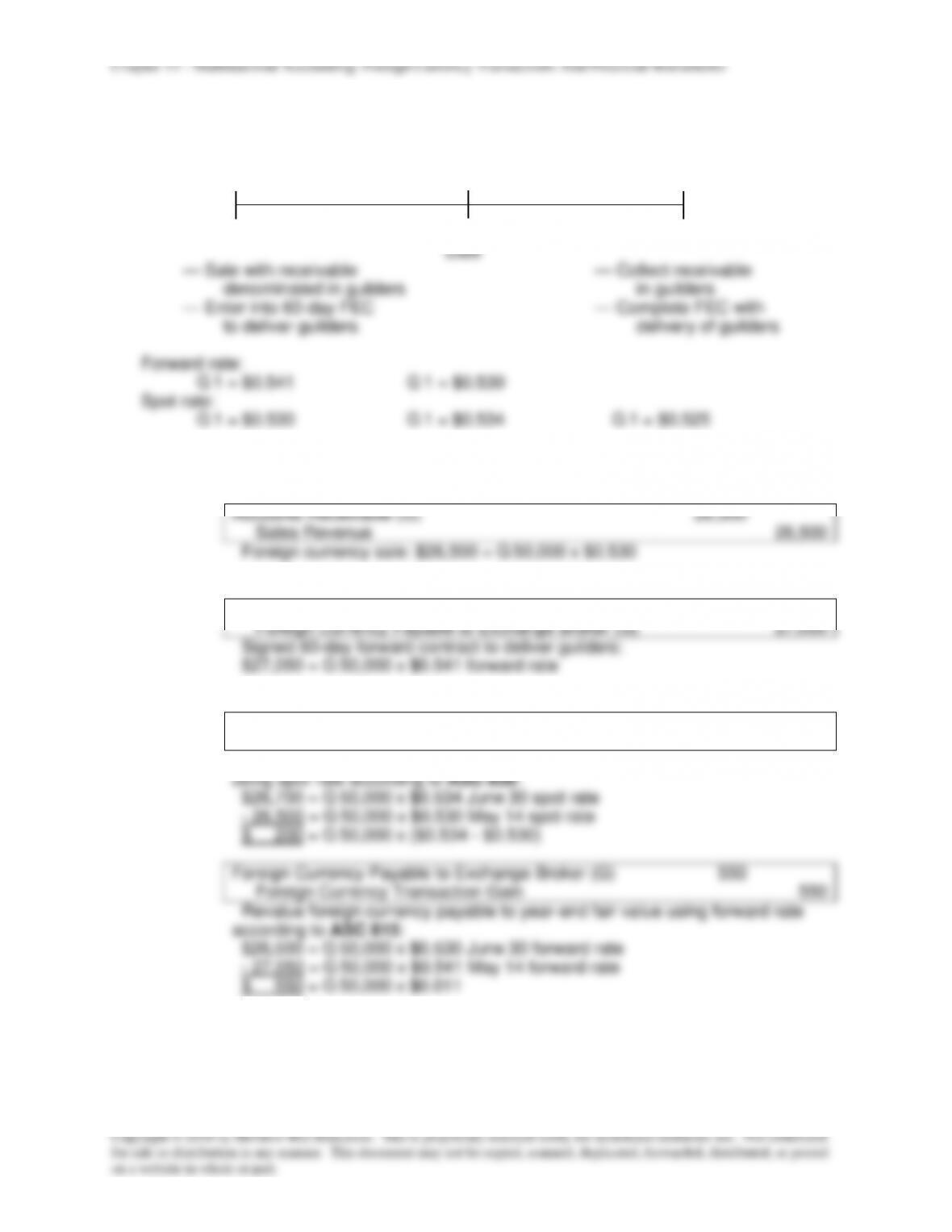

Foreign Currency Exchange Loss (with Swiss Co.)

Foreign Currency Exchange Gain (with Broker)

Net effect on income

c.

Overall effect of transactions:

20X7 Net Foreign Currency Gain

20X8 Foreign Currency Loss on receivable

20X8 Foreign Currency Transaction Gain on payable

Overall effect