On the statement of operations prepared for a private, not-for-profit hospital, patient

service revenue earned during the year is reported net of amounts for which of the

following items?

I. Contractual adjustments

II. Bad debts expense

A. I only

B. II only

C. I and II

D. Neither I nor II

Mint Corporation has several transactions with foreign entities. Each transaction is

denominated in the local currency unit of the country in which the foreign entity is

located. On November 2, 20X8, Mint sold confectionary items to a foreign company at

a price of LCU 23,000 when the direct exchange rate was 1 LCU = $1.08. The account

has not been settled as of December 31, 20X8, when the exchange rate has increased to

1 LCU = $1.10. The foreign exchange gain or loss on Mint’s records at year-end for this

transaction will be:

A. $460 loss

B. $387 loss

C. $387 gain

D. $460 gain

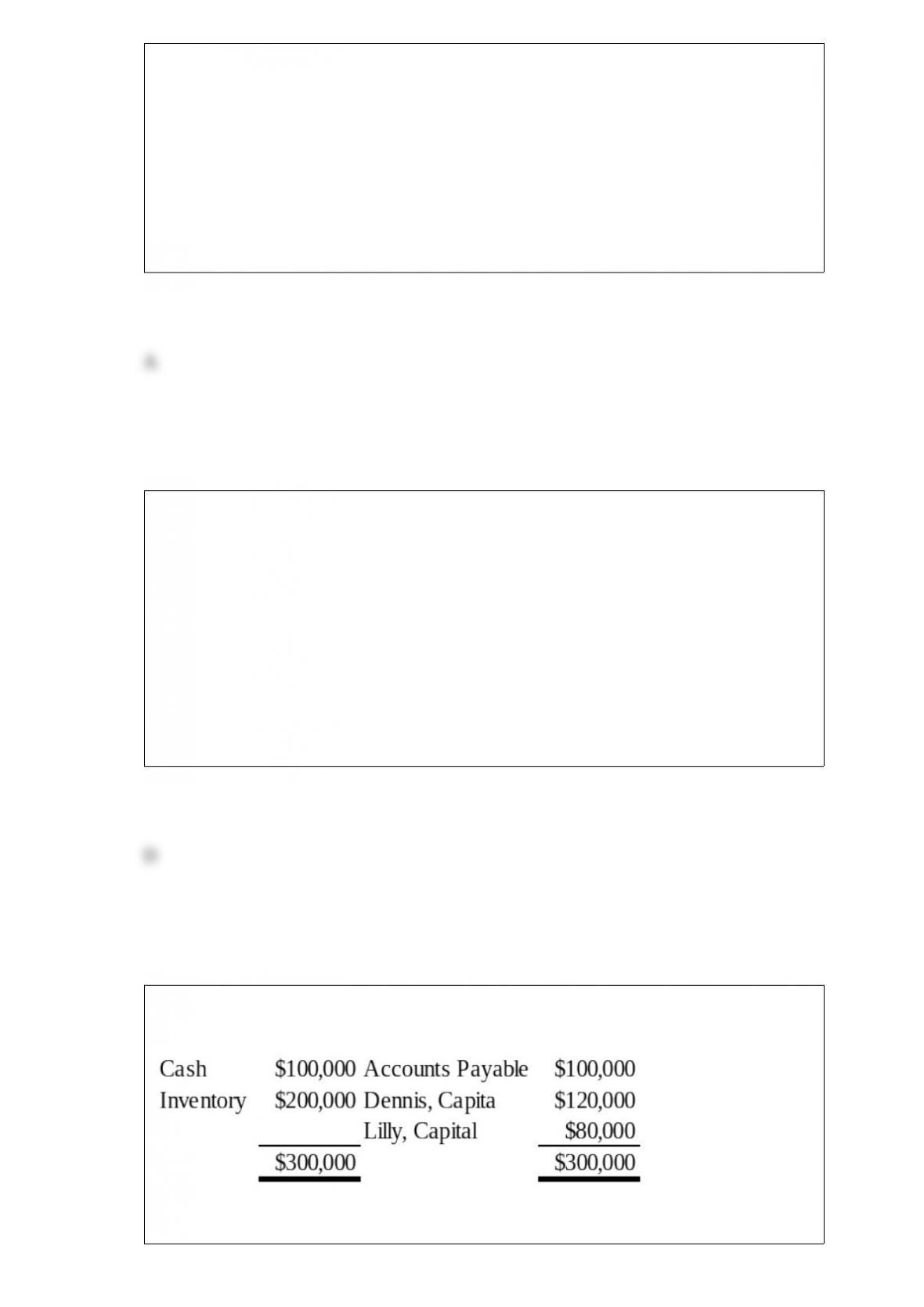

Partners Dennis and Lilly have decided to liquidate their business. The following

information is available:

Dennis and Lilly share profits and losses in a 3:2 ratio. During the first month of

liquidation, half the inventory is sold for $60,000, and $60,000 of the accounts payable

is paid. During the second month, the rest of the inventory is sold for $45,000, and the

remaining accounts payable are paid. Cash is distributed at the end of each month, and

the liquidation is completed at the end of the second month.

Refer to the information provided above. Using a safe payments schedule, how much

cash will be distributed to Dennis at the end of the second month?

A. $18,000

B. $27,000

C. $36,000

D. $60,000

James Dixon, a partner in an accounting firm, decided to withdraw from the

partnership. Dixon’s share of the partnership profits and losses was 20%. Upon

withdrawing from the partnership he was paid $74,000 in final settlement for his

interest. The total of the partners’ capital accounts before recognition of partnership

goodwill prior to Dixon’s withdrawal was $210,000. After his withdrawal the remaining

partners’ capital accounts, excluding their share of goodwill, totaled $160,000. The total

agreed upon goodwill of the firm was

A. $250,000

B. $140,000

C. $160,000

D. $120,000

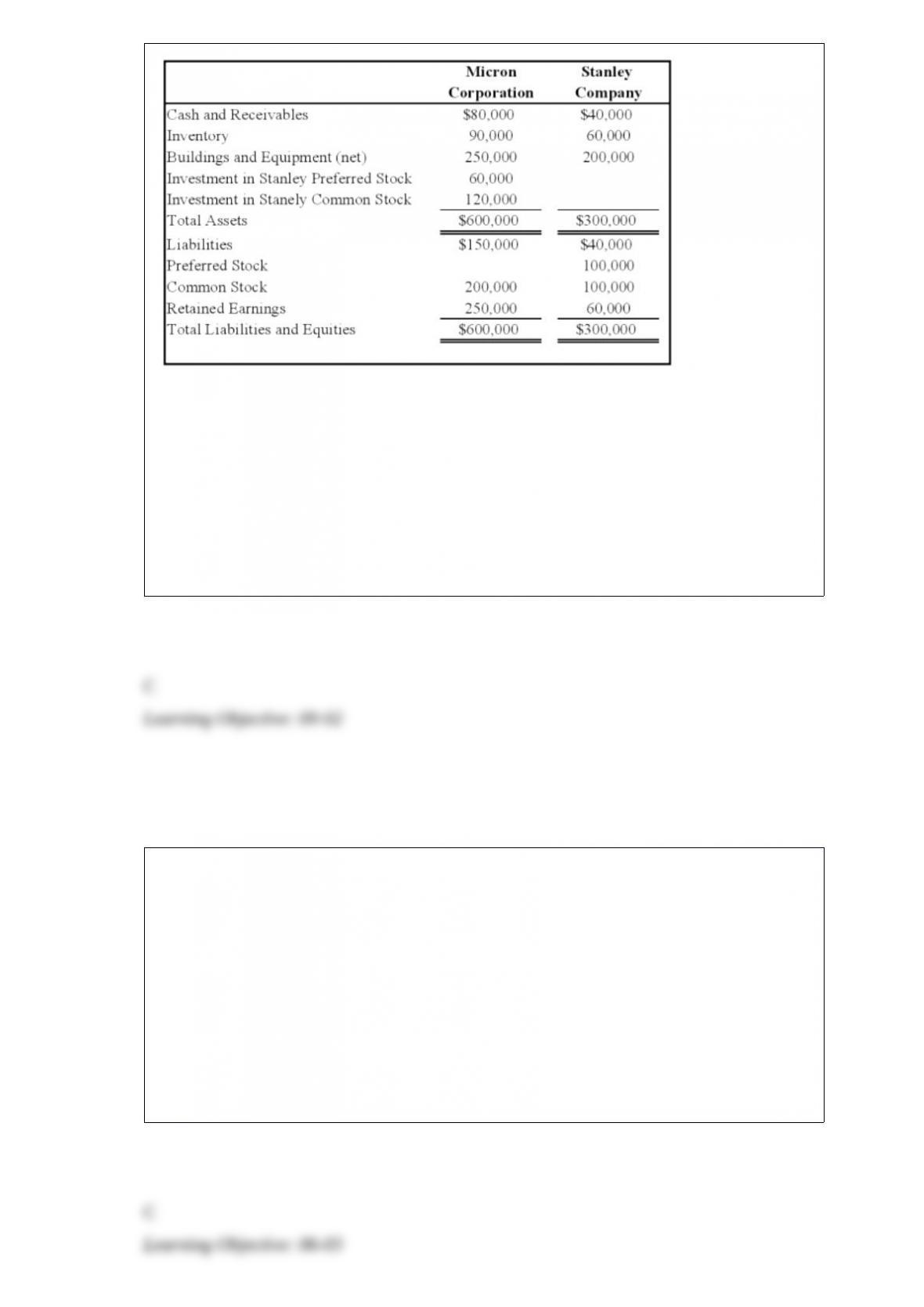

Micron Corporation owns 75 percent of the common shares and 60 percent of the

preferred shares of Stanley Company, all acquired at underlying book value on January

1, 20X8. At that date, the fair value of the noncontrolling interest in Stanley’s common

stock was equal to 25 percent of the book value of its common stock. The balance

sheets of Micron and Stanley immediately after the acquisition contained these

balances:

Stanley’s preferred stock pays a 12 percent dividend and is cumulative. For 20X8,

Stanley reports net income of $40,000 and pays no dividends. Micron reports income

from its separate operations of $75,000 and pays dividends of $30,000 during 20X8.

Based on the preceding information, what is the income assigned to the noncontrolling

interest in the 20X8 consolidated income statement?

A. $10,000

B. $7,000

C. $11,800

D. $4,800

ABC Corporation owns 75 percent of XYZ Company’s voting shares. During 20X8,

ABC produced 50,000 chairs at a cost of $79 each and sold 35,000 chairs to XYZ for

$90 each. XYZ sold 18,000 of the chairs to unaffiliated companies for $117 each prior

to December 31, 20X8, and sold the remainder in early 20X9 to unaffiliated companies

for $130 each. Both companies use perpetual inventory systems.

Based on the information given above, what amount of cost of goods sold must be

reported in the consolidated income statement for 20X8?

A. $2,765,000

B. $1,620,000

C. $1,422,000

D. $2,963,000

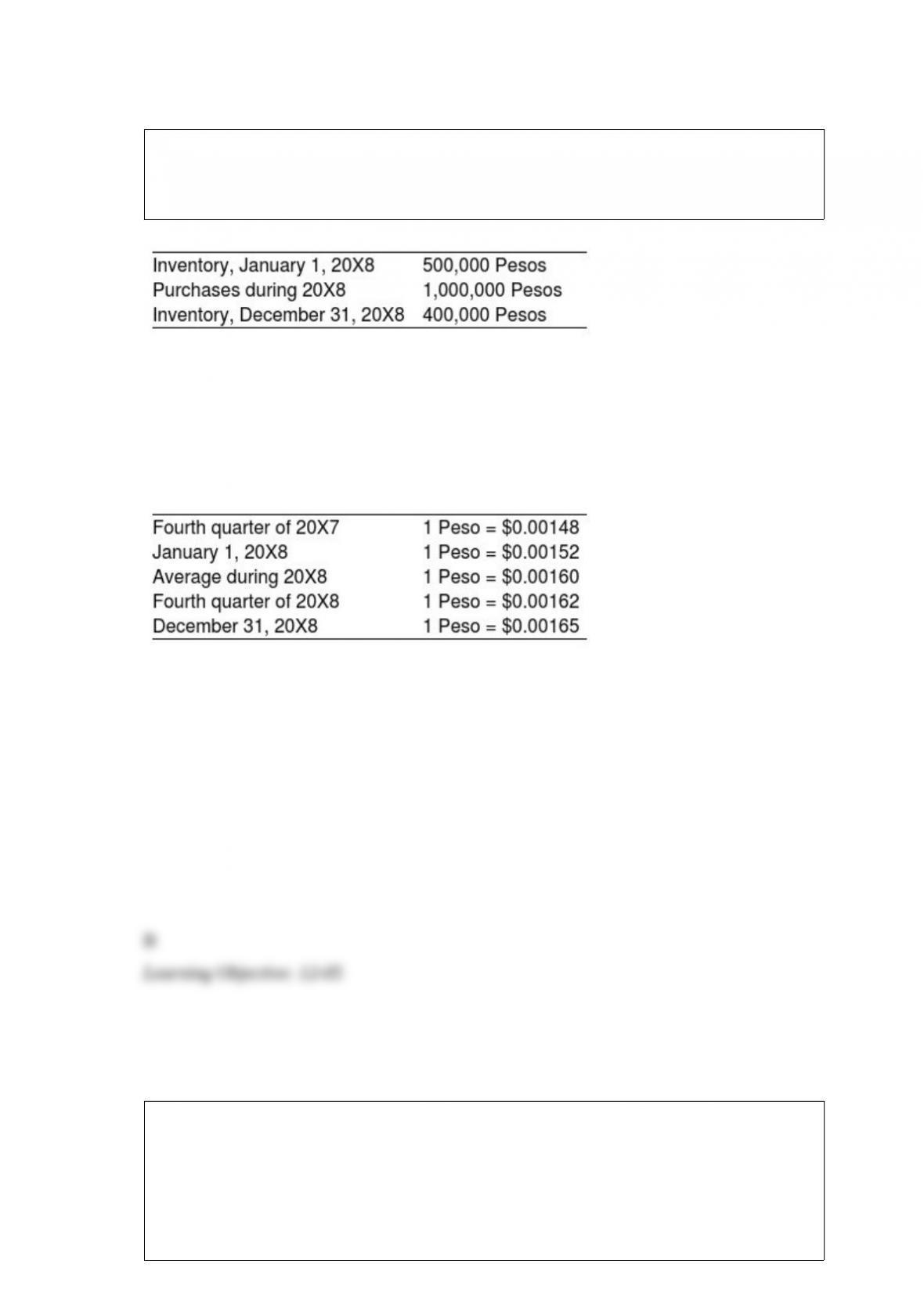

Mercury Company is a subsidiary of Neptune Company and is located in Valparaso,

Chile, where the currency is the Chilean Peso. Data on Mercury’s inventory and

purchases are as follows:

The beginning inventory was acquired during the fourth quarter of 20X7, and the ending

inventory was acquired during the fourth quarter of 20X8. Purchases were made evenly

over the year. Exchange rates were as follows:

Based on the preceding information, the translation of cost of goods sold for 20X8,

assuming that the Spanish peseta is the functional currency is:

A. $1,700.

B. $1,760.

C. $1,680.

D. $1,692.

Neptune Corporation owns 70 percent of Pluto Company’s stock. On July 1, 20X4,

Neptune sold a piece of equipment to Pluto for $56,350. Neptune had purchased this

equipment on January 1, 20X1, for $63,000. The equipment’s original 15-year

estimated total economic life remains unchanged. Both companies use straight-line

depreciation. The equipment’s residual value is considered negligible.

Based on the information provided, the gain on the sale of the equipment eliminated in

the consolidated financial statements for 20X4 is

A. $5,950.

B. $8,050

C. $10,150

D. $14,700

Barcode Corporation acquired 70% of the common stock of a Russian company on

January 1, 20X6. The goodwill associated with this acquisition was $12,520. Exchange

rates at various dates during 20X6 follow:

January 1, 20X6 1 ruble = $0.0313

December 31, 20X6 1 ruble = $0.0308

Average for 20X6 1 ruble = $0.031

Goodwill suffered an impairment of 25 percent during the year. If the functional

currency is the U.S. dollar, how much goodwill impairment loss should be reported on

Barcode’s consolidated statement of income for 20X6?

A. $3,080

B. $3,090

C. $3,100

D. $3,130

FASB has specified a “75% percent consolidated revenue test”.

Required:

a) What is the 75% test?

b) How is the 75% test impacted by the “10% Significance Rule”?

Chapter 7 of the Bankruptcy Code provides for:

I. Reorganization.

II. Liquidation.

A. I only

B. II only

C. Both I and II

D. Neither I nor II

On January 1, 20X6, Climber Corporation acquired 90 percent of Wisden Corporation

for $180,000 cash. Wisden reported net income of $30,000 and dividends of $10,000

for 20X6, 20X7, and 20X8. On January 1, 20X6, Wisden reported common stock

outstanding of $100,000 and retained earnings of $60,000, and the fair value of the

noncontrolling interest was $20,000. It held land with a book value of $30,000 and a

market value of $35,000 and equipment with a book value of $50,000 and a market

value of $60,000 at the date of combination. The remainder of the differential at

acquisition was attributable to an increase in the value of patents, which had a

remaining useful life of five years. All depreciable assets held by Wisden at the date of

acquisition had a remaining economic life of five years. Climber uses the equity method

in accounting for its investment in Wisden.

Based on the preceding information, what balance would Climber report as its

investment in Wisden at January 1, 20X8?

A. $230,400

B. $180,000

C. $234,000

D. $203,400

On January 1, 20X2, Ephraim Corporation acquired 80 percent of Lilac Corporation for

$200,000 cash. Lilac reported net income of $25,000 each year and dividends of $5,000

each year for 20X2, 20X3, and 20X4. On January 1, 20X2, Lilac reported common

stock outstanding of $160,000 and retained earnings of $40,000, and the fair value of

the noncontrolling interest was $50,000. It held land with a book value of $90,000 and a

market value of $100,000, and equipment with a book value of $40,000 and a market

value of $48,000 at the date of combination. The remainder of the differential at

acquisition was attributable to an increase in the value of patents, which had a

remaining useful life of eight years. All depreciable assets held by Lilac at the date of

acquisition had a remaining economic life of eight years. Ephraim uses the equity

method in accounting for its investment in Lilac.

Based on the preceding information, the increase in the fair value of patents held by

Lilac is

A. $10,000

B. $18,000

C. $32,000

D. $50,000

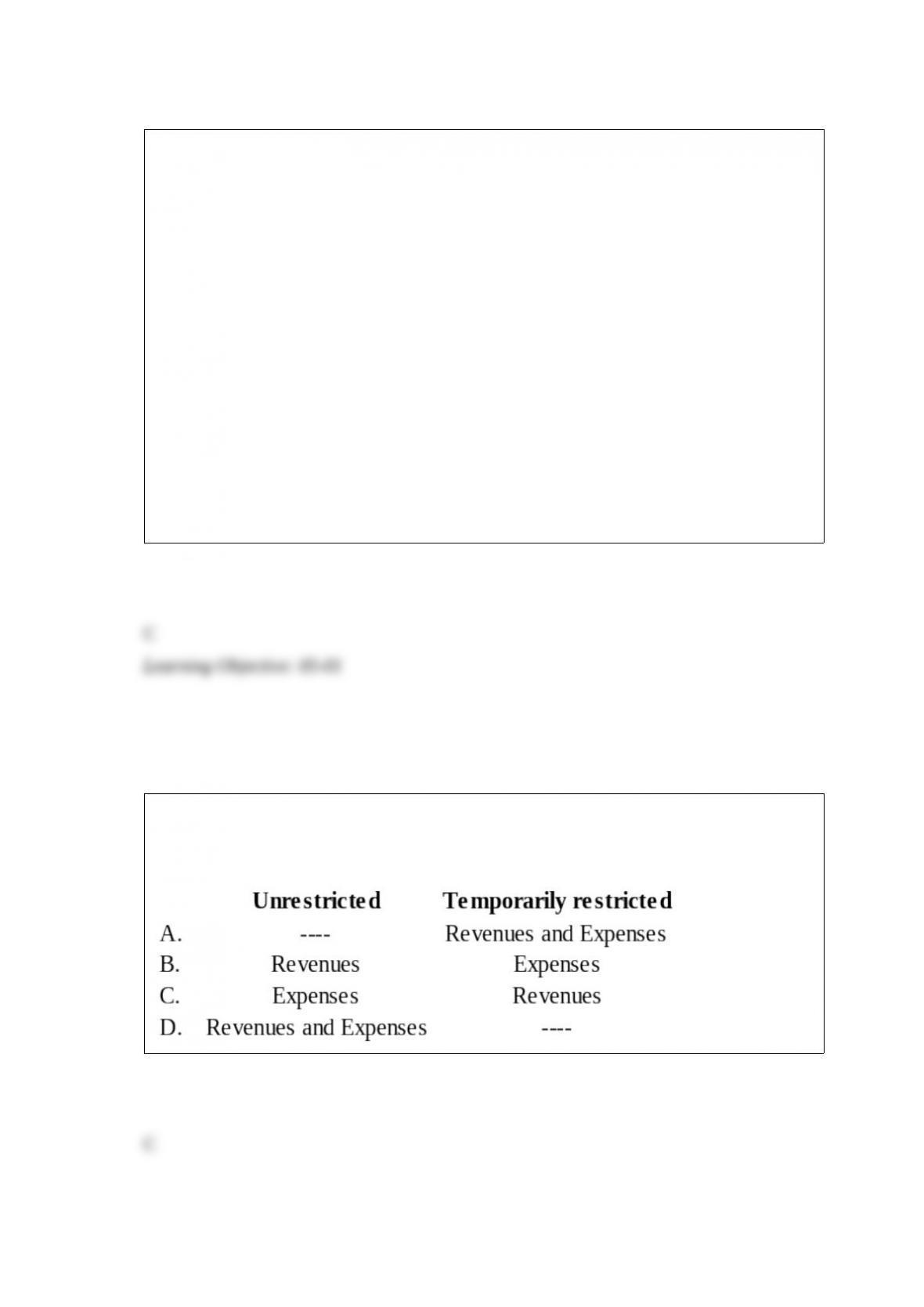

A not-for-profit organization received a donation temporarily restricted as to use. The

donated amount was later spent in accordance with the restriction. In which

category(ies) of net assets should the related revenues and expenses be recognized?

The general fund of Sun City was billed $7,000 for using the services of one of its

internal service funds. The general fund should account for this transaction as a(n)

A. interfund transfer.

B. interfund loan.

C. interfund service.

D. interfund reimbursement for services rendered.

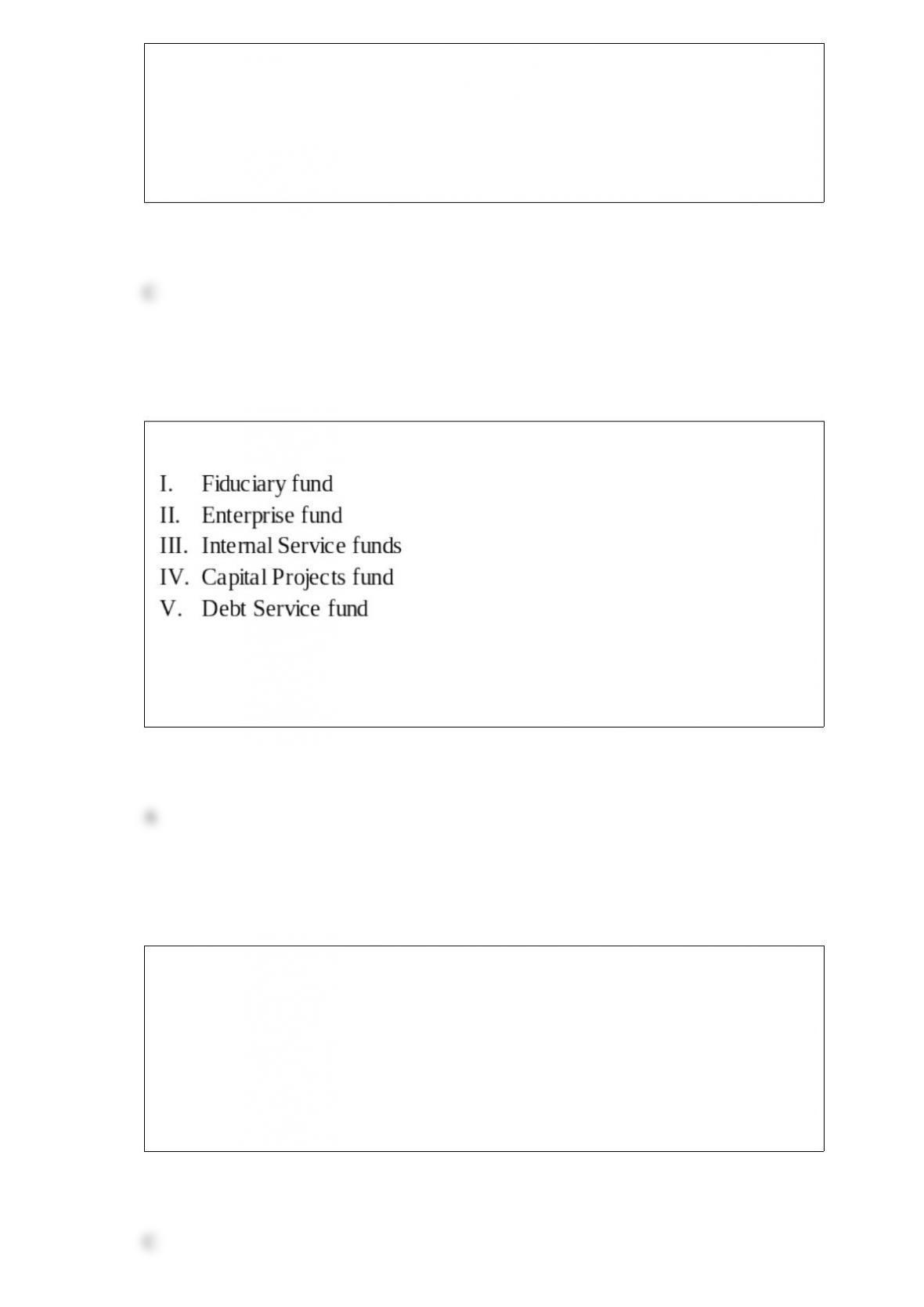

Fixed assets and investments are reported in which of the following funds?

A. I, II, III

B. II, IV, V

C. I, II, V

D. II, III, IV

Which of the following statements concerning pro forma disclosures is not true?

A. They show the effects of major transactions that occur after the end of the fiscal

period.

B. They show the effects of major transactions that have occurred during the year but

are not fully reflected in the company’s historical cost financial statements.

C. The SEC requires these to be presented only when the company has made an unusual

asset exchange, or a restructuring of existing indebtedness.

D. They often take the form of summarized financial statements.

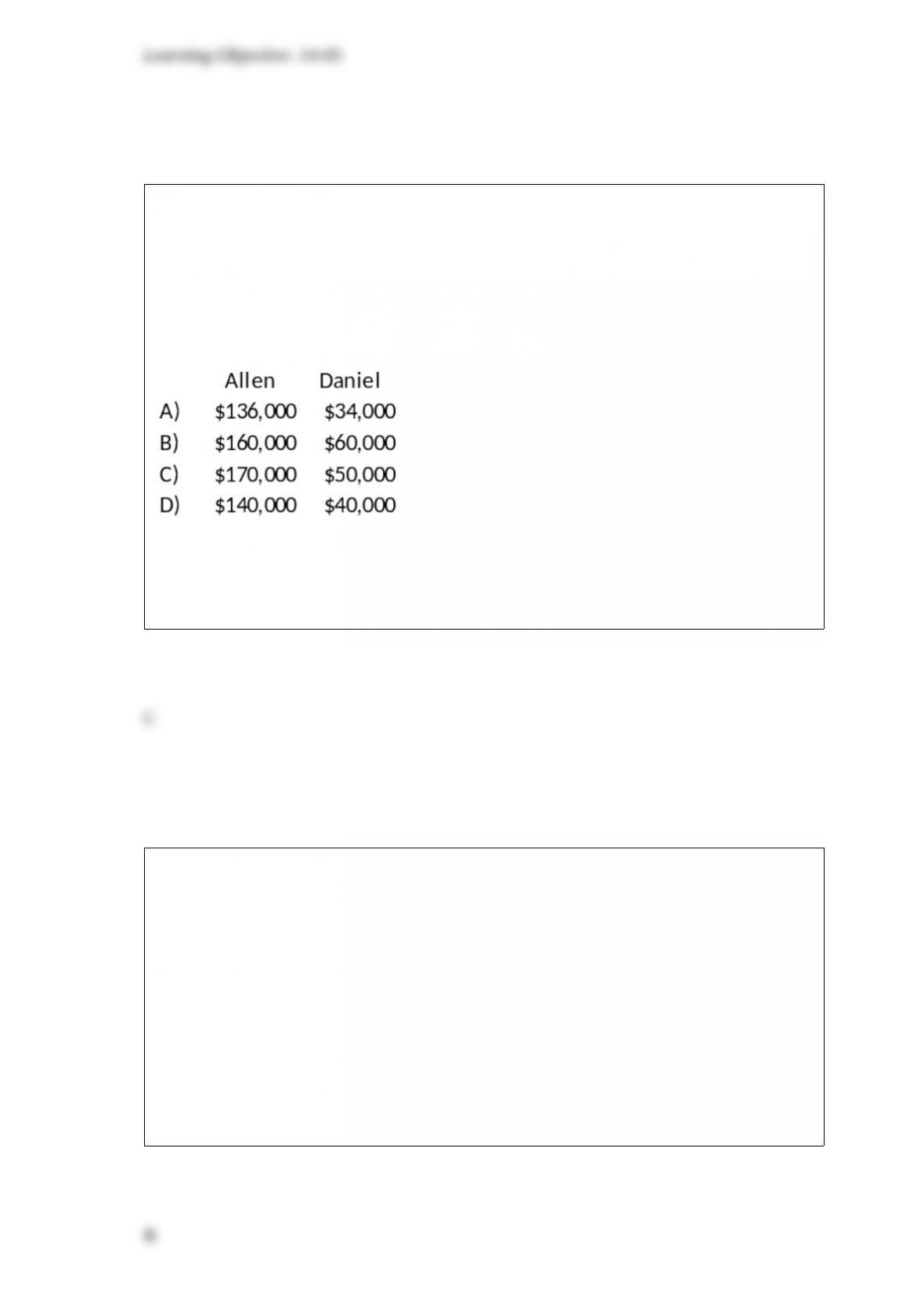

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. David directly purchases a one-fifth interest

by paying Allen $34,000 and Daniel $10,000. The land account is increased before

David is admitted. What are the capital balances of Allen and Daniel after David is

admitted into the partnership?

A. Option A

B. Option B

C. Option C

D. Option D

Davis Company uses LIFO for all of its inventories. During its second quarter of 20X9,

Davis experienced a LIFO liquidation. Davis fully expects to replace the liquidated

inventory in the early part of the third quarter. How should Davis report the inventory

temporarily liquidated on its income statement for the second quarter?

A. Cost of goods sold for the second quarter should include the acquisition cost of the

goods temporarily liquidated.

B. Cost of goods sold for the second quarter should include the expected replacement

cost of the goods temporarily liquidated.

C. Cost of goods sold for the second quarter should not include the expected

replacement cost of the goods temporarily liquidated.

D. Cost of goods sold for the second quarter is not affected by the temporary liquidation

of LIFO inventory.

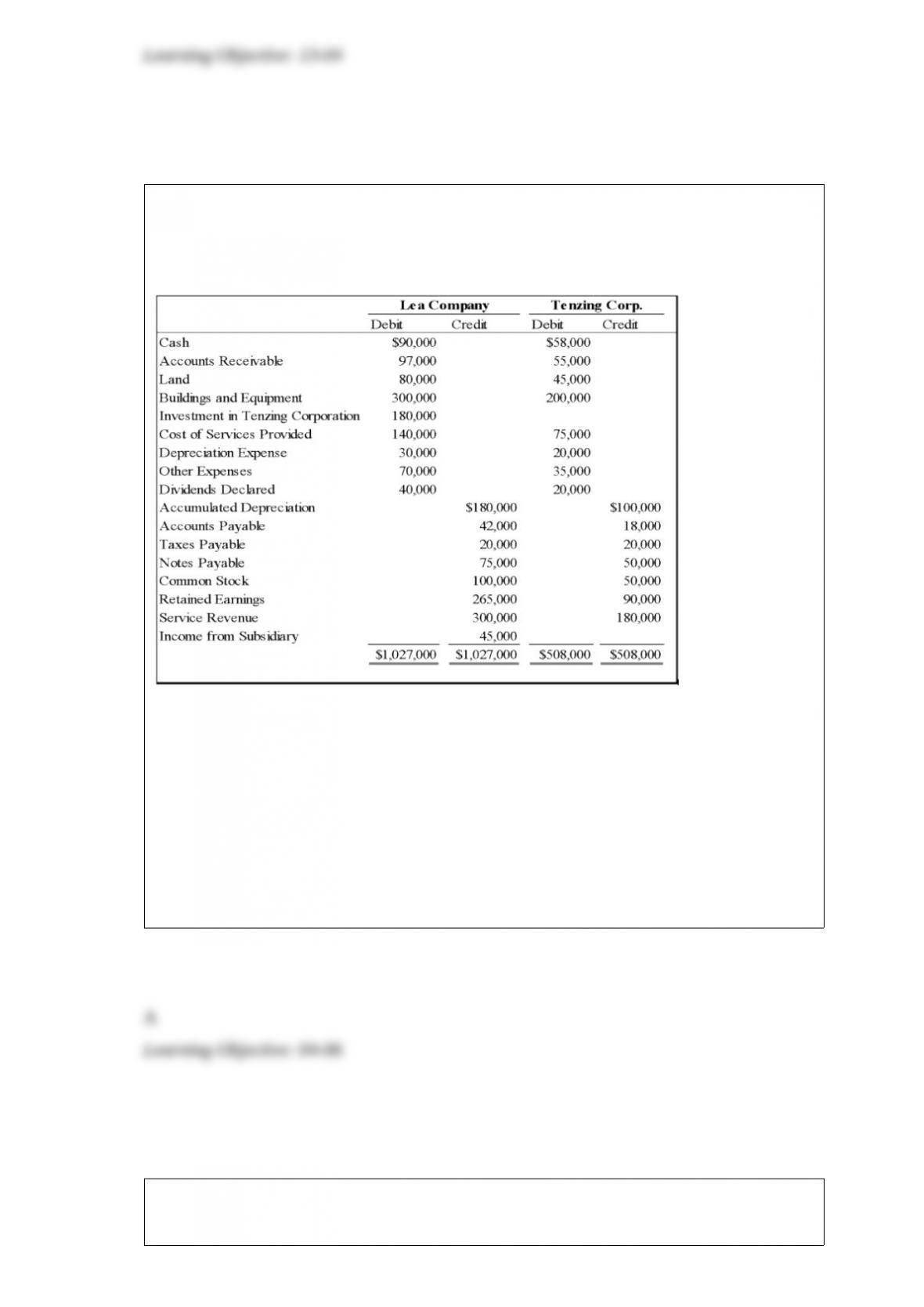

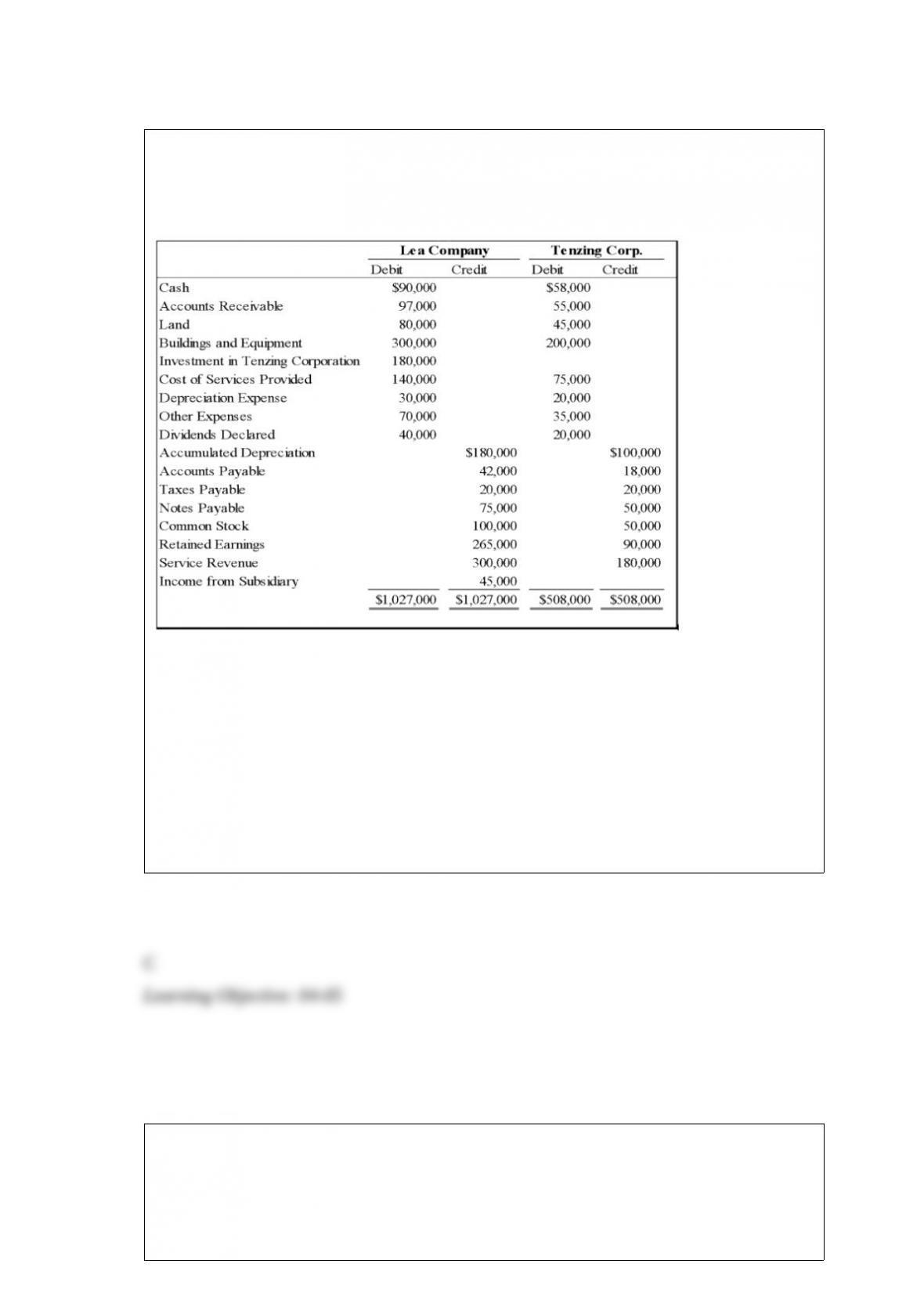

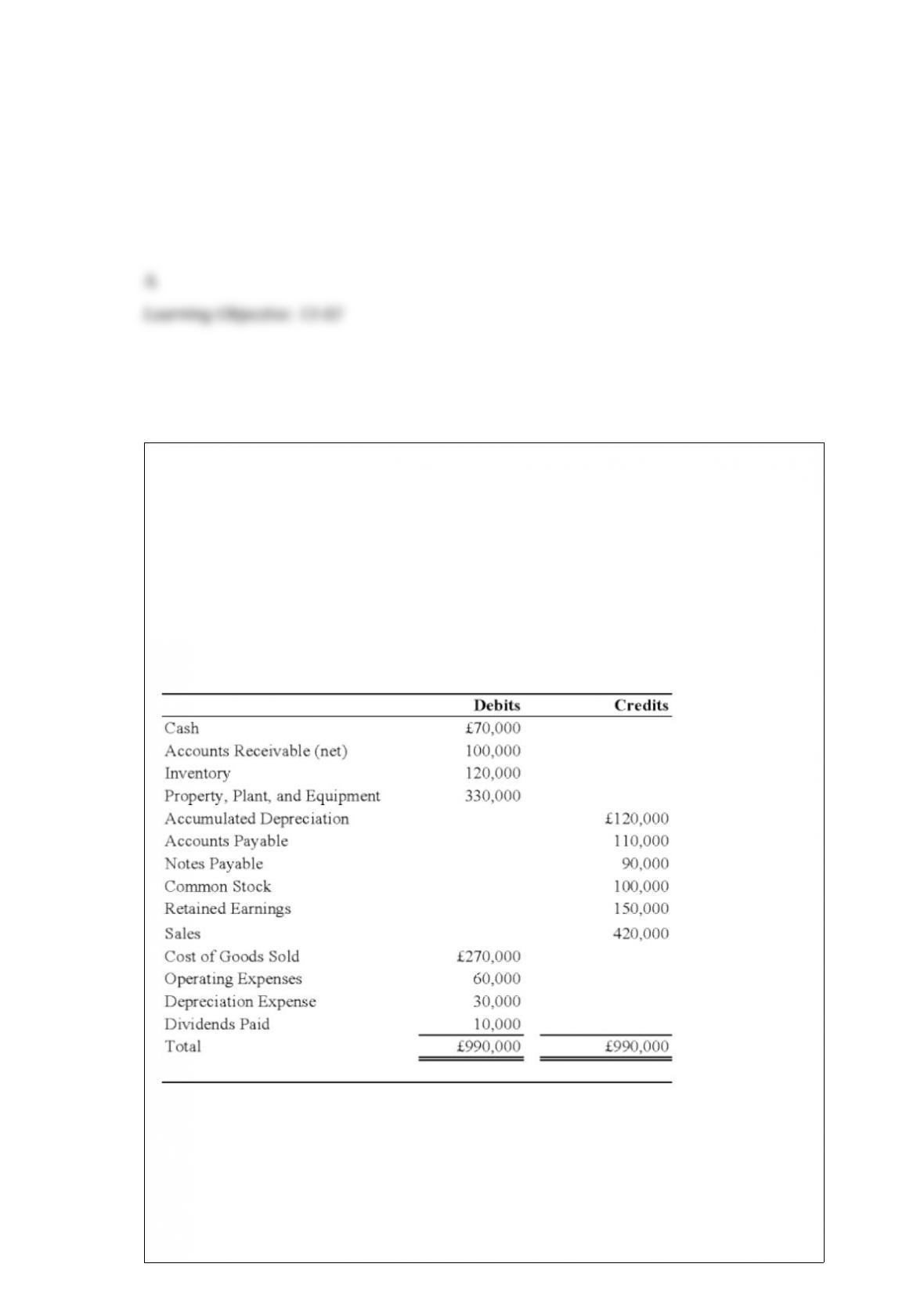

Lea Company acquired all of Tenzing Corporation’s stock on January 1, 20X6 for

$150,000 cash. On December 31, 20X8, the trial balances of the two companies were as

follows:

Tenzing Corporation reported retained earnings of $75,000 at the date of acquisition.

The difference between the acquisition price and underlying book value is assigned to

buildings and equipment with a remaining economic life of five years from the date of

acquisition. At December 31, 20X8, Tenzing owed Lea $4,000 for services provided.

Based on the preceding information, what amount will be reported for total accounts

payable in the consolidated balance sheet for the year 20X8?

A. $56,000

B. $46,000

C. $60,000

D. $42,000

Briefly explain the following terms associated with accounting for foreign entities:

a) Functional Currency

b) Translation

c) Remeasurement

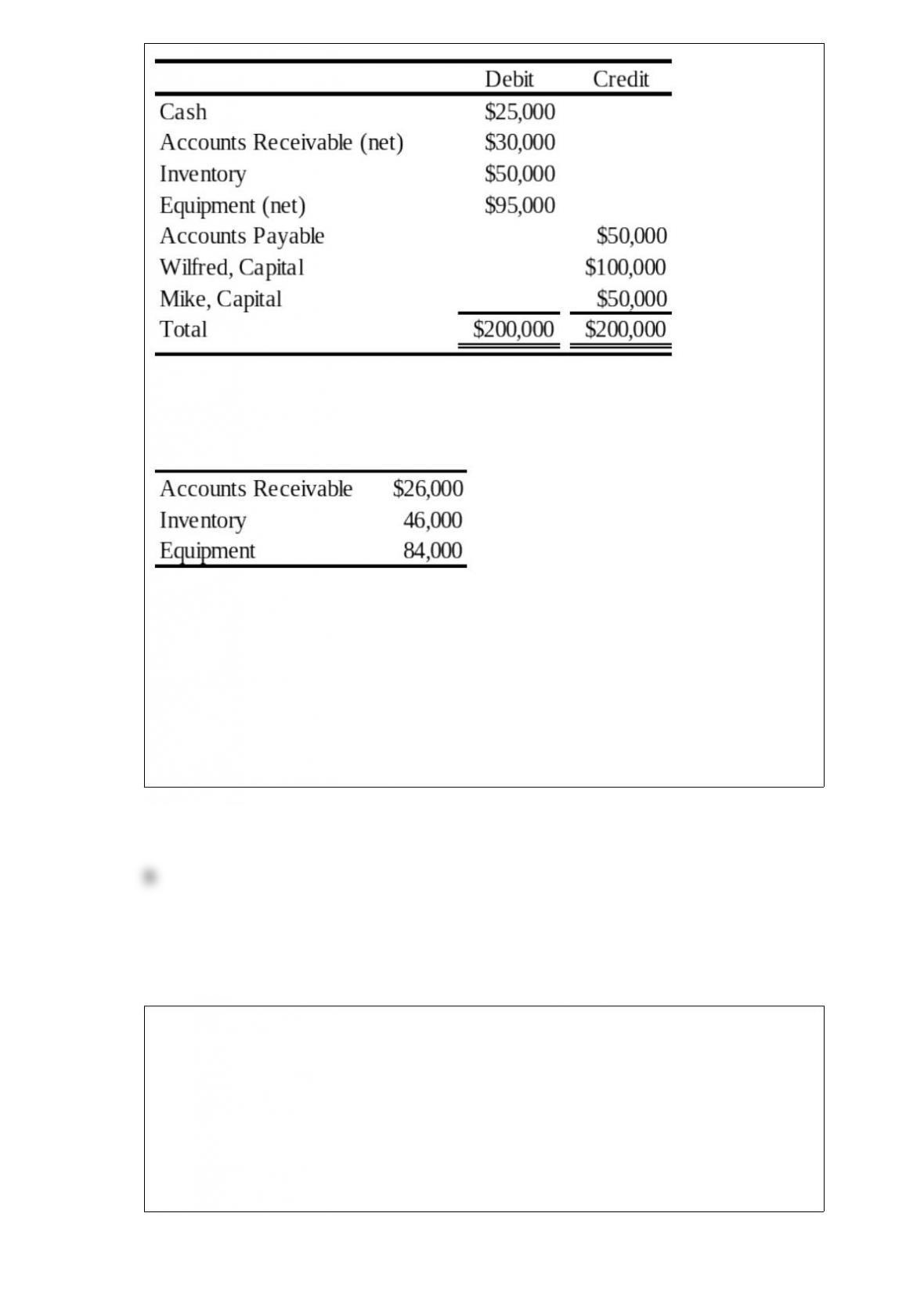

The trial balance of WM Partnership is as follows:

Wilfred and Mike decide to incorporate their partnership. The partnership’s books will

be closed, and new books will be used for W & M Corporation. The following

additional information is available:

1) The estimated fair values of the assets follow:

2)All assets and liabilities are transferred to the corporation.

3) The common stock is $10 par. Wilfred and Mike receive a total of 10,000 shares.

4) The partners share profits and losses in the ratio 7:3.

Based on the preceding information, the journal entry on the partnership’s books to

record the Investment in W&M Corporation Stock will be debited for:

A. $181,000

B. $131,000

C. $200,000

D. $150,000

During the liquidation of the FGH partnership, a cash distribution was made to all the

partners, who share profits and losses 60 percent, 20 percent, and 20 percent,

respectively. Assuming that the cash distribution referred to was made properly, how

much would G receive if an additional $60,000 was distributed?

A. $60,000

B. $20,000

C. $17,000

D. $12,000

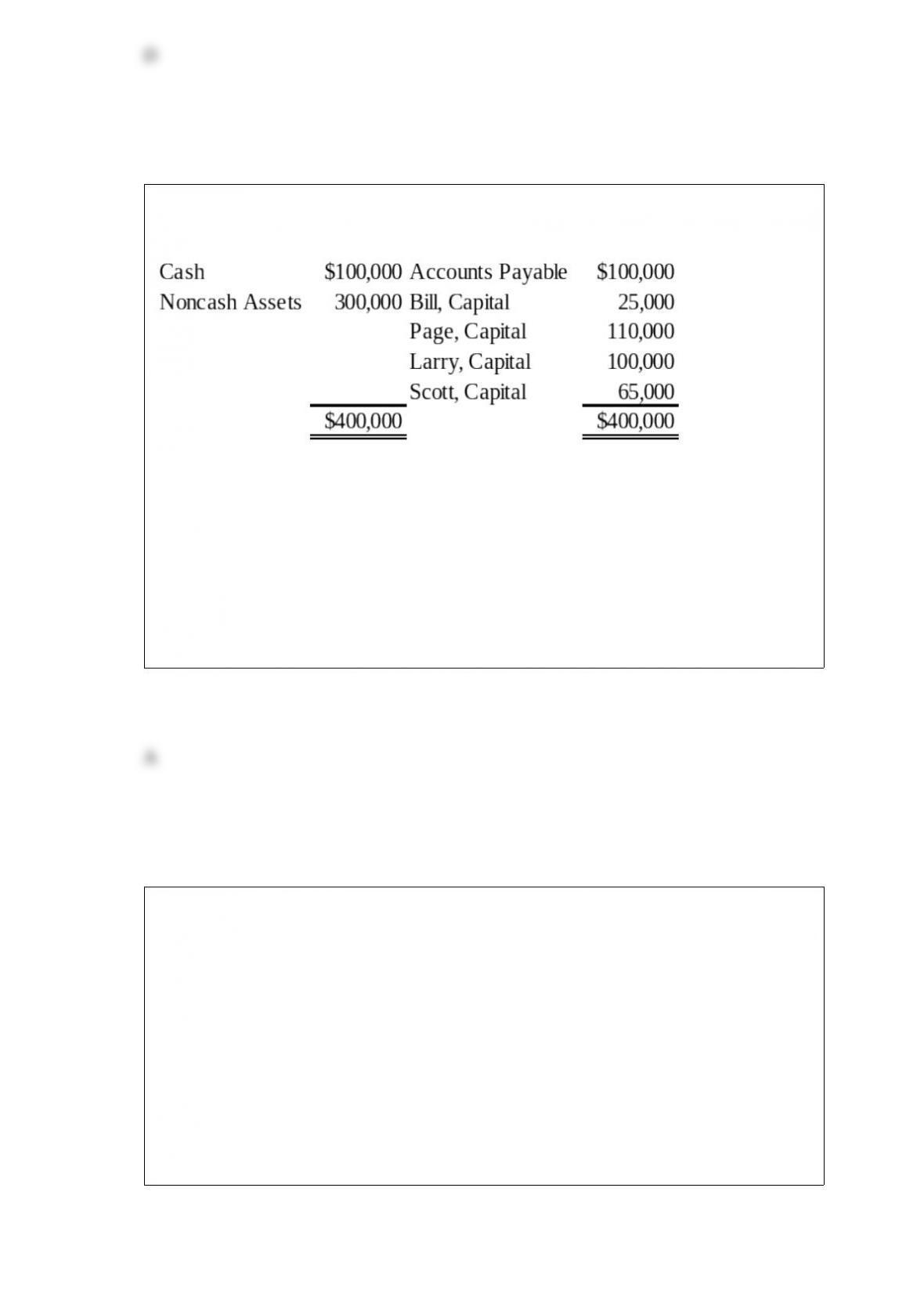

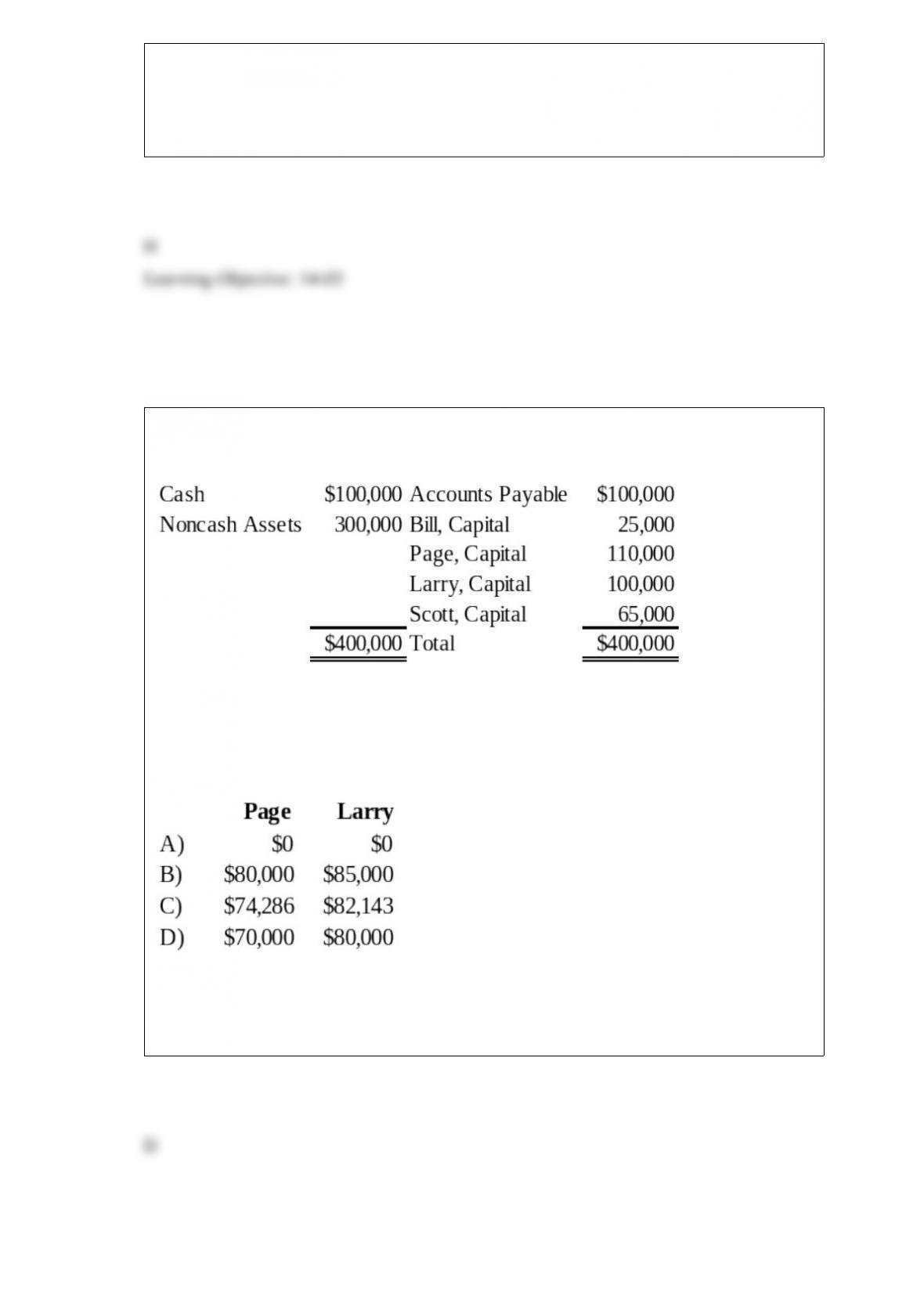

Bill, Page, Larry, and Scott have decided to terminate their partnership. The

partnership’s balance sheet at the time they decide to wind up is as follows:

During the winding up of the partnership, the other assets are sold for $150,000 and the

accounts payable are paid. Page and Larry are personally solvent, but Bill and Scott are

personally insolvent. The partners share profits and losses in the ratio of 4:2:1:3.

Based on the preceding information, what amount will be paid out to Bill upon

liquidation of the partnership?

A. $0

B. $25,000

C. $11,667

D. $2,500

During the fiscal year ended June 30, 20X9, a private, not-for-profit hospital acquired

equipment costing $75,000, with cash contributed by donors who restricted their

contributions for this purpose. On the hospital’s statement of cash flows for the year

ended June 30, 20X9, the equipment acquisition should be reported in which of the

following sections?

I. Operating activities

II. Financing activities

III. Investing activities

A. I

B. II

C. III

D. I, II, III

Paccu Corporation acquired 100 percent of Sallee Company’s common stock on

January 1, 20X7. Balance sheet data for the two companies immediately following the

acquisition follow:

Paccu Sallee

Cash $50,000 $30,000

Accounts Receivable 60,000 35,000

Inventory 130,000 45,000

Land 75,000 60,000

Buildings and Equipment 310,000 170,000

Less: Accumulated Depreciation (130,000) (30,000)

Investment in Sallee Company Stock 250,000

Total Assets $745,000 $310,000

Accounts Payable $40,000 $35,000

Taxes Payable 30,000 12,000

Bonds Payable 250,000 50,000

Common Stock 75,000 75,000

Retained Earnings 350,000 138,000

Total Liabilities and Stockholders’ Equity $745,000 $310,000

At the date of the business combination, the book values of Sallee’s assets and liabilities

approximated fair value except for inventory, which had a fair value of $55,000, and

land, which had a fair value of $65,000. The fair value of land for Paccu Corporation

was estimated at $90,000 immediately prior to the acquisition.

Based on the preceding information, what amount of goodwill will be reported in the

consolidated balance sheet prepared immediately after the business combinations?

A. $37,000

B. $22,000

C. $15,000

D. $0,000

Plummet Corporation reported the book value of its net assets at $400,000 when Zenith

Corporation acquired 100 percent ownership. The fair value of Plummet’s net assets

was determined to be $510,000 on that date.

Based on the preceding information, what amount of goodwill will be reported in

consolidated financial statements presented immediately following the combination if

Zenith paid $550,000 for the acquisition?

A. $0

B. $50,000

C. $150,000

D. $40,000

According to the provisions of the Sarbanes-Oxley Act,

A. accounting firms can provide both audit and non-audit services to the same

company.

B. the auditor should report directly to, and have its work overseen by, the company’s

management.

C. audit committees should be composed of non-management members of a company’s

board of directors.

D. both the lead audit partner and the audit review partner for publicly held companies

should be rotated at least every two years.

On the statement of activities for a private, not-for-profit literary society, expenses

decrease which of the following classes of net assets?

I. temporarily restricted net assets

II. unrestricted net assets

A. I only

B. II only

C. Either I or II

D. Neither I nor II

Lea Company acquired all of Tenzing Corporation’s stock on January 1, 20X6 for

$150,000 cash. On December 31, 20X8, the trial balances of the two companies were as

follows:

Tenzing Corporation reported retained earnings of $75,000 at the date of acquisition.

The difference between the acquisition price and underlying book value is assigned to

buildings and equipment with a remaining economic life of five years from the date of

acquisition. At December 31, 20X8, Tenzing owed Lea $4,000 for services provided.

Based on the preceding information, what amount will be reported as total assets in the

consolidated balance sheet for 20X8?

A. $666,000

B. $747,000

C. $651,000

D. $946,000

In the AD partnership, Allen’s capital is $140,000 and Daniel’s is $40,000 and they

share income in a 3:1 ratio, respectively. They decide to admit David to the partnership.

Each of the following questions is independent of the others.

Refer to the information provided above. David invests $40,000 for a one-fifth interest

in the total capital of $220,000. The journal to record David’s admission into the

partnership will include:

A. a credit to Cash for $40,000.

B. a debit to Allen, Capital for $3,000.

C. a credit to David, Capital for $40,000.

D. a credit to Daniel, Capital for $1,000.

Company X denominated a December 1, 20X9, purchase of goods in a currency other

than its functional currency. The transaction resulted in a payable fixed in terms of the

amount of foreign currency, and was paid on the settlement date, January 10, 2010.

Exchange rates moved unfavorably at December 31, 20X9, resulting in a loss that

should:

A. be included as a separate component of stockholders’ equity at Dec. 31, 20X9.

B. be included as a component of income from continuing operations for 20X9.

C. be included as a deferred charge at December 31, 20X9.

D. not be reported until January 10, 2010, the settlement date.

Each of the following questions names an item. Select the correct description of the

item from this list. Indicate your selection by entering the letter of the description.

Descriptions

a. Provides preliminary information to investors about an upcoming issue.

b. Informs investors of an upcoming offering.

c. Required annual filing to the SEC.

d. Discloses unscheduled material events.

e. Includes amendments to the Securities Act, additional disclosure requirements, and

other current issues regarding accounting and auditing principles and standards.

f. Results in a thorough examination by the SEC of a registration statement.

g. Issued by the staff of the SEC and contains differences that must be corrected in a

registration statement before the securities may be offered or sale.

h. Quarterly report to SEC.

i. Includes new or revised administrative practices and interpretations used in reviewing

financial statements.

j. Includes the results of actions taken against accountants or other participants because

false or misleading statements were filed.

k. Includes Regulations S-X and S-K.

Form 10-Q

Bill, Page, Larry, and Scott have decided to terminate their partnership. The

partnership’s balance sheet at the time they decide to wind up is as follows:

During the winding up of the partnership, the other assets are sold for $150,000 and the

accounts payable are paid. Page and Larry are personally solvent, but Bill and Scott are

personally insolvent. The partners share profits and losses in the ratio of 3:2:1:4.

Based on the preceding information, what amounts will be distributed to Page and

Larry upon liquidation of the partnership?

A. Option A

B. Option B

C. Option C

D. Option D

On January 1, 20X6, Joseph Company acquired 80% of Salt Company’s outstanding

stock for cash. The fair value of the noncontrolling interest was equal to a proportionate

share of the book value of Salt Company’s net assets at the date of acquisition. Selected

balance sheet data at December 31, 20X6 are as follows:

Joseph Salt

Total Assets $564,000 $241,000

Liabilities $180,000 $65,000

Common Stock 150,000 80,000

Retained Earnings 234,000 96,000

$564,000 $241,000

Based on the preceding information, what amount will Joseph Company report as

common stock outstanding in its consolidated balance sheet at December 31, 20X6?

A. $214,000

B. $150,000

C. $184,000

D. $230,000

Alpha Company acquired 100 percent of the voting common shares of Gamma

Corporation by issuing bonds with a par value and fair value of $200,000. Immediately

prior to the acquisition, Alpha reported total assets of $600,000, liabilities of $370,000,

and stockholders’ equity of $230,000. At that date, Gamma reported total assets of

$500,000, liabilities of $300,000, and stockholders’ equity of $200,000. Included in

Gamma’s liabilities was an account payable to Alpha in the amount of $50,000, which

Alpha included in its accounts receivable.

Based on the preceding information, what amount of total assets was reported in the

consolidated balance sheet immediately after acquisition?

A. $600,000

B. $800,000

C. $1,050,000

D. $1,150,0000

Follett Company incurred a first quarter operating loss before income tax effect of

$2,000,000. This is a normal occurrence for Follett because of seasonal fluctuations.

Experience has demonstrated the income earned during the remaining quarters far

exceeds the first quarter losses each year. Follett estimates its annual income tax rate

will be 35 percent. What net loss should Follett report for the first quarter?

A. $0

B. $700,000

C. $1,300,000

D. $2,000,000

Why are consolidation entries used?

Clocktower Corporation reported net income for the current year of $370,000 and paid

cash dividends of $50,000. Slide Company holds 40 percent of the outstanding voting

stock of Clocktower. However, another corporation holds the other 60 percent

ownership and does not take Slide’s wants and wishes into consideration when making

financing and operating decisions for Clocktower. What investment income should

Slide recognize for the current year?

A. $0

B. $20,000

C. $128,000

D. $148,000

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Classification of contributions restricted by purpose” describes which term listed

above?

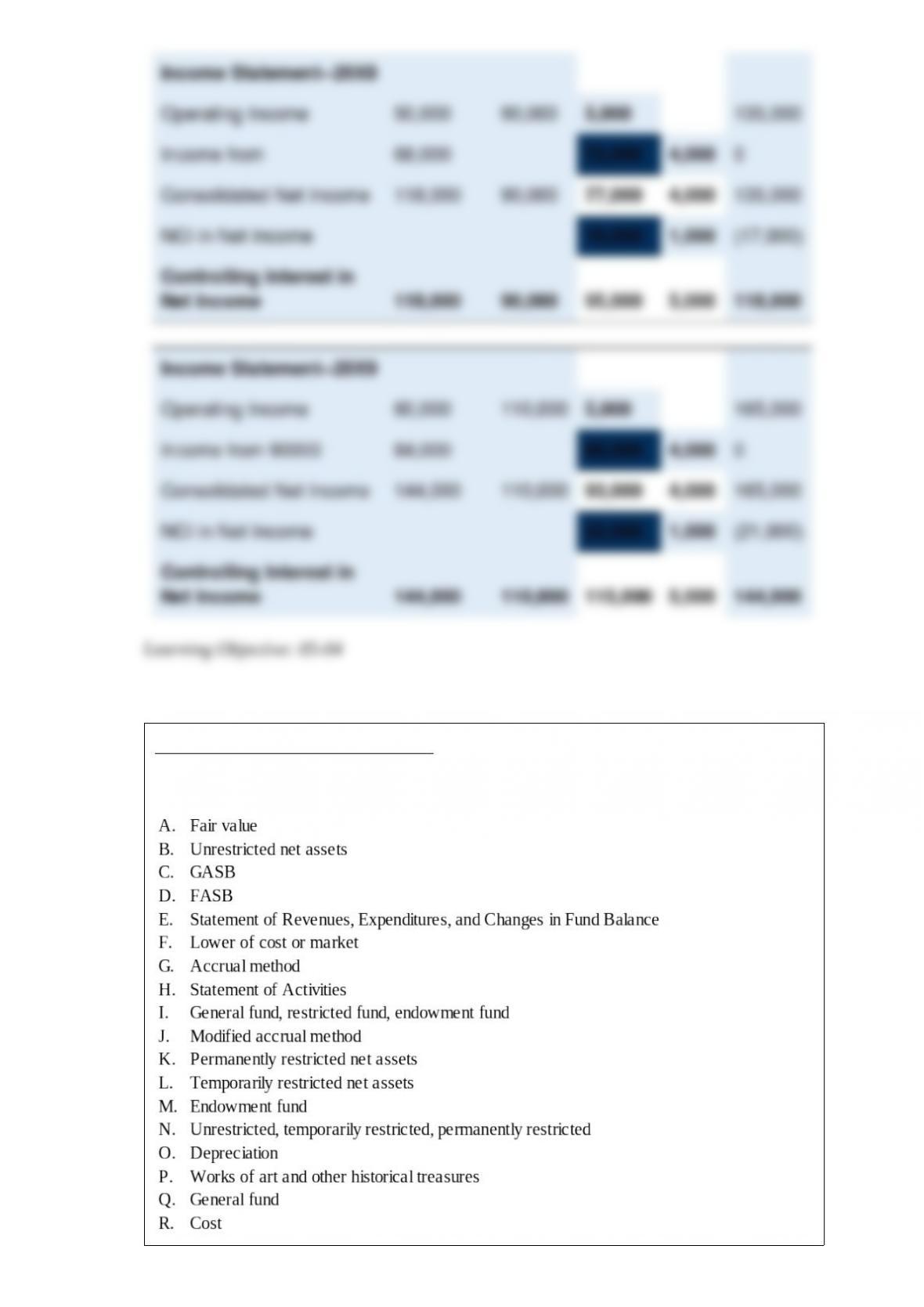

Top Corporation acquired 80 percent of Bottom Corporation’s common stock on

January 1, 20X8, for $520,000. At that date, Bottom reported common stock

outstanding of $250,000 and retained earnings of $375,000. Assume the fair value of

the noncontrolling interest on January 1, 20X8 was $130,000. The book values and fair

values of Bottom’s assets and liabilities were equal on the acquisition date, except for

other intangible assets, which had a fair value $25,000 greater than book value and a

5-year remaining life. Top and Bottom reported the following data for 20X8 and 20X9:

a. Compute consolidated comprehensive income for 20X8 and 20X9.

b. Compute comprehensive income attributable to the controlling interest for 20X8

and 20X9.

Private Not-For-Profit (NFP) Entities.

Select from this list of terms to answer the following questions.

Indicate your choice by entering the letter corresponding to the correct term. A term

may be used more than once or not at all.

”Net asset classifications per FAC 6” describes which term listed above?

Magellan Corporation acquired 80 percent ownership of Dipper Corporation on January

1, 20X8, for $200,000. At that date, Dipper reported common stock outstanding of

$75,000 and retained earnings of $150,000. The fair value of the noncontrolling interest

was $50,000. The differential is assigned to equipment, which had a fair value $25,000

greater than book value and a remaining economic life of five years at the date of the

business combination. Dipper reported net income of $40,000 and paid dividends of

$20,000 in 20X8.

Required:

1) Provide the journal entries recorded by Magellan during 20X8 on its books if it

accounts for its investment in Dipper using the equity method.

2) Give the consolidating entries needed at December 31, 20X8, to prepare consolidated

financial statements.

The ABC partnership had net income of $100,000 for 20X9. They allocate profits and

losses in the ratio 5:3:2. After closing the 12/31/20X9 books they discovered that

$30,000 was spent on a piece of land in December 20X9 and was expensed. What

should happen?

Dragon Company has two reportable segments, A and B. Segment A made $3,000,000

of sales to external customers and $200,000 of sales to other operating segments.

Segment B made sales of $5,000,000 to external customers and $1,200,000 of sales to

other operating segments. Dragon Company reported $9,600,000 of revenues on its

consolidated income statement. What calculation below correctly determines whether

Dragon Company’s reportable segments satisfy the 75% revenue test?

A. $8,000,000/$9,600,000

B. $8,000,000/$11,000,000

C. $9,400,000/$9,600,000

D. $9,400,000/$11,000,000

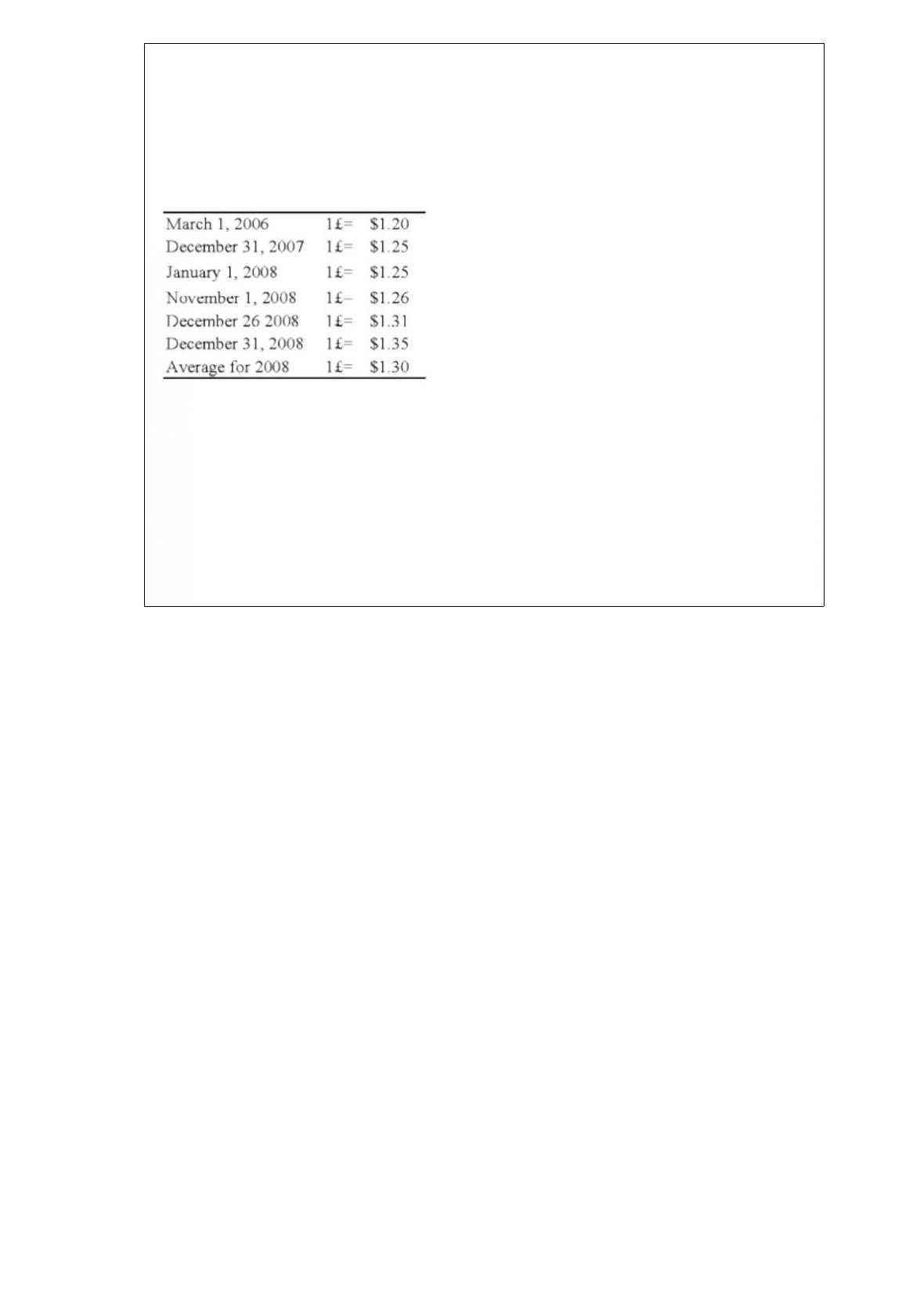

On January 1, 2008, Pace Company acquired all of the outstanding stock of Spin PLC,

a British Company, for $350,000. Spin’s net assets on the date of acquisition were

250,000 pounds (). On January 1, 2008, the book and fair values of the Spin’s

identifiable assets and liabilities approximated their fair values except for property,

plant, and equipment and trademarks. The fair value of Spin’s property, plant, and

equipment exceeded its book value by $25,000. The remaining useful life of Spin’s

equipment at January 1, 2008, was 10 years. The remainder of the differential was

attributable to a trademark having an estimated useful life of 5 years. Spin’s trial

balance on December 31, 2008, in pounds, follows:

Additional Information

1) Spin uses the FIFO method for its inventory. The beginning inventory was acquired

on December 31, 2007, and ending inventory was acquired on December 26, 2008.

Purchases of 300,000 were made evenly throughout 2008.

2) Spin acquired all of its property, plant, and equipment on March 1, 2006, and uses

straight-line depreciation.

3) Spin’s sales were made evenly throughout 2008, and its operating expenses were

incurred evenly throughout 2008.

4) The dividends were declared and paid on November 1, 2008.

5) Pace’s income from its own operations was $150,000 for 2008, and its total

stockholders’ equity on January 1, 2008, was $1,000,000. Pace declared $50,000 of

dividends during 2008.

6) Exchange rates were as follows:

Required:

1) Prepare a schedule translating the trial balance from British pounds into U.S. dollars.

Assume the pound is the functional currency.

2) Assume that Pace uses the fully adjusted equity method. Record all journal entries

that relate to its investment in the British subsidiary during 2008. Provide the necessary

documentation and support for the amounts in the journal entries, including a schedule

of the translation adjustment related to the differential.

3) Prepare a schedule that determines Pace’s consolidated comprehensive income for

2008.

Prior to closing the accounts at the end of the most recent fiscal year, the Town of

Sonora reports the following amounts (in thousands):

Required:

Applying the criteria specified in GASB 34, determine which of the above funds should

be classified as major funds for reporting purposes.

The transactions described in the following questions occurred in a voluntary health and

welfare organization during the year ended December 31, 20X8. For each transaction,

indicate its effect(s) on the organization’s statement of activities prepared for the year

ended December 31, 20X8. List all effects of transactions affecting more than one class

of net assets. Indicate your choice(s) by entering the letter corresponding to the effects

listed here:

Income was earned from investments of assets that the board previously designated for

plant expansion.